Quantitative Tightening shed 43% of the assets the Fed had added during pandemic QE. Bank-panic facility BTFP is vanishing.

By Wolf Richter for WOLF STREET.

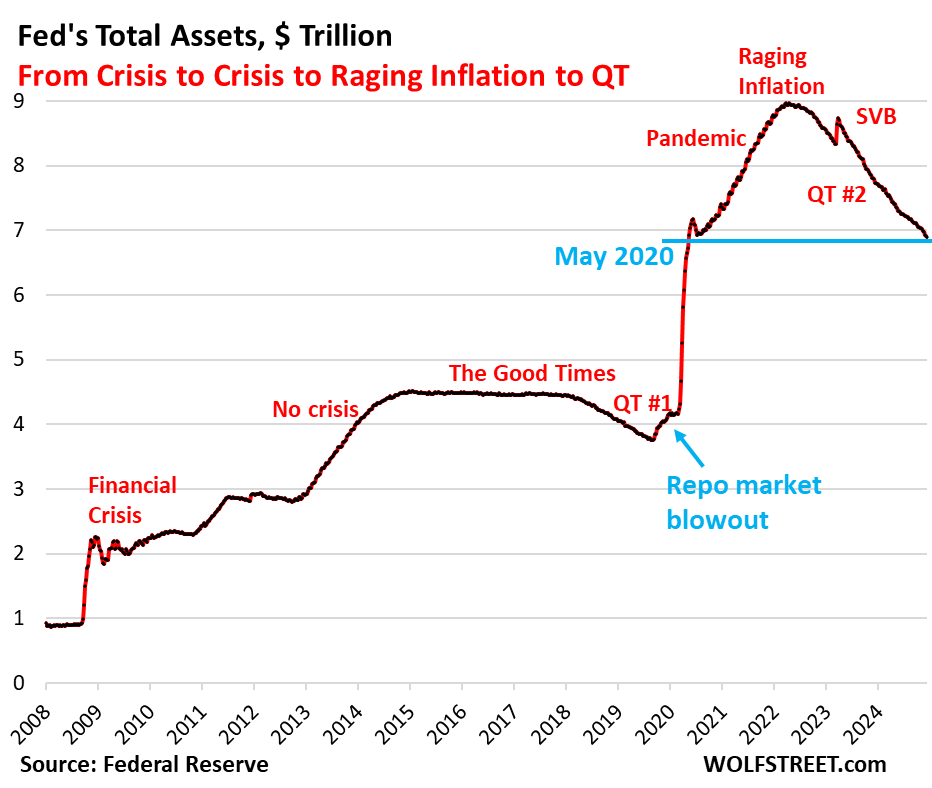

Total assets on the Fed’s balance sheet dropped by $98 billion in November, to $6.896 trillion, the lowest since May 2020, according to the Fed’s weekly balance sheet today.

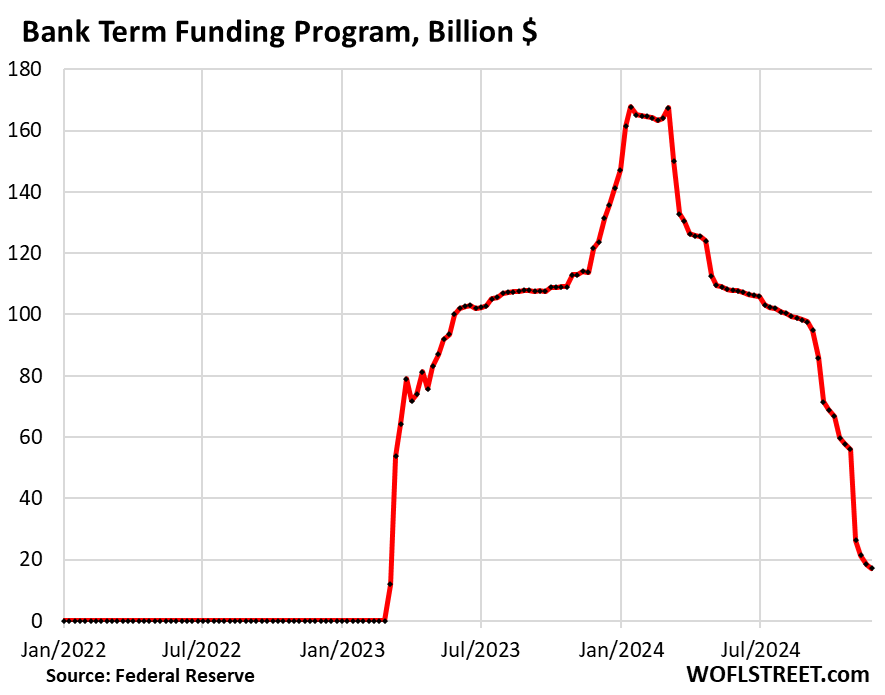

One of the big drivers of the $98 billion drop in November was the bank panic facility BTFP, cobbled together over the weekend in March 2023 to deal with the fallout from the SVB collapse. It dropped by $39 billion in November, is down by 77% from the peak, and will be zero no later than March 11, 2025.

And another QT milestone: Since the end of QE in April 2022, the Fed has shed $2.07 trillion in assets. It amounts to 23% of its holdings at the time. In terms of the assets piled on during pandemic QE, the Fed has now shed 43% of them.

QT assets by category.

