QT keeps draining liquidity from the financial markets.

By Wolf Richter for WOLF STREET.

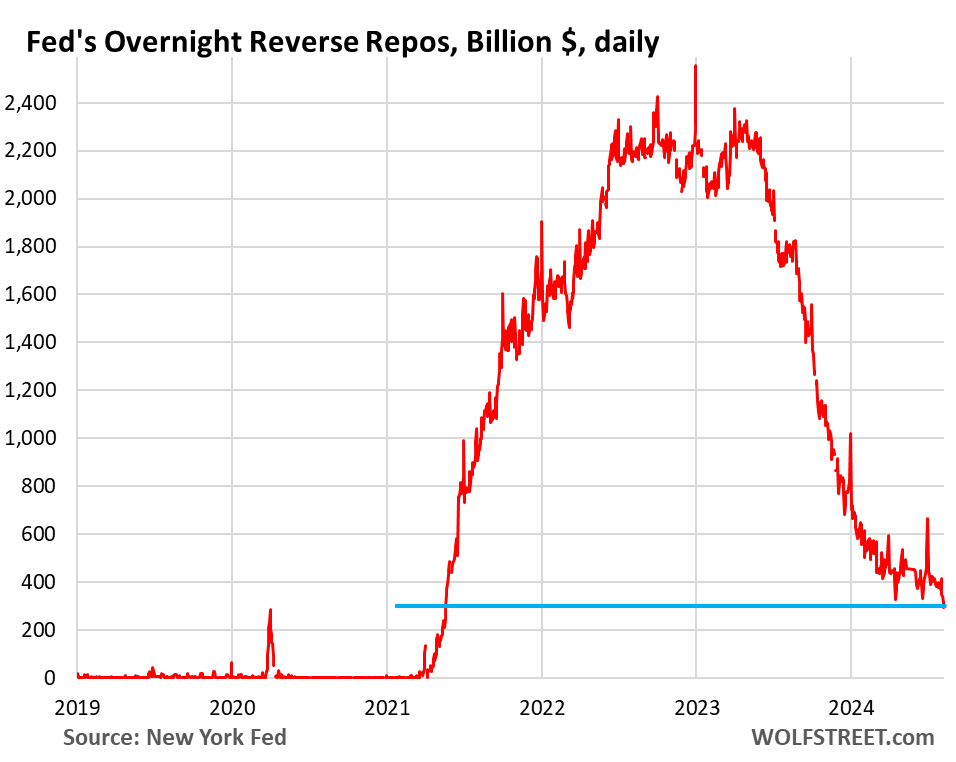

ON RRPs, or Overnight Reverse Repurchase agreements, on the Fed’s balance sheet fell to $292 billion today, the lowest since May 2021, down by over $2 trillion from the $2.3 trillion range in May 2022 through June 2023, and down by $2.26 trillion from the absolute peak at the end of December 2022. They’re well on their way to zero, or near zero, where they were in normal times.

The plunge in ON RRPs is largely a result of the Fed’s QT, which has shed $1.78 trillion in assets from the balance sheet. ON RRPs represent cash that the Fed’s domestic counterparties, mostly approved money market funds, have put on deposit at the Fed to earn 5.3%, a rate set by the Fed as part of its monetary policy rates.

In addition to the QT drainage, a smaller portion of ON RRPs has shifted into the banking system and to reserves, which is cash that banks have put on deposit at the Fed.

Excess liquidity is getting drained.

ON RRPs represent largely excess liquidity that the Fed created during QE that financial markets don’t know what else to do with. The spikes in the chart occurred at quarter-end and at year-end for window-dressing purposes.

ON RRPs have been used mostly by money market funds that have to invest in high-quality short-term instruments. Money market funds have many other options, including Treasury bills and lending to the repo market. They will shift funds to where they can earn a little more and still satisfy their liquidity needs.

Other approved counterparties are banks, government-sponsored enterprises (Fannie Mae, Freddie Mac, etc.), the Federal Home Loan Banks, etc.

ON RRPs have existed for many years, but in normal times, they’re zero or near zero. And now they’re going back toward their normal level.

Nothing has blown up yet.

