Will foreign investors buy the Recklessly Ballooning US Debt? Increasingly crucial question. But yield solves demand problems.

By Wolf Richter for WOLF STREET:

As the recklessly ballooning US Treasury debt is spiraling toward $36.0 trillion, amid fears about its trajectory, investors around the world, from central banks to private investors, are facing a bizarre situation: They might fret about the trajectory of the US Treasury debt, but they like the higher yields, and they loaded up.

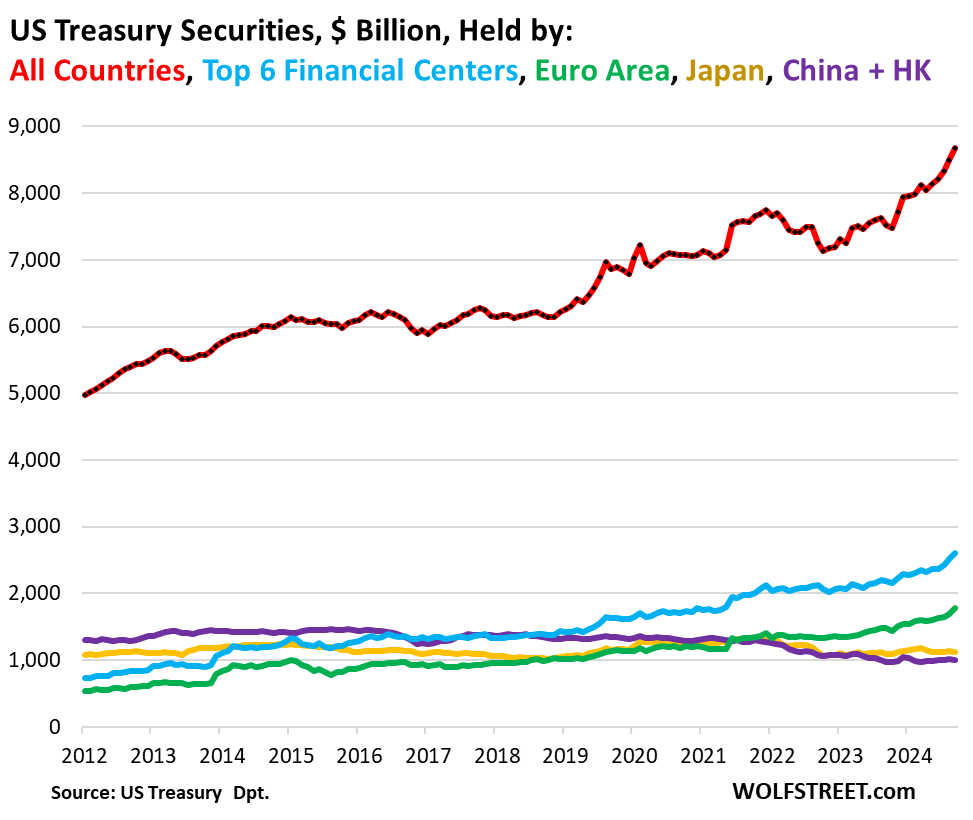

In September, all foreign entities combined (red line in the chart) added $170 billion to their holdings of US Treasury securities – well over half of that increase was by the Euro Area – bringing their holdings to a record $8.67 trillion, according to the Treasury Department today. Over the past 12 months, they increased their holdings by $880 billion, or by 15.4%!

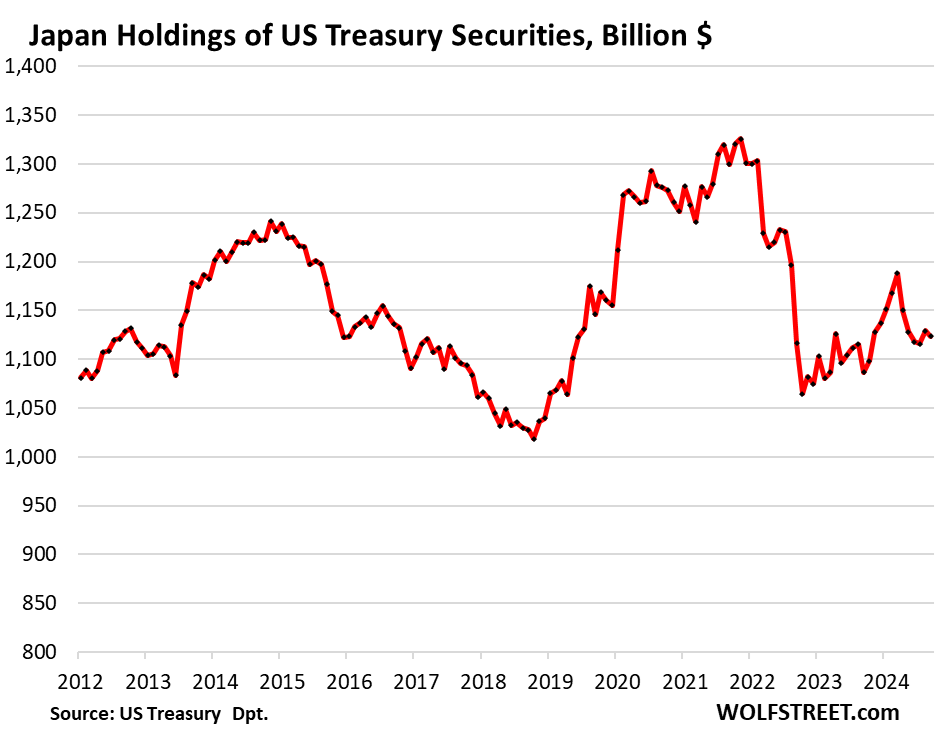

The chart also shows the Top six financial centers ($2.60 trillion in blue: London, Belgium, Luxembourg, Switzerland, Cayman Islands, and Ireland); the Euro Area ($1.78 trillion, green); Japan ($1.12 trillion, gold); and China and Hong Kong combined ($1.0 trillion, purple). It’s no longer Japan and China that the US government is relying on to buy the fruits of its excesses:

Yields of US Treasury securities have remained relatively high – with short-term yields falling only a little and long-term yields, after a drop, surging again, as the Fed has lagged with its rate cuts compared to other central banks in developed economies, and that lag started from higher rates to begin with.

Today, the 10-year Treasury yield is at 4.42%, while the German 10-year yield is at 2.37% and the Japanese 10-year yield is at 1.08%.

The 3-month Treasury yield is at 4.51%, while the German 3-month yield is at 2.77% and the Japanese 3-month yield is at 0.12%.

But inflation rates are similar in those countries. So in comparison to what is out there for foreign investors in their own currencies, US Treasury yields look like a deal.