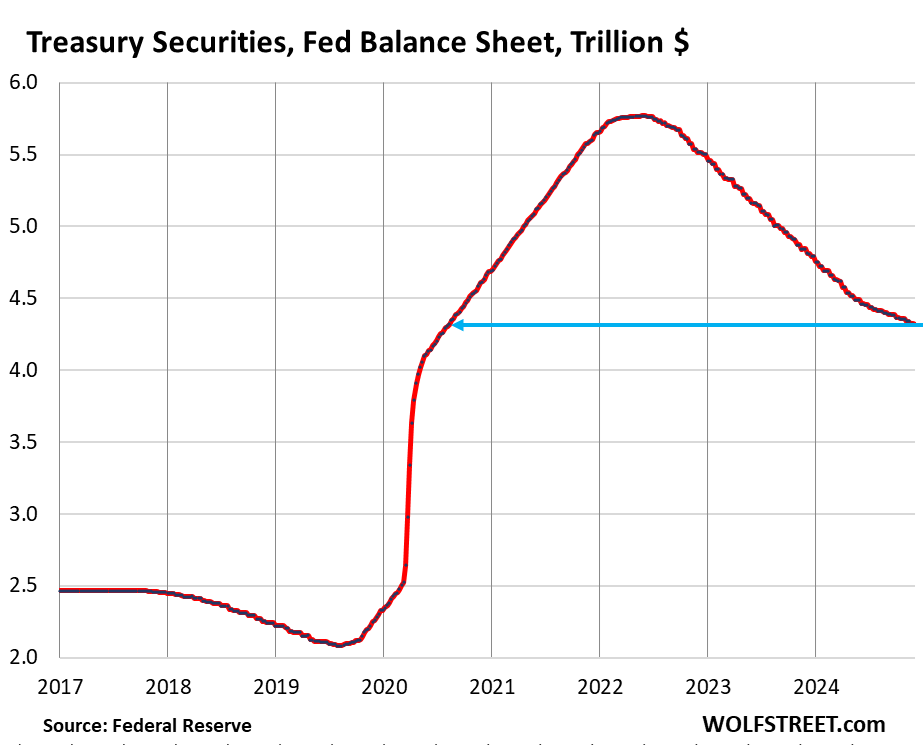

Treasury securities: -$24 billion in November, -$1.46 trillion from peak in June 2022, or -25%, to $4.32 trillion, the lowest since August 2020.

In terms of the $3.27 trillion pile of Treasuries added during pandemic QE, the Fed has now shed 45% of them.

Treasury notes (2- to 10-year) and Treasury bonds (20- & 30-year) “roll off” the balance sheet mid-month and at the end of the month when they mature and the Fed gets paid face value. Since June, the roll-off has been capped at $25 billion per month. About that much rolled off in November, minus the amount of inflation protection the Fed earns on its Treasury Inflation Protected Securities (TIPS) that was added to the principal of the TIPS.

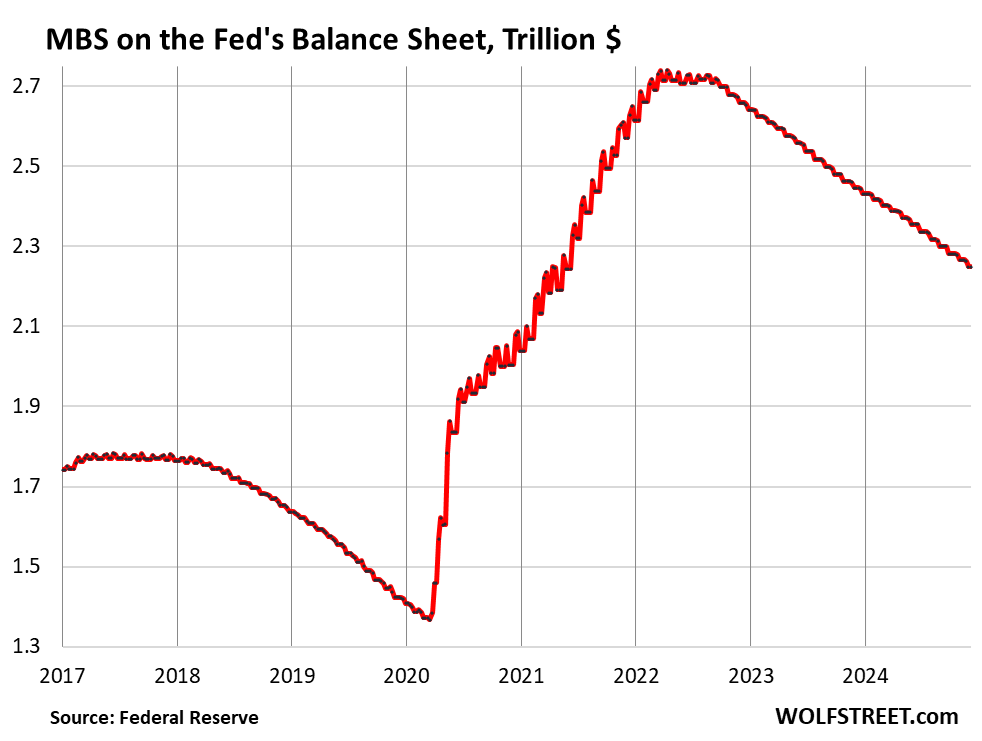

Mortgage-Backed Securities (MBS): -$17 billion in November, -$491 billion from the peak, to $2.25 trillion, the lowest since June 2021. The Fed has shed 36% of the MBS it had added during pandemic QE.

MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when mortgage payments are made. But sales of existing homes have plunged to the lowest since 1995, and mortgage refinancing has collapsed. So fewer mortgages got paid off, and passthrough principal payments to MBS holders, such as the Fed, have been reduced to a trickle. As a result, MBS have come off the balance sheet at a pace that has been below $20 billion in most months.

There has been some discussion at the Fed, including in October by Dallas Fed President Lorie Logan, about outright selling MBS to speed up the process of getting rid of them, and getting rid of all of the MBS even after QT ends, and replacing them with Treasury securities.

The Fed only holds “agency” MBS that are guaranteed by the government, and is therefore not exposed to credit risk if borrowers default on mortgages.

