In Calgary, the first drop after a relentless surge. Edmonton and Quebec City set new highs.

By Wolf Richter for WOLF STREET.

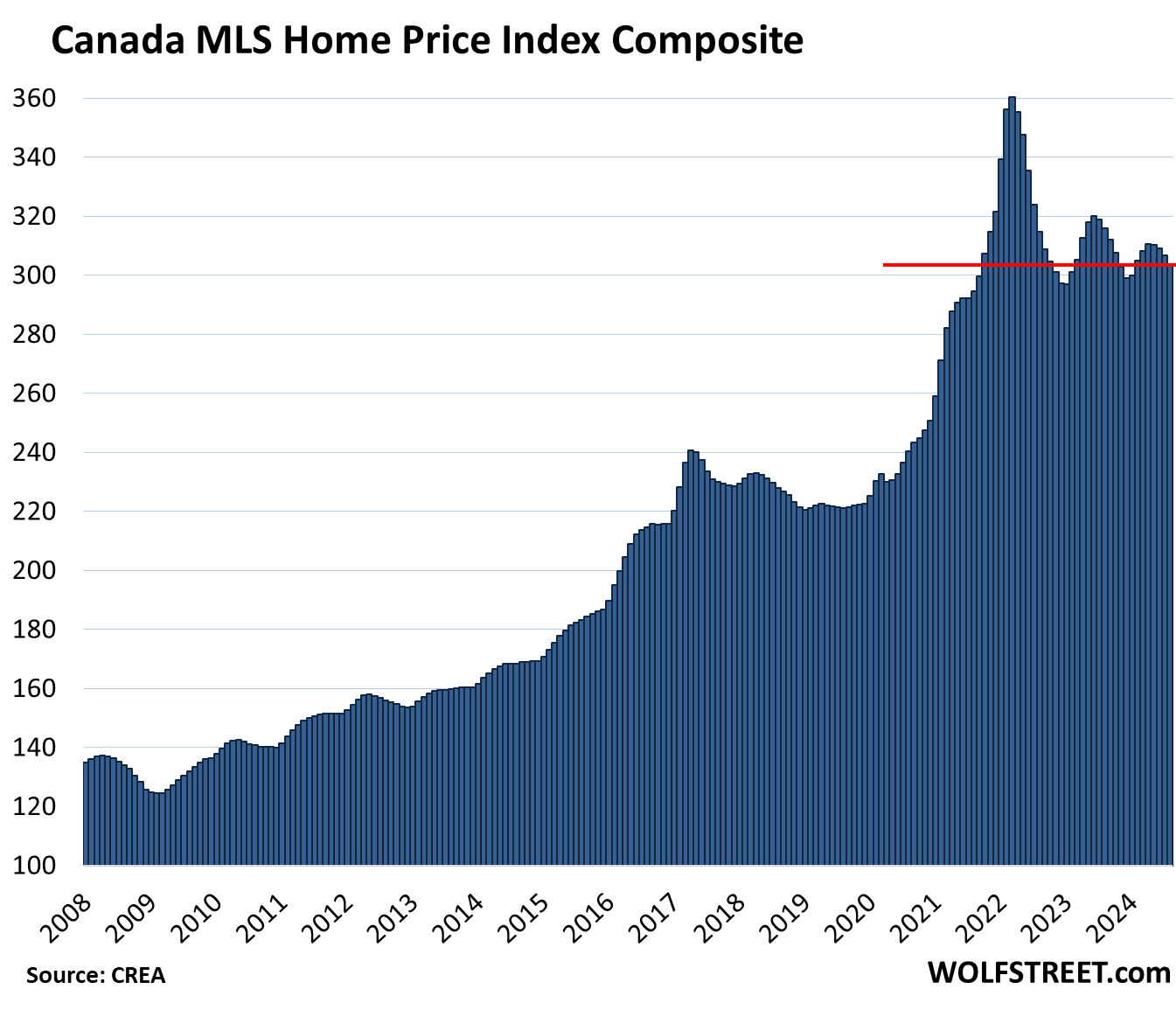

Across Canada, home prices (actual, not seasonally adjusted) dipped in August from July, were down 3.9% year-over-year – the fifth year-over-year decline in a row – and were down 15.8% from the peak in March 2022, with single-family prices down 16.2% and condo prices 10.4% from their peaks, according to data from the Canadian Real Estate Association (CREA) today.

But each of the major markets is dancing to its own drummer, with prices down from the peak the most in the Hamilton-Burlington metro (-21%) and in Greater Toronto (-17.5%), while they were down just a hair from record highs in Calgary, and hit a new highs in Quebec City and Edmonton.

Sales and inventory in Canada.

Home sales in Canada inched up by 1.3% in August from July, seasonally adjusted. Not seasonally adjusted and compared to August last year, home sales fell 2.1%. “The bigger picture appears to be a market mostly stuck in a holding pattern,” CREA said today.

Compared to the 10-year average for this time of the year, home sales were down 9.0%, despite the third rate cut by the Bank of Canada, including two by the end of July, just in time for the August housing market. But the BoC’s QT continues, and it has shed 52% of its balance sheet by now.

New listings rose by 1.1% in August from July, the sixth month of increases over the past six months.

Total listings jumped by 18.8% from a year ago, to 177,450 homes. Compared to the average number of listings for this time of the year, they were down 11%, but with sales down 9%, supply ticked down to 4.1 months of sales in August, from 4.2 months in July, but was up from 3.5 months in August 2023.

Home prices by market in Canada.

All prices below are actual prices, not seasonally adjusted. All in Canadian dollars.

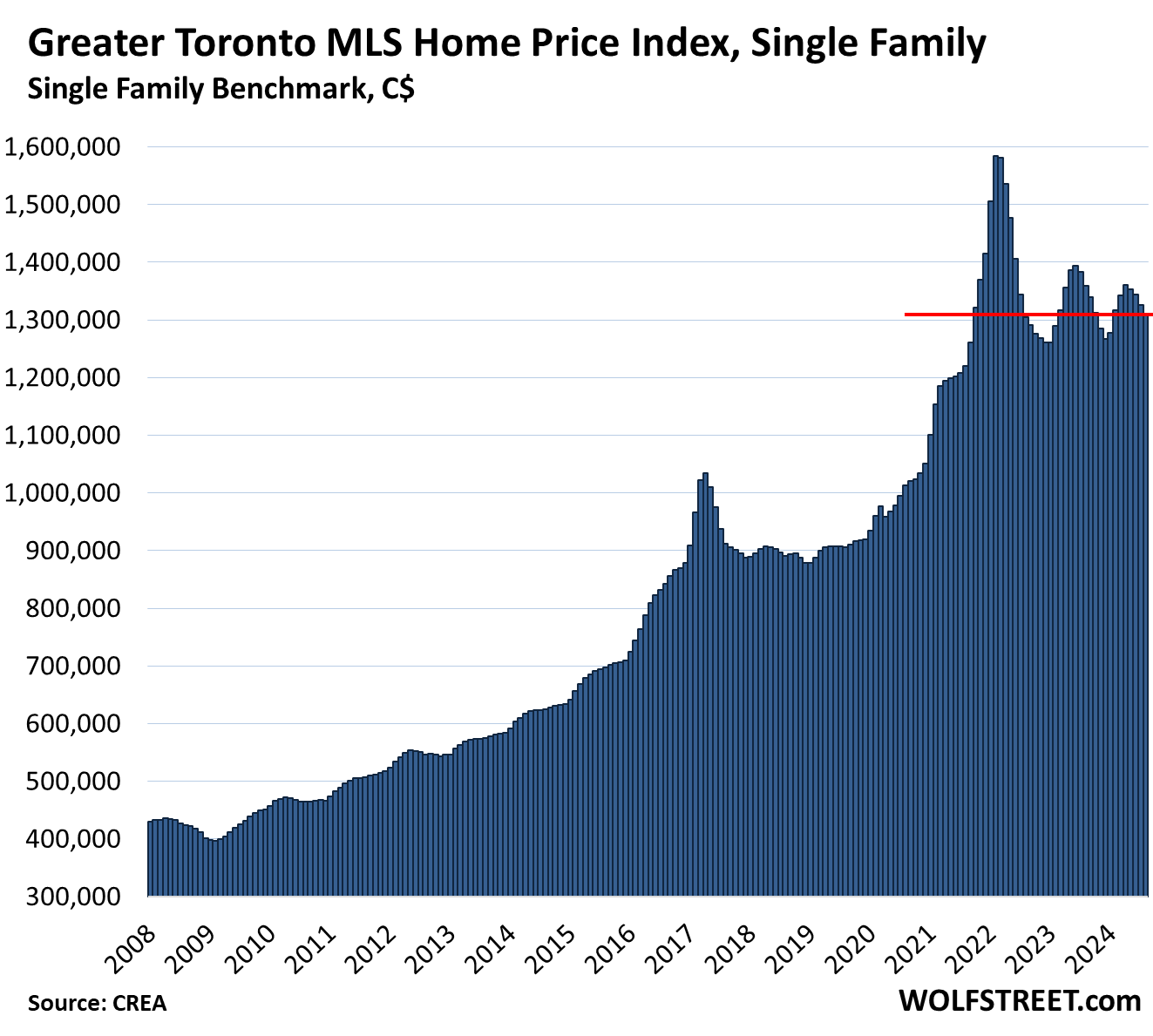

Greater Toronto Area, single-family MLS Home Price Benchmark Index:

- Month-to-month: -1.4% to $1,307,400; below October 2021

- From peak in February 2022: -17.5%

- Year-over-year: -3.8%, fourth month of year-over-year declines in a row.

