Measuring a level at month-end versus a flow over the past 12 months: Descend with us into delinquency geekdom.

By Wolf Richter for WOLF STREET.

There are different ways to look at the issue of delinquency with the hope of figuring out what’s going on. Let’s use the example of a reservoir. Among the things we can measure are, for example, these two: The amount of water that flowed into the reservoir over the past 12 months, and the level of the water in the reservoir at a point in time.

That important distinction between a “flow” and a “level” is what we now need in order to understand the different measures of credit card delinquencies.

“Delinquency transition rates”: a 12-month flow.

The New York Fed has a unique angle: It tracks the balances that flowed (“transitioned”) into delinquency over the past 12 months. It calls this metric “transition into delinquency” and “delinquency transition rates.”

The New York Fed does not produce “delinquency rates” (the measure of a level) that everyone else produces.

But the Federal Reserve Board of Governors, Equifax, Fitch Ratings, and others produce “delinquency rates” (levels of delinquent balances at month-end).

The New York Fed defines “delinquency transition rate” as the percentage of balances that transitioned into delinquency over the past 12 months. This is a flow into delinquency over a 12-month period, and doesn’t take into account the amounts that flowed out of delinquency (for example, when borrowers caught up with their payments), and it doesn’t measure the level of delinquent amounts at the end of the quarter. But it’s an important indicator that the Fed likes to look at and that Powell has cited during the press conference.

The NY Fed’s Consumer Debt and Credit Report for Q2 said this:

“Over the last year, approximately 9.1% of credit card balances … transitioned into delinquency.”

This line in italics was then widely misreported in the financial media and blogosphere as a delinquency rate of 9.1% (as if it were a level at quarter-end), when it was in fact an annual flow into delinquency.

Meanwhile, the actual “delinquency rate” was 2.81% for bank cards and 4.44% for private-label cards as per Equifax; and 0.99% for prime-rated credit cards as per Fitch. The Fed’s credit card delinquency rate at commercial banks will come in at around 2.96% for Q2.