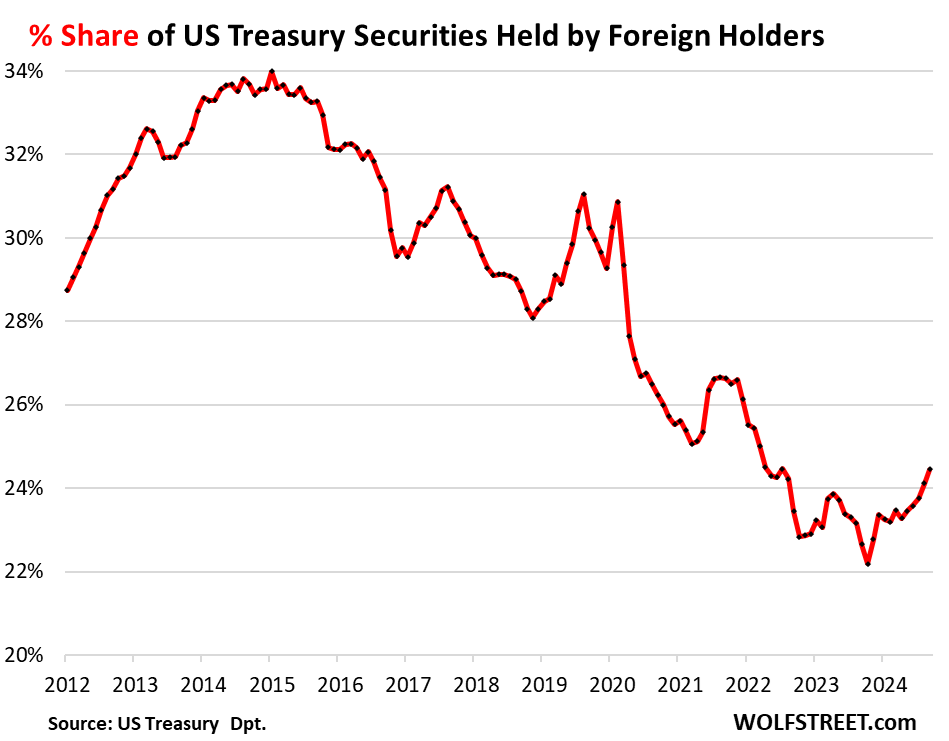

The share of foreign holdings as a percentage of the total Treasury debt U-Turned in October last year from the low point, and has been rising for 11 months to 24.5% in September, the highest since July 2022.

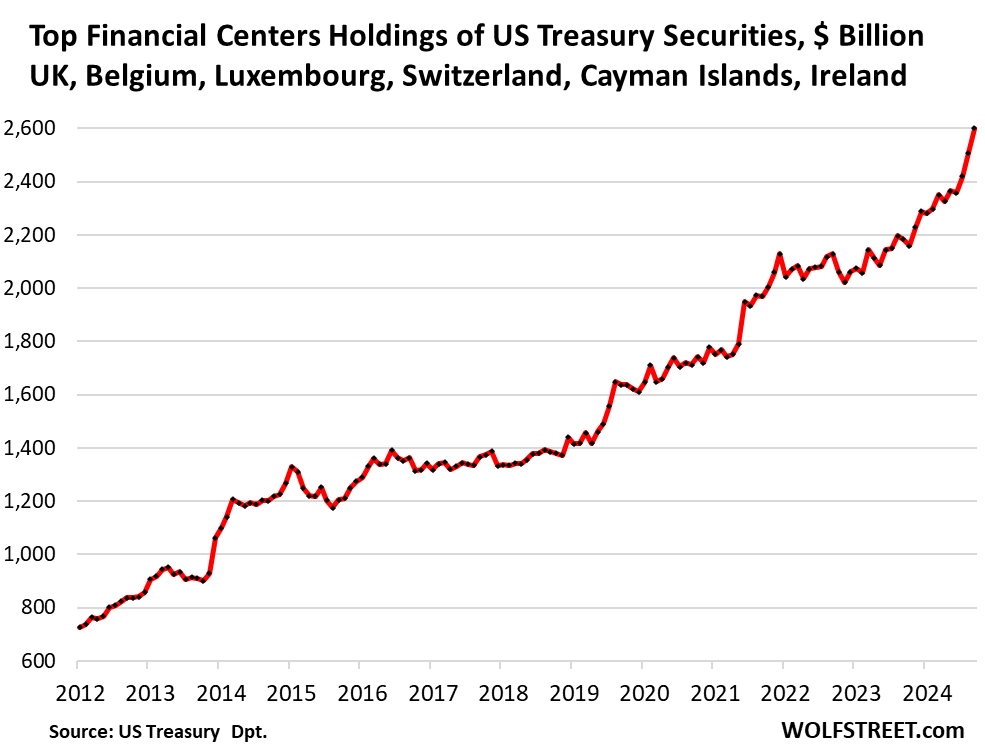

The six largest financial centers added $92 billion in Treasury securities in September (+3.7%) and $312 billion over the past 12 months, to a record $2.60 trillion. Since 2012, their holdings have more than tripled!

These countries specialize in handling the financial holdings of global companies, individuals, and governments. Ireland is a favorite for US mega-corporations to store their profits. So a portion of the holdings at these financial centers are actually held for US entities, and not foreign investors.

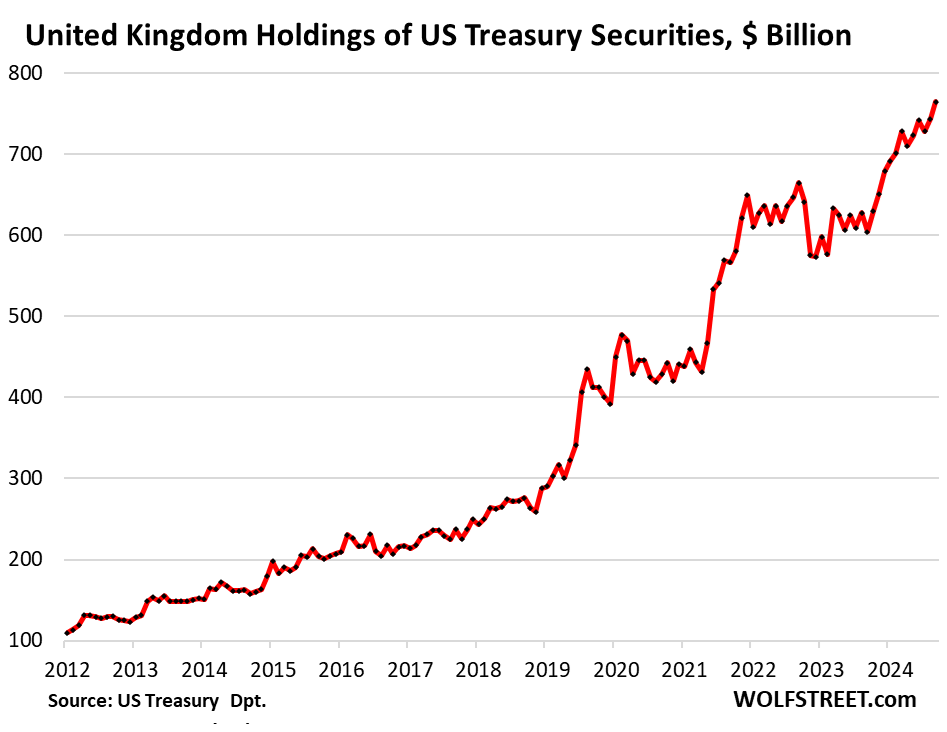

- UK (“City of London” financial center): +2.8% MoM, +26.5% YoY, to $765 billion

- Luxembourg: +3.9% MoM, +11.8% YoY, to $418 billion

- Cayman Islands: +0.1% MoM, +33.4% YoY to $420 billion

- Ireland: +1.8% MoM, +11.3% YoY, to $328 billion

- Belgium (home of Euroclear): +12.8% MoM, +15.6% YoY, to $367 billion

- Switzerland: +2.7% MoM, +8.6% YoY to $304 billion.

