Going to further crush demand for existing homes. Bondholders feel the pain.

By Wolf Richter for WOLF STREET.

Longer-term Treasury yields spiked this morning, on top of the surge since the September rate cut. Spiking yields means plunging prices, and it has been a bloodbath for bondholders.

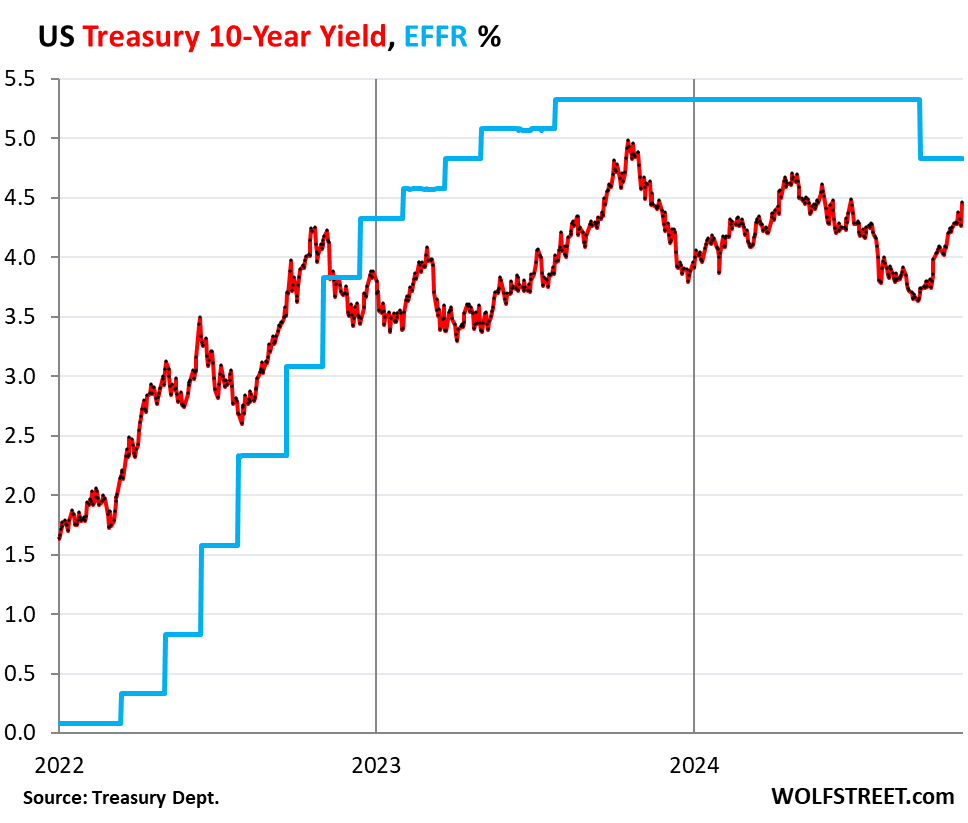

The 10-year Treasury yield spiked by 20 basis points this morning, to 4.46% at the moment, the highest since June 10. Since the Fed’s September 18 rate cut, the 10-year yield has shot up by 81 basis points. 5% here we come?

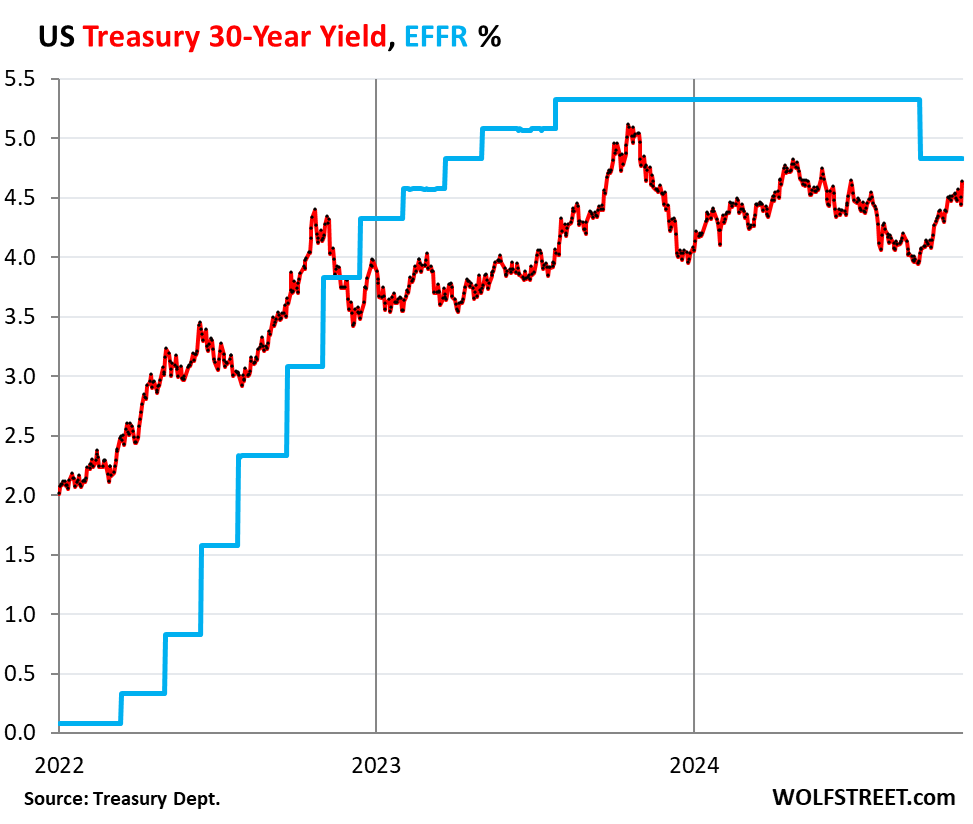

The 30-year Treasury yield spiked by 20 basis points this morning, to 4.64%, the highest since May 31 May 30. Since the Fed’s rate cut on September 18, it has shot up by 68 basis points.

So all the bond market needs to get spooked further are more rate cuts?

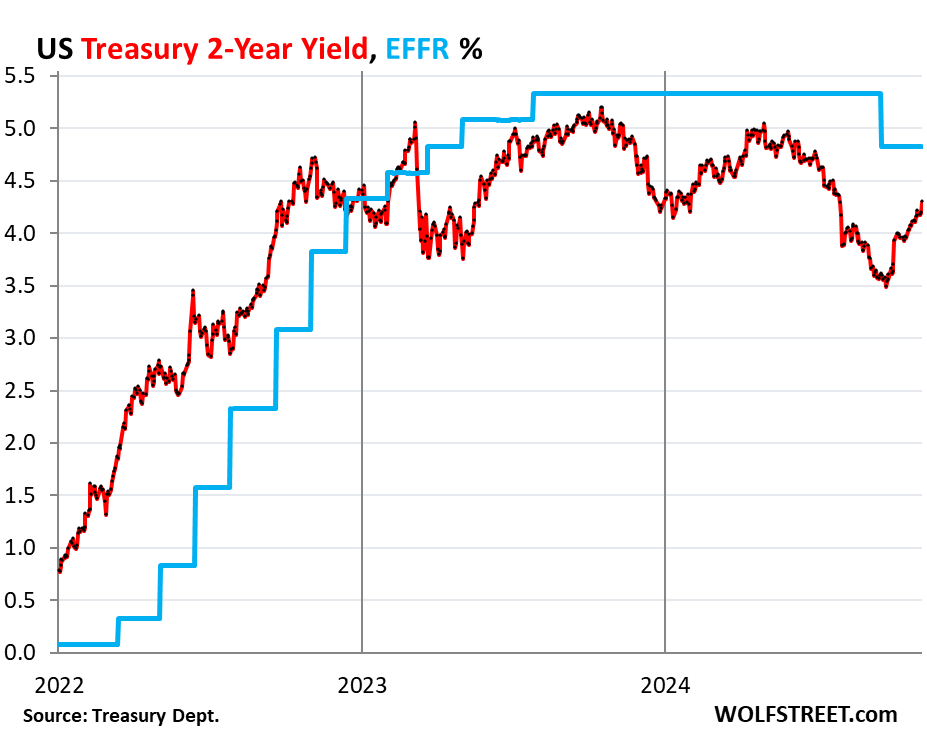

The 2-year Treasury yield shot up by 10 basis points this morning, to 4.29%, the highest since July 31. Since the rate cut, it has shot up by 69 basis points.