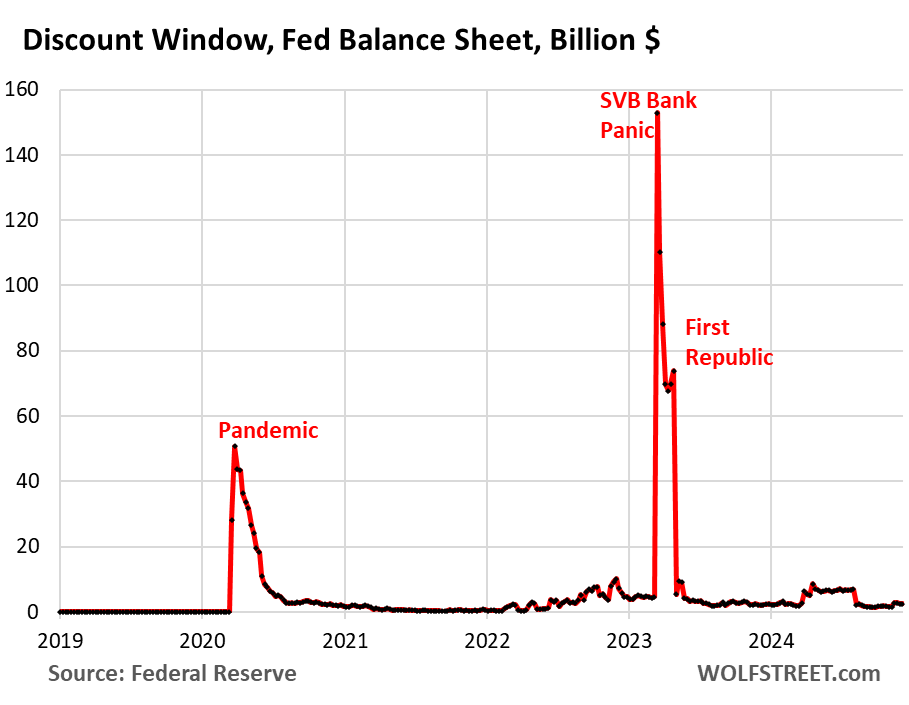

Bank liquidity facilities.

The only two bank liquidity facilities that currently have a balance that’s above zero or near-zero are the Discount Window and the Bank Term Funding Program (BTFP). The other bank liquidity facilities that were heavily used after the SVB collapse are either at zero or near zero:

- Central Bank Liquidity Swaps ($101 million)

- Repos ($7 million)

- Loans to the FDIC ($0).

Bank Term Funding Program (BTFP): -$39 billion in November, to $17 billion, down 77% from the peak ($168 billion).

The BTFP had a fatal flaw when it was conceived in March 2023 after SVB had failed: Its rate was based on a market rate. When Rate-Cut Mania kicked off in November 2023, market rates plunged even as the Fed’s policy rates were unchanged, including the 5.4% the Fed paid banks on reserves. Some banks then used the BTFP for arbitrage profits, borrowing at the BTFP at a lower market rate and leaving the cash in their reserve account at the Fed to earn 5.4%. This arbitrage caused the BTFP balances to spike to $168 billion.

The Fed shut down the arbitrage in January by changing the rate and decided to let the BTFP expire on March 11, 2024. Loans that were taken out before that date can still be carried for a year from when they were taken out. So, no later than March 11, 2025, the BTFP will be zero, removing another $17 billion from the Fed’s balance sheet by then.

Discount Window: +$830 million in November, to $2.4 billion. During the bank panic in March 2023, loans had spiked to $153 billion.

The Discount Window is the Fed’s classic liquidity supply to banks. As of the rate cut on November 7, the Fed charges banks 4.75% in interest on these loans and demands collateral at market value, which is expensive money for banks.

In his battle to remove the stigma attached to borrowing at the Discount Window, Powell has been exhorting banks to use this facility more often, and practice using it with small-value exercise transactions, and to even get set up to use it, and to pre-position collateral so that they can use it when they need to. It’s a bit “clunky” to use, according to Powell.

What else caused total assets on the balance sheet to drop?

The balance sheet declined in total by $98 billion in November. Above, we accounted for about $80 billion:

- Treasury securities: -$24.4 billion

- MBS: -$17 billion

- BTFP: -$39 billion

- Discount Window: +$830 million

And another $16.2 billion came off the balance sheet in November in these two accounts:

“Other assets”: $14.6 billion, mostly accrued interest on its bond holdings that the Fed had set up as a receivable, and that it got paid in November. When it gets paid interest, it destroys that money (the Fed doesn’t have a “cash” account, like companies do; it creates money when it pays for something and destroys money when it gets paid, such as when it gets paid interest).

