It was obviously “unexpected.” But the Bank of Canada has been leery of this sort of mess showing up.

By Wolf Richter for WOLF STREET.

When the Bank of Canada cut its policy rates by 25 basis points earlier in June, it based that cut on the inflation rates that had cooled sharply, and it based further cuts on these trends continuing. But leery of just the sort of reversal inflation dished up today, BOC governor Tiff Macklem said at the press conference that future cuts would depend on two big Ifs: “If inflation continues to ease” (#1 IF), and if “our confidence that inflation is headed sustainably to the 2% target continues to increase” (#2 IF).

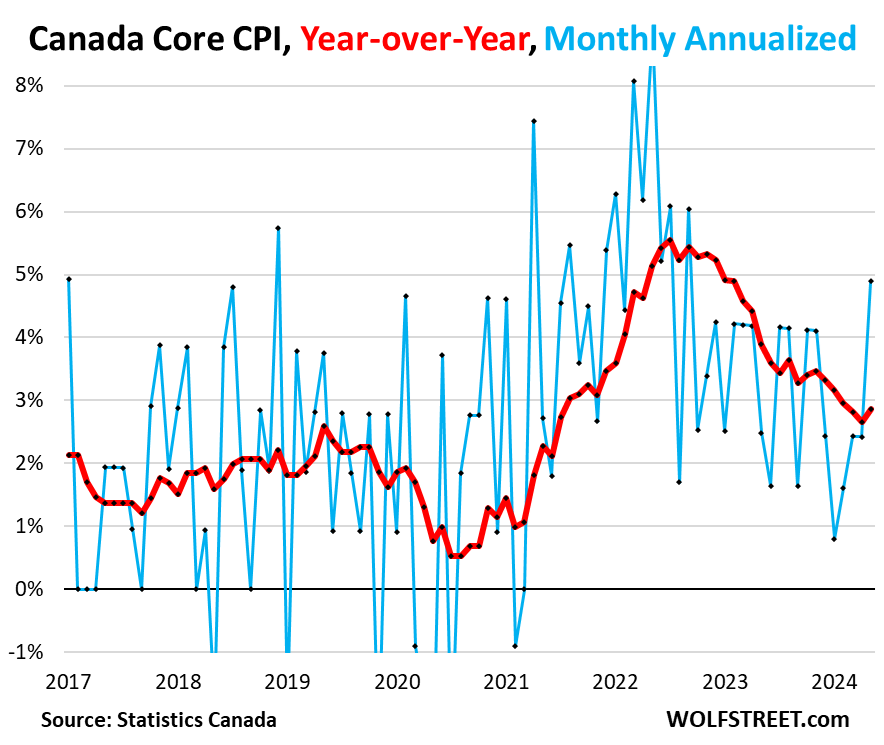

Core CPI – goods and services less food and energy – spiked by 4.9% month-to-month annualized in May from April, the hottest since September 2022 (blue), according to Statistic Canada today.

This spike caused the year-over-year Core CPI to accelerate to 2.9% (red). It has now been stuck at this just-below-3% level for the fourth month in a row.

