Loosey-goosey financial conditions don’t mean low borrowing costs. They just mean narrow yield spreads.

By Wolf Richter for WOLF STREET.

Measures of “financial conditions” and “financial stress” have loosened dramatically since 2023 and are now nearly as loosey-goosey as they had been during the reckless monetary policy era in 2021, when the Fed’s policy rates were at near 0% and QE still ruled, despite surging inflation.

These measures, such as the Chicago Fed’s National Financial Conditions Index (NFCI) and the St. Louis Fed Financial Stress Index, are in part driven by a basket of “yield spreads,” and yield spreads have narrowed sharply and are very tight, near record tight.

But just because “financial conditions” are near-record loose as yield spreads have narrowed in a mindboggling manner doesn’t mean that corporate borrowing costs are as low as they were in 2021. Far from it.

Corporate borrowing costs – including Commercial Real Estate – are much higher than they had been in 2021. It’s just that credit-market mania has crushed risk premiums, to where investors are demanding only a little extra compensation in form of yield to take on a lot more credit risks.

Here, we’ll look at the junk-rated (higher risk) corporate credit spectrum: leveraged loans and junk bonds.

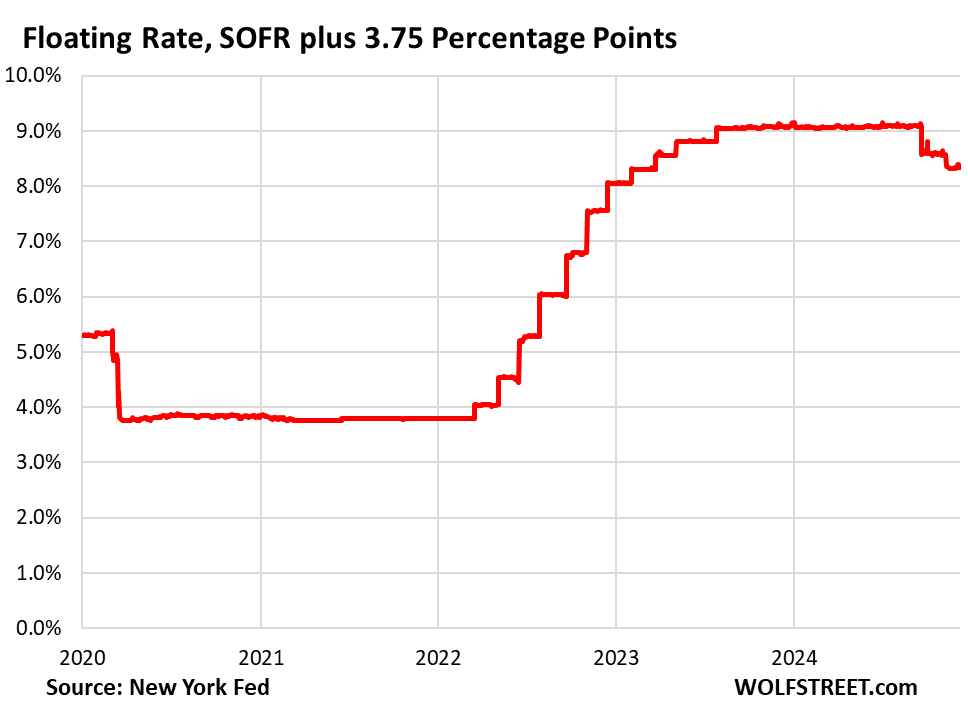

Leveraged loans are mostly floating-rate loans that trade like junk bonds, or are securitized into collateralized loan obligations (CLOs). The floating rate is now based on the Secured Overnight Financing Rate (SOFR), which has replaced LIBOR. SOFR is based on transactions in the Treasury repo market, where yields are close to the Fed’s policy rates.

Most leveraged loans are priced at SOFR plus some percentage points, for example, SOFR plus 3.75 percentage points, such as Cornerstone Generation’s newly issued loan package which S&P rated ‘BB-‘ (our cheat sheet for corporate credit ratings by rating agency).

SOFR on Friday was 4.60%, according to the New York Fed, which calculates and publishes SOFR. That’s right in the middle of the Fed’s five policy rates since the November rate cut, ranging from 4.50% to 4.75%. SOFR plus 3.75% would be 8.35%, compared to about 3.80% in 2021.

