Subprime is always in trouble, and now, after the reckless-subprime lending era, more so. Prime is in pristine shape. Car-Mart joins our Imploded Stocks.

By Wolf Richter for WOLF STREET.

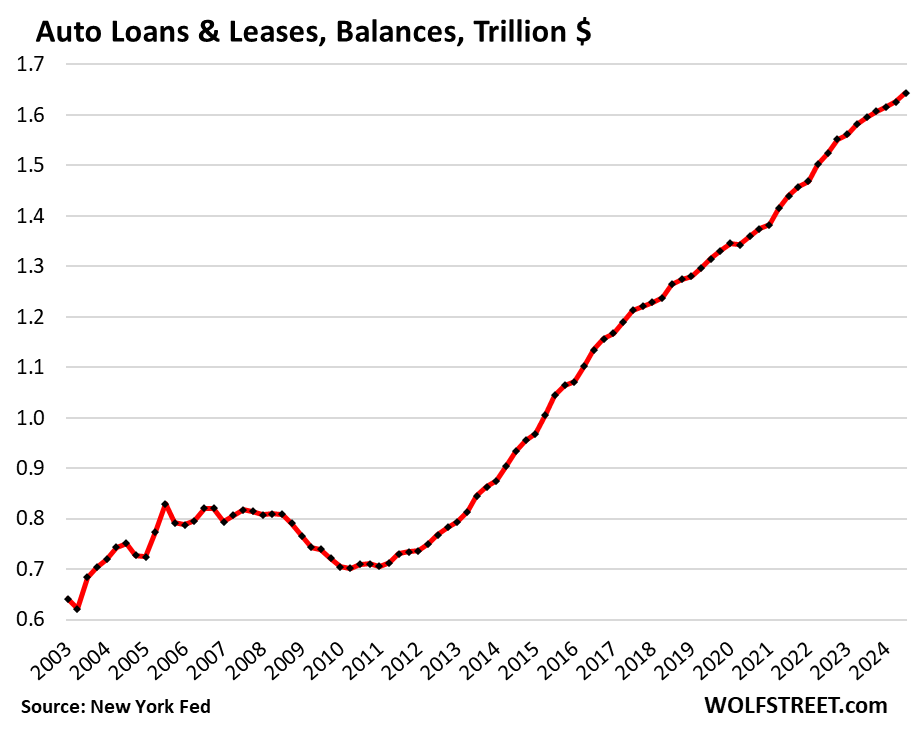

Total balances of auto loans and leases for new and used vehicles rose by 1.1%, or by $18 billion in Q3 from Q2, and by 3.1% year-over-year, to $1.64 trillion, according to data from the New York Fed’s Household Debt and Credit Report.

But the 3.1% year-over-year growth rate was the second-smallest since Q1 2021, behind only Q2 this year (2.8%) and the third smallest since Q4 2018.

One of the reasons balances grew at a relatively slow rate is that more people are paying cash for their vehicles due to the higher interest rates. For new vehicles, the share of cash purchases rose to 20% in recent quarters, from 18% in Q1 2022. For used vehicles, the share of cash purchases rose to 64%, from 59% in Q1 2022, per Experian data. We’ll look at other reasons for the slower increase in a moment.

