One of the big changes that came out of the chaos of the pandemic. And robots cost nearly the same anywhere.

By Wolf Richter for WOLF STREET.

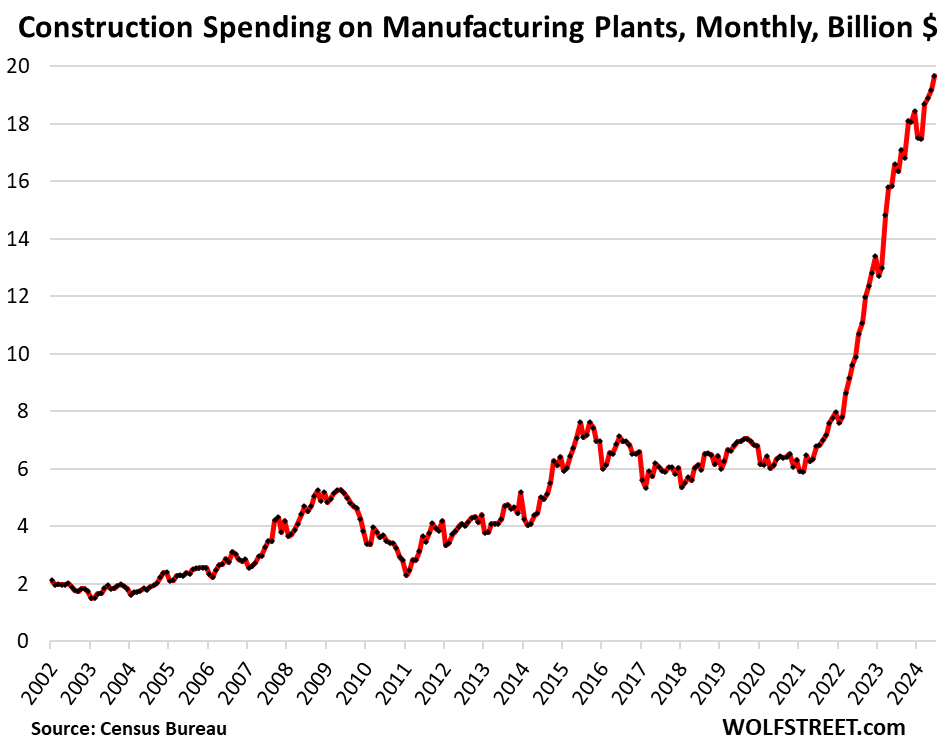

Companies invested a record $19.7 billion in June in the construction of manufacturing facilities, up by 18.6% from the already surging levels in June 2023, up by nearly 100% from June 2022, and up by 209% from June 2019, according to the Census Bureau today.

The investment totals here only cover the actual construction costs of the facilities, not the costs of the manufacturing equipment and installation that can dwarf the construction costs of the building. The total cost of a big chip plant might reach $20 billion, but the construction costs are the smallest part of it. So the total amounts invested in manufacturing plants, including the equipment and installation, are much higher. But here, the amounts only refer to the construction of the plants, and can be seen as a directional indicator of total investment in manufacturing.

In addition to the construction boom of semiconductor plants, a large number of other manufacturing plants have been announced, and continue to be announced.

The explosion in factory construction that started in the second half of 2021 was one of the changes that came out of the pandemic when America’s scary dependence on China became apparent in massive shortages of all kinds of goods, including semiconductor shortages, and unbelievable supply-chain and transportation chaos, that caused corporate America and policy makers to rethink the strategy of endless globalization.

The CHIPS Act, signed into law in August 2022, was part of the movement. While the first awards have been announced, there is lots of stuff left to do, including due diligence, and the cash hasn’t been disbursed yet. That’s still to come.

