On re-spiking motor vehicle prices, jumping food & gasoline prices. But housing inflation backs off.

By Wolf Richter for WOLF STREET.

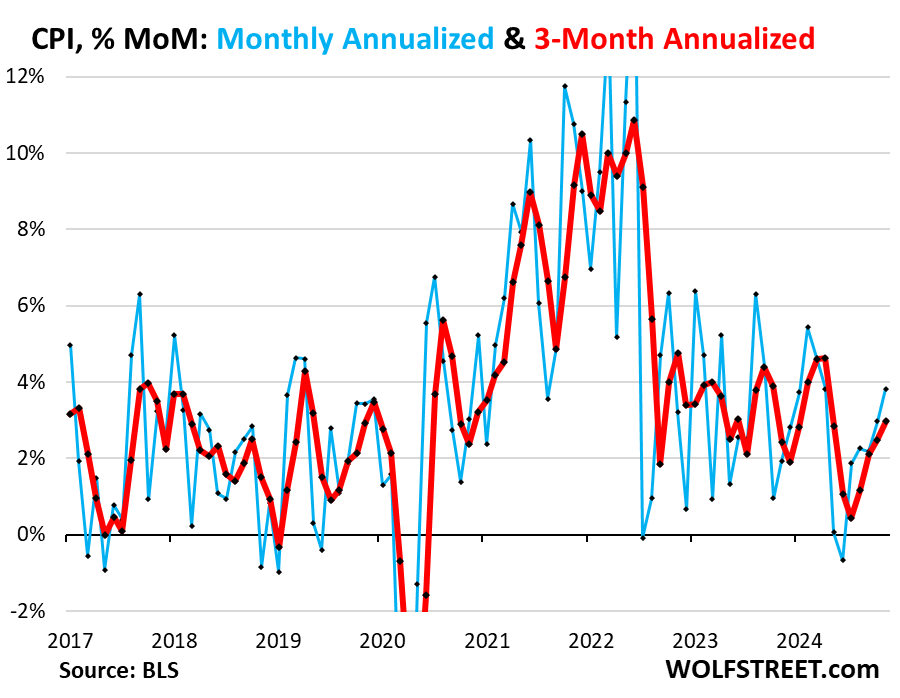

The overall Consumer Price Index rose by 0.31% (+3.8% annualized) in November from October, the sharpest increase since April. It has been accelerating since June (blue).

The three-month average jumped by 3.0% annualized, also the sharpest increase since April, and the fourth month-to-month acceleration in a row:

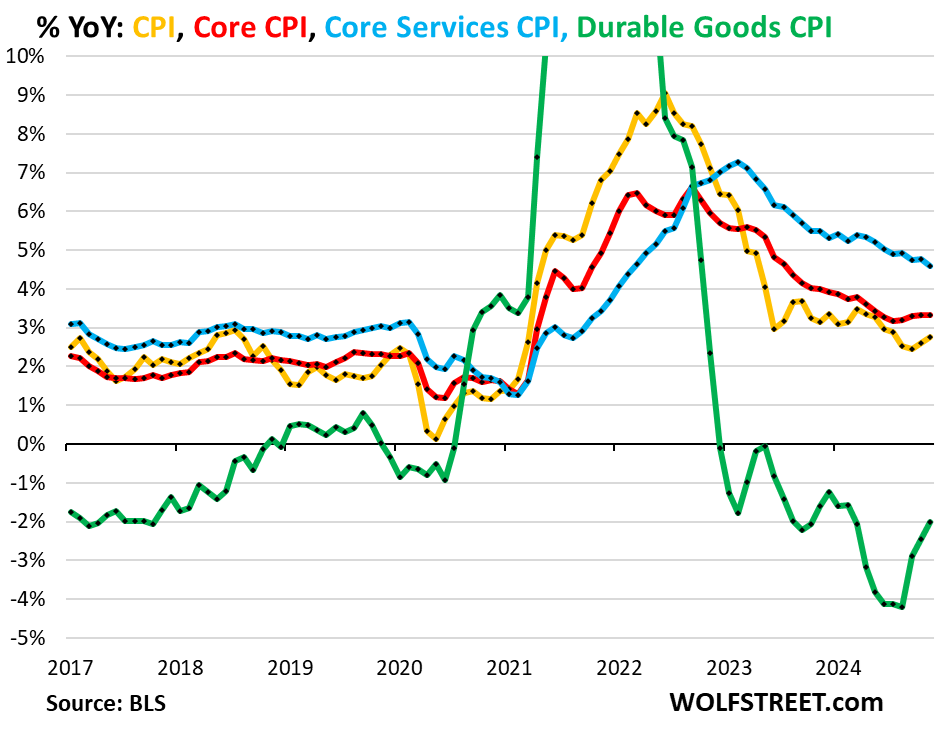

On a year-over-year basis, CPI rose by 2.75% in November, the second month in a row of acceleration, up from 2.60% in October.

The Core CPI, which excludes food and energy components to track underlying inflation, rose by 3.32% year-over-year. It has been in this range for the sixth month in a row, and above where it had been in June.

The major components, year-over-year:

- Overall CPI: +2.75% (yellow).

- Core CPI +3.32% (red).

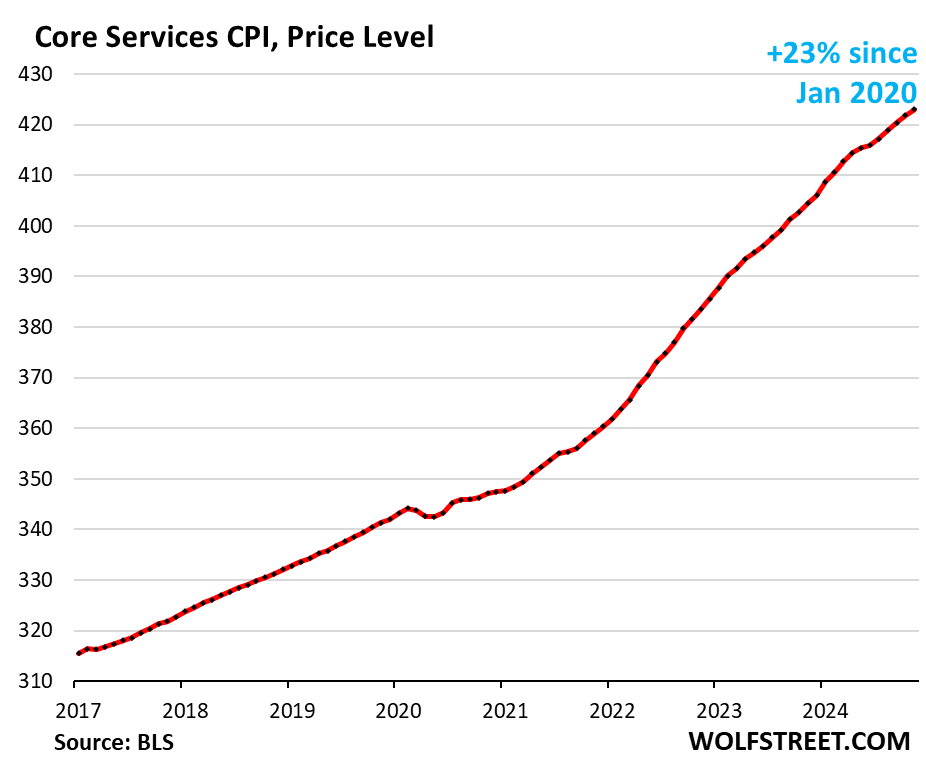

- Core Services CPI: +4.58% (blue).

- Durable goods CPI: -2.01% (green).

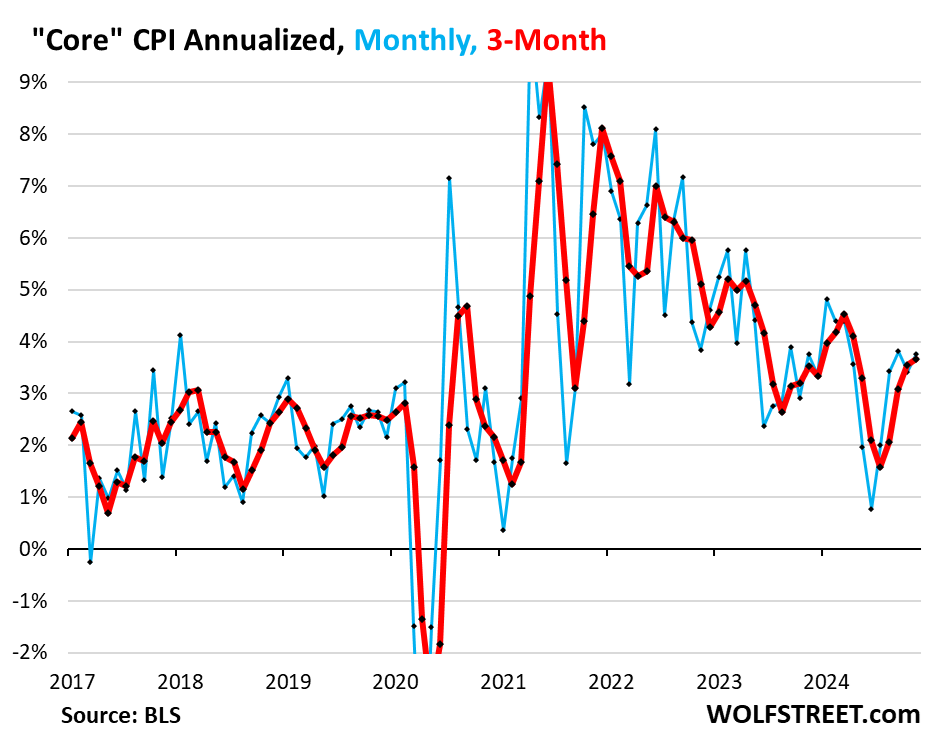

Month-to-month “Core” CPI rose by 0.31% (+3.8% annualized) in November from October. Over the past four months, core CPI has risen in this range of +3.4% to +3.8% annualized, the biggest increases since March (blue in the chart below).