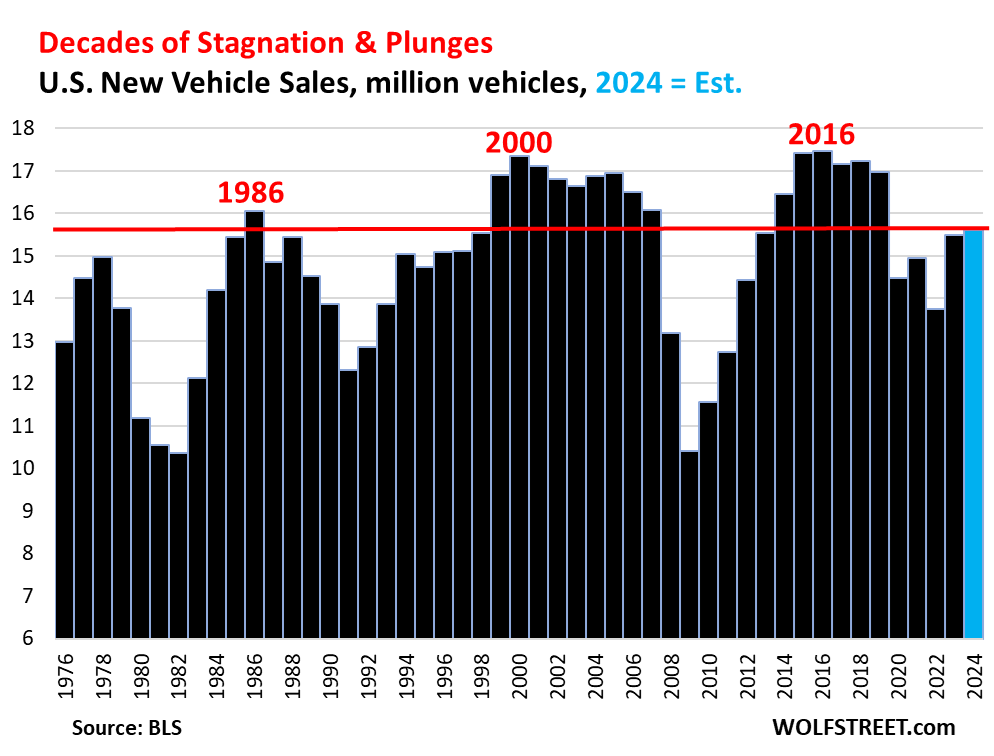

Auto loan balances over the past 20 years ballooned by 135%, but not because of spectacular unit-sales growth – far from it, new vehicle sales, responsible for the vast majority of auto loan and lease balances, have stagnated for two decades, interrupted by two big plunges:

Rampant price increases and automakers taking their models upscale are what drove up auto loan balances through 2020. Then in 2021 and 2022, prices exploded and pushed up dramatically the amounts financed, even as sales volume plunged due to the vehicle shortages.

But prices of new vehicles started edging down in 2023 and through Q3 2024, just a tad – new vehicles, with their much higher price tags and 80% finance penetration dominate auto loans and leases. Used vehicle prices plunged over the same period, but with their much smaller loan amounts and small 35% finance penetration, they play a much smaller role in this equation (details and charts of new-vehicle CPI and used-vehicle CPI).

Those slight price declines of new vehicles kept a lid on the amounts to be financed and slowed the growth of the auto loan and lease balances so far this year.

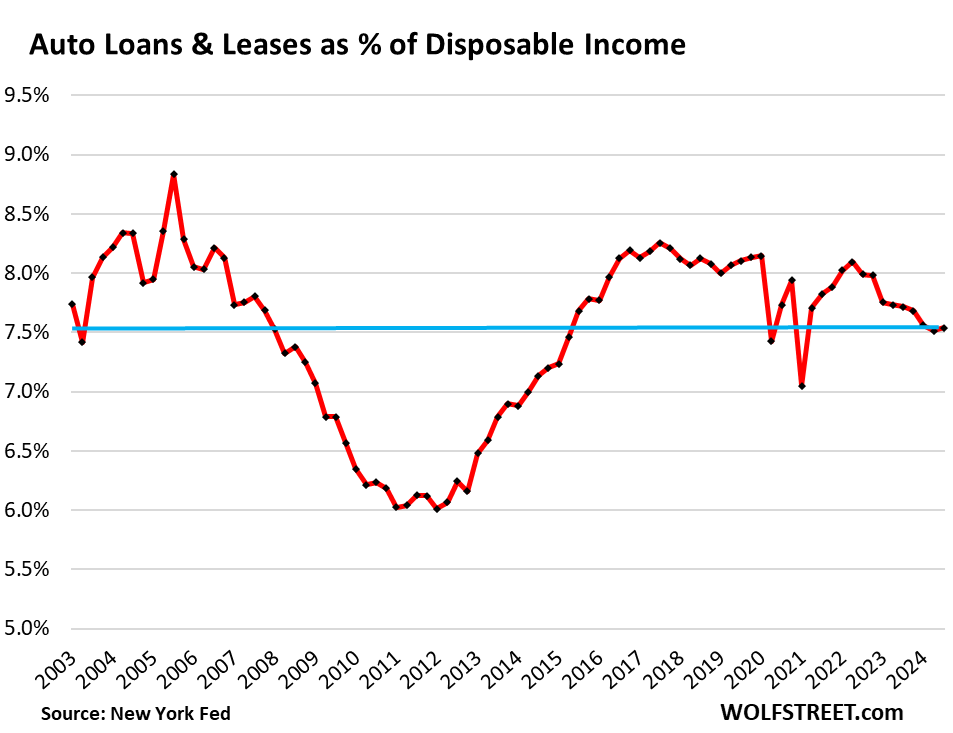

The burden of auto loans and leases.

One way to measure the burden of auto-loan debt on households is the comparison to their disposable income, which includes after-tax wages, plus income from interest, dividends, rentals, farms, small businesses, transfer payments, etc. It’s what households have left over to pay for their costs of living and service their debts.

Rising incomes and stagnating or declining new-vehicle unit sales volume should have caused the burden of auto loans and leases to decline sharply over the past two decades. But rampant price increases over the years saw to it that the burden only moved up and down in a fairly narrow band, with the exception of the 2008-2012 collapse of the auto industry in the US.

As prices began declining in mid-2022, slowing the growth of the auto loan balances, disposable income rose sharply. And so, the debt-to-disposable income ratio started declining two years ago, and in Q1 2024 dipped to 7.5% and has roughly stayed there through Q3.