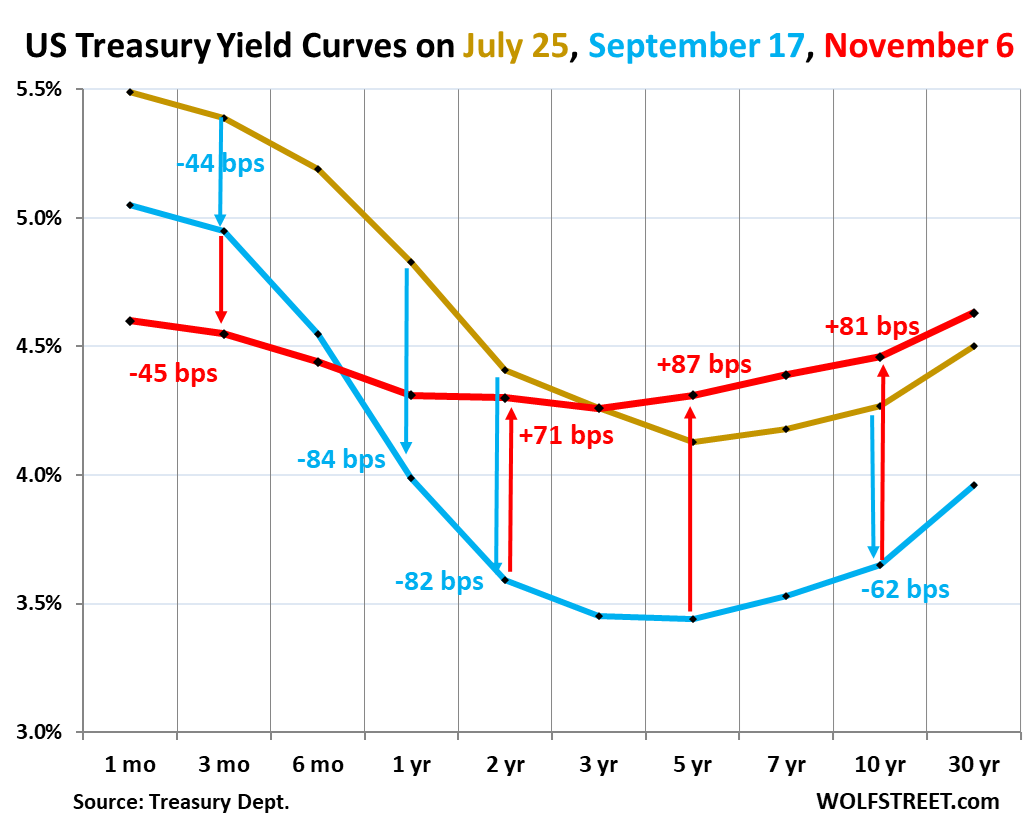

The “yield curve” un-inverted further in another massive leap today, continuing the process of un-inverting, driven by the surge in longer-term yields and the decline in short-term yields.

The normal condition of the yield curve is that longer-term Treasury yields are higher than short-term yields. The yield curve is considered “inverted” when longer-term yields are below short-term yields, which began in July 2022 as the Fed jacked up its policy rates, pushing up short-term Treasury yields, while longer-term yields also rose but more slowly, and thereby fell behind. The yield curve is now in the process of normalizing, with longer-term yields surging and surpassing short-term yields.

The chart below shows the “yield curve” with Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: July 25, 2024, before the labor market data went into a tailspin that has now been revised away.

- Blue: September 17, 2024, the day before the Fed’s mega-rate cut.

- Red: This morning, November 6, 2024 after the election results.

The 30-year yield is now higher than all other yields, and it has un-inverted completely. The 10-year yield is just a few basis points from un-inverting completely.

Note by how far those longer-term yields have risen since the September rate cut (blue line). The yields from 3-years through 10-years have shot up by over 80 basis points since the September rate cut, a screeching-tire U-turn, going down in two months, going back up faster and further in seven weeks, amid huge volatility in the Treasury market.

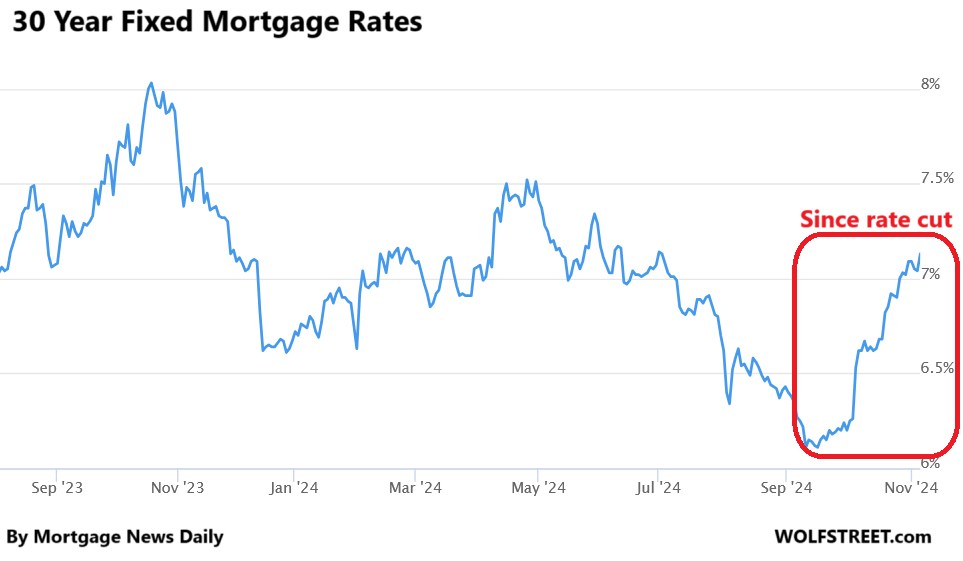

Mortgage rates too. They roughly parallel the 10-year yield, and they spiked today 7.13%, according to the daily measure from Mortgage News Daily.

Mortgage applications through the latest reporting week, which doesn’t capture the last two days, already dropped further from the frozen levels before, pushing down further the demand for existing homes, which is on track to plunge to the lowest levels since 1995 this year.

For the housing industry, and for home sellers, this U-turn was a painful slap in the face. At this pace, the yield curve will enter the normal range soon – but in the opposite way of what the real estate industry had hoped. It had hoped that the Fed would cause short-term yields to plunge to super-low levels in no time, which would drag down longer-term yields, and mortgage rates would follow.

But mortgage rates had already plunged from nearly 8% in November last year to 6.1% by mid-September this year, without any rate cuts, on just a wing and a prayer, thereby pricing in all kinds rate cuts and whatnot. And since the rate cut, much of the wing-and-a-prayer plunge in longer-term yields has reversed, that’s all that has really happened.

The real estate industry was expecting 5.x% mortgages by about right now, and they were already close in mid-September with 6.1% mortgages, and some were talking about 4.x% mortgages just in time for spring selling season, and today they’re looking at 7.13% mortgages.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Are we on recession watch now that the curve is uninverting. Tariffs, mass layoffs of government employees… will also play a part, but I’m feeling it.

We’ve been on recession watch here since mid-June 2022, and it has been fruitless. The yield curve is un-inverting the wrong way, it’s un-inverting with longer-term yields spiking on inflation fears driven by high demand.

This is not a recession-fears un-inversion, where short-term yields plunge a lot for a long time, below long-term yields that also drop but more slowly, as the Fed cuts policy rates in big junks, by 50 basis points and 100 basis points into a recession. Now the Fed is cutting (more slowly going forward) into above-average economic growth and re-kindled inflation.

I think things may look different as higher long term rates are accepted as here to stay.

But correlation is not causation, I agree with you generally that the yield curve isn’t the recession indicator it used to be, it may just be coincidental this time.

So it sounds like you agree that they have to let inflation run a little hot. Treasury yields will be such that nominal returns with be weak, and real returns will be negative…

Lovely.

