Second month-to-month acceleration in a row. Year-over-year, Core CPI and Core Services CPI show first acceleration since March.

By Wolf Richter for WOLF STREET.

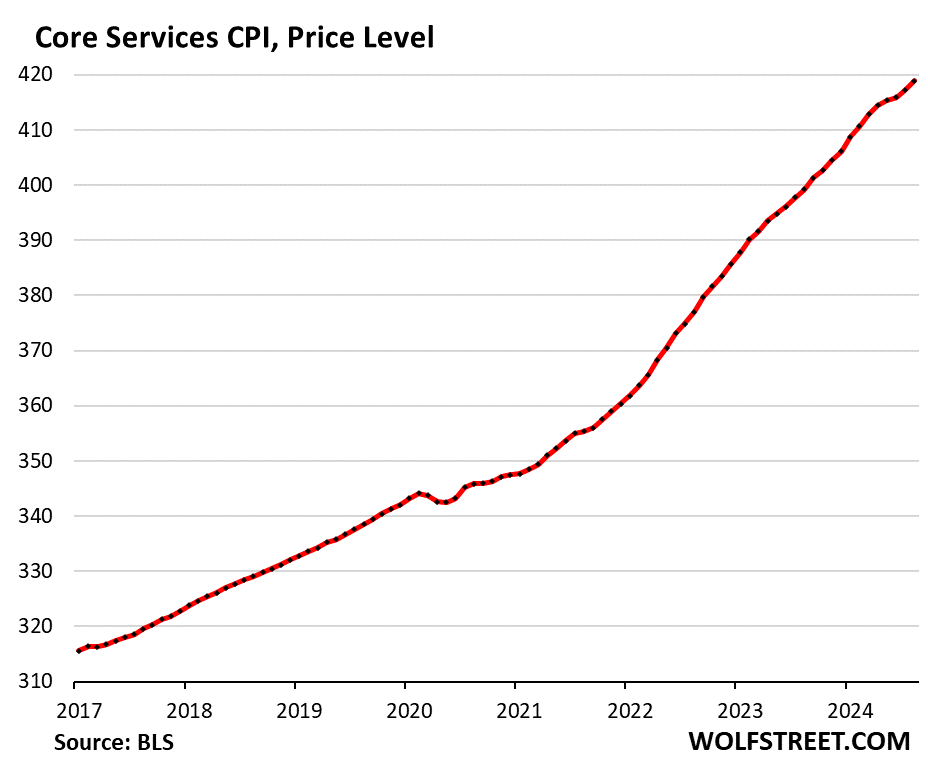

On a month-to-month basis in a most unwelcome development, “core services” re-accelerated for the second month in a row in August, to 5.0% annualized, which fueled the re-acceleration of the overall Consumer Price Index (CPI) and Core CPI. Core Services make up about 65% of the Consumer Price Index and include housing, healthcare, and insurance.

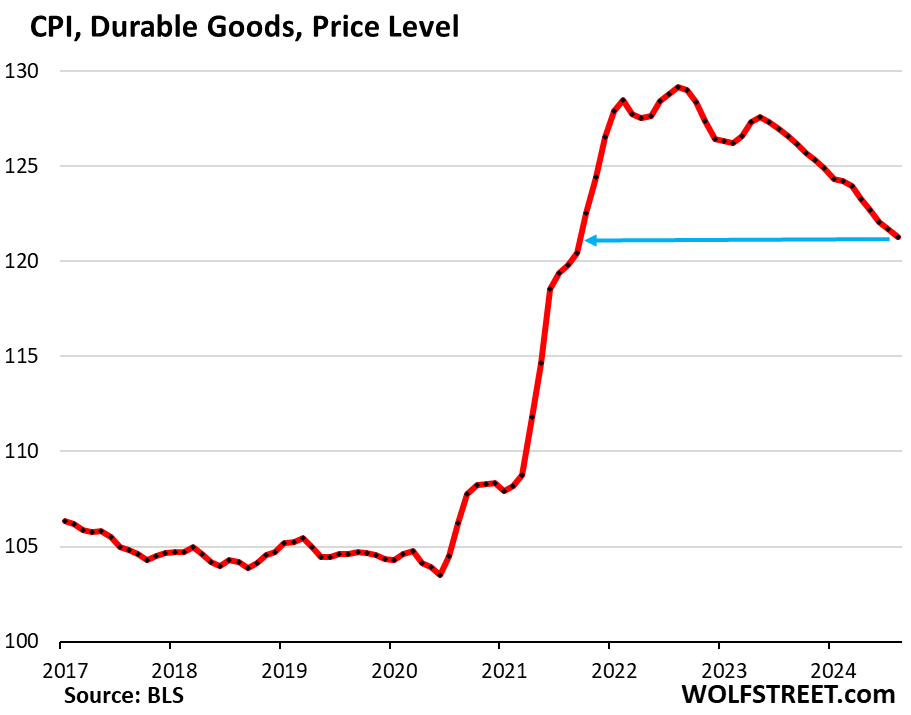

On the positive side of the inflation ledger were durable goods (motor vehicles, furniture, electronics, etc.), where prices dropped even faster in August, and energy, where prices dropped across the board, while food prices remained roughly stable, according to the Bureau of Labor Statistics today.

On a month-to-month basis:

- Overall CPI: +0.19% (+2.3% annualized), 2nd acceleration in a row.

- Core CPI: +0.28% (+3.4% annualized), 2nd acceleration in a row.

- Core Services CPI: +0.41% (+5.0% annualized), 2nd acceleration.

- Durable goods CPI: -0.36% (-4.3% annualized), a faster drop.

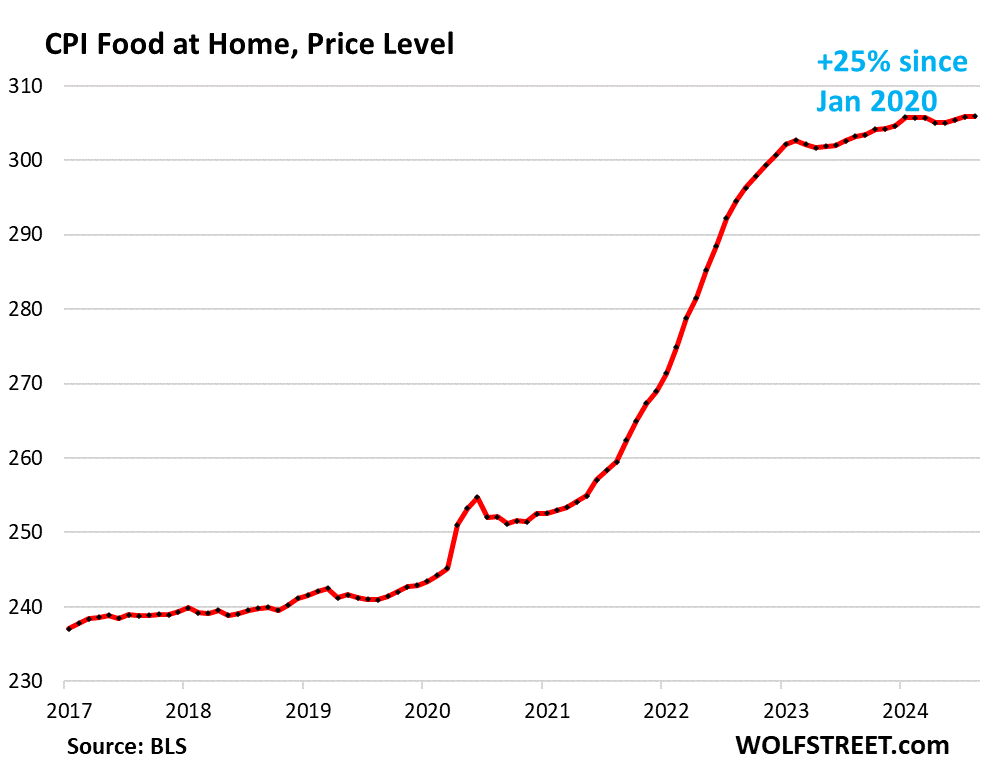

- Food at home CPI: unchanged.

- Energy: -0.78%, after being unchanged in July.

On a year-over-year basis, in summary:

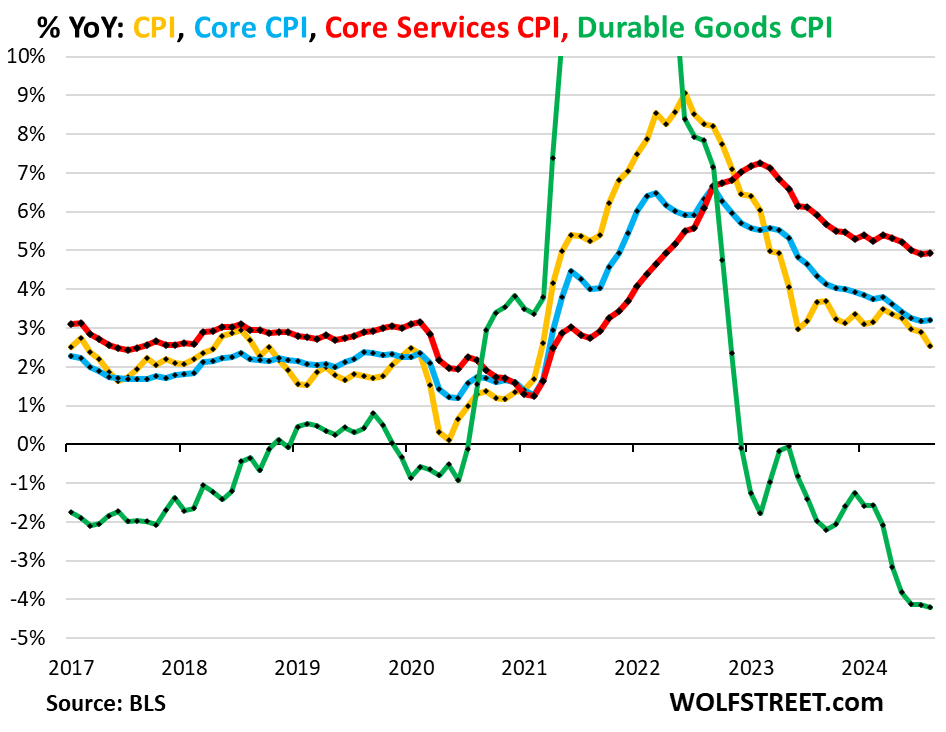

Core services CPI (red in the chart below) rose by 4.93% year-over-year in August, a slight acceleration from July (4.90%). It has been near the 5% line since December 2023. It includes all services except energy services.

Durable goods CPI (green) has been falling since mid-2022 as it unwinds the historic spike during the pandemic. Used-vehicle prices have plunged. In August, durable goods CPI fell by 4.2% year-over-year, a downward acceleration from July, and the biggest year-over-year drop since 2003.

Core CPI (blue), which excludes food and energy, rose by 3.20% year-over-year, a slight acceleration from July (3.17%), with services pushing it into one direction, and durable goods into the other.

Overall CPI (yellow) rose by 2.5% year-over-year, a deceleration from July, on a drop in energy prices and stability in food prices.

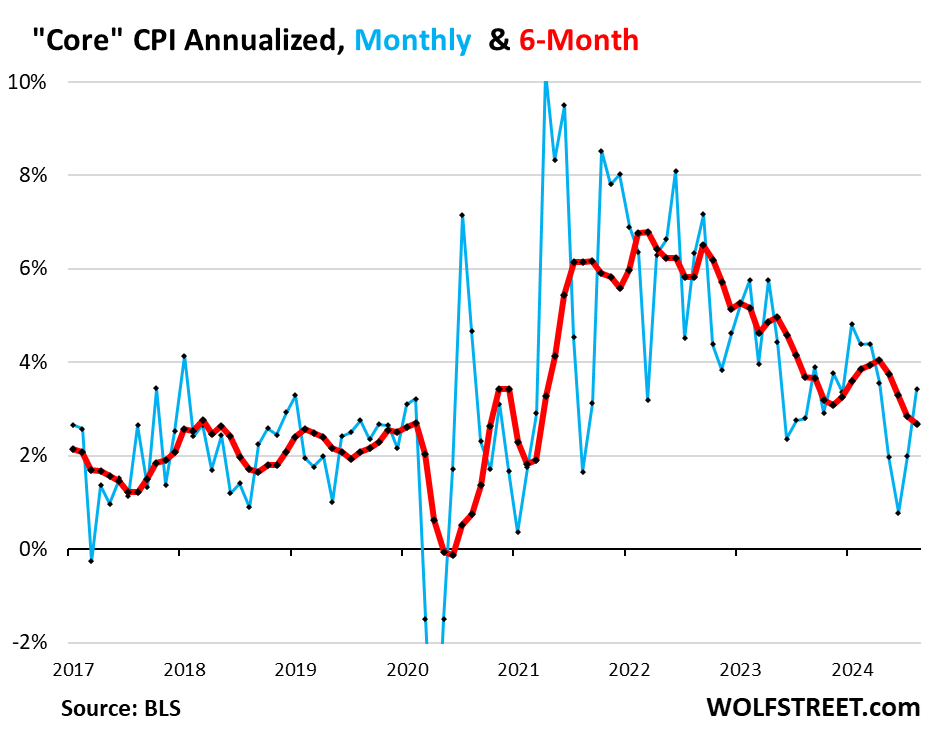

“Core” CPI, month-to-month.

