Fewer workers quit (rattled by layoff headlines?), so fewer vacant slots to fill and less hiring. But actual layoffs are at historic lows.

By Wolf Richter for WOLF STREET.

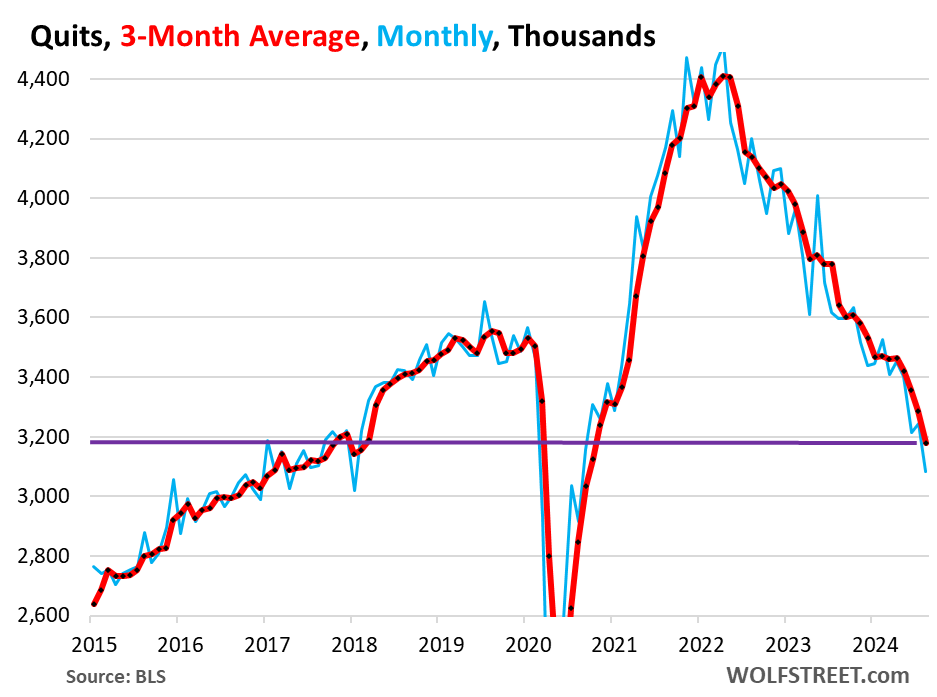

Powell talks a lot about the balance in the labor market, about job openings, quits, layoffs, and hires – and we got the latest data today. They depict a labor market dynamic where workers hang on to their jobs rather than looking for the greener grass on the other side; they either got scared by all the layoff talk as employers re-exert control they’d lost during the pandemic, or they’re happy where they are, and they’re just not quitting anymore, and the number of quits plunged to the lowest level since early 2018.

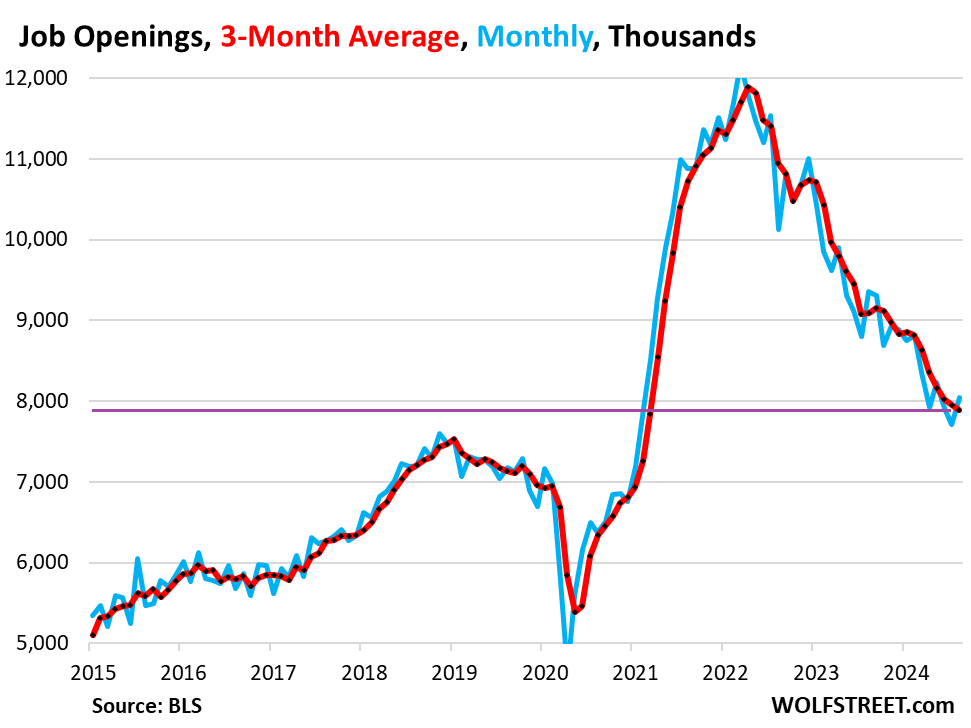

And because fewer workers quit, there are fewer empty slots left behind that companies have to fill, so fewer job openings – though they remain historically high – and less hiring.

In other words, the historic churn in the labor force during the pandemic has calmed down, while layoffs and discharges remain at historic lows.

But in addition, and disconcertingly, creation of new jobs has also slowed down dramatically – which came out in the data and revisions last month. So we’ll start at the beginning:

Workers quit quitting. Voluntary quits fell to 3.08 million in August, the lowest since January 2018, according to the Job Openings and Labor Turnover Survey (JOLTS) data released today by the Bureau of Labor Statistics, based on surveys of about 21,000 work sites.

The three-month average fell to 3.18 million, the lowest since March 2018. The huge churn during the pandemic, when workers jumped jobs and industries to improve their lot, thereby driving employers nuts and triggering the biggest pay increases in decades, has settled down.

Fewer voluntary quits mean fewer newly open slots that have to be filled, so fewer job openings, and fewer hires to fill those openings.

For employers, this is a huge accomplishment. They have been able to re-exert control and clean out the deadwood. Pay increases have moderated because employers no longer have to poach each other’s employees by offering better pay. Productivity rises when workers stay longer and learn the ropes, which has been helpful for employers.