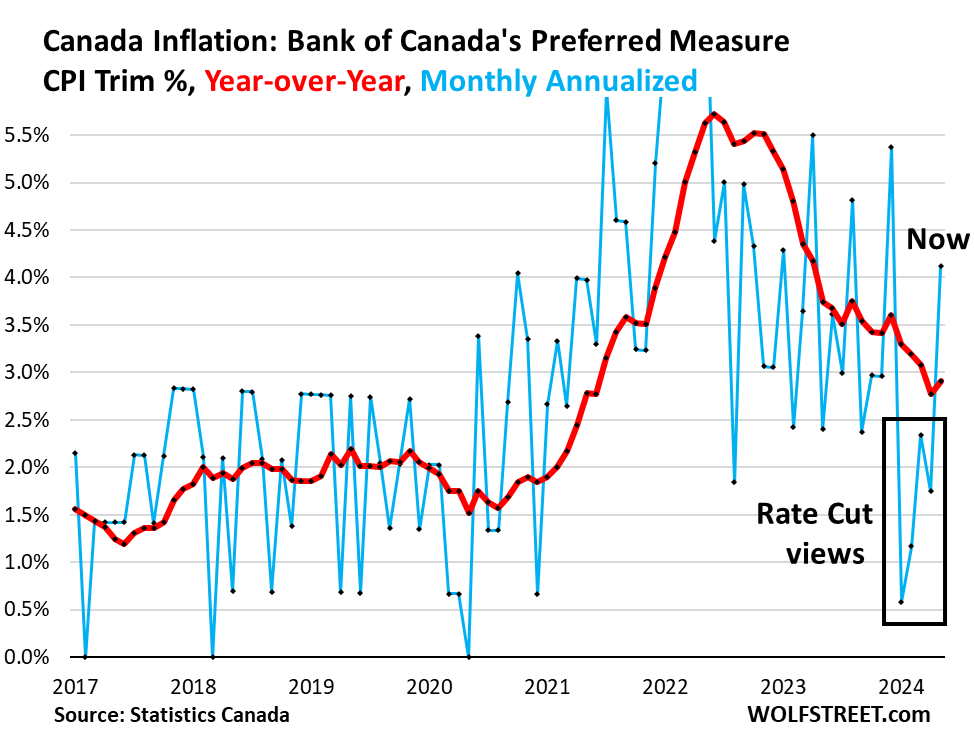

BOC’s preferred measures of underlying inflation accelerated.

The BoC’s two preferred inflation measuring sticks for its monetary policy decisions – “CPI trim” and “CPI median” – both re-accelerated sharply month-to-month. This caused the 12-month readings to accelerate for the first time after a series of declines, which was “unexpected.”

CPI trim jumped month-to-month by 4.1% annualized, a big acceleration and the hottest since December, and the third acceleration in four months (blue).

Year-over-year, CPI trim accelerated to 2.9%, the first acceleration after falling for three months in a row (red).

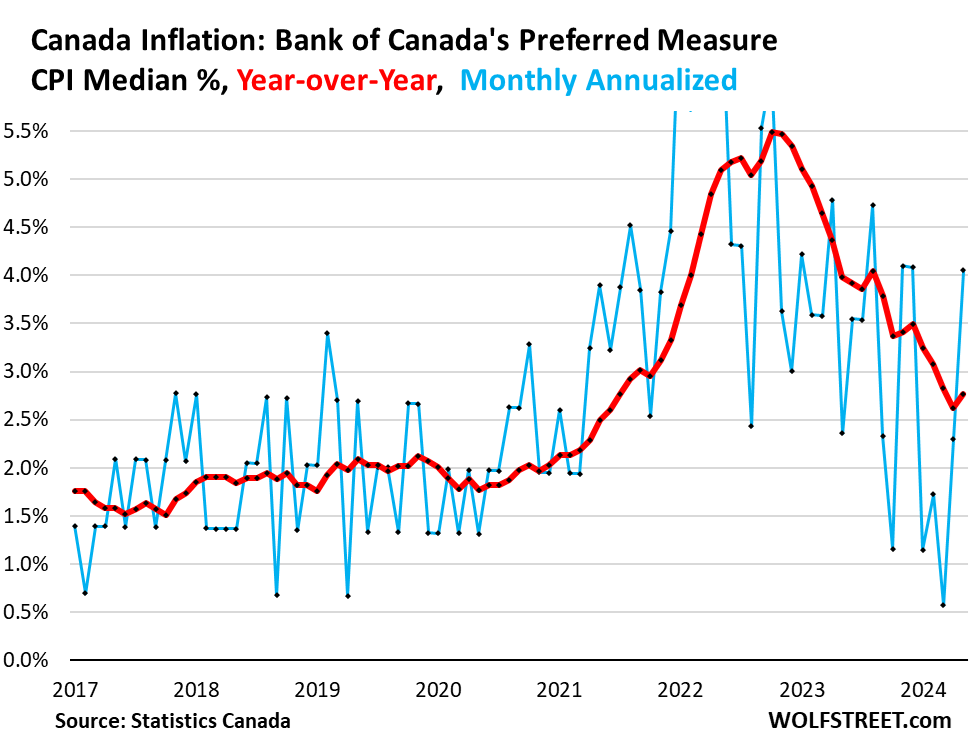

CPI median jumped month-to-month by 4.1% annualized, the most since December, and the second month in a row of acceleration. Year-over-year, CPI median accelerated to 2.8% (red).