Core CPI accelerated for the second month in a row, by 0.28% in August from July, or +3.4% annualized, the biggest increase since April (blue in the chart below).

The culprit for the re-acceleration was core services CPI, while the durable goods CPI continued to drop and pulled in the opposite direction.

The six-month core CPI, which irons out some of the month-to-month squiggles, rose by 2.7% annualized, as slight deceleration from July, as the high reading of February fell out of the six-month range.

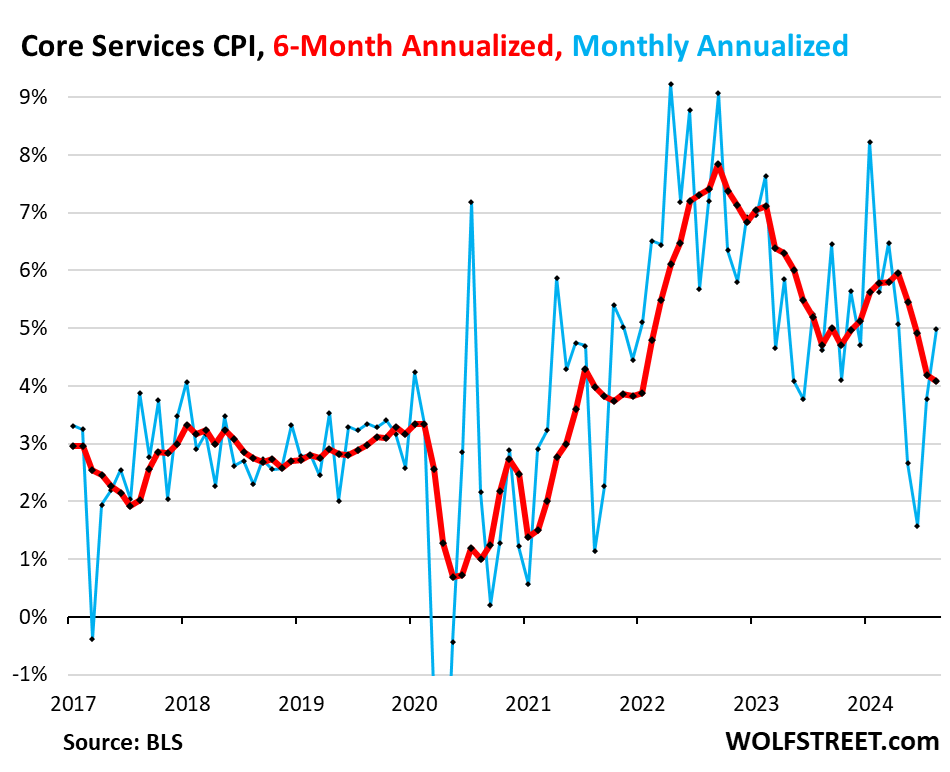

“Core services” CPI bounced for the second month.

Core services CPI increased by 5.0% annualized in August from July (+0.41% not annualized), the second big bounce-back from the outlier in June and May (blue line).

The six-month core services CPI decelerated a tad to 4.1% annualized, the smallest increase since January 2022 (red).

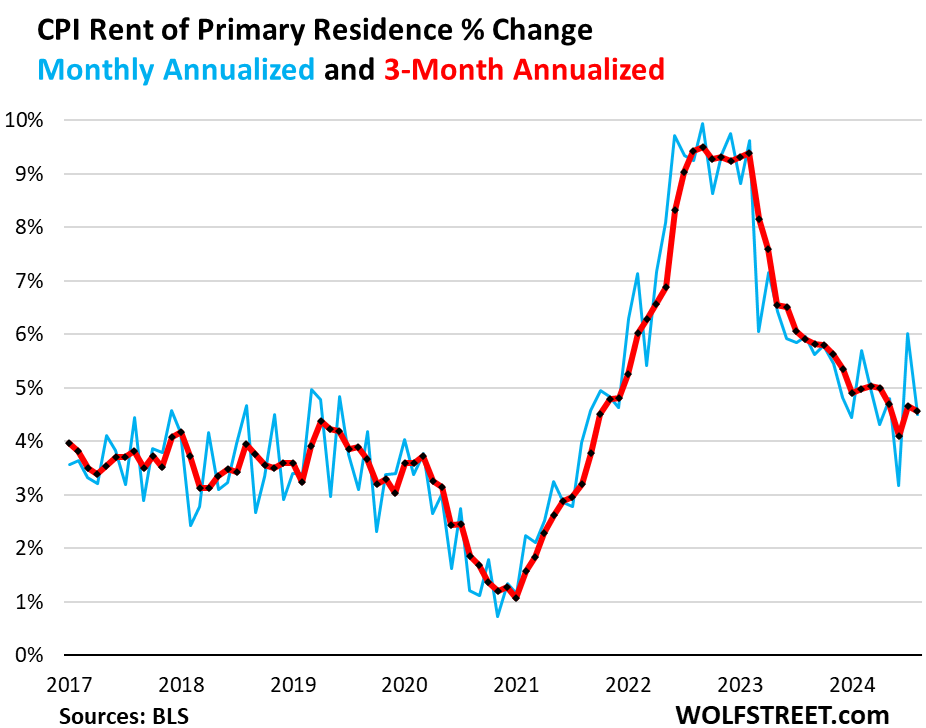

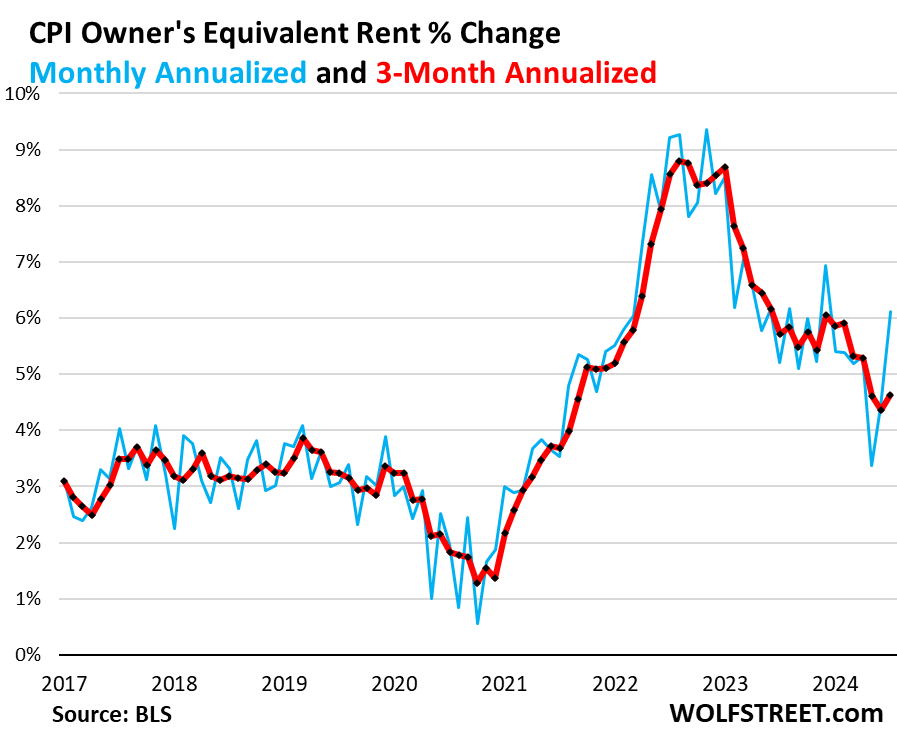

The housing components of core services CPI.

Rent of Primary Residence CPI decelerated, increasing by 4.5% annualized in August from July. It has been in the same range all year (blue).

The three-month rate rose by 4.6%, a slight deceleration from the prior month. After cooling a lot in 2023, rent inflation hasn’t cooled much this year.

Rent CPI accounts for 7.6% of overall CPI. It is based on rents that tenants actually paid, not on asking rents of advertised vacant units for rent. The survey follows the same large group of rental houses and apartments over time and tracks the rents that the current tenants, who come and go, actually paid in these units.

The Owners’ Equivalent of Rent CPI bounced for the second month, rising by 6.1% annualized in August from July.

The three-month OER CPI accelerated to 4.6% annualized (red).

The OER index accounts for 26.8% of overall CPI. It estimates inflation of “shelter” as a service for homeowners – as a stand-in for the services that homeowners pay for, such as interest, homeowner’s insurance, HOA fees, maintenance, and property taxes. As an approximation, it is based on what a large group of homeowners estimates their home would rent for, the assumption being that a homeowner would want to recoup their cost increases by raising the rent.

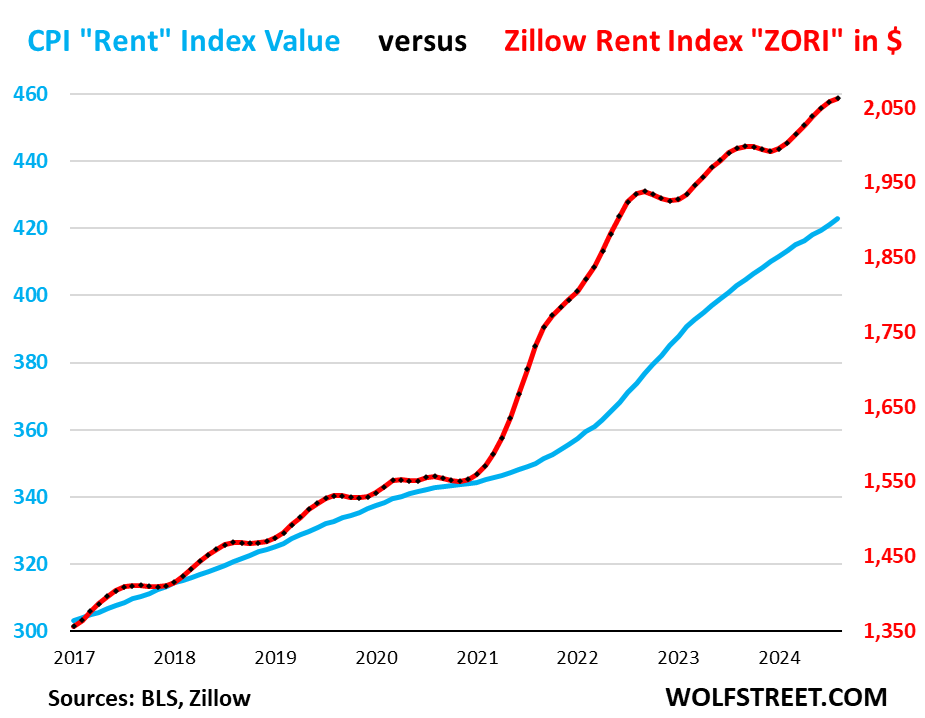

“Asking rents…” The Zillow Observed Rent Index (ZORI) and other private-sector rent indices track “asking rents,” which are advertised rents of vacant units on the market. Because rentals don’t turn over that much, the ZORI’s spike in 2021 through mid-2022 never fully translated into the CPI indices because not many people actually ended up paying those high asking rents.

For August, the ZORI rose by 0.22% month-to-month and by 3.4% year-over-year.

The chart shows the CPI Rent of Primary Residence (blue, left scale) as index value, not percentage change; and the ZORI in dollars (red, right scale). The left and right axes are set so that they both increase each by 55% from January 2017. The ZORI was up by 52% from January 2017, and the CPI Rent was up by 39% over the same period.