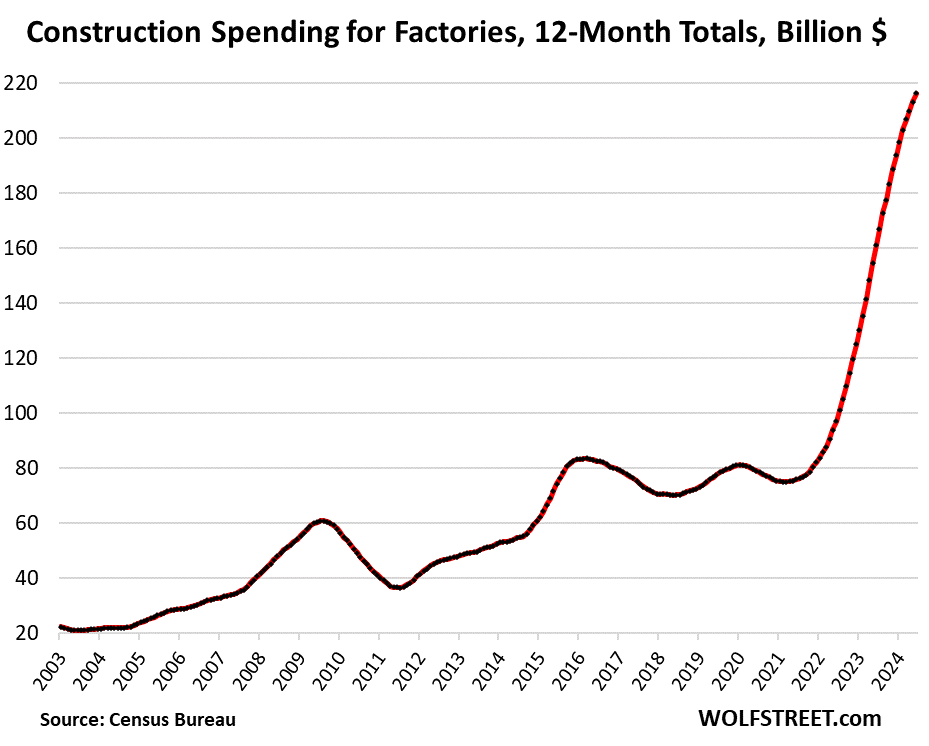

The 12-month total of investment in manufacturing plants jumped to $235.5 billion, up by 19% from the same period a year ago, up by 100% from two years ago, and up by 217% from the same period in 2019.

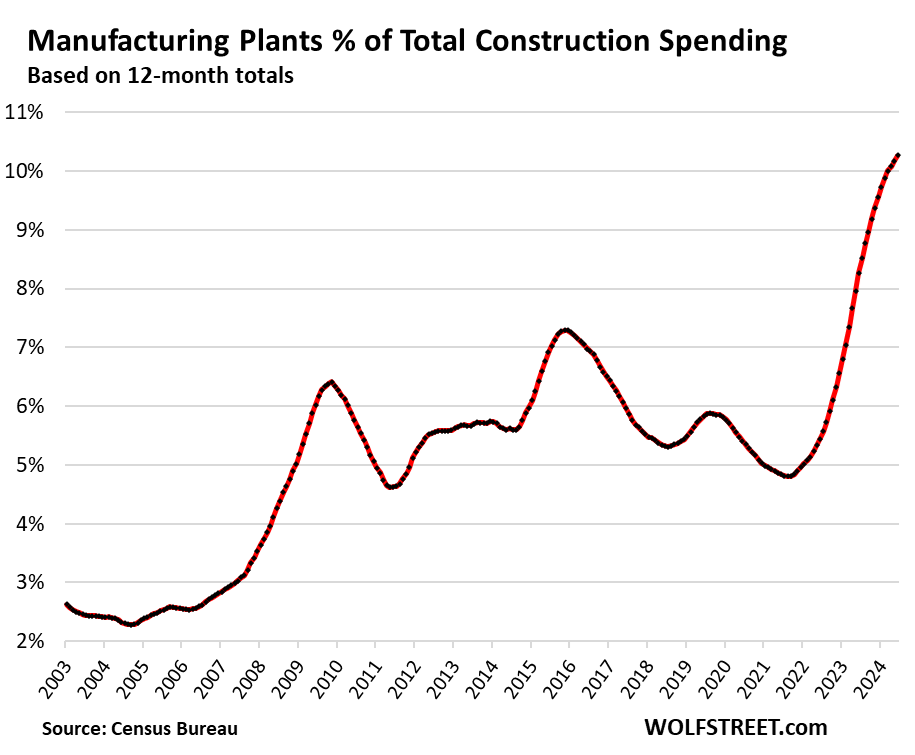

Construction spending on manufacturing facilities now accounts for over 10% of total construction spending in the US, residential and non-residential, from single-family houses to roads and power plants.