The 3-month average “core” CPI accelerated to +3.7% annualized, the fourth month of acceleration in a row, and the highest since April (red).

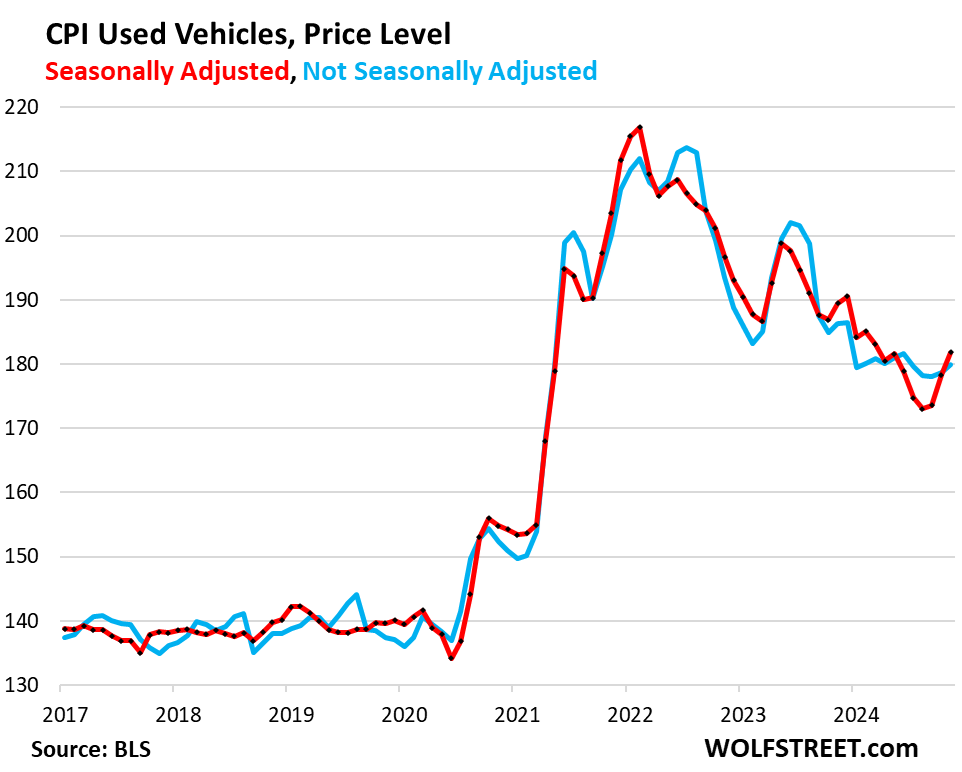

The sharp price increase of used vehicles in November, the third month in a row of price increases, was a big factor in the stubbornly high and accelerating core CPI rate, having U-turned from a historic plunge that until mid-2024 had been one of the big factors in the cooling of core inflation.

Used vehicles, on a month-to-month basis, are now fueling inflation, and we have seen that for months beneath the surface in rising used-vehicle wholesale prices, very tight inventories, and strong demand (stimulated by the plunge in prices from early 2022 till mid-2024).

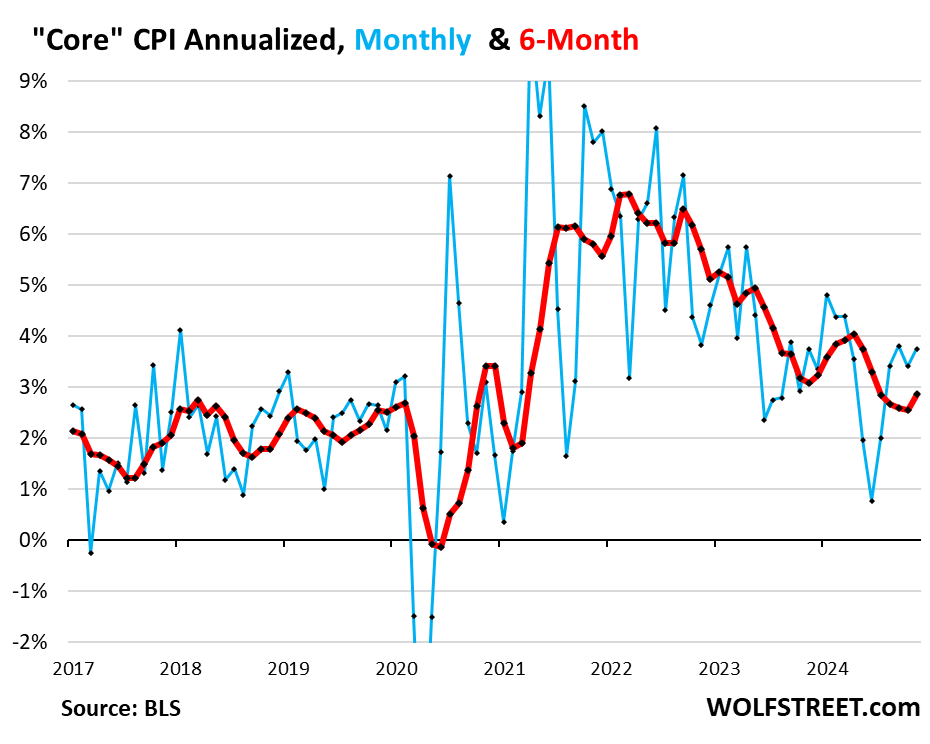

The 6-month average “core” CPI – which irons out most of the month-to-month squiggles but lags further behind – accelerated to +2.9% (red):

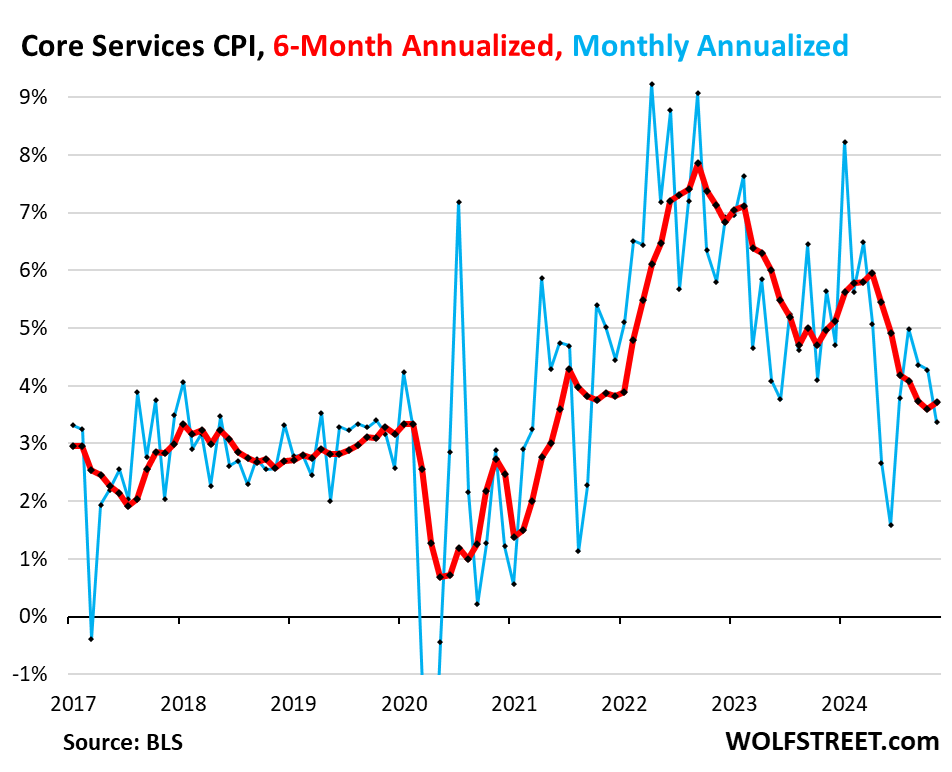

“Core services” CPI.