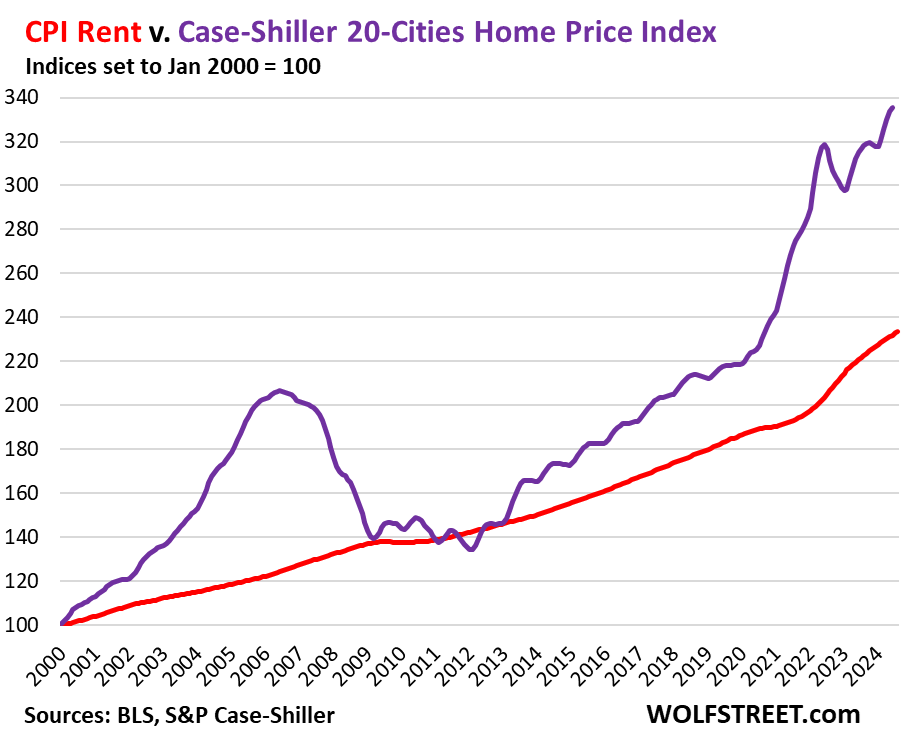

Rent inflation vs. home-price inflation: The red line in the chart below represents the CPI for Rent of Primary Residence as index value. The purple line represents the Case-Shiller 20-Cities Home Price Index. Both indexes are set to 100 for January 2000:

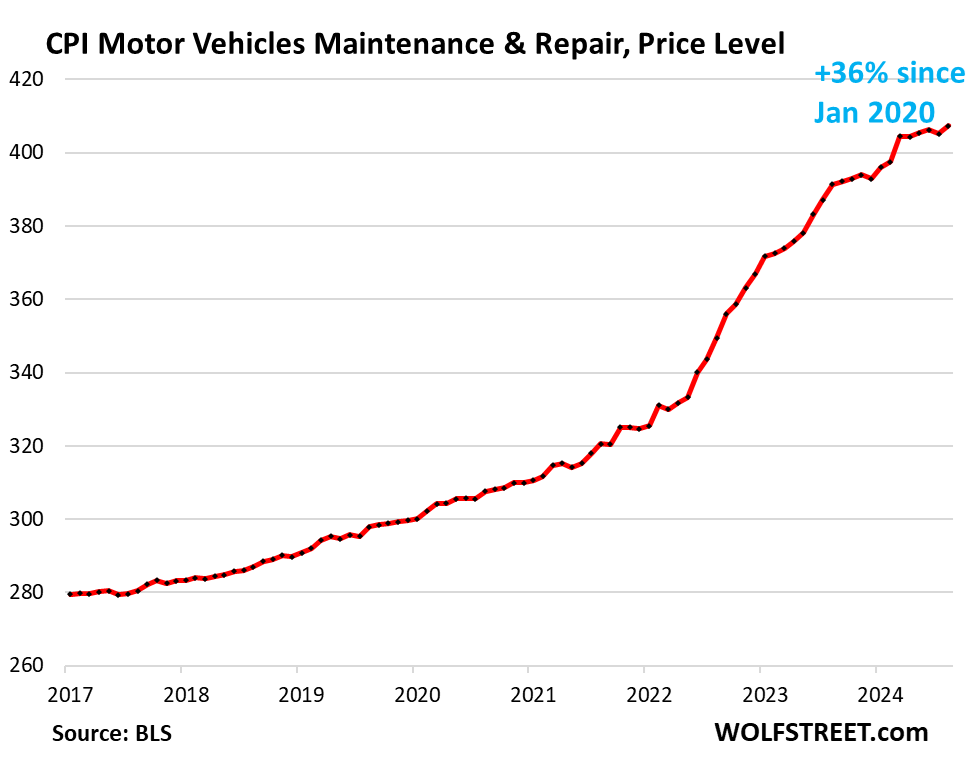

Motor-vehicle maintenance & repair inflation, after cooling for months, re-accelerated in August, jumping by 6.9% annualized from July. Year-over-year, it was up 4.1%.

Since January 2020, it has spiked by 36% as labor costs of auto-repair technicians have surged, and as prices of replacement parts have surged.

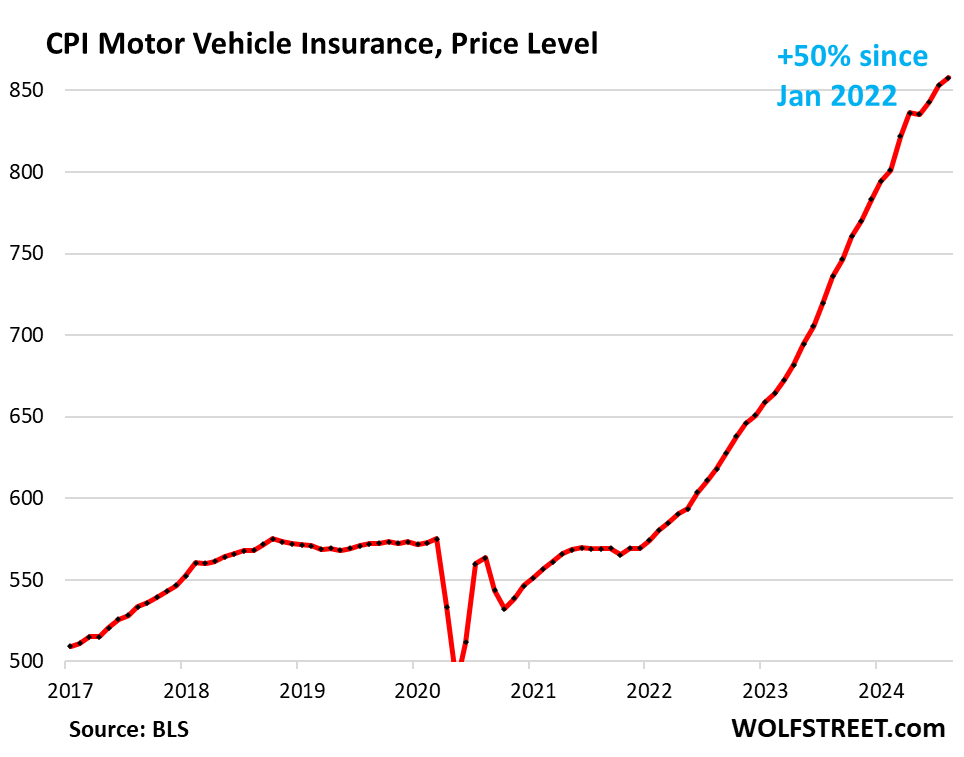

Motor vehicle insurance inflation continues to surge; it exploded in 2022 and 2023 because motor vehicle repair costs surged, and because used-vehicle prices (replacement values) had exploded in 2021 and 2022. And now it continues to surge because auto insurers are increasing their profit margins. For example, Buffett’s Berkshire Hathaway reported for Q2 that at GEICO, its auto insurance unit, big increases in premiums despite reduced costs of claims caused underwriting profits to more than triple!

- In August from July from June: +6.9 annualized

- Year-over-year: +16.5%

- Since January 2022: +50%

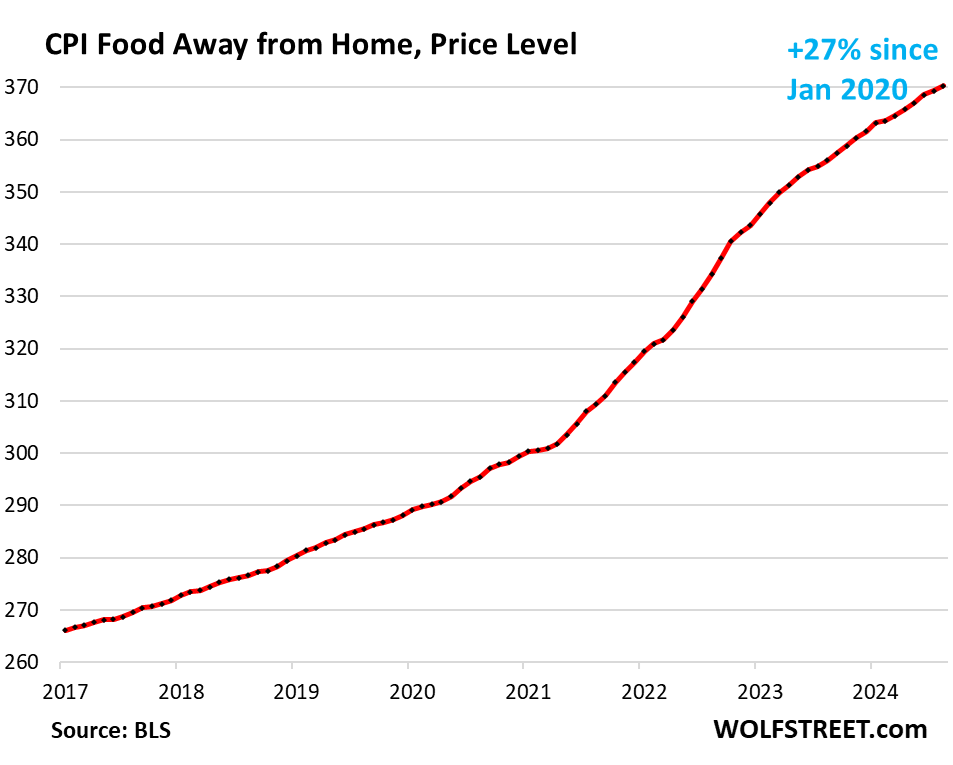

Food away from Home CPI – often called food services – includes full-service and limited-service meals and snacks served away from home, food at cafeterias in schools and work sites, food served at stalls, etc.

- In August from July annualized: +3.2%, an acceleration

- Year-over-year: +4.0%, in the same range around 4% for the past five months.

- Since January 2020: +28%.

Core services CPI has surge by 22% since January 2020. In a sign that services inflation has been very broad and went well beyond housing, Core Services excluding rent and OER have surged by 20%.

| Major Services ex. Energy Services | Weight in CPI | MoM | YoY |

| Core Services | 64% | 0.4% | 4.9% |

| Owner’s equivalent of rent | 26.8% | 0.5% | 5.4% |

| Rent of primary residence | 7.6% | 0.4% | 5.0% |

| Medical care services & insurance | 6.5% | -0.1% | 3.2% |

| Food services (food away from home) | 5.4% | 0.3% | 4.0% |

| Education and communication services | 5.0% | 0.2% | 2.3% |

| Motor vehicle insurance | 2.9% | 0.6% | 16.5% |

| Admission, movies, concerts, sports events, club memberships | 1.8% | -0.8% | 5.5% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 1.5% | 0.2% | 4.6% |

| Lodging away from home, incl Hotels, motels | 1.3% | 1.8% | 1.8% |

| Motor vehicle maintenance & repair | 1.2% | 0.6% | 4.1% |

| Public transportation (airline fares, etc.) | 1.2% | 2.5% | -1.1% |

| Water, sewer, trash collection services | 1.1% | 0.2% | 4.2% |

| Video and audio services, cable, streaming | 0.9% | 0.1% | 2.0% |

| Pet services, including veterinary | 0.4% | 0.3% | 6.0% |

| Tenants’ & Household insurance | 0.4% | 0.8% | 3.6% |

| Car and truck rental | 0.1% | -1.5% | -8.4% |

| Postage & delivery services | 0.1% | 0.5% | 5.5% |

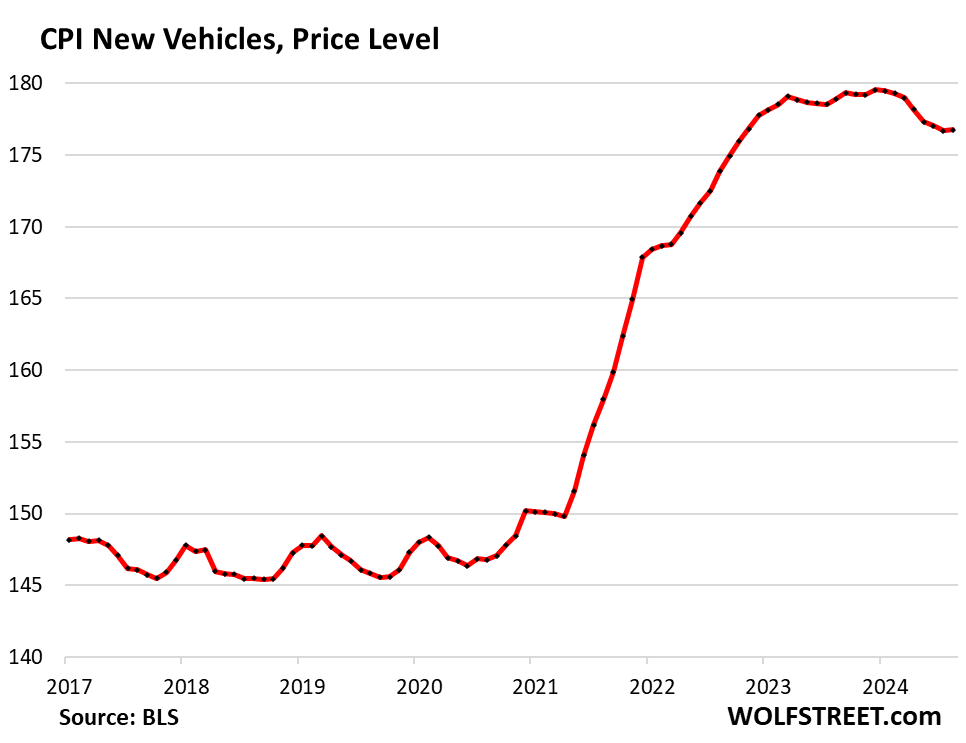

Durable goods CPI.