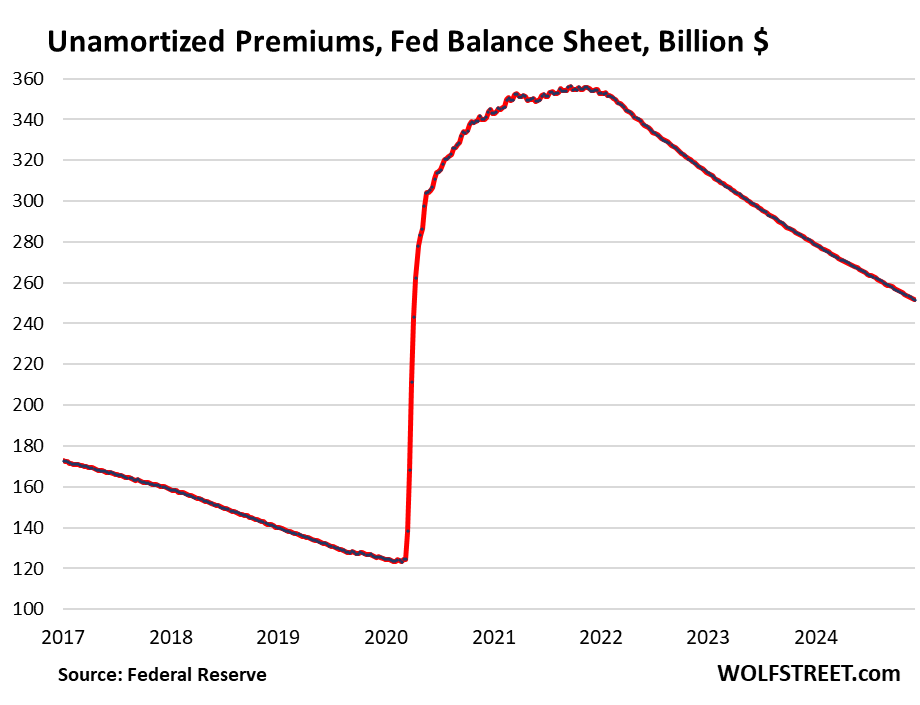

“Unamortized premiums”: $2.2 billion. This is the amount the Fed writes off every month to account for the premium over face value it had to pay for bonds during QE that had been issued with higher coupon interest rates earlier and that had gained value as yields dropped before the Fed bought them. Like all institutional bondholders, the Fed amortize that premium over the life of the bond. The remaining balance of unamortized premiums is now down to $252 billion, from $356 billion at the peak in November 2021:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

However, M2 has risen by about $400 billion in the past year. This may explain why QT is not really biting inflation or the stock market. You would think at some point QT would start to have an impact.

M2 is a nonsense measure. For example, M2 rises by $110,000 if your $110,000 CD matures and the cash goes into your checking account. But if your $50,000 CD matures and the cash goes into your checking account, M2 doesn’t change. There are other screwed-up things in M2. It’s an outdated measure that doesn’t mean anything anymore. Which is why no one outside of the blogosphere uses it anymore. Not even the Fed uses it, though it puts M2 together and releases it as part of its H.6 money-stock measures.

An economy creates and destroys money with the normal ebbs and flows of the economy. A growing profitable economy creates money. That’s natural. That’s not the part you need to worry about. The part you need to worry about is the artificially created QE money that central banks have created by the trillions over the years, and that is now being mopped up.

Wolf, M2 may be unusable, but then what is the best metric to use to get at total money in the US economy? Fed’s balance sheet is only part of the picture no? Don’t you also have to take into account bank lending, TGA, RRP? Is it just too complicated to measure?

And to touch on the motivation of this question – if one subscribes to the quantity theory of money (M*V = P*Q, or more simply future inflation is proportional to money supply), you can base a prediction of inflation off of money supply – hopefully I have that right.

Why is that even a concern? Money creation in a growing economy with growing profitable businesses is normal. It’s not inflationary. It’s just more businesses, more people, more work, more profits, more money. Of course, there can be inflationary sources in that type of economy — such as inflationary shocks, think energy, supply chain problems, government stimulus, etc. — but it’s not this kind of normal money creation from growing profitable economic activity.

The problem is money creation by central bank. This money just comes out of nowhere. That’s inflationary. And we track that right here in this article, first chart at the top.

Surely it should be of some concern? If the money supply is increasing and financial conditions are loosening elsewhere Fed should start thinking about speeding up the pace of the treasury roll off again to the pace it was at before.

Any estimate of when the Fed stops paying the banking system interest on their reserves.

Great article. The Fed balance sheet is still morbidly obese.

Funny money seems too be keeping the spinning dishes air born.

Multiple asset price record highs while the cost of living for the stooges is increasing continuously seems like a dilemma.

given the FED stealing income via suppressed interest rates

I am advocate of auditing FED and ending FED entirely

GOLD STANDARD is OK with me

and making CONgress pay REAL INTERST RATES on debt = balanced budget

“The part you need to worry about is the artificially created QE money that central banks have created by the trillions over the years, and that is now being mopped up.”

But the NFCI continues to show loosening financial conditions. Last week it hit the lowest reading since Oct. 2021. If QT is mopping up the liquitity, why the loosening conditions?

Maybe there’s no corelation, but I guess in my feeble goat mind, I would think there would be?

printed money leads to loose conditions, but the reverse is not necessarily true. loose conditions just means that banks and other parties aren’t demanding high yields to lend money. you can’t force lenders and other liquidity providers to charge higher rates, even if what they’re doing is unwise.

There is no correlation between QT and “financial conditions” or “financial stress” indices. Yields are much higher. There is a correlation between QT and yields. But what happened is that corporate yields also rose, but not as much as Treasury yields, and so the spreads narrowed, including junk spreads. This happened in all kinds of instruments – like corporate credit markets are not really buying into the rise in Treasury yields, in part because there is huge demand for corporate credits. So longer-term yields are higher, but spreads are narrower, which is why “financial conditions” — which track all kinds of spreads and swaps and similar stuff — are looser, though yields are higher.

Thanks Wolf… that explains it well.

Sure does- Thx great thread all

Some brave souls would even suggest that not only is monetary policy not restrictive. It is inflationary.

Which is where we are now. Powell promised the street a December rate cut of 25 bpt. All hell would break loose if he reneges. Fully priced in.

What do I know, nothing.

Powell didn’t “promise” a rate cut at all. Where does this BS come from? Your own twisted imagination?

Thanks Wolf. Always look forward for this update on first Thursday of month.

Good thing is FED is following through what they have been saying for last 2 years. I hope they do in 2025 and beyond too.

By slowing down QT pace, they claimed they wont be be breaking things.

So hope they go far enough by slowing down.