Subprime is always in trouble, which is why it’s subprime.

Subprime lending is largely confined to used vehicles, particularly to older used vehicles, sold by specialized subprime dealer-lender chains, or financed by specialized subprime lenders. All these lenders then package these auto loans into Asset Backed Securities (ABS) and sell them as bonds to pension funds and other institutional investors that buy them for their higher yield.

Of the auto loans originated in Q3, 16.9% by balance of were subprime, down from the prepandemic range of 19% to 25%, according to New York Fed data.

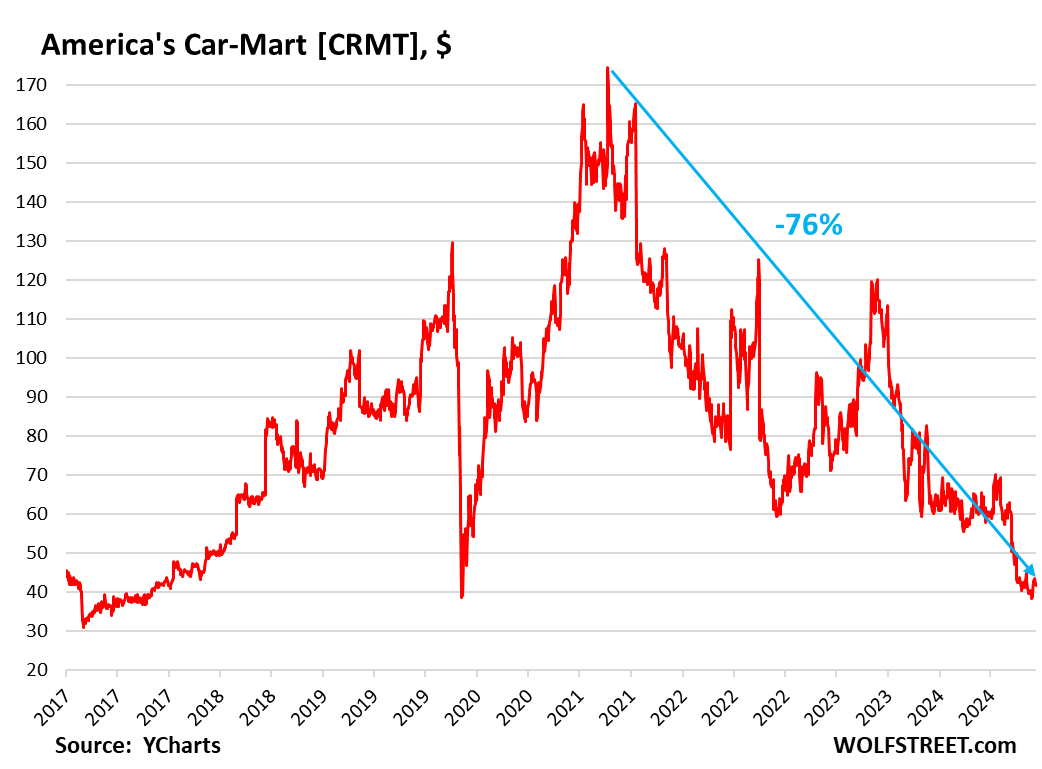

During the free-money era, the specialized subprime dealer-lenders loosened their credit standards and got very aggressive. They built in huge profit margins into the vehicle sales amount and into the interest. At the same time, used-vehicle prices exploded. And the risks piled up. And when used-vehicle prices began to tank and interest rates began to jump in 2022 and 2023, those risks came home to roost. In 2023, several PE-firm-owned subprime-specialized dealer-chains filed for bankruptcy.

Even the large publicly traded subprime dealer-lender America’s Car-Mart disclosed massive problems in December 2023, and its shares [CRMT] tanked. On November 1, they closed at $38.21, the lowest since September 2017. On Friday, they closed at $41.77, still down 76% from the all-time high in May 2021, and now in our pantheon of Imploded Stocks.