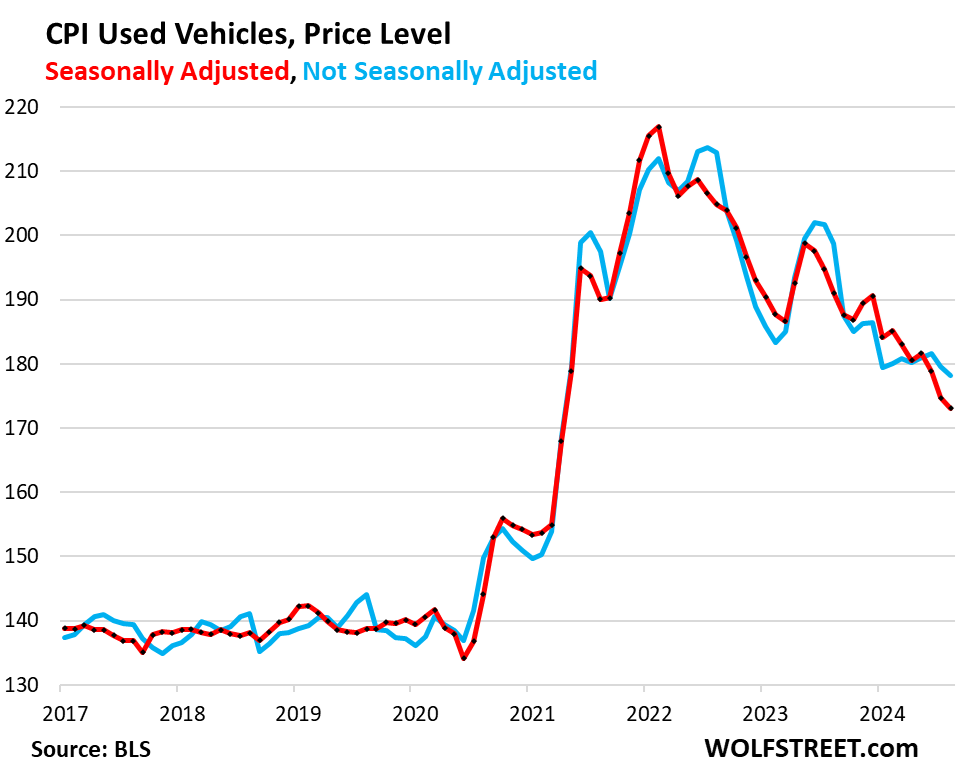

The durable goods CPI fell by 4.3% annualized (-0.36% not annualized) in August from July, and by 4.2% year-over-year, a downward acceleration from the prior month, and the biggest year-over-year drop since 2003.

New and used vehicles dominate this index. Other goods include information technology products (computers, smartphones, home network equipment, etc.), appliances, furniture, fixtures, etc. All categories have been experiencing price declines starting in late 2022, following the price spike during the pandemic.

From January 2020 to the peak in August 2022, durable goods prices spiked by 24%. Since then, they have unwound about one-third of the pandemic spike. Compared to January 2020, the index is still up 16%.

| Major durable goods categories | MoM | YoY |

| Durable goods overall | -0.4% | -4.2% |

| New vehicles | 0.0% | -1.2% |

| Used vehicles | -1.0% | -10.4% |

| Information technology (computers, smartphones, etc.) | -0.5% | -6.5% |

| Sporting goods (bicycles, equipment, etc.) | 0.0% | -1.9% |

| Household furnishings (furniture, appliances, floor coverings, tools) | -0.3% | -2.6% |

New vehicles CPI rose just a hair (+0.6% annualized) in August from July, after seven months in a row of small declines. Year-over-year, the index fell by 1.2%.

Prices of new vehicles have been sticky after the blistering spike from early 2021 into early 2023 – unlike used vehicle prices – and have only given up a little ground since the peak, despite the glut of new vehicles on many lots, and amid calls for big incentives and discounts to move the vehicles. The index is still up 19% from January 2020:

In the years before the pandemic, the new vehicle CPI zigzagged along a flat line, though vehicles were getting more expensive. This is the effect of “hedonic quality adjustments” applied to the CPIs for new and used vehicles and some other products (see our explanation of hedonic quality adjustments in the CPI).

Used vehicle CPI, seasonally adjusted, dropped in August from July by 11% annualized (-0.96% not annualized), and by 10.4% year-over-year, a slower decline than in the prior two months (red).

Not seasonally adjusted, used vehicle prices fell 8.9% annualized (-0.77% not annualized) in August from July (blue).

This decline may not last much longer. On the wholesale side, private-sector data from Manheim, the largest auto auction in the US, showed big price increases in August, as retail inventories have tightened and dealers tried to restock, amid strong sales. These higher wholesale prices will filter into retail prices and into CPI, which reflects retail prices, over the next few months.

Used vehicle CPI has now given up nearly 60% of the spike from January 2020 through January 2022, but is still 24% higher than in January 2020. Wholesale data indicates that this may be about as good as it gets going forward.

Food Inflation.

Inflation of “Food at home” – food purchased at stores and markets and eaten off premises – has essentially flattened out this year at a very high plateau.

| MoM | YoY | |

| Food at home | 0.0% | 0.9% |

| Cereals, breads, bakery products | -0.1% | -0.3% |

| Beef and veal | 0.3% | 4.2% |

| Pork | 0.1% | 1.8% |

| Poultry | 1.0% | 0.9% |

| Fish and seafood | 0.2% | -2.3% |

| Eggs | 4.8% | 28.1% |

| Dairy and related products | 0.5% | 0.4% |

| Fresh fruits | 0.7% | -0.6% |

| Fresh vegetables | -1.1% | -0.4% |

| Juices and nonalcoholic drinks | -0.5% | 1.8% |

| Coffee, tea, etc. | -2.2% | -2.1% |

| Fats and oils | -0.9% | 2.4% |

| Baby food & formula | -0.5% | 3.7% |

| Alcoholic beverages at home | 0.0% | 1.9% |

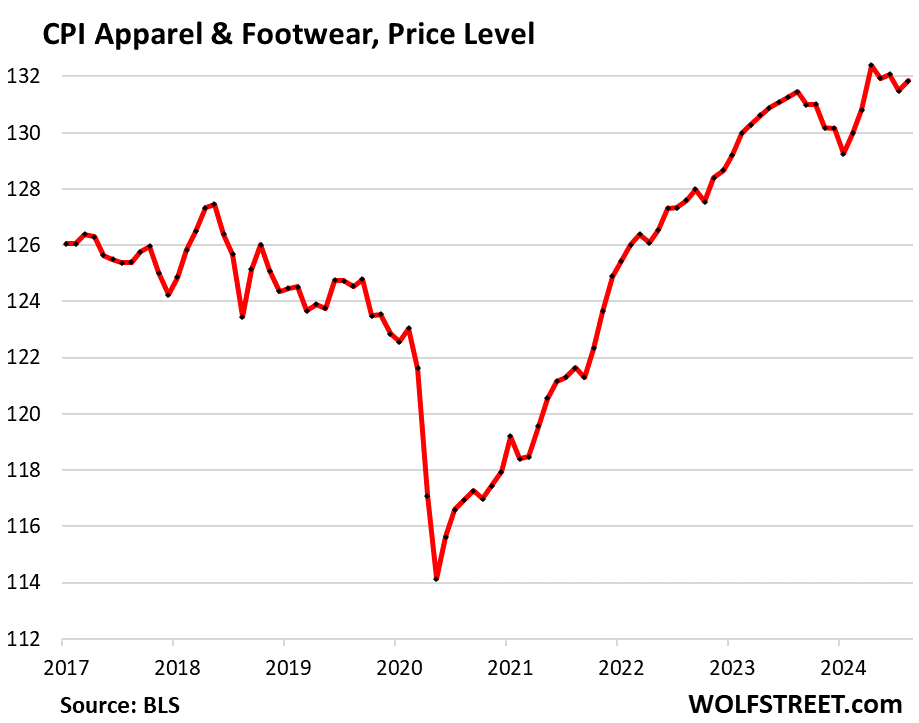

Apparel and footwear.

Apparel and footwear are components of nondurable goods, along with food, energy products, household supplies, and other stuff.

Month-to-month, the CPI for apparel and footwear rose by 0.29%. Year-over-year, the index was about flat. Note that prices trended lower in the years before the pandemic. That trend seems to have ended:

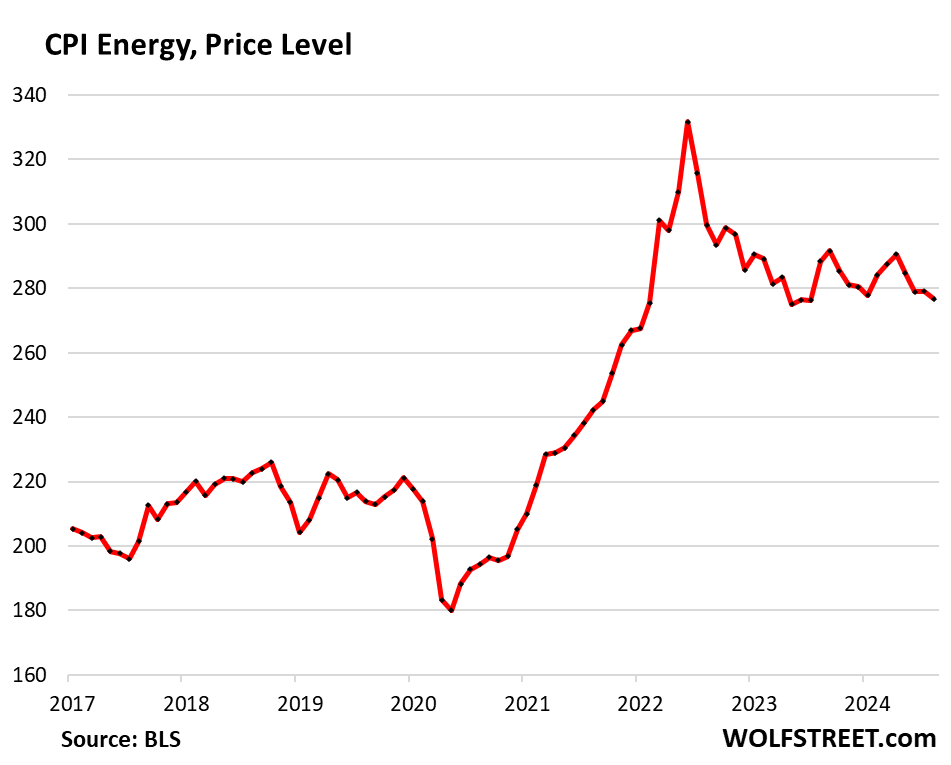

Energy.

