It’s like someone turned on the spigot in July and forgot to turn it off.

By Wolf Richter for WOLF STREET.

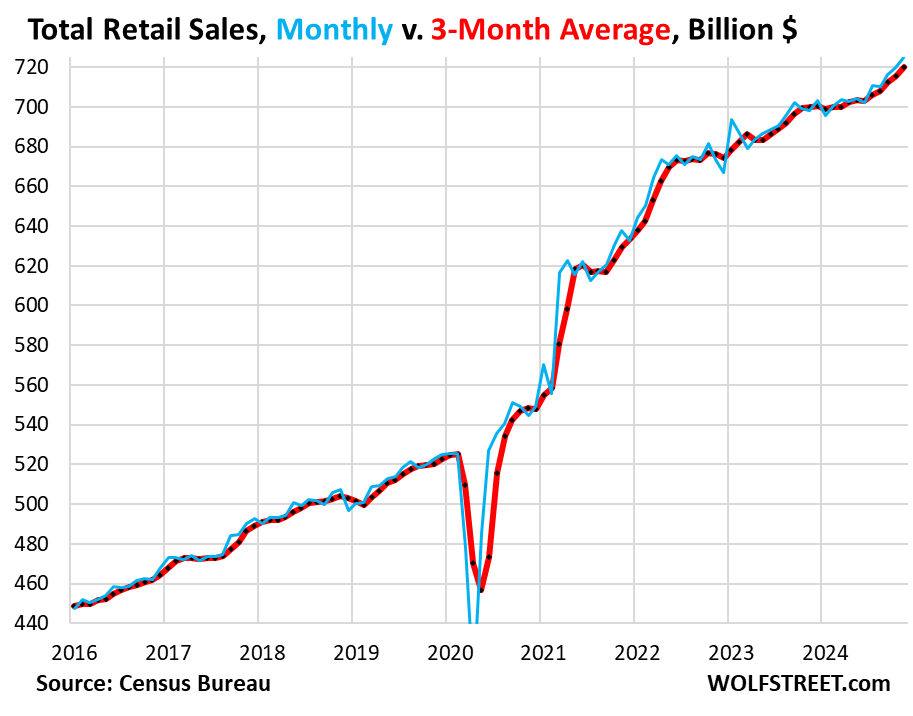

Retail sales jumped by 0.7% in November from October, to $720 billion, seasonally adjusted, and October was revised higher (blue in the chart below), and so we look at the 3-month average (red in the chart), which irons out the month-to-month squiggles and includes the revisions, and it jumped by 0.7% as well.

November’s sales increase and the three-month average sales increase annualized amount to +8.6%! And it wasn’t just November, or the past three months. The spending spree started in July.

Retail sales have sharply accelerated month-to-month, starting in July. It’s like someone turned on the spigot in July and forgot to turn if off:

- 6-month January-June total: -0.1%, for an annual pace of -0.2%.

- 5-month July-November total +3.2%, for an annual pace of +7.6%.

Our Drunken Sailors, as we lovingly and facetiously have come to call them, are in the mood to spend, empowered by wage increases that have been outrunning inflation for the past two years, and flush with cash in money market funds and CDs that is still earning over 4% in interest, and buoyed by massive gains in their stock holdings, cryptos, home prices, and whatever, while their credit burden is historically low and their credit largely in excellent condition, even on their credit cards except for a small subsegment of subprime-rated accounts.

Second wind for inflation? This is where consumer demand is coming from, people are out there buying, and they’re buying feverishly online, once again spending money left and right, especially on big ticket items, such as motor vehicles. And after two years of big price declines, prices of new and used vehicles are already rising again. And that’s bad news on the inflation front. The Fed needs to watch out here in order to not throw more fuel on this demand.

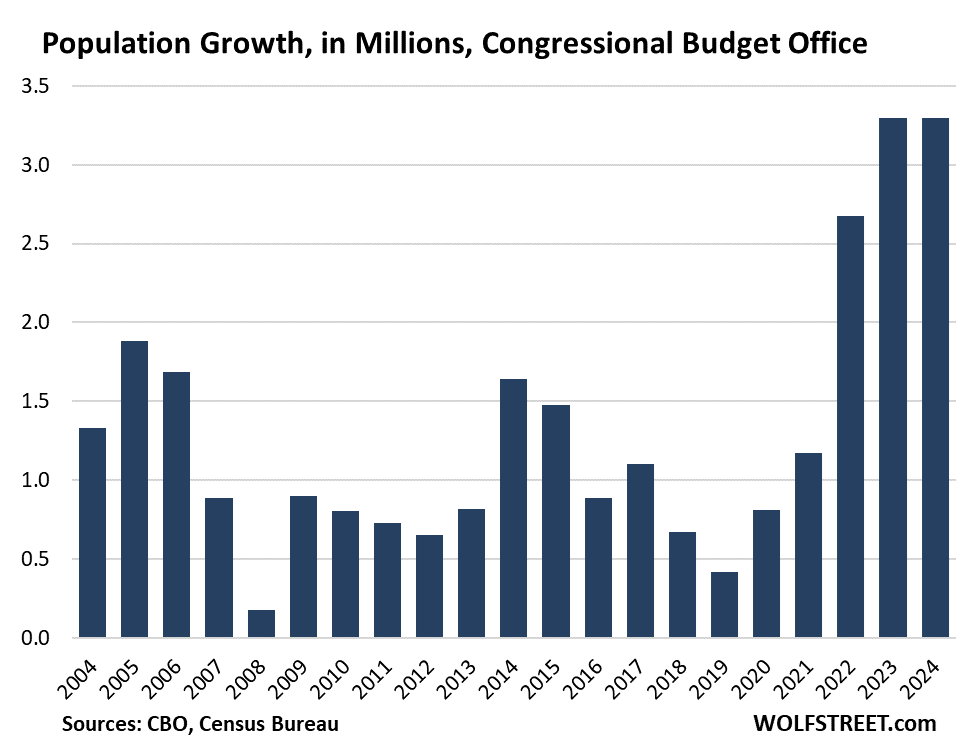

The wave of immigration contributes to demand growth. The US population has surged in 2022 and 2023 by 6 million people due to immigration, and in 2024 has continued to rise, according to the Congressional Budget Office, using ICE and Census data.

Most of the immigrants work as soon as they find work, and they spend money, though they’re generally not big spenders. And this spending by this large new population is contributing to this sharp increase in demand.

Retail sales by category.

The biggest drivers of this growth were the two biggest retailer categories: new and used vehicle sales and ecommerce, combined accounting for 36% of total retail sales.

We have already seen that new vehicle retail sales in November, in terms of the number of vehicles delivered to retail customers, jumped by 10% year-over-year.