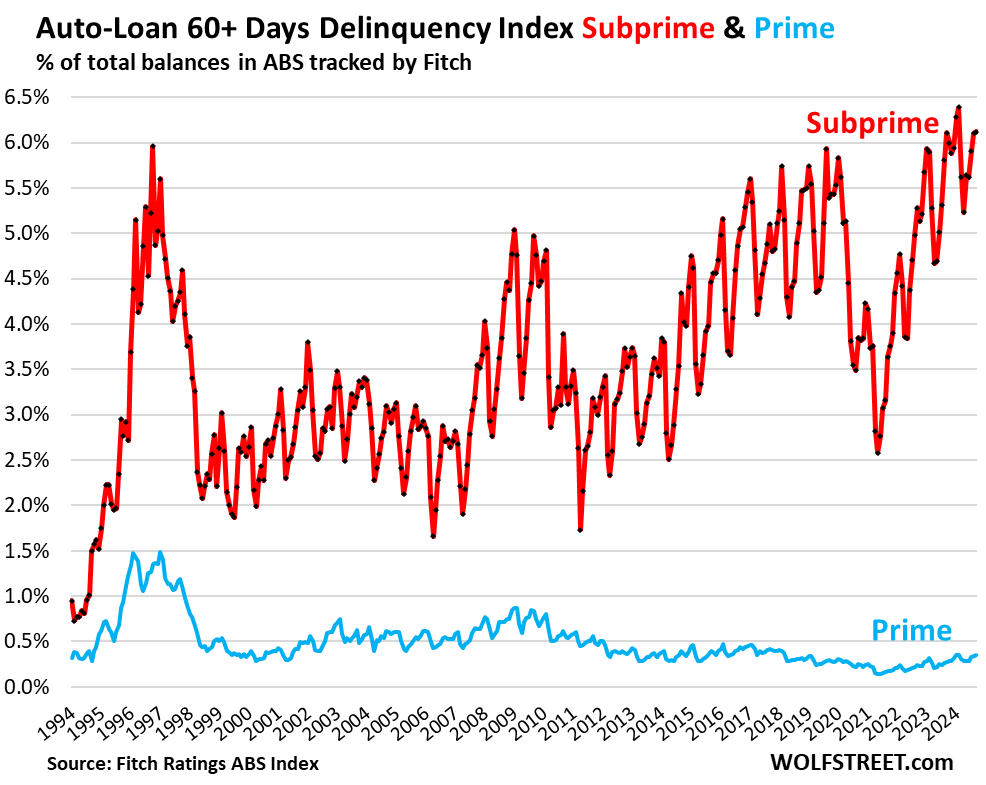

Delinquency rates: total, subprime, and prime.

The total 60-plus day delinquency rate, as tracked by Equifax, was 1.55% in September. The highs this year had been in January (1.59%) and February (1.61%). This year’s range is up by about 50 basis points from the prepandemic range centered around 1.0%.

The overall delinquency rate has been rising since early 2023, reflecting the mix of the surging subprime delinquency rates and the pristine prime delinquency rate.

Fitch, which rates ABS backed by auto loans, splits out the delinquency rates for prime-rated auto loans (blue in the chart below) and subprime-rated auto loans (red). Subprime is always in trouble, and after the reckless-subprime-lending era more so than before. Prime is in pristine condition. And let’s remember: only 16.9% of auto loans originated in Q3 were subprime. It’s a small specialized part of auto lending.

The subprime 60-plus day delinquency rate in September remained at 6.1%, same as in August, and same as in September 2023, according to Fitch (red). The fact that the delinquency rate didn’t worsen year-over-year indicates that the spike in delinquencies out of the reckless-subprime-lending era has begun to slow. These delinquency rates peak in January or February. They hit an all-time high of 6.4% in February this year and may end up in the same neighborhood next February.

The prime 60-plus day delinquency rate has been in the 0.28% to 0.35% range all year (blue), which is minuscule. Even during the Great Recession, the prime delinquency rate rose to only 0.9% at the worst moments.

In case you missed the earlier parts of household debt and credit: Here Come the HELOCs: Mortgages, the Burden of Housing Debt, Serious Delinquencies, and Foreclosures in Q3 2024

And from a day earlier: Household Debt, Delinquencies, Collections, Foreclosures, and Bankruptcies: Our Drunken Sailors and their Debts in Q3 2024

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It is a tale of two cities. It was the best of times. It was the worst of times. The evident pain in subprime seems to have had a knock on effect in the election.

What’s in pain are the subprime dealer-lenders, some of which filed for bankruptcy, while Car-Mart’s stock imploded. What’s in pain are the investors – PE firms and stockholders – that own these companies. What’s in pain are the holders of the subprime ABS bonds. What’s not so much in pain are the subprime borrowers. They can drive the vehicle for free for a while, and then, when it gets repossessed, they can buy something older with cash, or maybe get another subprime loan. There’s a reason why credit scores are subprime. Subprime does not mean poor; it means bad credit.

Just wanted to add some serious WAY to Go Wolf,,,

Especially for your last sentence in the above…

FOLX really and truly MUST understand that no maTTER, what so ever their ”STATUS”… IF they don’t pay their obligations,,, THEY ”WILL” become haunted and hunted

Been there and been done there in the very dark past, And will only wish and want and pray for those on here paying attention to Wolf’s Wisdom,,, dispensed daily per many other frequent commenters,,, but also

THE comments, some from regulars, some from others…

YA absolutely gotta make YOUR decisions yourself…

SO similar to other aspects of YOUR life…

Good Luck,,,

Regarding the “haunted and hunted” comment – it brings up the too little discussed “deficiency judgment” concept in home mortgages (ie, you may get foreclosed, lose your equity, and still be on the hook for loan repayment shortfall – which seems obvious…but is hardly ever mentioned).