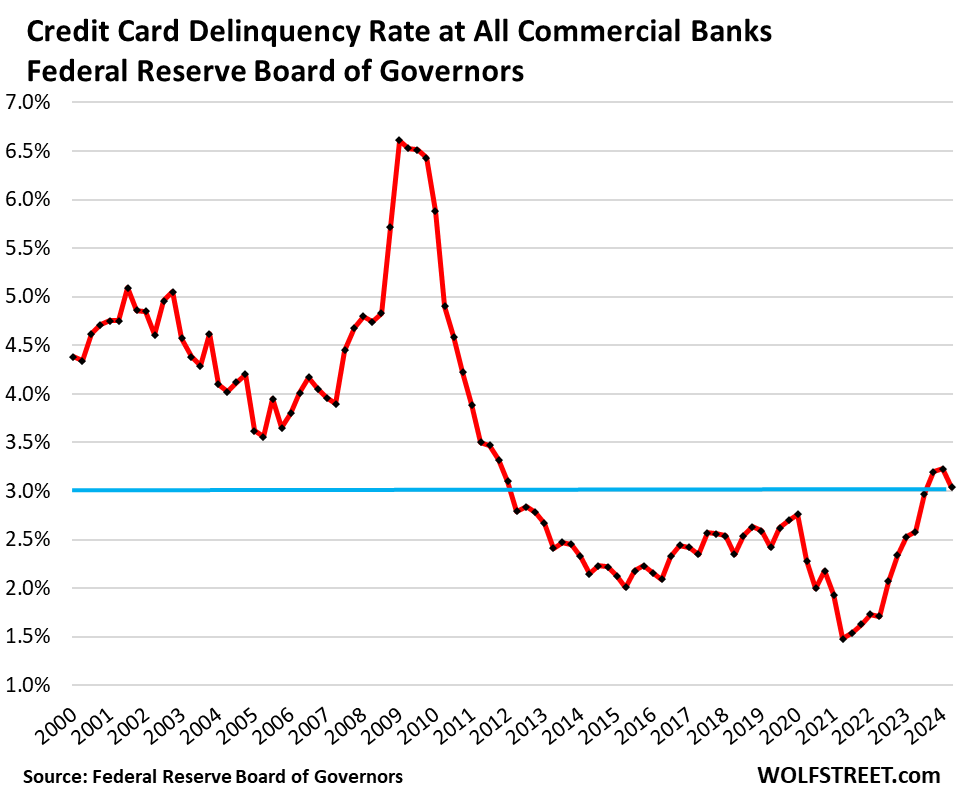

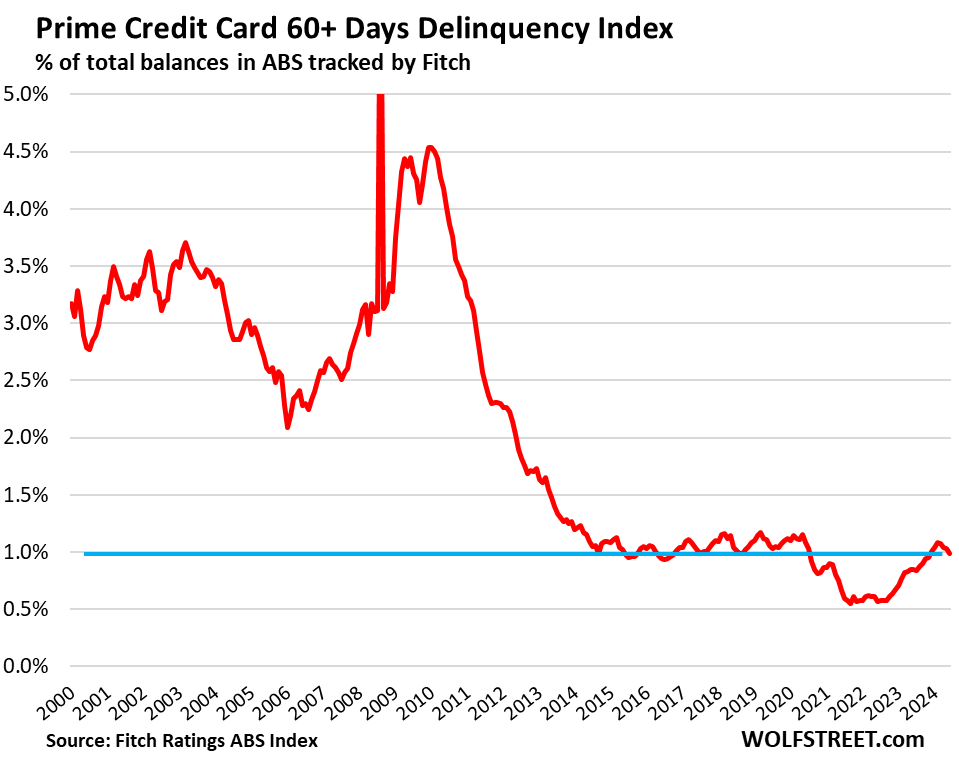

“Delinquency rates” drop for 4th month in a row.

Equifax, the Federal Reserve Board of Governors, and Fitch Ratings report “delinquency rates” the way we normally understand them as a level at a certain point in time (month end or quarter end).

Delinquency rates on credit card balances (the levels) plunged during the free-money era when people used the cash to catch up with their past-dues and hit a historic low in Q2 2021. Then they began to rise again. They overshot some in 2023 and early Q1 2024, but started dropping again in March, and have declined every month since then. They remain somewhat higher than during the Good Times before the pandemic, but are lower than prior years.

Equifax reported that the 60-day (“severe”) delinquency rates in June declined for the fourth month in a row:

- Bank cards: 2.83% (from the high in February of 3.21%).

- Private label credit cards: 4.44% (from the high in February of 5.01%).

Federal Reserve Board of Governors reported that credit card delinquency rates of 30+ days at all commercial banks in Q2 (not seasonally adjusted) dipped to 3.04%, from 3.23% in Q1:

Fitch Ratings reported that its 60-day delinquency rate for prime credit cards (excludes subprime) also declined for the fourth month in a row to 0.99% from the high in February of 1.08%

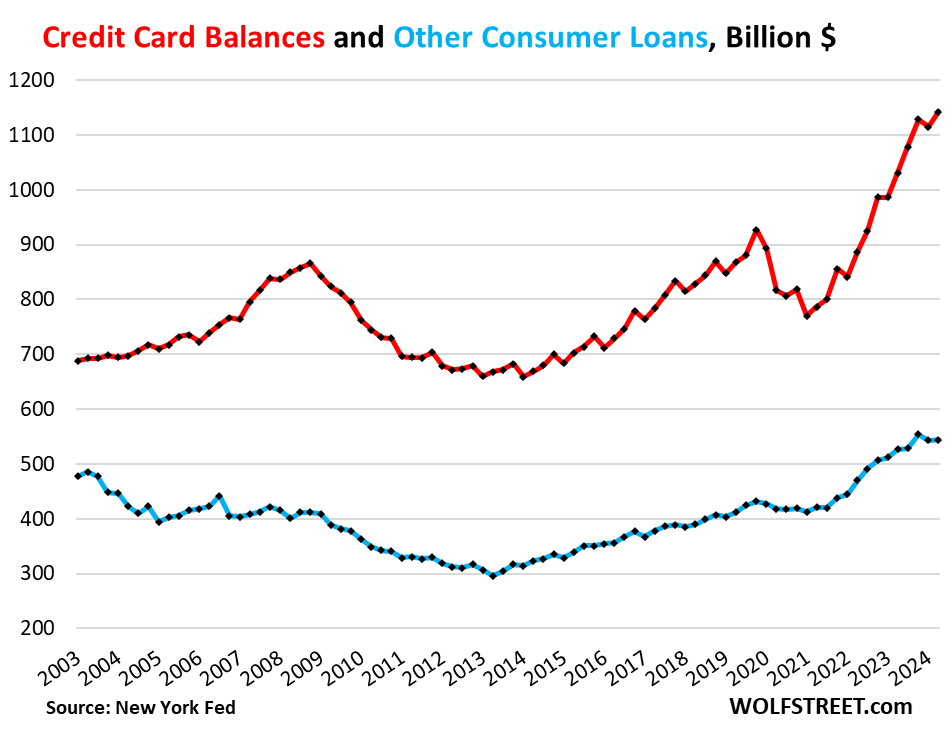

Credit Card Balances.

Credit card balances are a measure of consumer spending – including for expensive business trips that are reimbursed. They’re not a measure of borrowing because most balances are paid off by due date and never accrue interest, but allow cardholders to get their 1% or 2% cashback, airmiles, and other loyalty benefits. Credit cards are the dominant payment method used by consumers in the US, ahead of debit cards, and far ahead of other payment methods, such as checks or cash.

Credit card statement balances rose by $27 billion, or 2.4%, in Q2 from Q1, to $1.14 trillion, more than making up for the seasonal drop in Q1, according to the New York Fed’s Household Debt and Credit report.

Year-over-year, credit card balances rose by $110 billion, or by 10.8%, in line with healthy growth in consumer spending including on travels and unhealthy growth in prices (red line in the chart below).

“Other” consumer loans, such as personal loans, payday loans, and Buy-Now-Pay-Later (BNPL) loans remained essentially unchanged in Q2 from Q1, at $544 billion, after dropping in the prior quarter. Year-over-year, the rose 3.2% (blue line).