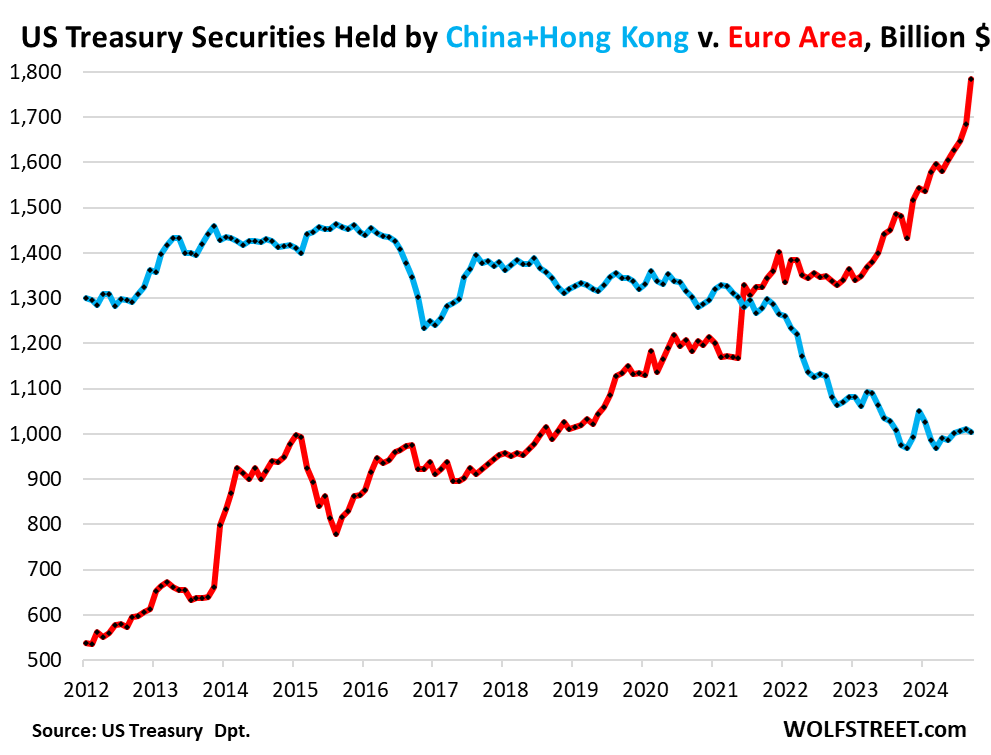

Euro Area v. China + Hong Kong.

In September, China and Hong Kong combined reduced their holdings by 0.5%, to $1.0 trillion. Over the past 12 months, they’ve shed 5.3%. Since the 2015 peak, they’ve shed 31% (blue).

The countries of the Euro Area added $99 billion, or 5.9%, in September and $200 billion, or 20.4%, over the past 12 months. Since 2012, they increased their holdings by 234%, from $534 billion in 2012 to $1.78 trillion in September (red).

There have been reports that China has shifted some of its USD holdings from Treasury securities to US Agency securities due to their slightly higher yields. US Agency debt is not included here.

Japan’s holdings dipped in September by 0.5%, and declined by 5.8% over the past 12 months, to $1.12 trillion.

The Ministry of Finance and the Bank of Japan have been struggling to contain the plunge of the yen. Since early 2022, the yen has lost roughly 30% of its value against the USD because the Bank of Japan has decided that it would do almost nothing – and as late as possible – to tighten monetary policy in face of inflation, which is running at about the same rate as in the US.

The BoJ has hiked policy rates in two tiny baby steps, from -0.1% to 0.25% currently, and that’s kind of the accomplishment for the year. And it started slow-motion QT. The Ministry of Finance intervened in the foreign exchange markets multiple times, selling large amounts of USD holdings to buy yen with it.

Since 2012, Japan’s Treasury holdings jumped up and down and ended up back where they’d started out:

The United Kingdom added $21 billion (+2.8%) in September and $116 billion (+26.5%) over the past 12 months, to bring the pile to $765 billion.

The City of London is one of the top financial centers in the world, and that’s where this is taking place, and so a portion of those securities are held for US clients. The UK is also included in the Top Six Financial Centers above.

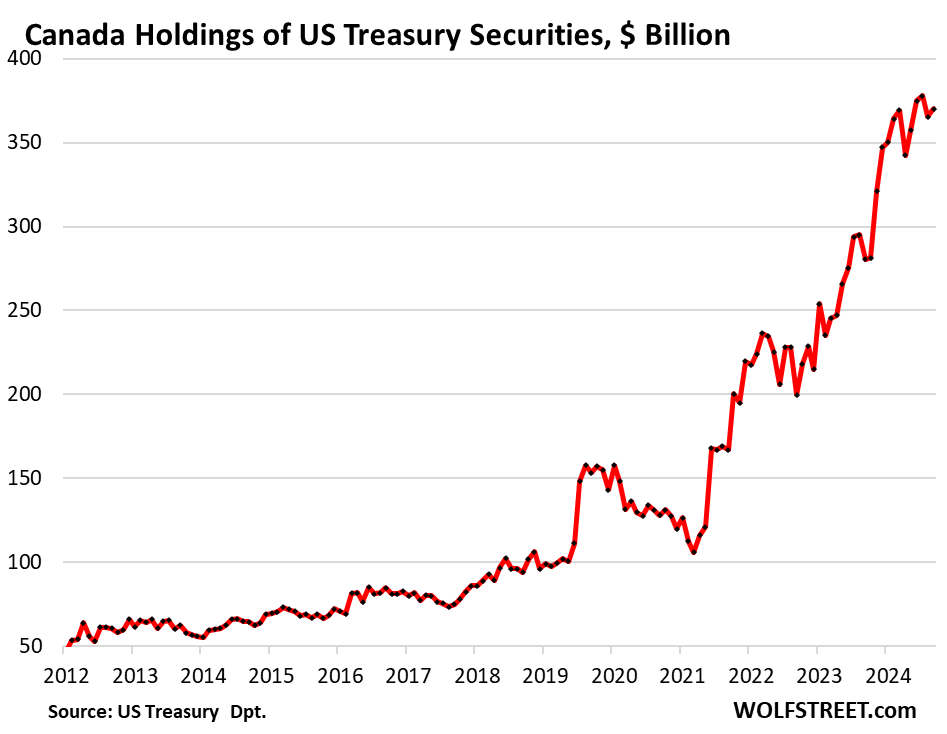

Canada added $4.8 billion (+1.3%) in September and $70 billion (+32%) over the past 12 month to $370 billion. Since March 2021, holdings have more than tripled. Since 2012, holdings have multiplied by a factor of 7!

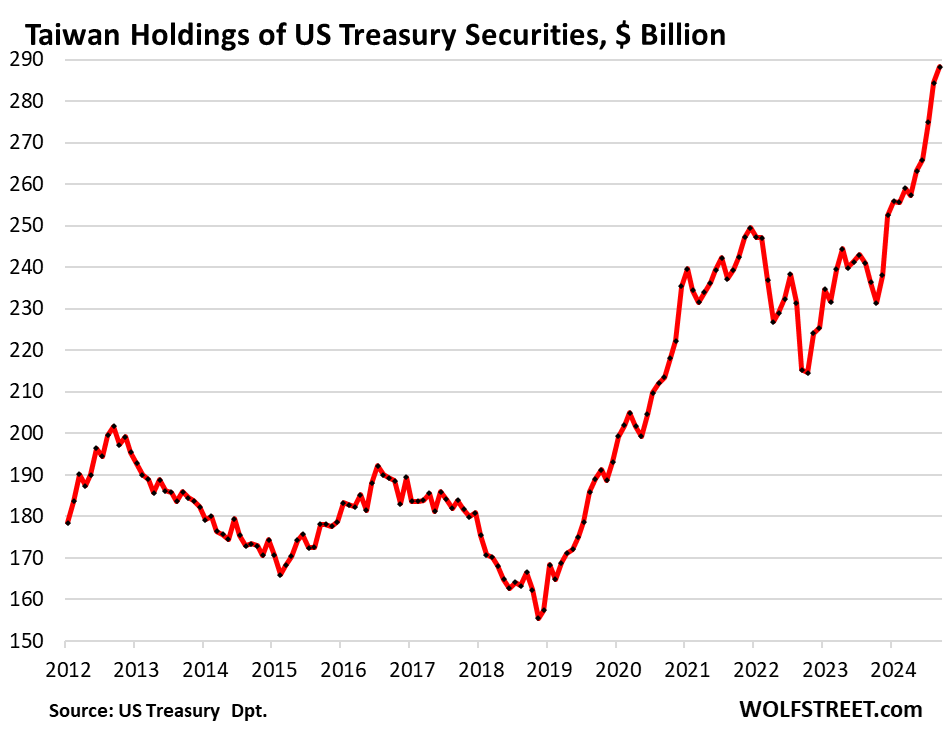

Taiwan: +$3.8 billion (+1.3%) MoM, +$43 billion (+22%) YoY, to $288 billion:

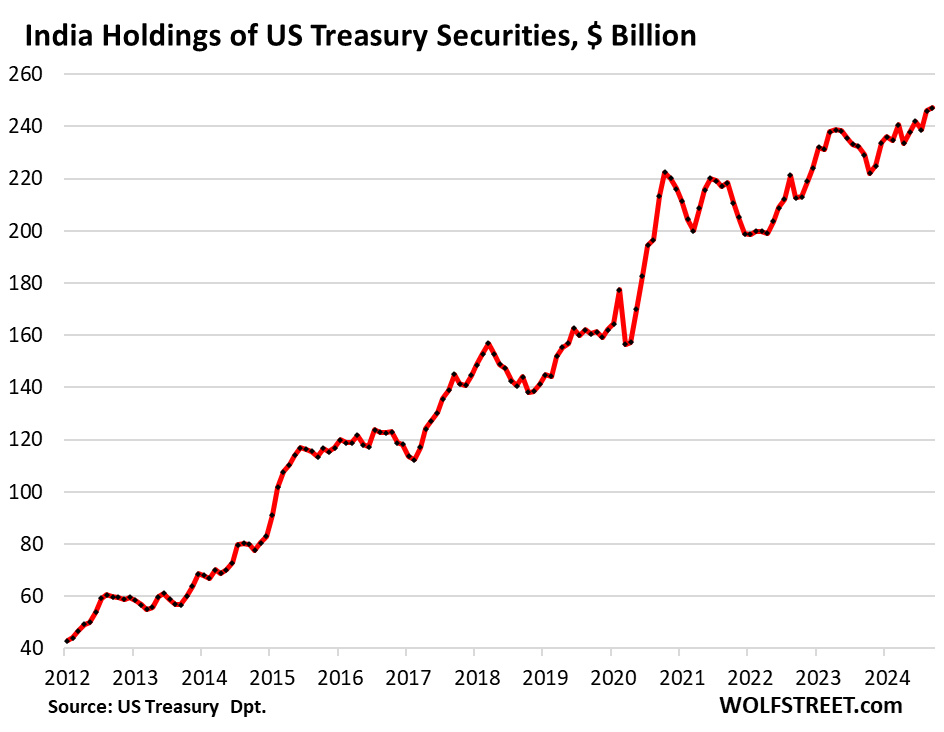

India: +$1.3 billion (+0.5%) MoM, +$13 billion (+8%) YoY, to $247 billion. Since 2012, its holdings have multiplied by a factor of 6:

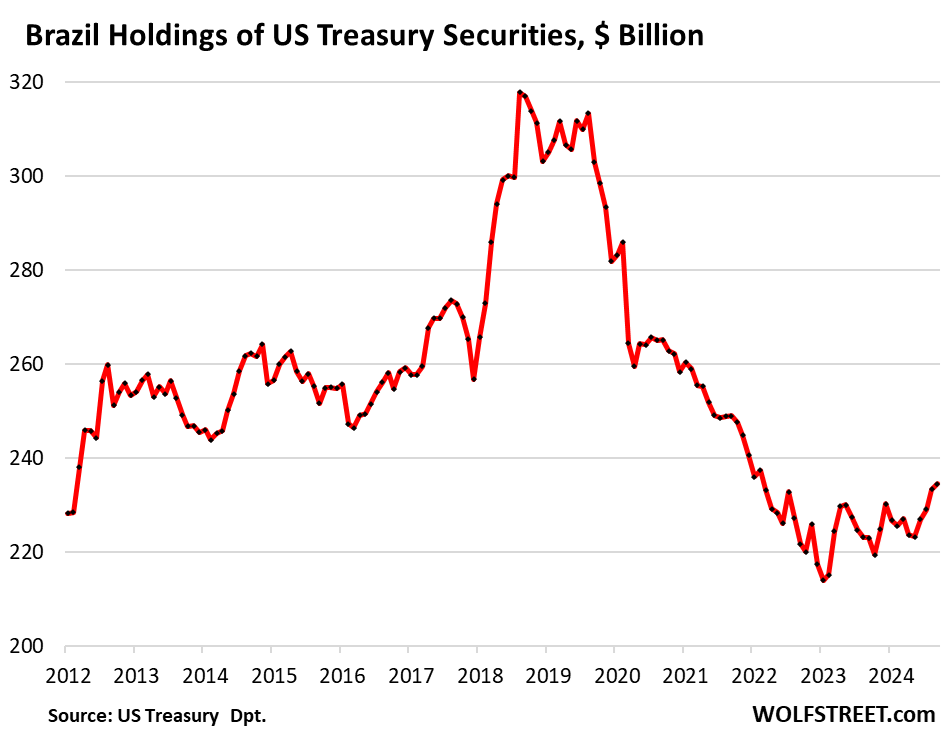

Brazil: +$1.2 billion (+0.5%) MoM, +$10 billion (+5.2%) YoY, to $235 billion, where it had been in 2012.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The Fed has successfully out-hawked the rest of the world and their central banks.

Not sure about out-hawked, but they sure have out-printed the rest of them.

Not according to the dollar index (DXY). The FRN remains the best horse at the glue factory. Unless you are telling us that you would rather hold yuan, yen, rubles, or some other currency…

good luck with that.

And yet the rest of the world has higher inflation and lower bond yields…

Calling Depth Charge …

So financial capitals are the new yield seekers. Either these intermediaries are adding $312B in assets in the last 12 months or they are rotating into treasuries.

These are the kind of things that should scare central bankers. That is how risks get concentrated. Likely a handful of banks with $312B additional US debt in matter of months.

Will Bernanke become a full chapter in financial history? Time will tell :)

It is my opinion that the tail of financialization has been wagging the dog for far too long. Hey Elon you want to balance the budget then pay your fucking taxes to support the society that makes your impossible fortune possible.

Dang-

Are you arguing against the current tax system, with its subsidies and tax preferences, designed to incent taxable entities toward certain activities deemed desirable by DC lawmakers in return for the sheltering of income from taxation?

Or are you suggesting Musk has broken tax laws?

More specificity would help pinpoint the anger and resentment you emote.

Wonder what will happen if Trump takes action to weaken the dollar against these currencies

Well firstly, Trump will not take action.

The wealth inequality is a corruption drug infecting America.

Beauty is in the eye of the beholder. Personally, I mourn the loss of freedom that our ignorance afforded us 30 or 40 years ago.

My mother chastised me for not playing ” who stole the cookie from the cookie from the cookie jar”, a fortnight till the draft.

The Big Wonder is Trump’s much touted ‘Tariffs on Everything’.

The Smoot-Hawley tariffs are universally seen by economists as one cause of The Depression.

Whatever reservations one has about Musk, he is making waves at Florida’s Vatican by questioning the wisdom of tariffs on China, where he has substantial business. This is one policy where the interests of the (real) multi-billionaire and anyone buying a winter coat align.