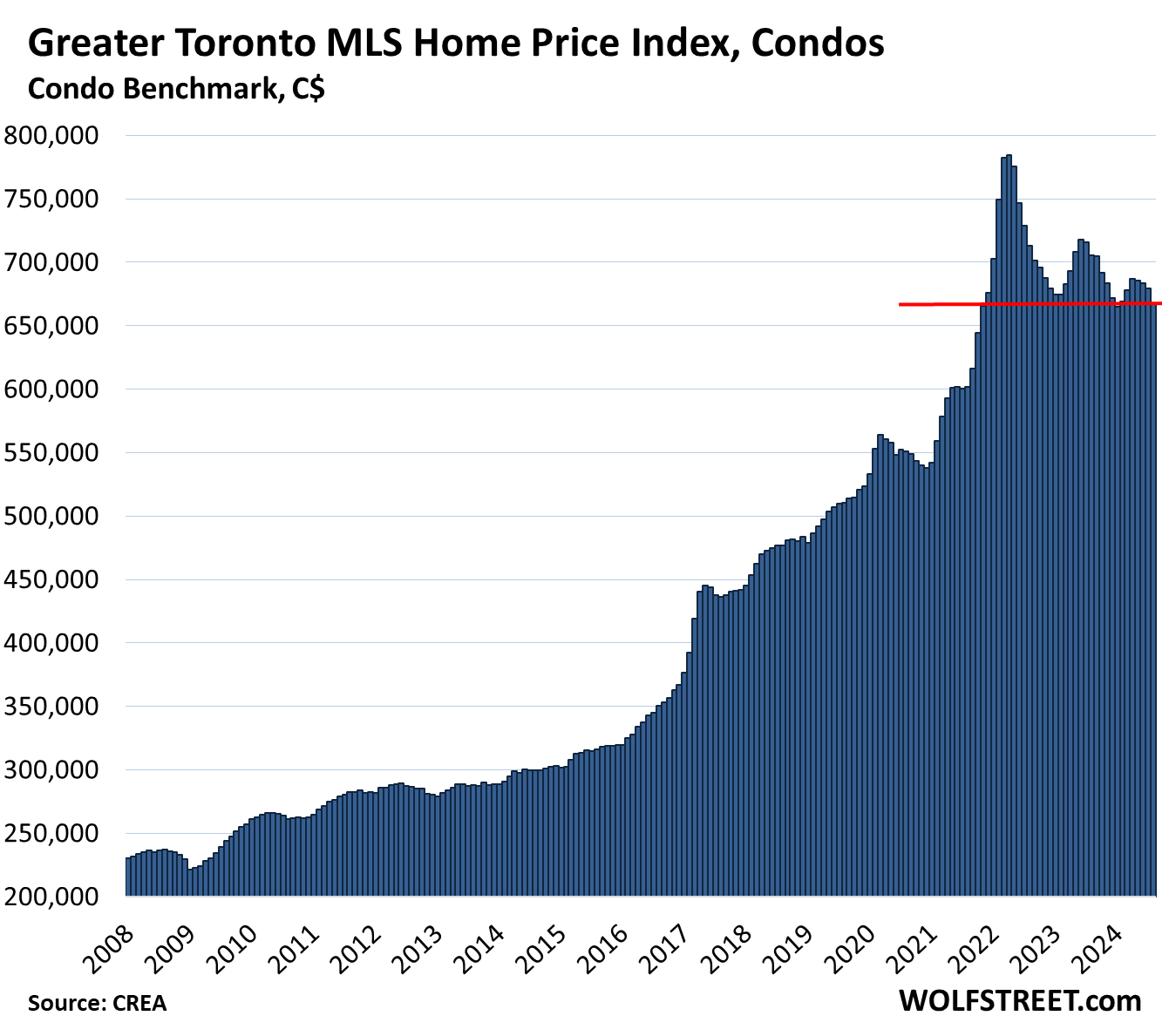

Greater Toronto Area, condo benchmark price:

- Month-to-month: -1.7% to $667,700, back to November 2021

- From peak in April 2022: -14.9%

- Year-over-year: -5.3%, with 19 of the past 20 months booking year-over-year declines.