“Inflation had not said its last word,” is how analysts of Economics and Strategy at the National Bank of Canada eloquently titled their inflation report today. They too were surprised.

This is the kind of surprise that the BOC – along with the Fed and the ECB – have been cautioning about. Inflation does this sort of thing. After it reaches the magnitude of the type it had reached in 2022, it doesn’t just go away quietly on its own.

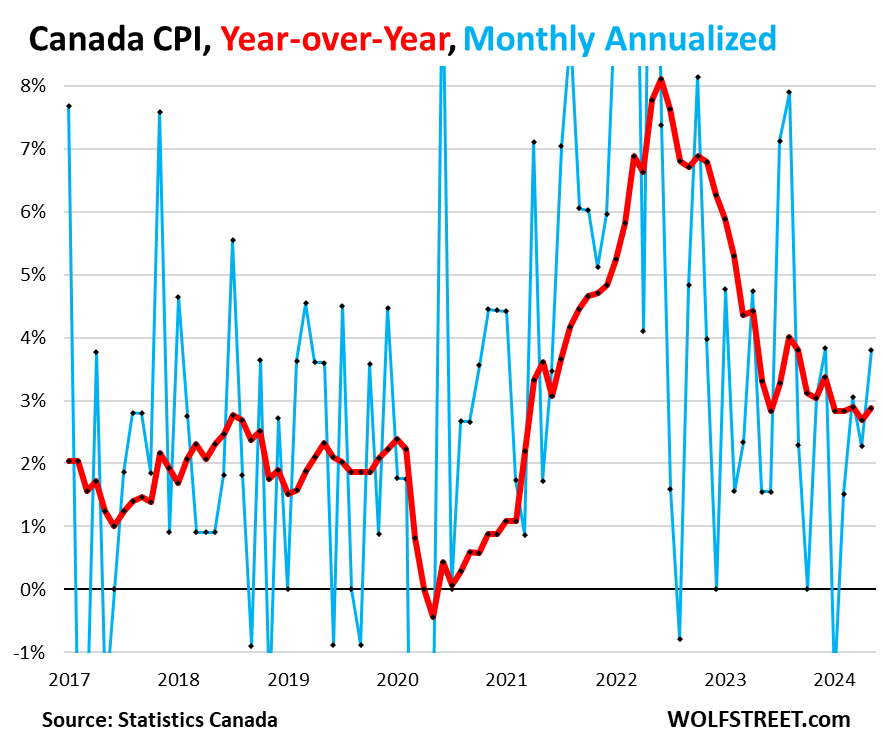

Overall CPI month-to-month accelerated to 3.8% annualized, the sharpest increase since December.

Year-over-year, CPI accelerated to 2.9%. It has now been stuck at this just-below-3% level for the fifth month in a row.