No tariff is going to create a million American jobs bending over sewing machines for 5 $ an hour.

Nick Kelly,

In terms of your statement on tariffs, what you cited is globalist copy-and-paste propaganda. Obviously, non-Americans have gotten fat off the profits made by these huge trade deficits that the US has, so you would be opposed to ending this gravy train for foreign producers.

Tariffs are tax on the profit margins of foreign producers and US importers. They may or may not be able to pass them on. And tariffs don’t stop trade, but they change the math of where something is produced.

Read that above paragraph over and over again until it sinks in.

The Chinese have used heavy tariffs very successfully in building and protecting their manufacturing industries that now dominate the world. Other countries have too, including Canada.

Tariffs shift the economics to producing more in highly automated plants in the US than producing in factories overseas. This is not instant, but it’s high time that the US protect and build its manufacturing base in order to not be entirely overrun by heavily subsidized and protected manufacturers overseas.

For example, in the auto industry, where a big part of the production takes place in the US — all major foreign automakers manufacture vehicles in the US — importers are unlikely to be able to pass on tariffs. Instead, they’re going to eat the tariffs because if they try to raise prices on imported vehicles, consumers are going to buy a US-produced vehicle for less.

Currently prices are falling in the US because they’ve been jacked up too high and demand is weak if prices rise further. Inventories are piling up. Demand is decent at lower prices. Vehicles is about 20% of retail sales, it’s huge, and good luck trying to pass on tariffs. So tariffs are an effective tax on foreign producers and importers of motor vehicles. Consumers will not pay them, shareholders will. And foreign producers will.

When foreign automakers and US importers get tired of eating the tariffs, they will shift production of vehicles and components to the US — that’s the purpose of tariffs, and it’s working with motor vehicles.

Some items like T-shirts might get more expensive. 60% tariffs on T-shirts might make a T-shirts $0.60 more expensive, so it might cost $10.59 instead of $9.99, if the consumers go for it. That’s = 60% tariff on $1, the price at which the Bangladesh factory sells the T-shirt to the US importer (such as Walmart). Tariffs are imposed on the importer’s cost, not on the retail price in the US. But apparel is only a small part of what the US spends its money on, and it’s not a critical technology.

Thank you, thank you, thank you for explaining this in such an easily consumable form. I’ve felt beaten down, trying to explain and show examples to the constant forwards from friends and family startled by posts about the tariff monster coming our way.

> The Chinese have used heavy tariffs very successfully in building and protecting their manufacturing industries that now dominate the world.

China can do that because they are communist and have a direct vote in public companies. They also disappear owners who might hurt the overall economy for gain. The US can’t compete with central planned economies. China needed houses so they built houses until 90% of the population could afford a house and 20% could afford 2 or more. China will build things that aren’t profitable tomorrow, and they do things cheaper because capitalists can’t oppose them. They essentially built 2-3x NYCs and high speed rail to increase the speed of their businesses with a long term goal of productivity. We can’t compete in the US.

> This is not instant, but it’s high time that the US protect and build its manufacturing base in order to not be entirely overrun by heavily subsidized and protected manufacturers overseas.

We literally can’t win without either taking inflation on the nose or taking the Chinese route of government guided industry. Where are we getting our workers from? Our declining population? Deportations are going to cause worker shortages. The US doesn’t have the work force without automation which doesn’t help the working people. Without some sort of divided ownership of capital, the american people don’t see improvements in their lives.

> because if they try to raise prices on imported vehicles, consumers are going to buy a US-produced vehicle for less.

This assumes American producers won’t simply raise prices against a captive market. We’ve seen this happen with previous tariffs done by Trump on washing machines where US companies simply raised prices because they were the lowest on the market.

> When foreign automakers and US importers get tired of eating the tariffs, they will shift production of vehicles and components to the US

Is this why there are a glut of Chinese automakers making cars in the US? NO! There is no guarantee that foreign automakers will shift production to the US if they don’t already have a large presence. Many foreign automakers are already here but even Ford isn’t 100% domestic. The nuts and bolts are all foreign made, they will still see increases with tariffs until production is brought back with the steel industry.

All of those prices will increase because we don’t have the workers that won’t be taken from other industries that will also suffer and have to raise prices. This is why we have so much discontent in the US and it will get worse under this conditions.

An American,

“This assumes American producers won’t simply raise prices against a captive market.”

NO they can’t unless they’re ok with plunging sales and going out of business. New vehicle sales are down a whole bunch because prices are too high, and now prices are getting cut, and automakers/dealers, if they want to sell, have to lower their prices just to maintain sales at these lower volume levels. And they’re doing it.

Companies have run into the price ceiling. They cannot raise any further without losing sales. Competition is for every customer. And customers are now paying attention.

A buyers’ strike is what you’re seeing. A buyers’ strike is powerful in bringing down too-high prices, and Americans can and did pull that off, so automakers cannot hike prices and get away with it. They can hike prices but their volume will plunge – as we have seen. Or they can cut prices and maintain their volume or gain volume. Tesla cut prices and gained lots of volume at the expense of others. Chart #2 below.

“There is no guarantee that foreign automakers will shift production to the US if they don’t already have a large presence…”

They’re already shifting production of EVs and EV batteries to the US to get the EV incentives, which are a less powerful incentives than the bigger tariffs. Part of the factory construction boom we’re seeing now are EV factories and battery factories. Semiconductor factories are also getting built here. This stuff, especially tariffs, really works in bringing high-value manufacturing to the US. Chart #1 below:

But yes, forget T-shirts. They’re going to be made in Bangladesh, and consumers might have to pay 60 cents more per each, and pay $10.65 instead of $9.99, or Walmart is going to eat that 60 cents, and T-shirts stay at $9.99.

Good food for thought. My thing is, I don’t want to pay more for already-expensive Scotch, and I am not a huge fan of bourbon or rye.

I read what you said, but I feel like the dynamics of this particular scenario may play out differently since we’re never going to be able to make actual Scotch over here. I feel like in that case, they really will just pass the costs on to the consumer.

I’m all about not buying Chinese crap – we should have all stopped voluntarily decades ago – but Scotch…

Also foreign wine and foods. They’re already way overpriced compared to buying locally overseas because someone wants to call them “luxury”?

Thoughts?

I looked up US spending on apparel but the answer according to an outfit called Statistica, is so large I hesitate to quote it. It includes ‘apparel services’…cleaning? A stat area we can all accept: female spending is roughly double male.

However, the outlay on winter clothing, parkas etc, for lower income Midwest family with kids is very substantial. This is why in T’s first term his advisers were able to talk him out of a huge tariff on apparel just before winter.

Re: Bangladesh T shirts. Yes, a whole lot of impoverished places make T shirts , skirts, etc. Apparel includes foot wear, and shoes, work boots, winter boots, are out of their league. So are parkas.

Agree, apparel is not a critical tech.

One thing puzzles me: why more of this work can’t happen in Mexico.

Nick Kelly,

I give the figures for US apparel spending nearly every month, as part of my retail sales, including a chart.

https://wolfstreet.com/2024/10/17/landing-cancelled-retail-sales-jump-prior-months-revised-up-boost-atlanta-fed-gdpnow-to-3-4-inflation-adjusted-gdp-growth/

Retail sales per month:

Total retail: $710 billion

New and used vehicles and parts: $134 billion

Clothing, shoes, accessories: $26 billion = 3.7% of total retail sales

You shouldn’t argue with me about this without having read the data I give you every month.

So if I’m understanding it right, tariffs will not increase prices because all they’re doing is effectively adding to the “production” cost of foreign products and bringing their cost up to parity with US products? With the difference being that the money goes to the government instead of US workers directly?