| CPI for Energy, by Category | MoM | YoY |

| Overall Energy CPI | -0.8% | -4.0% |

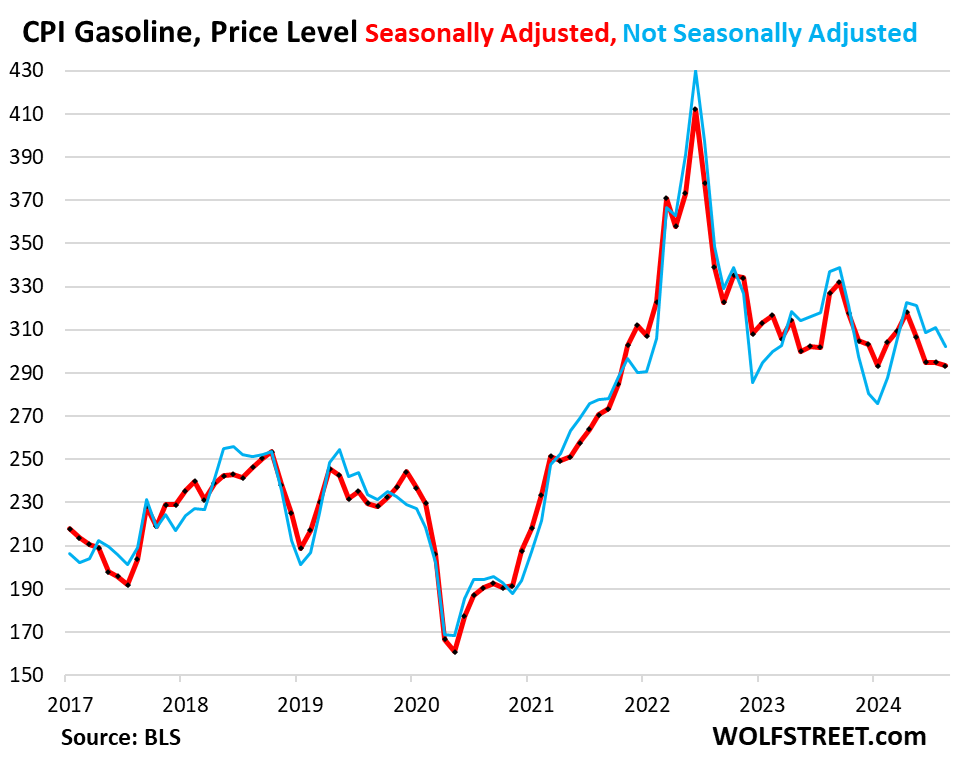

| Gasoline | -0.6% | -10.3% |

| Electricity service | -0.7% | 3.9% |

| Utility natural gas to home | -1.9% | 0.1% |

| Heating oil, propane, kerosene, firewood | -1.5% | -7.0% |

The CPI for energy covers energy products and services that consumers buy and pay for directly:

Gasoline prices, which account for about half of the energy price index, are very seasonal. Seasonal adjustments are trying to iron out the seasonality. We’ll look at both.

Not seasonally adjusted, gasoline prices fell in August from July (blue). Seasonally adjusted, prices also dipped (red). Since the top of the spike in June 2022, gasoline prices have dropped 29% (seasonally adjusted):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Core CPI a far cry from 2%. But let’s cut anyway.

If your argument is that they should pick and choose where a given component of inflation is relative to 2% rather than overall CPI, doesn’t it make just as much sense to choose, say, durable goods? If they use that component then we should be looking for a massive cut in interest rates next week.

Core CPI exists to measure general inflation in the economy without volatile food and energy prices. Durable goods are a part of Core CPI, just like everything else except food and energy. So no, it doesn’t make just as much sense to choose durable goods. Given the volatility of food and energy prices, Core CPI at 3.2% should be a concern for the Fed.

Food and energy, two of the most essential goods with actual market prices should be excluded, yet OER, something no one pays, and isn’t a market price is ok. You’re cherry picking.

Core CPI is not cherry picking, it’s separately stated for the very important reason I stated above: volatility. Core CPI excludes two highly volatile items to better show inflation in the general economy. Whether it does is arguable, but that’s why it’s reported separately from CPI. Cherry picking is asserting that “durable goods” or “OER” are somehow analogous to Core CPI as a measure of inflation.

This morning and this afternoon I was out back raspberry picking. Mid day I was out front apple picking.

Probably a bit too far north for cherries though.

Had to look it up. The U of MN fruit breeding program released two cherry varieties way back in 1950 and in 1952. Nothing in the works these days and these varieties were best suited for baking, rather than eating fresh.

Lucky for us we can avoid buying food and energy to reduce the financial strain of both food and energy. I wonder if I can BBQ my washing machine in lieu of food. (This is sarcasm).

Well as long as the gamblers on wall street are happy, which in turn makes the congress critters happy; that’s the important part. The working class can eat bugs.

“Far cry”? It’s 1.4% over target, i.e., less than double. Opinions vary, but it seems like a “near cry” to me.

As for when to cut: again, opinions may very, but it seems inarguable that restrictive policy should be eased -before- the target is reached, to avoid drastically overshooting. Rate decisions are about trying to predict the future, not about trying to reverse the past.

It’s kind of like applying your car brakes: if you wait until you’ve reached the stop sign, then you’ll definitely not stop in time to avoid cross-traffic.

“It’s kind of like applying your car brakes: if you wait until you’ve reached the stop sign, then you’ll definitely not stop in time to avoid cross-traffic.”

No, it’s not. That’s a stupid analogy. There is nothing wrong with deflation. In fact, it would help most. But the asset holders – the people who control public policy – wouldn’t even hear of that because it would adversely affect their net worths, so they spin tall tales about how bad it would be.

OK, if you want deflation, then people need to give up their recent wage gains too. Falling wages are part of deflation, just like rising wages are part of inflation. But when wages are falling, people suddenly cannot make their mortgage payments — you know the house they bought a few years ago, and now their wages are falling, and their mortgage payments are fixed.

Deflation in manufactured goods is kind of normal due to manufacturing efficiencies. But overall deflation across the board entails falling wages.

Deflation for thee but not for me. You’ll be left wondering why everything is cheaper but you still can’t afford it.

If a rising tide lifts all boats what do you think happens when the tide goes out?

Thank you, Wolf. I have no idea where this notion that deflation is harmless, let alone “would help most” people comes from, but it’s ahistorical nonsense as any familiarity with several episodes during the 19th century and The Great Depression ought to dispel.

“OK, if you want deflation, then people need to give up their recent wage gains too.”

Absolutely I do. Undoubtedly.

Depth Charge,

LOL. You go first.

Give up 20% of your income to to get 20% lower insurance premiums and food costs. Used cars and trucks have already come down by more than that, and so have some other things, so they don’t need to change but might go up along with your falling wages. But your mortgage payments stay fixed because you cannot renegotiate the price of the house you bought years ago. Maybe you can refi the mortgage at a lower rate, might save some. but if you have a 3% or 4% or even a 5% mortgage, good luck.

You think rising prices are bad. Wait till the overall population gets lower wages year after year. That has a huge psychological impact. It’s depressing. People stop buying stuff, and so jobs vanish, and everything heads lower.

But be my guest, rather than imposing your dreams of lower wages on me, find a lower-paying job yourself, and then next year find an even lower paying job, etc., to see what it’s like. And then watch prices decline of things you cannot afford anymore anyway. You crack me up sometimes.

Wolf, you miss the fact that in deflation, when prices and wages fall, people with cash in the banks win. Buy assets when there is blood in the streets.

Wolf, most people I know did not get *any* raises during the last 3 years, other than maybe 1-2%.

How do you even know what raises they got??? Do you sit down, the whole bunch of you, and you show each other your paychecks?????

Obviously. The thing folks don’t understand is that deflation occurs WAY faster than inflation and is MUCH harder to reverse. Think speed of balloon inflating compared to speed deflating when punctured.

Japan has been trying to reverse deflation for 20+ years. They have even tried ‘helicopter money’, free certificates for goods that must be spent or they expire.

There are a lot of people who you do not want controlling an industrial process or being at the helm of a super tanker, where it takes a mile to stop from when you begin reversing engines.

Hahaha! Fantasy much?

– Imprecise information (think recent revisions)

– Counter-cyclicality of separate industries

– Career aspirations of institutional leaders

– Often faulty economic theory

– Experimentation (“hail-mary”) actions during perceived emergencies

– Pro-cyclic history of past central bank manipulations

I can’t help but believe that letting the market set it’s own rates (laissez-faire), with all it’s violent but brief ups and downs, would be better than centralized interest-rate, balance-sheet manipulation, and stabilization policy.

It’s not whose at the helm, but the structure of the tanker that is problematic.

And yes, Japan is a great example. Argentina too.

(Let the arrows fly!)

Bailouts are preferred over deflation.

The Fed is not the government. It didn’t deal the cards, it’s just managing with what it’s dealt by a population that wants goodies. This population will punish politicians who try to tighten spending. Maybe think of the Fed as the business manager of a spendthrift rock star.

Sure, you can argue that there should be a recession, to clear out the excess but it is not within the Fed’s mandate to create recessions.

Hear here!

I have always found that food and energy is volatile, they are measurable and therefore must be included in CPi if u want more info about inflation.

The assumption underlying core preference is that this volatility all “evens out over a year” Do the numbers always bear this out? Food especially has been on a muti year upward trajectory, it’s crazy to pretend this doesn’t exist so they dont have to explain uncomfortable truths.

Also, the two items that every lower or middle.class citizen gets directly affected by this volativity and makes up a disproportionately larger impact of their discretionary spending than wealthier folks, I’m lucky I can shrug my shoulders but it matters for the majority.

I think the real problem is the core services CPI. It is stuck and not going down, because housing inflation is absolutely horrible. Without deflating the ultra-mega-hyper inflated asset bubble (re, stocks, crypto) it is near impossible to solve the housing inflation and core services will remain stuck. But there is absolutely no intention to deflate this bubble, because nearly all the party funders and vast majority of the voters are asset holders. An average voter, may complain about the grocery, hospital and utility bills going up, but the price appreciation they see for their homes on zillow is much more and balances it out. You can surely understand this from “owner’s equivalent rent”. Hence, most of the voters are happy.

So, we will have to leave with inflated assets -> inflated housing -> inflated services and inflated wealth disparity. A sharp QT could solve the problem, but it is too little, too slow.

Why are political hallucinations allowed? I could reply in kind but then the entire site degenerates.

Possible late 1970’s through 1980 down & rebound / head fake brewing. Look out, JPowell! Don’t cut rates too fast. Make sure you’re data driven.

Powell is WS friends driven.

Either sex elk tag & Buck tag Muzzle loading leaving tomorrow. Trying to just escape some semblance of inanity for 10 days.

Gonp – Bow season starts down my way 9/28. I can’t wait!

He’s not Greenspan, he’s bad at data!

Very informative. It seems that high services inflation in a service based economy is not a problem anymore? Ok then.

Inflation will come roaring back as soon as oil goes back up. Right now wall street is acting like china is slowing down and will never use oil again. But we know this is just a cycle.

Cheaper oil means everything gets a little less expensive. The fact that inflation is still 3.2% should be concerning.

Hard for oil to go up in a sustainable manner as US frackers keep hitting new production records. The US is the largest oil producer in the world, and the production isn’t run by a monolithic state-controlled national oil company, but by thousands of small and big companies that all want to maximize production and revenues, and they cannot be controlled, hence overproduction. This has already caused two massive oil busts (2014-2016) and 2020. It’s hard for the price of oil to rise in a sustainable manner because a higher oil price will just unleash more funding to go into fracking and unleash even more production. So we say in the US: the best cure of a high oil price is a high oil price. Works every time.

In other words… Capitalism works!

On the flip side, Wolf, don’t occasional supply disruptions rearing up still cause “transitory” oil-price spikes — leaving us with a medium term range of say $50 to $150 per barrel.

That still leaves Harrold’s inflation comment possible or likely, doesn’t it?

John H.

There were no real supply disruptions in decades. Everyone has got oil coming out of their ears. No one ran out of oil. There were no gasoline shortages with people waiting hours to get two gallons of gas, anywhere in the developed world in recent history. That last happened when OPEC still ran the show in the 1970s. It hasn’t happened since the US became a top oil producer. Any “supply disruptions” are just rampant speculation, market manipulation, and fear mongering by the betting community that makes huge amounts of money on directional bets. And they can cause prices to spike briefly. This happens in commodities all the time. But that doesn’t make for a lasting higher price, just price spikes and plunges. I thought that was clear by now.

I don’t disagree that extractive technological gains make a huge difference.

My concerns center mostly around geopolitics and world-wide energy policy (local, regional, federal, and international). Disruptions in these areas are as unpredictable as they are inevitable…

blah, looks like WS initially didn’t like this but shrugged it off later in the session and likely turn this into another barely down day because they know these numbers won’t budge at all from the planned 25 basis points cut and there’s still hope for a 50 basis point cut.

It feels like Pow Pow is soon going to find out soon enough the joy of cutting then eating his words again and raising again if this picks up even more…good times

Nvidia CEO came out with a market-boosting comment about huge demand for Nvidia chips. Check it out. The whole market is run by Nvidia. That’s what triggered the recovery of the S&P 500. It’s like, forget CPI, we’ve got a morsel from Nvidia.