The core services CPI decelerated to +3.4% annualized in November from October (blue line in the chart below), which cooled the 3-month average to +4.0%.

The 6-month core services CPI, which irons out a lot of the month-to-month squiggles, accelerated to 3.7% annualized (red).

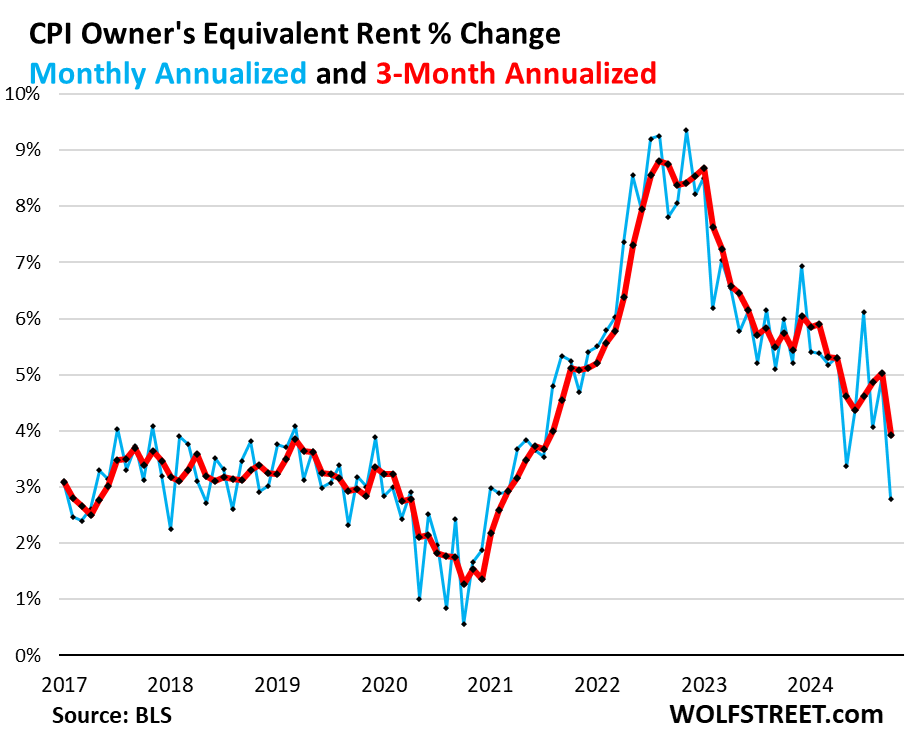

The housing components of core services.

The Owners’ Equivalent of Rent CPI decelerated sharply to +2.8% annualized in November from October (blue in the chart below). The three-month average decelerated to +3.9% annualized (red). Both of these increases were the lowest since 2021, after the sharp increases in the prior months.

OER indirectly reflects the day-to-day expenses of homeownership: homeowners’ insurance, HOA fees, property taxes, and maintenance. It is based on what a large group of homeowners estimates their home would rent for, with assumption that a homeowner would want to recoup their cost increases by raising the rent.

It accounts for 27% of overall CPI and estimates inflation of shelter as a service for homeowners – as a stand-in for the costs that homeowners pay for, such as interest, homeowner’s insurance, HOA fees, maintenance, and property taxes.

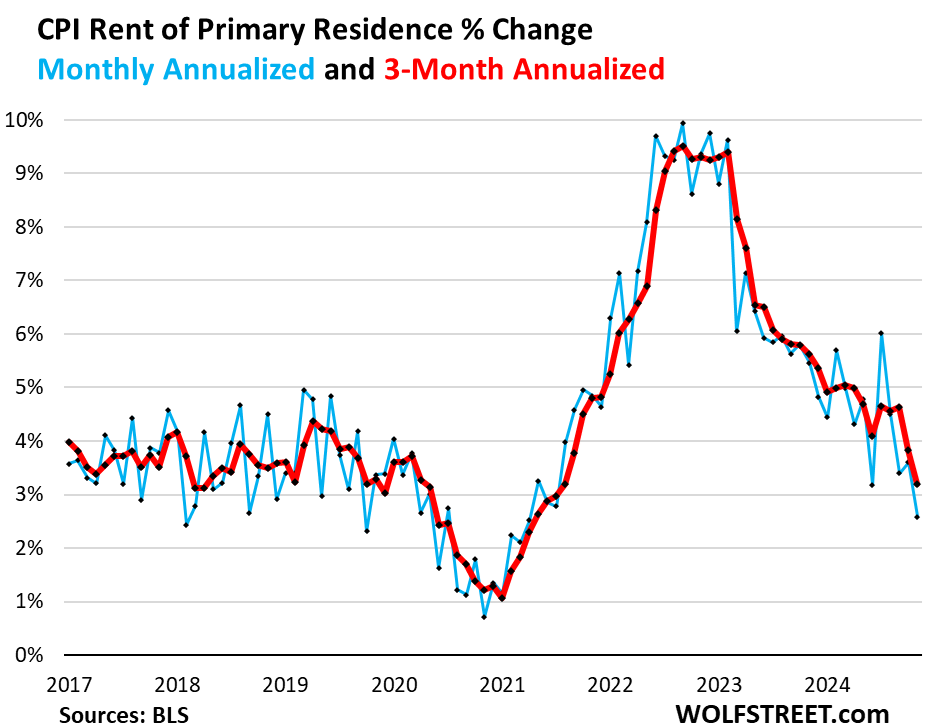

Rent of Primary Residence CPI decelerated to +2.6% annualized in November from October (blue in the chart below). The 3-month rate decelerated to +3.2%. Both of them were the lowest since 2021.

Rent CPI accounts for 7.7% of overall CPI. It is based on rents that tenants actually paid, not on asking rents of advertised vacant units for rent. The survey follows the same large group of rental houses and apartments over time and tracks the rents that the current tenants, who come and go, paid in rent for these units.

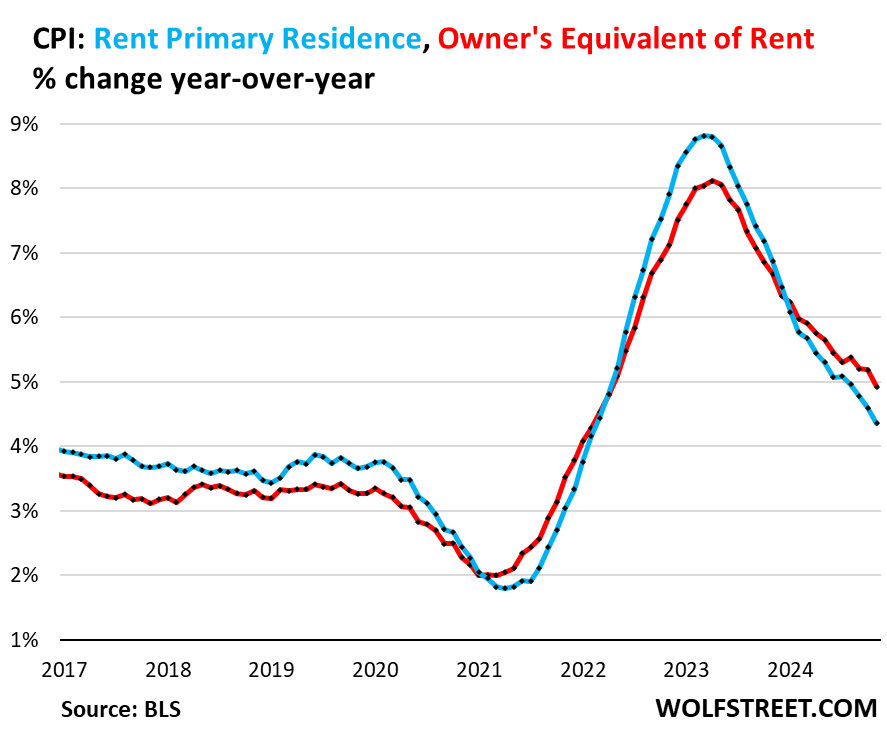

Year-over-year, both continued to decelerate: OER CPI +4.9% (red), Rent CPI +4.4% (blue):