Considering that about 15% of home mortgage borrowers (about 8 million households) got foreclosed during Bubble implosion 1.0, it is kinda amazing that “deficiency judgments” never became a major, major issue of discussion.

Perhaps all the workout programs for home debtors and bailouts for bank creditors somehow re-routed around the “deficiency judgment” process (although even *that* was hardly talked about) – but I’m not sure.

Considering that creditors owed tens/hundreds of thousands almost never just “let things go” (if for no other reason than *they* in turn owe money that can only come from mortgage repayments) it is kinda strange about the near “radio silence” on deficiency judgments.

You do very rarely hear about “surprised” home debtors getting hit with “zombie mortgages” but those are close to one-offs…not millions of households.

I wonder if Wolf has some detailed insight.

Over the past 10 years, there weren’t a lot of foreclosures, and so the number of deficiency judgements in the 38 states where they’re legal was small and not worth talking about. The old rule still counts: You cannot squeeze blood out of a turnip. For a lender, getting a deficiency judgement adds to the cost. So if the borrower files for bankruptcy, getting the deficiency judgement was a waste. If the borrower doesn’t have anything that is worth getting, the deficiency judgement was a waste too. The lender will just drop it and take the loss.

Wolf,

I was talking about in the wake of Housing Implosion 1.0 (2008-2014, 15% of all mortgage debtors got foreclosed – about 8 million households…yet very, very little subsequent discussion of deficiency judgments).

I get the “blood-from-a-turnip” point – although historically, creditors haven’t been too shy about at least *trying* (quite a bit in fact) – and that’s how you end up with deficiency judgment rules written into law in the first place.

And as I mentioned, it is possible that the debt-workout, bank-bailouts re-routed (millions?) around the whole deficiency judgment process (at the cost of money printing/inflation…to finance all those millions of workouts/bailouts..) but in general the specifics of the linkages don’t seem to have been discussed a bunch.

My general sense is that while the workout/bailout process might have forestalled the completed-foreclosure/deficiency judgment process for a bunch of defaulted home-owners…it was nowhere near 8 million (the number who ended up in foreclosures).

Since DC basically seems to have no other tools/ideas other than doomed-finance, boom-bust economic policies propped up (barely, for a little while) by interest rate manipulation/money printing, it probably might be worthwhile to really understand (in detail) how Housing Implosion actually resolved/worked itself out.

I just recently started reading you — thank you!

Quick question from the uninitiated. I always considered “disposable income” to be truly disposable == (all income you have) – (all mandatory expenses, i.e. taxes, mortgage, loans, utilities, food, healthcare). I’m my mind that’s the truly disposable income, and that’s what economists should be looking at. When you analyze burden of loans — this seems like a much better measure than the definition you used. For instance, if I bring home 5k monthly, the burden of 1k car loan doesn’t sound that bad. But if I bring same 5k home, and pay 3k mortgage+insurance, 1k food+utilities, then the burden of 1k car loan is crushing. Why don’t people use truly disposable income to analyze burdens? Is it because the numbers are less reliable / unavailable? Or the picture is much worse?

You’re talking about “discretionary spending” = spending on non-essential goods and services. A vehicle purchase is considered discretionary spending. Food, housing, insurance, etc. are non-discretionary goods and services. That’s a very different concept than “disposable income.”

Disposable income is income that is available to pay for all discretionary and non-discretionary goods and services, including interest, and to save the rest.

They should just call it net income. The income after taxes and deductions are paid. Disposable means you use it and throw it away like a paper plate or something.

another industry = RV

that now is in same/worse boat

however the dealers all think they have upper hand

no one can afford $1,000 month payment and still live

why prices have crashed

keep up the ascerbic criticism Wolf, it’s why im a fan. Fuck dummies.

I wonder whether we could do a column on “net liquidity” I mean you have dones several on the net liabilities and assets of the fed, and how those have changed. With reverse repos at zero and bank deposits much lower than they used to be, we might approach a point where treasury issuance, really begins to drain the stock market.

Then there are things like the treasury buying back its debt, which debits the treasury’s bank account and credits a lot of others, so net liquidity positive.

I don’t know where to directly find total us bank deposits, or the level of the treasurys deposit account at the FED etc.

Would appreciate your guidance.

I’ll tackle the last 3 items:

In terms of the Treasury buybacks, since the government has a large deficit, rather than a surplus, the Treasury Department has to borrow the cash (issue new bonds) to buy back the old bonds. This is a wash, with no change in “net liquidity.”