It’s all based on the principle that industrial robots cost the same in the US and China, that manual labor is a much smaller cost component in modern automated manufacturing, and that transportation costs (which spiked during the pandemic) and loss of Intellectual Property (IP), which is a given in China, and other risks have to be added to cost equation.

In addition, the increasingly complicated and stressed relationship between the US and China has exposed for all to see that the reckless dependence by US companies on production in China is a fundamental risk, not only for the companies, but also for national security.

No one is going to build a factory in the US to make low-value products, such as T-shirts. It’s all focused on complicated high-value products, such as motor vehicles, chips, electrical and electronic products, heavy components and equipment, etc.

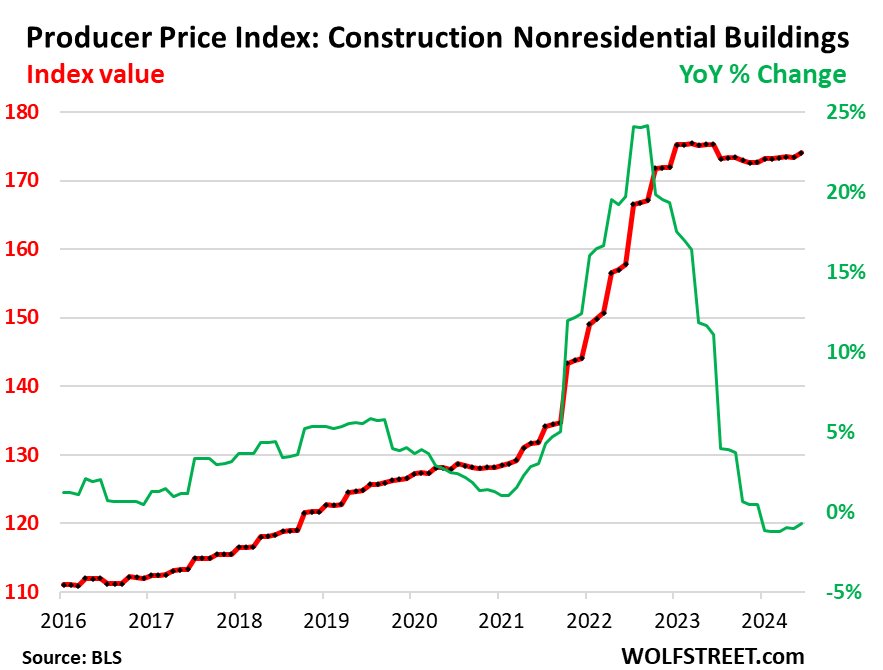

Inflation in construction has abated.

The Producer Price Index for construction costs of nonresidential buildings, after blowing out in mid-2021 through 2022, started plateauing in early 2023 and has remained roughly unchanged since then (red in the chart below).

On a year-over-year basis, the PPI for nonresidential construction has been flat to slightly negative since late 2023, after having spiked by as much as 24% in mid-2022 (green).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

They aren’t calling warehouses ‘factories’ now are they?

That’s about the only new construction I tend to see.

No, warehouse construction is in a separate category (“commercial” which includes retail, wholesale, warehouses, farm buildings, and other commercial). Warehouse construction was red hot over the past few years, so it has backed off some now.

Fascinating. I would love to see that information as well presented in chart form for the last 20 years (how far does data go back?).

As I said, the data is for “commercial” — not just warehouses. It includes retail (malls), where construction has totally collapsed, as part of the Brick-and-Mortar Meltdown and zombie malls. So the “commercial” chart shows this mix where retail construction, which used to dominate this sector, has totally collapsed. It’s unfortunate that the data cannot be broken out further.

We know from reporting from the CRE side (where warehouses are called “industrial”) that warehouse construction and leasing, including by Amazon, was white-hot during the pandemic and it’s still by far the best performing sector of CRE.

2017 TCJA Tax cuts and Jobs Act. Corporations repatriated money starting in 2018. Once they started putting it to work we get this…new factories and new jobs. Trumpanomics works.