When rates get cut – and if they get cut by as much as these borrowers and Wall Street are dreaming about – the interest costs of all existing floating-rate loans are going to drop (which is very different from junk bonds, as we’ll see in a moment). But at the moment, leveraged-loan rates remain high:

Where the “yield spread” comes in is the percentage over SOFR. If financial conditions weren’t as loosey-goosey, the Cornerstone Generation loan package might have been priced at SOFR plus 4.5 percentage points to find investors. But now investors are chasing yield, creating huge demand for higher-risk corporate credits, thereby narrowing the spread between leveraged-loan rates and SOFR.

These ultra-loose financial conditions – allowing Cornerstone to issue leveraged loans rated ‘BB-‘ at a spread of only 3.75 percentage points over a near-risk-free short-term rate – are the reason there has been a massive surge in leveraged-loan issuance in recent months.

Floating rate CRE loans are priced the same way, SOFR-plus, which is why CRE mortgages with floating rates were the first to default because the properties didn’t generate enough cash from rent payments to pay the interest payments that had more than doubled (though landlords could hedge against some of that risk, and many did, but not enough).

SOFR-based floating rates have come down by only about 75 basis points from the peak after the Fed’s 75-basis-points in rate cuts, and remain very high. And now companies with this kind of debt, and landlords with floating-rate mortgages are praying for massive rate cuts by the Fed, which would directly reduce the interest costs of existing floating rate leveraged loans and CRE mortgages.

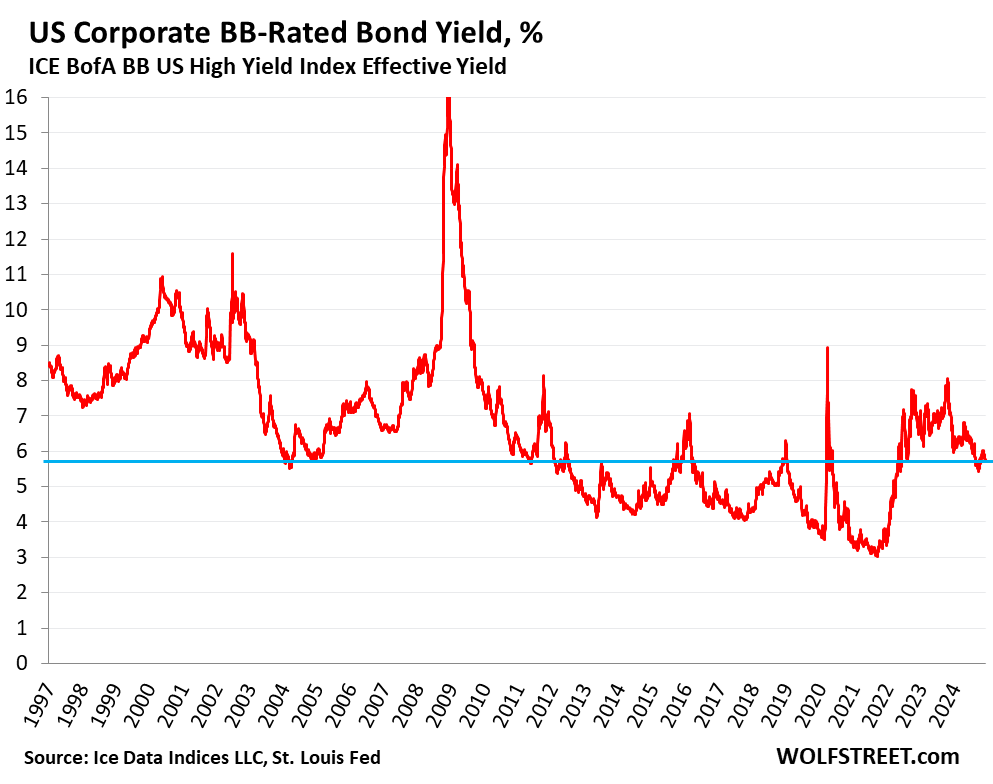

Junk bonds are usually fixed-rate debt. Once borrowers issue the bonds, their interest payments don’t change through maturity of the bond, regardless of what the Fed does or where long-term bond yields go. Issuers have to live with that rate.

At the upper end of the junk bond spectrum, the yield of BB-rated corporate bonds (our cheat sheet for corporate credit ratings) was on average 5.71% at Friday’s close, according to the ICE BofA BB US High Yield Index, up by about 2.7 percentage points from the low in 2021.

So the BB-rated yield has nearly doubled from the low of 2021, but is way down from the top of the spike in October last year, of around 8%.