The Treasury General Account (TGA) is the government’s checking account at the Fed. It’s on the Fed’s balance sheet under liabilities. Google: H.4.1

The Fed releases monthly data on all commercial banks, assets and liabilities. One of the liabilities is deposits. You can find them here: (H.8)

https://www.federalreserve.gov/releases/h8/current/default.htm

The liquidity you haven’t mentioned is money market funds. We discuss them (and CDs) here quarterly. Last one:

https://wolfstreet.com/2024/09/13/money-market-funds-large-cds-small-cds-and-t-bills-americans-and-their-huge-piles-of-interest-earning-cash/

Wolf, re the 60+ day delinquency chart, appears to be a seasonal aspect to the delinquencies as well – but I can’t tell from the chart which are the high months and which are the low.

Is this a consistent patter (such as borrowers using tax refunds to get out of a hole)?

Yes, the Fitch chart is very seasonal raw data. You can set your clock by the seasonality. So it’s important to look at YoY which in September was essentially unchanged from the record September last year.

Holiday spending season causes a debt increase, which causes delinquencies to rise to peak in Jan/Feb. Tax refund season brings delinquencies back down. Then following travel season and back-to-school season, delinquency rates rise again.

It’s funny what all is seasonal, even the traffic on my website, LOL

– How many borrowed this company to buy back its stock ?

– There are signs that second hand /used cars are falling in price. and that doesn’t bode well for all the lenders. Does the Mannheim index (for second hand cars) fall as well ?

One used car dealer reported last week that about 2 months ago he was only able to buy 4 cars in the price range ( $ 2500 or less). Last week he reported that he was able to buy 14 cars for less than $ 2500.

This used car dealer buys these cheap cars, makes some repairs and then sells them for $ 5000 or less. He also reported that for him business is still very good.

“Does the Mannheim index (for second hand cars) fall as well ?”

It plunged from mid-2022 through 2023. But this year, it essentially flatlined:

https://wolfstreet.com/2024/10/07/more-evidence-this-may-be-the-end-of-the-historic-plunge-of-used-vehicle-prices-that-had-pushed-down-cpi/

– I assume this index has gone lower in the last weeks/months.

The low point was June, after a long hard plunge. It has wriggled 3.4% higher through October 31, since then (red line seasonally adjusted).

– This used car dealer (see my previous answer) has a YouTube channel called “CarQuestionsAnswered”.

Trucks are ingrained in american culture, that is for sure. They are everywhere out west…

The horse was also engrained in American culture, so was the american Indian, then they weren’t .

Pretty soon you will be able to ride your AI robot into town…piggyback style, then send it to go pick up groceries while you get your nails done. Could be the robot will be so advanced one day it might contemplate the usefulness of us humans.

But for now the love for our trucks outwest is only matched by our dogs.

You don’t have to go to the grocery store anymore. You can buy groceries online (I’m NOT talking about Instacart where you pay humans a little to go to a classic grocery store), but online grocery stores) and have it delivered to your home. Much of the stuff behind the scenes is handled by computers and machines, from processing your order to designing the delivery route. Big operators have started to use robots to pick your packaged goods. Drivers are already being automated away, see the success of the Waymos. They are everywhere here, and they work a lot better than human drivers. And when you stand at a crosswalk trying to cross, a Waymo will actually stop, even when it’s coming around the corner, while human drivers would rather run over you than stop. In healthcare, a lot of work is already being done by AI, including summaries of doctor visits, interpretation of tests, etc. … has been done for years. Much of the stuff you see on the internet today, including by major publications, is AI generated. Like it or not, it has been here for a while, you just didn’t notice.

“when you stand at a crosswalk trying to cross, a Waymo will actually stop”

Not testing that.

Especially when they arrive here in the frozen North.

I’m testing it every day. And I tell you that I would long be dead if I had relied on human drivers to stop at crosswalks or even at traffic lights even when they have a red light. For example, they turn right on red to cross a crosswalk where pedestrians have a green light, but the driver doesn’t stop. They come around the corner, turn right on red, and they drive right over you because they’re looking left for oncoming traffic from the left. Human drivers are the worst drivers out there. They kill 40,000 people a year and severely injure two million. As a pedestrian, I love Waymos.

I have a hard time making eye contact with Waymo drivers.

[ran out of reply buttons]

“I’m testing it every day. ”

In your area, where temps vary 25 degrees annually and above freezing, I’d be less leery. Cold in general and ice in particular are difficult variables to account for with electronics.

Your point about human drivers in general is well-taken but still, they are strongly adverse (for practical and moral reasons) to rolling over conspicuously visible and cautious pedestrians.

NoBadCake,

The Waymo and the human have the same ABS brake system. The Waymo will react more quickly.

NBC – you make a good point, albeit one that only applies to a small portion of the country and only during winter.

Would Waymos be able to recover from a spinout? Pump the brakes to avoid locking them up? Drive in a lower gear to help with traction on hills?

Driving on snow & ice requires a fundamentally different skillset than driving on dry pavement.

ShortTLT,

Humans do NOT know how to drive on snow and ice. Humans are idiots behind the wheel when it gets slick. Nothing is worse than human drivers. Just look at reality out there when it’s snowing.