You go raise an interesting point.

My first job out of engineering school was for a design-build firm specializing in tilt-up industrial construction.

90% of the job before the end-user’s specialized equipment came into play was exactly the same.

In fact we converted or built-out many speculative or otherwise vacant warehouses into manufacturing facilities.

I can see how the data could be muddled.

There is some small-scale production and fabrication in converted warehouse space, sure. But any major manufacturing plant is purpose built for manufacturing.

1:04 PM 8/1/2024

Dow 40,347.38 -495.41 -1.21%

S&P 500 5,446.62 -75.68 -1.37%

Nasdaq 17,194.15 -405.25 -2.30%

VIX 18.51 2.15 13.14%

Gold 2,487.30 14.30 0.58%

Oil 76.99 -0.92 -1.18%

All the office towers were a sigh to behold not to far back, once proud and manicured. A horrible fate could await these new mc’builds, but that’s for down the road, now it’s time to cheer on our good fortunes.

We’re not dogs that make t-shirts, we make complicated high value products.

But we also make millions of drugged up drunken street creepers…just as a side note.

Maybe get them to make the T-shirts? Do you think they would?

Data centers?

No

Look people, manufacturing is manufacturing. It’s not storage of stuff or housing servers connected to the internet.

A factory is that magical place in China where products are conjured into existence after being ordered using software run by data centers in the USA, and later stored in warehouses until wholesale delivery. I can see the reason for confusion.

Seriously though, I almost fell out of my chair when Wolf had to explain (twice) what a factory is.

Seriously though, I almost fell out of my chair when Wolf had to explain (twice) what a factory is.

Well, it’s understandable… we haven’t had any for so long.

The funny thing is in colonial times the term factory originated (I think from a Portuguese term) and was closer to what we think of as a warehouse. Kinda of a cross between a warehouse and trading post.

Boeing started in a barn, story goes.

The faster the US can reshore (to some significant extent) the better…

US Imports from China –

1985 – $4 billion

1990 – $15

1995 – $45

2000 – $100

2005 – $243

2010 – $365

2015 – $483

2018 – $539 (peak)

2020 – $433

2022 – $536

2023 – $427

I guarantee you there are very, very few US-based production related metrics (GDP, employment, etc) that come anywhere remotely near the growth rates of Chinese imports into the US from 1985 to 2018.

Mortgaging US assets in order to actually pay for 40 years of ever more massive trade deficits turned out to be a pretty moronic idea in practice, long immunized to empirical reality.

Those “freed” US industrial workers didn’t become brain surgeons – they became barristas.

(They could have become home builders…but that is another fiasco).

International trade makes a lot of sense (nobody is in favor of getting extorted by politically insulated US producers) but there had better be a lot more of a godd*mn plan to actually adapt, relative to the 40 years of leadersh*t actually demonstrated in practice.

The US imports more from Mexico than China.

C’mon cas,,, anyone with eyes can see who put in their pockets the billions of dollars of ”campaign contributions,” etc., as well as profits from sales, that not only enabled the incredible transfer of manufacturing from USA to other countries, but empowered it.

While I still own and use top quality tools purchased in the 1980s and earlier ”Made in USA” ,,, most of the same brands — though not all — have been made much cheaply elsewhere and sold for the same or more money to profit those same folks.

Time and enough to bring it home and put our working folx back to work making the same quality.

What jobs are created in this new manufacturing will be much fewer than before ie automation ie robots etc. And for those jobs that are not highly skilled the pay will be much lower than they used to be unless the unions in this country make a major comeback.

The chase for corporate profit isn’t the only cause for our massive trade imbalance. Our manufacturing base was gutted by CARB and other well intentioned environmental regulations. It started in the Los Angeles basin in the 1970s. Maybe if the Supreme Court hadn’t waited 40 years to address this issue, we might still have manufacturing capacity here.

Regardless, China was smart enough to buy our idled capital for pennies on the dollar. They didn’t have to learn anything about our economy or consumer behavior to be successful either, they just sold us the same products we were already buying.

Elevated logistics costs and lead times go a long way towards reducing labor rate advantages. This is where manufacturing profits are being lost now and a big driver for localizing manufacturing regionally around the world. This isn’t just a US issue.