That seems to open up a lot of questions, depending on where the revenue goes and what effect it has on domestic producer pricing power, as well as the potential for some kind of reverse China Shock because of the lag time. So many ways that could play out.

I guess there’s also the question that if the goal is to strategically force producers to re-shore our industries, aren’t tariffs intended to do that *by* increasing end consumer prices up to parity with domestics to incentivize consumers to buy here?

Looks like construction for manufacturing during Trump 1 was flat and during Biden might be due to his infrastructure give away.

This chart covers only factory construction (manufacturing plants), not infrastructure. There would be a separate chart for infrastructure.

But yes, the surge is in part due to the incentives by the Biden administration to manufacture in the US, including the EV rebates that have production location requirements of the vehicles and batteries, and the CHIPS Act though the first monies may still not have been handed out (Intel, the biggest grant recipient, said in its earnings call recently that it still hasn’t been sent the actual funds). But they’re building chips plants in anticipation of getting the funds eventually.

The surge is also due to the supply-chain chaos during the pandemic, after which lots of companies decided to produce in the US. So the factory construction boom extends to products and components for which there are no incentives. This factory construction boom is a pretty big deal long-term. And I’m glad to see it.

‘And tariffs don’t stop trade, but they change the math of where something is produced.’

Agree. The point of a tariff is to encourage domestic industry. So what level of tariff results in the formation of a significant US apparel industry? I don’t think a hundred percent even begins it.

Somewhere further down the column I seem to be accused of arguing that apparel is expensive. Not so. I didn’t quote Statistica’s 1600 a year because I don’t see how that can be. My argument for which I’ll take heat is that apparel is so cheap it is not practical to make it in the richest country.

I’m a China hawk. By all means prevent tech transfer. Physically confront them in the South China sea, when they ram Philippine fishing vessels. No shooting needed, I think the US still has a mobile battleship.

Nick Kelly

You keep barking up the wrong tree. Apparel doesn’t matter. I told you. It’s not a key technology. It’s not a big part of US spending. Importers and consumers might have to pay a few cents more per T-shirt. And foreign producers might get a few cents less per T-shirt. The US needs to collect taxes, and collecting taxes from foreign producers, importers, and consumers is one of the goals of tariffs, better than collecting more taxes on US income.

Motor vehicles, semiconductors, components of all kinds, products NOT sold to consumers such as industrial equipment, industrial robots, big computers, utility-scale solar panels, oil and gas drilling equipment, mining equipment, ultimately shipbuilding, steel towers for suspension bridges (the new tower of the SF Bay Bridge was made in China because no one could make it anymore in the US because China had taken over that business because the US had failed to protect it), etc. those a key technologies whose production needs to be protected in the US, and needs to return to the US, including for strategic reasons.

And that is starting to happen. And additional tariffs will help that process further. But it takes a long time to rebuild the manufacturing capacity and the infrastructure and knowhow to do it. The US got run over by Corporate America’s love for cheap labor and China, and it’s time to reverse course.

Smoot Hawley was passed in response to other countries imposing tariffs. At the time the US

was the largest exporter. Now the

US was the largest importer. Different circumstances.

@NR: Same here. Especially as it is one of his stated goals, for whatever that is worth.

Foreign Investors are usually a contrary indicator. What ever they are buying is a good candidate for a short sale. I’m sticking with short term (less than 1 year).

Same, <=1 year. I'm seeing this story in the US news too: "Investors flock to long-term bonds."

"'There is a general acknowledgment that growth is strong, inflation is not completely slain, that budget deficits likely widen and that there is little reason for the long end to go down,' said Michael Contopoulos, head of fixed-income at Richard Bernstein Advisors LLC."

Alright but what about duration risk? I'm no expert but I feel like if we actually follow through on Trumponomics these people are going to be way underwater at 4.5%.

I also just keep wondering, given the debt and all, how much closer we are to some kind of deficit spiral now than in the past. Is my understanding right in that the situation we were just in, with the high growth and high inflation of an overheated economy, it's easier to control it via Fed rates than a low-growth, high inflation economy? In the latter case it would seem like market confidence is a much more significant factor in especially long-term rates than Fed policy is, and it's much less controllable.

I know Wolf has talked before about interest costs as a % of revenue, but it might be a lot more important now. Is there a scenario where the debt reaches a point that a recession could push that ratio high enough, and bond market confidence low enough, that it kicks off a feedback effect?

Matt B

the problem is that the future is unknown. I don’t think the Fed or anyone else knows how this will play out.

While inflation is likely so is deflation. With debt levels where they are deflation cannot be ruled out either.

One this is sure that there are too many imbalances built up and they can blow up. Whether they will or will diffuse quietly, only time will tell.

I have spent countless hours thinking about this and have concluded that this cannot be figured out. The best option is to play the game prudently and hope like hell that all works out.

I know I didn’t add much to your comment.

Aman

“I have spent countless hours thinking about this and have concluded that this cannot be figured out. The best option is to play the game prudently and hope like hell that all works out.”

Now that’s an honest statement………………and I feel your pain.

We all struggle to understand the game when the perceived rules we were following change. May we all find a better day, with smaller government, no market interference, and a stable money supply.

Until then, rejoice in the scraps that fall from their table.

“If we actually follow through on Trumponomics….” That’s the catch. Trump, whether you agree or disagree with any particular policy, doesn’t really follow through on anything. So, if you hate Trump, that’s your salvation. If you agree with Trump or want him to do something, it’s frustrating.

Trade War 1 with China? Ended when they agreed to buy a few soybeans, which they never followed through on. Wall with Mexico? Built a few miles and then lost interest. Agreement with North Korea? Not sure there was any content. Infrastructure Week? Still waiting for it. The list goes on… And remember, he had 2 years with a Republican House and Senate the first term, so the opposition party can’t be blamed for any of these things.

I do hope there is more decoupling from China, whether it is tariffs or technology limitations like Biden did, because the US doesn’t get anything out of the relationship except cheap consumer products on Amazon. And, if decoupling happens, it will be inflationary. But I’m not holding my breath that there will be any follow through. Hopefully, I’ll be wrong.

That being said, even without any decisive policy by Trump, I still agree with your conclusion: “people are going to be way underwater at 4.5%.”

‘doesn’t get anything out of the relationship except cheap consumer products’

What do you want, expensive products?

If you are implying by ‘cheap’ that the products are substandard this is not true in apparel, the second largest category of imports from China. Of course with so many US cos and others manufacturing there, there will be lower quality stuff in the budget range. One that isn’t, is the one I’m looking at, Pronto-Uomo.

I’m not a China fan or booster. I support selective controls on tech transfer etc. As far as Taiwan goes, I’d like to see the US codify into treaty its spoken resolve to defend Taiwan, just as it has with Philippines.

Big Bird

I also agree that “people are going to be way underwater at 4.5%.”

Consider: cutting taxes is inflationary and will increase interest on the debt, which increases interest rates.

Deporting workers, especially from the construction industry, is inflationary.

Increased tariffs are totally inflationary.

Where does inflation and interest rates end up?

PS As a retiree on fixed income I actually do appreciate cheap consumer products from Amazon. I could not get by without them. -sigh-

As to decoupling, the more coupled the less chance of war (too much to lose), the more decoupled the higher chance of adventurism as so much less to lose.

@Nick Kelly, I didn’t mean to imply lower quality. I really did mean only low price. And for the consumer, it’s obviously great, the definition of low inflation. But it comes at a steep cost: massive job transfers, technology transfers, and supply chains even in critical industries that are completely dependent upon an economic and geopolitical rival.