Or, tsy yields move up with inflation so real yields stay positive.

well no hurry

looking for another house but won’t over pay

of course I could leverage but likely won’t

“…as the Fed cuts policy rates in big chunks, by 50 basis points and 100 basis points into a recession…”

Wolf, “everyone” (so they say) is pricing a near-certainty Fed will cut another 0.25% tomorrow. Cutting 0.75% in less than 3 months seems either panic (thinking the economy will tank) or recklessness (thinking inflation is vanquished).

What do you think is their argument/thought process here?

LOL. When the Fed panics, its cuts by…

150 basis points in ONE WEEK (March 2020) to near 0%. It would have cut more if it had had more room to cut, but it was already at the lower bound.

200 basis points in 8 weeks (2008) to near 0%. It would have also cut more if it had had more room to cut, but it was already at the lower bound.

In both cases it used lots of QE to supplement the rate cuts because there was no more room to cut. That’s what it looks like when the Fed panics. Now, the Fed’s rates are still way above inflation and Fed is just easing them closer to inflation.

maybe Powell can summon the bond vigilantes by cutting 150 basis points

wouldn’t it be funny to see market rates rise if he cuts them

Wolf, now Trump won, and their administration cuts useless programs and lowers debt; removing money from the “system” will this make the dollar stronger?

Presidents cannot cut any spending. They’re told by Congress what to spend and who to spend it on. Congress passes the appropriation bills, the President signs them, and the Executive Branch has to, um, execute these instructions.

So the question is: what will Congress cut? Republican-run Congresses have been able to cut taxes, but not spending. So that would increase the deficit, which is how that worked in the past. And that seems to be the plan now. We’ll have to see.

Part of the problem is that a lot of the spending, including 75% of the CHIPS act, is flowing to red states/districts, and they want to keep the money flowing, and so it’s unlikely to get cut.

Wolf, Why are they saying they will cut out $2 trillion on waste? CHIPS is on policy, green new deal, Inflation reduction act. Are they stating that congress can make an appropriation bill that will replace all 3? Or all is set in stone.

I have no idea why they’re saying what they’re saying. You need to ask them.

Since the discretionary portion of the federal budget is only $1.7 trillion, half of which is defense, they are either lying, or they will be cutting Social Security ($1.3 trillion), or Medicare/Medicaid ($1.6 trillion).

Which would you like?

They can’t cut SS and Medicare because they have their own funding through employment taxes. SS is totally self-funded, Medicare is largely self-funded.

“Wolf, Why are they saying they will cut out $2 trillion on waste? CHIPS is on policy, green new deal, Inflation reduction act. Are they stating that congress can make an appropriation bill that will replace all 3? Or all is set in stone.”

Answer: they’ll cut $200B of alleged future spending growth, and say it cuts $2T over a decade (the usual way of quoting costs).

Gattopardo,

🤣👍 nailed it!

LOL! First, presidents don’t determine spending levels, CONgress does. Second, neither party has a track record for cutting spending, and that is the problem.

cash is seeking yield, period, risk on! More billionaires being made and $50 bread on incoming!

Gattopardo, the 2017 tax cuts were what started all of this inflation. 2.5 trillion to Corps. for no good reason.

Lowered the home deduction potential by 1/4 for no good reason

Cut out every small business getting by with 10k of deductions.

Totally wiped out any healthcare deductions. (Unless you are terribly ill)

Betcha these next Corp tax cuts of 25-26 will be 4x-10x larger too.

“Wolf, Why are they saying they will cut out $2 trillion on waste? ”

I swear to god, every one of his voters is an idiot. Why not cut $2 quadrillion in waste while you’re at it? You’ll lap it up.

Not just inflation fears, but deficit fears–future supply of treasuries outpacing demand., particularly as the market priced in an $8T Trump deficit vs “only” $4T for Harris. TIPS have only moved about half as much as nominal bonds during this period, so about half the move in nominals is from inflation expectations, the other half term premium.

Inflation! You ain*t seen nothing yet. I lived i n Latin America. When a country can not afford what it is spending: just like a household which has to borrow money to pay for daily expenses, you get BIG inflation before it goes broke.

I hope Trumps tariff, tax cut plan can fix this. But please Federal Reserve you can now stop cutting rates perhaps rase them. You do not have to make so much low cost borrowing available to the Democrats. And please Mr. Musk save us 2-3 trillion in a hurry.

Andrew, Trump’s tariff plan (if instituted)is going to drive the economy into a cliff. Not to mention the mass deportation plan.

And a household budget is NOT like a country’s fiscal budget. Please. There are plenty of explanations avaiable with a litle google searching (I know Wolf does not allow links).

First and Long.

🍿 🪑

Kick back and watch the show buddy.

😂

oh my sweet summer child… tariffs and tax cuts are inflationary. “$2 trillion in waste” has the credibility of “full self driving by 2017”

Markets can stay irrational longer than you can stay solvent.

All spending is someone’s income and government spending actually goes into the private economy.

Private + public spending = total income. If you cut $2-trillion in spending that’s a lot of people who don’t have money to spend.

The economy is not hot now so much as manic.

There’s an important distinction between deflation that is the result of greater productivity or innovation, or deflation that is the result of a crisis.

Inflation is a double edged sword for workers, because while it means higher costs, if people are getting wage increases they can better pay down existing debt. With deflation, the opposite is true. The more you pay, the more you owe.

You end up with something like the Great Depression or a Balance Sheet Recession like they had in Japan after their crash.

I read on Twitter that this is the first time the Fed has initiated a cutting cycle and the long end yields have gone up, instead of down. I tried to research it this morning but the only thing I could find was 1998. But with that cutting cycle, rates on the 10YR dropped initially, for what looks like a month, before heading higher.

Do you know if this is the only time the Fed has started a rate cutting cycle and yields on the long end went up instead of down? If this is the only time it’s happened, would really appreciate your thoughts on why it’s happening now.

Yes, looks like it going back to 1962, at least superficially from looking at the chart. This could be because this is the first time the Fed cut without a recession in sight, and with the labor market still growing a decent pace. It’s a very different scenario. Inflation fell dramatically without a recession and labor market pain. I don’t know how many times that has happened before, maybe never.

But I caution you, this is 60 years of data, and it squishes everything together, including the current episode. So it’s hard to see the details to confirm it. We’d have to look at the actual numbers for each rate-cut cycle, and that’s a lot of work, and I’m not doing it. I just look at the picture. And good enough. Click on the chart to enlarge it

Probably only going to get the sugar so tax cuts no layoffs 5050 on the tariffs basically stimulus

Nice! The sooner and higher rates rise the better.

Yet 24 of the larger Central Bank have cut rates while only 9 have raised over the past few months. All the countries who have cut have seen big drops in CPI YOY.

I just read an article that provided a list of 36 countries that have deflation or dangerously low inflation. Thus there are more countries on this list than countries with good growth and high inflation.

I am not sure what to think. Maybe the US is just so much more economically healthier than most other countries. Most of the 9 countries that have hiked are having currency issues. A few countries with strong economies driving up inflation and that hiked rates are India, Japan and Australia.

“…or dangerously low inflation.”

🤣 like “a “dangerously beautiful day?”

The stuff people concoct is sometimes just funny. Many goods prices have dropped/plunged = deflation in goods = a great thing because people can afford to buy them more easily. And prices are still very high.

“deflation or dangerously low inflation”

How very 2002, Establishment-Bogey-Man of you.

How did the subsequent 20 years of Fed distortions in response to that Bogey-Man work out for the country?

And look at the horrific impact that decades of deflation had on the global adoption of, say, computer technology.

“dangerously low inflation” –while we all love some deflation as consumers, policymakers like those at the Fed fear it incredibly as it may sober up the drunken sailors to the realization that if they can tough it out a few more months with their 12-month-old iPhone, their upgrade will cost a bit less. The treadmill’s gears slow.

LOL I did copy the “dangerously low” from the headlines but now that you call it out. That adverb is funny.

Amen.

Yeah, great if you are older, own your own home, and have no real debt so you can get richer. Way to look out for yourself. Sorry if my response is terse, but today is not a good day.

Higher rates mean home prices crash faster and young people will be able to buy in at reasonable prices, so in that sense the boomuhs get the shiv. We need to definancialize houses.