There was a big to-do early this year in the financial media about the Fed being “forced” to end QT when ON RRPs drop to $700 billion or whatever, because it would draw so much liquidity out of the system that something would blow up.

The Fed leaned against that notion, and Fed governors Waller and Logan, in discussing the future of QT earlier this year, have pointed out that the normal balance for ON RRPs is near or at zero, and they expected QT to continue as ON RRPs reach that level. And nothing has blown up yet.

Draining liquidity is risky and something could blow up…

Liquidity doesn’t always move around the financial system smoothly and equally, to get where it’s needed from where it’s in oversupply. That’s the function of yield; where liquidity is needed the most, yields rise, and where it’s in excess, yields fall, and so cash follows the higher yield to where it’s needed.

But if liquidity doesn’t get there in time, something could blow up. So the Fed has slowed QT as of June to give liquidity time to move to where it’s needed. In July, total assets fell by $43 billion, roughly half the average pace in prior months.

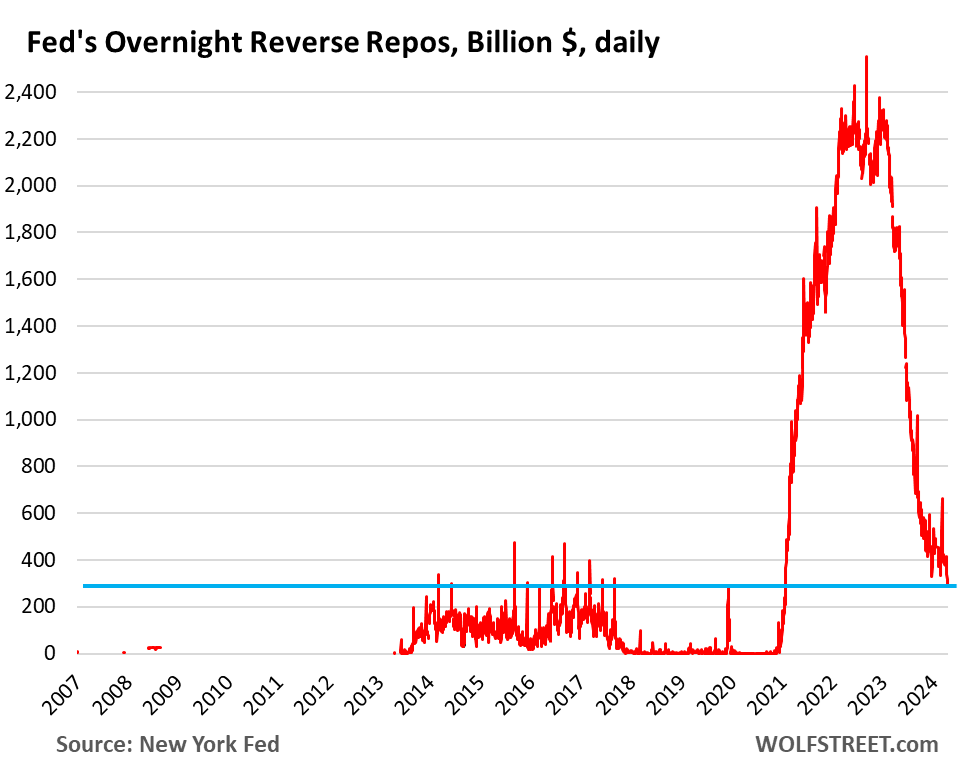

The long-term chart of ON RRPs also shows the effects of the first wave of QE after the Financial Crisis. Excess liquidity with no place to go started building up in ON RRPs toward the end of QE in 2014. The first wave of QE ended in December 2014, after which the Fed kept its balance sheet roughly level until late 2017. QT-1 started in late 2017. ON RRP balances started declining in 2017 and returned to near-zero in 2018.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Today I received an email from Schwab, which is playing the gimmick to attract deposit with cash rewards now. Many banks are offering attractive CD rates and outstanding preferred dividend. Last time I saw this is 2008 from banks like Washington Mutual.