Junk-bond yields have dropped since October last year, for two reasons: because the long-term Treasury yields have dropped from the peak in October last year; and because the yield spread from junk debt to Treasury debt has narrowed sharply and is now near record lows.

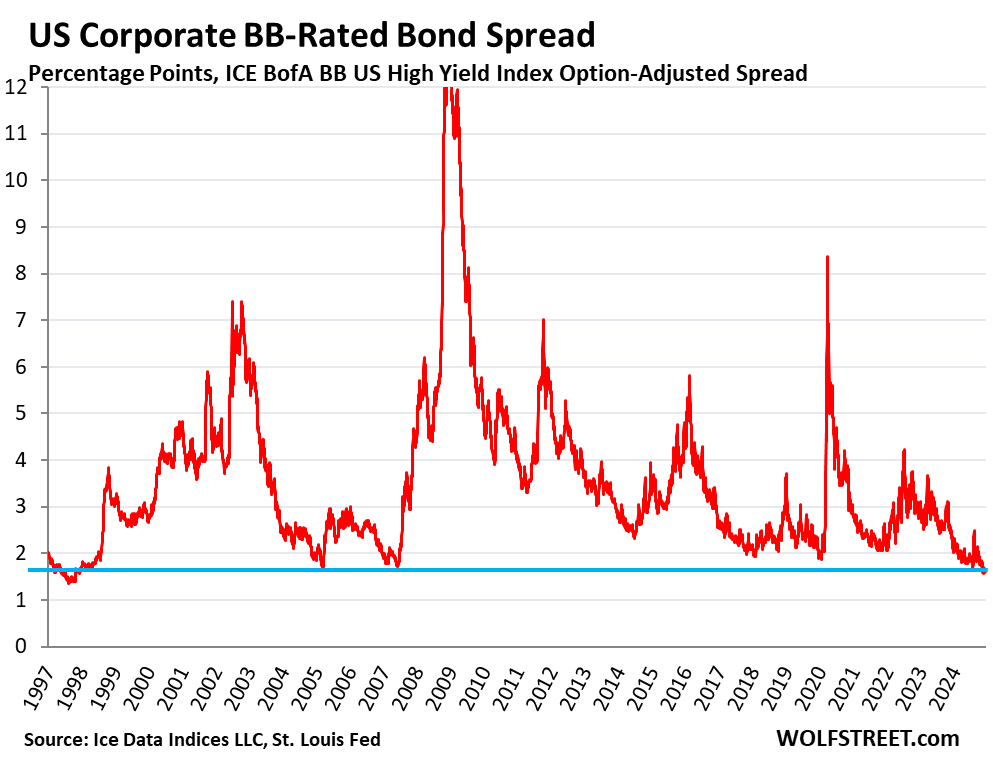

For example, the yield spread of BB-rated junk bonds to Treasury debt with equivalent maturity dropped as low as 1.57 percentage points in November – the narrowest since the late 1990s. On Friday, the yield spread was 1.62 percentage points, according to the ICE BofA BB US High Yield Index Option-Adjusted Spread Index.

Junk bonds have also seen a surge in issuance in recent months amid ravenous demand from investors, and this ravenous demand from investors chasing a little extra yield for a lot more risk is what caused spreads to narrow, and financial conditions to loosen.

These spreads are the signs of a credit-market mania – even though interest rates and yields are still higher, and in terms of floating rate debt, high.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf-

Could you please comment on the term “Repo market blowout” that you have used in the past, and whether that can re-occur?

As you say above “The floating rate is now based on the Secured Overnight Financing Rate (SOFR), which has replaced LIBOR. SOFR is based on transactions in the Treasury repo market.” If SORF spikes as it did then, is the Leveraged Loan market at any significant risk, and what Fed response should we expect.

Or is the plumbing different now?

SOFR covers specific repos in the overall repo market. There were only 2 days — on Sep 17 and 18, 2019 — when SOFR spiked briefly to over 5%. The rest of the time, it was somewhere between 1.6% and 2.3% sometimes a little higher intraday.

Floating rate loans are usually based on some kind of average SOFR rate, so a one-day spike doesn’t make much difference.

The Fed always had a Standing Repo Facility, where banks could engage with the Fed in repo transactions to meet their short-term funding needs. But in 2009, QE flooded the financial system with liquidity, and the Fed shut down the SRF because it wasn’t used anymore. Which it came to regret in the fall of 2019, after QT had drained some of the liquidity back out, and the Fed ended up directly intervening in the repo market to calm it down.