Also we can just hope there wont be any QE with NEW FED Chair in 2026. OTherwise its all over starts again.

There are no guarantees in life. So one cannot rule out the Fed doing QE whenever it feels it needs to. Eg. If stock market crashes or financial system breaks. Remember the Fed is a law into itself. It can not only print money but also justify the printing by saying exactly opposite of what it had said yesterday and all the other mortals can only nod their heads and accept their explanations. Instead of taking them to the back of the woodshed not to return one by one.

This stuff is really funny. The Fed has been shedding assets for two years, and it shed $2 trillion, far more than anyone thought possible, and all you people are doing month after month is fantasizing about QE. We want our QE back. The Fed’s going to do QE again!

I’m getting really sick of this BS, after two years of having to read it here every month.

I think it’s called “Bright Sided”. Read Barbara Ehrenreich’s book on the topic. I’m sorry Wolf but it’s a recurring problem and as long as reader’s want to live in a fantasy world, the press will keep on writing articles for them.

In the meantime, keep up the great work. Another excellent article.

Chase D has hut the nail on the head. Too many confuse fake information sources that tell the consumers what they want to hear with information sources that actually inform.

So many people look to use sources that reinforce their existing views (even if wrong) rather than tell them actual facts that describe reality (and may go against what their consumers believe).

As a result a whole industry has risen that entertain and reinforce their viewers views regardless of the facts. They pretend they are news channels when in reality they are not. It has overtaken investing, politics, and even sports.

I always ask people when the last time a “news” source they use surprises them by giving them information contrary to their thinking and actually changes their thinking. Most people can’t answer it because it never happens.

Use good information sources and get good information. Use poor sources that just reinforce an agenda and you end up getting poor information.

Most of us agree QE was very bad policy & that QT should continue as long as possible,

I’m worried there will be a repeat of 2018 with DJT pressuring Powell to end QT.

QE seems to make the skin crawl and the hairs stand up for many of us.

Which is the basis of the debate

Is the Fed policy correct for every single American or a select few.

I think the Fed policy has minimized the damage their previous fifteen year monetarist experiment caused.

At the current pace of MBS rolloff, is there a projection for how long it’ll take for all of them to be off the balance sheet?

Just what difference would that make? All MBS instruments only involve conforming mortgages whereas nearly all mortgages now in California and other places are non-conforming jumbo mortgages.

That’s an exaggeration. For 2025, the conforming loan limit is $806,500 as a base. In high-cost counties, CCL jumps to $1,209,750. Lots of homes sell under those limits in California. San Diego is a high-cost county, with a median price of $1.01 million. Median price means 50% of the homes sold for less.

The vast majority of the mortgage market is conforming mortgages. How does that not matter?

Nothing positive. They would have to realize the capital loss rather rolling them off at maturity.

The Fed is probably handling the MBS correctly in that regard.

If held consistent at the current rate it would be roughly 2030.

It’s not really reasonable to expect this, but if they run off for at the same rate as they have for the last ~2 years it’ll take ~10 years.

Quick math is – 2.7 and change trillion in September of 2022 compared to just about 2.25 today is a bit over 200,000 billion a year. 2.25 trillion/200 some billion is about 10.

Nice information on the Federal Reserve which is no doubt accurate. What I don’t get is how we now have well more than $100 trillion in US dollar denominated assets in the US and yet have a Federal Reserve with a balance sheet below $7 trillion. What is the ‘monetary base’ for assets in the US to be over $100 trillion and increasing every day and GDP at around $28 trillion a year? What constitutes ‘money’ these days in the US economy and what is being used as ‘money’ to underpin it all?

Look up the definition of “money” in a good dictionary. Turns out it means a lot of things. My Random House Webster’s Unabridged Dictionary has 20 meanings.

Some of the meanings equate “money” with “assets,” such as: “he has a lot of money in his 401k.” And that seems to be what you’re doing.

The Fed with its old “money supply” or “money stock” measures (M1 and M2) is trying to define readily available “money” in a specific way by selecting some accounts that go into it, but excluding other accounts, and splitting accounts by balance (CDs), etc., and what comes out is nonsense.

There are a lot of other conceptual issues with this nebulous concept of “money.” Which is why there is so much confusion around it.

If it’s always a “crisis” it’s never a crisis…..

The feds balance sheet sounds a bit funny, if my balance sheet was 36 trillion in debt…but ok. We can clean the sheets using “Mr clean” and get some rest.

I’ve heard that everything will be ok, we just pay people more money so they won’t care about high prices. Pay no attention to the walrus in the corner, he’s just taking notes.

If the national debt was not 36 trillion and -0- instead, who would care about the fed Balance sheet…nobody would.

All this balancing…. deeper in debt…

The Fed still operates relatively free from political interference, and that’s a good thing. With Trump 47 getting only one more term of office, there’s no real incentive to meddle in 2028 and the Fed can sail through choppy waters like the elegant ship it is.

What a bloated, disgusting abomination.

That describes the entire federal government quite well.

It’s a LOT less bloated than it was. It lost 23% of its weight in two years. That’s quite an accomplishment, as any dieter can tell you.

I lost 15% of my body weight within 3 months after a breakup this past year. Fasted for the brief few days where I could barely eat. Had cut out sugar aside from fruits. Directed my time and attention towards exercise.

The Fed is trying to do similarly but also needs to not suffer from cardiac arrest from exercising too hard. Or fasting to the point of passing out while on a jog (actually walk because the Fed’s balance is too obese to jog). The Fed is obese and needs to cut cut cut. Same with the congressional budget, as you, Wolf, and J. Powell have indicated.

Patience, Depth Charge. I think we’d agree we don’t want a KABOOM…slow and steady wins the race.

Thanks as always Wolf for these updates and your analyses.