“Pump the brakes to avoid locking them up?” LOL… Time to buy a modern car? ABS and stability control (standard on ALL cars for over a decade) DO KNOW how to pump the brakes, and do so wheel-by-wheel, releasing only the locked wheels, while the other wheels continue to brake, something humans can never even dream of doing.

Wolf,

No disagreement that people are terrible behind the wheel… in any weather LOL.

My car does have ABS, but I can feel my wheels slipping long before it kicks in. Ditto when hitting the gas – I don’t need to wait for the TCS light to come on, I know when I’ve got wheelslip.

I’m sure my decision-making process could be codified into a bunch of if-thens… but I maintain that driving with poor traction is a different skill than doing so on dry pavement. Just look at all those videos of [human] drivers in southern cities trying to drive after they get an inch of snow.

With ABS, if you get in trouble, you step on the brake and let the ABS do the work. If you try to pump yourself, you negate the effects of the ABS. The ABS will pump (release) each locked wheel several times a second. Obviously, if you don’t have to brake, and can gently steer your way out of trouble, you get off the brake and let the car roll. But if you have to brake, step on it and let the ABS do it.

Why can’t your robot do your nails?

Robots do surgery already. Been around for years.

Nail salons generally hire cheap recent immigrants. From a cost point of view, it’s difficult to replace cheap labor with expensive robots for basic jobs like that. But if labor gets expensive enough, they might.

Pickups, a sector the Japanese are making inroads into, have long been a source of much profit for GM and Ford. Even Chrysler has a toe in the waters.

The positive aura of pickup trucks — usually fed by popular culture such as country music soundtracks — was only enhanced by the rise of the SUV. Larger vehicles as a whole got a boost from that event.

Detroit has been coasting on goodwill in the sector for quite a while, complacently believing it has a lock on the market, and in the meanwhile Tokyo comes out with the Tundra and other offerings. Can the Koreans be far behind? (Their Santa Fe SUV suggests they could put forth a competitor to Detroit’s line-up.)

In the greater scheme of things, the goal of Detroit is not only to continue their dominance of the market but to ensure foreign entrants never get a real toehold. The Tundra marks the first crack in that philosophy. Selling quality pickups at a reasonable price ensures that Toyota can compete on an even keel with GM/Ford. The F-150 trembles when it sees the Tundra approach.

With winter basically here, it’s time to put snow tires on those pickups and send them on their way. A Christmas dusting of snow in the backs of those pickups would look kind of funny.

Why are Carvana and Carmart stocks behaving so differently? Their business models couldn’t be that different, could they?

Used vehicle sales are doing fine, no problem. That’s what CarMax and Carvana are into.

In terms of financing, they’re into prime not subprime. And they’re not lenders, they just arrange the loans. And prime, which is the vast majority of US consumers, is doing great.

Stocks are behaving differently because Carvana has hit a Gross Profit per Unit of $7400 while Carmax is around $2300 I think. Carvana has been increasing the GPU YOY and is considered a growth stock. Carmax is not considered a growth stock .

So far this year revenue rose 12% YOY for Carvana while revenue has dropped -4% for 6 months YOY for Carmax.

Isn’t Carvana shrinking inventory? Isn’t it saddled with elevated operating costs?

If you just retired.

You need a car. You get 80,000 a year.

Do you pay with cash?

Do you take out a Loan?

Do you feel lucky punk? Well do you?

Interest rates are too high to take out a loan. I’m considering buying a new car and did the math. Theoretically, I could put say 20% down and put the other 80% in the market and gain more capital gains than I would pay in loan interest. I’ve averaged 12%/year returns over the last few years. But the new administration’s economic policies scare the bejesus out of me, so I’ll probably just pay cash.

Imo this logic makes more sense with a duration-matched fixed-income product. For example, you take out a 5-year loan @ 3.5% apy, and then buy a 5-year note yielding 4.5% – there’s 100bps of spread to profit off before taxes.

As long as treasuries pay at least 4%, I will continue to pay down my 2.7% mortgage as slowly as possible, since the treasuries will accrue interest faster.

I was going to pay cash, but they were offering 1.99% ( new ).

Ad seen last night during footy was for ZERO interest for up to 60 months for truck, don’t remember brand…

Gotta admit it piques my interest when we are getting around 5% on Treasuries, eh?

So far, gonna stick with my 20+ year old car and truck w. far less ”new tech” to go wrong, etc., etc., ,,waiting for the EV of my dreams,,, LOL

I wonder when all these 0% financing offers will die off.

At my day job, the company offers 0% financing promos thru Synchrony bank. My understanding is these are subsidized by the manufacturers’ – but the terms are becoming less and less persuasive (used to be 18 months @ 0%, then it was 12 months, now it’s 6 months…)

I recently had some Synchrony corporate bonds mature with a 4.25% coupon (NB; purchased below par with a 7% YTM). I’m not sure how long Synchrony can continue to offer 0% financing when people like me can loan money to them at very positive interest rates…

I’m retired and have a decent fixed income (for now).