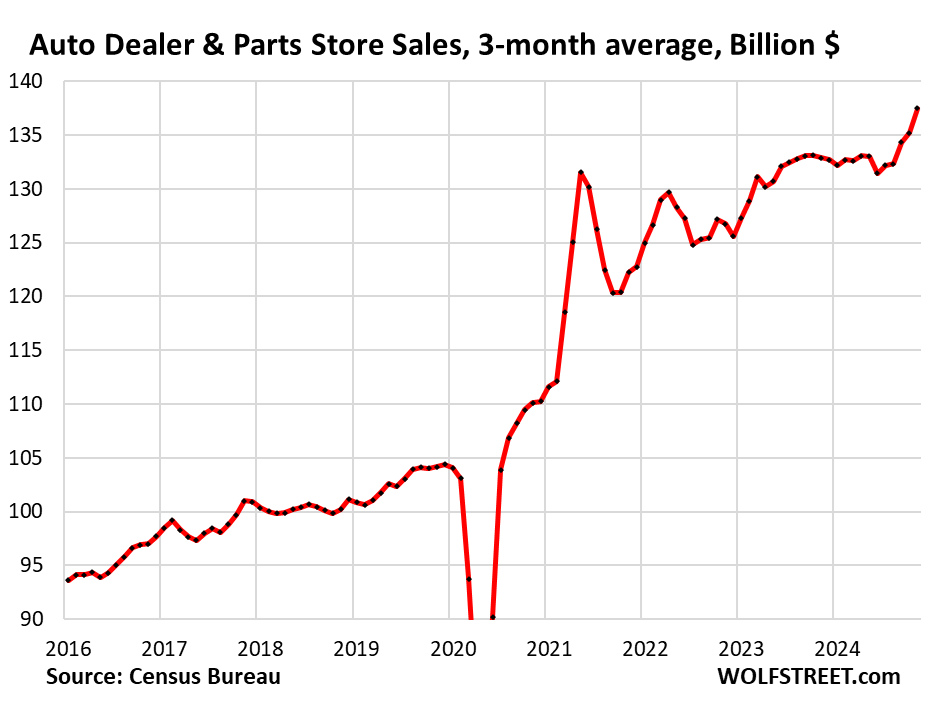

New and used vehicle dealers and parts stores (#1 category, 19% of total retail):

- Sales: $141 billion

- From prior month: +2.6%

- From prior month, 3-month average: +1.7%

- Year-over-year: +6.5%

The spike in dollar-sales in 2021 and 2022 was caused by ridiculous price increases. Starting in mid-2022, prices dropped overall, with used vehicle prices plunging. These price declines caused the dollar-sales for those 18 months to flatten out, despite rising retail unit-sales.

But that’s now over – prices are rising again while unit-sales volume is surging:

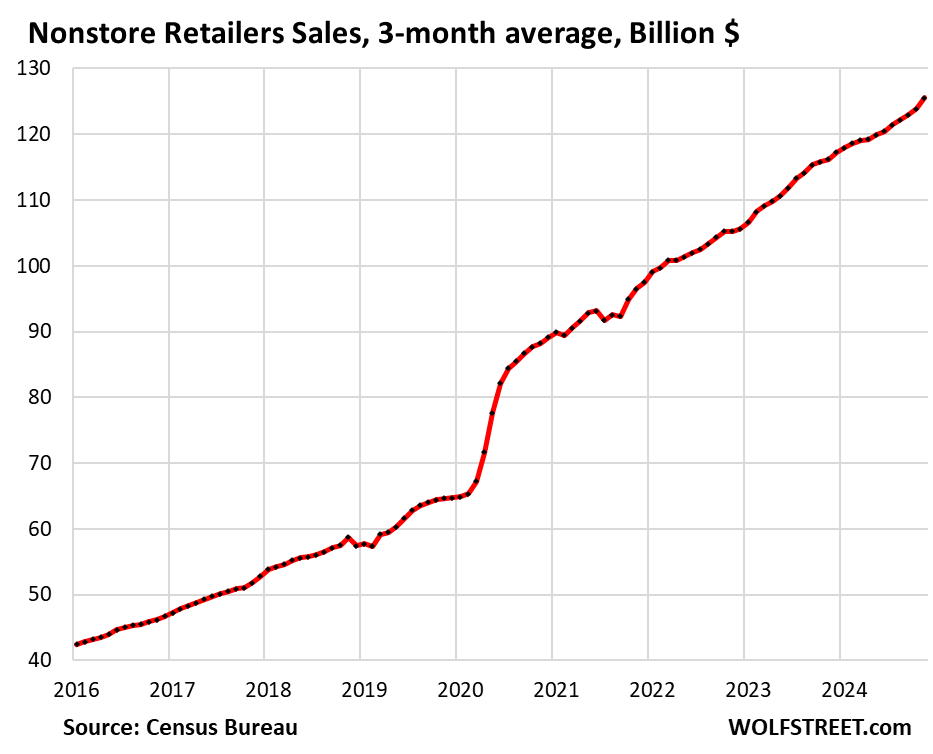

Ecommerce and other “nonstore retailers” (#2 category, 17% of retail), includes ecommerce retailers, ecommerce operations of brick-and-mortar retailers, and stalls and markets:

- Sales: $127 billion

- From prior month: +1.8%

- From prior month, 3-month average: +1.4%

- Year-over-year: +9.8%

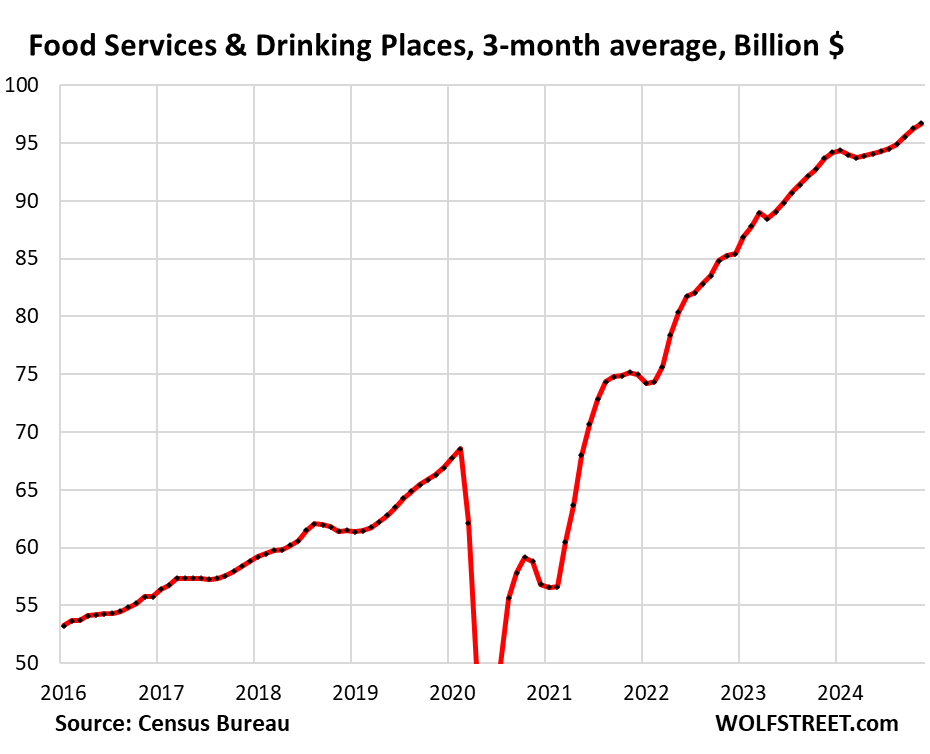

Food services and drinking places (#3 category, 13% of total retail), includes everything from cafeterias to restaurants and bars.

After a decline in early 2024, growth resumed:

- Sales: $97 billion

- From prior month: -0.4%

- From prior month, 3-month average: +0.4%

- Year-over-year: +1.9%

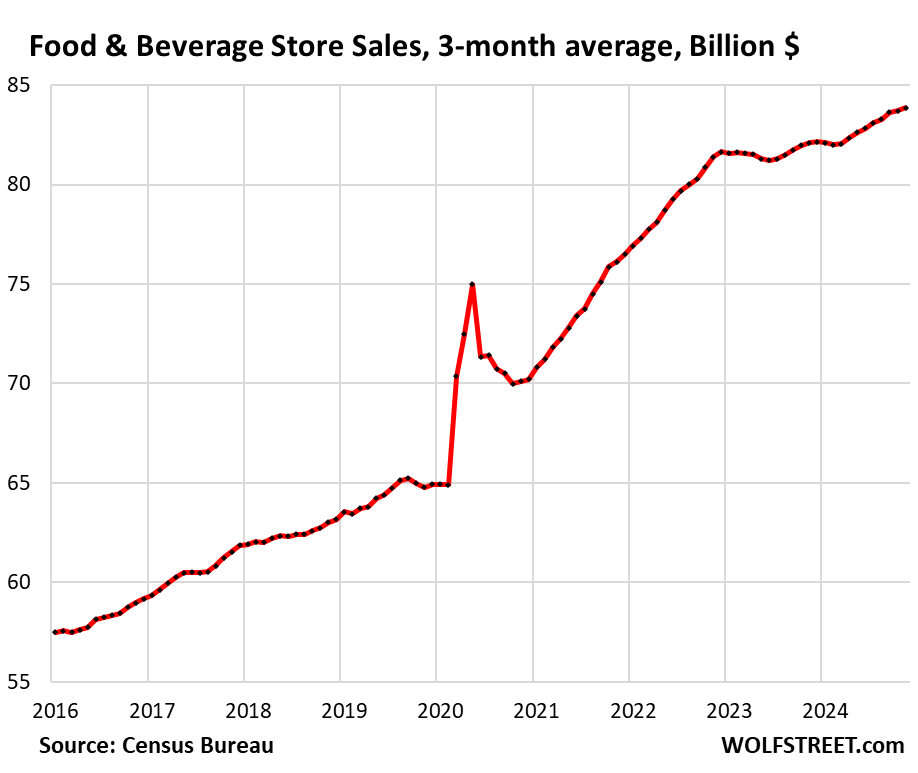

Food and Beverage Stores (12% of total retail). Prices per CPI for food at home exploded from 2020 to early 2023, which caused the spike in sales, then flattened out at high levels for a while, before starting to rise again:

- Sales: $84 billion

- From prior month: -0.2%

- From prior month, 3-month average: +0.2%

- Year-over-year: +1.8%

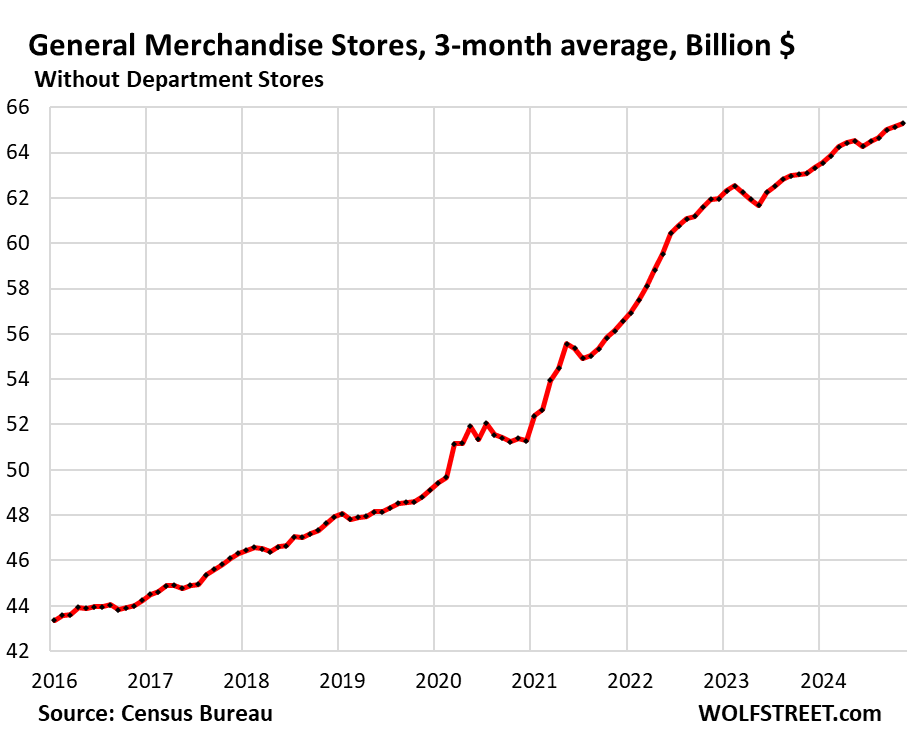

General merchandise stores, without department stores (9% of total retail), including retailers such as Walmart, which is also the largest grocer in the US.

- Sales: $65 billion

- From prior month: no change

- From prior month, 3-month average: +0.2%

- Year-over-year: +3.4%

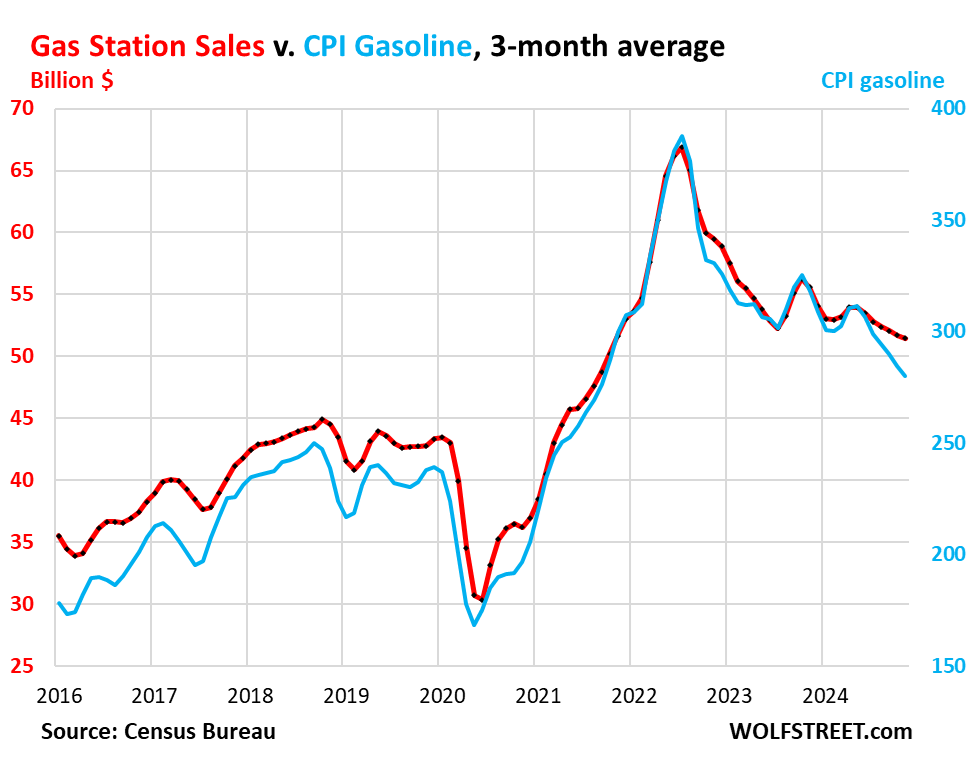

Gas stations (7% of total retail sales). Dollar-sales at gas stations move in near-lockstep with the price of gasoline. The price of gasoline plunged starting in mid-2022 and has continued to trend lower. These price declines push down dollar-sales at gas stations. Sales at gas stations also include all the other merchandise gas stations sell.