So fewer job openings to fill, after workers quit quitting. The number of job openings in August rose to 8.04 million. The three-month average, which irons out the month-to-month squiggles, dipped to 7.89 million, the lowest since March 2021.

This number of job openings is still historically high, and would be a record in the data except for the pandemic, but it’s way down from the pandemic’s churn.

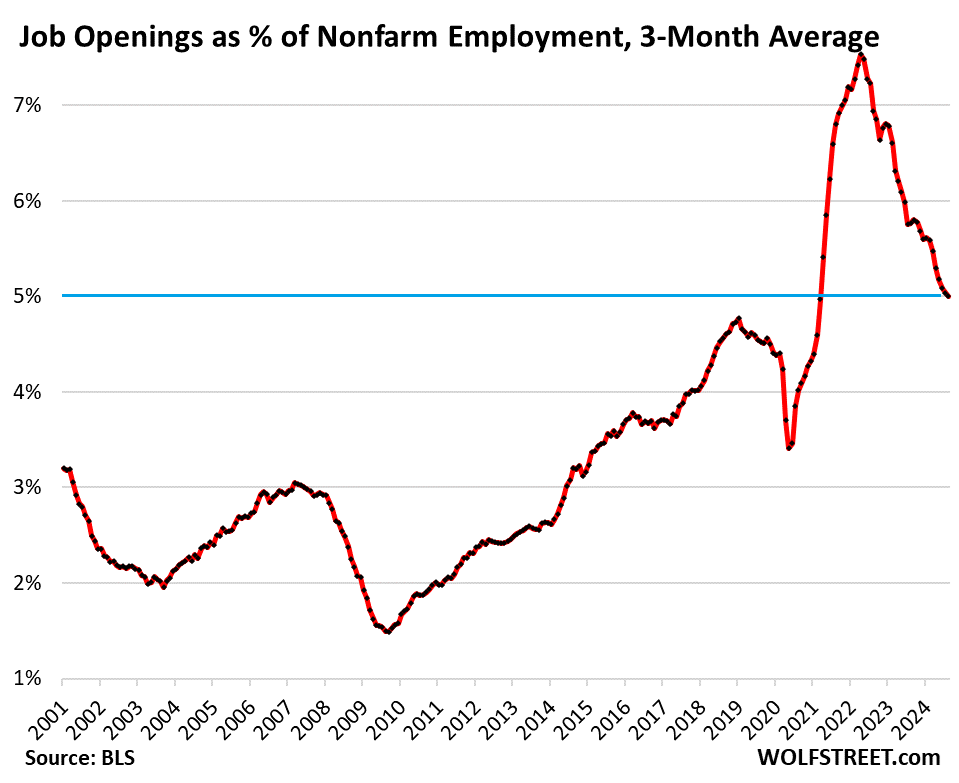

Employment has been growing over the years. So in relationship to nonfarm payrolls, the number of job openings is historically high, and still above the pre-pandemic record of January 2019.

In August, the three-month average of job openings was 5.0% of nonfarm payroll, still above the prepandemic record in January 2019 of 4.8%. At the peak before the Great Recession, it topped out at 3.0%.

But this trend needs to start flattening out pretty soon for the labor market to remain healthy.

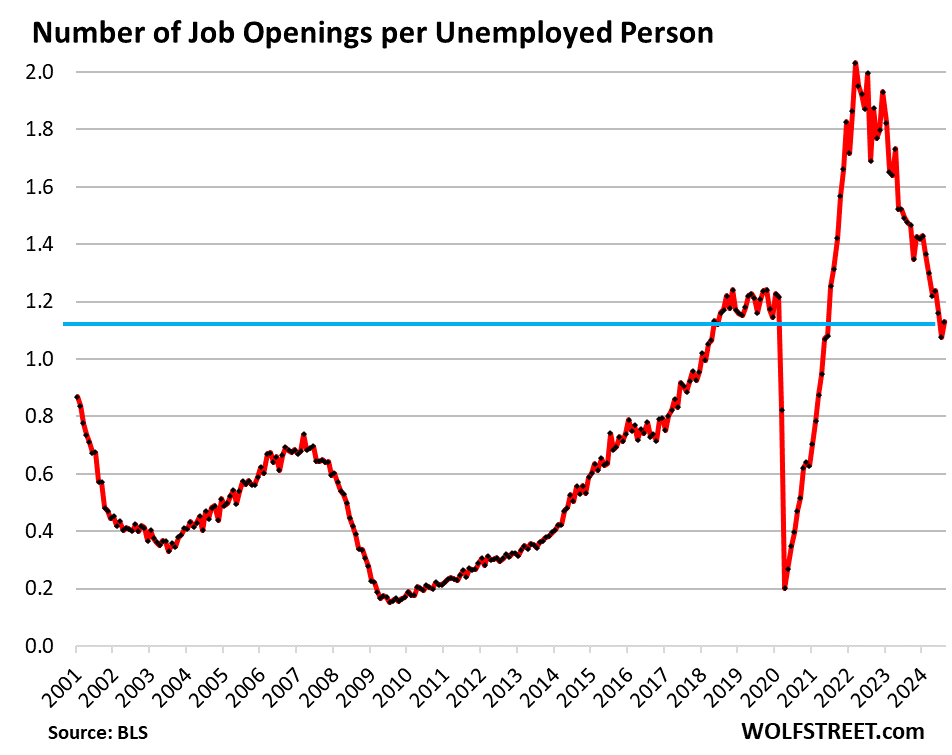

The number of job openings per unemployed person – another ratio that Powell cites a lot as one of the indicators of labor market tightness – remains above 1. In August, it ticked up to 1.13, meaning there are still more job openings (7.89 million three-month average) than unemployed people looking for work (7.11 million).

While relatively high, the ratio is lower than it was during the hot labor market in late 2018 through February 2020, which was one of the reasons Powell cited as sign of a labor market that is become less tight, and that the Fed doesn’t want to loosen further – hence the 50 basis-point cut.