End of lease I looked at releasing another. Low miles on this vehicle.

Prices WAY out of line, leasing costs also very high for a lesser vehicle.

Bought out the lease I had and am very happy remaining debt free.

Just one guy’s story. “Your results may vary”.

Imposter, way to say it bro

I follow Car Dealership Guy on X, and a dealer finance person posted Wells Fargo recently said they will now loan 84 months up to 135% LTV and subprime down to 540s. Wow

Good site with weekly column. I follow it too.

Didn’t mortgage lenders go down this rabbit hole some time back? That didn’t work out too good.

84 months (7 years) has been available for years. And it makes sense in a way because vehicles last a lot longer and stay in good shape and look good for a lot longer than they used to decades ago when 60 months was the max.

135% LTV has been pretty common too. It’s riskier for the lender because the recovery is going to be smaller. But they generally figure on a loss ratio of 50% at default, so that 135% LTV is already baked into their calculations. And the riskier the loan, the higher the interest rate (profit for the lender). So generally it works out.

With unsecured loans, such as credit cards or personal loans, banks’ loss ratios are often over 90%. And there is no LTV at all because there is no V (value of the collateral as there is no collateral). And they figure that into their calculations, which is why credit card interest rates are so high because risks are high, and lenders want to be compensated for those risks.

Lenders are in the business of making money on loans, and they figure this stuff into their calculations. But sometimes, there are massive changes in the market, including the price gyrations since 2020, and that’s where some of the math goes wrong.

Volkswagen will take what they can get out of Americans right now. They were offering 60 mo same as cash. I’ve heard several buy American types say that they are considering Volkswagen just for the financing available.

Subprime is always in trouble?, that seems to be its nature… like the girl you met by the whirlpool.

Do you know the third biggest expenditure for the fat unhealthy American after the house and car….. it’s that girl you met at the whirlpool. No actually it’s healthcare, then divorce.

Or maybe you met the right girl by the whirlpool, stayed in shape and took care of yourself, bought a modest house and car, and never divorced! Happens every day…

Girl by the whirlpool looking for a new fool…Bob Dylan was singing about her after her car got repossessed. Her credit was bad…so sad.

With the number of DoorDash deliveries to my apartments I would not be surprised if some of my tenants spend more on food than leasing their cars (a Starbucks Latte and Scone before work every day inexpensive, but it is just crazy expensive when you have DoorDash bring it to you every day).

Rising prices, rising debt and the accompanying high rates continue to shine a bright light on the haves vs the have nots

Thought it was interesting that FICO, while small, announced the first drop in ave score in a decade

… after the huge surge during the pandemic when people got free money to fixe their delinquent debts. We discussed that surge in FICO scores at the time. And after that first dip, it’s still far above normal.

Maybe some FICO scores going down from credit NOT being used Wolf?

Mine just did, or, rather I just noticed it, after not using credit to buy for 5 years, just CC paid off every month

To get to the top credit score of 850, you need to have a perfect credit history plus some credit, such as a mortgage, or a mortgage that you recently paid off. With no mortgage in years and all credit cards paid off monthly, you might max out at 830 or so. There is only a small deduction in the FICO score system for not having debt.

If your FICO score is in the 700 range, it should rise when you pay off some debts (lower your leverage).

Wolf – can I request an article on how FICO scores are calculated? I’ve been wondering why my score bobs up and down despite not opening any new lines of credit, and having all major loans set to autopay.

It seems to be based on my credit card usage (lower available credit = lower score), but doesn’t my creditor *want* to see me borrowing and making regular on-time payments? I’ve literally never made a late payment.

Transunion is telling me I can improve my score by having older accounts and paying down more of my mortgage – the former is in progress, and the latter I won’t do since Treasuries yield more than the rate on my mortgage.

@ShortTLT as Wolf says “when you pay off some debts (lower your leverage)” you score should go up, but your score should also go up if you get more credit since the FICO model like to see a you use a “lower “percent of available credit”. I have a $1mm HELOC on my primary home (I paid off the purchase loan early) and when I got the HELOC my “percentage of available credit” used” really dropped and my credit score went up. I have never had a credit car balance but every month with my 5% cash back Amazon VISA buys everything in Amazon, another 2% cash back VISA is for all recuring charges and never leaves the house and a third 2% cash back VISA pays for everything else. I was getting close to my VISA credit limits (before they got the auto pay payments that pay them off in full each month) and increasing my limits to more than triple what I ever charge increased my credit scores even more.

Thanks for clarifying the % of available credit – that makes sense. I guess I don’t really see my credit card as credit since I just use it for the points & fraud protection.

Yes, I see the irony in that sentence.

If you cannot afford your next car, don’t buy it.

Simple

Americans will give up their houses before stopping payments on their cars. They are still required at the plantation even when homeless.