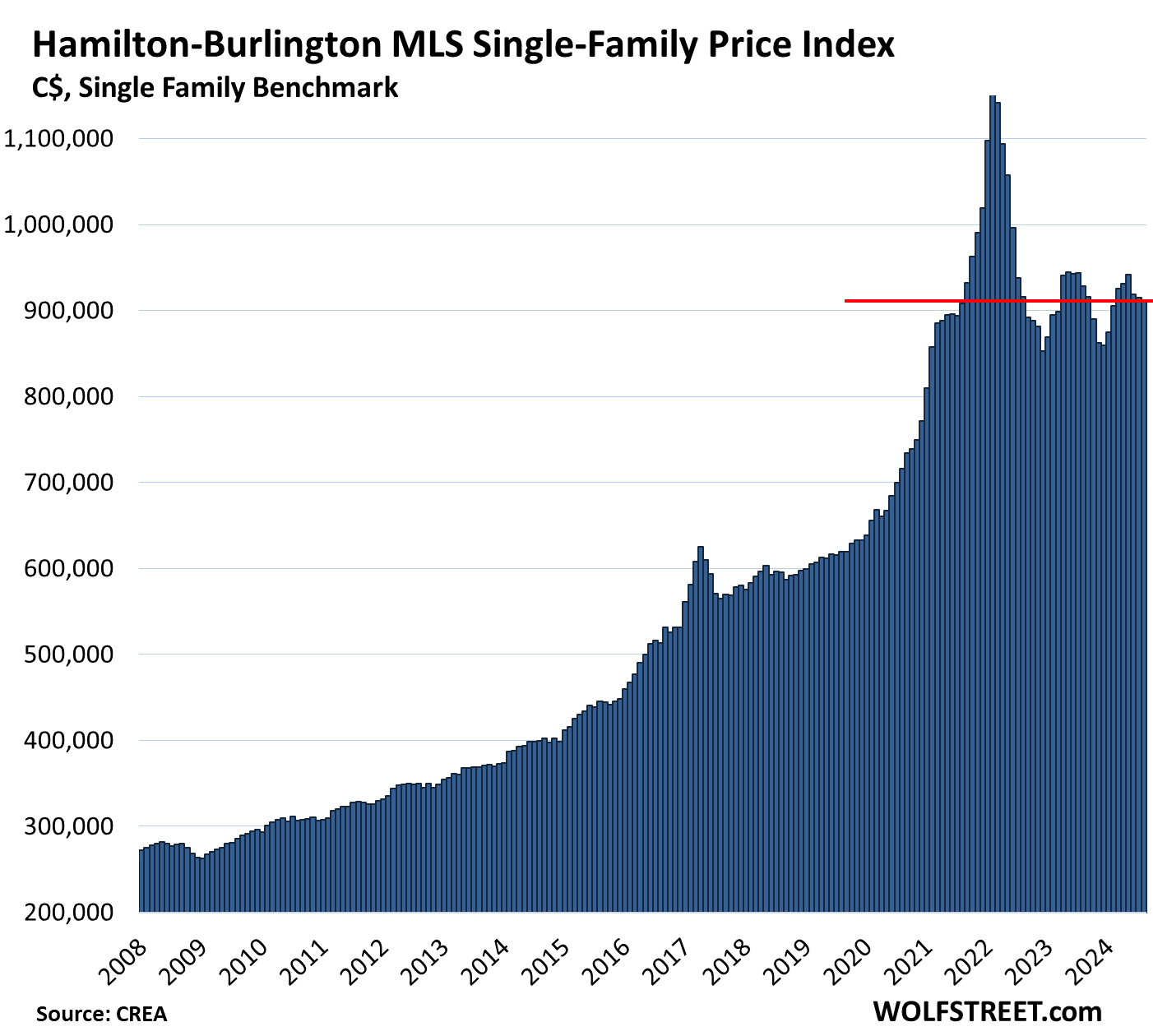

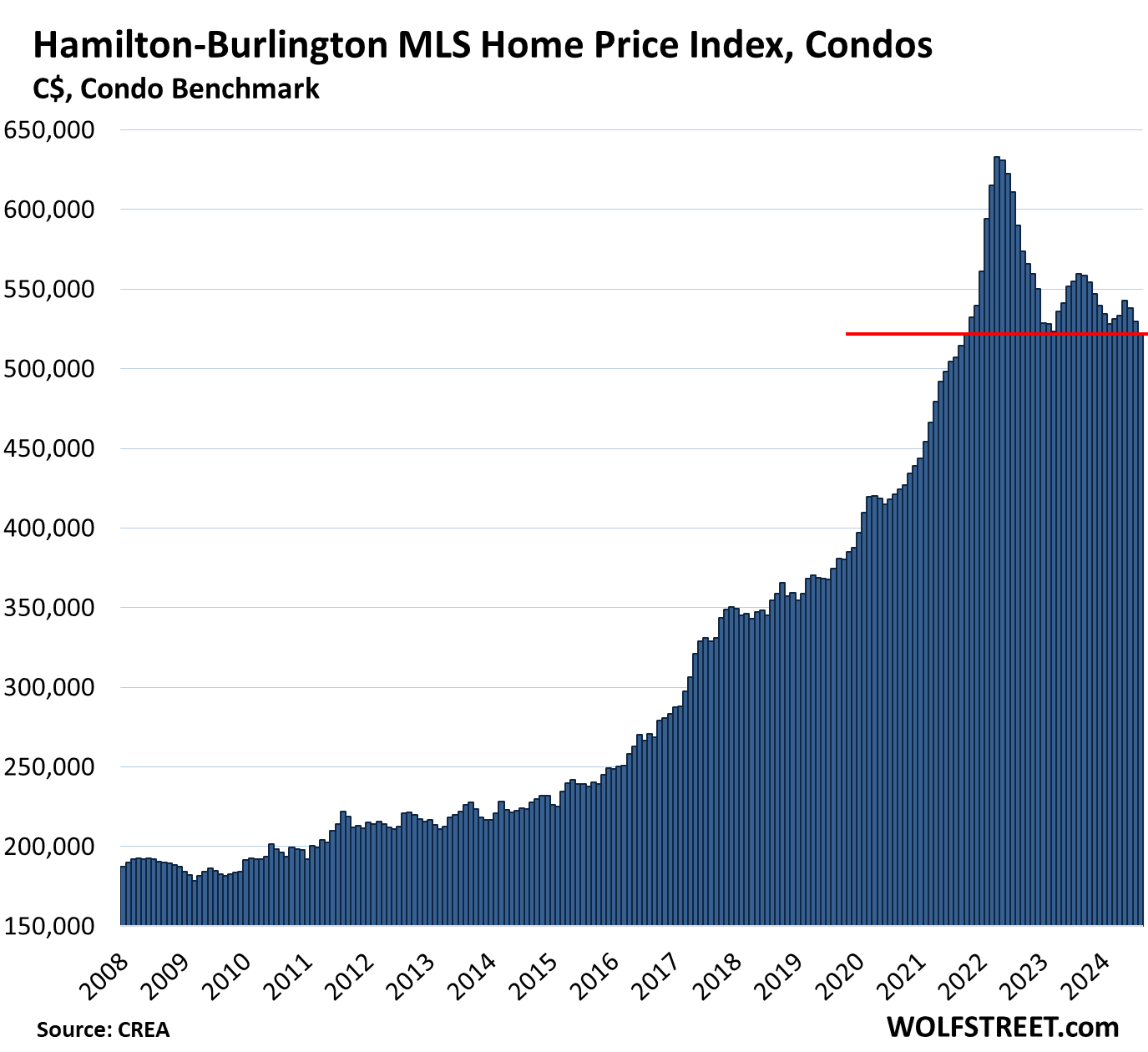

Hamilton-Burlington metro single family benchmark price (part of the “Greater Toronto and Hamilton Area”):

- Month-to-month: -0.4% to $911,500, where it had been in August 2021

- From peak in February 2022: -21.2%

- Year-over-year: -1.8%, fifth month in a row of declines.

Hamilton-Burlington metro condo benchmark price:

- Month-to-month: -1.6% to $521,300, the lowest since October 2021.

- From peak in April 2022: -17.6%

- Year-over-year: -6.8%, third month in a row of declines.

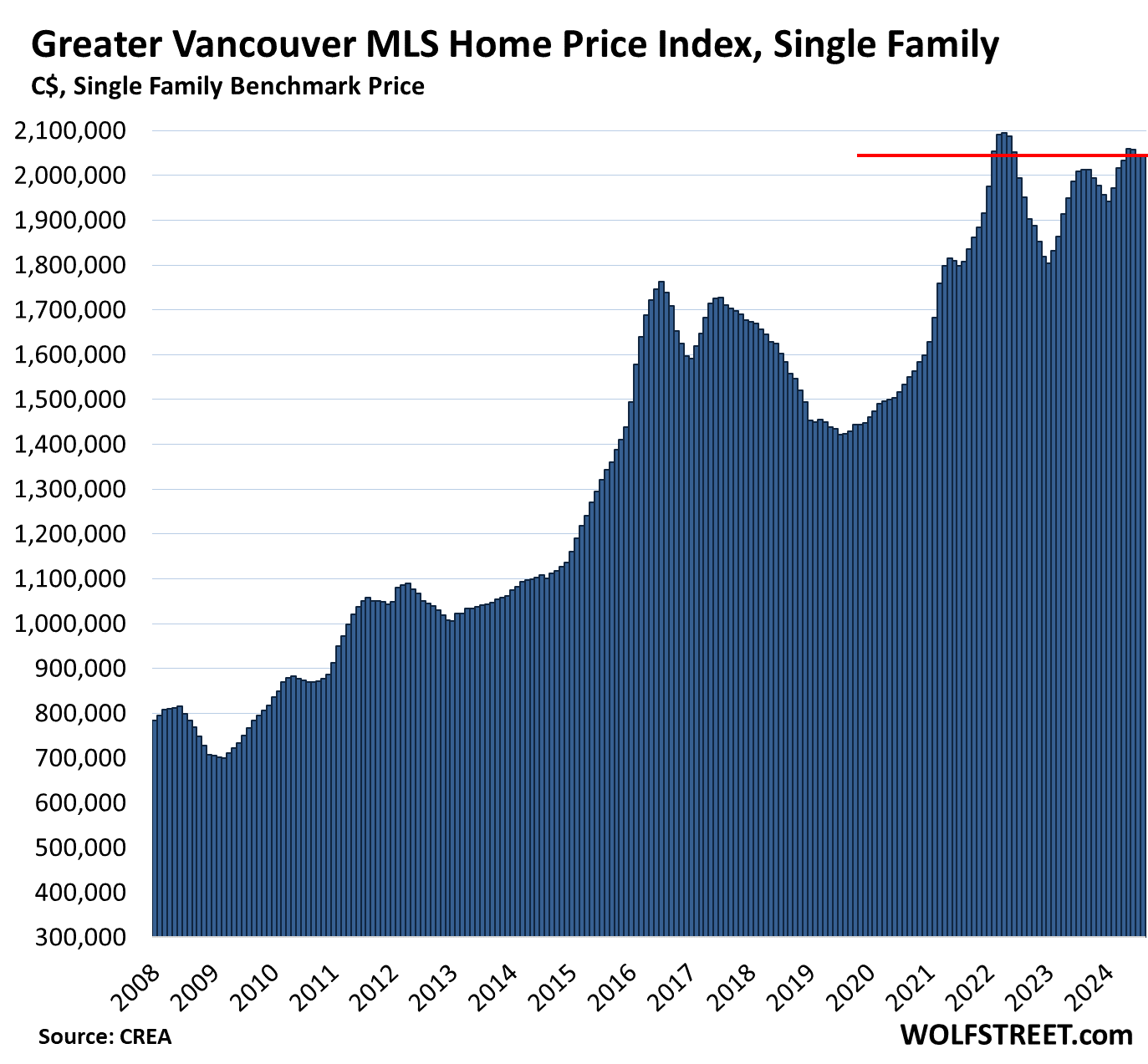

Greater Vancouver single-family benchmark price:

- Month-to-month: unchanged, at $2,045,200, and below February 2022.

- From peak in April 2022: -2.4%

- Year-over-year: +1.6%, smallest gain in 13 months.

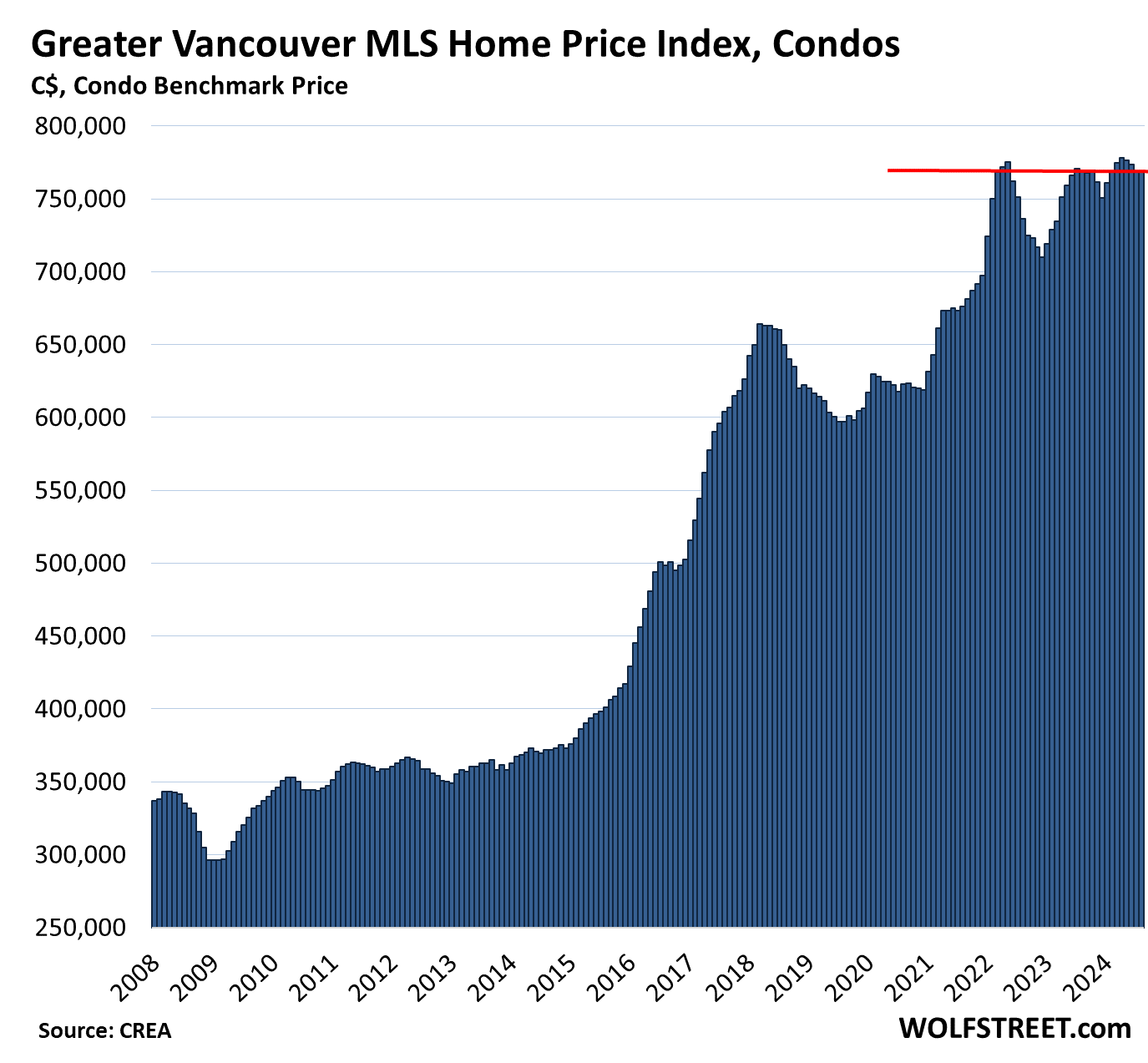

Greater Vancouver condo benchmark price:

- Month-to-month: unchanged, at $768,200, same as in March 2022.