- Sales: $52 billion

- From prior month: +0.1%

- From prior month, 3-month average: -0.4%

- Year-over-year: -3.9%

Sales in billions of dollars at gas stations (red, left axis); and the CPI for gasoline (blue, right axis):

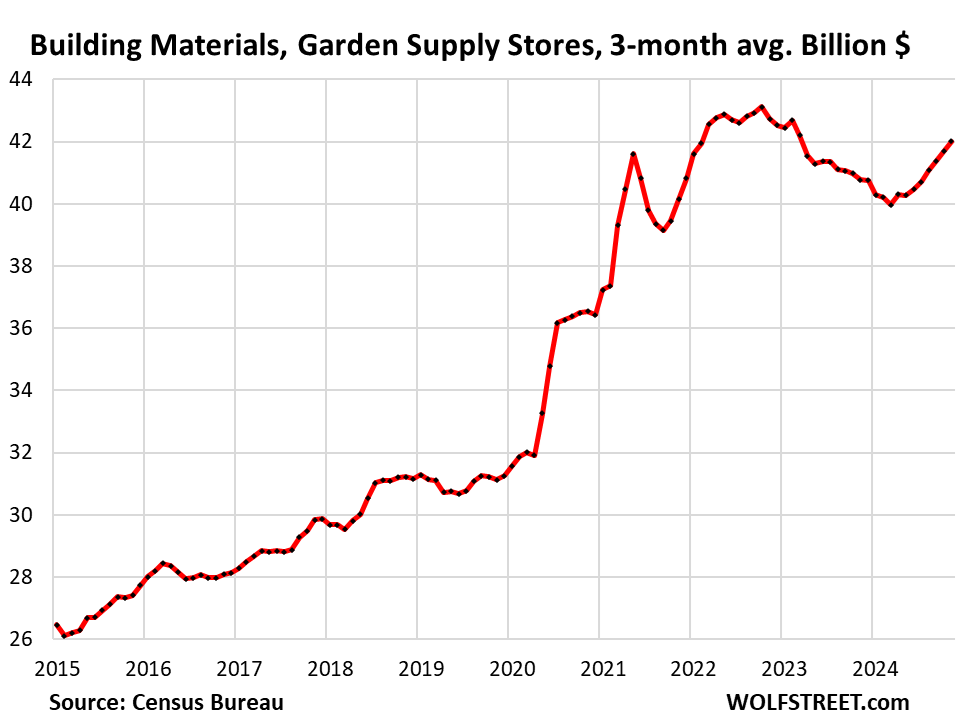

Building materials, garden supply and equipment stores (6% of total retail). The pandemic remodeling boom petered out in late 2022, and sales fell for a while. Starting in June this year, sales began rising again, though they remain well below the peak of the pandemic boom:

- Sales: $42 billion

- From prior month: +0.4%

- From prior month, 3-month average: +0.8%

- Year-over-year: +5.8%

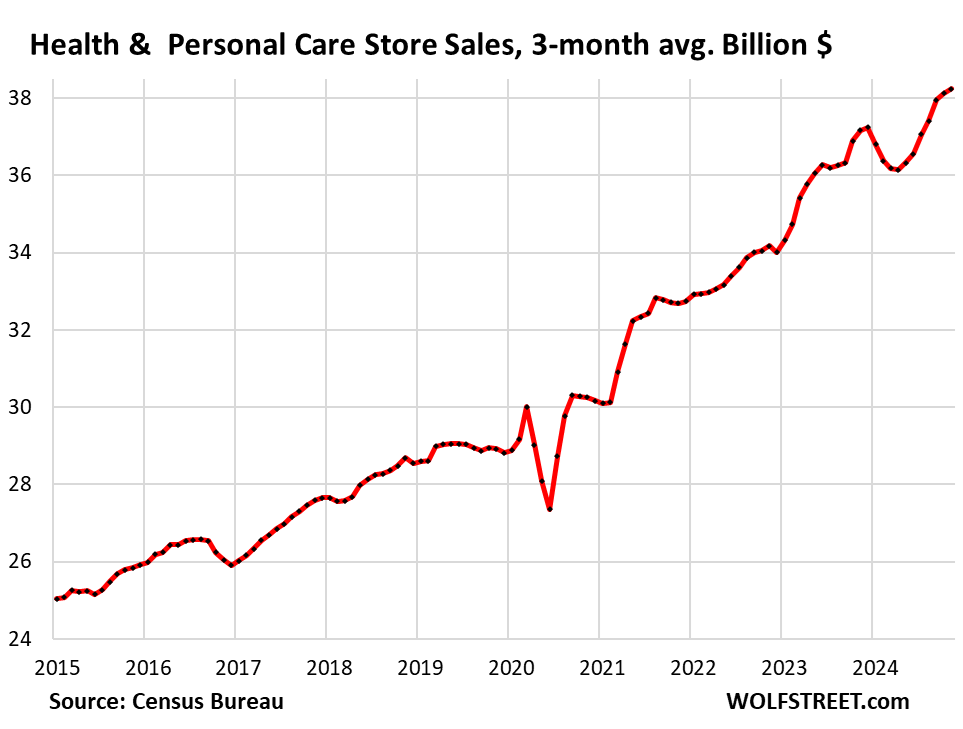

Health and personal care stores (5% of total retail). Note the sharp drop in early 2024, but in May, sales began to recover:

- Sales: $38 billion

- From prior month: unchanged

- From prior month, 3-month average: +0.3%

- Year-over-year: +2.9%

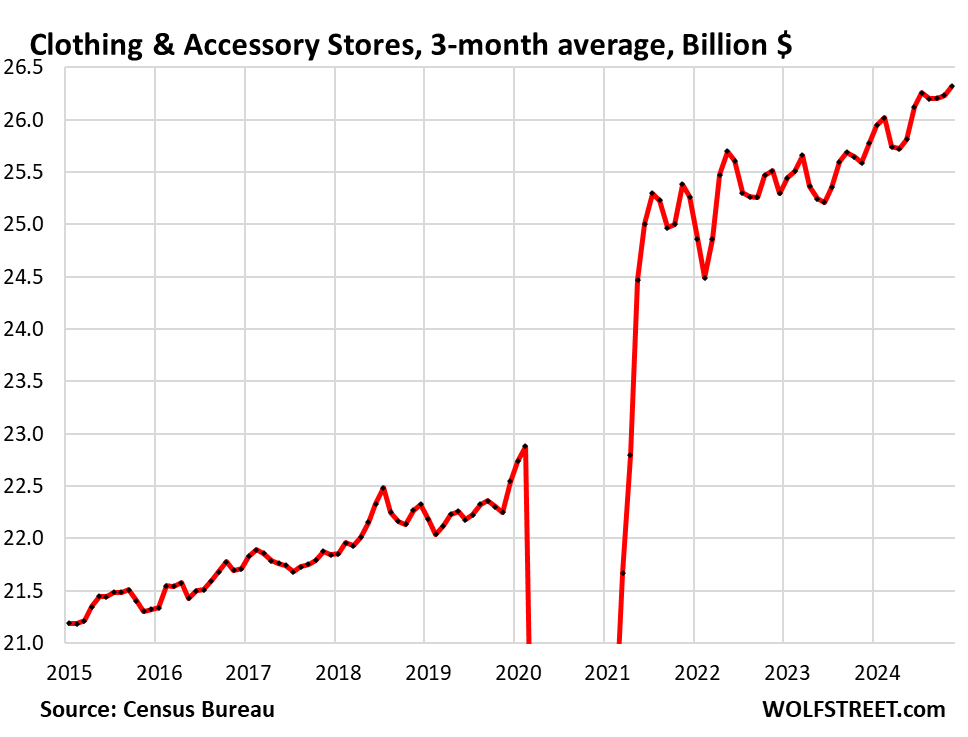

Clothing and accessory stores (3.7% of retail):

- Sales: $26 billion

- From prior month: -0.2%

- From prior month, 3-month average: +0.3%

- Year-over-year: +2.2%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

My worry is that wage increases may have slowed for the bottom half at a time when inflation appears to be reaccelerating.

Fair question. Is the inflation target really 2%? Inflation has been materially higher for years now.

Stock markets smell a problem.

A well respected multi billion asset manager said this week that the stock market IS the economy. It aligns with what I’ve been thinking for many years.

Which begs the question, who exactly are you going to sell too ?

Should the deflation of any one of numerous bubbles that are mysteriously inflated, given our religious belief that God would not do this too us actually makes it more likely that that is exactly what he/she deems to do.

Best wishes

Let’s look at the facts:

[1] GDP growth ~3%. Above the post-WWII average.

[2] Unemployment rate ~4%. Well below the post-WWII average.

[3] Job creation ~175k per month.

[4] Wage growth > 4%. Well above inflation.

[5] Inflation ~3%. The preponderance of evidence suggests it’s increasing — not decreasing.

[6] US stocks at highest valuations ever (or perhaps 2nd to 1999).

[7] US housing at highest valuation ever.