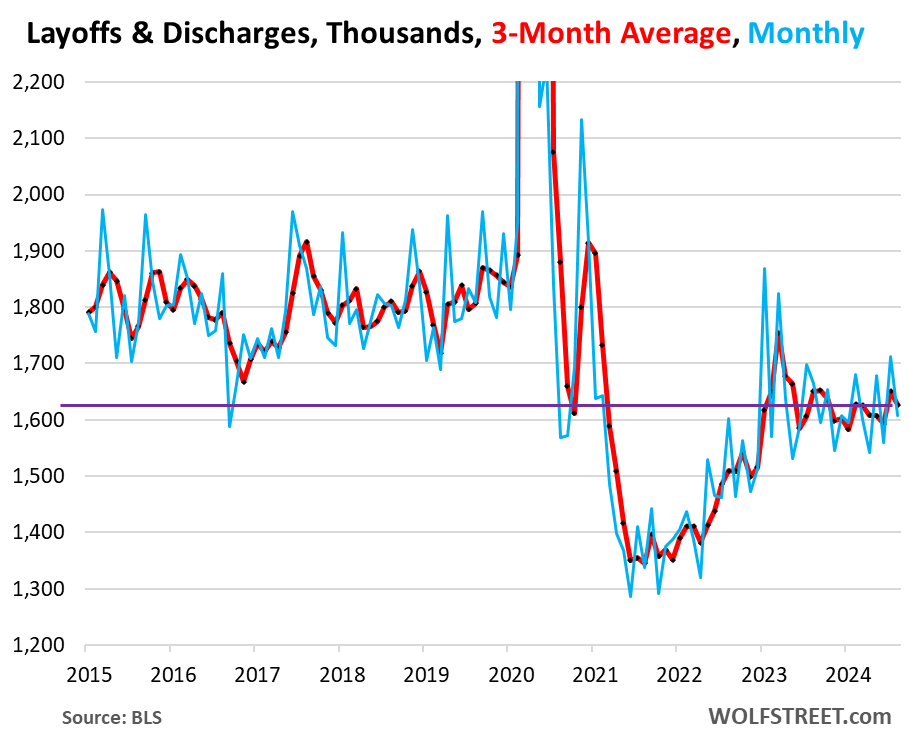

Layoffs and discharges fell to 1.61 million in August, and the spike in July was revised back down, so the three-month average dipped to 1.63 million. All of these numbers are historically low – meaning employers are shedding people at a rate that is much lower than during the Good Times before the pandemic.

Companies are hanging on to the workers they’ve got; workers aren’t quitting; so there are fewer slots to fill, and fewer job openings, and less need to hire in order to fill those fewer job openings. This is the picture of a labor market that has settled in after huge turmoil during the pandemic.

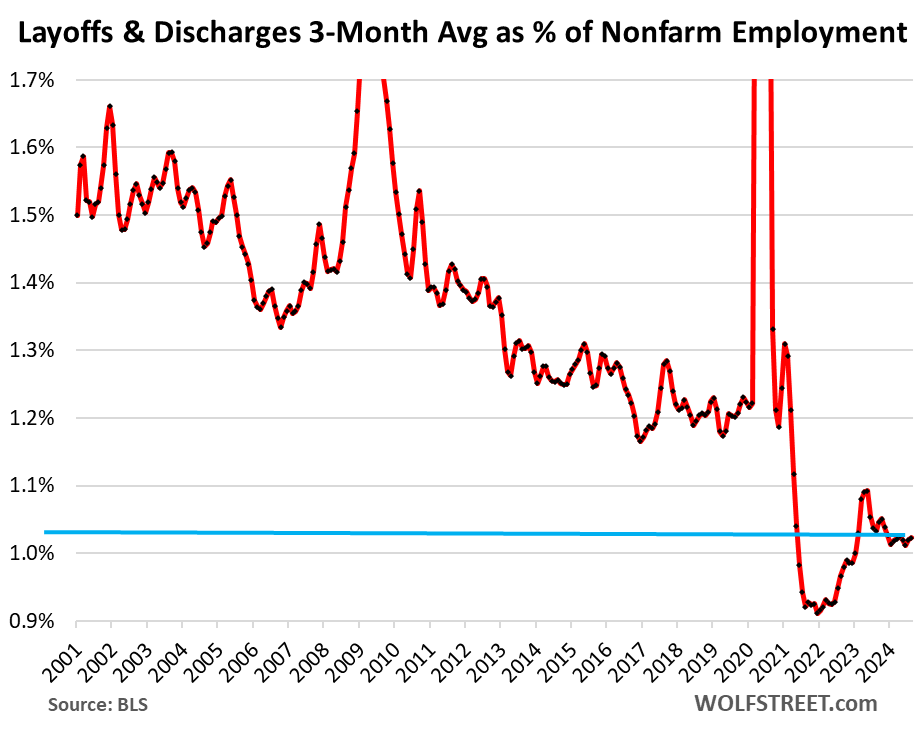

Layoffs and discharges in relationship to nonfarm employment – a ratio that accounts for growing employment over the years – shows this trend even more forcefully.

Layoffs and discharges were just a hair over 1% of nonfarm employment over the past several months (1.02% in August).

There have been speculations around here at the shop that employers are clinging to their staff because they got burned by the labor shortages after the pandemic when they couldn’t easily rehire the masses of people that they’d let go in the early months of the pandemic. And we speculated that maybe employers actually learned something about the value of retaining talent – and that would be a good thing for everyone, including employers.