BNPL loans are short-term and interest-free loans that are subsidized by the merchant. They’re a modernized version of installment buying, a concept that has been around forever.

What’s surprising is how little balances have risen in two decades.

“Other” consumer loans are barely up by only 14% from where they had been 20 years ago despite 73% CPI inflation and 16% population growth.

Credit card balances, which reflect spending and not borrowing, are up only 63% from 20 years ago, despite 73% CPI inflation and 16% population growth.

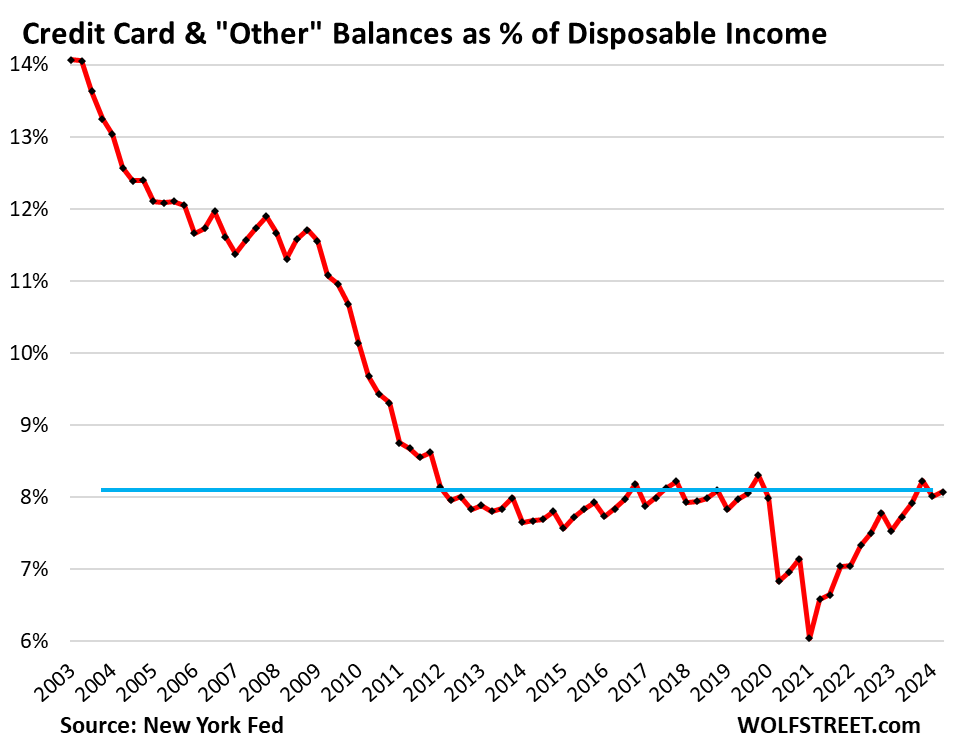

The relative burden of credit card and “other” balances.

As a result, the combined amounts have risen more slowly than household income. Credit card balances and “other” consumer debt combined, at $1.69 trillion, amounted to 8.1% of disposable income in Q2, roughly in the same range as in the past two quarters and in the years before the pandemic.

Disposable income is total income from all sources minus payroll taxes and social insurance payments. It includes wages, interest, dividends, rental income, farm income, small business income, transfer payments, etc., but not capital gains. It’s what households have left over to pay for their monthly expenditures and servicing their debts.

Banks are still eager to open new accounts.

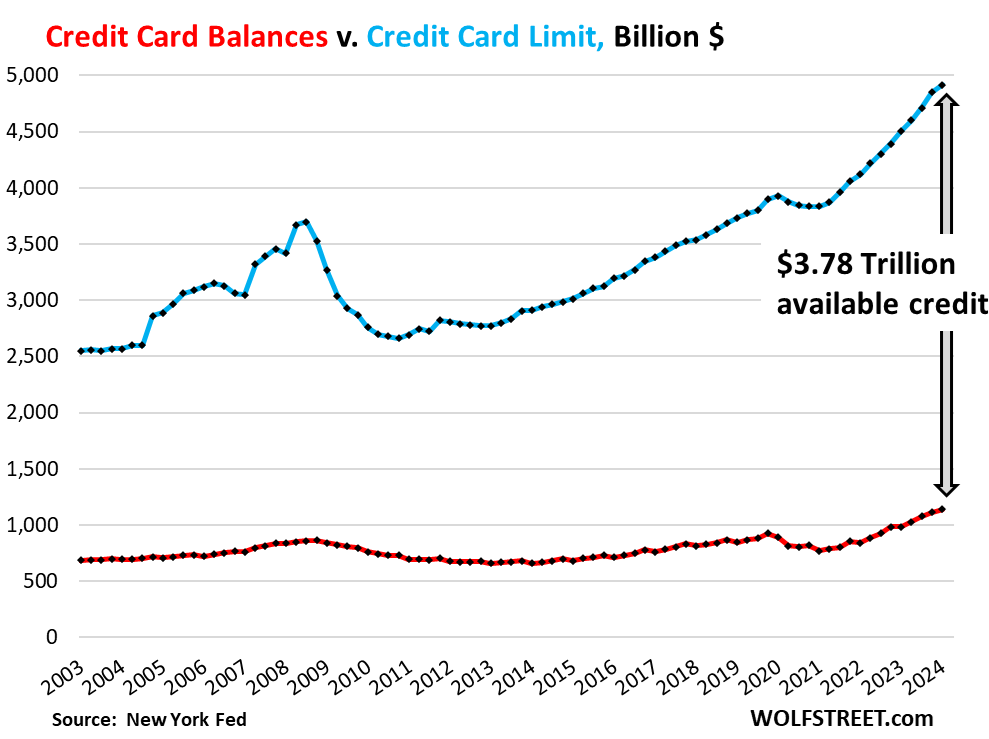

The aggregate credit limit rose by $379 billion year-over-year, to $4.92 trillion, a result of more card accounts (banks are trying as aggressively as ever to get people to set up new accounts) and higher credit limits. Over the same period, credit card statement balances rose by $111 billion, to $1.14 trillion.