[8] US junk bond spread is lowest ever.

[9] An incoming president whose policies will likely be inflationary. (How much of course is unclear.)

Also — the Fed let inflation run rampant in 2021 while pouring on the QE.

If the Fed’s target were truly 2% — this fact pattern suggests they should raise rates (or at a minimum hold flat). Yet apparently they’ll cut.

What does all this tell you?

It tells the Fed to lower rates. Powell lost all credibility when he dropped 50 bp.

Inflation is going to be well over 2%, get used to it, and interest rates are going to be a lot higher than they were before, get used to it.

Now interest rates are about 4.5% and headline inflation is 2.7%. And the Fed is still doing QT.

Back in 2021, as inflation was shooting higher, interest rates were 0% and the Fed was still doing QT.

So people who draw comparisons to back then need to have their head examined.

Lots of bullshit getting spread here.

This is all by design, the US GOVMT DEBT is becoming too much of a burden from the standpoint of interest repayments owed. The GOVMT only has one way out of their spending problem, spend less… PAHAHAHAH just kidding. The GOVMT isn’t going to SPEND LESS. They are going to INFLATE out of the issue.

The fed at this point is nothing more than a TOOL of the GOVMT and the fed will use ANY rationale in order to justify the coming rate cuts

I am not sure that we should still use the “post-WWII” frame for comparison. 1945 was a LONG time ago… and the economic environment looked a LOT different than it does now. For the first 50 years of that timeframe there were no WTO or Free Trade Agreements for one thing… no Internet either.

Picking the year 2000 as the start of a new benchmark let me restate some of your statistics in bold…

[1] GDP growth ~3%. Average from 1950-1999 = 3.6% Average from 2000-2023 = 2.1%

[2] Unemployment rate ~4%. Average from 1946-1999 = 5.6% Average from 2000-2023 = 5.4%

[3] Job creation ~175k per month.

[4] Wage growth > 4%. (currently about one percent above inflation in 2024 but increasing as of late)

[5] Inflation ~3%. The preponderance of evidence suggests it’s increasing — not decreasing. Average Rate of inflation since 2000 = 2.5%

[6] US stocks at highest valuations ever (or perhaps 2nd to 1999).

[7] US housing at highest valuation ever.

[8] US junk bond spread is lowest ever.

[9] An incoming president whose policies will likely be inflationary. (How much of course is unclear.)

I am not sure what all this means but a case can be made for any direction the Fed moves… lower rates to promote GDP growth… raise them to lower inflation back to the quarter-century average…. stand pat and focus on reducing their Balance Sheet. I suppose this situation is what you get when you actually pull off the “soft landing” that you were aiming for.

**** ITEM 1 ****

Limiting to post-2000 only strengthens my point.

[1] GDP: We’re running ~50% hotter (~3% vs 2.1%).

[2] Unemployment: Data are unchanged by period.

[5] Inflation: On a CAGR basis, inflation was only 2% from 2000-2019. It was ~4% from 1945-1999.

You didn’t address points [3]-[4] and [6]-[9]. Regardless of time period, those points suggest we’re in:

[3]-[4] Good times.

[6]-[8] An all-time financial mania.

[9] A likely upcoming period of inflationary policy.

**** ITEM 2 ****

SpencerG and Thurd2:

You guys missed the point of my post.

I’m NOT asking “What will the Fed do?” (Thurd2) or “What should the Fed do?” (SpencerG).

I’m asking — “What is the Fed’s actual inflation target?” Not what they say — what they really want.

Wolf’s post (above) is on the right track. Perhaps I’m too hard a grader — but I’m looking for a little bit more. :-D

(And no — it’s not “they’re trying to make all their rich friends richer” like some folks here just love to rant. 🙄)

People are spending more on Retail because they have No choice.

It certainly is not fueled by a surge of CONfidence in the Economy.

LOL, you should look at the consumer confidence surveys that came out after Nov 5. The confidence of Republican-leaning consumers — which was in the dumpster before the election — exploded after the election. The confidence of Democrat-leaning consumers dipped a little after the election, but not much. And so overall consumer confidence surveys rose a bunch.

But what consumers have been spending on in 2024 and 2023 were even big discretionary items, such as motor vehicles. Consumers are flush with money, with wealth from the markets, with wealth from the home price surge in recent years (65% of households own their own homes), they’re sitting on trillions of dollars in cash, they got the biggest pay increases in decades, non-farm employment is at record levels, the burden of their debts are low… this is why demand from consumers is so strong.

I’ve been showing you this data in details over the past two years with countless articles. How could you have missed it? Or do you not ever read anything here? This is why people like you will never understand the US economy, and will always be surprised by it, and will come up with conspiracy theories to explain away its strength.

In 2020, there were 20 million unemployed and Wall Street was doing gangbusters.

Consumer spending is red hot in my little corner of the internet. Every time I refresh my orders page, there are new orders to be filled.

I feel a little bad for the salespeople standing around with no sales… customers just want to order stuff online instead. Store pickup orders placed thru the retailer’s website are also a big thing now.

The raw truth is the first step, which unless I misunderstood the message.

In store visits have been rejected in favor of the convenience of the on line impulse purchase.

That is so American.

Your comment is a form of e-commerce in action wang-dang, instead of going to the newspaper and paying for your comment to be printed in next week’s newsletter you do it for free electronically on Wolfs most splendid site.

Online orders and instore pickup has been my go to at the local home improvement store. I let them shop and bring it to the front of the store. They also take cash at that location and none other, so that works also. No more wandering around trying to find stuff that might not be there.

Also, since the cost to rent is now substantially lower (30-40%) than the cost to own a home, and 66% of Americans rent, they are saving huge amounts every month that are available to spend on everything else.

Really? So when my rent went up 30%, but home ownership went up 70%, I have 40% left to spend? Why wasn’t I informed sooner? I’m getting a boat!

The way it seems to work best is when the citizens work together to maximize the American way of life as the Founders took as a second nature while trying to imagine 2025.

Capitalism is normally distributed

The other way around, about 66% of households own their home.

Wait, are you telling me I need to cool it with my Lego purchases to help bring down inflation? Is my wife putting you up to this?

I think my family may be who you’re talking about. Not only is our mortgage on a 4bd home cheaper than the rent if a nearby 1 bd apartment, but the last two years I’ve seen the largest COLAs in my 17 years with my employer.

You are right. We are flush with cash. And we’re spending some but not too much. I’m going back and forth on whether to buy a Kia Telluride or Honda Passport.

I always love these – comments. Yes if you bought years ago your home is cheap.

People are talking about the cost to rent versus the cost buy currently.

Currently I can put 30% down on a house and still pay $2k more a month for a mortgage than rent. Therefore – currently buying would be terrible choice.

And that’s without the cost of maintenance and keeping the home somewhat updated.

But congrats to you on being in the right place at the right time – gen z may not be so lucky.

Or maybe we get another crash and they will be, hard to say.

I was just pointing out CCCB had the rent/ownership percentages backwards. But yes, lots of people who have either owned their home a long time or made a significant downpayment have mortgages well below the cost of comparable (or in your case much smaller) rentals.

Apartment rents have been insane since about 2010 and they all moved upmarket to chase being ‘luxury apartments'(it is still likely that there will be a dope dealer a few doors down). Many areas see 1 bedroom apartment rents just 20%-30% less than renting a 3 br/2ba house. A better comparison is mortgage cost for a comp versus rent/lease in the area for something similair.

76% of American homeowners have mortgages below 5% or no mortgage at all.

That is a huge factoid if accurate. The 76 pct are holding on to their lower monthly payment rather than laddering up in over priced real estate.

Meaningless, how much is their payment all in – including taxes and insurance. My owner neighbors pay 4-6x what I rent.

@Joshua here in CA it will cost around $7K month to “buy” a typical “million dollar home” (with a 20% down payment) but the rent will be closer to 50% in most places. Where are you renting a home for LESS than 25% of the cost to buy?