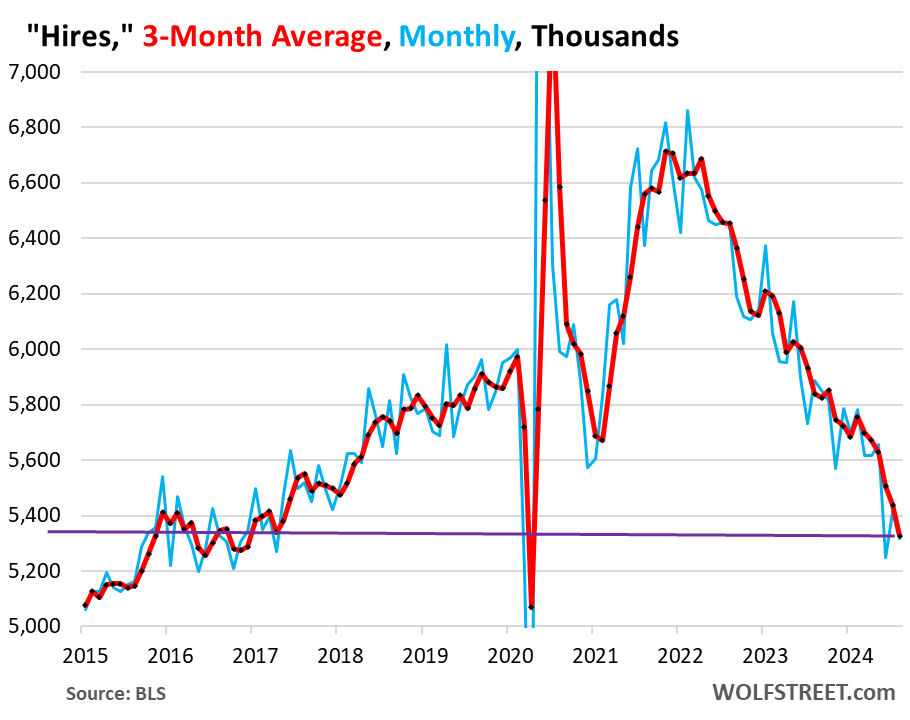

Hires dropped to 5.32 million in August – down from July, but up from June. The three-month average dropped to 5.33 million.

Fewer quits and historically low layoffs and discharges as employers hang on to their workers mean fewer job openings to fill, which means less need to hire.

But an additional and more disconcerting reason is that employers are creating new jobs at a slower rate than during the Good Times before the pandemic. The deterioration over the past three months was one of the factors Fed speakers cited for the 50-basis-point cut.

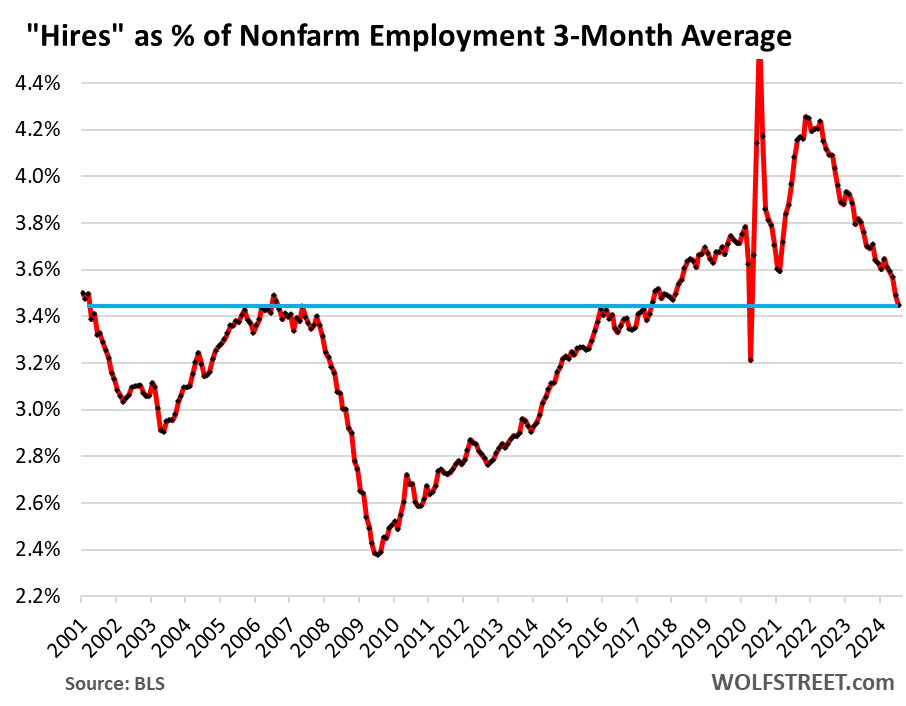

The ratio of hires to nonfarm payrolls dropped to 3.4%, below where it had been in the 2017-2019 years, which were considered a tight labor market (amid Fed rate hikes and QT).

So the labor market has settled down, and fewer people quit, requiring less hiring; but in addition, employers have slowed creating new jobs. And we can see that here too:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The balance of power is shifting…Amazon already fired the first shot of 5 days back in the office, expect many if not all eventually will follow IMHO. Crazy how this is all before any sign of a recession, imagine how much more big corp America will push for if we experience another 2008..

To the many who think remote or hybrid work is forever a thing…this is what over-optimism looks like..buy a house in Boise at work remote collecting a fat salary because what happened in a year or two will somehow extrapolate into being the future forever…that’s a funny one..

Yep, a few folks in my neighborhood that were “working from home” are now getting up and driving to the office in the early morning rather than to the golf course for an early tee time. One heads out before 6:00 AM!

Early bird gets the worm… At 6AM roads are actually already quite busy in Chicago, so maybe that’s the reason.

And soon we will hear complaints how people have to sit in traffic for hours each way, because they were working remotely and bought a house far away from physical offices.

I am sure Chicago is bad but you know what to know what real hell looks like? Try LA’s 405, 91, 101..etc. Probably the worst in the world maybe outside of those insane traffic pictures you see coming out of China (not sure how real they are)…here’s a data point for you. I can leave at 6 in the morning from Long beach and to drive into West LA will take an hour and a half on a normal day…one traffic collision, you’re looking at 2hrs probably…

Can’t wait until this becomes a 5 days a week or more event…4 hours are gone each day….tempting to drive my car straight off the overpass…

I met my wife for dinner at a Japanese restaurant here in SF in the South of Market area near the Salesforce tower. I was on foot — thankfully because the downtown era was gridlocked. Throngs of people on the sidewalks. She drove up from Silicon Valley, got stuck in traffic, and was quite a bit late. The Dreamforce event was going on. It was just total chaos.

In the general area I live in many leave for work at 4:30am to make it for 8:00am.

I DID “work from home” sorta sometimes when parking my bread van in the company lot. I lived in that around 4 years, but moved around a lot….friends homes, apts, etc. Ran extension cord where I could for heat and used their toilet for #2….#1 went don tube into street.