Tariffs don’t fix anything either. Tariffs helped raise prices for domestic manufacturers temporarily but that’s all. They didn’t make the US more competitive or change the legal operating environment. The tariffs were good for Mexico’s economy though. Many Chinese companies are buying and building factories in Mexico to avoid them.

Unless the legal/environmental barriers are addressed, the waves of factory investments will be short lived and our trade imbalance will shift from China to Mexico.

TJ – …reckon then it’s just down to the half-assed, but profitable, ‘solution’ of the export of industrial capital to those nations that lack ‘good intentions’ and are willing (at least for awhile) to profitably-poison THEIR people, rather than the exporters seriously tackling those difficult, difficult issues at home?

may we all find a better day.

No. If anything, CARB exposed all the bad management decisions made by the Big 3.

Volvo (BTW, a small independent automaker who was crazy enough to put seat belts in cars before it was mandated) integrated the first O2 sensors in their 240’s around 1976 (I think) with Bosch fuel injection and they were magic compared to anything Detroit was designing.

The corporate overlords at GM said it was impossible to meet emissions standards, which was probably true for a company that wanted to keep making the same crap well past the time it made any technical sense. (have you every tried to work on an 86 Monte with a Qjet?)

86 Monte? Sure have. Much easier than my 15′ VW.

northern-historical note (apologies, Wolf)-Ford offered seatbelts as an option in the mid/late-’50’s (well-before the advent of youth soccer in the U.S.) to an overwhelming yawn from the buying public…(‘SIGNAL 30’, one of the goriest driver’s-ed films of the times not seeming to have much of an impact (sorry) on traffic-fatality rates, either (although I remember my old man being what is now termed an ‘early adopter’, installing color-matched aftermarket belts in our ’62 Country Sedan, and making sure we acquired the buckle-up habit…)).

may we all find a better day.

Before there was china there was Germany then Japan that was going to dominate the world. Business follows the cheapest cost to manufacturer. Remember the US was the supplier to the world because of the lowest cost. The shifting cost of production brings a coming and going of different industries. The reshoreing of chips and battery and auto is a result of costs and government incentives

There has also been a large increase in imports from ASEAN and India in the last decade or so that has taken some of that business out of China. For better or worse.

The US is getting some of its muscle back.

The cost…..higher costs relative to China and all those other inflation sinks…..which translates into higher inflation ongoing in the US.

Good for the country.

Good for workers.

Good for Government revenue.

Good for the trade deficit and government deficit.

Good for some corporation profits…..bad for others.

Bad for folks on fixed income.

As for warehouses…..if anybody wants to see new warehouses visit the east side of Indianapolis. Indy is an important transport hub for the country. New huge warehouses that go for as far as you can see. Hundreds of them…..each one acres in size.

Somebody wants the dollar to tank…….and yellow rocks smell it. New high.

Check out the I81corridor in pa. It is 12hr to 1/3 of the US pop.

The guys and gals in the unemployment offices who are laid off from manufacturing in the construction equipment, marine, and RV industries will be happy to hear this. If anyone is looking for a new boat or PWC, prices are dropping by the week. I plan on buying both this Fall with cash. And each week, more and more Powersports dealers aren’t charging bogus freight and setup charges aka ADP.

They’re coming off a huge gigantic ginormous boom in consumer goods during the pandemic. A lot of manufacturers are. The pandemic boom in consumer goods, along with the huge price spikes, was historic. But that has been over for two years. Prices have fallen. Inventory piled up. Deals are to be had.

New warehousing and manufacturing here in Reno Nv. is ramping up visually, but I have no stats. Reno has been the major distribution for avoiding the warehouse inventory tax across the line in CommieFornia.

The only construction to put that to pale is HUGE multi family apartments.

Cool– do you have any insights into Las Vegas metro and what is happening down there?

The place that has a modest cost advantage in using robots is Japan. They make most of the world’s industrial robot arms and can supply them to manufacturers with a much shorter supply and service chain.

If you want a robot system here in the US using FANUC robot arms you have to go to an integrator who packages up and assembles the arms and other stuff needed. In Japan the small size of the country allows you to buy an entire system straight from the factory.