But in July 2021, having learned a lesson from the 2019 episode, the Fed revived the SRF. The fact that the SRF is back likely means that the repo market will remain calm, because when repo yields spike, the banks can borrow via repos at the Fed’s SRF rate and lend to the rest of the repo market at the spiked rates and make a ton of money, which instantly calms down the market. Before 2009, that’s how the Fed had always done it, and there hadn’t been any problems. The Fed seems to be going back to the pre-QE way of doing things.

Thanks, Wolf.

Does the last sentence above, “The Fed seems to be going back to the pre-QE way of doing things.” include going back from an “ample” reserves to a “scarce” reserves regime?

How would this impact Fed balance sheet, which ballooned from under $1T to over $6T now (by way of $9T!) as the old regime changed to the current “ample reserves” regime?

Or is a “scarce reserves” regime gone forever…?

Possibly. But first it has to get back down to “ample.” And QT does that. That’s the announced path it’s on. everything beyond that is speculation.

And so I speculate about a theoretical option — whether or not the Fed will go there is another question, and I don’t have an opinion on that, but I do see it slowly setting up for it:

Once it has “down to ample” under its belt, it can continue to gradually lower the threshold of “ample” with QT while its SRF supplies banks with liquidity as needed. At the same time, it would have to revive its reserve requirement (required reserves, something like 10% or more of a formula of deposits).

This would be a good change. Now the Fed pays interest on reserves (cash on deposit at the Fed). By reducing overall liquidity by going below ample, some banks will manage their day-to-day liquidity needs in other ways, including via the SRF, and then THEY pay interest to the Fed. And a minimum reserve requirement would force banks to keep some liquidity on hand.

That system worked for many decades and dealt successfully with the crises as they came, including 9/11 when markets were shut down altogether.

But note, the balance sheet mathematically cannot drop below the sum of these three liability accounts:

So the Fed would still have a balance sheet of $4.2 trillion at a minimum. But under the ample reserves regime, the Fed would be lucky to get down to $6 trillion (currently $6.9 trillion).

The evolved system you imagine, where “… some banks will manage their day-to-day liquidity needs in other ways, including via the SRF, and then THEY pay interest to the Fed,” and with a substantial reserve requirement, seems like a much more viable method by which to enforce member bank prudence than paying them to hold reserves (to the indirect detriment of the taxpayer).

A smaller Fed footprint seems desirable too, especially when one considers the enabling effect of open market operations on Treasury’s ability to increase federal indebtedness.

Many thanks for your explanations and informed conjectures.

Junk bonds are the dumbest investment anyone can make right now. You can get 5% CDs guaranteed at your local credit union with no risk, and instant liquidity. Who are these morons who are buying these junk bonds?

Creature, agreed wholeheartedly. This (kind of) worries me. It depends on who the morons are. If they are pension funds and target retirement accounts in 401ks, the middle class is in for a ride. I don’t understand why US Treasuries wouldn’t be the #1 choice over these junk bonds. BB- rating versus (practically) risk-free return? Cmon.

Many pension funds and target date retirement funds are restricted to investment-grade bonds, meaning no junk bonds.

Someone is in for a ride, but it isn’t the middle class.

With spreads over impossible-to-default Treasuries (at worst you’ll get repaid in DC Monopoly Money in Weimar America…) at just 1% or 2% above loans to blatantly troubled junk debtors it *is* a massive mystery as to who in the hell is buying that literal junk and *why*.

To drive spreads down so much, you would think it has to be institutions or governments. But why?

Scary to think some institutions are so desperate for yield (to meet their *own* fixed liabilities) that they would take the risk.

Ditto for some government silently/illegally/tactically doing so.

Christ, the world economy has turned in the oldest-established-permanent-floating-crap game.

Per SIFMA, the vast majority of corporate bonds are investment-grade issues. So it’s not like the restrictions to investment-grade issues in some vehicles mean there is some huge pool of junk credit somewhere else. There’s just not that much junk credit to worry about.

Junk bonds are pretty spread out. There are dedicated junk bond funds for advisors to put investors. Junk bonds also show up in a small number of index funds like the iShares Total USD Bond Fund, IUSB. Insurance companies and banks are allowed to buy them, as long as they have adequate capital and they’re a relatively small portion of the portfolio. I imagine shareholder insurance companies are major buyers; they might even be using weird offshore captive reinsurance schemes where ABC Insurance Co. selling annuities in the U.S. reinsures longevity risk to ABC Bermuda Insurance Co. which holds lots of junk bonds. Things like that.