So the aggregate available unused credit surged by $235 billion year-over-year, to a record $3.78 trillion.

By contrast, during a credit crunch, aggregate credit limits (blue line) decline – and this economy is far from it:

In case you missed the rest of our consumer credit series over the past two days:

Auto Loans, the Burden of Auto Loans, Subprime Lending, and Delinquencies in Q2

Here Come the HELOCs: Mortgages, the Burden of Mortgage Debt, Delinquencies, and Foreclosures in Q2

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

My apologies for the off-topic post, but how about the good professor from Wharton backtracking on his call for a 75 basis point emergency rate cut after the July jobs report? From massive emergency rate cut needed to no emergency rate cut needed in a few days. That’s just good, stable analysis by Mr. Siegel. No credibility. No shame. Hopefully, one day, no audiance for his views.

WS will always need a shill like Siegel to pump up their narratives of easy money, low interest rates and QE. Just like RE industry will always need a shill economist like Lawrence Yun

Lawrence Yun is explicit in his motive.

And Siegel isn’t or are you saying his view is purely based on incompetence as an economist?

He has some role in some ETFs, I forget the name. So he is out there touting rate cuts to prop them up. Unfortunate when academicians start touting stuff and their biases are not clearly visible to the viewers and investors.

The history of the person might give glimpse of direction.

The unknown unknowns are always about….

The credit card story is pleasant, looks like a good night to star gaze and ponder.

“Why make business simple when you can make it complicated?”

-quote by a Rockefeller friend made to Bucky Fuller….I believe Bucky.

Think it is obvious why…..to confuse and thereby protect source of income while staying free of any accountability for how you actually got it.

Creating confusion……..ALL organizations do it……I have even had bosses of 12 person shops try to do it to me. (sob stories about how every single thing they owned was collateral…….

I tried to start a posting of wages on the company bulletin board……you can guess how far that went, even among workers……A pipe smoking, swearing lesbian bookkeeper spilled the beans….she was immediately fired. Many quit or made other plans at that time, including me.

Thanks for some good unravelling, Wolf, even if I can’t put together a real good picture in “me-think”…..or maybe too lazy to. I HAVE learned a LOT here over the years from my ONLY social media effort EVER.

But I’m hell on all the BS in so-called “Biochemistry” and to varying degrees the other “sciences”…..and have a lot of other good education and experience with this society of ours.

Still searching for my place in the world and how best to think about it…..that effort will never end till I do.

Probably everyone I share this time with is doing the same thing.

NBay – Tom Paxton also eloquently-voiced the same in 1963 (“I Can’t Help But Wonder (Where I’m Bound)” )…

Two steps for’ard and one back, some days. The converse on others. Best.

may we all find a better day.

Hey, DO, I missed this! One of your best concise yet inclusive replies. ALL should look up the comment that brought it on.

Later.

MCM – SOMEBODY’s been hiring ’em all along (…and it ain’t other illegals…). Severely/reliably-enforced card-check would dim the ‘welcome’ sign (and possibly bring that long-awaited recession from a resultant increase in labor compensation…).

may we all find a better day.

Oh, CC Delequency rates Aug 9 was where I copied it, and it IS relevant to ECON.

Exactly. He should be taken to the cleaners during one of his classes. Strip him in the classes with pointed questions.

I was also wondering how can a “rate-cut” affiniando, who only wants to send stock market journey that has nothing to do with fundamentals really teach finance. How do such morons get selected? In fact the Dean can also pull him up and ask him to explain as he damages the reputation of the college itself. Shame on the institutions that employ such guys too.

As an aside he can take a few classes at Wolf Street Media so that he will get into his thick skull (hopefully) that ‘Nothing goes to heck in a straight line’ and keep his mouth shut.

I don’t know what happened to Siegel, his book Stocks for the Long Run was written in the 90s, went through 4 editions (impressive by business books standards) and is very much buy and hold.

My guess is he is a big Dem, and got hooked on low rates through the long canyon of Obama era zirp cuts, that this was the new normal. Guessing though.

The other guy the pull out for go go fiscal policy is the tic-ridden Alan Blinder, also always wrong. They are recognizable and have affiliations with the ‘best’ schools.

Another wall street shill running around calling for emergency rate cut is Danielle Demartino Booth… listening to her it seems like prices for everything are back down to 2015, and evil fed should go back down to 0. So the clowns on Wall Street can go back to gambling with free money while everyone scrapes by.

Can’t wait to see how many gloom and doom Youtuber or DiMartino Booth will spin this one to “warn” us about Depression is right at the doorstep and we need to cut rates now because all the drunken sailors are still struggling

Every time I see a video with her name in the title I skip it. She’s totally delegitimized herself over the years with her sky is falling act.

The sky is not falling, but it is kinda “behaving differently”, and not economically.

The insurance game is changing because of said sky changes and that should probably be factored in, for example.

Would also help if people realized their lifestyle could use some adjusting……without being told or forced to……..

NBay – …reckon the sky IS ‘falling’ if observed in terms of rising sea levels (surface height and thermally…my apologies, Wolf!), insurance co.’s and our Navy certainly seem to think so…best!

may we all find a better day.

She’s been doom & gloom since early this year. Eventually, she’ll be right.

But for now, no sign of a recession here. Move along, kiddos!

Just like in 1980s….there IS a recession if YOU are in it. Been there….no fun.

Buy gold!

Those guys love gold. lol

Hide in your bunker!