Bear, the problem is that people like me and presumably Depth Charge here don’t trust them. If we had say a Volcker at the helm I would keep my mouth shut because I would trust that despite the errors of the past we had a serious person in charge now and were going to do what needed to be done. Powell? LOL. To call the man a wet noodle would be an insult to wet noodles.

Anon,

Volcker destroyed innumerable businesses and careers. I got out of grad school with a masters during the double-dip recession when unemployment was 8% and heading to over 10% and no one was hiring, and companies were going bankrupt left and right. Unemployment stayed above 7% for six years. It took 17 years for the unemployment rate to finally drop below 5%. In the 1980s, I went through five years of hell. Volcker is no hero in my book. People have this romanticized notion of him. He did a huge amount of damage to the economy. It was brutal for people who just started out their careers. I don’t wish that on anyone. And it was brutal for small and even larger business, many of which collapsed because they couldn’t get funding, and their lines of credit were canceled, or got too expensive, etc.

and instead today, they’re destroying the futures of the young and middle class by putting retirement assets and houses out of reach.

is that any better?

Depth would not agree with your assertion that you both don’t want KABOOM….

Depth really wants KABOOM.

He has had a miserable life so he wants everyone else to suffer as well.

I’ve been reading this blog for almost a decade. It was obscene when I started reading – as you very well know because you were reporting on it – and today it is more obscene than it was then. The fact that it’s less obscene than it was during covid when the fed went completely off the rails and implemented the most irresponsible monetary policy in decades is cold comfort. These people should not get any credit whatsoever for half-assedly starting to fix a problem they themselves created. They had to practically be dragged kicking and screaming to this point. I think abomination describes it very well.

Well said @Anon

This is hands down the best article I have ever read about the Fed’s balance sheet. It’s refreshing to read something that’s written by someone who clearly knows what he’s talking about.

Wolf is the only finance blog/person I follow now. The rest of them are all trying to sell you something and/or will always twist the facts to suit some kind of narrative.

Thank you for these. These are the highlight of the month. :)

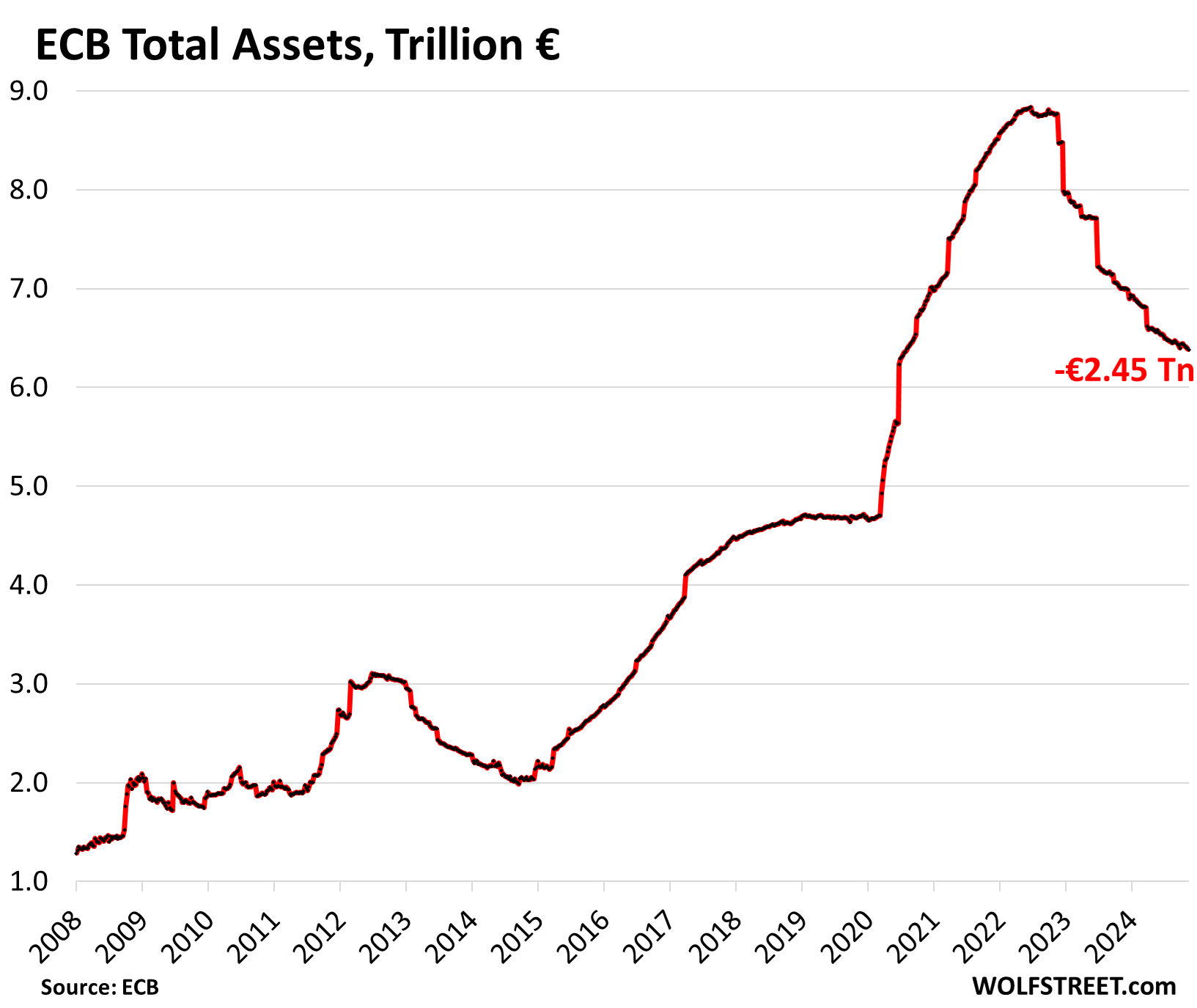

How is it going for ECB and BOJ?