The same people paying 100k for fake coins and NFTs (yes, people still trade them) and the corporate geniuses that were way over FDIC limits at Silly Valley Bank. And that guy that paid a bank for a banana duct taped to a wall. We are in a time of mass hysteria, haven’t you noticed?

Morons? Vast numbers (or at least a few who labor) go out and work in exchange for that toilet paper branded as Federal Reserve Notes. Hell, they don’t even demand a real pay envelope stuffed with “money”, but simply accept electronic chits that aren’t anything of substance. And these people running the game are devaluing those notes at 10% or more annually while setting up this 5% back game! And you can find Morons? Stick your head out the window and look about…you’ll even get an accurate weather report that way. And as far as “risk free”…you’re using up your alloted health and whatever time you have left on this planet to pursue payment in crap crackers and all you end up with is a mouthful of dried green shite (or an electro-representation of this horse pucky). Do you really believe this junk they’re paying with is made for someone other than the “morons” of this country? Jeez, do we need a collapse…and soon.

BuySome. You need to chill out. Working people need a medium of exchange for their labor. FIAT is the grease that makes the economy go round. FIAT money is used to purchase the necessities of life.

Government creates “money” when it decides what they will accept in payment for their fees, fines, taxes, bribes, etc. etc. It does not matter if it is seashells, pretty rocks, tulips, or paper. Money is whatever the government decides is a legal tender.

You seem obsessed with saving. I think we all understand how that has been going. Sorry, I can’t advise on what you need to “save”. This site is packed with people wondering how to speculate on what the government/FRB/Banks will do next (most people will fail). Nothing is risk free.

Wishing you good luck (you’re going to need it).

Old Ghost,

You talk like you own the Soylent Green factory.

People don’t *want* to be paid in evaporating “crap crackers” (nice term, BTW).

Safety and security…purchased through effort…are central to the human condition.

Centrally run, systemic fraud in the monetary system is how governments/nations/civilizations self-destruct.

DC has been saying “Don’t Worry About It” since the early 70’s.

It is long past time to start worrying about it, regardless of the excrement that comes out of politicians’ mouths.

We have not gotten to the point where we will need wheel barrows to carry around our shopping money, but one never knows. In 1956 (when I started to collect stamps for a few years), a first class stamp cost 3 cents. Now, the cost to mail a letter is 73 cents. So we have had lots of inflation over the years. But my standard of living has gone up a lot since 1956. I have not bought any bonds since Meredith Whitney caused a sharp sell off in California muni bonds back in 2010-11. Whitney has faded into obscurity and my last bonds come due in 2018.

Recommended reading: “Wealth War and Wisdom” by Barton Biggs, published in 2008.

2018 should read 2028.

Anon1970 wrote: “We have not gotten to the point where we will need wheel barrows to carry around our shopping money, but one never knows.”

Wheel barrows are old school. We will have plastic cards instead of wheel barrows.

LOL. Do you have any of the preprinted (and sold by the USPO) half cent postcards too ? ? I had a stack of them that I inherited from Dad. I think they had Ben Franklin on them, and were left over from the 1940’s.

Old ghost: I don’t think there will be many credit cards around if US prices are going up at a rate that German prices were increasing in 1923.

Anon1970. I was thinking debit cards, not credit cards.

I should have been more specific. My bad.

A few junk bonds with a better yield in the portfolio I can get behind, but who is investing with such a bad spread?

That was true over the summer, back when you could get ~7% on junk bonds, but not anymore. I have some Backstone & Prospect Capital bonds (technically a notch above junk) bought during that time with 6.5% & 7% YTM respectively.

I’d guess 3-mo brokered CD yields are around 4-4.25% these days.

The Junk Bond ETFs are paying close to 8 – 10 % depending on the fund you are looking at. Floating bod funds have paid closer to 10% the past two years alone.

The “morons” are the unsophisticated contingent of American heroes that worked their entire life for sufficient funds for the late fall and winter of their lives. Reaching for yield by buying into a high yield bond fund that is buying these shit bonds for the next quarter dividend.

Believing that someone could lose money on a bond. The risk free integrity of the currency was trounced when the conservative investors who owned 30 year treasuries lost 45 pct or so when the Ivy league scholars decided that perhaps, ZIRP wasn’t a good idea after all. Some people say, “Who knew Bernanke was a quack.”