That doesn’t actually impact affordability, plenty of people maxed themselves out bidding 150k+ over asking in 2021. Now the property tax and home owners insurance increases have hit. All that matters is what the monthly payment is relative to their income – the rate doesn’t matter.

The only thing rate impacts is they don’t want to sell because they couldn’t afford an equivalent house with the current interest rates

Yes, recent FOMO buyers face a financial pickle. Many are listing their homes right now to avoid losses. They might derail the gravy train for all residential RE holders.

Based on a review of Redfin, many are trying to sell at 2021 prices, but there are no bites in many cases. Many homes are listed for 150 days or more.

Prices will likely keep dropping, but there is lots of variance by location. If there is new home building nearby, the outlook is dim.

While I’m sure *some* number of people have sold their home to rent for less, most renters have been renters while rents have been skyrocketing the past few years. So saying renters are “saving huge amounts” is not accurate IMHO.

In a very technical sense, it”s accurate. In a real sense it’s absurd. I’m “saving” many thousands of dollars by not buying and insuring a Ferrari, but the cost of my current car didn’t go down and the cost to insure my car keeps going up! More to the point, I can’t afford a Ferrari so by definition I can’t afford any of the luxuries I might buy with the money I’m saving not buying one

As a renter who saves about $40k a year by renting I disagree.

That’s without repair and maintenance costs considered so actually probably a bit more.

I’m also not unique, I know numerous people in the same boat.

What’s also a renting benefit but seldom thought about is the “opportunity cost” of the principle that’s embedded in home ownership. With 20% down, typically, and amortizing principle as part of a monthly bill, a homeowner earns nothing on that money. At minimum, right now, you’re missing out on 4.5%/annually on that idle cash.

If you consider that it’s possible that the full value of that principle, after 30 years (which few probably hang around for), not earning 4.5% and the compounding of that 4.5%, that adds up to a sizable “opportunity cost”.

@MM1 are you really “saving” and investing the $40K or are you just kike me and @Pea Sea that have both “saved” $600K by not buying a Ferrari SF 90 this year?

You mean the people who locked in low rates are saving tons while rents have skyrocketed. Saving a ton as the old place I rented more than doubled in rent since covid. Cheeehoo. Where am I going next??

It seems like, of the working class, there are two sub-categories. Those who have purchasing power due to their low mortgage rates, and those who are holding on for dear life waiting for rates to drop. People with purchasing power are keeping inflation on the rise which is crushing the people that are burdened by the homes they recently bought. The fed isn’t going to make significant rate cuts until the upper echelon of the working class cools it. The difference between this run of inflation and the last is that there are so many of these people locked in at 3%. Remember Wolf’s post a couple weeks ago where he commented that rates have almost never been at covid or post 2007 levels? The gap is growing again and this time its with the working class.

Wait, are you telling me I need to cool it with my Lego purchases to help bring down inflation? Is my wife putting you up to this?

I think my family may be who you’re talking about. Not only is our mortgage on a 4bd home cheaper than the rent if a nearby 1 bd apartment, but the last two years I’ve seen the largest COLAs in my 17 years with my employer.

You are right. We are flush with cash. And we’re spending some but not too much. I’m going back and forth on whether to buy a Kia Telluride or Honda Passport.

The success of the individual always shines on the community.

The fed should have just manned up and caused a mild recession in 2022. Instead by dragging this out it’s made everything worse. And yes especially for the poor.

At least some of people locked in low rates probably dont realize their good luck and are spending a lot keeping up with the Jones or whatever. And though I rent myself, Im kînd of suspicious of the tone of lot of these supposed renter posts. Maybe they are paying less than mortgage but some of the rents still sound high, like theyre renting a big cushy place. Thats fine if you can save a lot I guess but lets not shovel cash to greedy landlords levered up with cheap debt either.

This is only true if you’re comparing the costs of a new purchase (at current prices & rates) to renting.

However the result changes if you compare owner-occupied costs of a home, purchased at a lower price & rate, to current rents of a similar dwelling.

You guys are getting screwed in rents and mortgages because of the QE lowered the discounted cash flow hurdle.

If it’s of any use let me tell you a story about the housing market in 1982 when the interest rate was fifteen percent which stopped the rise in asset prices.

I, overcome by love and perhaps the nesting instinct bought a house against all rational warnings, which turned out to be a wrong headed thing to do.

Except when compared to the love that permeates the human population.

Consumers rushed to buy cars and other goodies to preempt Trump’s

25% tariff on Mexico and Canada and 60% on China.

The spread between US 10Y and the ECB, BoC, BOJ and PBOC is too high. Money might flow from all over the globe to finance our economy, unless they hike to 4%/4.5%. If they do there will be a run on the banks.

“The spread between US 10Y and the ECB, BoC, BOJ and PBOC is too high.”

This is by design. The Fed wants to out-hawk the rest of the world’s central banks to keep a bid under Treasuries.

Why would there be any ‘run on banks’ at all?

In 2025 demand for Chinese goods from Europe and the US might wane.

Iran has no money to maintain their oil assets. It’s (-)20C in Iran. The gov shut water and electricity for 3hrs/ day. They are using mazut (heavy oil for ships) to generate electricity. 90% of Iran is covered by poisonous clouds. If Iran cannot produce the PBOC might have to hike.

I was at a mall the other day, not my usual haunts. But there was certainly a happy energy and a LOT of bags being carried around. People not just browsing but buying. Maybe the election combined with record breaking stock prices have led to a “party like it’s 1999” vibe. That’s 25 years ago if you can believe it. Of course we all know how that ended but at the moment it was definitely something to be a part of. If you sold before the “pop” you were happy..but few did.

Something’s got to give as the national debt is set to hit $40T in about a year – but for now people are spending and dining out and buying cars and seeing $16 movies.

My problem is with the quantity of non recyclable packaging which vendors could be forced to pay for the external damage they cause.

I’m pretty sure the vendors are well aware of their free lunch. Discharge and dispose to avoid the cost of treating the disharge.

I’m a car dealer, selling vehicles mainly under $20k. This time of year prices are usually down, well……. These prices have drastically increased! Buy stock in Nike, going to be a lot of people walking.

For the most important people in the USA, (hint: That’s not us) 2 to 5% inflation is glorious. Pour it on Fed, the ultra-rich have never had it so good.

I am not an important person, but I have positioned my portfolio to benefit from rising inflation. You can too.

The Fed is now getting ready to lower interest rates in the face of rising inflation. This is the same J Powell who kept interest rates zero bound in 2022 in the face of 9% inflation. This clown is the worst Federal Reserve chair in the History of the Fed. He needs to submit his resignation ASAP.

He’s a lot better than the noodle Trump is going to put in his place, LOL. Trump wants 0% interest rates whatever inflation is. Trump is a real estate guy, he hates these interest rates we now have.

Yes but he can buy CME for pennies on the $. So which is better for a real estate guy?

Wolf, you are being a little hard on Trump, so to speak. Unlike his first term when he appointed all sorts of jackasses to his administration, he seems to be getting better advice now. He already said he is not going to try to force Powell to step down. However he is very likely to replace him when his term is up. Who he nominates is anybody’s guess. He might be a noodle, as you say, but he might not be.

if Trump is smart, he will replace Powell with an inflation hawk, and then roll responsibility for the higher inflation his policies might entail onto the Fed and let the Fed mess with it. “It’s the Fed’s job to deal with inflation,” he could say and wash his hands off it. But that would contradict his earlier pronouncements about wanting more control over the Fed, and lower interest rates.

What politicians say they’ll do to actually get elected and what they do when in office are 2 different things.

Trump won because of inflation but also knows Americans were upset over high interest rates. Which lowering interest rates is likely to cause inflation.