Competition for cash deposits has been going on for two years. Maybe you missed it as we were discussing it here. Money market funds and T-bills drove it, as people yanked their money out from banks, including Schwab Bank, and put it into MMFs and T-bills. But Schwab Bank has refused to offer 5% or even 2% on its high-yield savings account and sweep account, and customer put their cash into MMFs and T-bills. They’re still just counting on the laziness of its customers and use their cash for nearly free to lend out at 8% for margin loans — what’s not to like, if you’re Schwab? But eventually, people get smart, and cash left Schwab’s sweep accounts and went to elsewhere to earn 5%.

When companies treat you that way, you yank all cash out of that account that you can. Maybe you need some trading cash and operating cash, so OK, but the rest needs to go where it earns something.

raisin fka savebetter is offering a 14-month 5.15% cd through sallie mae.

Schwab offers a 5.15% MMF with their brokerage which is very competitive. If people move their money from their Schwab bank account to their Schwab brokerage account, how is Schwab negatively affected by this?

Maybe they’re not allowed to loan the MMF funds out to margin accounts?

DM,

1. Moving cash from Schwab Bank’s sweep account or regular bank account into a Schwab money market fund is a huge problem for Schwab. If too much of this happens, Schwab Bank would be at risk of collapsing. There is a fundamental distinction between your cash on deposit at Schwab, and when you buy securities with that cash, such as a MMF. When you buy a security, no matter what kind, Schwab no longer has that cash. It’s gone.

When customers shift cash from Schwab Bank to MMFs, that cash LEAVES Schwab, because Schwab’s MMF is a mutual funds that sells securities to investors, and it has to use investor cash to buy T-bills, corporate paper, lend to the repo market, etc. It’s no longer Schwab’s cash at all. Now the customer has a security (SWVXX for example), not cash. And Schwab doesn’t have that cash anymore either, if went into credit markets. For Schwab Bank, it’s no different than if you bought stocks with that cash.

2. The cash in Schwab Bank is cash that Schwab can lend to margin borrowers or it can buy T-bills with it, and whatever income from the spread it makes is Schwab’s income. But if you buy Schwab’s MMF, the income from the cash goes to you, and Schwab only gets a 0.25% annual fee.

Jeez, really??? I have fidelity and interactive brokers. They both pay close to the treaury market rate for idle cash. It’s not just lazy leaving your money uninvested at schwab. It’s lazy to keep an account there at all.

I believe Wolf is referring to the laziness of those who don’t move it to a MM fund.

Schwab sweep account pays a whopping 0.45%. If a client moves from schwab bank to schwab brokerage account without moving those funds to a MM fund that’s what they receive.

Until 2-3 years ago they did have a MM fund account which brokerage account holders could use to have settled funds swept.

So Schwab is negatively affected when client’s move their free cash to a MM fund.

Wolf is talking about two Schwab entities: Schwab Bank and the Schwab Brokerage. Separate operations: one’s a FDIC bank; the other is the brokerage.

I have an account at Schwab, and when I try to buy treasuries, there is a minimum purchase of $200,000 to $1M required to get a decent interest rate. It wasn’t this way 6 months ago. Perhaps they are trying to upscale the customer base.

I haven’t looked into this problem because there are other options for buying treasuries. At ETrade, I can buy quantities in the $20,000 to $100,000 range without any difficulty, and I get the market rate.

In any case, any money left uninvested at these brokers is going to earn just a faction of a percent annually. Best to keep excess funds in an ultra short-term treasury etf you can buy and sell instantaneously while earning 5%.

I have no trouble buying T bills through Schwab. I can buy $ 20K or $200K. I do it online, as the department that handles them is either too busy or doesn’t like working with small investors.

Are you buying after hours? That’s when I see the huge minimums. If I buy during working hours, I can always get under $25k minimums (often $1k)

Exactly.

Don’t take this the wrong way, but do you know how to look at the depth of book at Schwab? Or I think they call it Market Depth. During trading hours there are usually amounts of $5000 or less. Unless that has changed in the last couple days.

You can also just buy at TreasuryDirect in small increments. Super easy.

I have no problem buying treasuries in bundles of $1000 thru my Schwab account. Some CUSIPs have high minimums; most don’t.