I think it means investors will just keep buying anything decent up with cash. High end stuff keeps turning over to wealthy people.

That is a great word “definancialize housing” I love it. And we can do it. Just buy a smaller home on a smaller lot . Tiny houses on the internet cost anywhere from 10-100k . Perhaps 1/2 acre in the country for 5K. Now President Trump, just get rid of the building regulations stopping this. And if all else fails, try adue housing for young marrieds

Half acre isn’t a small lot.

I’m on a fifth of an acre and it still takes me over an hour to mow the damn lawn.

Unless you already loaded up on treasuries during the last once-in-a-generation opportunity in May. Or the one before that in April. Or the one prior last October…in that case, you’re about to stare at losses again.

We may never have a good day again.

Are you new here?

Don’t worry, any logical person is going to get frustrated reading the comments SoCalBeachDude writes.

You’ll get used to it

Once you work 50-60 years save money be responsible .Your welcome to get in the boat .Quit crying grow a set and become responsible not hard

I have been curious as to how the yield curve would un-invert. Would the short end stay at 5-6.0, with yields going higher further out the curve, or would the short end just drop (seemed impossible considering the coming issuance)?

Looks like it will be a combination of lower yields on the short end and higher yields on the long end (thanks for the data Wolf).

So, now that Trump is president, and he insists that taxes won’t go up, how is Uncle Sam going to fund it’s budget AND service the debt? Where is the break-point in terms of the ten-year? That’s what I want to know. At a minimum, I see an inflationary recession, unless CONgress actually balances the budget… Thoughts?

MMT will save the day. But it’s only 1 day after the election. 2 months to inauguration. No idea what Trumps actual government will look like or what policies will actually turn into practice or to what degree the machinery of government will implement them. I think the only thing we can say for certain is that Trump favors production. Thats not nothing, but will it be enough. To the degree that credit is a confidence game, Trump today appears to be good for confidence. Tomorrow ?

Printing money, not production, is key, when we keep outspending our tax revenue, and when we keep bailing out the rich now along with the poor.

Production is key when we tax at higher rates; however, ramping up production now enough to pay for all our spending hasn’t worked since Reagan drastically lowered income tax rates. Unleashing the capitalist spirit hasn’t worked enough to keep up.

Let’s stop spending, or let’s stop bailing out the rich, I humbly say.

10-4 v-d

Growing up in 1940s-50s meant folx who wanted money, including kids, WORKED for it…

SO sad for SO many folx, including many family who grew up with everything needed or wanted without raising a sweat, etc., etc.

Sooner, and also later, all these kinds of ”free lunches” will stop, and some have already stopped the last few decades.

While I adore the proverb, ” Find what you love to do, and the world will reward you.” I have found over the last 8 decades that works SOME of the time…

Well, the commodity space still looks cheap to me, especially if we are going to expand debt.

Interesting times.

Spending will have to be moderated or cut outright. Of course this would have been the case regardless of who won the election.

Trump in first term talking with Head Economic adviser Gary Cohen, who has concerns about budget deficit: The latter has an issue with budget deficit: Response: ‘Just print the money’

Pretty much everyone on this site has castigated Powell for too low interest rates, brought in right or wrong for Covid crisis. In 2018 Powell took first baby steps to raise rates. ‘Worse than Xi’ thundered Trump.

Deficits are going to increase, of course, but so is the rate of increase.

Mexico will pay for it.

Trumps answer is to increase tariffs on imports resulting in greater tax revenue without increasing domestic income taxes. Domestic producers benefit by increasing their own prices. Down side will be increasing inflation.. although it is claimed that China, Mexico or someone else will pay the tariffs… good luck with that.

When he first proposed tariffs it soon became clear he thought the exporter paid them, like an admission fee. In other words, he didn’t know what a tariff was. At one stage in first admin, he wanted a huge tariff on Chinese stuff including apparel. This was just before winter and folks would be looking at up to double for coats etc. Advisers prevailed. The reason for tariffs is to encourage domestic production but ex expensive niches, there is negligible US or Canadian apparel industry. One hybrid is laser cutting of leather in US which is then stitched into jackets in Mexico.

I think it’s more about “punish them and protect us” mentality. Or a hollow campaign promise to ignite the serfs.

As if in some magic world a business can impart pain on another business (or country in this case) without hurting your own business in the process.

99% of the stuff they say is promising to make Harry Potter magic real. Like what moron believes this stuff?

I guess someone who didn’t take econ 101 and their diet of financial advice derives from Joe Rogan or Social media posts.

Try putting tarrifs on all goods coming into america. We did this way back when, and did not even need or have an income tax. A lot of our suppliers are then going to set-up shop here and employ people. GDP will rise. The GDP debt ratio will get better. Perhaps, perhaps, perhaps……….

I have perhaps a silly question. Are Treasury yields heavily dependent on the Federal Reserve interest rates, or are they determined based on other factors? It seems like Treasury yields rise even when the Federal Reserve rates decrease, but there is also some correlation between the two?

Short-term Treasury yields (1-month through 6-month) move with expected Fed policy rates within their maturity window for most part.

Long-term Treasury yields (esp. 10 & 30 years) move with inflation expectations and supply expectations (funding of government deficits). Lots of inflation and lots of supply is a toxic mix for the bond market. That’s what gave rise to the bond vigilantes in the 1980s – 1990s. They scared the bejesus out of the governments at the time, which finally led to a halfway decent budget.

And as I understand it, unlike the 80’s and 90’s, banks no longer really have control to set the mortgage rates since the paper is now packaged and sold as MBS on the secondary market. And that market, which competes against the 10 year treasury yields, is the one that effectively sets mortgage rates. Please correct me if my understanding is too simple or needs adjustment.

Bond vigilantes are our only hope then. Good thing to keep an eye out for if they actually sell bonds that can’t be redeemed these days.

Re: our only hope…

Since 1957 there have been four major bouts of core inflation with peaks in late 1970, early 1975, mid-1980 thru mid-1981, and 2022. ’70 and ‘80/81 were followed ~3 years later by big upward movement in the ten-year treasury yield. In contract terms it looks like a well-designed clawback period. ’75 was oil shock driven and the ten-year barely moved.*

August of ‘73, 33 months after the Nov/Dec ’70 core CPI peak, yield on the ten was 425 bp higher than core CPI.

August of ’83, 38 months after the Jun ’80 core CPI top, ten-year yield was 875 bp higher than core.

If they let core run at or near 3%, and the market is allowed to have its way, we could see yields on the ten continue to rise for another 12-18 months. 7% ain’t out of the question.

*Yes, I know core strips out food and energy, but energy inflation eventually makes into core via production and transport.

My namesake trade continues to outperform. Here we go 5% 10-year!

Everything is fine, get your spacesuits ready and make sandwiches for the trip!

NVDA almost to 150 like I expected

Wolf ought to cover the economic implications of the AI revolution destroying the need for “knowledge workers” but he won’t

Sometime pretty soon, I will write an article with a headline like this: “We Might Not Get our Recession until the AI Spending Bubble Implodes.”

The amount of money that gets SPENT on AI is just mind-boggling right now, from servers to power plants and construction of data centers. Big Tech is burning through their cash piles right now to do this. Most of this spending for accounting purposes is an “investment,” so it goes on the balance sheet as an asset (capital investment), and does not show up as an expense on the income statement and does not drag down earnings until later in drips and drabs when it’s depreciated or written off. Since this huge amount of spending comes from corporate balance sheets and not from AI-income, it’ll have to run out someday. You’ll see that in the earnings calls from Meta, Alphabet, etc. They’re already under pressure to show results and slow down this cash burn. And when they do slow down the cash burn on AI spending, that may be when we get the recession. Two years of dotcom bust (tech spending slowdown) when the Nasdaq collapsed by 78% and many highfliers went to zero also finally led to a recession. But this stuff takes years. Until then, that kind of widespread spending from corporate balance sheets is very stimulative to the economy since they’re plowing their hoarded cash back into the economy.

2026 peak.

2027 rollover.

2028-2029 could be like the Great Depression. Celebrating 100 year anniversary.

The big ugly is building, but it’s not happening yet.

I say this housing cycle must be completed. It should peak in 2026 or early 2027.