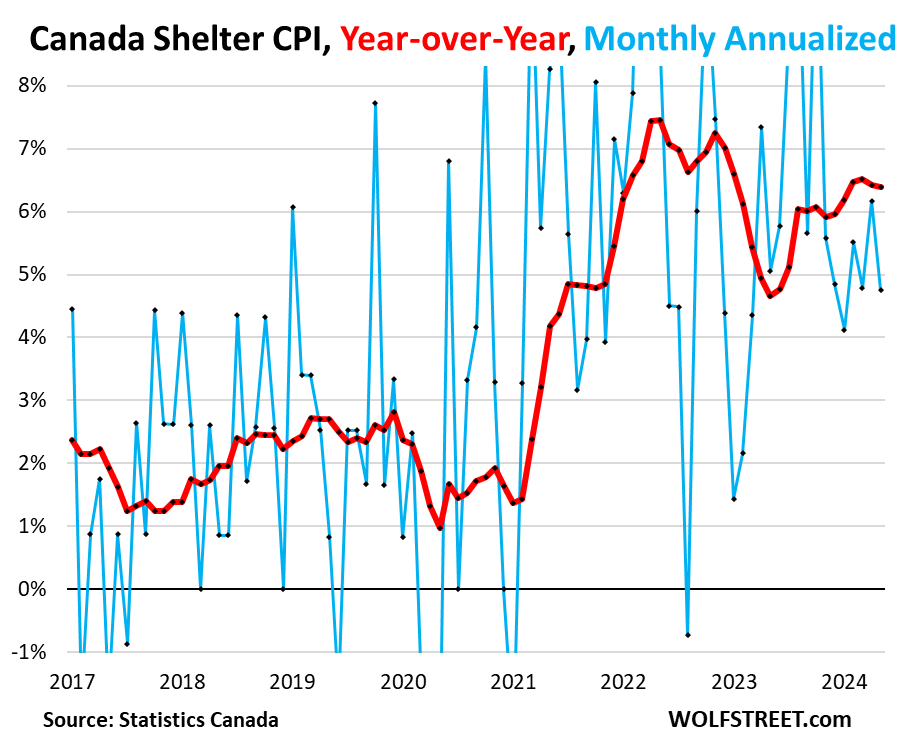

Housing. The CPI for “shelter,” which includes rents and a separate measure tracking the costs of homeownership (insurance, mortgage rates, maintenance, replacement costs, etc.) remained very high, though it was less hot than it had been last year.

The CPI for shelter jumped by 4.7% month-to-month annualized (blue), and by 6.4% year-over-year (red), now in the 6.4% to 6.5% range for the fourth month in a row, the highest since January 2023:

The other major categories, on a year-over-year basis (from inflation rate in the prior month):

- Transportation: +3.5% (from 3.1%)

- Food: +2.4% (from 2.3%)

- Energy: +4.1% (from 4.5%)

- Healthcare and personal care: +3.6% (from 3.0%)

- Alcoholic beverages and tobacco products: +3.2% (from 3.4%)

- Recreation, education, reading: +1.3% (from 1.0%)

- Household operations, furnishings, equipment: -1.5% (from -2.1%)

- Clothing and footwear: -3.0% (from -2.6%).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Nothing like cutting rates to stoke inflation. Even the mere rumor of possible rate cuts, months away, stokes speculative manias to new highs.

“Clothing and footwear: -3.0% (from 2.6%).”

What’s going on here? A single data point, but does it portend something bigger in the minds of the consumer?

I am seeing a resurgence in “recession watch” type articles (a sure way to push the next recession further out?). One I noticed brought up the “lipstick indicator” implying that is an early area of consumer cutback (and therefore distress.).

The global economy seems to be in a rolling state of weakness and strength. Card houses on windy days.

“What’s going on here” is a typo. The “-” in front of the 2.6% got swallowed by the keyboard shark. thanks.

Got it! Thanks!

While a rate cut in the US would be akin to a market on (an increased dose) of steroids.

Screw the market, pay attention to the real problem, Inflation still above target, and of a US 30% fiscal deficit!

Who is wagging the dog, US or Canada?

The fat lady has left the stage.

I don’t know why the dog bit me, he just started to growl then he bit me?

You were screwing with the dog again, weren’t you? that’s why he bit you. Leave the dog alone, he doesn’t like you.

cut the “well no f*cking $hit” meme right here

I mean duh.

Good thing they got out ahead and lowered rates 🙄. I’ll be stuck working out of town to dodge shelter costs forever me thinks, unless I can figure out how to make a meal out of sneakers since those are starting to come down.

Excuse the downer post but inflation is a b*tch for working people.

Ha. Good point; they gave themselves some room to raise :)

Sneakers for dinner ! Excellent idea .

Howdy Youngins. Better hope the FED meant it ” Higher for Longer”.