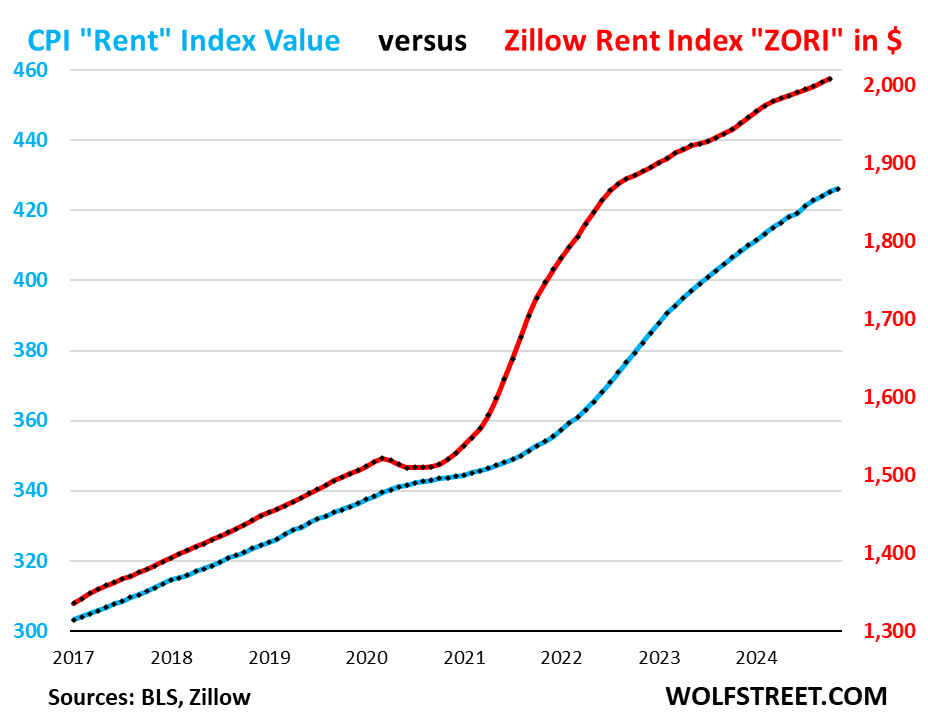

“Asking rents…” The Zillow Observed Rent Index (ZORI) and other private-sector rent indices track “asking rents,” which are advertised rents of vacant units on the market for rent. Because rentals don’t turn over that much, the spike in asking rents through mid-2022 never fully translated into the CPI indices because not many people actually ended up paying those jacked-up asking rents.

For October, the ZORI (seasonally adjusted) rose by 0.24% month-to-month and by 3.3% year-over-year. Zillow has not yet released the November figures.

The chart shows the CPI Rent of Primary Residence (blue, left scale) as index value, not percentage change; and the ZORI in dollars (red, right scale). The left and right axes are set so that they both increase each by 55% from January 2017.

Since January 2017, the ZORI has soared by 50%, and the CPI Rent by 41%. Since January 2020, the ZORI has soared by 33% and the CPI rent by 26%.

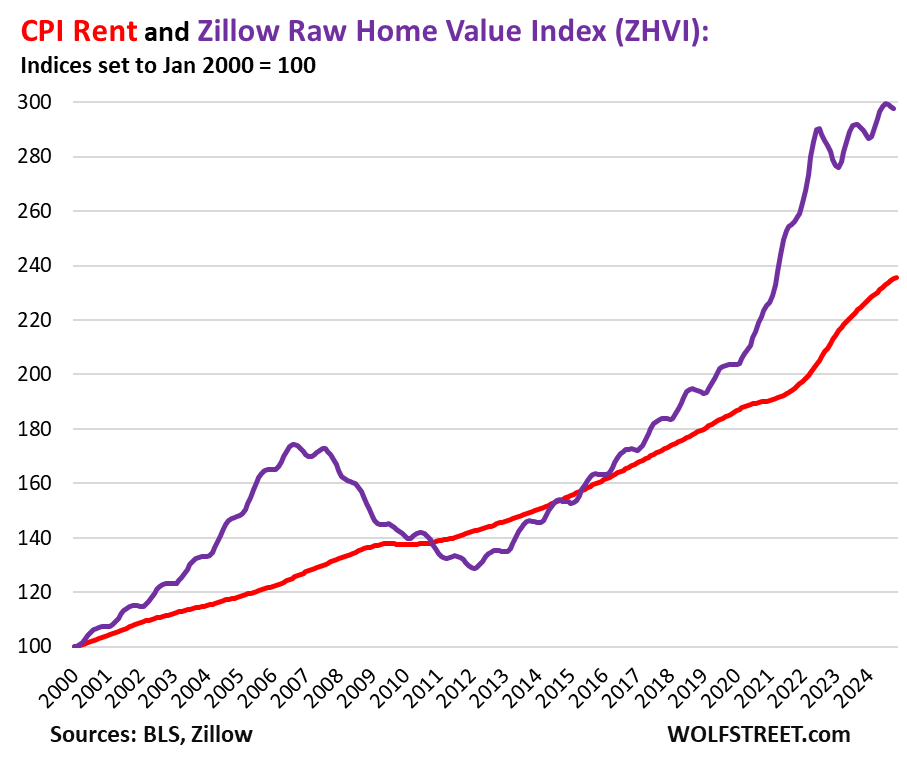

Rent inflation vs. home-price inflation: The red line in the chart below represents the CPI for Rent of Primary Residence as index value. The purple line represents Zillow’s “raw” Home Value Index for the US. Zillow has not yet released the November data [for charts of each of the largest, most expensive 30 metros, check out The Most Splendid Housing Bubbles in America ]. Both indexes are set to 100 for January 2000:

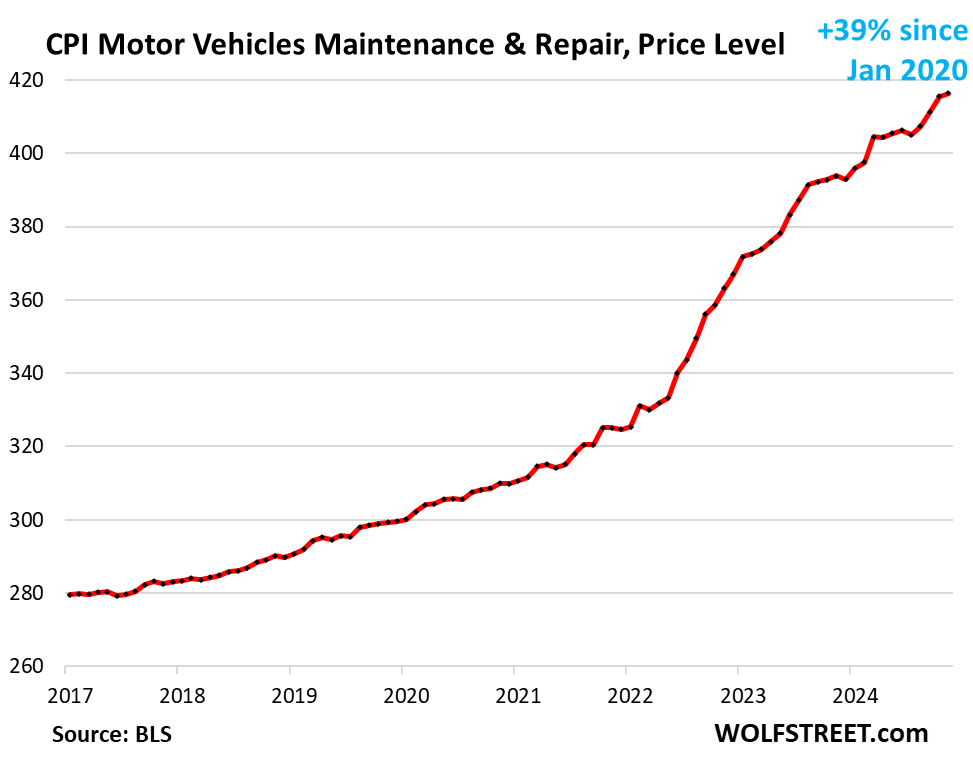

The CPI for motor-vehicle maintenance & repair ticked up by 2.4% annualized in October from November, after having spiked by 13% and 12% annualized in the prior two months.

Year-over-year, the index rose by 5.7%, after the 5.8% increase in October, both of which are the highest since June.

Since January 2020, it has spiked by 39% as the costs of labor and replacement parts have surged.

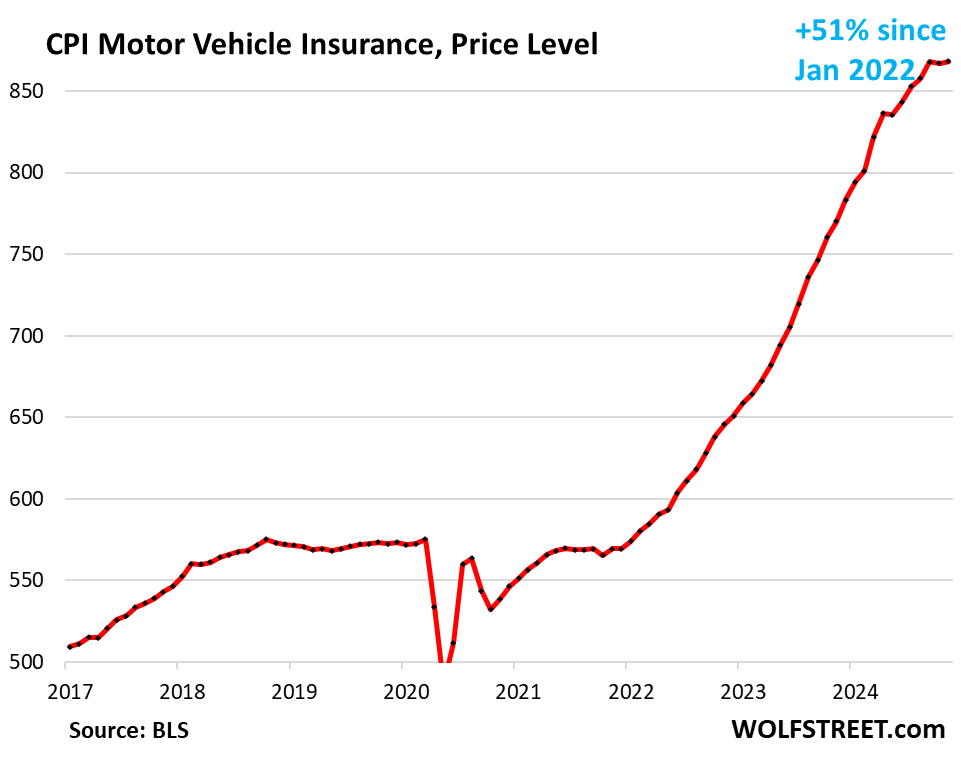

The CPI for motor vehicle insurance rose by 1.6% annualized in November from October, after a dip in October, and a 15% annualized spike in September.