- Year-over-year: -0.1%, second year-over-year decline in a row.

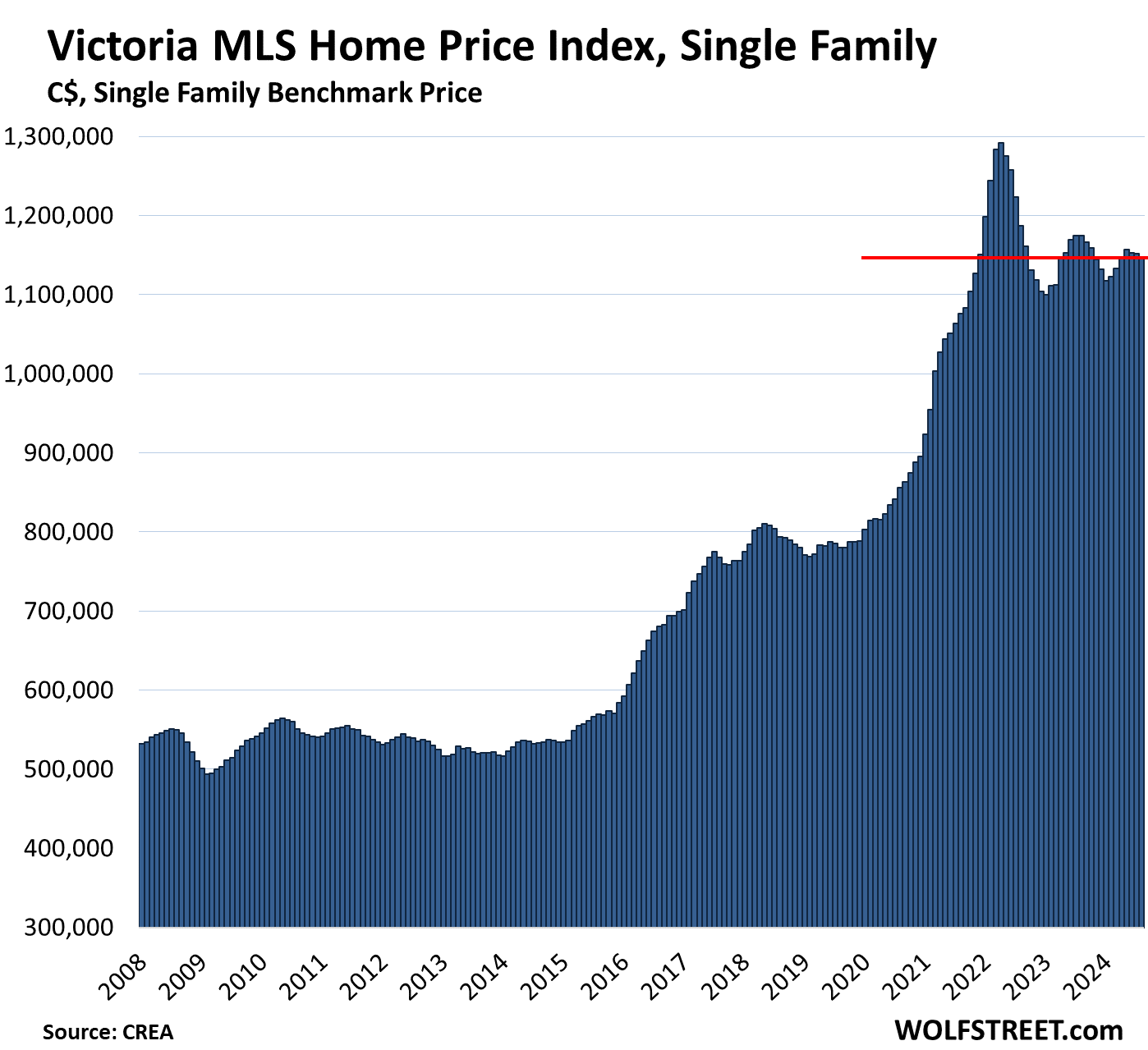

Victoria, single-family benchmark price:

- Month-to-month: -0.5%, to $1,146,400, below November 2021

- From peak in April 2022: -11.3%

- Year-over-year: -2.4%, third year-over-year decline in a row.

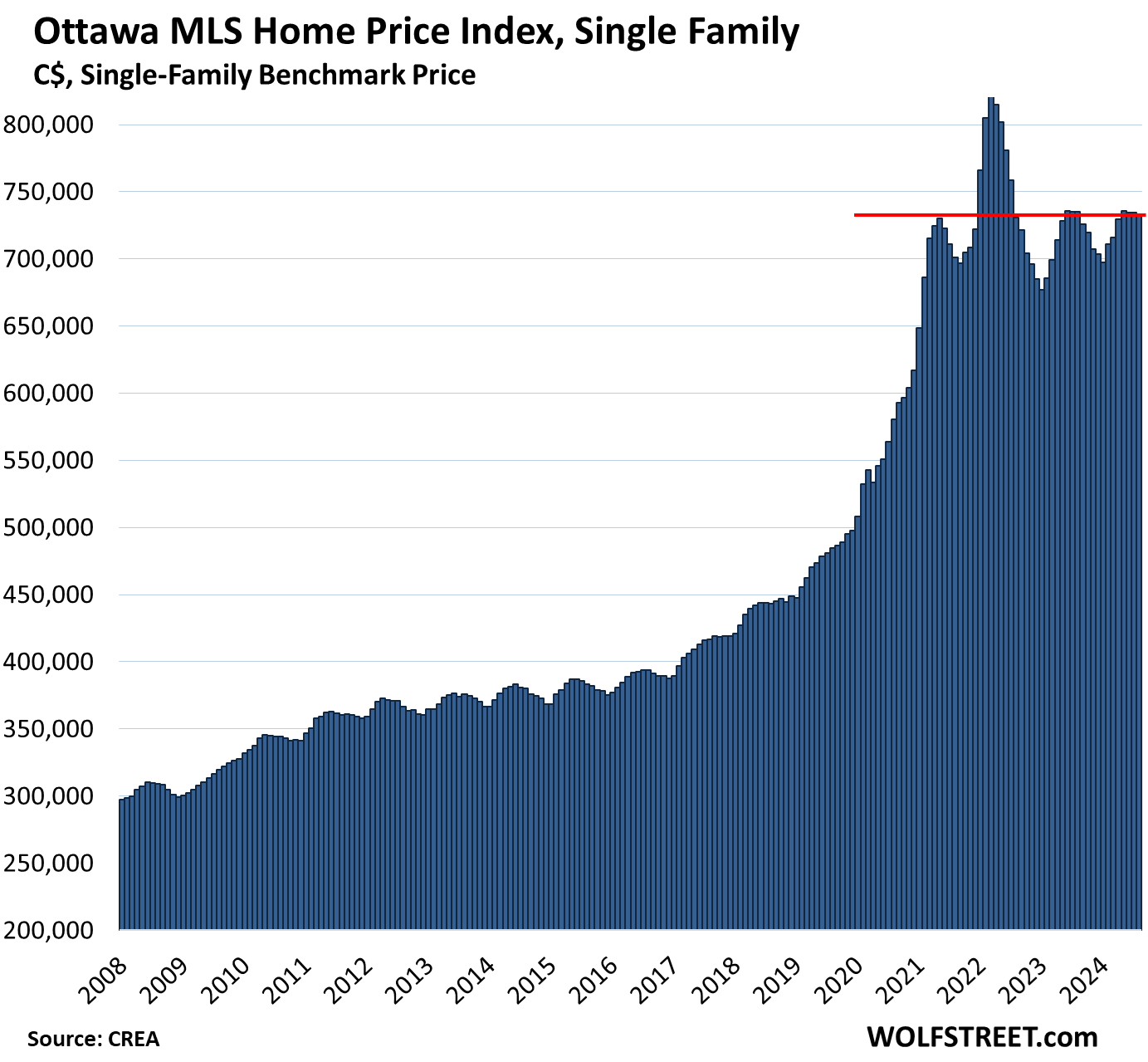

Ottawa, single family benchmark price:

- Month-to-month: -0.3% to $732,500, back to May 2021

- From peak in March 2022: -10.8%

- Year-over-year: -0.3%, third year-over-year decline in a row.