I feel like this may be a good thing. More people can find jobs and potentially more products will be manufactured at affordable price thanks to these investments. But I wonder whether the demand will catch up with the increasing supply, unless fed panics again and prints another round of several trillions.

Demand is already there. It’s now getting satisfied by imports. Putting this manufacturing capacity into the US will shift sales from foreign locations to US manufacturers. It will reduce imports, or at least slow the growth of imports. That’s all it is.

I agree, it looks like good news is good news! Unless it’s an inflation driven over-expansion of the production capacity. Might be, short term, but long term I think any reshoring is a good thing.

Curious to know who’s spending the billions to build these manufacturing facilities?

So the Chinese and other foreign actors decided it was more profitable to build their plants here, since the robot works for cheap and not much labor needed…eliminate the shipping.

Just looking at the automotive sector in the US, how many are owned and ran and profited by Americans?

I have a feeling we are being eaten alive, our future new president of the US has just been born somewhere in china or India.

I’m way of base probably but over the last 40-50 years the US seems to be slipping in most every category?

Thanks wolf…

1. Tesla has built the biggest auto plants in the US of anyone in years. Tesla is a US company.

2. It doesn’t matter that much whether it’s a US brand or a German brand or a Japanese brand that builds an assembly plant in the US. The results for the US are about the same.

True it’s is the same, but with a 🤐

Not sure on this Wolf. Tesla is Elon Musk, who is South African, brought a fresh brain to an otherwise stale and decaying US car business? An aside. The main point is that mere assembly of vehicles is mostly only providing employment to manual labour. Design and management stay at home, with profits and dividends of all types repatriated to Germany or Japan. This is directly analogous to Apple, designed in USA, earning 40% profit doing this, and built in China, who bearly scraped 10 %, as was loudly boasted by Steve Jobs. No good news here at all. Building ‘factories’ to work in is useful to local contractors but is once off profit only. I am not denigrating USA, a very much better economy than a slowingly decaying socialist Germany and a rapidly dying Japanese one, due to its ageing population,but it must keep in charge by continuing to educate clever and highly skilled people. Your trade deficit alarms everyone.

“…our future new president of the US has just been born somewhere in china or India.”

More ‘burfer’ shit. Wasn’t your MAGA god born in a manger? That makes him a ‘furin-er’

Mr. Wolf writes: “The total cost of a big chip plant might reach $20 billion.”

CNBC wites: “Intel awarded up to $8.5 billion in CHIPS Act grants, with billions more in loans available

Published Wed, Mar 20 2024 5:00 AM EDT

Updated Wed, Mar 20 2024 4:32 PM EDT”

Spending is spending, so the effect on the economy is the same, but the grant will just be thrown on the deficit mountain to fuel some more inflation. However, more interesting is this Wolf report headline comment about “big corporate rethink;” if someone was to give me $8.5 billion in special interest corporate welfare I would rethink our Government & Federal Reserve (engine & transmission) system.

Why do you google around to get this stuff about Intel. You could have just used my article from March 20:

“Intel to Get $23 Billion in Government Grants & Loans Plus $25 Billion Investment Tax Credits, to Invest $100 Billion in the US, after Wasting $94 Billion on Share Buybacks in 15 Years”

The government is expected to award Intel $23 billion in subsidies, plus Intel expects to claim another $25 billion in Investment Tax Credits in order to invest $100 billion over five years in chip making capacity, research and development, and advanced packaging projects in the US, according to a slew of announcements today.

But since 2008, Intel has incinerated $94 billion in cash to buy back its own shares to prop up the price of its shares. Intel stopped doing share buybacks in 2021 under the new CEO Pat Gelsinger, as he steered the company back to investing its cash – and now taxpayer cash – into the future of the company in order to not be totally left behind.

If Intel hadn’t wasted $94 billion in cash on share buybacks to enrich its shareholders, it would now have the $94 billion in cash for its $100 billion investment, or it could have invested the $94 billion years ago in US-based research, development, and manufacturing plants, and it wouldn’t be so far behind now.

Yeah. Intel is toast.

The recent layoffs are just the most recent hit.

I don’t see how Intel is toast, long term. The government has anointed them as a winner.