Year-over-year, it rose by 12.7%. Since January 2022, it exploded by 51%.

The massive inflation in motor vehicle insurance was fueled initially by the spike in repair costs and used-vehicle prices (replacement values) in 2021 and 2022, though used-vehicle prices have plunged since then. Since 2023, insurers were able to increase their profit margins by increasing their premiums even as replacement costs plunged.

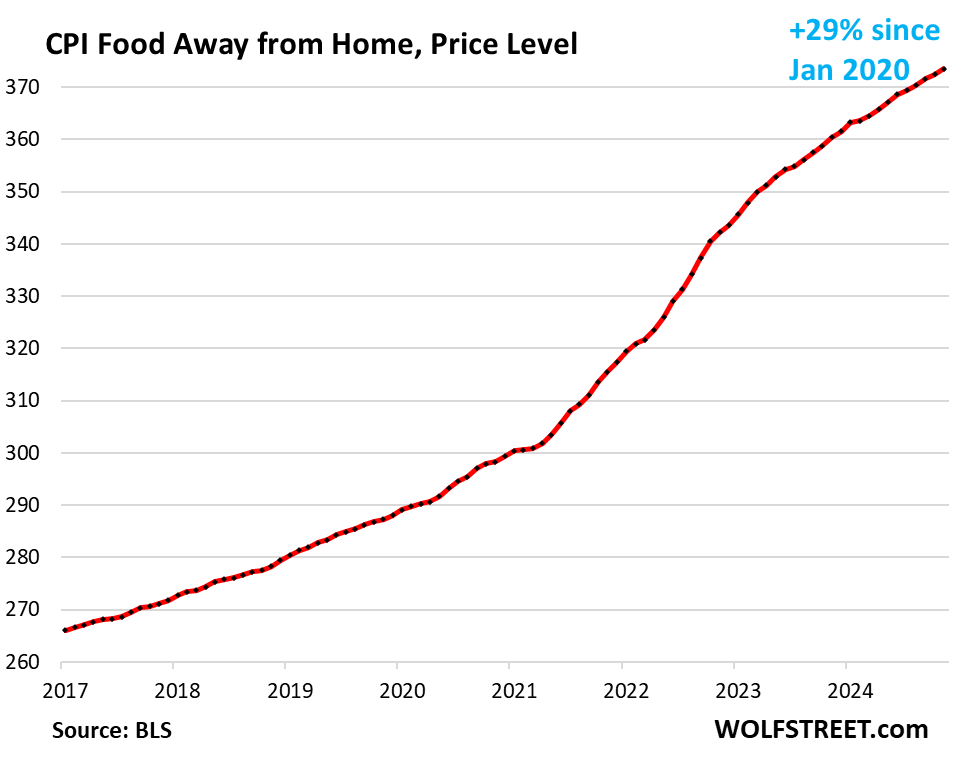

Food away from Home CPI rose by 3.4% annualized (+0.28% not annualized) in November from October.

Year-over-year, it rose by 3.6%, the smallest increase since August 2020. Since January 2020, it has surged by 29%.

Often called food services, the category includes full-service and limited-service meals and snacks served away from home, such as in restaurants, cafeterias, at stalls, etc.

| Major Services ex. Energy Services | Weight in CPI | MoM | YoY |

| Core Services | 65% | 0.3% | 4.8% |

| Owner’s equivalent of rent | 27.1% | 0.2% | 4.9% |

| Rent of primary residence | 7.7% | 0.2% | 4.4% |

| Medical care services & insurance | 6.5% | 0.4% | 3.7% |

| Food services (food away from home) | 5.4% | 0.3% | 3.6% |

| Education and communication services | 5.0% | -0.2% | 1.8% |

| Motor vehicle insurance | 3.0% | 0.1% | 12.7% |

| Admission, movies, concerts, sports events, club memberships | 1.8% | 1.2% | 4.1% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 1.5% | 0.4% | 4.2% |

| Lodging away from home, incl Hotels, motels | 1.4% | 3.2% | 3.7% |

| Motor vehicle maintenance & repair | 1.3% | 0.2% | 5.7% |

| Public transportation (airline fares, etc.) | 1.1% | 0.0% | 2.9% |

| Water, sewer, trash collection services | 1.1% | 0.6% | 5.2% |

| Video and audio services, cable, streaming | 0.9% | 0.7% | 3.5% |

| Pet services, including veterinary | 0.4% | 0.6% | 7.1% |

| Tenants’ & Household insurance | 0.4% | 0.0% | 2.0% |

| Car and truck rental | 0.1% | -3.0% | -8.0% |

| Postage & delivery services | 0.1% | -0.1% | 9.8% |

The Core services CPI overall has risen by 23% since January 2020.

Durable goods.

New and used vehicles dominate this category, followed by information technology products (computers, smartphones, home network equipment, etc.), appliances, furniture, fixtures, etc. All categories experienced price declines starting in late 2022, after the price spike during the pandemic. But the sharp month-to-month price declines in motor vehicles ended in September, and prices have risen since then.

The used vehicle CPI jumped by 2.0% not annualized in November from October (+27% annualized), seasonally adjusted, the third month-to-month increase in a row (red).

Not seasonally adjusted, the index jumped by 8.5% annualized in November from October (blue).

On a year-over-year basis, the index was down 3.4%, compared to the 10%-plus drops over the summer.

The plunge of used vehicle prices from early 2022 through mid-2024 was a powerful contributor to the cooling of core CPI. But it has ended.

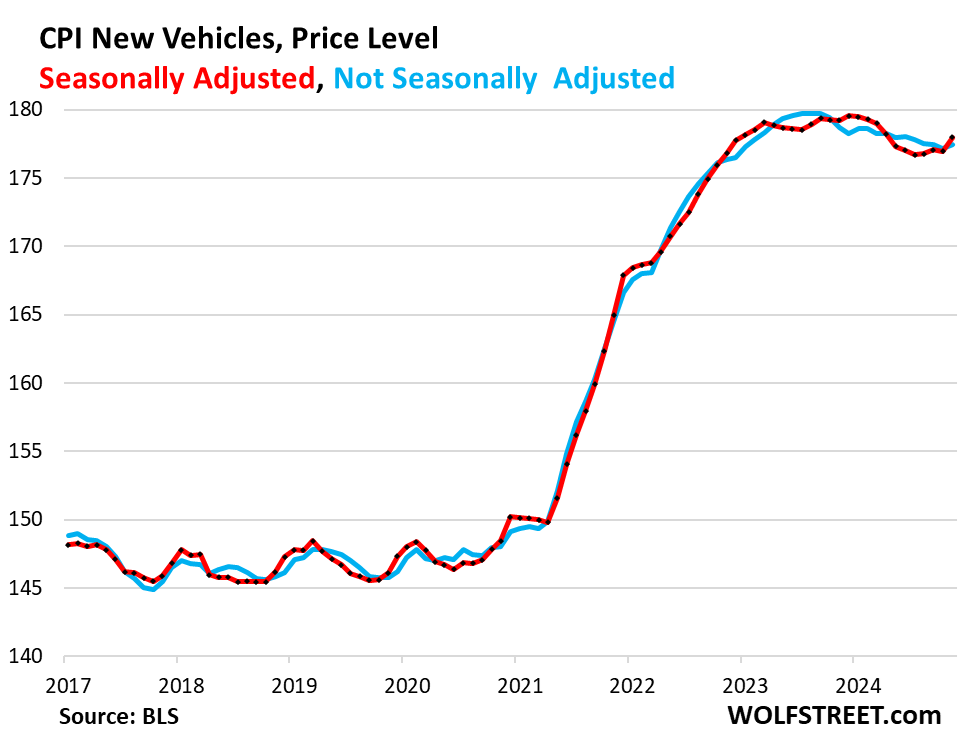

New vehicles CPI jumped by 0.58% not annualized (+7.2% annualized) in November from October, seasonally adjusted, having now increased in three of the past four months (red).