Police left you alone back then, even when I lived in my 67 Chev truck, not like today.

Also far fewer little “factories”.

Did manage retire at 55 to work on off-grid home/84 acre ranch…..actually started living almost full time up there at around 50 and commuted 75 mi…..stayed at sisters if too tired sometimes.

Since 1969 I have always been what is known as an “Industrial Shitworker” ( even have union t-shirt art dept drew and had made at one place.

Anyway, it means you are minimum wage or a bit above and when someone asks you what you do for a living it is very difficult to answer.

Anyway my point is that ALL these people started work (and still do) at 7-7:30.

9 to 5 is just a song….and flex time is a pipe dream. Clock rings strictly enforced, so, often there is a line at time clock. We often quacked in line.

These are preferred hours by such employees as they had time to get things done at banks, etc, after work.

Needless to say, nobody knew what a “tee time” was or could afford to play golf. But there was generally a BB hoop set up somewhere in the industrial areas these small companies were found….maybe even a VB net for breaks, lunch, and after work.

I doubt this is widely the case: “work remote collecting a fat salary”

I am employed by one of the FAANG companies, and salaries depend on COL (“cost of labor” not “cost of living”), so if you move to a low COL area then you will earn a significantly lower salary than someone in a medium or high COL area.

For example, an employee in a high COL area will have a 15-20% higher salary than an employee in a medium COL area working on the same product under the same manager at the same technical level.

My company does a similar thing however they don’t do salary decreases if you move. Just had a coworker move from Santa Barbara to somewhere in Arkansas. He is probably rich in Arkansas.

Speak for yourself. I work for a company that’s almost entirely remote. Every one of my 8 member team is in a different city and the head office is in Atlanta. ~800 person company and less than 100 actually live in Atlanta. I’m not planning to leave any time soon that’s for sure.

I work for a healthcare organization that is located in NYC, but has hybrid and remote workers (me be remote). Hybrid and remote positions attract good people. Watch Microsoft pick off people from Amazon (especially good technical people in AI and the Cloud space) because of RTO. And yes I work from home so no commute for me :-). I am staying with this position until I have enough to retire in 2 to 3 years.

Yeah it will be interesting to see how this plays out. I’m fully remote for now, but if you’re near a designated hub (I’m not) you’re supposed to be hybrid. That being said it’s been 6 months and they still haven’t gotten office space for half their hub cities. We’re tech but not FAANG so I think they’re waiting to see how this plays out. I think a lot of these 5 days a week companies will lose a lot of talent to those who offer remote.

Similarly talking to a friend who’s a recruiter in the accounting space candidates are telling her they’ll take a pay cut for fully remote. And clients keep being surprised when a candidate has more than one offer and one is remote and one is not remote – the in office client tends to lose regardless of pay or prestigiousness of the day.

The thing is no one wants to spend 2+ hours commuting each day.

Personally I think this a great strategy though to get people to quit versus having to due layoffs if a company is overstaffed. If they actually need to keep their employees it’s a terrible strategy.

This also gives tier 2 and 3 companies willing to offer fully remote an easy way to attract talent that they might not have had a shot at previously.

*prestigiousness of the company.

My phone’s desire to autocorrect everything has gotten out of control

Here is a Novel idea, move somewhere that’s not souther California. That would probably be easier then offing yourself. Just a thought,

It is widely believed that the Amazon RTO announcement is part of a workforce reduction plan for 2025 (featuring among other things slashing middle management). It’s a slim reed upon which to hang a broader claim about the future of hybrid work.

Hybrid work was already happening for years — the pandemic merely accelerated its adoption. Successful companies are going to identify which roles suit which layer of the remote to on-site spectrum and arrange themselves accordingly. 2019 is never coming back no matter how many corporate dinosaurs roar for its return.

Productivity tidbit as perspective:

“ George Pearkes at Bespoke Investment Group said right now, there’s already a lot of investment in advanced manufacturing. Think: electric vehicle batteries, solar panels and semiconductors.

In other words, valuable products that don’t require a lot of labor.

“If you’re producing a lot of stuff, and it doesn’t require a ton more hours to do that, that’s going to mean everybody is better off ultimately. Because there’s more income flowing around, it means that we have a higher standard of living,” Pearkes said”

Add on to that, with people being laid off who are becoming pizza delivery entrepreneurs and the vastly growing gig economy that chugs along with creation of mini jobs

“Add on to that, with people being laid off..”

RTGDFA. Layoffs are at historic lows.

Even the guy you cited wasn’t talking about layoffs, but about NEW high-tech manufacturing plants being created that require fewer NEW jobs.

From what I see in manufacturing – many employees now work less hours (no overtime and some only 32hrs), which could explain the low layoff figures if the trend follows in other industries. This helps employers with salary expenses as well as finding and training new employees.

They’ve begun that in retail. You have a manager and a store lead with 2-3 other full timers. The rest are part timers.

My experience is that many companies are bringing employees back to the office but with worse effects. Many places downsized space and got to hotelling. What this means is you commute to work, pay for parking, and then simply dial into meetings and for collaboration. This just pisses employees of as if you can’t reap the benefits of in person collaboration, which I think for many things is important, then why bother?

5 days a week does seem like a solid strategy to reducing the workforce and not having to pay unemployment. Big downside is might lose employees you don’t want to. I’m still 100% telework so hoping that continues. Really hard to imagine and more than 2 days a week. After over four years of 100% this is my new normal.

Exactly. The good people that want to stay remote and can get another remote job will leave. The ones who want another remote job but cant get it will stay but they will be looking at the door all day. The rest will stay busy distracting you with stories about their cat.

I left my last company when they started to RTO. Productivity dropped about 30-40% once we returned and overall morale nose dived.

Any idea of how many of “the quitters” are late boomer retirees?

Zero. Retirements are not in “quits” but in “other separations.”

I looked at the data collection form the BLS uses on their website, and it doesn’t appear there is any guidance to respondents on what = “retirement” vs. a “quit,” so I can imagine the distinction isn’t super clean in the data. For example, if I as a fed-up person in my late ’50’s elect to leave my job voluntarily, I don’t know whether my employer will call that a retirement or a quit. Heck, I can’t even be sure which it really is on the day.

https://www.bls.gov/jlt/jltdef.htm

The labor market is cooling substantially, yet inflation still has not reached the Fed’s 2% target.