Re: “ Why do you google around to get this stuff about Intel. You could have just used my article from March 20”

The Google algorithms are a clear example of why ai is ridiculously overrated and useless — as these ai search bugs scrape data and search, they miss vast amounts of information and then pretend to assume they have relevance.

It’s actually entertaining to think Wolfstreet is a superior financial darabase compared to the mighty Google Goliath!

I seriously think I have to alter my approach to research — and actually search Wolf’s RTGDFA first, before exploring Google stupidity.

Definitely time to re-watch:

Dr. Strangelove or: How I Learned to Stop Worrying and Love the Bomb

Searching Mr. Wolf’s work first is good advice and noted.

Manufacturing in the Anglosphere has been quietly bouncing back for a decade or more. The UK has seen a relative upswing in manufacturing since about 2010, and few noticed. Now the US is really rolling, in the 2020s.

Great to see the folly of the past 40 years of gifting Western factories and IP to communist China is now (at least in theory) being rolled back.

Trading with communist un-democratic China today is no different to trading with the communist un-democratic USSR of yesterday — such activity in the future 2030s should become unthinkable.

The USSR couldn’t supply the USSR with consumer goods, much like Russia today.

Yes, but today, Russia can get all it’s consumer goods from China. There’s a good article in the magazine Foreign Policy about winners from US-China Decoupling. As Wolf’s article suggests, it’s good for America and it’s probably good for China and the wider world as well.

It isn’t being “rolled-back”.

Manufacturing isn’t leaving China. The tariffs simply resulted Chinese manufacturers shipping primary and intermediate components to other countries in the Global South where they are assembled into finished goods for shipment to the USA. Thus, they skirt the tariffs.

There was a lot of hype about reshoring beginning around 2010. By 2015 this had been thoroughly debunked.

There’s been a lot of hype about reshoing since early 2022. I’m confident that this will eventually be debunked also.

The “Rehsoring Initiative” like to trumpet figures like “287,000 jobs reshored in 2023”. But once you delve into their report and methodology – there isn’t lots of reason to be optimistic about reshoring and that jobs are returning from China.

https://reshorenow.org/content/pdf/Reshoring_Initiative_2023_Annual_Report.pdf

First of all, the “reshored jobs” figure actually included jobs added by FDI. That’s not reshoring.

Second, only about 6.5% of the jobs concerned China. And some % of those jobs were FDI by Chinese companies – not reshored jobs.

We did a much better job attracting jobs from South Korea, Germany, UK, Japan, et. al. Again, what % of that was reshoring vs. FDI.

So the reshoring argument is paper-thin.

We haven’t got anywhere near the infrastructure, workforce, regulatory regime, or cheap energy to compete with China. The last item is worthy of mention since we are busy shutting down the last vestiges of our aluminum smelting industry to placate Bitcoin miners and data centers.

It’s hard to be optimistic about the re-industrialization prospects when there’s no evidence that policymakers actually understand the problem.

“Reshoring” is a misnomer and a misunderstanding. It’s not that existing manufacturing jobs overseas are shipped to the US. It’s that NEW manufacturing capacity is built in the US to produce high-value products in the US, creating NEW jobs in the US, so that those new products won’t be imported, and therefore preventing those NEW jobs from being created in other countries, but in the US. That’s how that works.

WSJ: INTEL laying off 15,000…

Intel has been in shambles for years, done in by two decades of financial engineering.

Will the demand be there when all these new builds are ready? The US has spent billions to increase chip production at home, but Intel lost $1.6 billion last quarter and plans to lay off 18,000. I guess the government can buy Intel’s chips and store them as a strategic reserve/museum.

1. Intel has been in shambles for years, done in by two decades of financial engineering.

2. The thing is to make the chips in the US, and not import them. This US capacity takes production away from overseas producers – that’s the purpose. It doesn’t matter what global demand is, this is reducing US imports of chips.

I hope we’re doing a better job with build quality when constructing factories as we are with houses. I’ve been on a lot of big jobs even and there are non-legals even on those, not that the build quality is garbage just because of them. Build quality is bad starting from the top down, from materials, contractors, project managers, inspectors, etc. I worked on a prison that was even built like crapola. Lot’s of guards were attacked once it was put into service. It was expensive and built cheap, essentially tilt-up concrete walled warehouse buildings with pre-fab cells. Only cost over a billion dollars. Oops, now some people might know what state that was in. Major corruption. White collar criminal capital of the US.