A couple things why I think it’s hard to predict:

1. He can blame the inflation problem on the current administration and be the hero if he were to bring it down. If he wants to go that route he’ll be unlikely to push for zero interest rates. There’s nothing that a narcissist loves more than being the victim or the hero. This gives him both.

2. If he wants him and his buddies to be able to buy real estate for pennies on the $ rates stay high. Probably depends on his portfolio – he’s a debt guy so the likelihood he can weather high rates might be low.

3. If he wants to inflate his and his friends asset prices and not purchase anything, rates go to zero.

4. Inflation loses elections and now that it’s on everyone’s mind we all notice the price increases everywhere – if he cares at all about his approval rating or his parties future – he needs to tackle inflation. Narcissists care a lot about approval ratings as well as their legacy.

5. He can’t be elected again so people’s incentive to appease him goes down over the course of his term.

6. The fed might just be a scapegoat he likes blaming for things. He could publicly berate them, while privately saying keep rates where they are.

This all assumes he can influence interest rates. The fed is supposedly independent.

Thurd2-

“He might be a noodle,” as Wolf stated….

Or, SHE might be a hard-money advocate.

Trump’s been throwing wrenches around, and showed interest in Judy Shelton during his last Whitehouse stint.

Shelton’s Yahoo Finance interview of 8/1/24 is substantive, sober and realistically Fed-critical. (Keep in mind that the interview is conducted before the 50BP and today’s 25BP cuts, as well as well before the presidential election.)

Perhaps a RE-nomination?

I remember seeing an interview with Trump when it was president last time and he was upset because Jerome Powell wouldn’t give him negative interest rates.

He said with negative interest rates he could go out and buy up real estate cheap and make a lot of money.

I know Trump is supposed to be a super smart guy I’m surprised he doesn’t understand that low holding interest rates artificially low for a long time and quantitative easing is not good for the savers, it’s not good for the poor middle class.

I voted for Trump three times, because the left has gone crazy and been taken over by communist. The core Democratic party was complaining about this how the left has been taken over by Marxist.

I don’t know what’s going to happen, well I do know what’s going to happen it’s already happening we’re heading into a recession. Why do you think the FED is cutting rates.

This is going to be the mother of on recessions too people don’t see it coming but it’s going to be huge. Look how deep the 3-month and 10-year have inverted.

“The few who understand the system…will either be so interested in its profits or so dependent on its favors that there will be no opposition from that class, while on the other hand, the great body of people, mentally incapable of comprehending…will bear its burdens without complaint.”

— John Kenneth Galbraith

“… we’re heading into a recession. Why do you think the FED is cutting rates.”

BS. Interest rates are about 4.5% and headline CPI inflation is 2.7%. And the Fed is still doing QT.

The Fed CAN cut because rates are substantially higher than inflation. Nothing to do with a recession. Why is this so hard to grasp? What mental capability do you people lack to grasp this?

Back in 2021, as inflation was shooting higher, interest rates were 0% and the Fed was still doing QT. That was reckless, but that’s not the case today.

How would negative interest rates make real estate cost pennies on the $? Negative rates would make prices soar and be super expensive.

The 3-month and 10-year are no longer inverted (as of last Friday). Saying “look how deep” they’ve inverted is untrue and missing out on what’s happening in the economy. Since early September, all intermediate points on the yield curve are up 50-60 basis points while the 3-month has dropped nearly 80 basis points. Yesterday, for instance, the 3-month was 4.38% and the 10-year was 4.40%. The Forward Curve is also showing short-term rates falling more (sub-4%) while long-term rates inch up another basis point or two in the next year. The FC is never right, but it’s a better prognosticator than the inane babble above.

Also, the comments about communists and marxists is lame. I voted against Trump 3x and I can assure you it had nothing to do with communism or marxism, as if you even know what those terms mean vs. just hearing them bandied about on the internet.

Granted, current rates are substantially higher than inflation, but inflation is still way above the supposed 2% target. If they cut, inflation fighting isn’t the priority. Fighting recessions is the priority. Shouldn’t they be transparent about that?

Also, if there isn’t any timeline for getting inflation down to 2%, there is no pressure to achieve the goal.

John-

Galbraith’s OTHER quote about what is “understood” in economics:

“The function of economic forecasting is to make astrology look respectable.”

—John Kenneth Galbraith

Didn’t Trump appoint Powell?

Sure. And then Trump keelhauled Powell on a daily basis over the 2% interest rates and that little bitty QT they were doing at the time.

Didn’t he marry Marla Maples? Build 3 competing casinos in one town? Start a pro football team? Etc.

And, as a reminder, Powell is Trump’s guy from the last time around. Not an economist but rather a “businessman”. Businessmen have no business being in government positions.

If you want a preview of where we are going, I think the period between 1970 and 1985 gives a good picture of our future. A lot of very interesting stuff occurred in that particular timeframe.

Swamp Creature,

I’m still waiting for you to provide an example of a new-issue CD that offers a 5% yield. You keep claming they exist but I don’t think they do.

I don’t sense (just an opinion) that inflation is done. People are keeping up with the Jones’s and then some. But – my property tax is going up 5.24% next year. And my YouTube TV is going from 72 to $82 per month next year. And my utility asked the State for a 9% increase. Auto insurance 12% and so on. It aint over yet.

TK – Agree 100%. If by “inflation is done” you mean inflation is on course to drop back down to the Fed’s stated 2% target, it’s nowhere close to done. There’s still far too much money (and paper wealth) floating around, and the Fed’s rate cutting and the government’s deficit spending aren’t helping. The purchasing power of the U.S. Dollar is under attack. The Dollar is the cleanest of all the dirty shirts, but boy is it getting dirty. And forget about it if we see major new tariffs on foreign goods next year… just wow. To repeat, we are nowhere close to done with inflation. Wolf’s recent articles about consumer and producer inflation bear this out.

I can’t wait to see the reactions of those who trade out of US dollars into intangible shadow offshore digital assets, with help from the cronies of the new promoter in chief. They are even further out on a limb.

I still cannot get over $13 for a #1 combo at most fast-food establishments especially when a Longhorn Steakhouse lunch is $9.99.

Will the fed lower tomorrow? They like to see things as a blob of moving mass that needs many pokes to fully alter its course. The greatest fear is a depression-like condition where money exchange slows, and it is unable to parasitic binge feed to support the endless commitments of debt.

Yeah, I think they lower despite the signs.

Inflation will never go down with a stock market at all time highs. Higher stock prices == more spending power.

We’re going to have it for years because the fed wants to lower inflation without causing the stock market to go down or unemployment going up – which imo is an impossible task.

To bring inflation down people need to spend less – to cause that there will need to be some suffering.

“To bring inflation down people need to spend less”

Or companies will need to produce more.

“Higher stock prices == more spending power.”

I don’t think this is true. I just tried to pay for some groceries with my stocks but I was told I can’t use them for payment.

I think you have to /sell/ the stock first before it can be used to pay for something – but then you no longer own the stock.

I don’t think they’ve ever been data dependent, otherwise we wouldn’t have had 9% inflation.

So here’s the million $ question – the fed won’t step up and deal with inflation. So what black swan event will take down the market and create a more spending cautious consumer?

In spite of all those signals that Inflation on rise, FED will cut rate tomorrow Dec 18.

FED is catering to Wall St more than US common people.

Powell himself said we have put 100 BP point cuts in Sept SEP meeting. It is like he was committing to it. If they were serious, all of them had ample opportunity to change Market expectation of 25 BP cut in Dec. When they got 2 Jobs report and 2 CPI reports. They never took that opportunity. So its like kind of decided.

Real courage will be NO CUT in December.

It is most certainly not the job of the Federal Reserve to cater to so-called ‘common people’ at all. It is the US bank of banks which regulates and allocates funds to member banks. Period.