Much more common for agency & corporate bonds to have high ($10k-100k) minimums.

Really Boober? I buy 10-20K amounts of T-bills regularly @ Schwab. Rates are the similar as @ Fido, trending down toward 5% over the last few weeks. Definitly slightly better rates when buying larger quantities but only slightly.

You can buy in $1k increments if you go to the Treasury Auction page. Orders placed Tuesday and Wednesday are executed on Thursday.

Why aren’t you simply using treasury direct? I buy pretty much whatever I want (minimum to maximum, which for T-bills is $100 to 10 million) during the regularly auctions/offerings. Having a bank or brokerage do anything for you just pays their fees.

Fuck the middlemen, they are the problem.

Related to the above discussion, today I was unable to *sell* one of my T-bills because it has a 50K minimum on the sell side in my brokerage (Merril), which is more than the amount I hold. Not a huge deal as I rarely sell things before maturity, but this was surprising to see.

The CUSIP is 912797KA4 if anyone’s curious.

“Why aren’t you simply using treasury direct?”

Because I frequently move money between risk assets and T-bills which are my ‘cash pile’ in my brokerage. This would be a PITA if I held them in my TreasuryDirect account, which I only use for I-bonds.

I was getting a special relationship rate MMA with a regional bank above 5.3% for about 7 months. Near the end of the deal, they wanted to bump it down to like 4% citing future rate cuts and other nonsense. Kept on pushing to buy a CD.

I told them keep it the same and I will keep my money there. I have other options if you don’t. They basically told me I was full of sh1t and called my “bluff”. FAFO, MFers.

So, the end of my term, I came in and asked for a cashier’s check and closed my account. The manager’s eyes freaking bulged out of her head. It was funny. I was being a serious d1ck and said that I told you that I would do this a few weeks ago. Do you think a guy who can put this amount of money f@cks around? Not often can you slap a bank around a bit. Banks are NOT your friends.

Branch managers are underlings. They have no authority to change interest rates offered on accounts. Those are corporate decisions made in part by algos. It’s take-it-or-leave-it at the branch.

But kudos for yanking your money out. Banks need more of that. That’s the competitive pressure that can keep deposit rates higher. Or else they go back to zero, if banks had their druthers.

Sorry, if I sounded a bit too harsh on the managers, they are just playing their part. Yes, they have to go up the chain to get permission to give me the their special relational rates, tier 1-3 or A-C or whatever. It is usually nice affair where I get to sit in the manager’s office and have a cup of coffee or water.

I was just rather shocked when they denied me and actually had the rudeness to ask the name the bank that was giving me better terms. Without missing a beat, I said follow the money and asked for a cashier’s check. Yeah, I won’t be getting a holiday fruit basket this year from them.

I don’t have a huge amount of money to threaten lowly bankers with, just a meager portion of the down-payment for a place I’m hoping to buy eventually. However, all of it is sitting in MMF short term T-bill etfs, I keep my account only because I don’t feel like changing direct deposits and stuff like that but as soon as cash hits the account it mostly goes to t-bills right away, they get my $10 a month service or whatever.

At one point my banks CC department was trying to attract debtors so they offered 0% for a year on debt transferred to the card with a 3% transfer fee, I bought everything on a cash back card from another bank until the cutoff date, collected that % (between 2%-4%), transferred the debt to the promo card and instead of paying it off all these months just dump more into t-bills. I’m pretty sure they expected cuts much sooner, in 2 months it’ll be a full year so I’ll pay it off in full and they’ll have let me earn interest on money they loaned me almost for free. Not huge amounts but it feels good to take advantage of them for once.

Fidelity is getting more of my business than Schwab right now because of the cash sweep interest rate crap. But I do have accounts (myself and family) that need to stay there for various reasons. SWVXX (taxable) and SWTXX (muni tax-free) require manual buy/sell with the end of day lag. SNAXX will give you 5.3% if you have that much sitting around.

Schwab was like “ You no sell ok?”

Oh no….sky is falling….we need rate cuts 3 times in Sept now…better yet, emergency meeting to cut 75 basis pts next week…..today’s up day? Ignore that….