This commodities cycle is also only in the 2nd or 3rd inning.

Short term treasuries, 2 year, will rollover soon and move back to 3.5%

10 year moves to 3.75-4%

30 year will stay elevated up to 4.5%

Oil could easily move back to $100+ and in 2027 I wouldn’t rule out $150?

I’m staying long miners, energy, emerging markets, agribusiness and long grade A/B bonds.

Watch for the HELOC’s levels to climb as The MAC’s flood the system with that $11 trillion in tappable fake equity.

Banks are going to make killing the next 18-30 months. Then the implosion will be a huge deflationary period.

50% at least on the stock market. 30% drop in housing at least. The Big Ugjy is coming. Thank you Wolf.

roger, i’ll be stunned if it lasts 3-4 years, but i guess we live in interesting times.

Roger S. Mitchell,

You had me until you wrote “10-year moves to 3.75-4%”

Pretty sure that ship has sailed.

I’ve learned so much from this site. Even just a year ago I was basically clueless to a lot of the things I understand now. However the majority of what I HAVE learned, can be boiled down to: “Why weren’t you born BEFORE 1991 stoopid?”

Palantir is using AI to defend us atm.

So I mean, while top top secret, it does seem to be working.

Peter thiel is a mind behind palantir and the ceo is the other. The ceo is quite the character.

Trump: “I am the king of debt”.

Sure enough, his only legislative achievement was an unneeded tax cut that would ostensibly only add ~$1T to the debt (I say that having personally benefited). Of course it ended up being more like $2T — dry powder we could have used for the pandemic.

So yeah, I don’t see much cutting or paid-for spending. And thus, likely pressure on bonds. The 20% tariff threat portents ill on the inflation front as well (He also wants, with senator Lummis, to print money — i.e. inflate M1 –to buy Bitcoin… Huh???) This could be a nasty brew.

As the man once said… “Will be wild!!!”

See collapse of Taj casino, losses to bond holders and huge licensing, management and financing fees. At the end the Taj was paying a million a day in interest.

Oh man look up… is it Deustche Bank?

Phew, rogue bankers are wild.

Think Le Chirrfe from Casino Royale

Did you know they sell one of their AI thingamabobs for 100k! And it’s the size of half a vcr.

Crazyness!

Although differences are present (and I don’t want to jump to any conclusions), similarities are also present between today and Black Monday in October of 1987. The 10 year treasury rate rose from approximately 7.3% in 11/86 to almost 9.4% in 9/87, a 200+ BP increase over ten months or roughly 29%. The DOW, which was considered overvalued in 1987 reached roughly 7,300 in 8/87 and then corrected in a violent manner in October 1987 and settled at 5,000 in 11/87. Yes I realize other problems were present in the stock markets before Black Monday but one that seemed to be shrugged off was the rapid rise in interest rates over that 10 month period.

Today, as WR has clearly pointed out, the 10 year treasury has risen from roughly 3.66% in 9/24 to 4.46% today, an 80 BP increase or roughly 22% in just two months. The 30 year is displaying the same trend.

What is critical to understand is that long-term US treasury rates are used as a basis to value a wide range of assets ranging from bonds, to real estate, to stocks, investment annuities, and other assets. The higher these rates move, the more impact it will have on asset valuations, especially assets that are valued based on cash flow streams that are further out into the future. Unless cash flow streams (i.e., future earnings) can increase at a quicker rate than the negative impact caused by increasing long-term interest rates, eventually, asset values will be reset which as we’ve seen historically, can be a violent process.

Please note that I’m not predicting a stock market correction/crash but if, as WR mentioned in his article, 5% 10-year treasury rates are realized (and then subsequently increase from this point), there’s going to be a collision that needs to be sorted out in the markets. WR has clearly documented this is already occurring in the residential real estate market as higher interest rates are killing demand. The solution, as noted by WR is simple. Lower prices.

We’ve already seen significantly lower prices realized in CRE (especially office) with weakness in prices beginning to show in residential real estate markets. Bond values/prices are now under pressure (especially the long-end) so it would appear that the stock market is the last one to get the message (which is usually the case).

From my perspective, long-term interest rates are the key as if these rates continue to increase at relatively rapid rates, pierce the 5% level, and continue their ascent, I’m not sure how the stock markets can diverge from this trend over the long-run.

BTW, it looks like good old Mr. Buffett appears to be ahead of the game again. Record cash/ST treasury positions, heavy liquidation of certain stocks including Apple and BOA, waiting like he always does, for the market to clear and stocks to reset to more reasonable values.

Yep. I am of a like mind. Some companies are undervalued, mostly in the ag and commodity space. I am buying these, but that’s about it.

Ummm the S&P climbed a ton today. 137 points and counting. I mean holy batman that’s good!

I think from just relief that indecision 2024 is over.

is it good? is stock mania completely divorced from earnings or productivity good in and of itself?

i’m having a hard time seeing how it is.

Sell the rumor, buy the news.

A 1 million $ 401k made 30,000$ yesterday.

3% in 1 day. Thats ridiculously good.

Now 94% of 401ks are in boring target date retirement. So they MAY have seen about 1% due to them being so conservative. I really dislike foreign and emerging markets. They just have nothing going on atm. It’s all integrated heavily into the US market. I mean obviously Taiwan is foreign but you might as well just say it’s in the US market.

AMZN rises have been massive lately too.

Even INTC is up! Woo.

What a time. 😃

sufferinsucatash, please tell me how it’s good, much less ridiculously good for an absurd asset bubble to inflate farther?

great, my 401k is up. but i can’t access it without penalties for 15 years. because of my plan, i also can’t really reallocate it to something less risky. so really, this is all paper wealth. i’ll reiterate, asset prices increasing is only good if it’s a result of growing economic productivity. if it’s due to bubbles and mania, that’s not good, as it’ll eventually collapse and leave devastation in its wake.

It’s just a cycle franz,

From a historic stock market perspective its very exciting.

If you have zero control over your 401k, then that is not good.

Maybe start an IRA you can control more?

A “historic asset bubble” is kind of pessimistic, when people are profiting so much. Business is really good, these are fundamentals why it’s going up.

One could wait out the next large drop, or you could get your portfolio a much larger life vest to survive the drop while we all wait on that drop.

Also one could completely stay out of the market, have little risk but also have little reward.

I just feel it is a good time. Finger’s crossed! And if the S&P goes up so much, think how much single stocks are going up.

business is really good? okay, i’ll bow out here.

Your Dow numbers for 1987 look way, way off.

some random thoughts.

the stock market definitely doesn’t get it based on 203% of gdp. that’s basically zirp and qe level valuations, and there is qt and a fed funds rate of 5%.

70% of people polled yesterday said the economy was bad. this should lay rest to the bs from wall street that americans feel good about the economy when the stock market is up. they don’t.

More than half of Americans have a reading level below 6th grade so I take what “they” say with a large grain of salt. Most don’t seem to either recognize nor care whether facts are involved at all these days.

Since I found out the government can control the weather, I am wondering where I need to send my next weather-related property damage bill? /sarcasm

that’s not really the point. if a booming and bubbled stock market is so great for america as a whole, why would 70% feel bad about the economy? shouldn’t they feel rich, after all, the stock market is the economy?

We know which half that is. H.L. Mencken called it when he said, “Democracy is the theory that the common people know what they want, and deserve to get it good and hard.”

Reading level below 6th grade?

I didn’t realize you had to know how to READ, In order to be aware that your bank account is EMPTY.

But I do learn something new on this site every day

NSACBD – …recalling a (not always a) joke from an earlier, pre-interweb/pay-by-phone/autopay day:

“…how can I be OUT of money?!? I still have checks in my checkbook!!!…”.

may we all find a better day.

Yeah Franz,

They are just dumb. I’m sorry but that’s how we ended up here. Easily manipulated dumb dumbs. (On both sides as well)

But hey it’s easy to get ahead! Woo.

I do feel for our country. ❤️

Not similar at all to Black Monday. Greenspan just tanked reserves during contemporaneous reserve accounting.

“BTW, it looks like good old Mr. Buffett appears to be ahead of the game again.”