This whittled down the year-over-year drop to just 0.7%. Since January 2020, the index is up 19%.

New-vehicle prices have been sticky after the surge from 2021 through early 2023 and have only given up a little ground since the peak, unlike used-vehicle prices, despite the glut of new vehicles now on many lots. The big incentives and discounts that have been getting thrown around in recent months to move their inventory mostly just undid the big increases in MSRPs of the 2023 and 2024 model years.

| Major durable goods categories | MoM | YoY |

| Durable goods overall | 0.2% | -2.0% |

| New vehicles | 0.6% | -0.7% |

| Used vehicles | 2.0% | -3.4% |

| Information technology (computers, smartphones, etc.) | -2.0% | -7.1% |

| Sporting goods (bicycles, equipment, etc.) | -0.3% | -2.8% |

| Household furnishings (furniture, appliances, floor coverings, tools) | 0.7% | -1.0% |

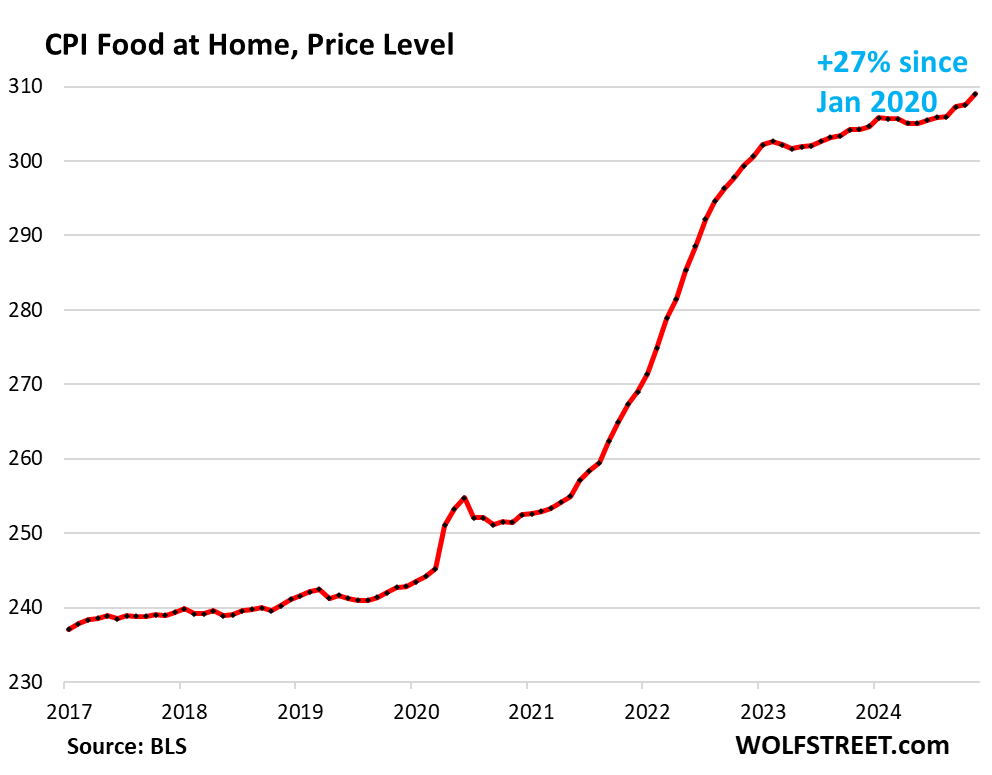

Food Inflation.

The CPI for “Food at home” jumped by 5.8% annualized in November from October (+0.47% not annualized). That’s the second month of the past three months with big increases like this.

This caused the year-over-year rate to rise to +1.6%, the most in a year, on top of the already aggravatingly high prices. The CPI for food at home is up by 27% since January 2020.

Food at home includes food purchased at stores and markets and eaten off premises.

Note how the bird flu outbreak is once again hitting egg prices, up by 37% from a year ago:

| MoM | YoY | |

| Food at home | 0.5% | 1.6% |

| Cereals, breads, bakery products | -1.1% | -0.5% |

| Beef and veal | 3.1% | 5.0% |

| Pork | 1.2% | 1.7% |

| Poultry | -0.5% | 0.4% |

| Fish and seafood | 0.1% | -1.7% |

| Eggs | 8.2% | 37.5% |

| Dairy and related products | 0.1% | 1.2% |

| Fresh fruits | 0.0% | 1.3% |

| Fresh vegetables | 1.0% | 1.6% |

| Juices and nonalcoholic drinks | 1.6% | 3.1% |

| Coffee, tea, etc. | 2.1% | 1.9% |

| Fats and oils | 0.0% | 1.9% |

| Baby food & formula | -0.1% | 1.2% |

| Alcoholic beverages at home | 1.5% | 2.8% |

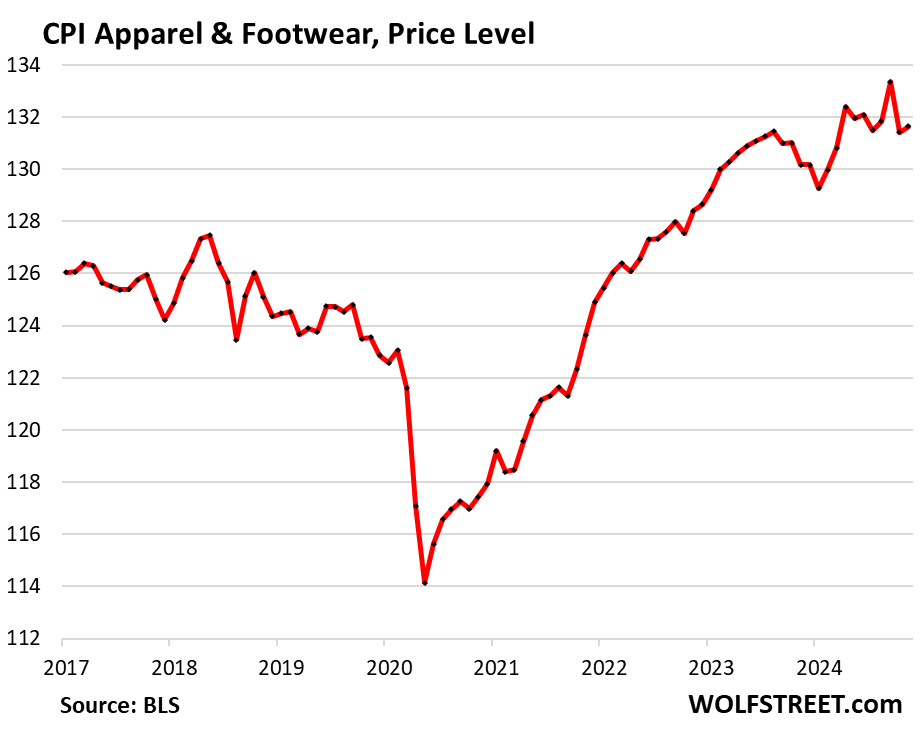

Apparel and footwear.

Month-to-month, the CPI for apparel and footwear ticked up in November from October, and year-over-year was up by 1.1%.

Apparel and footwear are components of nondurable goods, along with food, energy products, household supplies, personal care items, and other stuff.

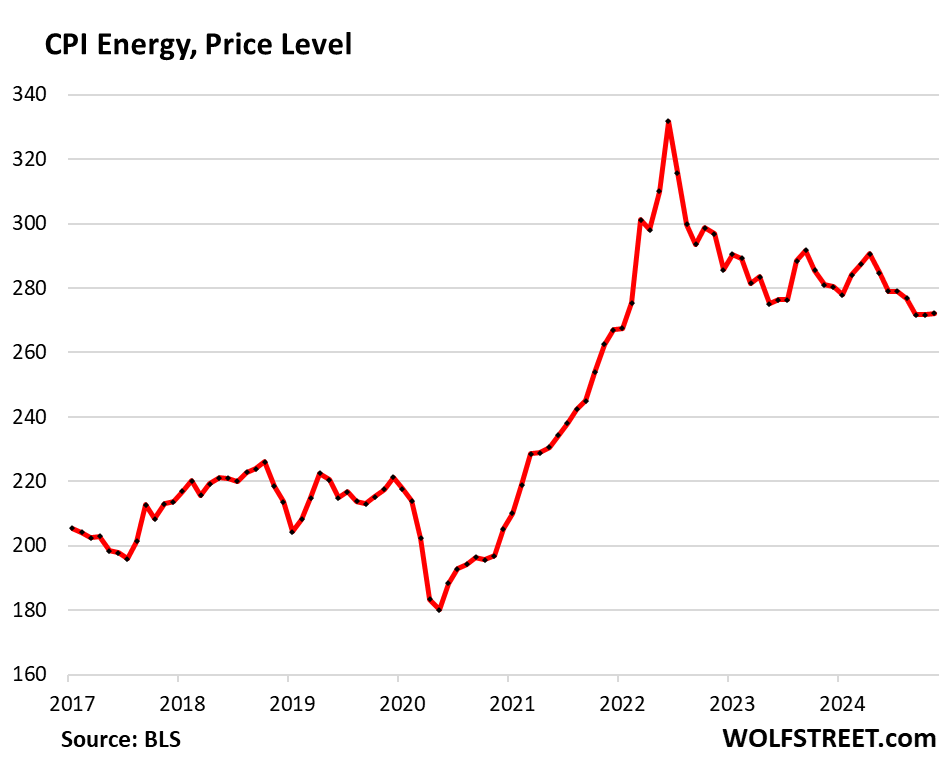

Energy.