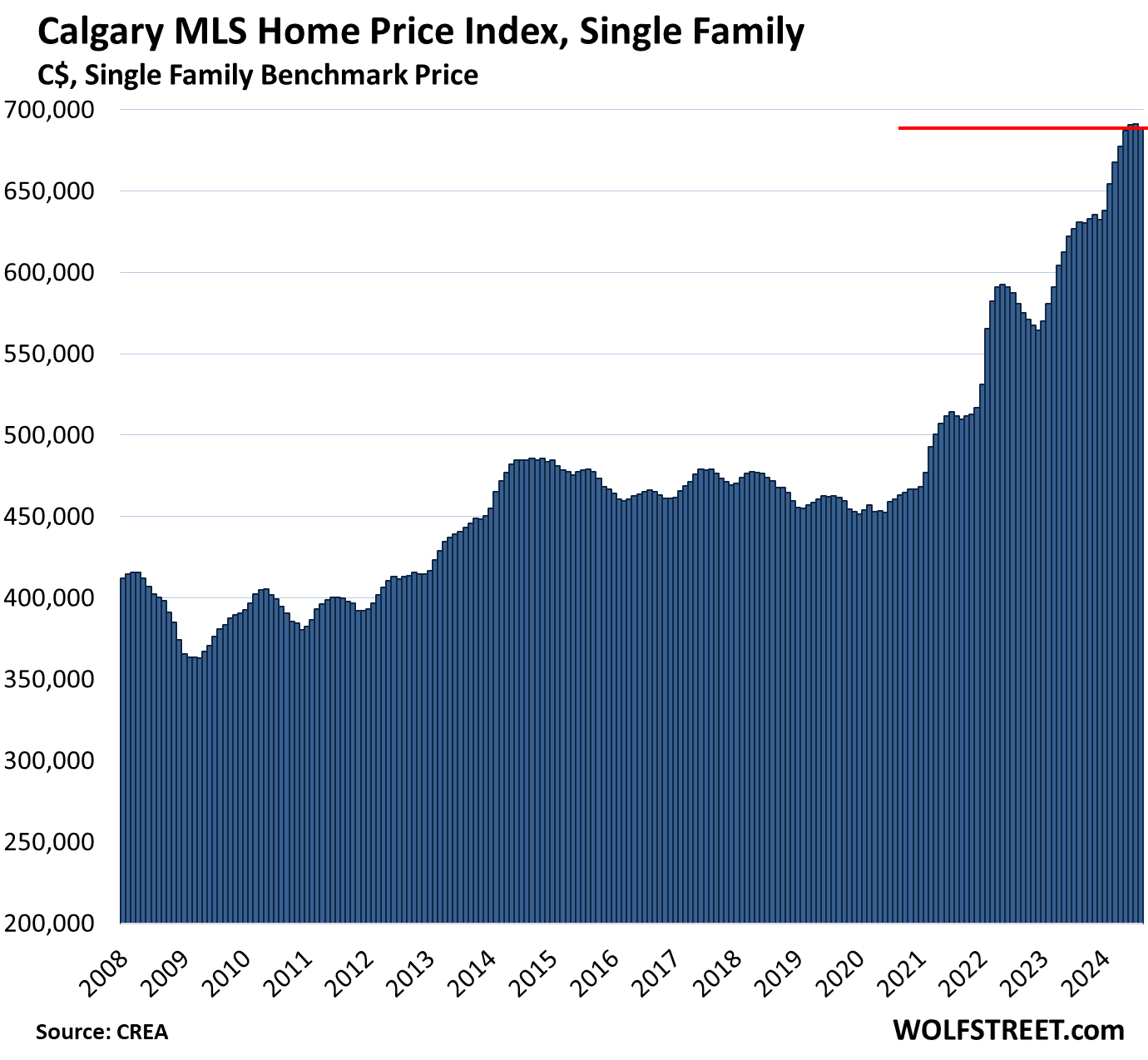

Calgary, single family benchmark price:

- Month-to-month: -0.4% from the record in the prior month, to $688,900, the first month-to-month dip since December 2023. In August a year ago, prices rose 0.6% from the prior month. So maybe finally time to take a breath?

- Year-over-year: +9.2%, the smallest gain since August 2023.

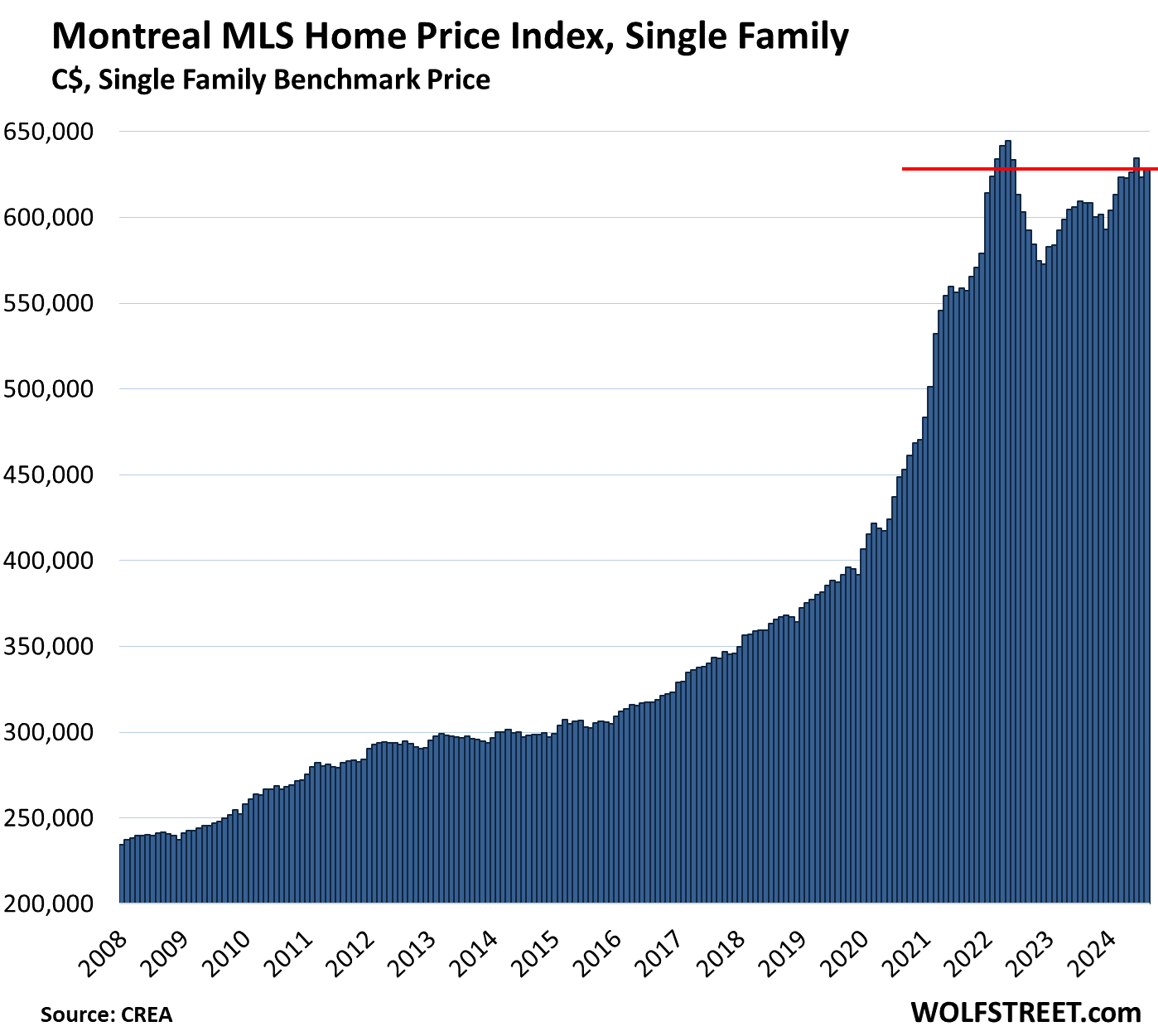

Montreal, single family benchmark price:

- Month-to-month: +0.8%, to $628,300, back to around February 2022.

- From peak in May 2022: -2.5%

- Year-over-year: +3.3%.

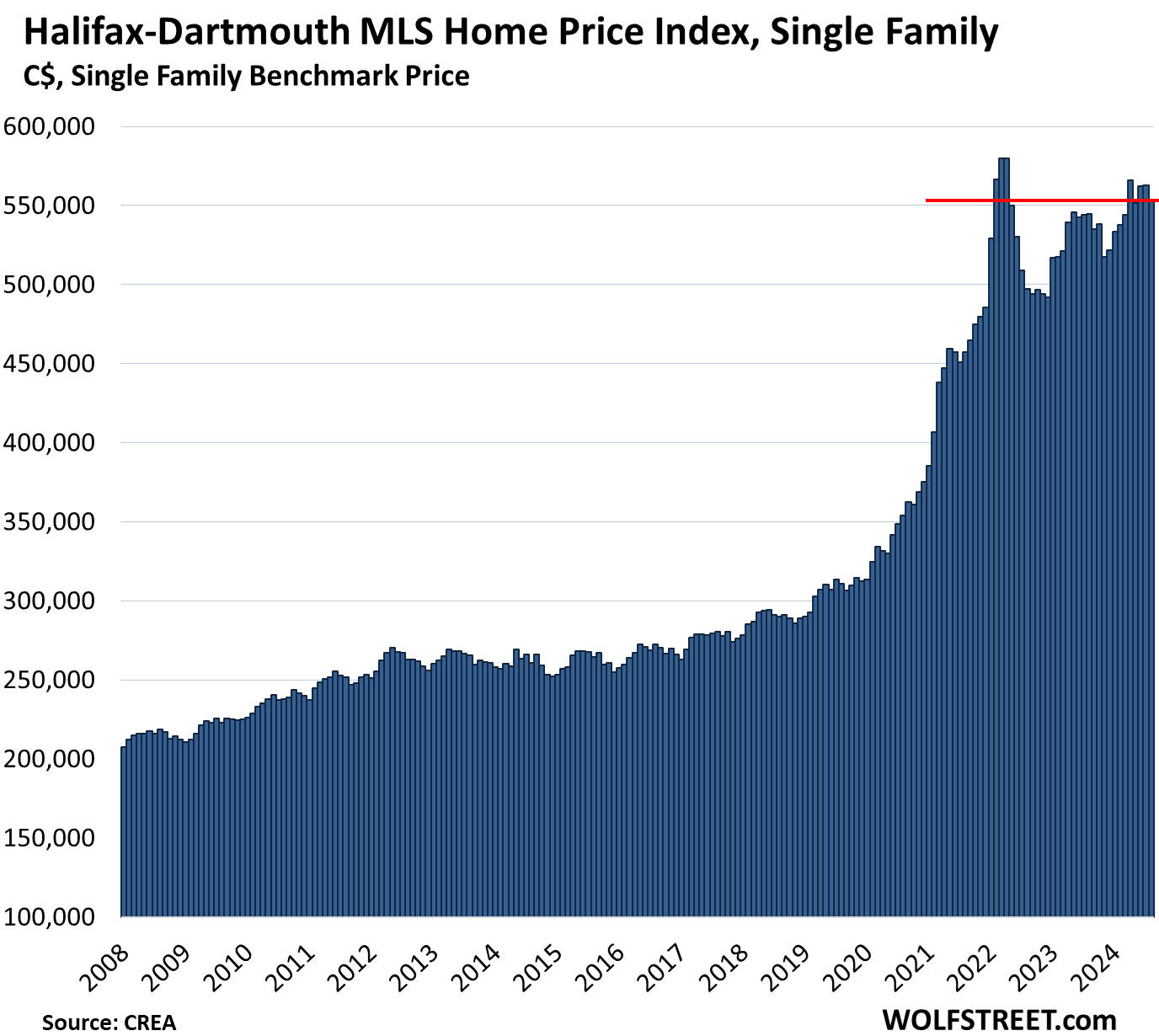

Halifax-Dartmouth, single family benchmark price:

- Month-to-month: -1.8% to $552,700

- From peak in April 2022: -4.7%

- Year-over-year: +1.5%.