Yeah, sure. He sold lots of e.g. BAC, missed the 8.5% up today. Yeah he is an oracle. Glad I’m not doing such trades.

Now the question is, how long he will sit on the cash? Years? But apparently whatever he does is gold.

He still holds LOTS of BAC. He’ll sell the next batch and make even more on it. There is nothing better than unwinding a huge position when prices are still going up. It’s nearly impossible to unwind a huge position like this when prices are already plunging.

Ok, but how do we know his future steps and the next batches?

Besides, my general amusement/frustration about the media/any coverage of WB is like what he does, or guessed what he does, is the right reality but just often the market is wrongly not cooperating. Like a cult ;)

biker, what exactly is your thesis? that valuations don’t matter? that 65 p/es are all fine and dandy, and that we should cheerlead for 80 p/es?

Not my point.

Just the reality is at it is. No morality, involved, just numbers. The only game is how we respond to the reality.

We just guess hoping to catch the reality.

That is the best stock market strategy.

It goes against everything in your fiber of being to sell as a greedy human.

Then buying when there is blood in the streets is against the mental grain.

You sound triggered. I mean I’m excited the market it up too. But do I think it’s rational? No. I just hope it stays up until my stock based comp vests this year and I can sell. Here’s the difference – I’m excited to make money off this market, but I also know it’s total bullshit.

my feeling too. i have very little confidence the bubble will be maintained by the time i actually need the funds.

once it pops, the value is gone. that’s the problem with bubbles. easy come, easy go.

Who’s right?

Who’s wrong?

Who cares if you have profits in cash and a Mai tai in your hand on a beach.

I’ll also add – there’s nothing politicians like more than being the hero. If there’s a time for a recession, it’s 2025 when it came be blamed on the predecessor administration. I’m not saying they can cause a recession exactly, but the only reason we avoided on thus far was the gov’t spending propping the economy up to avoid a recession going into an election season.

If recession is inevitable – you do one of two things, let it happen in 2025 or spend your way through until it’s someone else’s problem down the road.

It’ll be 2026-27.

Do some good ol Corp tax cuts to “stimulate things”.

“Water yachts are so 2017, we need yachts in the sky!” – Young Executive overheard in 2026

“….if, as WR mentioned in his article, 5% 10-year treasury rates are realized (and then subsequently increase from this point), there’s going to be a collision that needs to be sorted out in the markets. WR has clearly documented this is already occurring in the residential real estate market as higher interest rates are killing demand. The solution, as noted by WR is simple. Lower prices.

We’ve already seen significantly lower prices realized in CRE (especially office) with weakness in prices beginning to show in residential real estate markets. Bond values/prices are now under pressure (especially the long-end) so it would appear that the stock market is the last one to get the message (which is usually the case).”

INDEED!

Quote from Trading Places maybe? Randolph Duke “If Mr. Beeks does what we paid him to do, we should have a very happy New Year”, Mortimer Duke “Indeed”.

Indubitably!

All tweaks, twiddles, and toying with economic inputs, outputs, and impressions must be absorbed by the systems at work in the economy.

We have yet to see the end of this session of fiddling and it will take more time for it all to be absorbed. Its unlikely to be fully comprehensible before the new team starts fiddling again.

Keep your eyes on the assets in which you invest and let those determine your fear and invest accordingly. Everything else is noise.

Seems like we are heading back north with long interest rates. What will the FED’s next move be with fed funds rate cuts?

Will they just blow this situation off as a one time event caused by election afterbirth or start raising rates again in anticipation of rising inflation?

Or will they just sit tight?

“Long-term Treasury yields (esp. 10 & 30 years) move with inflation expectations and supply expectations (funding of government deficits). Lots of inflation and lots of supply is a toxic mix for the bond market. ”

Wolf, based on your statement the only way to suppress the long end is for the Fed to go back to QE (as before). The balance sheet is at 7.5 trillion. How much room do you honesly think is left for another round of QE before the whole thing might potentially blow up for US debt?

I believe you mentioned the balance sheet would settle around 5 trillion, but I wonder how high it can go before serious dislocations.

“the only way to suppress the long end is for the Fed to go back to QE”

NO, that’s perverted wishful-thinking BS. Because under QE NOW, inflation would completely blow out, and then you have 10%-plus inflation and an economic and political nightmare. Americans HATE HATE HATE inflation. EVERYONE knows that except you?

Rising long-term yields will tamp down on inflation, that’s what is needed. And it’s what is needed for Congress to start dealing with reality. It’s a good thing, it’s what this nation and economy needs.

Apparently Americans abhorrently despise egg and milk prices to rise.

If that was not obvious, at sunrise today it was.

sobering

Apparently they hate insurance premiums spiking 40%, all services going thru the roof, real estate and rent becoming ridiculous. I think it might be a little more than the price of eggs and milk.

Yeah, grimp, they hated the people who brought them 5% inflation and voted for the guy who is going to give them 10% inflation!

Yeah it’s the Egg and Milk prices that are keeping me “trapped” in my home that I purchased in 2018 without any hope in site of ever being able to afford even a SIMILIAR home somewhere ELSE, unless my income magically doubles

i see little evidence that his proposed policies would cause 10% inflation, even if you accept that he could get them through congress.

NASCBD,

Why did you buy if you weren’t planning on staying put? That’s what renting is for.

Think of housing like bonds: as long as you can buy and hold till maturity, you won’t lose money. But if you sell early, you might.

If only day Americans would realize or that it’s the politicians from the party they vote for, not just the party they vote against that are a big cause of inflation. But I understand it’s normal for younger people, which was also my case when younger, to not be aware of govt overspending. And I guess maybe a some of older folks, nothing against age because I’m over the hill, are aware that theyre party overspends too, but will still vote for them instead of libertarian policies that would go after inflations root causes.

The Fed won’t need to suppress the long end as long as there’s an orderly rise in yields. And if yields spike, they have other tools to deal with it.

Lack of demand for Treasuries is a self-solving problem because eventually the yield goes high enough to bring back demand.

All the FED has to do is activate monetarism. As Dr. Milton Friedman posited; From Carol A. Ledenham’s Hoover Institution archives: “I would make reserve requirements the same for time and demand deposits”. Dec. 16, 1959.

Link: Fiscal Dominance and the Return of Zero-Interest Bank Reserve Requirements (stlouisfed.org)

“imposing high reserve requirements for zero-interest paying reserves may seem quite attractive to a policymaker interested in reducing the inflationary consequences of fiscal dominance.”

The only tool at the disposal of the monetary authority in a free capitalistic system through which the volume of money can be properly controlled is legal reserves.

The first rule of reserves and reserve ratios should be to require that all money creating institutions have the same legal reserve requirements, both as to types of assets eligible for reserves, as well as the level of reserve ratios. Monetary policy should limit all reserves to balances in the Federal Reserve banks (IBDDs), and have uniform reserve ratios, for all deposits, in all banks, irrespective of size.

What in tarnation did I just read?

“What in tarnation did I just read?”

Well before keyboard jockeys there were these thick books called Noveld, which are the essence of a genius’s whole working life.

In today’s society they would: “make brainy hurt. Need Joe Rogan to tell me how to think. Woman where is protein shake?”

😂

Novels*

Mr Market must be confused by all the disinformation.

Mr market was always crazy.

1M QQQ is giggling.

problem is, trump’s proposed policies, leaving aside whether he’ll be able to implement them or not, would benefit u.s. manufacturing, which is good.

what percentage of the s&p is bigtech? remember, he sees them as the enemy. i could see him trying to neuter them.

You forgot the second part “would benefit U.S. manufacturing, at high cost to the U.S. consumer”. I can only imagine, if Trump announces 60% tariffs on Chinese goods, your average U.S. consumer walking into a Walmart and seeing prices on many items jump by 60%. If you think there was inflationary backlash this time around, try that one. “Oh, but it benefits U.S. Manufacturing – who will now make the same Chinese widget for only 30% more than before!”

Election promises are easy to make, hard to keep.

That’s not how tariffs work. That 60% is not on the retail price. That 60% would be applied to Walmart’s product COST, not including transportation. When Walmart buys containers full of T-shirts, each T-shirt might cost Walmart $1 in China, and that’s what that 60% would be applied to, so 60 cents per T-shirt. Walmart might normally sell that T-shirt for $9.99, and so now it has an additional cost of 60 cents. Can it pass all of it on and price the T-shirt at $10.59 instead of $9.99 without losing sales? Maybe.