I’m not under the illusion that the Rust Belt would suddenly be full high paying factory jobs again, if the US were to completely decouple from China. Industry in places like Detroit and Youngstown, OH has been disappearing apart since the 70’s. But I think some of the worst aspects of the current US-China relationship could be mitigated.

Biden at least had the start of an industrial policy with the CHIPS Act and the Inflation Reduction Act (the name seems to be a terrible description of what it did, but it still may have been a good idea), as well as limiting technology transfers. I have to imagine that is at least one factor (along with Covid disruptions) behind the booming factory construction charts Wolf posts from time to time. Now if Trump could continue it with tariffs, things might start to get interesting…

You are totally misreading how the Trump policies ended. The trade war with China ended with the Chinese buying not “a few soybeans” but over $180 billion in soybeans. Not bad for a first effort which was always intended as a shot across China’s bow.

As to the “Wall” on the Mexican border… there are only 800 to 1000 miles of the border that require pedestrian barriers and Trump built or rebuilt 400 miles of them in his first term and had another 200 miles in the pipeline when his term ended.

Trump’s second government looks to be a lot more unified and is bringing in true China and immigration hawks. Add to that fact that he plans to get off to a faster start this time and it looks like “past is NOT prologue.”

The real question is how much of a difference will all that make. For instance the last 200 miles of the “wall” that needs to be built is the most difficult. It is along the Rio Grande (so the design that was easy to build in the desert may have to be re-tooled) and in terms of getting access to (eminent domain rules). BUT that is the 200 miles that needs to be secured since that is where most of the illegal immigrants are coming through. A conundrum that his people may have spent the last four years in the wilderness thinking about… or not.

Same for China. What is it that he wants to ACTUALLY achieve there? Isn’t that the FIRST question that needs to be asked? Maybe they spent four years coming up with an answer (and hopefully a plan)… but are the hawks like Vance and Rubio on board with the limitations? We shall see.

I don’t see any of this as particularly inflationary. Whatever is being made in China will simply go to the second cheapest countries that can produce it… coupled with Americans buying less of it should hold prices in check.

I just want to say that any discussion about what tariffs or deportations actually do or don’t do or will do is only relevant to people who have their eyes open. What matters to the majority is how they “feel”. Polls have repeatedly and consistently shown that a very large number of people “feel” less financially secure and also blame the incumbent administration for inflation. Obviously they aren’t reading this blog or they would know they are out-earning inflation and that the independent FED is primarily responsible for inflation and that both parties spend like drunken sailers.

I am not sure why. But Wolf’s post brought to mind a really old quote.

“The capitalists will sell us the rope with which we will hang them” is a quote often attributed to Vladimir Lenin.

Must be a subconscious thing ?

The similarities between the pre-1930’s and the current set up, makes me concerned that the non-holistic structure that we pretend is normal will not end in the same way.

I used too buy drinks for me and my WW1 veteran friend.

The Euro is headed down to parity with the US Dollar which is soaring so foreign investment is likely not a very bright notion these days.

Nouriel Roubini and Stephen Miran described “Activist Treasury Issuance” in a paper recently. Does it even make sense to count the amount of debt held by foreigners? I would be more curious about the duration exposure they hold. Are they actually trusting the Fed and the long term strength of the Dollar or just holding T-Bills opportunistically out of short term convenience?

Your leading questions are pretty much leading in the wrong direction.

There are only about $6 trillion in total T-bills outstanding. And I hold some of them, and so does Buffett and everyone else, LOL.

Foreign investors hold $8.67 trillion in total Treasuries, of which $1.17 trillion are T-bills (13.5%) and $7.5 trillion are notes and bonds (86.5%).

Overall, T-bills account for 22% of marketable Treasury securities. So with their 13.5% allocation to T-bills foreign investors are light on T-bills and heavy on notes and bonds.

That’s an interesting sidelight, because of all the BRICS headlines one would think the members would be short term treasuries. I guess they have more confidence in the US than they let on.

I also am curious about the “duration” (or maturity schedule) of foreign Treasury securities held by foreign investors.

Does info exist about the remaining life of the 86% portion invested in notes and bonds (i.e. are these securities that are close to their respective maturity dates)?

Also, at acquisition, are most of these notes and bonds picked up at issuance, or as seasoned securities on the secondary market.

Apologies if irrelevant or ignorant questions.

They hold nearly 25% of all Treasury securities, and about 33% of all marketable Treasury securities. In other words, about 1/3 of all Treasuries that are available and traded are held by foreigners. They cannot just hold those with shorter remaining lives. It’s not possible. There are not enough of these older securities out there, and other investors hold them too.

By the sheer magnitude of their holdings — 1/3 of all marketable Treasuries — they must constantly replace maturing notes and bonds with new notes and bonds that are then for the full term.

You can see that at the auction results of 10-year notes and 20- and 30-year bonds: Foreigners are big buyers. they’re heavily invested in long duration.

The US, Canada, and Mexico as a traiding block are well positioned compared to the rest of the world. Most of the other economies listed here have serious demographic headwins in comparison. The US is still a good bet.

One prays that you are wrong. Anchoring to an impotent trade block like North America.

A country built on, Ben Franklin’s musings, it’s a nice Republic if you can keep it

Love will win, eventually.

Thanks Wolf. Interesting viewing who is buying treasuries. Given the Fed and other central banks are not, and instead buying gold.

That’s why all those foreigners are rushing buy good old made in USA bonds!

We ARE geniuses!

The Fed is not buying any gold and owns practically zero gold.

Oh for Gods sakes:

The US govt is the world’s largest holder of gold with 82 hundred tons.

As of October 2024, the book value of the gold bullion held by the Federal Reserve Bank in New York is $564,805,851.07.

Note: ‘book value’ The NY Fed uses 42 US $ per fine troy oz as its book value.

The products are not cheap. The costs

are the loss of jobs and a overstretched,

safety net.

The Federal Reserve is NOT the US Treasury and the Fed owns none of the 8 trillion or so tonnes of gold owned by the US Treasury which is valued at $42.42 per ounce for a total value according to the US Treasury of around $11 billion. The Federal Reserve offers storage services which it charges for related to gold it does not own, and once again, the Federal Reserve owns practically zero gold.

RE: ‘Gold stored by FED is stored for others and is not US owned gold.

WRONG

‘Current holdings

As of 2021, the U.S. gold reserves total 8,134 metric tons. The next highest holdings were Germany’s, whose gold reserves were 3,364 metric tons.’

Wikipedia.

‘US gold reserves’ means US GOLD RESERVES

Apologies to anyone else for caps but for heaven’s sake how hard is it to look this up? What’s next: ‘but who really knows it’s there man? ‘

Luxembourg and Caymans are hedge funds, right? Should we be worried? What if they are de grossing concurrent with a big auction?

No, they’re not hedge funds. They provide fiduciary services to where you as Corporate America or Germany AG or whatever can set up an account at one of their firms, along with mailbox service, and feed that account from your overseas profits and then buy Treasuries with that cash in those accounts. They provide lots of other services too, but that’s the one that is relevant here.

I would love to hear more about how the rich hide their money, and what these “financial hubs” do for the world, much like how you explained how Buffet got out of paying taxes via donations in a previous comments section once (but in greater detail).

Y’know, if you’re ever feeling bored from lack of topics to write about.

With the US deficit seemingly structurally fixed at ~$2-3T a year now, despite there not being a “crisis” or declared war, I do find myself wondering what the effect of this (goofily named) “DOGE” effort will be. There are many ways to get to zero deficit – hold the budget flat in dollars as the economy (hopefully) grows, cut deep immediately, or spend more with the hope that it leads to even more growth. Both parties seem to have focused on this last approach and it has not been working. Deep and immediate cuts of $2T will probably be too painful. But this incoming administration is probably going to be different than anything the US has seen in a long time so who knows. A balanced budget, last seen in the Gingrich/Clinton days – I really have no idea how rates would react. I think they would plummet because the demand for “absolute safety” in US Notes and Bonds will still be there and entities would pay to get it.