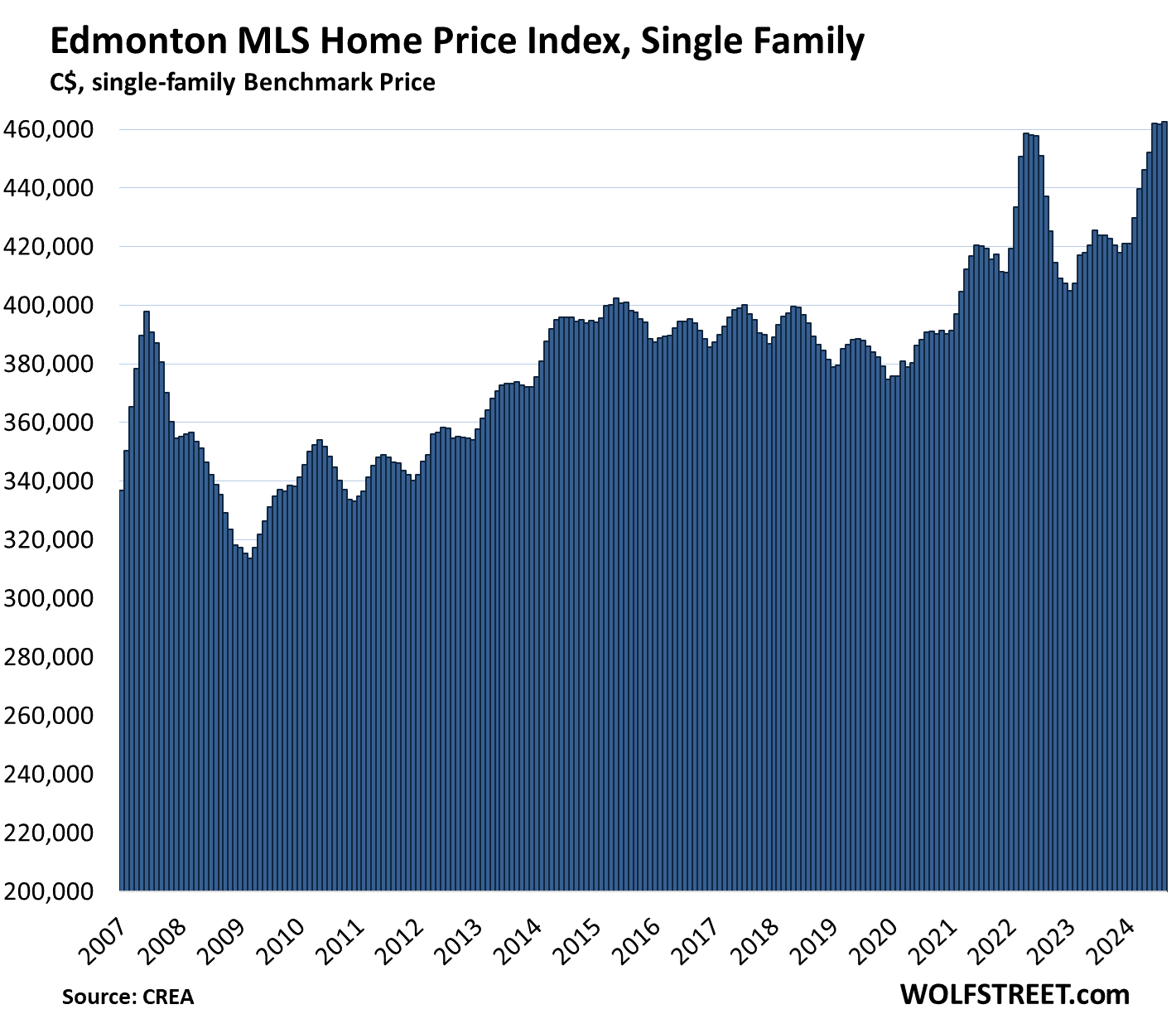

Edmonton, single-family benchmark price:

- Month-to-month: +0.2% to $462,500

- New high

- Year-over-year: +9.1%

- In the 17 years since the peak of the prior bubble in June 2007, the index is up 16%.

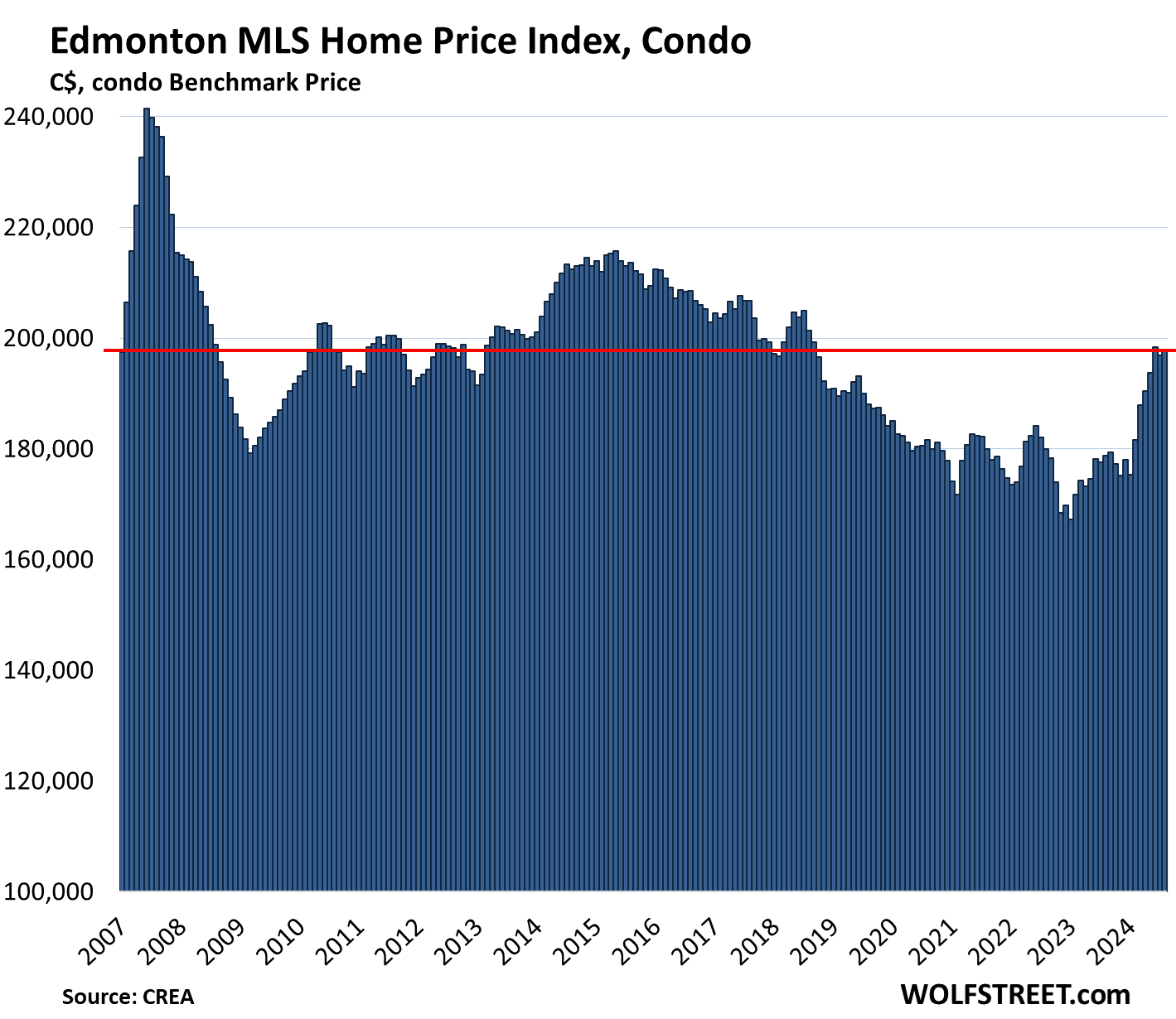

Edmonton, condo benchmark price: An epic condo bubble dissolved. Despite the surge since early 2023, the index is down 18% from the peak in June 2007.

- Month-to-month: +0.5% to $197,800, first seen in January 2007.