With cars, the answer is no, because all major foreign and domestic automakers manufacture cars in the US, and so importing cars from China with 60% tariffs (at import cost) will likely make them noncompetitive, and the automaker either eats the tariff (tax on their gross margin) or they lose the sale.

Tariffs have two purposes: collecting taxes from foreign producers and US importers that they may or may not be able to pass on; and two encourage buyers to buy from local producers because these produces are more competitive.

@Franz

As nearly all raw materials (other than petrochemicals and steel) are imported how will a 20% or 60% increase in the raw materials inputs help exporters?

Google What percentage of the US economy is exports? and you get “U.S. exports represent approximately ten percent of its GDP, which amounted to about 3.01 trillion U.S. dollars in 2022”

So our exporters have to pay tariffs on materials which are then exported? How does that help us be competitive? How does that help manufacturing?

…hm, in a way, settlement of the recent longshoreman’s strike might be considered a U.S. ‘self-tariff’ (and, if the incoming administration and a certain tech-titan adviser don’t make good on their avowed labor-suppression proclivities in concert with the envisioned return of manufacturing to the nation, there will be more of those ‘self-tariffs’ (successful wage-increase actions) arising from the work force in order to secure some chunk of this excess liquidity that we’re now and future swimming in-at least among labor that can run faster than automation and AI…).

may we all find a better day.

Annuities are about to start looking very interesting.

They’ve been interesting for the last couple years.

Another great point. The payouts on those are tied to long term rates too, higher the better. The comments have been enlightening about the benefits of long term rates rising. My biggest takeaway: we are simply normalizing. It’s been so long we have all forgotten what that looks like.

Can anyone explain why there was an overall decline in yields between July 2024 (Gold) and September 2024 (Blue)?

Also, did the inverted yield curve also steepen during that time and if so, any ideas why? It looks like it did a bit based on the graph.

Bond traders positioning themselves for Fed rate cuts.

Nothing goes to heck in a straight line, as Wolf says.

“why there was an overall decline in yields between July 2024 (Gold) and September 2024 (Blue)?”

Because markets were pricing in a gazillion big fast rate cuts to respond to a crashing labor market and inflation heading to and staying at or below 2% for the long-term. Those themes have now been obviated by revised data and new data. It was a market move like so many market moves.

So investors wanted to buy up Treasuries ahead of expected rate cuts, and as a result prices increased and yields fell?

Sounds about right.

Makes sense as a reaction to Trump. Potential tariffs, tax cuts, his desire for a booming economy, a reduction in immigration, all inflationary to an already strong economy. There will be some spending cuts, but unless they’re planning on taking an axe to defense or social security spending, it’ll never be enough. Rates will have to compensate.

It’s always been sorta understood, but this is the first time a president actually claimed a dual mandate…….including the working in mysterious ways part.

I wish I could link the Barry Goldwater “Mark my words….” quote.

Social security does not drive the deficit. It’s funded from a separate payroll tax. Maybe you meant social program spending?

Cole – the Executive and Congress, given their recently-granted SC-hall passes, could find the way to raid Social Security-they’ve done it before…

may we all find a better day.

we haven’t even seen the updated mortgage rates for today. they will be significantly higher than 7.13%, i know because the 10yr was up quite a bit and the national mortgage rates avg gets posted at 4pm eastern.

If rates don’t start moving down quickly. we are going to see a complete halt in construction for residential and for multifamily in the sun belt. we already have declining rents and building inventories.

last 2 recessions began with construction layoffs spiking if I remember correctly.

I don’t agree with this.

Higher rates are not the problem but the higher prices are.

Prices need to come down a lot and builders are bringing it down in various ways and still making tons of money.

I definitely agree. Even small landlords like myself have seen income jump with rents and now we need to do something with the cash. Maintenance costs are real, but commodities are cheap (relative to the COVID times) so picking up another rental, or developing another property is also a possibility. With cash, mortgage rates are irrelevant and there is plenty of cash sloshing around right now.

Having said all that. Get your projects done ASAP, because that cash will drive inflation as it gets deployed.

Yes, prices need to come down, or rates need to move lower, or some combination of the two. Its all about affordability. It is clear, based upon increasing inventories, and based upon a 40yr low in mortgage originations, that the combination of prices/rates relative to incomes is in clear bubble territory.

I was wrong. They released the daily avg rate way ahead of time. Also, based upon the move on the 10yr treasury I would’ve expected a higher mortgage rate, spreads must’ve tightened a bit, even though 10yr went markedly higher.

Really glad to see higher rates on longer term bonds, way overdue. Great job Fed with the counterproductive rate cut in September /s

the idiot conspiracy theorists said it was to help get kamala harris elected. if that was the goal, it failed obviously.

yeah, because cutting rates close to an election with all the stellar economic numbers that were being reported made “apolitical” sense. LMFAO!

they wanted to please wall street. not please harris.

After the Trump victory, it’s very likely that the Trump Admin will run some version of the Shock Doctrine here in the US. If you are not familiar with Naomi Klein’s work, please get a copy and read it.

DD – quintuple-check.

may we all find a better day.

That was SOMA’s T-bills in O/N RRPs that funded the federal deficits since 2022. We didn’t have a recession in 2024 because of the infusion of cash. Now that’s exhausted.

That’s what QT does. So ON RRPs are nearly exhausted, but reserves are still plump. And they’re next.

Ben Bernanke drained reserves for 29 contiguous months. But he didn’t offset the decline in the velocity of circulation.

So far, in C-19, the nonbanks have outbid the banks for loanable funds. That has temporarily, kept things going.

Non-Bank Financial Institutions’ Assets to GDP for United States (DDDI03USA156NWDB) | FRED | St. Louis Fed

TLT to $85

R2K to 2750

Get er done!

Look out below!

1:04 PM 11/6/2024

Dow 43,729.93 1,508.05 3.57%

S&P 500 5,929.04 146.28 2.53%

Nasdaq 18,983.47 544.29 2.95%

VIX 16.27 -4.22 -20.60%

Gold 2,668.00 -81.70 -2.97%

Oil 71.85 -0.14 -0.19%

Haha gold got crushed.

Wolf, what’s your long term view on the housing market? I’m not sure what to do because Trump has said he will fire Powell and that he’s a “low interest guy”… are we looking at inflation part 2 in a year?

If inflation takes off again, mortgage rates might go back to 10%+. Some of us are still remember them. 10% mortgages mean much lower prices. Trump needs to be careful here. My base-case scenario is that Trump will be reasonably careful when it comes interest rates and inflation. He understands that Americans HATE HATE HATE inflation. But I could be wrong.

Americans may Hate inflation, but they may be on the verge of getting a heavy dose of it in the very near future. JP is going to cut rates and expand the money supply in order to keep the economy from collapsing like a house of cards. Look for the 10 year to go above 5% and mortgage rates to bust through 8%. We’re so busy because of the FOMO panic to get deals through before the next mortgage rate increase.

Agreed. There were many issues this election but inflation was the elephant in the room. It’s the ultimate tax.

I guess we have to make a bet on whether Trump will be reasonable or if he’ll just print his problems away with a new Fed chief and debt. Last time he inherited a decent economy but this time it’s so difficult … I can think of plenty of ways the economy can go haywire but not many ways it can remain strong with moderate inflation. This is his second term, he has no plans of re-election. We are screwed aren’t we?

The market was up 1200 before the open? What a joke. Must of got Buffet up early to start selling again.

Wouldn’t it be that people bought the market?

To make it rise and all.

Think of adding water to the ocean. It rises

Also the potential upside increased. Analysts expectations of the future ceiling the market will top out at.

The Canadian real estate industry is waiting on 0.99% 3-year variable mortgage rates again.

Canadian 10-year bond yields are lower than more than 100 bps compared to the United States by the way…

Trump’s win was probably a good thing for the markets — but not for the deficit. He’s going to cut taxes but be unable to hack at spending — the bane of any Republican administration.

“5% here we come?”

If only.