I haven’t done the BOJ’s balance sheet since it started QT. It goes in three-month cycles (down two, up one). So to compare, I have to pick every third month. I might do the balance sheet that comes out in January for December (my classic corner of the three-month cycle).

Here is the ECB:

That chart of MBS should make everyone angry. This financial “product” violated over 100 years of contract law at the time it was created. Banks raked in billions in profits on the way up AND on the way down. In fact the banks involved were pushing MBS onto clients while shorting MBS at the very same time. The banks then sent Hank Paulsen to congress to demand a bailout from the taxpayers. The banks have since lobbied CONgress and changed the laws regarding MBS and “chain of title” laws, and THIS should also infuriate everyone. The system works, so long as there is some actual “rule of law” that all businesses/corporations/people are treat the same under. The former soviet union learned this the hard way in the late 80’s and early 90’s. Events like what we just witnessed in New York were common in the former soviet union, along with people simply being taken into custody, never to be seen again. The point is, the Fed’s balance sheet is evidence of their owners (primary dealer banks) ENABLING BAD BEHAVIOR. None of this changes until K-street is shut down, CONgress balances the damn budget, and we return to the principles laid out in the founding of our CONSTITUTIONAL REPUBLIC.

FYI- Having Elon Musk, a serious benefactor of government spending put in charge of government spending is fucking insane.

I thank Wolf, and others for providing the unbiased data that help me navigate the utter fraud running rampant now and I don’t see how this improves in the short term.

Interesting times, to be sure.

You ain’t seen nothing yet. We’re half way to social / commie dictatorship. The next “crisis” we’ll be all in.

You have moral hazard is embedded in every nook and cranny of the system. You can not fix it without destroying it. It’s too sick. This is all a scam, and when people figure that out, it is going to get very ugly. Unfortunately people being as stupid as they are will blame capitalism even though what we have now is quite literally the opposite.

Re Elon Musk and Trump and all of that, once you understand that you are watching a reality TV show it will make a lot more sense.

Correction, I realize that DOGE has no power and congress controls spending, but my point is simple. Musk has, and has had, numerous lucrative contract with the government, include grants that do not need to be paid back. The only fucking thing Mr. musk should be doing right now is managing his companies and saying “thank you” to all the taxpayers.

This shouldn’t surprise you. Get ready for nepotists and shitty businessmen running the departments we rely on for our health and security, just like last time. No science here, move right along. ‘Merica!

My forward guidance is to include “…Lowest since April 2020” or “…Lowest since May 2020” in the headline for the next 48 quarters.

Sounds reasonable, LOL

The outright selling of MBS must start immediately, and Mrs. Logan is right with her remarks. For now the real estate market is in good shape which means on the other site a good demand by investors for the government guaranteed MBS.

Whether these proceeds should be invested in bills or treasuries is initially irrelevant, important is to unload the MBS from the balance sheet.

This is exactly why people don’t trust the fed. This is clearly the most resilient housing market ever (stocks too) and they are pussyfooting around with rolloff. How do you think they’re going to behave if there is any kind of actual correction? They will go right back to what they did during covid. Hell, during covid they didn’t even wait for the market to crash, they just bailed it out preemptively.

The market did crash massively. there were several days when the S&P 500 crashed by about 10% for that day, and followed by huge bounce the next day. Go look at some of those articles from that time.

right, and within three-five weeks of that, they printed $3 trillion to reverse it.

that’s the reason that every asset right now is in a bubble. the market, rightly or wrongly, believes they will do it again if things get bad again and the bond market seizes up.

“within three-five weeks of that, they printed $3 trillion to…”

It’s this kind of fact-altering manipulative BS, spread by this QE-troll army, to which you seem to belong, that makes “The Fed will soon do QE again” such an exasperating chore here.

It did NOT take “three to five weeks” for the Fed to print $3 trillion.

Starting from the balance sheet as of March 3, released on March 4, 2020 ($4.24 trillion), which was right before the pandemic-QE began, it took the Fed 38 weeks (till Nov 18, 2020) to print $3 trillion.

Even if you go down to $2.9 trillion, it took the Fed 14 weeks to print $2.9 trillion.

In the first 3 weeks, the Fed printed $1 trillion; in the first 5 weeks, the Fed printed $1.8 trillion.

And that happened during a pandemic of the kind that hadn’t occurred in several generations, when the government decided to shut down part of the economy, and flood the economy with stimulus cash to keep businesses and consumers flush with cash as 23 million people lost their jobs essentially overnight. This situation was a multi-generation outlier. And people who spread BS to the effect that the next recession is going to trigger the same response are manipulative QE-trolls. And I’m done with them here. Spread that shit on X. That’s what X is for.

IN ADDITION:

What if the sun doesn’t rise in the morning? I get really tired of this hypothetical BS that I have had to read here for nearly three years: QT doesn’t matter because the Fed is soon going to flip to QE… It’s been nearly three years that QE ended and over 2.5 years that QT started, and $2 trillion later, I’m still getting the same hypothetical BS. It’s exasperating. I have deleted at least 15 of those BS comments on this article. Clearly I haven’t deleted nearly enough. All future comments of this type will be deleted 100%. It’s now turned into a troll mania. And the only way to deal with a troll mania is to squash it, or else it turns the comment section into a receptacle for bullshit. Do you want to join that list?

Her, those bonds rolling off by the Fed are no longer a financial commodity, they don’t exist in the market……buying TIPS isn’t excessive, until it is.