The CPI for energy, which covers energy products and services that consumers buy and pay for directly, inched up only a little in November from October, and was down year-over-year. About half of the energy CPI is gasoline, which rose on a month-to-month basis, but was still down 8.1% from a year ago.

| CPI for Energy, by Category | MoM | YoY |

| Overall Energy CPI | 0.2% | -3.2% |

| Gasoline | 0.6% | -8.1% |

| Electricity service | -0.1% | 3.1% |

| Utility natural gas to home | 1.0% | 1.8% |

| Heating oil, propane, kerosene, firewood | 0.4% | -10.7% |

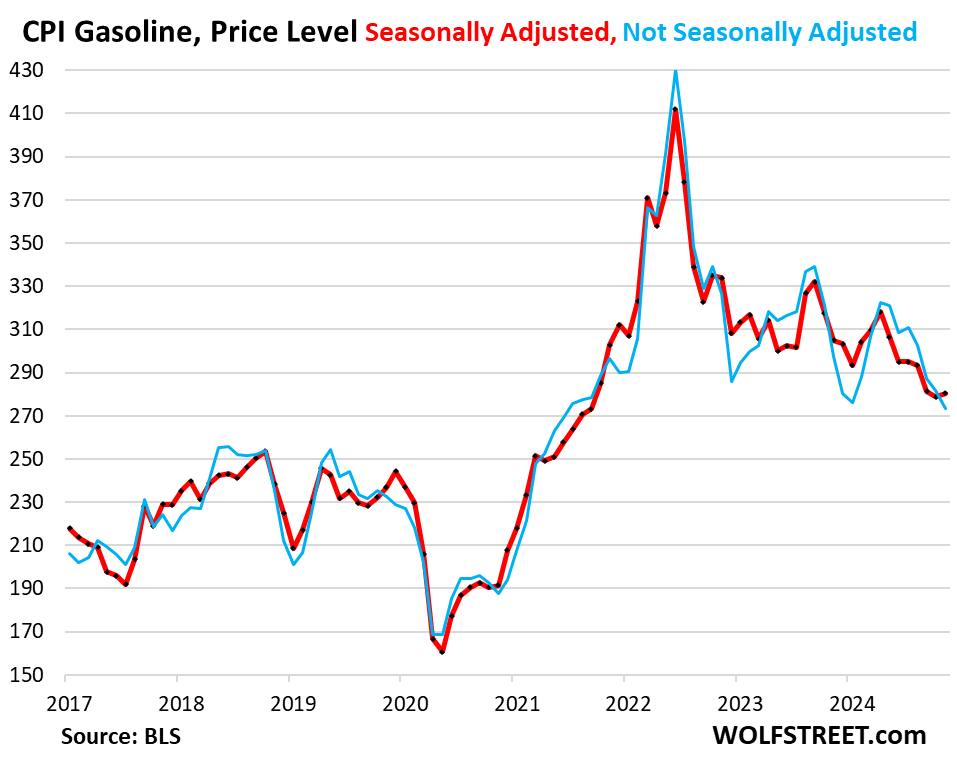

Gasoline prices rose in November from October seasonally adjusted (red), but fell not seasonally adjusted as they nearly always do this time of the year (blue).

Year-over-year, gasoline prices were still down 8.1%. Compared to the peak in the summer of 2021, they were down by 32% (seasonally adjusted).

The plunge in gasoline prices since mid-2022 was a big factor in the deceleration of the overall CPI since then, though now overall CPI has started to rise again:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Inflation doesn’t matter we will melt up get on Elon’s rocket fellas we are going to the mooon 🚀🚀🚀

Mars.

Moon is old hat. I was a kid when folks started traipsing around on the moon. “To the moon” with stocks means taking the Dow back to 800, where it had been in 1969 when folks went to the moon?

Relativity. Who would have thunk it. I suppose Einstein’s theory applies to money and what it is worth. Merry Christmas wolf.

Everything I’m reading is saying 98% chance of a .25 cut next week.

Am I missing something? What in this data suggests that interest rates are too high?

Not much..it is what they anticipate what’s coming.

A replay of history possibly coming our way. In the early 70s, post war Vietnam, inflation was running slightly hot. President Nixon was cajoling Fed chair Arthur Burns to cut interest rates and against his better judgment, he did, as I recall. It wasn’t long before the “great inflation” started and it would take draconian efforts by another fed chairman (Volker) in the 80s to finally get it somewhat under control. We had better hope they do not cut interest rates any time soon. The one thing we will learn from history is we don’t learn anything from history.

Nixon got his ’72 reelection and then, with some lag, oil supply shocks drove inflation deeper and longer. In 2018 or so, Powell was starting to “normalize” to higher rates, hen Trump jawboned him ad that ended. Then with some lag, the pandemic arrived, with supply shocks, federal spending and rate cuts and so on, driving inflation to the surface, to now. All we need now is some kind of shock next year, to see something in that nature happen again. And shocks happen often enough. There may be some self-induced ones (Tariffs? labor supply reduction?)

There were also price controls and other such nonsense that will not be present this time around. So buyer beware.

They’re not looking at the data except interest expense.

Question – is that last 1.0% of inflation from 3.0% to 2.0% all that important to the economy, to the consumer? Is it important enough for the fed to change directions with rates?

Charles Dickens would say “yes”, as would anyone who can only afford 80-99% of their bills as a result of “just 1% more” on top of the ~25% since 2020…

Annual income twenty pounds, annual expenditure nineteen nineteen and six , result happiness.

Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery

Charles Dickens, David Copperfield

BG-

Your depiction is a useful analogy using a household budget.

Here’s a description of the pathology of a “monetary policy” induced system-wide inflation:

“Everyone loves an early inflation. The effects at the beginning of inflation are all good. There is steepened money expansion, rising government spending, increased government budget deficits, booming stock markets, and spectacular general prosperity, all in the midst of temporarily stable prices. Everyone benefits, and no one pays. That is the early part of the cycle. In the later inflation, on the other hand, the effects are all bad. The government may steadily increase the money inflation in order to stave off the latter effects, but the latter effects patiently wait. In the terminal inflation, there is faltering prosperity, tightness of money, falling stock markets, rising taxes, still larger government deficits, and still roaring money expansion, now accompanied by soaring prices and an ineffectiveness of all traditional remedies. Everyone pays and no one benefits. That is the full cycle of every inflation.”

—Jens O. Parsson (pen name of Ronald H. Marcks, 1931-2021), Dying of Money

the terminal part is staved off in the united states for quite a long time due to the reserve currency of the dollar. so it looks like the fed is doing a good job, when it’s really failing miserably.

^That, and the fact that Treasuries consistently yield more than other DM bonds.

“is that last 1.0% of inflation from 3.0% to 2.0% all that important to the economy, to the consumer?”

Yes, very much so.

“Is it important enough for the fed to change directions with rates?”

They shouldn’t have changed directions with rates a few months ago.

They probably should change directions again (with a raise to erase the unnecessary cuts), but whether or not they should, they won’t.

Inflation is legalized theft.

I am a novice on this stuff but just from a common sense perspective it seems wise to wait and see and not cut rates right now. I just dont understand the rush to lower rates with unemployment historically low and inflation starting to go back up from their own professed goal of 2 percent that they never fully reached. The FED is slowly becoming nontrustworthy like the media. IMHO

the rush is that wall street and the government are tied at the tip. as they ask, so shall thy receive.

Must be reading different #s than Wolf is giving us. Makes no sense to cut rates looking at these numbers.

“The FED is slowly becoming nontrustworthy like the media.”

You’re late to the party but still no cops and plenty of booze! Be happy you made it. There’s a LOT of sheep joining the lemmings at the cliff outside.

Glad to see Russell found a good home with Tomlin!

I think the Fed is trying to normalize the yield curve, which remains very flat. Lowering rates on repos and other short duration stuff helps accomplish this.

And the 10 year note today is more than the 10 year note a year ago, so it might be working?

Indeed. The yield curve was totally inverted a year ago.

That said, it was right around 13 months ago that the 10-year touched 5% (before being aggressively bid back down).

The Y/Y CPI is down since June 2022. Lower lows, lower highs. It plunged in one year from 9.1 in June 2022 to 3.0 in June 2023.

Thereafter the downthrust is more moderate, but still lower lows, lower highs. The CPI might cross zero next year. Will the Fed preempt ????

Is technical analysis valid with something like CPI?