Jesus, this kind of stuff needs to stop…between all the tech bros running their mouths and blatantly pumping their stock, one day it’s Jen-Hsu, then Zuchniniberg then back to Musk promising we will have all $50K robot by next year just so stock can rocket up while they cash out…

Market and most BTFD retailers are something else too, fool me once, fool me 10000x times, let me still chase the hype…

Well, don’t eorry, the Fed is going to tamp down on this raging irrational exuberance by cutting interest rates. That’ll learn ’em!

Cmon, make some chang on the way.

Harness the sand worm that is Nvidia!

*change

💵 💰 💴

It would probably help if people started talking more about the increasing correlations between the Big Tech players.

They *do* have real revenues *but* considering that a very large percentage of Nvidia’s revenues come from a pretty damn small number of major players with significantly elevated PE ratios themselves (Microsoft, Google, Facebook, etc.) the groundwork is there for a downward domino effect (if any of the 3 or 4 decide they’ve pissed away enough tens of billions trying to re-invent the MS Paperclip Man using Underpants Gnome AI hardware).

Even Facebook eventually stopping huffing its own paint over the Meta-land? Meta-sphere? Meta-dongle? Meta-verb? Meta-vibe? Metaverse.

Yes, the Human Condition is creative and adaptive, informed and naive, some are ruthless. The perils of spontaneity be darned in this case.

Totally agree. When all this unwinds with forced buying for NVDA via passive funds this could as ugly as the 2000 dot com bubble.

Well they only have 2.5,5 or 15% of Nvidia from what I’m seeing.

So the risk is at least spread out a bit.

The upside is magnifique’. Downside would be a blip. But anywho! We’ll see

Hopium is strong with the individual below who believes companies trading at 50x fwd earnings would merely ‘blip’ down with a 2-15% drop in revenue. Someone doesn’t understand equity valuations.

It didn’t look to me like it was just Nvidia that brought the market back, but it was a heck of a reversal, the QQQ had a swing of $18 (WTF??!!) from the low to the high. The Dow almost broke 4K, so it was more than NVDA. But it’s incredible to see the QQQ finish up $10 when the DIA finishes only up $1 and the IWM only up 60 cents.

NVDA is just an options traders’ gambling instrument now. I don’t see it making a new high, and I’m staying with call that the S&P is a LOCK to see 4500 again.

Nvda was 42% of the s&p gain yesterday — which demonstrated the stupidity of a broken index that isn’t diversified — but gaining in risk exposure

Let the buyer beware

What else is nvidia’s founder-ceo going to say besides pumping his own company? Even as revenues were plummeting in 2018 & 2022, he continued talking about rainbows & unicorns.

The lemming effect.

We have seen this movie before.

You think they’ll actually raise again once they start cutting? At best we’ll maybe get a hold and wait and see, bad data will be called transitory and outliers until inflation is considerably higher again. Look how long it took them to raise initially….

Corporate layoffs cause unemployment to rise, CPI services come down, and we have a recession, and deficits explode, but durable goods, that one is the biggest head fake of all but provides some cushion when people lose their jobs. Even when people lose their jobs the wage increases will stick.

Olive oil jumped many months ago and hasn’t budged since (we’re big consumers), so the month-to-month price change was 0%. Not sure about butter, we consume little. Lots of other dairy has dipped in recent months.

Your second sentence is typical BS.

Is the current course a recipe for Stagflation?

No. GDP growth adjusted for inflation was 3.0% in Q2. For Q3, Atlanta Fed GDPNow estimates that it might come in at 2.5% adjusted for inflation. Both are far above 10-year average growth of 2.0%. For stagflation, you need to have two components: “stagnation” and “inflation.” We’ve got one, “inflation,” we don’t have the other, “stagnation.”

It’s the reason why we don’t see “stagnation” that concerns me, because I assign as that reason, federal deficits north of 6% of GDP when GDP is coming in at ~3%. I think absent those sizable deficits, we would be seeing stagnation.

Absolutely! Deficits are the elephant in the room that everyone ignores at their peril.

Not yet😈

Housing prices have decided that they will not be dropping, all the circling buzzards waiting for this price drop have left, disappeared, word is the buzzards have been eaten by the new Immigrants, the black swan has also been killed off. The “goose has been cooked as well.

Let’s cut the rates a bit, the migrants need it so they can work…get a job, if it doesn’t work out, well we can raise the rates again.

Wolf, any idea why the US treasury bond yields are falling so much? 10 yr down to 3.676% as I write this. Do you think the bond market might be sniffing out lower inflation down the road?

I was not asked, but bond market had 5 cuts for damn sure in 2023. The bond market may be sniffing, but what I can’t tell you…

Good point dougzero….all the collective wisdom of the bond market can be wrong. Question is, it right or wrong this time?

So actually right now, the 10-year yield is up a smidge. Been bouncing up and down today from 3.61% to 3.69% on CPI kneejerk at first, then drop back to 3.62%, then jump back to 3.68%, then tapering again, now 3.66%, still up a little for the day, like whatever.

There were lots of people not long ago talking 5%+ 10 year UST. Just wondering if some of those folks are still thinking that? And their time line for that happening? My crystal ball is cloudy as usual :)

Maybe China’s apparent continued economic slowing causes less inflation? Job market not collapsing, but maybe loosening a bit? Will the American consumers keep carrying us indefinately?

anyone who buys 10 year treasuries for 3.676% is an idiot, just like anyone who buys nvda at these stupid valuations because the ceo comes out with some nonsense about “incredible demand” is an idiot.

how much of nvidia’s demand is from the other mag7?

i don’t want to abuse wolf’s site, but wall street has turned into a huge circle j_rk.

Well those who do not own stocks cannot gain nor lose.

But can complain.

It’s all about risk

The top 10% of wealthy individuals own 90% of individual stocks. Or so I read on a blog today. Something about a Gini index…

what does that have to do with the bond yields?

Franz NVDA is a stock (business).

Above ppl were complaining about it.

I am sure the RE industry and hold-out home sellers will love this….30yrs mortgage rates will go even lower. This is the only lifeline they have left to have a fighting chance to move those overpriced houses without lowering prices. So far with the minor drop, it’s not doing them a favor but if it can get to below 5%, who knows, they might just come out ahead in this Mexican standoff…

Any mortgage below 5% is a no brainer in IMHO. Not sure if it will ever happen again but then again I never thought I would see ZIRP where a bank would pay you interest to take out an mortgage. This actually happened in a few place in Europe.

Yeah, it’s those nifty low interest rates that helped supply jet fuel to prices in housing, giving us a a bubble redux.

Example: I’m looking at a house I had earmarked way back 2011 in 90046 zip code. It sold for $670K and then doubled in price six years later.

Once rates fall to some magic number, will the market become flooded with the shadow inventory that’s been on the sidelines? And if so, what will that do to home prices?

Paradoxically, a significant drop in rates could be the very event that bursts the housing bubble.

Mortgage rates are certainly down. They’ve been sinking steadily for a while now, despite rate cuts being “thoroughly priced in.”

Barely — just enough to rope a dope.

Nah. More like enough for builders to remove any incentives.

Backroad, market emotions are turning more negative (ie. Pricing in a slowing economy and lower rates – or positive, lower inflation). Either way, since the fed follows the markets, they’ll be cutting to catch up with the lower rates.

Cut too slow = recession. Cut too fast = inflation rebound.

The bond market is sniffing out a weakening job market which typically leads to recession

Problem is inflation is unlikely to stay reliability at 2 percent so that’ll be a problem again in the future.

Technically speaking it’s a corrective bounce or dead cat bounce if you’d like

Apartment rental inflation is the real killer.

Rent (or home mortgages) being the biggest chunk of anyone’s income, when you find yourself faced with a $5000/yr raise in your home expenditure, that’s going to fuel a shocked reaction of paranormal proportions.

Somebody clearly said to the businessmen of the world, now is an ideal time to price-gouge the public. And the public went along with it in sectors like used-cars (which were selling for outrageous rates, almost comparable to new cars), accepting the lack of competition and the general secret agreement to price-gouge. It is the unscrupulousness of business owners that has always been one of the Achilles’ heels of the free market, dating before modern capitalism, and it is the weakness of the consumer that has always been his bane.

You don’t need a secret agreement. What you need is the general public to have an expectation of price increases. Once that expectation is set, you can increase prices and they won’t even blame you. And your increase helps maintain that expectation. It is a cycle that is very hard to reverse.

Looks like Social Security raises are on track for next year to increase at 2.4%. That will sure help with my 25% car and home insurance increase in August and 6% food increase this year and 9% car repair increase this year and 5% utility increase this year and ….

So buy gasoline, which has plunged, Buy a used car, those prices have plunged. Buy a laptop, whose prices have plunged. Etc. People only care about the prices that have risen. No one ever looks at prices that decline.

But yes, homeownership is a money pit. It’s an expense that keeps on rising. Did no one ever tell you that?

But if you’re a cycling Luddite with a creeping grocery bill, those choice other items are cold comfort at best.

Because everyone and their mom are convinced that for some reason a house is a money printing machine and just like nvidia it will go up, up and up, nevermind property tax, insurance, HOA will also only go up up and up and never down…..

Those kool aid are sure delicious though…

For people who already own cars and laptops that price deflation means nothing.

My car ins went up 40% yoy with no traffic citations, it’s an old car so I just took off collision coverage and now I’m paying what I was last year for significantly less coverage on a car that’s a year older and worth even less than the year before. Shouldn’t as your car becomes worth less the insurance become cheaper? Luckily I can afford it, but for those who are on a more fixed income that’s just ridiculous – especially with replacement cost on vehicles dropping as they age.

Bread too expensive? Buy cake!

MM1,

Sure auto insurance went a bunch. We’ve discussed this endlessly. Auto insurance is included in CPI, DUH!!!. RTGDFA, at least look at the picture for auto insurance, it’s up 50% since Jan 2020.

That’s what this article is all about.

But eat something healthy: The price of fresh fish and seafood dropped mom and yoy. Fresh fruit and vegetables also dropped mom and yoy. We buy lots of fresh fish, fruit, and vegetables, and the CPI for them seems about right, lower than a year ago. We just had black cod (butterfish) Saturday night when we had friends over for dinner, which we love to serve since it’s delicious and easy to prepare, bought fresh hours before, cheaper than a year ago.

Also, to keep your tastebuds active, enjoy some good coffee, roasted coffee dropped mom and yoy.

“Shouldn’t as your car becomes worth less the insurance become cheaper?”

Kind of a selfish outlook since the mandatory part of insurance is to reimburse OTHER people for their damaged cars & medical bills should the driver happen to hit them.

Now if a person on a fixed income cannot afford to insure the risk they’re presenting to other people while on the road, isn’t that the kind of situation where we DO want them to stop driving?

Or would you prefer poor people driving around hitting things & people (as is inevitable), but the the victims are out of luck because the guy who caused the accident says “but my car is old and cheap, so I shouldn’t be responsible for your rising medical bills!”

@Grant taking collision off means they don’t fix my car in an accident if I hit someone. Liability insurance is what covers the other persons car and injuries, which is required by law. Also not poor, just not paying an insane an extra couple of hundred $ every six months plus a $1K deductible when my car has a 190K miles and is worth about 5K. Again not poor, just own a Volvo that will run forever.

As for the poor, I assume if you think they should stop driving, then they should also stop working too? Because how else would they get to work in a lot of our cities which don’t have a great public transportation? I assume you also think if they can’t work we also shouldn’t send them money? So then they should starve? Unfortunately cost of transportation and auto insurance is a necessity for a lot of the population.

Mine too. I complained to my agent. They offered me dropping collision and the difference when I asked was trivial. Seemed like a bad bet.

I was told it went up so much because the car was older and it was likely an accident of any kind with higher repair costs would total it. So they had more risk. My reply was, hey would that mean if I buy a somewhat newer car, like 5 years newer insurance would be less? Well no it wouldn’t. So I said you just told me a story you hoped I would believe. Did not get a reply to that. Certainly with Wolf’s documented drop in used car pricing their cost of totaling it is lower than a year ago.

@Wolf prices might be different in different parts of the country. I cannot get fresh fish for cheap unfortunately but that sounds delicious. Also I generally do only eat healthy produce.

Last nights salad:

Kroger

organic spring mix 2024 -$5.99 2020 $3.99 on sale frequently to $4.99 full price

organic cheery tomatoes – 2024 $3.99 for 10oz 2020 $2.39 for 12oz

organic kalamata olives – 2024 $3.99 2020 $1.99

red onion – 2024 $1.69/lb 2020 varied but under $1/lb

organic red bell pepper – 2024 $3.29 2020 $1.99-2.29

crumbled blue cheese – 2024 $5.99 2020 $2.99-$3.99

organic carrot chips – 2024 $2.99 2020 $2.49

Costco:

organic chicken from costco 2024 $5.99/lb 2021 $4.99/lb

kirkland pinot griggio 2024 – $4.99 2022 $4.99

I can detail the rest of my meals for the week if you’d like….