Men carry more debt than women across all categories including c-card debt, except in student loan debt, women take home the gold.

Sorry no “gold” in my tale, just thought I’d sneak in uninvited…my apologies Mr suffering.

In 1970s women weren’t allowed c-cards unless co-signed by husband.

“Fiat currency always eventually returns to its intrinsic value – zero.”

– Voltaire

1. There are a lot of things whose intrinsic value is zero, including crypto and a lot of financial instruments. The intrinsic value of a building is ultimately zero because it will be torn down. The list goes on. Which makes the concept of “intrinsic value” kind of a funny thingy.

Also check out when Voltaire lived. Does this 250-year-old stuff still matter? They didn’t even have the internet back then, LOL, or phones, motorized vehicles, planes, mass-production, nada. People were dying at a young age in horrible ways because there were no actual treatments for even simple things, like infections… It was a different world.

2. No one invests in fiat currency, you can’t! You can only buy assets. Even the paper dollars are “notes” — and asset for you and a liability for the Fed — they just don’t pay interest, unlike other notes, and so they’re a bad deal and most people don’t hold a lot of them (unless they need to for some usually illegal reasons).

Voltaire should have added “… in a social democracy with an economically illiterate population” sorta like, you know, this one.

Nothing really has intrinsic value. Even a lot land had zero intrinsic value after the great plagues of Europe in the late Middle Ages.

Something is only ever worth what someone is willing to trade. Money makes it easy as it is a translator.

Without fiat currency you would be selling your house for other goods, such as 100 cattle, 3 pigs and a Toyota Corrolla.

You would work 40 hours and get paid in a new kitchen table and a TV.

Why all the relatively recent purchases of gold by countries (i.e. BRICs) and not the USA? I doubt it’s simply a hobby, i.e. I have a 100 Trillion Zimbabwe note that’s worthless.

So who is SELLING them the gold?? What do the SELLERS know that we don’t?

Who’s selling gold? Those who believe that the current fiat money growth will not cause a major financial crisis. From the beginning of the year DOW is up 4.4% while spot gold up 17.7%. Same pattern for 2000-2024. Same for the NASDAQ returns as well.

AIR and WATER have intrinsic value……the same for us, for Voltaire, or “most” any other critter that ever lived, as far as we know. Except virus, prions and some fringe chemical constructs like that.

There’s a 4+Billion year truth for ya’ll….although we are still just guessing….we weren’t there.

Just what is this FN “intrinsic” concept. anyway? A function of “x”, for you calculus fans.

The supposedly great Bloomberg reported in a daily email this week that credit card delinquencies were getting out of hand again.

What BS are these news agencies trying to promote?

The poor banks are crying because most people gained a lot of prudence during the pandemic and don’t want their credit. Doing without many items because they were out of stock or super inflated just showed us life is still good even with what we don’t have.

I may well be the only one in the publishing industry that actually tried to understand what the New York Fed’s “Transition into Delinquency Rate” means, how it is defined, what it is trying to say, and why it is multiple times higher than the “delinquency rate” by Equifax, the Fed, and Fitch. I spent hours trying to figure this out. It has been bothering me for years, and I finally nailed it (I think).

But it’s a lot harder to try to dig up and understand this stuff than it is to write clickbait BS about the tapped-out buckling consumer and the collapsing economy. And then the clickbait BS will obviously get all the clicks, LOL, which is why it exists.

EXACTLY WHY I do send you a ”generous” contribution every year Wolf!

Just so you will have the time to do your excellent reporting and analyses…

Please keep up the good work.

Thank you.

VintageVNet,

I agree 100% as to why we should all read – and try to understand – Wolf’s reporting every day.

He does his best to interpret the data and then explain it as clearly as he can.

I’m sure I’ve learned more about finance and money here than from any other website.

Or course or book for that matter.

I try to make an anonymous donation to him every year.

So anonymous , bet he would never guess you were the one.

Wolfs most splendid works.

An artist stands back and smiles at his work but for a moment…or two.

I remember my first credit card back when, such a fine gentleman I was, “put it on my card pussycat”.

Me too.

My first one had a limit of $50….early 70s. I could borrow $5 and get a gram of coke and share it (it makes you want to share). Soon realized that stuff is only for lawyers, rockstars, etc, and went back to those little white meth tabs that were everywhere….till I saw enough human wreckage to realize the “Speed Kills” slogan was very very true.

Still have credit card…..only use it ONLY for a few auto pays. Pay it ALL off every month if possible. Balance is usually zero.

LOVE the ATM.

With apologies if I missed it (I did RTGDA), do you know the definition of “delinquent” in the “transition into delinquency” rate? If it’s a single missed payment, it’s telling a much different story from 60+ days.

There are different degrees of “delinquent,” from newly delinquent (30+ days past due) to seriously delinquent (usually 90+ days past due).

You’re 30+ days delinquent when you, after having missed the regular due date, fail to make a payment by the next due date.

The measures here: Equifax and Fitch use 60+ days past due (as it says in the article).

The Fed’s measure here tracks 30+ days past due.

The NY Fed’s “transition into delinquency” has two measures: 30 days (the 9.1%) citied and 90 days (not cited here).

That’s why I read everything you publish even if I’m not so interested in some particular area, knowledge and understanding have real value, we are lucky you do this

…I particularly like and admire that the only books Wolf has EVER talked are his biographical ones…

may we all find a better day.

That’s true….never thought of that.

Maybe that’s why I like this site.

Later, Dustoff.

I’d be grateful for your take on Slide 12 of the NYFed Consumer Credit report, entitled “Percent of Balance 90+ Days Delinquent by Loan Type”. That graph is apparently NOT about “Transition Rates”. The data for credit card “percent of balance 90+ delinquent” is much higher than other reports, which is odd. It’s not clear how the data are generated, but if taken at face value, the trend in the series is quite concerning.