Honestly, one of the craziest charts I’ve seen in years. Genuinely impressive stuff. America is roaring back!

This is a good news story, and one that is long overdue.

I wouldn’t count my chickens just yet.

A lot of this stuff is tied up in the IRA or the overall Green Transition. If 45 becomes 47 – a lot of the needed incentives could go away.

Also not sure if South Korea and Taiwan will want to keep building fabs if 47 decides that our armed forces should be wielded as a protection racket.

And it’s really hard to be bullish on re-industrialization if stuff like Bitcoin mining and AI data centers are drive the cost of electricity to the moon.

I enjoy a good train wreck. The following article gives a history of the many bad management decisions that damaged Intel.

Intel manufacturers on three continents.

Its home page shows “Global Manufacturing at Intel”

It is expanding capacity in several foreign sites. There is 33 Billion Euros in Germany and 8.5 Billion in Poland. Plans for expansion have been reduced or dropped for Vietnam and Israel.

During a visit to Vietnam in Sept. 2023, Biden promised support for the chip industry in Vietnam. I need to look deeper into the details. US companies to benefit apparently do not include Intel.

All that manufacturing requires real inputs! More justification for adding to energy and commodity positions.

With the blowout in construction you would think the materials sector would be performing better

Weak internal demand in China is weighing on things like steel & aluminum prices.

Also (my own theory here) I think the factory spending data is skewed towards the building of a relatively-small number of facilities of great sophistication and cost.

There’s likely at least some considerable distortion in this data arising from the CHIPS act.

First reason: we can’t go a month without hearing about one of these projects incurring a delay or facing increased costs.

Second reason: This is much, much more subtle.

It’s true that the construction spending tracked by the Census doesn’t include expenditures for the direct capital goods required for chip-making (e.g. EUV machines)

But there’s a catch.

The spending DOES include items like HVAC, water filtration, etc. The systems in these categories in semiconductor facilities are of eye-popping sophistication and cost. And there is some fuzziness/crossover as to whether some of these components aren’t really capital goods in disguise. For example, (and I have confirmed this with a friend who works for Wolfspeed) – the enormously-complex vacuum systems that support semiconductor manufacturing ARE included in the factory construction costs because they are lumped in the larger HVAC category. This seems inappropriate.

Yes, I acknowledge that it takes time for a factory to be completed and hire workers – but manufacturing employment (as collected by the BLS) has been flat-ish for more than a year. And the mostly-lousy-looking ISM manufacturing reports for the last 18 months or so don’t suggest anything like a major re-industrialization project is under way in the USA.

It will take somebody smarter than myself to fully-explain the disconnect between factory-spending data and the health of the US manufacturing sector as a whole – but the disconnect seems large and growing.

Wolf, Despite all these new factories are we producing less than 2000. Or are we producing goods at the highest ever. Where can we get that data. Could you please share

new battery factories are common hereabouts (OH), since they’re retooling the old auto plants for EV assembly…

i imagine a lot of it is Biden’s green new deal, windmill & solar components, machinery to build them, et al…IRA mandates domestic components, union jobs, et al

but what will be the cradle to grave carbon bootprint of all those factories? more than the CO2 they curtail, i suspect…

i was curious, so i googled battery factories….from a couple weeks ago:

Tracking the EV battery factory construction boom across North America

https://techcrunch.com/2024/07/20/tracking-the-ev-battery-factory-construction-boom-across-north-america/

– “In 2019, just two battery factories were operating in the United States with another two under construction. Today there are about 34 battery factories either planned, under construction or operational in the country.”

then just now, a friend to whom i sent this article, responded with this:

https://home.treasury.gov/news/featured-stories/unpacking-the-boom-in-us-construction-of-manufacturing-facilities

” the Infrastructure Investment and Jobs Act (IIJA), Inflation Reduction Act (IRA), and CHIPS Act each provided direct funding and tax incentives for public and private manufacturing construction. “

The batteries are protected but the solvents and electrolytes are not. They just pour across the border business as usual.