Great commentary. Subscribed!

I wonder how much the “Big 7 Tech Companies” money is in Treasuries???

It finally happened, specifically, the last 30-year bond auction had an interest rate above the last 4 week T-bill. The Nov. 19th 4 week T-bill closed with an interest rate of 4.5% while the Nov. 15th 30-year bond auction closed with a high yield rate of 4.6 %.

Not that I would ever lend Uncle Sam money for 30 years at that rate, but like Wolf and others, aside from a few solid dividend-paying companies, my rotation in T-bills has grown over the last year as I took profits into the election and last week really. Let’s see who actually gets into the cabinet.

WB,

I think this is a milestone and I’m watching this closely.

As I approach retirement, I have a stash of cash that I intended to pay off the mortgage. I held off on paying it off and put the stash in TBills when TBill yields reached 5.5%, I decided to arbitrage my 3% mortgage. The financial (greedy) side of me realized that making a net 2.5% in a safe investment was a better choice than paying it off.

There were 2 problems with this.

1) The 5.5% was not guaranteed for the life of the mortgage. At some point I’d have to make a decision again on whether to pay off the loan. TBills are now 4.5% so the spread is less attractive.

2) The interest made on 5.5% did not generate the entire mortgage payment so there was still a net outflow of cash every month. It more than paid the interest on the mortgage so it was still a good financial choice.

If TBill rates drop below 4%, then the decision will be forced again. Should I pay off the house or sell it?

As you pointed out, long term rates are rising.

A simple calculation shows that if long term rates rise above 6%, then rolling this cash stash into a 6+%, 10, 20, or 30 year bond will pay BOTH the interest and principal on a 30 year mortgage at 3%. That would be ideal since the monthly bond payments will directly pay the entire mortgage and would resolve the cash flow issue.

Historically, long term bonds should be paying more than 6%, There may never be a good reason to pay off or sell the house if/when this happens. It would effectively be a free house over the next 10-30 years with an extremely safe investment guaranteed to last the life of the mortgage.

My parents had this same situation in the 1980’s when their 30 year mortgage was 6% and bonds were 15%. They were able to pay the mortgage, property taxes, insurance, and some repairs with the bond monthly income without having to pay off their house. This has happened before and helped many Pre-Boomers.

BobE

The question is do you really want to lock up funds for 30 years? I would be scared of locking up funds for more than perhaps 4 years. Is the slightly higher interest rates worth the lockup?

“The question is do you really want to lock up funds for 30 years?”

I think the idea here is that you’re buying a duration-matched bond instead of paying off the mortgage – not instead of shorter-duration income products.

In both scenarios, your funds are ‘locked up’ in an asset.

I also hold part of a mortgage (in retrospect, I was foolish to pay some of it off, but that was my safe game plan before interest rates rose) that I could pay off if I sold my brokerage account.

But I really want to get an arbitrage situation going like you mentioned.

Every time someone mentions having to pay taxes on treasury interest, Wolf calls them an idiot. But if I have to pay 30% (or are treasuries exempt from State taxes?) back of my 5% gains, now I’m down to making 3% of real money, which is less than my 3.125% mortgage. So, that’s obviously not worth it, right? But Wolf always yells at people who mention this, so I am second-guessing myself even though I have a Math minor. Am I thinking about this clearly?

Also, stocks should make more money in the long run, and if yields go up later, you might feel like an idiot, but a free mortgage payment is a free mortgage payment, so nothing wrong with playing it a little safe, either. So trying to figure out what is best…

Federal gov’t bonds are exempt from state & local taxes.

Yes, it’s really all about risk versus prudent investing. I don’t gamble, I do my research. The last stock I bought was 1,000 more shares of MO on October 25th ahead of their earnings. They tend to do well in election years and when inflation is rampant and people are stressed, but MO is also the only stock Greenspan ever admitted to owning and has historically been well managed and paid a good dividend. After a decent gain the question is “now what”, and I think it might be back to T-bills until after the inauguration and a cabinet is seated. I will say that I am building a position in energy, ag, mining (national and international). Solid companies with low P/E ratios and decent dividends. There are still eight billion of us that need to eat, stay warm and actually get shit done. That means there is plenty of demand for real things.

A preponderance of short-term securities would envisage a reallocation of funds.

Only 13.5% of their Treasury holdings are T-bills, 86.5% are notes and bonds. And they buy heavily in the 10-year note auctions and the 20- and 30-year bond auction. They’re into long duration.

All this noise about a ‘BRICS currency’ seems like an overreach when you compare India’s charts with those of other BRICS countries. China is rightly reducing its exposure given the current geopolitical environment and does not appear entirely driven by the intent to move toward a ‘BRICS currency’.

Recent memory says Putin ditched the BRICS currency several days after Trump was elected, according to TASS. I wonder how to interpret that.

From Goldmoney.com: “Last Friday, President Putin ruled out a new BRICS currency for now saying that it is not under consideration, promoting trade settlement in national currencies instead. “

Two of the BRICS, Russia and SA are economic basket cases. In SA the grid is completely unreliable. Most businesses have generators, with perishables it’s a must. As for Russia, it’s understandable they would want out of the ruble.

China’s SCO is also complying with US sanctions.

China has no interest in an accountable currency, communism requires control. Right now China can literal collaborate with anyone (and are), this will last so long as they are sitting on a mountain of dollars/treasuries.

Interesting times.

Wouldn’t a 60% tariff on a 10$ tshirt be 16$.

A business guy on tv said last trump tariff on a $100000 container cost him 125000 and the new trump tariff cold cost him 185000. And u s businesses can’t help because they are swamped already and are worried about finding help or losing help.

No. Tariffs are NOT applied to retail prices. Tariffs are applied to the cost that the importer pays for the product. They’re a tax on the profit margins of importers. If a T-shirts (purchased by the container) costs $1 from a sweatshop in Bangladesh, the 60% tariffs add 60 cents to the cost for the importer. So maybe Walmart’s costs go up 60 cents, and instead of selling the T-shirt at $9.99 it might try to sell them at $10.59, and if sales collapse because of the price increase, it will roll back the increase, as it has done on many products, and then Walmart eats the tariff or part of it. Consumers no longer pay whatever.

You say unlikely to raise prices but at the end of the day the lack of competition in businesses as well as other cost inputs will most likely be inflationary unless and until ai robots become usable and commonplace. Tariffs and deportations will not help especially if they overreach and it appears they will and go after the dreamers One of the inputs is skilled manual labor I am in the HVAC business and anyone I know in this type of business can’t find enough by a long shot. So post your prognostications we will know more in 18 months.

While tariffs are obviously an economic tool they are increasingly becoming a political tool. Obviously to position and win elections but also to flex international power. This area much harder to measure as not clear if the tariff is smart economic move or something else. I’m sure this has always been the case but seems more extreme now.

It will be interesting to see what the credit markets have to say about rates after Trump is sworn in. Best guess, higher rates for a longer period of time. The 10-yr UST could easily be priced to yield 5% or higher by the end of Q1 2025.

90+% of EURonians (including bank employees) are financially retarded:

– There is still around 0% interest on basic accounts.

– Most of them are using savings/term deposits accounts around 2+% depending on locked out period.

– Banking fees are big driver of profits for EU banks, so most people end up flat at 0% and/or negative after fees and collected interest and payed tax on it.

– EU banks take pool of money and buy US treasuries and collect nearly whole interest on investment. Free money.