What a joke…plenty of data still shows nothing is broken yet these MSM crybabies, crack addicts..

Sooner the RRP goes to zero, it is better for the health of the financial markets long term. Nothing will blow up because RRP goes to zero. To prevent blow-ups, Fed introduced standing facility repos for 500 billion. It there are signs of blow-ups, they can raise it to a trillion dollars in a second without any problem. I don’t think they will need to increase the standing facility.

With massive borrowing by treasury between now and the end of 24, it is very likely that RRP will approach zero very soon.

The RRP bal has been hovering as private repo spreads remain very tight. DVP repos are currently 5.35% and RRP is 5.3%… only 5bps of compensation for risk!

The SRF is totally different – that is meant to put a ceiling on repo rates (RRP puts a floor under rates). At quarter/year end, repo liquidity can get tight as banks do their “window dressing” trades to comply with regulatory reporting, causing repo rates to rise dramatically This is the reason for all the little spikes on a chart of SOFR (or private repo) rates.

I can see the RRP going to zero after the transition to centrally cleared repos is complete.

But isn’t the Treasury pumping liquidity via purchases of ST bills to fund the TGA? And isn’t the TGA flush with cash? Thereby having massive amounts of liquidity to inject, as needed.

You got that totally backwards. The Treasury is SUCKING UP liquidity (cash) by SELLING T-bills to fund the TGA (government’s checking account). Funds that are in the TGA are not in the economy, they’re at the Fed. When the TGA balance rises, it sucks liquidity out of the financial system. When the TGA declines, it adds the liquidity it had sucked out of the financial system back into the financial system.

Well explained! Eric, when US borrows, money moves from RRP to TGA on Fed Balance sheet. When TGA comes down, it finally ends up as increase in bank reserves at Fed or as RRP when banks discourage deposits, as big banks did a couple of years ago.

And at the rate the Treasury is increasing the sales of Treasuries, the amount of liquidity being sucked up has a big effect on the rest of the economy….

Wolf, I read an article the other day that the Treasury is manipulating the market by limiting the amount of long-dated notes / bonds over the last several months. With supply drying up, this is supposed to be pushing down yields.

Have you seen any evidence of this?

Thanks!

The Treasury Department is not “manipulating” the market, LOL. They’re selling products (bills, notes, and bonds) in a way that they hope will save taxpayers some money in the long run. That hope might not work out. But they’re trying, and as taxpayer, I’d say, OK.

Wall Street is who manipulates the market.

The Treasury Dept is trying to save the taxpayer money by adjusting the product mix they’re selling to not put too much upward pressure on long-term interest rates that would lock in high interest expenses for the government/taxpayers for many years to come.

Manipulating might be a bit strong but they did purposely change there allotment of debt to focus on issuing more short term last October. This was when the markets we’re crashing in what appeared to be a panic over rising yields and government debt.

Short term debt had been above 5 for quite a while

Long term debt below 5 so not sure where the tax payer savings comes in

Call it what you want but they didn’t want to add supply to the long end of the curve and put pressure on assets.

Kicking the can down the road usually just leads you into a really bad neighborhood

@GuessWhat

There have been credible reports that Treasury is restricting the supply of long bonds, and keeping short bonds plentiful

The critics describe this as “stupid”.

I don’t know if this is “manipulating the market”, but it sure looks like “managing the yield curve”.

My personal opinion is that they should have issued more long bonds when the interest rates were very low. Many people think that current long bond interest rates are pretty low, and that Treasury should be tilting towards sales of long-term paper.

Your mileage may vary.

1:04 PM 8/6/2024

Dow 38,997.66 294.39 0.76%

S&P 500 5,240.03 53.70 1.04%

Nasdaq 16,366.85 166.77 1.03%

VIX 27.71 -10.86 -28.16%

Gold 2,430.40 -14.00 -0.57%

Oil 73.00 0.06 0.08%

Yup. The Stock Market is “fluctuating”.

I wonder if the inflation balloon is still full of air. Maybe the balloon will just float away if we pretend it’s not there.

I’ve never found balloons to be that interesting, even tho some giant balloons filled with helium could get me a bit higher than usual…that would be fun.