Both 30-day and 90-day rates are “transition rates”: the first are the balances over a 12-month period that transitioned into 30-day “new” delinquency; the second are the balances over a 12-month period that transitioned into 90-day “serious” delinquency.

I get what you’re saying, but I believe my question is about a different graph than the ones you’re referring to.

I am looking at the original NY Fed “Household Debt and Credit” report that you referenced, not your article.

I am asking about Slide 12 in the NY Fed report, entitled “Percent of Balance 90+ Days Delinquent by Loan Type”.

According to the notes on Page 43, this is “levels” data, not flows or transitions. The notes read: “Percent of balance 90+ days late. Percent of balance that is either 90-day late, 120-day late or severely derogatory. 90+ days late is synonymous to seriously delinquent.”

I think the graph you’re referring to is on Slide 14, “Transition into Serious Delinquency (90+) by Loan Type”, which is “flow” data. I get that, but it’s not the one I’m asking about.

The “levels” data on slide 12 don’t seem to be consistent with the other data. But the trend is quite concerning.

This is what the NY Fed’s Data Dictionary says about “(seriously) delinquent balances”: “it is based on the net increase in the aggregate (seriously) delinquent balance for all accounts of that loan type belonging to an individual.” No further detail provided.

What I can see is that this refers to a “net increase” of a balance and not the balance itself. So I can see what this rate is not: it is not the delinquent balance divided by the total balance, which would be a normal 90-day delinquency rate.

Thank You! It’s definitely clear that the data on that page cannot be anything like what the title of the slide would indicate to any normal person.

While the journalists are guilty of clickbait-and-switch article writing, I think the Fed authors of that report – and their managers – need to be fired for lack of clarity in their reporting.

A standard monthly or quarterly report which attracts such a high level of misunderstanding needs to be much more carefully written. It should not be just a 2-page text note and a bunch of auto-generated slides with misleading titles, followed by an inadequate and ambiguous summary of methods used.

Agreed.

I do want to mention that page 12 data never gets discussed in the NY Fed reports. It’s exclusively the “transition rates” that get discussed. Those transition rates kind of make sense, but are conceptually hard to figure out and are too complex for headline material. But table 12 doesn’t make sense to me, and maybe it doesn’t make sense to the folks at the NY Fed either, which is why they never mention it. Maybe some researcher stuck it in there 15 years ago, and it has been autogenerated for 15 years without anyone paying attention to it.

“This line in italics was then widely misreported in the financial media and blogosphere”

Augmented, no doubt, by Artificial Ignorance as well as natural laziness and stupidity among the remaining members of the meaty media.

If only there was an independent source of vigorous and educated analytical content available to us all. I’m sure we’d all be willing to pay for such…

Brilliant work, as always, Mr. Richter.

“Credit card balances, which reflect spending and not borrowing, are up only 63% from 20 years ago, despite 73% CPI inflation and 16% population growth.”

How much did wages go up during this time?

Disposable income rose by 152% from 2003 to June 2024

It looks like all blended, weighted components of the CPI went from 184 in June 2003 (index value, with 1982-1984 set to 100) to 314 in June 2024.

That’s a 170% increase.

Greater than the reported 152% increase in disposable income.

(I wonder what disposable income did from 1982-84 to 2003…)

That result seems a lot more consistent with the general attitude of the country over the last 20 years than any sunnier version.

I’m still working on getting the housing CPI data for 2003 to 2023.

cas127

“That’s a 170% increase.”

From 184 to 314 is not a “170% increase,” LOL, but a 70% increase.

So a 70% CPI increase is NOT “Greater than the reported 152% increase in disposable income,” but less than half of it, meaning that disposable income outgrew CPI inflation by a big margin over those 20 years.

Do you ever just like run out of bullshit?

“Equifax, the Federal Reserve Board of Governors, and Fitch Ratings report “delinquency rates” the way we normally understand them as a level at a certain point in time (month end or quarter end).”

I understand that this is the way the rates in these instances are normally understood based on their common use but it’s just wrong. This is a constant frustration of mine with the media. A rate in all science communication is a value divided by the time in which the change occurred (i.e., change over time, gallons per minute). At a minimum it is normalized to SOMETHING (e.g., molX/molY, but that is stretching it and would normally be called yield). It is, and never should be, applied to a quantity (i.e,. level of a reservoir/reservoir volume, measured in gallons), which is what it’s being used for in these instances. I do not feel that there is much latitude with this. Rate seems to be misapplied left and right in the media and it drives me insane. The NY FED appears to be using this term correctly, despite the others, and it appears that Wolf also had a hard time figuring out WTF these misapplied uses mean. No wonder the public has such a hard time understanding! Semantics for president!

Your understanding of “rate” is so wrong it’s funny. Rate is used in many ways. There are exchange rates, for example, which is the rate at this very second. There are rates you’re being charged or paid for something. There are interest rates. There are rates of increase and decrease. He’s driving at a rate of 60 mph. There are rates of rates.

And so there’s the delinquency rate. A delinquency rate is the $-amount delinquent divided by the total $-balance at a point in time (for example, at month end).

But what the NY Fed is doing is NOT a “delinquency rate.” It’s a rate of “transitioning into delinquency” — it’s the $-amounts that transitioned into delinquency over a 12-month period divided by total $-balances.

I suggest that you get an unabridged dictionary and look up “rate.” You’ll see that it has a dozen-plus meanings and uses.

Wolf writes: “Rate is used in many ways.”

Which brings to mind a joke …

“A guy goes to see his Doctor who asks

‘How would you RATE your pain?’

The guy answers ‘Zero … would not recommend’”

I was illuminated to the existence of “contranyms” recently.