Oh and I dared to think about buying a snickers bar while camping last weekend – $1.89 when l swear the last time I bought one it was $0.79, decided to skip it.

“…bout buying a snickers bar”

Crap manufacturers of this type have been ripping off Americans for many years with their sugary unhealthy crap. No one should ever buy this stuff. It’s not fit for human consumption, it costs almost nothing to produce, and it’s expensive. If you want some snacks, buy some roasted unsalted nuts.

See, you never thought that you’d get free nutritional advice here.

Most service people need to buy, a lot of durable goods that are seeing deflation and are not regular purchases. That’s the difference, the cost of pretty much everything in my daily life besides gasoline has increased significantly.

I’m also curious when they track food inflation if they just look at categories like bread in general or a specific items like specific brand of bread. I typically buy the same items over time, and the majority of them are up 50%+ since 2020. Sure I could sacrifice quality to have prices only be up maybe 20%.

My biggest point to maintain the same lifestyle I had in 2020, I have to pay significantly more. Yes, one could make sacrifices to keep their cost of living the same, but then they’re still essentially poorer because they’re getting less for their money.

Mm1: The chart reflects the massive food price increase through the pandemic, not quite an “official” 50%, but close.

It appears that food prices are trending slightly up, along the same slope as pre-pandemic, at the 100 point higher plateau.

Fortunately energy is down, a major input for agriculture. I personally don’t expect that index to decrease substantially (and if it does it may portend something worse).

They’re happy to use hedonic adjustments when quality goes up but how about when it goes down?

Are laptops and used cars good to eat?

Generally not, I’d venture to say, too much plastic. But the price of fresh fish and seafood dropped mom and yoy. Fresh fruit and vegetables also dropped mom and yoy. We buy lots of fresh fish, fruit, and vegetables, and the CPI for them seems about right, lower than a year ago. We just had black cod (butterfish) Saturday night when we had friends over for dinner, which we love to serve since it’s delicious and easy to prepare, bought fresh hours before, cheaper than a year ago. So eat something healthier than laptops.

Also, to keep your tastebuds active, enjoy some good coffee, roasted coffee dropped mom and yoy.

Hey wolf

Bag of strbucks whole bean 18oz was $18 today at target.

$13 at a kroger owned affiliate

I like the way the bagged Starbucks tastes.

Tried Peet’s and it was kinda rough.

Yeah, pay through your nose for it if you think it’s fun. On Saturday, at Costco, I bought 3 bags of my favorite French roast Colombian Supremo 3-pound bags for $14.99 each, or $5.00 a pound.

Gasoline in N. Cal may be down a little from the all time highs, but it has not “plunged” (I paid $5.49 for regular on El Camino in San Carlos today). Last weekend gas was over $6.00/gallon in Tahoe City and $9.95/gallon at the Tahoe City gas dock. Other than computers and flat screen TVs I can’t think of anyting I buy that has dropped in price. I was at Sherwin Williams today and they are charging over $100/gallon for lots of paint, but it is even worse since “srinkflation” had reduced the size of the “gallon” of paint to 123oz (96% of a gallon) so that $133 “pail” of paint is a $138 “gallon of paint”…

@Wolf, that is a great deal on the coffee, I thought I was getting a great deal at Safeway when I got a 12oz bag of Starbucks House blend for $7.99 club card special down from $14.49 “regular” price this month…

The price of fresh fish and seafood dropped mom and yoy. Fresh fruit and vegetables also dropped mom and yoy. We buy lots of fresh fish, fruit, and vegetables, and the CPI for them seems about right, lower than a year ago. We just had black cod (butterfish) Saturday night when we had friends over for dinner, which we love to serve since it’s delicious and easy to prepare, bought fresh hours before, cheaper than a year ago.

Fresh fruit and vegetables have dropped in price. Also, fish is still reasonably priced. What has gone up in price is imported items such as olive oil, jam, etc.

Where is a recent picture of Wolf’s “Gas Station from Hell”?

Wall St analysts keep saying “sHeLtEr InFlAtIoN iS lAgGeD dAtA iT’lL cOmE dOwN any DaY nOw”

It’s now been 4.5 years of ballooning home prices & rents!

Durable goods might be falling b/c I can’t afford to buy any after paying my insurance and eating out.

Yep NVDA drives the Nasdaq spx and the markets with nvda up over 5 percent today with a market cap in the top 5 . Can’t keep track of who is #1

Most of the things that are trending down are the gifts to the first world citizens by those living in shackles and day to pay check living. Great irony!!

The US produces all of its own gasoline and natural gas. And it exports a bunch of gasoline too, and exports a huge amount of natural gas, largest LNG exporter in the world. Lots of motor vehicles are manufactured in the US, by all global brands, so a lot of used cars you see were manufactured in the US. Most of the food consumed in the US is produced in the US. But yes, lots of other consumer goods were made overseas. Global trade is complex. Simple one-liners, however cute, don’t do it justice.

By contrast, nearly all services that consumers buy are produced in the US. And 65% of spending goes to services.

Is the bigger service economy due to the dollar becoming forever stronger by way of the Nixon deal with Saudi Arabia to buy the federal debt, as that hurt US industry exports and supported imports?

Huh?

I think esop is proposing that the petro dollar was a major factor in the shift from the US being a producer economy to a consumer economy. Therefore the national US economy has become a service based economy.

I am not sure if the petro dollar itself was the key?

At the same time the US became a debt based (juiced?) economy, began selling debt and therefore borrowing from the world and future generations to escalate the US lifestyle/ standard of living.

Basically the beginning of the “grand experiment” we call MMT?

If the petrodollar ever existed, it died long ago. The US is a net exporter of crude oil and petroleum products. The biggest oil-trade partners of the US are by far Mexico and Canada.

Offshoring manufacturing (trade deficit in goods) had nothing to do with the petrodollar or whatever. That’s just nonsense. It was about shifting manufacturing to countries with cheap labor.

DR_ECE_Prof_FinanceGuy, I don’t expect you’re going to find there’s a lot of sympathy in the metropole for those exploited on the periphery. ‘Twas ever thus …

I honestly did not think the FED could get interest rates this low this fast.

Rate cut or no rate cut, this is a pretty good inflation print considering where we were just a 1 1/2 years ago.

Where would be w/o the government running a ~6% deficit. Can I have a D Bob?

Maybe the bond market is actually paying attention.

SPY $600 EoY minimum. The roaring 20s have only just begun. No recession kiddos time to get a job!

A balanced report for everyone unless you’re an inflation hawk whose only mission in life is to rid the world of inflation, return to the gold standard, and put those uppity workers who actually expect to share in the wealth that they help create back in their place.

Ah yes because we all know inflation is great for the American working class. Scre those inflation hawks. /Sarcasm

Inflation is always and everywhere a distributional issue — that’s why it’s so politically salient.

You insinuate that wanting minimal inflation is somehow sinister without explaining why.

The Social Security cost-of-living adjustment for 2025 could shrink to 2.5% as inflation cools, according to analyst estimates

Meanwhile:

Earlier this year, the Medicare Board of Trustees estimated that the Part B premium, which is automatically deducted from monthly Social Security checks, would climb by $10.30, or 5.9%, to $185 per month in 2025

This is good, right?

The average SS benefit is now $1,782, and if those benefits rise by 2.5%, recipients receive an extra $44.55 a month. So they pay an extra $10.30 for Part B, and they can spend the extra $34.25 on other stuff. They should see the $ premium increases for people who now pay $1,000 for private health insurance a month, and the premium goes up 5.9% — the lucky ones! – they’re paying an extra $59 a month, not an extra $10.30. Medicare is a DEAL compared to the real world, so quit bitching.

Price increases are never good for consumers. Americans loathe price increases, and rightfully so. But it’s important to keep perspective.

I am glad that you pointed this out. Medicare is an incredible bargain but why do we have socialized medicine for only the over 65 crowd?

Try living on $1,782 dollars a month Richtor. Let us know how the fresh fruit and veggies diet works out.

As my CPA laid to out to me, “If SS had been been an individual drip reinvestment account in bonds you would have retired at 62 with $2,500,000 in your Treasury account.” Heck, even a dingbat investor like me cold have made $2.5m work well enough to retire on.

In reality I took retirement at 70, continue to work and provide for family around me. I could abandon family, move to Arkansas and retire but somehow find that unappealing. I see people that ‘retired” at 62 and grabbed that SS ring now working at HD. Lowes etc in their mid 70’s and even older! Oh, and my SS is completely taxed away and then some.

Your CPA is an idiot. Look up the meaning of the word risk, and then calculate the net present value of your SS benefit payments from the moment you took them until you’re 100, including the COLAs along the way.

And that NPV is “risk free.” In 2000-2002, the Nasdaq crashed by 78%. That’s “risk.” Risk means your retirement money may be gone. You bet the farm and lost it.

Your CPA should have known about risk. And he should have shown you the NPV including future COLAs of your SS benefits till you’re 100. The fact that your CPA didn’t, tells me that he is an idiot, and you should fire him.

In addition, SS is not designed to provide a life of grand splendor for 30 years. It’s designed to keep you out of abject poverty after you stop working.

It’s highly advised by everyone to have additional means and/or income in retirement.

If you don’t like your SS benefits, donate them to charity.

This is a lie: “my SS is completely taxed away and then some.”

Adios.

No stock bashing today!

What a rollercoaster 🎢 !!

i find the stock market as interesting as watching people play roulette.

that is, not at all.

That wheel does make some cool sounds tho.

Did you hear a guy cracked the algorithm to roulette using some equation?

They banned him 😆

Barron’s: Nvidia Stock Soars 8%. How Chips Helped the S&P 500 Stage Its Comeback.

The Dow index went from over 700 down early this morning to close at 124 up and all on no change whatsoever in any of the news!

Nvidia CEO came out with a market-moving comment about huge demand for Nvidia’s chips.

Even if true as to demand for its products why would that remotely affect any other stock than Nvidia?

Because people are nuts

Damn fine advertising copy——>>READ Wolf Richter…because, “People are nutz!!”. Or maybe even refrigerator magnet of the year in that [black box].

He literally says that every other day. If you really think that is the cause I have a Tesla Roadster to sell you.

Proof that news is irrelevant to market moves

Nvidia said they had a ton of demand during there earnings call and stock plunged for two weeks.

Doesn’t

Matter

If I am correct, FED looks at core CPI which is per WR: Core CPI: +0.28% (+3.4% annualized), 2nd acceleration in a row.

So current inflation is 70% above FED’s target rate of 2%.

Home prices flirting with all time high.

Stocks again close to ATH.

Extremely loose financial conditions.

and FED is about to cut rates.

People: This is not rocket science. Wake up and smell the coffee!!

Job creation went from decent to weak in August three month average. That was a big move from July to August, accomplished by revisions mostly, and the Fed doesn’t want it to get worse.

https://wolfstreet.com/2024/09/06/the-fed-has-room-to-cut-rates-are-high-relative-to-inflation-and-job-growth-could-use-some-juicing-up-to-maintain-momentum/

bobber said something brilliant the other day. the fed is being intentionally unclear as to its future goals and methods to protect stocks and bonds simultaneously.

if it comes out and says it will never do qe ever again, and never drop rates to 0, stocks would plummet.

but if it came out and said that it would do whatever it takes to protect stocks, even at the cost of the dollar, the bond market would crash as bond vigilantes would come back from hiding and refuse to buy 10 year treasuries at crap yields.

by being non-committal, they can let both narratives, which are fundamentally inconsistent with each other, thrive at the same time.

it’s kind of genius when you think about it.

Franz and bobber, the fed is crystal clear. In 2021 they said they were gokng ro raise rates and continued to say so and do so. They told us when they were going to stop and reevaluate and theyve now told us they are going to start loosening. If people would pay attention they could make a lot of money listening to the fed.

I started liquidating properties in 2022 and 2023 when rates shot up. I believe residential real estate will drop further from its highs, lower rates or not. I have friends who got out of commercial a year or so before the crash and I thought they were nuts. They were right on the money.

In real estate, if youre not early, youre late.

The uncertainty is the plan for use of QE, not interest rates. The use of QE to avoid recessions establishes a put that drives stock prices, asset prices, plus it’s pure money printing in the context of deficit spending.

It is QE that changed the game. The Fed has always piddled with interest rates, which is not a huge monetary violation, relative to QE.

Bobber if this bubble was like the earlier one. There were only 4 years to buy at a distressed price.