Old people want to believe and are targets of the Fed supported credit cartel. A synthetic market in which N – 1 of the variables are controlled.

Clearly the Fed has been recklessly implementing a monetarist experiment into a monetary policy that was unprecedented in recorded history.

Which certainly suggests that the people that ever lived over the past 7800 years or so, were smarter than us.

Federal Home Loan Bank bonds are going for a little over 6%. They aren’t guaranteed by the US gov’t (although they got bailed out during the ’08 debacle). They appear to be safer for those seeking income, more so than junk bonds. They are callable. There are other agencies that have about the same yield.

How are these purchased? Through Fanny and Freddie’s website or a broker? Treasury.direct has made the “T-bill and chill” trade effortless…

Look for agency bonds in your broker’s fixed income section.

Since they’re callable — and they do get called — you may not be able to benefit like you think you can. This call feature causes them to have a higher yield because bond investors hate callable bonds.

The problem with callable bonds is just when you are getting really happy you made the right choice to buy it the bond gets called away.

That’s the conclusion that I arrive at every time I evaluate the government sponsored bond market. The call option makes them too risky.

I’m a fan of FHLB and FFCB bonds, in moderation, due to the state and local tax exemption. However, these will almost certainly get called as interest rates decline. What you’re actually buying is either a very-high-yielding short-duration investment, or a decent-yielding middle-to-long-duration investment, subject to the whims of future market rates. If you need to sell before your bond gets called, you could lose a hefty amount of principal. Hence, my moderation.

I had FHLB and FFCB bonds called recently :( the latter had a juicy 5.98% coupon too

‘However, these will almost certainly get called as interest rates decline. ‘ Quite true.

Now, how positive are you rates are going to decline? I am not all that clear on inflation and rates over the next 5 years…

With spreads narrowing the way they are, doesn’t it also mean there’s a lot of optimism for future rate cuts as well as for increased earnings?

It seems both with be needed to cover future debt service on these loans.

I don’t think people who are buying these are thinking about the future at all lol

But seriously what could go wrong! Haha

Maybe people just think no matter what happens the government will make it rain money and bail everyone out

Investors will come to appreciate junk bonds once again as soon as market conditions change. With Trump in office and technological changes getting absorbed (particularly energy tech) we may be in for a once-in-a-lifetime bull market across the board.

Lol good luck with that… What would you call the last 80 year bull market?

Also appreciate junk bonds again?

The entire point of the article is how junk bonds are basically over appreciated right now to extreme levels hence the tight spreads between them and treasuries… Like I said good luck

No junk bonds for me. Perhaps AAA? I’m not sure.

Wow, awesome post Wolf! You explained the ‘risk’ factor in the NFCI for me really clearly! I had always wondered a bit about what the ‘risk’ factor was comprised of, but I think you got to the heart of it.

Looking at the recent NFCI, you can see that Credit & Leverage have satyed pretty consistant since Feb 2024, but risk has certainly increased. I guess primariy because of the narrowing yield spread you brought up.

Can you illuminate what the ‘adjustments for prevailing macroeconomic conditions’ are in the Adjusted NFCI (ANFCI)?

United health was a 60 cent stock in 1990. It’s been split 32 times and went to a 625.00 dollars while paying their executives millions and shareholders huge dividens

Look it up! Then they deny 32 % of claims.

MW: Federal judge blocks Kroger-Albertsons merger

The Federal Trade Commission sued to block the deal earlier this year, arguing that it would suppress competition and harm workers

My personal feeling is good. It is clearly a move by Kroger to concentrate market power to set prices higher than a competitive market would tolerate.

America has always been a social Democracy with a capitalist open cry micro-economic system as the accepted as the most efficient norm.

The big box culture, trying to monetize the essence of the American culture for free without over sight because excess regulation prevented an even bigger parasite to grow.

I think it’s about time to hear the various public AI models understanding of God.

MW: Investor optimism for U.S. stocks eclipsing 2000’s dot-com bubble raises ‘negative’ shock risk

Well there is nothing like seeing it in black and white to jar one into the milieu of reality from the cozy backdrop we have come to expect.

My parents were children who grew up during the great depression, WW2, atomic energy, the summer of love, etc.

T bill and chill. The thing about bubbles is that, like a hot air balloon, they require fuel otherwise they rapidly deflate.

Excellent article. Thank you.

What’s with all the hate for HY bonds in the comments? You guys know “junk” credit is still higher on a company’s capital structure than equity, right?

How many of you own stock in a company whose bonds you’d “never buy” ??