Powell & co are in a pickle.

and inflation is re-accelerating

And inflation won’t come down until yoy rent increases fall from 5.6% (as captured by the CPI). Rent is directly proportional to demands on wage increases at this point, in the current state of the economy. Inflation isn’t coming down until wage increases come down which won’t happen until rent increases come down. Everone knows that the shelter component is the root of all problems at the moment, but all government is doing is looking for new ways to push up shelter prices.

Rents are being pulled up by inflated RE prices. We need a meaningful correction in housing to bring RE prices and rents back down.

Completely agree with you but I am losing on hope will ever see this happening in my lifetime, especially in desirable areas in SoCal..

So instead, think I’ll just go doom shopping instead…more fun to look for a used Cayman GT4 or Lotus Emira than to look at another stupid $1M being advertised for sale..

So if California is so bad, housing prices are so high, you have to drive two hours to get to work that’s ten miles away, you’ll never be able to afford anything. Etc etc etc, like I said in my previous comment, have you ever consider you know, moving?

SoCal is beautiful. Weather, culture, etc. I’ve been to most other states, and none check all the boxes like CA does. If you’re making under 75k (and probably even 100k), you’re going to struggle here. But if you are affluent and have skills that are in demand (or were fortunate to get into SoCal RE when it was much lower than it is now), there aren’t many places on the planet that are better. There’s a reason why CA’s economy is bigger than most countries and collectively bigger than many other US states combined.

And the dock workers are throwing another wrench in the mix. We’ll see how that plays out.

Good. Maybe workers in “right to wok” States will get the idea of forming “combinations” as (your no doubt hero) Adam Smith said.

When I told my dentist, “You know, everyone hates you guys”, he said “Yes, we are very misunderstood”/

Same with Adam Smith….cherry picked to death.

I just can’t see why cooling from smoking hot to hot is a grave concern.

Love your data reports. Real world validation of economic theory with lags.

Classical economists made incorrect assumptions about instantaneous adjustments in wages and prices. In reality it is a process and this data shows it.

Thanks again for sharing this stuff

Who owns “economic theory” lately?

You can generalize if you want.

Nice

Home owners with low interest rates might want to stay put instead of looking for work elsewhere.

This looking for a new job thing seems quite stressful, quiting, moving, finding new lodging, new people to work with. Seems like a lot of energy…comes on kids were moving to Idaho.

One of the conditions for the dock workers strike is automation, theirs is a job that can be eliminated by the robots…I am the robot I’m here to help.

Correction for “Home toad”, it low mortgage rates you idiot.

Nice clean analysis. But confused about one thing: Number of “job openings” are considerably higher than 2019, but number of “hires” are considerably lower. What does this mean? Does it mean that companies open positions with a speed higher than 2019, but they are filling them at a much slower rate? Why?

The article explains that in detail. Start reading with quits at the top — hint: THAT’S THE KEY, which is why I put it at the top — and gnaw your way through the article bite by bite all the way down the article. You’ll get it. That’s WHY I wrote the article.

Sorry if I am mistaken. I’ve read it again and I’ve learned a lot of things. But I could not find the answer to this question. Compared to 2019, why there are more job openings but less hiring? If the companies have more job openings than 2019, it means they have more positions to fill compared to 2019. But they are hiring less than 2019. That’s intriguing.

FEWER QUITS

The whole entire article is about it, and I repeated it many times: Fewer quits means fewer newly vacated slots that need to be refilled, which means fewer job openings, which means less hiring to fill those fewer job openings.

Ponzi – It’s like the housing market. No one is selling so there is nothing to buy.

Wolf: Thanks, but that’s not I was asking. You say there are fewer quits and so fewer openings now. I am not asking why there are less openings and hires compared to pandemic days.

But what I am asking is, “There are MORE JOB OPENINGS now than 2019, but FEWER HIRES than 2019. Why?” If there are fewer quits than 2019, then, companies should have fewer job openings and fewer hires now as a result. But in contrast, they have MORE job openings than 2019 (which means they are looking for more employees) but they are hiring FEWER people. This seems like a contradiction.

One more interesting fact: It seems that actual number of layoffs is much lower than what most people think based on the headlines. Probably there is a mismatch between what is seen on media vs overall industry.

Maybe before the pandemic, the layoffs did not make headlines as they do today. That’s why many people think there are lots of layoffs. But in reality, the overall layoff volume is smaller. Indeed, most of those tech companies, which are making the headlines about layoffs, have still much larger head counts when compared to prepandemic (may be except for Twitter).

Or, those layoffs making the headlines are negligible amount in total volume when compared to overall workforce.

Employees have a lot more wage power than acknowledged. If that weren’t true, employers wouldn’t be trying so desperately to hold onto workers they have during supposed lower revenue. Look at the Boeing strike. Look at the port worker strike. Boeing is currently offering about a 10% raise a year for four years as part of that contract. Dock workers are demanding about 11% wage increase per year for six years. Employers have the upper hand on wages? Lol! Good luck.

A union is a different deal. Only a tiny portion of the US labor force is in a union. Unions have the legal power to slowly strangle an employer. If a union is reasonable, it’ll work with the company, and both thrive. But that’s not always the case. Years of union demands before the Great Recession ended up sending two of the US automakers into bankruptcy during the Great Recession, and it was in bankruptcy court that they shed some of those issues. Some point to Yellow as a more recent example of a union sending a weakened company into bankruptcy and liquidation – which Yellow’s CEO explained in detail. If union bosses want to get in the headlines and “make history,” instead of being reasonable, the worst can happen to workers and the company, though the union bosses might come out ahead. If union bosses are reasonable, all parties can thrive.

I worked for Roadway when it was bought by yellow and buried in debt. The recession killed them around 2008. We took pay cuts and they stopped paying pension contributions. Restarted at 25%. The union gave them everything to keep going although they were a zombie company from then on. For the Yellow CEO to blame the teamsters is a joke.