They didn’t teach me about those in grammar school!

ah the formula. great work . this has been bugging me , a former programmer analysts. all morning .

Also look up Ellie Goulding’s hit “Burn”!

lol just kidding

Wolf, you haven’t mentioned the great renaissance of the semiconductor manufacturing returning to America lately. I guess Intel, Wolfspeed, Global Foundries and Micron’s ever deeping losses from capital expenditures has something to do with it. You could add a new imploded stocks list from that group of foundry failures. When you first posted your semi manufacturing blog, I listed the many reasons that America’s 10s of billions spent on foundries would fail! What’s hilarious is Intc contracting its latest and supposedly greatest chips to TSM! Imagine what would happen to all the domestic car manufactures if Chinese EVs were allowed to be sold in America and the EU without tarrifs! Free trade is dead and mercantilism is great.

“…you haven’t mentioned the great renaissance of the semiconductor manufacturing returning to America lately. I guess Intel, Wolfspeed, Global Foundries and Micron’s ever deeping losses from capital expenditures has something to do with it.”

LOL, I most recently mentioned it on August 1 (roughly 9 days ago):

https://wolfstreet.com/2024/08/01/eyepopping-factory-construction-boom-in-the-us-reaches-new-highs-amid-big-corporate-strategic-rethink/

I admire you Wolf, being patient and have to correct these these people who come up with the most random of statements.

Wolf,

I believe the intended graph is missing for the “Credit card statement balances” paragraph in your report. You have a parenthetical remark about a “red line in the chart below”, but I don’t see the chart you are referring to.

Never mind — the graph is shared with “other consumer loans”. I see it now.

It would be interesting see these number broken out by income quintile. I keep hearing lots of people are hurting out there, it would be interesting to get a handle on who that is and why.

” I keep hearing lots of people are hurting out there”

The first thing you have to do is stop listening to clickbait bullshit out there on YouTube and on the internet about the collapsing consumer. It just pollutes your brain.

So 3% delinquency rate means that 3% of the balances are past due. So that’s a tiny portion of credit card holders that is in trouble.

Read the article on auto loans. About 63% of the people that buy a used car pay cash for it. Of the 37% that finance, 14% are subprime. (14% of 37% = 5% of used-car buyers. And on new cars, there are very few subprime finance deals being made.

As a rule of thumb, the bottom 20% on the income spectrum never have enough money and are hurting. And they’re unlikely to get a credit card, and if they get a credit card, it’s going to have a very low credit limit. Those are the people who are hurting. They have no financial leeway.

Then there’s a tiny sliver of the population (less than 1%) that is homeless in various stages and forms (including those living in a car or RV or couch-surfing). Obviously, if that sliver is 0.5% of the population, that’s still 1.5 million people, and so that’s a lot of people, but it’s a tiny sliver of the population.

If anyone making above the median income locally (top 50%) is “hurting,” it’s because of their own decisions to live beyond their means, or because of some unfortunate circumstance, such as a huge medical problem.

So true

Schwab has no credit cards. Investors/traders have a buying power and

cash available to withdraw. Since Schwab mange $10T cash available withdraw is in the trillions. If broker’s cash available is in c/c balances it

can explain the spread.

not directly, but they have a partnership with american express for the platinum card. you can get a discount on the $695 annual fee if you have a brokerage account with certain amounts of money in it.

SPX made a new all time high in July. Disposable personal income (DPI) is testing the money tsunami high. Disposable personal income excludes realized and unrealized gains. If demand for highly skilled and semi skilled workers will rise, along with the rise of RE and the stock markets consumers will have enough fuel in the tank to carry them for years, even

after a few stock market corrections, (realized gains).

The US gov will collect higher taxes, fill its coffer and will be able to cut

debt, if they are committed to cutting debt.

July 10th was my last favorite day.

If you know, you know. ;) haha

⬆️

As an engineer, the way I look at it with Wolf’s excellent explanation:

1) The standard way of reporting is just the total delinquencies in a given month. If this is 1%, I will yawn. If it is 50+%, then I might expect a recession soon.

2) The Fed is looking at rate of change of delinquencies. Again, if the rate changes 1%, I’m yawning (unless the total is already 99%). If the rate goes to 100% but the total is 3%, I would expect a correctable action could be implemented before the total reaches too high.

Wolf has clarified on how some mislead with statistics.

I recognize the transition to delinquency is metric is generally misunderstood, but still like looking at it to see how the latest transitions compare to prepandemic levels.

I’m more interested in seeing when commercial bank CECL provision expenses start increasing, that’s the canary I’m watching for.

Everything is wonderful. A bit weird perhaps, but wonderful.

This is a great article on CC delinquency rates but the best insights Wolf gave me has been his statements about how CC’s are growing as a basic payment mechanism. An expensive and inefficient payment mechanism (my words), but convenient nonetheless.

Over 50 years, people have learned how to use CC’s and/or Banks have become more adept at who and how much credit they extend.

Nobody seems to worry about money. Nobody seems to need a job. If you are careful not to pay any attention to the media the world is fine and everyone loves Americans just like they always have.

On the surface it seems like 30 years old is the new 21 as far as independence is concerned and fewer and fewer females seem to see child bearing as at thing. But those are generational problems.

It is odd though that suddenly the Coast Guard is out of the Icebreaker business. They had 2, but one (the Healy) just had an engine room fire and the other (the Polar Star) is 50 years old and still in dry dock as part of a life extension overhaul.

The Healy is back in port, but nobody can say when it will be repaired. It’s almost 30 years old and much of the supply chain for the ships engineering components on longer exists.