Price stability and maximum employment, isn’t that explicit in the job description? A manager of a flexible currency that adjusts to crashes, by spreading liquidity, then mopping it up again, isn’t that supposedly the basic architecture?

No. That’s how it used to work or at least people thought it worked a very long time ago, but certainly not now.

Oh, the strong retail sales, robust labor market, increasing inflation, massive government debt. Fed’s response: “It’s all transitory, let’s lower rates.”

Wolf, how about an article about who Powell is actually trying to please with these cuts in the face of obvious inflation?

I’m going to do an article about people spreading bullshit on my site.

Inflation is going to be well over 2%, get used to it, and interest rates are going to be a lot higher than they were before, get used to it.

Interest rates are about 4.5% and headline inflation is 2.7%. And the Fed is still doing QT.

The Fed CAN cut because rates are substantially higher than inflation. Why is this so hard to grasp. What mental capability do you people lack to grasp this?

Back in 2021, as inflation was shooting higher, interest rates were 0% and the Fed was still doing QE. That was reckless, but that’s not the case today.

You are confusing me. Third time you have stated the last paragraph. QT in 2021???

Typo. Thanks.

Why?

Inflation never hit 2%, it didnt even touch 2% for 1 single month in 3 years of rate hikes. And inflation is reaccelerating. Financial Conditions are loose, everything continues to make record highs except mortgage loans which is in the dump. How many years is it going to take to get back to 2% without a severe recession or depression?

The 10 year US treasury is on the verge of breaking out to the upside. Because of inflation expectations and risk.

The 10 and 30 year Japan and UK treasuries are also on the verge of breaking out to the upside.

And the moment China dumps massive stimulus and money, their treasury is going to do a Uturn to the upside.

The moment the bond market in the 10 year decides the FED is no longer getting back to 2% like the FED has been lying about for 3 years, is the moment the fun starts. Realtors and the mortgage industry are crying Uncle now. Its going to get a lot worse with higher 10 year yields. And it will create massive job loss with it.

The government in the US is burying the middle class. The US birth rate is at an all time low. People dont have kids when severe hardship takes place financially, look at the GFC data and how births cratered. Its only going to get worse with higher inflation.

The US has a MAJOR inflation problem. Truflation is warning about it. Apollo released and article warning about it. And now the talk of the town all over the place is the US 10 year treasury because everyone is talking about it going up and signaling a warning.

Wow! That’s a lot to digest. Lol. I thought Wolf inadvertently wrote QT when it was actually QE. ???

sure did. Typo, now fixed

What is the normal margin between inflation and interest rates? Inflation appears to be headed back to 4% in the near term (next 6 months or so).

The fed seems to have a bias to panic cut at any sign of weakness and to wait a long time before raising when there’s any sign of accelerating inflation. So I feel like we can call any rate semi- permanent because they won’t be reversed without at least a year of bad inflation data

The price of money sitting on the side doing nothing and getting a small reward for saving it so others can deploy it. Around 1.5%.

Want more? You must deploy it yourself.

If inflation heads back to 3%, or even 4%, the Fed can hike again. What’s the big deal? Right now inflation is 2.7% and rates are at around 4.5%. We haven’t had that big of a positive spread in decades. More often over the past two decades, it was a negative spread.

You mentioned a few articles ago that annualized CPI was 3.8%. Now the current fed funds rate is around 4.5%. The normal spread is about 1%. Do the math. The Fed should raise 25 bp, not cut 25 bp.

You picked the yearly CPI of 2.7% for your argument. Personally, i dont care what inflation was 12, 9 , 6 or even 3 months ago. I picked the most recent monthly data, just as we both picked the most recent fed funds rate.

We look at annualized monthly inflation as an indication of direction because year-over-year reacts so slowly to turning points. But this month-to-month data is very volatile with big ups and downs. So we look at year-over-year data for actual inflation rates the way they’re used and measured. The Fed’s policy statements when we see them today, all use the year-over-year figures.

Interest rates are not restrictive at these levels (as shown by the current and recent economic situation) no matter what the Taylor Rule would indicate. Plus, the “long and variable lags” of past rate hikes (the last from July 2023) are mostly already absorbed into the economy (likely – the big hikes came far previous to July 2023). The Fed is tapering QT and signs point to them ending it relatively soon. This does look like a repeat of 2021 in that they are yet again underestimating inflation and being overly dovish.

The bond market is calling the Feds bluff. 2% future inflation is a complete joke.

“The median home price in California declined by 4% on a monthly basis to $852,880 in November, according to the California Association of Realtors. ‘The November median price had the largest October-to-November drop since 2008′”

Ruh ohhhh. Now watch supply skyrocket in the months ahead as Fear in California, which everyone has waited for, starts. If Cali real estate breaks to the downside, you know what that means….

Rates are strangulation-restrictive in residential and commercial real estate, mortgage banking, real estate lending, CRE construction, etc. which are in a depression. In other areas, they’re not restrictive. So it’s every mixed.

I stand corrected after today’s Fed meeting and press conference.

Are you saying that Powell and the fed are good with inflation running hot?

Higher for longer, higher inflation and higher rates. The Fed has said it for two years, as have I.

I just read an article about 40 minutes ago that contriubtes the increase in car sales as happening mostly in the SouthEast, which experienced a historic number of storms in a very short period. Floods and damage from hurricanse totalled many vehicles, which needed to be replaced. However, in the rest of country the story is not the same as car makers have raised car prices to historic levels in the past 2 years. Now, in order to move these vehicles the car makers are reintroducing rebates and other financial incentives such as below market lending rates through their finance companies.

BS. That article, if it actually exists, was by morons for morons.

The manufacturer I work for has given special incentives to customers living in the areas affected by the hurricanes. I am not sure how much this has increased sales because we are not a part of that region. However, I can tell you that prices are way down and volume is way up on the other side of the country. There are some good deals to be had now that inventory for many models is plentiful.

There were hurricanes in the past that destroyed maybe 300,000 vehicles when they hit Houston and flooded parts of it. But the hurricanes this year didn’t destroy many cars.

Even when 300,000 vehicles ended up getting flood titles or salvage titles back then, some of them were fixed and used or sold, and others were replaced by other used vehicles — because that’s what the insurance pays for, it doesn’t pay for a new vehicle. So the impact even back then on new vehicles sales wasn’t even noticeable, in the large number of new vehicles sold over a multi-month period. We covered this at the time. What was noticeable was the appearance of these cars on the informal used vehicle market. And we warned people about it at time, check for signs of flood damage, we said.

These recession mongers always come up with some BS to try to support their fantasy that the economy is actually in a recession despite all the growth left and right.

The FED shouldn’t target interest rates. It should just drain reserves. Money is still too loose. Short-term monetary flows, the volume and velocity of money will push 4th qtr. R-gDp higher than the 3rd qtr.

“The Fed Needs to Watch Out to Not Throw More Fuel on this Demand”

LMAO. They’re cutting. You know it, I know it, everybody knows it. Raging inferno, meet fuel tanker.

What if’ there isn’t actually a correlation between rates and inflation? What if inflation was already coming down when the Fed started hiking?

Maybe the Fed thinks inflation will stay elevated despite any theoretical rate hikes, so what’s the point?

Maybe the Fed doesn’t want to stimulate by providing more interest income to bondholders?

Maybe the Fed feels continuing QT is enough to keep inflation in check?

Many possible explanations for the Fed doing what some call irrational rate cuts.

If these drunken sailors would save the money they could actually afford a home. Instead they live in despair and say I’ll never be able to afford one and spend their excess money.

Meanwhile those with paid off or nearly paid off mortgages don’t care what things cost and buy with no impulse control.

As far as wage increases, the only way I see them in higher salary ranges is to quit and find a new job. And that’s getting harder as the number of applicants in engineering, technology etc is literally 100 plus per job post

People will continue to spend money rather they have it or not because we are conditioned by our government that they will bail us out if it hits the fan. Few Americans are financially competent.