Well if the balloon isn’t going to burst and destroy the economy, than this movie is rather long and might I say a bit disturbing.

Anybody out there ever been attacked by a porky pine…

Nothing will happen when the RRP goes to zero, simply nothing. No blown up anything or a banking liquidity crisis. The whole panic earlier this year created by the so called analysts who knows nothing about the functionality was -as i said previously- completley unnecessary.

Schwab manage $10T of customer’s assets. ToSwim is bs. They make money on the spread. Yesterday’s spread was large. They pay u o/n nothing, but charge a lot. High net worth > $5M get a discount. Schwab feast on day traders who generate millions in annual vol : buy & sell, with a min of $25K account. Trading is hard work.

Example : $20K buy & $20K sell, one rd trip = $40K. three rd trips/week = $120K x 52 weeks ==> $6M.

ON RRP levels declining is good for overall financial system. But I feel decline has slowed down in recent months compared to 2022-2023.

When I see ON RRP chart for last 6 months I see levels going upto 600 B. Its fluctuating a lot and declining. But decline has slowed down.

FED should waited to ON RRP levels come to 100 B range before slow down QT. That would have been better move. Slow-down needed to go further. But it was too early.

It’s not a straight line. And it’s unpredictable, as we found out:

About $500 billion shifted from ON RRPs (MMFs) to reserves (banks) in the 12-month period from about April 2023 to March 2024, which is why reserves ROSE during that time, as ON RRPs plunged much faster than expected. QT was supposed to bring down reserves and ON RRPs, and it did at first, but suddenly reserves started rising again, as ON RRPs plunged, which surprised even the Fed. Starting in April 2024, reserves trended lower too, but they’re still about $400 billion higher than in early 2023.

So what you saw in 2023 and early 2024 was plunging ON RRPs because part of the liquidity shifted from ON RRPs to reserves, and part of it was the drawdown from QT.

So the drawdown of ON RRPs was much higher than QT (about $500 billion more than QT from absolute peak to now) and much faster than QT. When the Fed decided to slow QT in March/April, that’s what it saw… that ON RRPs were vanishing very rapidly, much faster than expected, and could have been zero by June at that pace.

But then about that time, reserves started coming down finally, and the shift to reserves ended, and so the decline of ON RRPs has slowed… after the Fed decided to slow QT.

Ultimately, it’s both reserves and ON RRPs added together that indicated financial market liquidity stashed away at the Fed.

Repo rates of yesterday:

GCF 5.43%

DVP 5.35%

RRP 5.3%

TriParty 5.27% (!)

There’s so much liquidity in repo markets that lenders are willing to lend to 3rd parties for a lower yield than what the Fed offers. No wonder there’s still demand for the RRP.

What do you think about BIL yield 5.25 fee .14

The QE policy following the 2007-2008 market crash was a real masterstroke. Those who are in power have managed to have the system unscathed from what was an existential crisis. Despite what you feel about Governments intervening in markets, currently, they have managed to reduce their exposure. Also, with a higher interest rate they have the leverage to make a big drop in the interest rate if there emerges any sign of break up. The reality is that there appears no sign of any catastrophic even barring a WW3!

The Fed induced a credit crunch. Instead of bolstering the nonbanks (like during Reg Q ceilings), the banks were gifted with IORs. So, the nonbanks shrank by 6.2 trillion while the banks expanded by 3.6 trillion.

LOL. You missed something somewhere. The nonbanks are now the dominant originators in mortgage lending. The nonbank lenders have totally blown away the banks in mortgage lending. United Wholesale Mortgage and Rocket Mortgage each originated nearly 300,000 mortgages in 2023, compared to the largest bank on the list, BofA, which originated just 92,000 mortgages. Wells Fargo, which used to be #1, fell off the top 10 list entirely.

Curious how much the drop in ON RRPs are simply just investors moving from MMF to buying treasuries directly from the auctions to reduce the tax burden?

From what I understand, the ON RRPs are implemented mainly via MMFs.