Of course, who cares about the Artic etc…But to me it’s just strange that our economy is so great, but seems less and less capable of building and maintaining stuff even if Credit Cards are not a problem etc…

“Everything is wonderful. A bit weird perhaps, but wonderful,” is the silliest and most grotesque misstatement ever, and no one but you said that here.

But what this article is saying is that the CONSUMER is not collapsing under the weight of credit card debt, and prior articles have said that the consumer is not collapsing under the weight of any debt, because the consumer has deleveraged since 2008, as you can tell by the ratio of debt to income.

In terms of debt, the problem has massively shifted to the government being way overindebted and totally on the wrong track, and to businesses that are way overleveraged, and to real estate being way overleveraged, and finance in general being way overleveraged. This has nothing to do with building ice breakers. It’s not a mass-produced item that you need a lot of. You said yourself, it has been decades since the last one was built. You’re cherry-picking a peculiar problem to then twist and torture that cherrypicked problem into a big economic BS theory. That’s just funny when you think about it.

Wolf: AND of course, all this ^ is the problem!

The music is still playing in the West, but the hegemony previously enjoyed is becoming more of an equal footing with the East.

The Fed has a public mandate, but the reality is that it has NOTHING without the confidence in the house of notes you allude to above.

We know the last crisis is not the next crisis (don’t look for the housing market to blow the house down) but we also know the Fed has to be quite concerned about overall stability in the financial system.

Sadly they just print the money and there’s a 1000 person committee that promises to spend at least 150% of whatever they can print.

Personally, these are the points I am concerned with. The flagging confidence can muddle along for decades more, or could evaporate overnight.

This from a January 2024 article by Cleveland dot com. Not sure where the idea came from that the CG is out of the icebreaking business.

“Here are three key numbers from the GAO report:

33 existing ice breaking vessels

The report said the Coast Guard generally meets its icebreaking goals in the Great Lakes, New England and the Mid-Atlantic with its 33 existing vessels used for icebreaking – including heavy, medium, and light domestic icebreakers as well as two types of ice-capable buoy tender vessels – but has challenges with its aging fleet and will need more heavy and medium capacity vessels to do the job in the future.”

1) For decades the Fed controlled the front end. After Oct 2008 The Fed

controlled both the front end and the long duration. The US gov rates were negative for decades. We got hooked on zero rates. So is Japan. For decades the inflation rate in Japan was higher than gov rates. Debt was rising, but deflating in real terms, though not at the same rate.

2) If the US gov will be fully committed to cutting debt and the Fed will cut rates it might boost the economy and help cutting debt in real and nominal terms.

3) After a few years, if it works or not, the Fed will have to raise rates to reduce risk. If successful, debt might drop by 25%/33%. Gen alpha, Gen Z and millennials will surf on it for decades.

Michael: I am not sure if I love your undying optimism

OR

If I should be deeply concerned about your delusional state?

Man you are spot on about how click bait works. That’s why I check here with Wolf for factual observations, minus the hype.

“I have some fantastic news about my new business!! Calling all investors!!”

Click Bait Headline:

“Lemon-aide stand sales are up 67% in one day!!”

Basis:

Yesterday sold 3 cups of lemon-aide, today sold 5.

Smile.

The NY Fed’s Consumer Debt and Credit Report for Q2 said this:

“Over the last year, approximately 9.1% of credit card balances … transitioned into delinquency.”

Wolf wrote: “This line in italics was then widely misreported in the financial media and blogosphere as a delinquency rate of 9.1% (as if it were a level at quarter-end), when it was in fact an annual flow into delinquency.

Meanwhile, the actual “delinquency rate” was 2.81% for bank cards and 4.44% for private-label cards as per Equifax; and 0.99% for prime-rated credit cards as per Fitch. The Fed’s credit card delinquency rate at commercial banks will come in at around 2.96% for Q2.”

So if the percentage of credit card balances (accounts?) that are delinquent at the end of a given quarter is, say 3%, but over the past 12 months the percent of balances (accounts?) that ‘transitioned into delinquency’ is 9.1%…. it appears that within that 12 month period, about 2/3 of CC accounts that went into delinquency likely came out of it?

Interesting. I wonder what a graph would look like over time, of ‘quarterly % of accounts in delinquency’ divided by ‘annual % of accounts entering (transitioning into) delinquency’. How that number would stack up during periods of inflation, deflation, QE, QT, recession, etc. (I’ll attempt but it’s above my pay grade!)

Yes, people fall behind with a payment and then catch up. Happens a lot. Some of it is accidental, such as an automatic payment not working properly and cardholders aren’t immediately aware of it, or people going on vacation and forgetting to make the payment before leaving. A lot of it happens in the typical way, tight on money (job loss, hospital, over-the-head purchases, etc.), so the payments get missed, but then people catch back up. This is fairly common, particularly with young people that are still learning the ropes. Which is why delinquency rates have always been much higher for young people; it’s part of the learning curve. Lots of data on it. And lenders know that too. And they know that these young customers can become loyal customers over the long term. So banks play along. They all want to bring young customers on board – that’s an investment in the future.

Actually, it doesn’t look like that ratio ( % of accounts Delinquent / % of accounts entering delinquency) tells us anything special. Just glancing at the two curves, they look highly correlated, dovetailing each other.

Never mind ;)

Credit Card and Auto Loan Delinquencies Surge in the Second Quarter

https://mishtalk.com/economics/credit-card-and-auto-loan-delinquencies-surge-in-the-second-quarter/

RTGDFA

LOL. That kind of ignorant clickbait bullshit is precisely why I wrote the article.

Mish wasn’t the only one. The whole blogosphere was full of this ignorant clickbait bullshit.

So DO READ my article. It explains it. And it shows you the actual delinquency rates from the Fed, Equifax, and Fitch, which declined for the fourth month in a row.

Great article. Wolf should be on CNBC. I wonder how much this affects banks.