Musk will head a new cabinet position, on Government efficiency. His initial target will be to cut 2 trillion dollars from the federal budget for starters. Millions of federal workers/contractors will be given pink slips, especially those deemed non-essential. The entire Dept of Education will be eliminated.

Those hot dog vendors in the Federal Triangle who thought business was bad during the work a home spree during/after the pandemic ain’t seen nothin yet.

Musk cannot cut any spending. That’s not how the US system works. Congress has the power of the purse. Musk has to cajole Congress into passing appropriation bills that are lower than prior appropriation bills, or bills that repeal bills that fund stuff. It’s Congress that decides what gets spent on what and when. The president signs the legislation, and then the executive branch has to implement it. The US is not Twitter.

If Trump controls Congress then Musk gets his cuts. No?

“Bring home the bacon” is the fundamental rule in Congress. Each representative must bring home the bacon, meaning federal money to their districts. 75% of the CHIPS Act for example has been awarded to manufacturing facilities in red districts. And those Republican congressmen are going to make sure that this CHIPS Act money keeps flowing. It’s the same thing with everything. That’s why it’s impossible for Congress to cut expenses – no congressman wants to cut off the flow of money to their districts.

Trump doesn’t personally control Congress just because the Republican Party has small minorities in both houses.

Your view of American politics is overly simplistic. Musk and others have the money and Trump and others have the political power to “cajole” Congressmen to do what they want. Congressmen are bought and sold daily.

How about impounding funds that haven’t been spent? A lot of Covid pandemic money has still not been spent. Nixon did it without Congress back in 1972. I see T copying Nixon on many fronts. I heard he’s setting up a “Supercabinet” just like Nixon. The actual cabinet members will be just gophers. Remember Sec of State Rogers. Kisseneger was the real power broker in the State Dept.

yeah, like many schools, from grade school up to university, got nearly $200 billion in grants to “reopen from covid.”

They used the money to buy laptops, new stadiums, and other crap they didn’t need.

Wolf,

I recall hearing that approved funds weren’t spent at times due to inability of departments to spend the money. Does congressional approval require spending or just allow it? I think it’s the latter, but i could be wrong.

Presidents have reorganization capabilities to consolidate, abolish, create agencies and of course some of those could be targeted like EPA and rolling back regulations. All of this has to be done with some amount of legislative oversight. I think this close to the election it is more wait and see. The GOP struggles to find consensus within the house so while having a quafector is a big deal it doesn’t mean anything big will change. Likely just another 4 years of a presidency with a lot of interesting memes.

EPA total budget is $0.01 trillion.

Congress passes laws that are fairly general and set goals and guidelines to achieve those goals. The President administers those laws and has significant leeway in how to implement the law. But the President still has to meet the goal within the guidelines. That’s essentially what an “executive order” does: changes the way a law is administered. If an executive order causes an agency to no longer be able to meet the goals of a law, the executive order can be challenged in court. That happened numerous times in President Trump’s first term.

See above. The federal budget is $6 trillion. Social Security is $1.3 trillion. Medicare/Medicaid is $1.6 trillion. Defense is $0.8 trillion. Interest on debt is $0.66 trillion. Other mandatory spending (federal pensions, veterans benefits, food stamps and unemployment) is $0.9 trillion.

Everything else combined is $0.9 trillion.

What do you cut to get to $2 trillion?

Foreign aid will be cut first. If Trump imposes tariffs, I think

that would strengthen the dollar which may cool inflation.

So man moving parts…

@sporkfed

Yes, I did see the dollar strengthen today, but that is more due to the increase in treasury yields. Forigen money is attracted to higher yields.

Unfortunately Trump is on record (for whatever that is worth) of wanting a weak dollar to help exporters. No inflation help there.

1st term all the globalists were preaching about

High inflation from tarrifs.

BLS charts on imports are better than the rag sheets. I would expect a repeat of china and europe devaluing their currency.

BYD break ground in Mexico yet?

Foreign aid is $0.06 trillion or 1% of the total. What else?

Past performance is the best predictor of future results.

America is very fortunate to have Elon volunteer to tackle the bloated Federal government.

Elon couldn’t figure out how to make an affordable EV, so he pivoted to making a robotaxi that may or may not ever see production. And he desperately needs tariffs on inexpensive, high-quality Chinese EVs in order to save Tesla from being competed out of existence. Trust in Elon at your own peril.

$35,000 isn’t an affordable EV?

My neighbors have TWO Teslas and BOTH of them are cheaper than my Hyundai

I think the point was that if China was allowed access to our markets with either low or no tariffs we would be looking at 20-25K EVs. The EU already has combined tariffs of 45%. Currently their prices are higher in EU for other reasons as currently too risky for China to establish factories given much of the demand is incentive driven and risky and expensive to build. BYD Seagull is very affordable in Canada for example.

I don’t honestly have any idea what will happen or where the market is going. Could be that battery cars get overtaken by hydrogen or another technology in a decade or so.

“Fortunate to have Elon volunteer to tackle the bloated Federal government”

Hasn’t Elon been sucking off Federal government contracts for the last decade? What am I missing here. That seems to be like putting Count Dracula in charge of your blood bank. Or maybe its a good move. Like hiring a criminal scam artist to counsel people on securing their bank credit cards.

Exactly.

Elon is the perfect person to pull up the ladder behind himself. He knows exactly how to milk Federal programs and he can make sure others can’t do the same.

Yeah shame on him for taking the governments money and doing something with it like build rockets to send to Mars.

What we SHOULD be doing is using that money to build more rockets to send to UKRAINE, more handouts for illegal immigrants, and we definitely need more money for bailouts

The best hackers, criminal and otherwise, are hired by companies to devise ways to prevent their company’s data from being hacked. It makes sense to hire the experts, except when those experts start hacking your company from the inside. It’s that old problem, “who is going to police the police?”

Will the mobility of homeowners be restricted due to the higher-for-longer mortgage rates?

Already is.

There is no “will”

People are trapped and will be trapped.

I’ve already been in my current home for 6+ years

Under a normal business cycle, wages would have gone up and a recession would have happened by now, enabling me to “upgrade” my starter home, after doing what I was “supposed to do”

Namely, work hard, pay down my mortgage for 6 years, build equity, survive through the inflation until my wages increase, and then I’d be “rewarded” for my amazing participation in this capitalist society, by being able to “upgrade” upon my first purchased home.

Where that would have been to get a larger home in a similar neighborhood, move to a smaller home that has more amenities, what have you, then MY HOME would become someone else’s “Starter home” and the cycle continues

Instead I’m going to be “stuck” in this house I purchased in 2018, for the next three, four, five years, until things finally “reset”

There is NO OUT of my current situation unless my income magically doubles

I enjoy your sarcasm. Would be nice if there were alternative models but appears we are locked into this one. I opted out of moving to Portland from California, which was probably for the best in the long run. I think often it isn’t that we would do something but we often like to think that is at least possible. Much of the possible has disappeared for many

My first starter home (800 sq feet) was purchased with the intention of staying 3 years and moving. Paul Volcker raised mortgage rates to 18% and I was locked in. I stayed 22 years.

Seems like you came up with a story about being entitled to something. Since when is it a given to upgrade houses every 6 years?

When those 6 years have come after 11 years of QE and almost 0 rates, these six years were supposed to contain a recessionary period.

We printed our way out of that

Hasnt your home appreciated a lot in those 6 years? Couldnt you sell for a nice gain, then rent a frugal place until the correction finally happens or do you not have a lot of equity in your home even with prices in a lot of places doubling in that time?

The problem is with a 30 year mortgage the first 10 years or so are almost all interest unless one has paid a bit more on principal thus 6 years is not an equity builder.

Oh yesss, housing prices have gone up. Mine has more than doubled since I remortgaged. Unfortunately so has everyone else’s house, so I would just move from one old starter home to another old starter home. Why even consider that when one is retired and on a fixed income?

(f) elon musk joining guvmint reminds me of Rexx Tillerson. One can draw their own conclusion on how it will turn out in future. More to do about his tax incentives then reducing expenses, imo.

CJ

Here, I fixed it for you:

Past performance is the best predictor of future results.

America is very fortunate to have Melon Husk volunteer to tackle the bloated Federal government.

/sarc