The business press (and their corporate ownership) is universally hostile to unions. Calibrate your interpretation of stories about unions, especially strikes, accordingly …

YES and YES!

And Wolf’s comments apply to public service unions…and the kicker, if they get big enough they become majority voter blocks

I wouldn’t like words put in my mouth, but it’s not my site.

What a timely post, in light of the longshoreman strike. Yes, as my grandfather (his business survived a great depression and two world wars) used to say; “you do everything you can to keep people who increase productivity, and are trustworthy. For everyone else, the minimum wage is zero.”

hedge accordingly

I’ll chime in as one of those job creators who is simply….not adding jobs.

The labor turmoil during the pandemic convinced us to put a massive amount of effort into three things: upskilling our talent, investing in automation everywhere it was feasible, and documenting/proceduralizing everything possible.

The net result is that going on almost 5 years of serious focus on this, we’ve just about doubled our client base and kept our staffing static. It’s taken a lot of work, but the effort is paying off:

1. Smaller workforce = easier to manage, flatter /more nimble organization

2. Fewer managers

3. Higher wages for the staff

4. Minimal HR headaches

5. Less “friction” within the organization due to less turnover/new training

6. Fewer costs related to talent acquisition, training, etc.

7. Key for us: staying below the 50 employee threshold….

We’re in technology management.

Interesting comment.

Encouraging to hear this concentrated effort working. Sometimes it feels like all efforts are futile and we managers are just along for the ride.

We are in transportation equipment manufacturing, and are banking heavily on automation to keep our American plant competitive in a global marketplace. We are welcoming our third weld robot to the line in two weeks, and making plans for a fourth. The goal isn’t necessarily to cut head count directly, but to raise revenue per employee.

The hard part in our game has been redesigning every high-volume part to be compatible with the technology. As a rule of thumb, the parts must be presented to the weld robot with a level of consistency and precision that is HALF the width of the weld wire in use. In our case 0.045” wire. There are seam tracking options available to help make looser tolerances work, but they complicate programming and severely slow down the run cycle.

After five years, our robotics effort is finally starting to hit a stride. IMO we are 5-10 years behind and desperately trying to catch up.

Is the 0.020” tolerance for placing the part or the parts dimensional tolerance (the later is crazy loose)

The rule of thumb is when a motor is switched on it draws 6 times running current. That’s why EVs can accelerate so fast…not sure about giving it back….too fast for any existing battery…needs a full blown capacitor….and a REALLY BIG one at that and in parallel to add capacity.

Nat’l Ignition Fac. has a bunch in parallel to run all those lasers for tiny fractions of a second.

Bomb testing stuff…..not a Fusion Energy break-through which was mentioned by commenter here.

In the time I worked at the USPS, the equipment I worked on ELIMINATED at least a couple hundred thousand jobs. I’m sure it is approaching a million by now. But I do NOT look at it as the goal being to “increase increase revenue per employee” It was job ELIMINATION by robots and I cop to doing it. Lot of fossil fuel burned, though, we even had so many big motors being switched off and on constantly we even had a PG&E switchyard just for our building, and with a 100Ksq ft workroom floor (not including side rooms and upstairs, just where machines except for HVAC were) we were a very SMALL P/O processing center. Pretty sure all that’s done there now is final delivery (to individual carrier route delivery IN ORDER sequence) sorting for 949 area.

What Gastons problem with your tolerance explanation is I don’t know, you were talking about welding robots.

Two comments –

1. If you keep your employees happy there is no need for a union.

2. The true minimum wage is $0.

I think your #2 confuses a legal requirement for simple joblessness.

eg – That’s the point.

If the cost of labor is too high, you don’t have to hire. I would consider the automation clause in the union deal a non-starter. Focus on doing your job well for a reasonable price and the industry won’t feed the need to automate. It works both ways. Both the employer and employee have an obligation.

Our workforce has definitely stabilized inline with these charts. After a year or three of high turnover, the shop is majority new faces in our mid-sized shop in the Midwest. We aggressively raised wages to respond to labor shortages. Luckily we were able to keep our most skilled folks.

We were forced to retain some really lazy when our demand was overheated, but the worst loafers just got the boot as the labor market has fallen back in balance. Good riddance. Our plant manager jokes that whenever unemployment gets below 5%, that last 5% are functionally unemployable.

A local agricultural manufacturing plant just got the axe by their parent company which allowed us to pick up a few hardworking and talented guys who would not have been looking for a job otherwise. Very similar machinery and processes to our operation, so they hit the ground running.

Inflation has eased in everything we buy, with steel erasing most of its prior gains, but aluminum has remained stubbornly high. The big stinker though…healthcare.

Met with our healthcare insurance broker today. Healthcare services and drug prices continue to skyrocket with no end in sight. We employers are pushing to find ways out of the scam that is our healthcare system. Haven’t found a good one yet.

That’s because the “healthcare” (in the US this term is a bad joke) industry is rife with economic rents — it’s market failures all the way down …

Besides, those “healthcare” Mgrs are so much better at FN other people than R=62 types EVER will be.

He should just quietly bend over and take his “medicine”.

They have a whole HUGE bought off MONSTER “Scientific Proof Industry” behind them.

I’m finding companies are struggling to find good senior management (especially in operations/manufacturing environments). Seems like all the baby boomers retired and it opened up tons of opportunities for 40 somethings like me. I’d see a recruiter reach out every few months 2022 – 2023, but this year, I’ve seen 2-3 per month. We’re struggling to find skilled labor, experienced engineers, and machinists especially. I guess manufacturing just isn’t cool anymore.

Here in Oregon, Intel is shutting down operations at the Hawthorn Farms campus in 2025. This campus consists of office and manufacturing space, as well as a very large parking lot. No fabs at this campus. Perhaps the buildings will be razed to make room for high-density housing. Prime real estate.

In Spain and europe is happening the same.

Very difficult to change jobs. I really dont see how this is going to help companies. They prefer bad employees rather than new employees…

And there is also a shift (since QE estarted) in the profile high tech firms were searching… most of them prefer influencers and “good looking wall street guys” rather than solid experience …

This is happening in the AI era. AI ( data science more especifically) it is not something you could achieve without engineers but a blogger or manager who keep posting BS about the wonders of AI in linkedin. Those profiles are being better considered than someone who could integrate and measure accuracy in those models.