- From peak in June 2007: -18%

- Year-over-year: +10.7%

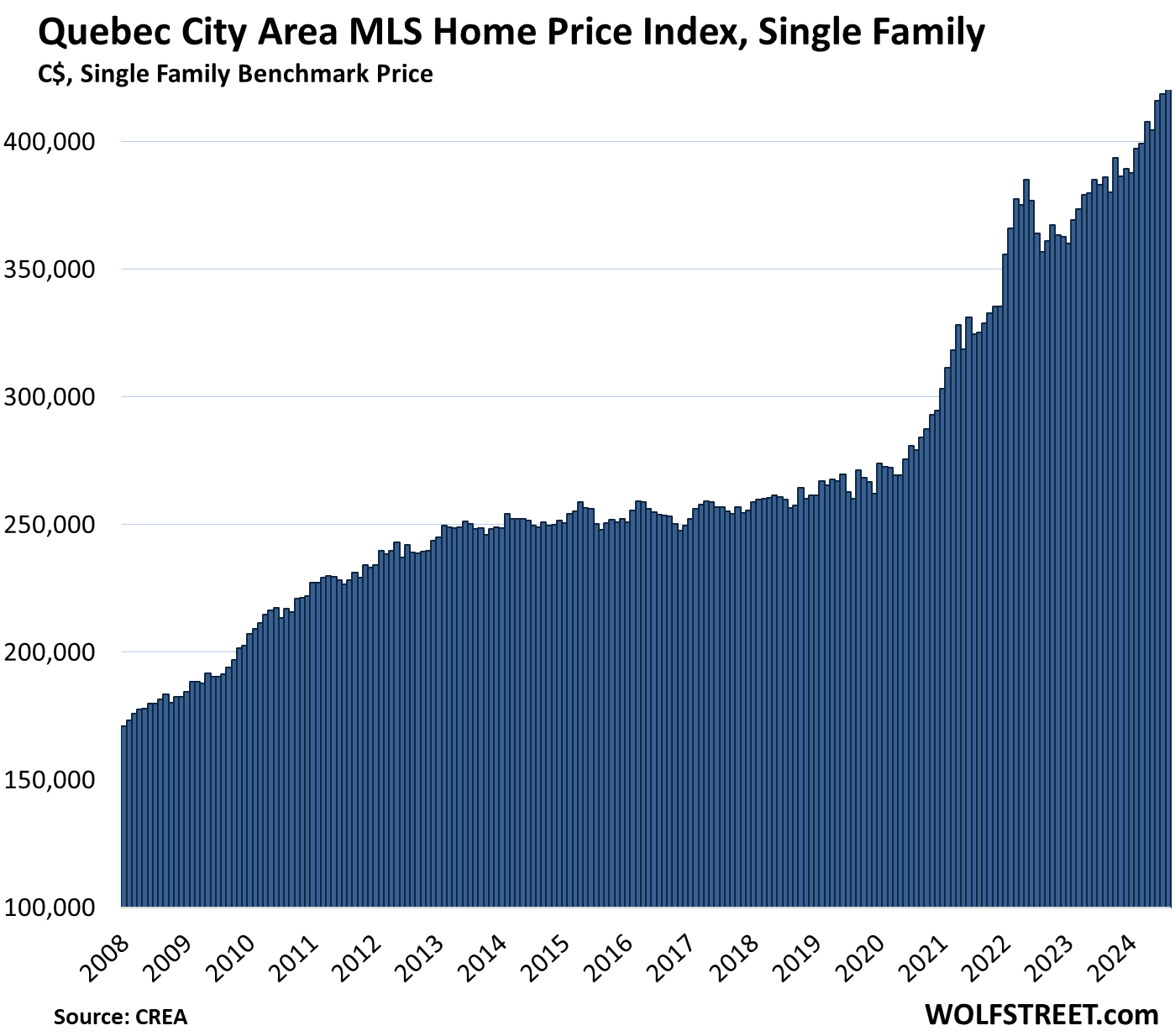

Quebec City Area, single-family benchmark price:

- Month-to-month: +1.4% to $424,700, a new high

- Year-over-year: +10.0%

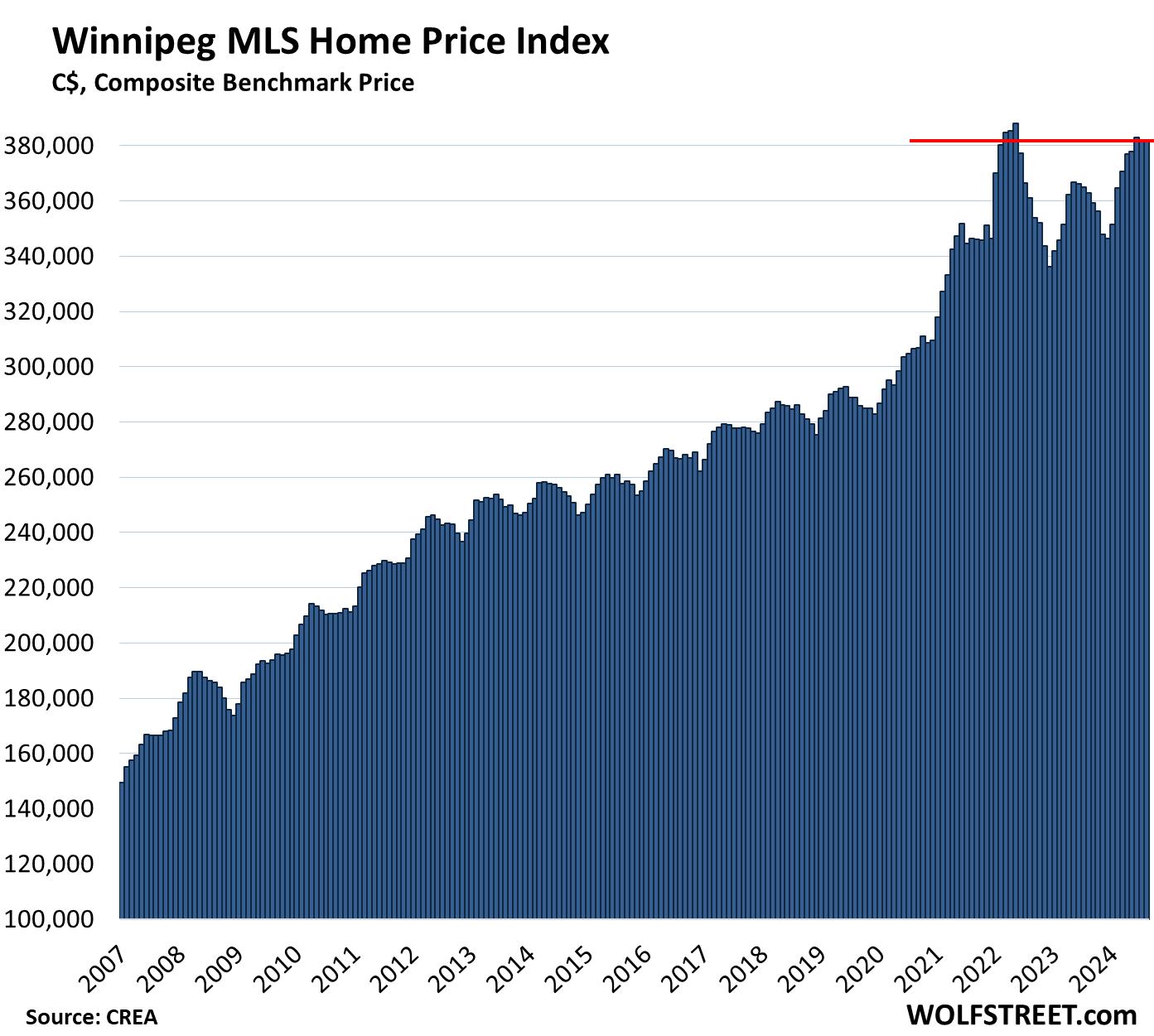

Winnipeg, single-family benchmark price:

- Month-to-month: unchanged at $381,900

- From peak in March 2022: -1.6%

- Year-over-year: +5.2%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

1:04 PM 9/16/2024

MW: Dow closes at record high as expectations grow for jumbo Fed interest-rate cut

Dow 41,622.08 228.30 0.55%

S&P 500 5,633.09 7.07 0.13%

Nasdaq 17,592.13 -91.85 -0.52%

VIX 17.05 0.49 2.96%

Gold 2,609.80 -0.90 -0.03%

Oil 70.44 1.79 2.61%

Cool, good to see this party will never end…either that or the market will fall flat on its face come next FOMC…let’s see…

Tech stocks were lower today. No way of knowing what today’s action meant, if anything, but it could be a set-up for a “Be careful what you wish for” scenario. The SPY dividend is Friday. It’s still September, the worst month for stocks. If it’s bad, it could be VERY bad, as the S&P has had only one down month going back to last October (!!!)

2022 was very bad.

Stocks AND Bonds tanked.

Bonds are supposed to be your ballast in bad stock times. So that was pretty rare, but not too surprising due to inflation.

So if 2022 was bad and the market is only bad 1/3 of the time, then odds are it’s going to be ok, if not Great, when the fed loosens.

We shall see!

So…you could buy five houses in Edmonton for the price of one in Van City…

Now will the bubble burst in nominal prices or only in real prices (factoring in inflation you can still have the price go up nominally while after inflation it’s down – e.g. nominal price goes up 2% but real inflation is 5% so …)?

When governments and citizens go into debt to buy foreign goods for 30 years, which eliminates high paying manufacturing jobs, it comes back to haunt in one form or another. Don’t blame the the foreign entrepreneurs, who are now buying every attractive piece of RE on the west coast that they can get their hands on.

Meant to say, WE can’t blame…

But then you would have to live in Edmonton….

Edmonton is a pretty nice place in terms of quality of life.

If you can hack the winters. I visited once and that was enough for me.

Well that’s about the only way to use the word nice and Edmonton together, good work! 😆

What Edmonton does have is affordability and a lot of good and very good paying blue collar jobs.

People are waiting for a recession or anything to bring house prices to affordable levels and at this point really don’t care what does it. There is a BRICS payment system rumored to go into effect with a large number of nations and we already have a trade war in semiconductors and electric vehicles; it seems that those may become economic factors that would affect housing prices.