Very good points! Although all of that checkbook money does go into a growing economy (as Wolf says) there are lags as to price effects. In the short run, prices will go up as higher demand from checkbook money gets spent. More demand pushes up prices, which gives a signal to business to increase output. Prices adjusting for changes in supply-demand ought to be considered beneficial, as the resultant higher output should counter the inflation. But it seems that after output increases, prices don’t seem to come down much because prices are “sticky”. Then, these price increases tend to beget other price increases, etc. So bank-created checkbook money (M2) ought to be a concern?

I think I disagree with your idea that money is created by a growing economy. In our economy money growth is a consequence of the growth of credit. Money is borrowed into existence. When credit contracts (loans are repaid, without those proceeds being reloaned) money supply contracts.

As debt rolls off – at least for TBills and Notes, The FED presents the paper to the Treasury for payment of the principal and interest. Simultaneously the Treasury is issuing the equivalent amount of new debt to re fund the old maturing debt.

It seems like the decline of the Feds balance sheet probably means very little – except to make room for a future expansion to meet the next crisis.

1. What you describe — growing credit — is the essential part of a growing profitable economy. There are ONLY TWO TYPES OF CAPITAL to invest: equity capital and debt capital (credit). Economic growth requires continued investment, and profits off those investments. So as the economy grows, credit (debt capital) grows. Simple as that.

2. “Money is borrowed into existence” = LOL. No one, including banks — other than the central bank — can lend money that they don’t have. Banks collapse if they run out of money. Banks have to borrow money (from depositors, markets, etc.) to lend money. Their business model is to borrow short and lend long.

Precisely why all the depression era laws need to be fully reinstated and bank need to go back to being just banks and not gambling houses.

I have always had the same misconception. While I’m open to learning my understanding has been that banks operate under fractional reserve lending. So for a simplistic example with $10M in deposits they can lend out $9M, thus creating $9M. The depositors “have” $10M. The debtors now have $9M, for a total of $19M.

The depositors can’t go grab all that money at once, the definition of a bank run would cause the bank to collapse (It’s a Wonderful Life is in rotation now). If the debtors fail to pay the bank back it would also go under which is why we have the FDIC.

The MBS loans are getting a few years older now. The amount of money going to principal with every payment is going up. 3-4 years does not make a lot of difference at the beginning of a 30 year mortgage, but it surely does make a difference in 15 year mortgages. Even with a 30 year the effect is small but should be noticeable at 4 years.

I keep expecting to see the amount of MBS being retired to gradually increase just a little bit more every month.

Why am I not seeing much of that effect? Is it due to a technicality in the way MBS are packaged?

Wolf,

I am greatly appreciative and eternally grateful for your excellent posts and graphs.

In 2020, from your charts above, the Fed launched QE into hyperdrive for 3 months from Feb 2020 to May 2020 at the start of the pandemic. It increased the Fed assets from under 4T to over 7T. That is over a 3T increase due to QE.

It is wonderful that that the Fed has now decreased the assets from the 9T peak down to around 7T. 2T is not quite halfway.

The pandemic asset increase from QE was 4T to 7T. Will that be reduced? I know that you have posts that it will never be completely reduced.

What happens if there is another dangerous pandemic? Bird Flu, Ebola? The Fed could reverse course and drive the assets up 3T again wiping out the 2T progress and increasing assets by another 1T. History repeats itself.

Am I a pessimist? This asset reduction seems to be on very shaky ground.

I am not waiting for, nor do I think QE is a good idea.

What happens if the sun doesn’t rise???? I get really tired of this hypothetical BS that I have had to read here for nearly three years: QT doesn’t matter because the Fed is soon going to flip to QE… It’s been nearly three years that QE ended and over 2.5 years that QT started, and $2 trillion later, I’m still getting the same hypothetical BS. It’s exasperating. I have deleted at least 15 of those BS comments on this article. Clearly I haven’t deleted nearly enough. Yours was the last one to not get deleted. All future comments of this type will be deleted 100%. It’s now turned into a troll mania. And the only way to deal with a troll mania is to squash it, or else it turns the comment section into a receptacle for bullshit. It’s like someone unleashed the QE troll army on me. Do you want to join that list?

Sorry. :-(

The problem is that you are comparing the balance sheet at various points in time without context.

Two examples of facts that your plain comparison would miss:

The economy has naturally grown between those two periods. A larger economy is going to generally require more currency to be in circulation than a smaller one. Especially when that currency is the cream of the crop and is desired all over the world. Considering that the rest of the world is unstable there is huge demand for dollar bills. An increase in currency in circulation will increase the FED balance sheet. It isn’t inflationary. It just is what it is. A larger economy requires more cash and more people want cash instead of other assets.

The second is that the FED’S balance sheet also includes the government checking account. This literally the amount of money the Federal government has on hand. It is completely outside the control of the FED. Since the economy has grown between those periods that you are comparing, in general it means there is more money flowing through the government’s checking account. Now this amount is highly variable and can be affected by many outside variables. For example, the government collects a lot of money in April (tax season) so it’s checking account swells slightly. Also, if there are things like government shutdowns it’s checking account can drastically dwindle. As a result, it is really hard to compare one particular month to another. Looking at some 3 or 6 month average is probably better. Either way, in general, a bigger economy means more money going through the account.

There are other minor factors that require context when comparing FED balance sheets from different eras but these are probably the biggest (and to be honest, I am not well versed enough to discuss them, Wolf would be a better source).

So right away, when comparing the FED balance sheet amount from two different time periods the first thing you should do is subtract the currency in circulation and the Federal government’s checking account balance from each period. They are beyond the FED’s control and are meaningless and do not add to liquidity.

If you do this, you will find the differences are much smaller that you think. The current balance sheet is still bloated compared to the past, but the difference is smaller.

In other words, even if the FED suddenly dumped all excess liquidity from its balance sheet, it still wouldn’t be able to get as low as the previous balance sheets. It is just too much of a different environment.