Well, MMF balances have spiked and hit a new record in Q1 of $6.44 trillion. So more new money went into MMFs than left for T-bills:

Wolf, i believe you addressed this before, so apologize for the inconvenience. The Reverse Repurchase Agreements (WLRRAL on FRED) balance is $813B as of 7/31. But per your note and per RRPONTSYD on FRED, the Overnight Reverse Repurchase Agreements for Treasuries Sold by the Fed is $292B as of 8/5.

I believe the later is a component of the former. Is the remaining $521B mostly consist of transactions with foreign central banks which are “business as usual” transactions? If so, that seems high to me historically as i believe that was closer to $300B pre-pandemic.

Your figure is a weekly figure (as of last Wednesday), of 2 types of reverse repos:

1. ON RRPs (used by domestic money market funds and other domestic counterparties)

PLUS

2. Foreign official reverse repos, where foreign central banks stash their excess USD cash.

My figure is a daily measure of only ON RRPs (domestic MMFs and other domestic counterparties)

Wolf. Please explain the effects on both short and long term interest rates with a “slower economy “ which reduces the public’s demand for money to fund purchases; while at the same time the US government is creating huge demand for funding by is spending deficits. Deficit’s usually go up in a recession or slower economy as tax collections decrease.

Relatively little consumer spending is funded with borrowed money. Homes don’t fall into consumer spending, they’re considered asset purchases, not “consumption.” 80% of new cars are financed or leased, and 40% of used cars. Higher rates have not really slowed demand there, and unit sales in 2024 are so far the highest since 2019. The rest of consumer spending is funded from income, and incomes are up.

The people that bought houses since mortgage rates went over 5%, they’re facing very high mortgage payments, and they’ve cut back some on their other purchases, but that’s just a small portion of households. The other homeowners don’t really feel higher mortgage rates, and they haven’t cut back spending. The 30-year-fixed rate mortgages are one of the reasons that consumer spending has kept growing at a decent pace despite higher rates. I’ve covered this in my articles many times.

Government finances are a huge mess, obviously, but this deficit spending is stimulating the economy. And there’s still lots of liquidity sloshing around from 15 years of QE that it’s chasing after everything, which you can see by the longer-term Treasury yields, such as the 10-year yield which is below 4%, and the fact that it’s so low is a sign that there is HUGE demand for this debt at this yield.

Is there enough from QE taking Fed balance sheet from $1T to $9T to fund future deficits of $2T annually for a long time? How long?

Do we not sometime have to “save” to fund government future deficits?

Will the Fed start QE again and grow balance sheet again to fund future and current govt deficits?

How long will savers and investors continue to fund 10 year and longer Treasuries at 4%; and does that answer depend on inflation expectations?

Why is the market not taming and restricting the USGovernment from incurring these large deficits with higher rates now?

Wolf said: “The plunge in ON RRPs is largely a result of the Fed’s QT”

————————————

Could it be that the plunge in RRPs is the result of Money Market Funds buying short term T-Bills?

You’re twisting it around. When the Fed removes excess liquidity, it comes out of two places: reserves and ON RRPs (meaning the banking system and the nonbank financial system). Everything else follows.

Yep, I’m confused. I thought the RRP facility was to keep money markets from “breaking the buck.” To provide the money market funds liquidity and a return in order to avoid mass withdrawals from depositors. This, I thought allowed money market funds time to transition to higher yielding short term treasury bills and other instruments.

“To provide the money market funds liquidity and a return in order to avoid mass withdrawals from depositors.”

Just to make sure I understand this line or yours. ON RRPs do NOT provide liquidity; they TAKE liquidity from the money market funds and pay interest on it.

I have no idea what your problem is.

Wolf said: “When the Fed removes excess liquidity, it comes out of two places: reserves and ON RRPs (meaning the banking system and the nonbank financial system).”

Wolf said: “ON RRPs do NOT provide liquidity; they TAKE liquidity from the money market funds and pay interest on it.”

———————–

I thought liquidity was removed by the FED destroying the dollars that the FED receives from the parties that owe on the Treasuries and MBS that the FED owns.

“Removing” liquidity via RRPs seems rather temporary. Are RRPs really done to remove liquidity, or to give money market funds a safe haven to earn interest.

Please try to read what I said. I’m wasting my time here.