There is a North American, USA, Canadian house market. And there’s Vancouver’s market. Different laws of physics apply.

And that, my friend, is why I am pleased to live south of the border…

Vancouver is fairly unique in Canada given its geographic constraints. It has the ocean to the west, mountains to the north and east, and the border to the south. There is limited room to continue to expand and build single family homes. The path to affordability lies with denser housing.

It’s all true in the long term but IMO is used today to justify the crazy valuations. I don’t really think it’s even necessary because the truth is Metro Van is a super nice place to be, on top of the industry that is there, so a lot of people want to live there and have the means to do so. In reality there is still tons of land East of the burbs, and it is getting developed, but the issues there are more with zoning, they’re very very slow in the lower mainland amending that. But yes, one day long into the future there won’t anywhere to develop except on the side of mountains

Just like in 2000 and 2007…the stock market hit all time highs right before the Fed started cutting.

Maybe it’s different this time? Maybe stocks have reached a permanently high plateau? Tbd.

Meanwhile housing has flatlined and will probably continue to do so until the market rebalances. Could be five years, could be ten years.

When @David wrote: “So…you could buy five houses in Edmonton for the price of one in Van City…” it reminded me that after looking at Wolf’s US charts this weekend I was thinking “So…you could buy five houses in Houston for the price of one in San Jose…”

Yeah, but how good is the avocado toast in Houston.

Next time around I could be a Canadian flying dung Beatles. The dunglord will want half my dung just for a dunghouse.

Houston is an excellent food town and one of the most racially diverse cities in the country. The problem isn’t the food, it’s the weather and topography.

Stocks, home prices, krypto-nite currencies, whatever, everything will fall again. There is something very wrong with the Fed lowering interest rates with asset valuations at or near all time highs. I am staying with my call that the S&P is a LOCK to see 4500 again at some point, and I am adjusting the probability of 4100-4200 from being a (50%) coin toss to 60%.

Pundits say the Fed doesn’t support asset prices. Instead, the Fed supports employment, which happens to depend on maintaining high asset prices. They pretend there is a meaningful distinction there.

There is. If you can’t see it that is your fault. Others can clearly see the distinction.

Maybe you should describe how that perceived distinction evidences itself in practice.

Examples please.

You are making the mistake of thinking the FED is making decisions based on asset prices. They are not. Their decisions are based on inflation and employment. They have messed up in the past but the current FED is pretty clearly focused on those two measurements.

Core inflation is still 50 percent higher than feds target rate

Unemployment is still historically low and job creation still in play

Stocks and housing prices flirting with all time high..

Financial conditions are extremely loose.

The above are despite the rates being restrictive

I just don’t understand the need to cut rates

“I just don’t understand the need to cut rates”

Job creation has slowed down a lot. It’s still positive, and nonfarm payroll jobs are still rising but too slowly to absorb the huge waves of immigrants. You have stated many times that some of your friends who work in tech have been looking for jobs for months. That’s the problem. Layoffs are few, but once people have to look for a job, it takes them longer to find one.

Another month like August, with revisions like we had for July and June, and nonfarm job creation could turn negative.

The Fed’s policy interest rates are VERY restrictive — they’re nearly double the rate of inflation. Inflation has come down a LOT, but the policy rate not come down at all.

The Fed did it to force retirees and savers to leave the country and move to Mexico to get an honest return on their money. Brazil isn’t really a choice and its too early in time to move to Russia.

Is your memory this short? In 2021 the Fed bought MBS and treasuries while inflation raged at 9%+, and unemployment was low. This is absolutely inexcusable and all involved should be fired.

Yes they did pivot hard with higher rates subsequently and inflation appears to be on a trajectory toward normal. Meanwhile our dollars lost 30% of their value. So much for half of their dual mandate.

They can talk all they want about their dual mandates but their recent actions are very mixed and they have acted to prop up assets in a massive way just 3 years ago.

At these sky high asset price levels and debt levels, it is pure fantasy to think the Fed would allow an asset price drop to unfold without a massive monetary response. Bernanke tethered the economy to asset prices (the wealth effect) decades ago, and this cannot be reversed without a significant recession.

The Finance Minister-Deputy PM assented to 30-year mortgages, and increasing the 20% downpayment required threshold from $1M to $1.5M

Leading up to the gfc, I believe they offered up to 40yr & zero percent down. No worries they certainly will not do that again……

The Liberals could bring that back in but it looks like Trudeau will lose the 2025 election.

Gen Z,

Does that mean Canada will have 30-year fixed* mortgages like we have in the States?

And does that mean you only need a 20% down payment if you’re buying a place over* $1.5M?

If the answer to both of these is “yes”, then I guess that supports high prices and puts regular people in debt for their whole lives just to buy a house? I’m asking you, you are the Canadian who has to live it…

No it means the mortgage will be amortized over 30 years. No one takes out anything longer than a 5 year mortgage because the rates for 10 year mortgages are far too high and 99 percent of the time are a bad choice for a mortgage. Going forward in time a 10 year mortgage will be the wrong choice 100 percent of the time. Covid was a one in a million fluke.

Wolf – unrelated to this topic but are you aware that the Michigan Consumer Survey shifted from live phone to online panel? They did it over a couple months and showed that the online panel is about 9 pts lower than the phone panel.

Both numbers have been going up since May but as the online panel took over the blended final index went down. In reality the Michigan number has been going up since May to today

MW: Tupperware is preparing to file for bankruptcy protection, Bloomberg reports

TUP -57.51%

I always wondered why they’re still even around.

Amortizations increased to 30 years for first time buyers for all dwellings – is it actual “first time” buyers or the FHSA’s definition of a first time buyer?? I don’t know. Found this quite predictable.

The government increased the public/federal mortgage loan insurers cap from $1 million to $1.5 million (per loan). A 50% increase. This change – I personally find bothersome. The CMHC has been identified as a financial moral hazard in the sense that it shifts risk from the mortgage lender to the taxpayers.

The potential policy for CRA income verification for mortgage loan applications is still in the “talk stages”.

Well, given the choice between letting the market correct on its own and intervening to try and support overly frothy price levels – the Canadian federal government has obviously chosen the latter.

If you believe that leaving housing entirely to “the markets” is appropriate, you probably ought to returns to the early Victorian era where you belong — along with the resisters to investments in public sanitation.

Yep. This is the reason why Americans moving to Europe are so impressed with life there.

These housing bubbles can deflate a bit and there will be no negative consequence. Americans and Canadians are doing well financially despite the now vanquished inflation and only a negligible few would be affected if a small percentage of their “home equity” was lost. Those young first time home buyers will benefit from lower prices and reasonable rates.

Agreed, it really only affects the investor class, builders, and banks. Normal people who can’t afford to buy additional investment properties could careless as they’ll have to shell out the same “gains” to buy another property to live in. Or hand it over to the old age jail homes that drain their life savings and joy away since all the family have moved to LCOL cities to have better quality of life.

Insane government policies for insane debt addicts. Last I checked, bank of mom and dad’s gift of 200K of HELOC money + new mortgage = 100%+ LTV of that new house since mom and dad now owes the bank 200K + HELOC interest. derp.

In most of Canada or where the people live there are no first time buyers. The first time buyer has been gone since the end of 2016.

Thanks Wolf. Excellent data as always.

Anecdotally: While Vancouver and Victoria pricing, shows as flatish. One example local to me, is a waterfront property in the Gulf islands, BC, Cdn.

Tax-Assessed was $1.3m. Sold $1.0m. 24% discount. 49 days on listing. Likely, 40% to 50% up from 8 to 10 years ago.

This area has demand as recreational properties; however, maybe 50% of the area is also full time residents. This sale was an older and smaller home, that was usable but in need of updates. Locally, off-island buyers are shifting to ~$2M range for newer and larger waterfront homes. While, a new build on the waterfront lots, are over $2m (2.5 to 3); as construction cost has escalated and is more than the lot value. My observations, this neighbourhood, the local residents live in more modest housing; while new buyers, are off island, and are buying/building a “recreational” property in the $2m- to 3m range.

I wouldn’t put much stock in the BC Assessment figure. Their valuation date is July 1 of the prior year and while they do a decent job estimating value of homogenous properties (condos, suburban SFDs) they often miss the mark on unique properties, such as waterfront.

Concur in general. But differ in usefulness.

Like the indexes which are useful, but here the combining and selection and averaging hides a load of important detail; and I always wonder what spin is included too. As some data series have become less reliable, so opens the questioning. It’s a starting point.

Assessed is dated but it’s a benchmark, too. A starting point.

The assesed component of land value of waterfront is currently close. The building value has a wide range. And in this case, at $1m, it’s mostly a land value sale, for what is 50/50 chsnce as a recreational property.

Discounted in this case, was the building; unlike couple of years ago, when even chicken coup built out of driftwood had a price.

Points were: Specific to this area, newer and bigger is holding to increasing. While older and smaller is discounted. And, implied is, while unfair and harsh on local workers, Vancouver, Victoria, and other similar areas have unique appeal, and that pricing support is often from buyers outside of the community.

Narratives in this post pandemic era are very fickle and reminiscent of the SVB bank runs from last year:

“ Canada’s young adults went from hearing a labor shortage narrative to facing an unemployment rate not seen outside of the worst recessions, in just a matter of months.”

I think everything is fragile and volatile these days and economic data is suspect — it tends to be overly noisy and perhaps unintentionally manipulated with compounding errors.

I guess Wolf points us towards the North Star?

Ignorant comment. Canada has had a gigantic influx of immigrants since the pandemic, proportionately much larger than the US. And these immigrants are going after the jobs that young Canadians normally go after, and they’re happy with less. This has become a huge well-known problem, it’s well-documented and much discussed. But you missed it???