Same happen with EV cars. In europe engineers are not high level jobs anymore . Not now, not ten years ago. The big car companies didnt want to improve their cars. I studied electronic engineering 9 years ago and no one in my career did get a job in the car manufacturing industry. They only hired mechanical engineers . Now they are hiring but you have old guys with no experience in this industry and new guys with no experience.

QE has a lot to do with this. In 2012 I saw a transformation in how tech projects were managed. We changed from meritocrats managers ( techie guys who knows their tech) to some kind of “shark” managers. This “shark” managers prefer to loose money and workers to land a project ( cheap and bad estimated initial projects) and then , after a few years of loosing money, start to earn a lot . ( Sales tech project with a german multibrand car manufacturer)

The problem with this strategy is the final buggy product and the high profiles you lost in the way to generate benefits.

Big fat margins but no innovation .

Now there is no margin and no innovation but shark managers still in their jobs…

terms are changing, meritocrats are the only ones that are able to move jobs but in a very slow pace. In the other hand , shark managers are being considered more and more as bad managers with are not able to keep good employees and good margins.

to summarize people are starting to realize influencers and sharks are crappy workers and no one is buying their BS anymore and no one want to put on their knees anymore to do a bad work. Instead people follow leaders which could teach workers how to do the good stuff.

but this is very slow trend, not sure if this is going to change fast enough.

it is funny to see how in tech companies gen z workers are ignoring those kind profiles, they are techie anarchists. they love their jobs but they will not move a single hand if the feel being used instead of being mentored. And shark guys does not have a clue. It is ver funny to see the face of a manager who was expecting a great product and instead he receives a “I didn’t know how to do it” project.

Before 1990 companies wanted married military veterans because they would follow orders and had dependents. Most companies want employees who show up, follow orders, and do an adequate job.

I recommend Mormons and Fundamentalist Christians. Easiest people in the world to work with.

Good people if you just want people to follow orders. If you want creativity, problem solvers, and people with drive, my experience hasn’t been good.

…a fascinating observation, here, of the scope of business management philosophies…

may we all find a better day.

Yeah…was funny (in a stupid sort of way) to me, too.

Everyone is working who wants to work or needs to work.

Nontraditional lifestyles depend on public and private transfer payments.

The historic record is full of attempts to discourage or recover from too many people living nontraditional lifestyles.

The latest move back to traditional lifestyles has just started.

Anon – Going off the grid or living simply is NOT an option. You MUST be a consumer! Capitalism doesn’t work unless we all consume our fair share. There is a need for continuous growth at all costs. FEED the beast!!!

The Beast doesn’t really care who feeds it or how, as long as it is fed and WELL!

{\displaystyle {\frac {f(t)}{1-F(t)}}=p+qF(t)} [2]

Mathematical representation of famous advertising (beast feeding aide) doesn’t paste well.

It’s actually a standard differential equation, using a “good guess” solution. Anyway, anyone in advertising knows what this formula is…and uses it!

q = how fast imitation spreads from lesser “inovators” (first buyers)

Seems like the huge wave of immigrants should be aimed towards the port strike. Unions are pushing way too hard for unrealistic concessions. This post pandemic economy, with a tsunami of illegal labor and ai threat (related to jobs) is reshaping the future of income stability.

It’s understandable that union people want to protect their futures, but their massive potential gains are everybody else’s losses — outrageous greed is not the solution, and it seems obvious these people can be replaced.

“ With a base salary of $81,000 a year (and some members earning over $200,000 with lots of overtime), the union reportedly is now demanding a 77% raise over its six-year contract and no further automation of operations”

The enemy of port workers is automation. There are fully automated container terminals in China, with autonomous trucks picking up the containers from fully automated container cranes. Everything is run by computers. These are amazing operations.

Was going to bed, but had to check into this. Still have to have many expendable little Chinamen (with expendable little limbs) crawling all over JOINING/UNJOINING containers at 4 corners each with HEAVY joining hardware while automated equipment does it’s thing at preset speeds and hopefully a few Chinaman hand sensors.

Pay is likely good for China.

Nonsense. There are no “little Chinamen” there, no people at all working with the containers.

It’s even happening here in the US, just on a smaller scale. Here is a video of the automated terminal at the Port of Los Angeles. That’s why unions are so scared. The video also has a segment on Rotterdam’s massive fully automated container terminals. There are no people there.

The jobs that there are at these automated ports are tech jobs, installing, servicing & repairing the equipment, etc., that require a much higher and a very different skill level than longshoremen and drivers. But instead of many thousands of driver and longshoremen jobs, there are just a few hundred tech, maintenance, and repair jobs.

https://www.youtube.com/watch?v=HkauiGYT6YY

No further automation of operations? That’s a ridiculous ask on top of 77% raise over 6 years. I’m not versed in this battle, but I can’t see any valid reason for those requests outside of “save my job from AI while giving me a fat raise every year.”

I’m just a self employed grunt.

Yes I’m union….Me & the Mrs make up the union.

I’m sure their union leader is no angel.

I do have some questions after reading some of their issues.

How in the h*ll is there any foreign ownership stake in our ports???

Does the EU or China have foreign ownership of theirs?

Who will be making this automation? China?

I have read article after article of bringing industry back to America.

Makes sense. Ports US owned, and AI US made makes sense as well.

77% over 6 yrs. no further breaking bargained automation…

did we expect them to ask for 3%/yr & full on AI?

Wage gain numbers just came in: 6.6% yoy for job changers and 4.7% yoy for job stayers. This directly impacts services inflation, and is well over 2x the Fed’s 2% inflation target. The Fed is a nervous Nelly, scared witless to allow the business cycle to unfold.

Where do retirements fit in? About 4 million workers are retiring every year – that must be creating a lot of openings.

“other discharges,” which I don’t cover here, and which are not included here.

That pretty much matches what I am seeing at my Fortune 500 casino employer. They aren’t pushing employees out the door for breaking rules but they are starting to crack down on rules being followed.