Just blowing off steam but its like the FED is one of those psycho parents with Munchausen Syndrome. They are trying to introduce a sickness (inflation) into the economy so they can step in and fix it over and over. Just read the data and apply the gas or brakes as needed.

LMFAO! Nailed it. Perfect. The FED is just as sick as those people.

LOL. Good one !

When you mentioned the word, I remembered NBC ‘The Blacklist’ episode where Mothers are doing that to their kids to gain sympathy.

FED has All the reasons to pause this Month. But as Markets demands through the bogus CME tool, they shall receive.

We can only wish FED will pause this month. If they do, iWall St babies will cry and soil their diapers.

1:04 PM 12/11/2024

Dow 44,148.56 -99.27 -0.22%

S&P 500 6,084.19 49.28 0.82%

Nasdaq 20,034.89 347.65 1.77%

VIX 13.58 -0.60 -4.23%

Gold 2,754.00 35.60 1.31%

Oil 70.29 1.70 2.48%

and tsla up 6% to now trade at a pe of nearly 120.

the fed is failing at its job to protect the currency, and no, i don’t consider the u.s. dollar doing well against other fiat currencies to be a cause for celebration.

Somewhat unrelated to this article, but any colour as to how the tariff threat has blown the spot gold basis to CME futures from circa -$20 to -$60 with liquidity providers refusing to price or making only extremely wide touch spread over a couple of days?

If the delivery of tariffed goods due to physical derivatives expirations are taxed then the liquidity for the underlying spot market will collapse as the spot becomes dislocated to futures.

Gasoline priced may be falling nationwide, but I noticed my “Gas Station from hell” is still posting $4.89 for regular gasoline. Same as last year. They are pocketing the difference in crude prices YOY. Haven’t seen Wolf’s “Gas station from heck” in a long time.

It hasn’t changed much, still above $5. True tourist-trap gas stations from hell with a lot of rental-car offices around it, so people go there to top off the tank of their rental cars. I’m waiting for the day when it’s twice as expensive as the national average. It’s already twice as expensive gas in lots of places.

Just filled up today at 2.23 here in flyover country

All along I-5 in So Cal, about $5. Shop wisely, $4 can be done. The spreads are amazing.

Does google maps show gas prices at petrol stations in the US?

Is GasBuddy still around?

@toby there’s an app called GasBuddy you can use to see lowest prices in your area and also along a route (I think, I haven’t tried that).

The typical difference between fed funds rate and cpi is about 1 percent. Annualized cpi is now 3.8%, fed funds about 4.5%. That’s a difference of .7 percent. Seems the fed is running a loose economy, which is about to get looser.

20 year bond rates jumped today, an indicator showing lack of faith in the fed’s ability to reign in inflation.

why is the 20 year yielding more than the 30 year? seems weird.

I think it has to do with lower liquidity on the 20 year?

Because nobody wants to buy 20 year bonds

What’s even crazier is the 1mo & 30y are only 1bps apart!

I may be talking my book but I think yields on long bonds have a long way to run.

ShortTLT-

Ironically, a rate cut next week could spur inflation fears, resulting in a return to the upward tilt!

Up is down and down is up in a post QE world…

John H,

I agree wholeheartedly. That happened after the last rate cuts – duration actually went UP in yield.

Data point:

“According to the latest Treasury data released today, in November – the second month of fiscal 2025 – the US spent a massive $584.2 billion, a 14% increase from the prior year, and a record for the month of November.”

TNX rate UP despite great auction….maybe the vigilantes are watching Night of the Living Dead….

Night of the Living Fed.

I guess the FED people are still working from home.

If I had been locked in a cave for the last decade or so, once I recovered consciousness after hearing who our president would be (and had been), and I had a few minutes to look at the stats….. I would say “of course the Fed will tighten next week. Duh.”

Core PCE has been expected to increased today to reach 2.97 % for November from Cleveland Fed Reserve Nowcast from 2.94 % the day before. For December it is expected to reach 3.04 % .

Confirmation will be from the PPI Values Thursday Morning as that is used to help calculate the PCE Values.

https://www.clevelandfed.org/indicators-and-data/inflation-nowcasting

In Canada they just pull the figures out of a hat and then use that as an excuse to cut interest rates.

I think Powell needs to get on top this transitory inflation by applying hedonic adjustments to services such as HVAC service calls. He could point to the hedonic adjusted new vehicle the tech drives along with the labor saving use of a smart phone diagnostic app and instruments that were not available 30 years ago just like in the hedonic adjusted car. Avoiding locked rotor start currents with a soft start compressor control board is like going from a carburetor to fuel injection. The Big Mac that the tech had for lunch made by a robot could be useful also. There are 30000 employees at the Fed so getting the brain power to get this done is not a problem. Cable bobble heads can explain it all to you with some newly minted experts to clarify the nuance of hedonic adjusted services. Nasdaq will love it and add a 1000 points while the general public roll their eyes and life goes on. Two things to avoid at a Christmas party are dosing events from a sneezer hovering over the cheese dip and any one armed with government data. Merry Christmas to WS and supporters.

Depth Charge has been right all along. The Fed cannot be trusted. You can’t just give Wall Street what they wanted. If financial media telegraphs a cut, you need to do the opposite to show your independence, or Wall Street will pump the asset value to unimaginable level. I hope there will be consequences for their action and inflation comes back with a vengeance .

This is how we slowly turn the US into a third world country. Inflation props up the stock market allowing the rich to get richer. The poor and middle class that aren’t heavily invested get poorer because everything costs more and the middle class slowly erodes. Long term large wealth divides are incredibly destabilizing for a country and with the cost of college being insane a lot of people who don’t start off in wealthy families with struggle to get ahead. (Yes there are trades – I’m just highlighting the economic path we’re on).

Still the cleanest dirty shirt.

Wolf, I find it interesting that you, and pretty much everything else I’ve read, are focused in on the adjusted numbers, when the reality is that the basket of goods cost less in November, than October (i.e. deflation). I’m not sure what is the adjustment formula, but I imagine it is weighting the annual seasonal component of the deflation that happened at the end of the last two years. The environment during 2022 and 2023 is not the same as now since inflation was rapidly rising prior to the end of those years. To apply those adjustments and yield a positive CPI growth during what could be the first part of a deflationary period is, I believe, a historical bias error. Sometimes a cigar is just a cigar.

1. Seasonality is NOT inflation. That’s the first thing you have to understand about inflation.

2. The annual (YoY) CPI rates are NEVER seasonally adjusted, obviously because seasonality doesn’t apply to year-over-year comparisons. So the yoy CPI rates you see near the top are NOT seasonally adjusted, quoted from the article:

3. Examples:

Gasoline prices, for example, always drop over the winter and surge during driving season in the summer. That’s not deflation and inflation, but seasonality. My gasoline chart gives you BOTH seasonally adjusted (red) and not seasonally adjusted (blue).

Used vehicle prices are very seasonal, rising in tax-refund season and weakening over the summer and fall. This is not inflation and deflation, but seasonal dynamics. My chart shows both, not seasonally adjusted (blue) and seasonally adjusted (red).

New vehicle prices are less seasonal as you can see in the chart I gave you, with both in red and blue.

If you confuse seasonality with inflation, you don’t understand what inflation is.

4. Seasonal adjustment factors do NOT go back only two years. They generally go back five years, but with the pandemic, seasonal adjustments have been tweaked to minimize the impact of that period on the seasonal factors. There is a lot of work that goes into building the seasonal factors, it’s not a simple five-year average.

Another 10%+ inflation in a few years because the Fed is beholden to Wall Street and despises the Working Classes.

“despises the Working Classes”

Where do people get this crap?

Looks like inflation is accelerating again with the recent PPI going up 3%. I noticed the lag time between PPI and CPI getting shorter and shorter. Price increases are noticable in every aspect of your life. Middle class people are noticing a dramatic decrease in their standard of living. I take care of essentials, food, shelter, transportation, health care and then I’m done for the month. If there is anything left over after that I put it into an emergency fund for “Black Swan” events like I’ve had once per years for the past 5 years.

They should say the recent uptick is transitory. What’s the big deal?

MW: Tesla’s stock keeps rising toward another record as valuation tops $1.3 trillion

It seems that prices/inflation aren’t necessarily reacting to fed moves. Instead they’re reacting to projected fed moves. The moment the fed starts cutting inflation rebounds. When the fed sounded hawkish, inflation improved. Perhaps they should stop promising things before they actually have data. Then they could truly be data dependent.

Now that they’ve promised the markets a December cut, it’s unlikely the have the balls to say the data came in bad so we’re not doing that, instead we’ll pause and evaluate again in January.

*the moment the fed starts talking about cutting and projects numerous rate cuts.

Not the moment the fed starts cutting. That was the opposite of my point.

But anyways they should hold here for 3 months to gather data especially with Trump coming in. Because despite the fact that they can turn around and raise rates, they won’t without a year of calling it transitory or an outlier. So better to pause and see what happens with Trump – they can always do another panic .50 cut if needed.