This bubble is longer but I feel like things recover more quickly. So I say 2-3 years max on distressed prices IF that even happens.

If you look at the line graph it’s more of an upward trend with these large surges in price over time, but eventually the line keeps moving up and out.

Basically to hold your breath is a waste of breath when in 4,5,6,7 years we will be in another bubble again.

The Federal Reserve has been perfectly consistent for a couple of years on its Quantitative Tightening (QT) policies. What is in any way even slightly unclear as to that?

QE can be a Ponzi if the printing can’t be stopped. Ponzi is a scheme where never ending new money is required to roll over existing debt and incur new debt. In a conventional Ponzi, the new investors cease, along with the new money, whereas, the monetary Ponzi has a printer for the new money, so it never need shut off.

Bobber-

Yours are thoughtful comments.

Not to quibble but when you say “interest rates,” (as opposed to QE/QT), you’re referring to Fed funds rate, meaning short rates, right? QE is also “interest rates,” except that it is meant to effect LONGER rates.

Both are interest rate fixing devices. The distinction is in the duration of the manipulation. Long-rate manipulation is even more dangerous than short rate manipulation, IMHO.

The Fed’s playbook — and Treasury Department’s Operation Twist 2.0, too — continues to be manipulation of interest rates regardless of whether FFR or longer Treasury rates.

Price fixing seems to always lead to greater future problems.

That uncertainty is a travesty in a capitalist economy. People have a right to know whether the government is going to print money to erode savings and accomplish wealth transfers.

Insightful commentary. Damn’d good

Franz G’s and Bobber’s comments were complete nonsense.

But people love bullshit. The bigger the bullshit, the more they love it.

The Fed told you everything in advance: from rate hikes to QT, months in advance.

The only uncertainty is life — all kinds of stuff happens, and things change, and that happens to the economy as well.

I strongly suspect the word bullshit will be the very last word to rattle out of your lungs at the end of the ride…

Meanwhile — what’s BS about it? Is the notorious Fed Put, née the Greenspan Put and sometimes the Powell Put not real? Is there not a tacit understanding that QE will be rolled out if things go enough sideways/south? Is it really a gross stretch to think this ace in the hole isn’t helping to keep things nuts?

You people are trafficking in homemade conspiracy theories on my site. That’s what X is for.

That’s the problem. They have plans for the good times. When they hit bumps, the plans go out the window.

If they can’t communicate their plans for challenging times, like during a recession, they really aren’t communicating much.

I’m not sure that makes sense.

The Federal Reserve FOMC couldn’t possibly be more clear.

So then the insane asset inflation over the 2017-2022 was all according to plan?

It was all due to crazed manic speculation without regard to normal valuation metrics such as PE ratios.

This is the essence of strategic ambiguity, and since the direction of rates is just about the only tool in the Fed’s toolkit, there’s a kind of selfish wisdom in its gnomic approach.

Of course, it’s also why monetary policy is the wrong tool for managing a macroeconomy — fiscal policy is infinitely more flexible and powerful for this purpose.

The FED is really not concerned about stocks as they know there are bubbles. They are more concerned about inflation and employment and how the banks are faring and the economy in general.

There has been a lot of money printed the past 5 or 6 years and it has to go somewhere. All assets are probably overvalued as there is more money than supply for stocks, housing, Bitcoin, etc. In the 1990s there were over 7000 public stocks to invest in and now there is only 3500ish. But the population has grown by almost 100 million and many have 401ks and the only place to invest is in stocks.

IMHO…20 PE is the new normal even though it indicates stocks are historically expensive.

There are currently around 7,000 publicly traded stocks in the US, not 3,500 as you incorrectly stated, and nothing has changed at all about the range of 6 to 15 being reasonable PE multiples for stocks. There isn’t even slightly enough money in the US to cashier out assets for anywhere near their aggregate $100+ trillion value as the money supply in the US by the broadest measure is only around $22 trillion.

It is not possible for bond vigilantes (as a measurable whole) to refuse to purchase treasuries as there is nowhere else to go. The sheer volume of new wealth created during the covid measures globally needs somewhere to go and there are only so much hard assets around. Nevermind the illiquid nature of most of these, which means that even if you want to put your wealth there, it can take many months or years to do so in a financially prudent manner.

So Fed is f$uc$ed and we are f$;ked.

nope, FED will be fine, every one of FED members will be just fine, no one will be hanging out to dry….look at Greenspan, Yellen…etc they all walked away just fine.

But yeah the non top 1% or 0.00001% are fXXked relative to how low you are on the class pyramid, closer to the bottom, then you’re more F

Scripture: Wealth and sons are allurements of the life of this world: But the things that endure, good deeds, are best in the sight of thy Lord, as rewards, and best as (the foundation for) hopes.

I’m seeing macro Alf calling the fed behind the curve and saying they will cut 50 bps in Sept.

I don’t have any idea what the fed WILL or SHOULD do. It seems the first cut is imminent. The global slowdown is real, the US is still hot between government spending, still near record high asset prices and overall decent sentiment.

I question how long the music will keep playing, with China an alleged falling rock, Europe a hot mess and seemingly the rest of the globe following those paths?

The recession has been on the horizon for months and now years. I hear both a chorus of bulls (Fed easing, record profits and demand) and bears (deflationary depression, geopolitical instability), meanwhile in my neighborhood everything seems pretty… average?

It feels like the CPI report looks: One hand heavy, the other hand light.

Which one is steering? (Does it depend if you sell goods, China, or services US/ Euro zone?)

Perhaps humanity will grow up and realize we are all in this together! Nope, not happening. Protectionism and nationalism the only direction to travel.

China has been struggling for awhile first the real estate melt down and now their slowing economy – but somehow we haven’t really felt it here other than in our durable goods deflation. I’m sure it’s a complex topic but does a chineese slowdown actually impact the US since the American consumer is a net buyer of Chinese products? I’m actually curious because I thought we’d feel more of it here but it doesn’t seem to have made an impact

MM1:

Exactly. Alf was talking about how “China is exporting deflation,” but the rest of the world is happy with lower goods prices.

Wage demand is ongoing in developed economies. The question is why China is ok with their economic softness and what the next “gotcha” move may be?

A 2015- style currency manipulation seems unlikely. Along the same lines, base metals prices are reflecting a general slowdown/ or confusion (4 months ago Copper at ATH, but now wanting to hold above the $4 handle).

I have been waiting for the “stag” wall to hit with the ’flation but the “pockets of weakness” is staying pocketed and not yet ready to spill over.

Seems like in a period of an idea I only barely understand called fiscal dominance where monetary policy can have only so much influence. Seems like tax revenue increases are needed and since either tax increases or spending deductions aren’t feasible then asset inflation is needed to keep coffers filling up. Inflation only helps to keep the debt manageable as well.

“…since either tax increases…”

Tax revenues are increasing (red line):

Tax receipts tested the 2022 highs and failed. I see them dropping.

Nah. What you’re seeing in the chart is the impact of capital gains taxes after huge rallies in the stock market. The big jump in Q1 and Q2 2022 were the capital gains taxes on capital gains in 2021. Then in 2023, capital gains tax receipts dropped sharply because 2022 was a shitty year. 2023 was a good year in the sense that the drop in 2022 was overcome, but because stocks in 2023 didn’t move above their 2021 highs, capital gains taxes weren’t that huge, and the capital gains tax receipts in Q1 and Q2 were therefore less than records.

Car insurance premiums are criminal. Corporate America greed is very much to blame, as almost everything we buy now is smaller and more expensive. I just noticed that toothpaste is being downsized, now 6 ounces instead of 8. UNREAL.

There is probably some leverage in pricing their premiums but I think it has a lot to do with the cost of repairs. I am in the car business and it’s been harder and harder to get good deals on reconditioning. Cost of labor and parts has gone up substantially. That inflation has fed into insurance rates. Just sucks because my insurance doubled on older cars and I have a perfect driving record.

All the uncertainty has adjusted my investments from long equity to selling weekly covered call options. Most say that’s an aggressive style, but I see it as defensive an leading to a small risk period with the cushion of premiums to limit downside risk.

When rates do fall there should be a flow to more dividend paying stocks that are somewhat defensive such as utilities etc. How long until that starts to impact value and growth stocks?

For a taste of your whiskey, I will give some advice.

Every gambler knows

That the secret to surviving

Is knowing what to throw away

Knowing what to keep

‘Cause every hand’s a winner

And every hand’s a loser

And the best that you can hope for

Is to die in your sleep.

Wolf,

In the past I recall you had done graphs of OER vs CS index… but in this article you did CPI rent instead of OER. Why the change?

Also, will you be using the Zillow index for this metric in the future, since you’re now using it for your most splendid housing bubble series?

I changed that a long time ago, over a year ago? Because people are always arguing about OER. It completely sidetracked the message of the chart. Both indices track very closely, so I just switched, which shut down the endless stupid stuff about OER.

Wolf – Just a question, hopefully it isn’t one that has been asked multiple times in the past. What is the difference between Owner’s equivalent of rent and Rent of primary residence and why are they listed separately?

It’s explained in the article. So RTGDFA

I did but still don’t understand. They both are the cost of your place of living. Owner’s equivalent is just that, the supposed conversion of home ownership costs to rent while rent is the direct cost of rent. I guess home ownership has a bigger impact on the economy as that segment accounts for ~3.5 times as much as direct rent, 26.8/7.6. The latest figures show there are ~2 times as many homeowners as renters. They may need to adjust their weighting.

The way I see it, the Fed should be cutting rates based upon this, but increasing the levels it works down it’s balance sheet. Lower rates should incentives the building of more homes and apartments bringing down the inflation there. Insurance should start to slow down by year’s end as insurance companies realize they can’t keep raising rates at this pace forever. The one that I can’t predict is the price of car parts. There seems to be no motivation to increase production there.

The Federal Reserve policy interest rates have nothing whatsoever to do with mortgage interest rates which are based on the yield of 10 year US Treasuries plus around 3%. Insurance companies are required by all 50 state insurance departments to maintain solvency at all times and will continue to raise premiums to ensure that or just shut down offering any coverage at all if they can’t main profitability.

SoCalBeachDude – Your response sounded like one of my favorite brews, Arrogant Bastard. You can educate without belittling.

He didn’t even mention mortgage rates. The cost of borrowing will go down so builders can extend their lines of credit and will be able to build more homes. I don’t quite follow his cause and effect, but as the price of homes levels off, insurance will follow.

Insurance premiums will not fall a single penny as long as the underlying costs paid out by insurance continue to rise rather dramatically including the costs of cars, settlements, and repair and parts for these vehicles. Mortgage rates are particular to housing and the fact of the matter is that they are based nearly entirely on the yield of 10 year US Treasuries plus around 3% and not based on any other notions as you suggest at all. The core problem with housing is that prices are totally out of whack with reality and the only thing that will change that and make housing more affordable is for prices to fall substantially by about 50% or more from where they are now.

SoCal – you are the only one talking about mortgage rates. They must be on your mind.

No ‘builder’ can ever borrow at the Federal Funds Rate as they are not banks so that rate is irrelevant to ‘builders’ who would only borrow by taking out commercial construction rates which will continue to carry a high amount of risk of loss and are thus not likely to be lowered at all. As to mortgage rates, I do not have a mortgage on the house I own, but about two-thirds of all homeowers do have on and this is a huge issue for most in the housing markets.

Yields on the 10 year do tend to be affected by the Fed funds rate. I don’t think a quarter percent change would, but .75 might.

Insurance doesn’t just include home insurance. Home owners’ insurance will continue to rise as people like to build in areas prone to storms, fires, etc. Home prices are leveling off though, so total loss claims will factor into a decreasing rate.

Auto insurance though doesn’t need to increase except for profits. Car prices new and used have come down.

Health insurance rates can only adjust based on the cost of health care. Health care inflation is not very high. Remember health insurance has a profit cap and anything over that has to be returned to the insured.

The discussions about Starbucks and Costco coffee reminded me of this link:

https://hip2save.com/tips/name-brands-behind-costco-kirkland-signature/

Looks like round one goes to Wolf …..

The 10 year is only at 3.69% I don’t see much need to get real aggressive with the cuts. Noone is gaming out a high inflation scenario yet, just a 2-2.5% core PCE instead of 1-2%.

I live in full boycott mode. Don’t count on me to waste dollars at restaurants, bars, shopping centers, etc. I refuse to pay ridiculous prices for a slight convenience. I won’t even order take-out anymore. I’d rather cook my own meals – the way I like – much healthier, and enjoy home entertainment. It’s far safer than being a sitting duck in public places. No malls or movie theaters for me. Those days are gone.

And that means less gasoline wasted. I refuse to support or participate in a rigged financial system. I won’t play.