Get out your “Disco Duck” record and start dancing, because it is back to the 1970s.

You can say that when the FED rate is double digits; not before.

The #1 mandate is keep assets inflating.

the farcical game trying determining if the toilet paper the Canadian $ has become is two ply or three. Actually TP is more valuable, especially more so than the hundreds, as they are so slick and plasticy…… Wax paper would be better. And be careful with the huns in your wallet. Either fly all over or stick together, so suddenly you’re handing over a couple of brownies for that wee bag of groceries.

You young people do not remember the early 2000s when CAD$ was even lower value vs USD$.

On the flipside, it has also risen above par a few times in the past 50 years.

If you truly think your Canadian money is “toilet paper” just be patient and economic cycles will raise its relative value again in time.

Everything changed when Stephen Poloz got in. Interest rates in Canada were always higher than interest rates in America until Poloz got in and now the rates in Canada have been a lot lower ever since. This means the odds of the Canadian dollar ever going above 80 cents U.S. are slim and none. The Bank of Canada always sells Canadian dollars and buys U.S. dollars when or if the Canadian dollar ever hits 80 cents U.S. again.

You have to be kidding. relative value to what? The U.S.D ? That is scarcely compensation for the many decent people who worked hard for decades to save tokens now worth a fraction of when that labor commenced.

Currency depreciation is in essence a measure of government dishonesty and by extension a willingness of the citizens to believe the lies. The current government is certainly not unique, but is about as bad as it gets when it comes to fiscal integrity and that is reflected in the pitiful amount $100 buys. And that is not coming back.

Alot of my colleagues bought rental real estate just before the pandemic and thought it would easy money. They lost alot of money, close to $125,000 in rental income from tenants not paying. Now, they have 3 rental properties worth 15% less and that is not including the real estate commission, HST and other closing costs which can add up to another 7%+ loss to sell their properties. They laughed at me for putting the maximum in my RRSPs and TFSAs for years now. I guess good old saving works after all. I moved from India to Canada since 2010.

I put most of it since they matured in GICs at 5.25% to 5.5% GIC rates for 10 years plus compounding works out to 67% to 70% guaranteed compound interest by 2032 and tax free, TFSAs, tax deferred RRSPs, basically tax advantaged. Even this year I am finding 4.5% to 4.6% GIC rates in my RRSPs, TFSAs.

There is no major market in Canada where the real estate price index has dropped lower than pre-covid.

The only way your friends’ property is worth 15% less is if they paid 20+% over market when they purchased. That is a bit unbelievable, but if they also fail to collect $125,000 in rent, it matches a pattern of being incredibly inept at being a landlord.

In such a case it has nothing to do with inflation or bank rates, and everything to do simple incompetence.

Rogers bonds are paying or were paying today around 5.45 percent for 16 and a half years. The 6.11 out to August 25th 2040. The 6.56 Rogers bonds are callable a year early out to September 22nd 2041. About 5.3 percent for 10 years was the highest I saw at Motive Financial without going through a GIC broker. The CDIC limit is a joke and now the Manitoba credit unions pay less interest as some of them merged together.

Todays Australian CPI was a shocker at 11.1% higher than the last quarter, being 3.6% then -> today, expected 3.8% -> actual inflation 4%.

We are all being swallowed whole by Central Bankers who know they must raise to kill the beast but can’t because it will cause a recession.

Meanwhile the dirt hole diggers down under have three cities in the top 10 in the entire world that are Unaffordable to home buyer, even to very Very rich people.

Its coming !

Rates are like a full percentage point higher than Canada at the 5 and 10 year which leads anyone to believe the Bank of Canada just pulls figures out of the hat the first 4 months of this year. They must have stated inflation was higher so they didn’t have to shell out billions to try to protect the Canadian dollar after the unnecessary rate cut.

This was expected I belive, but the real question is: which is worst the fact that central banks are gambling the market’s credibility, which can result in significantly higher rates that the current level to regain that credibility, or the fact that if they don’t even try to lower rates a bit is certain that they will trigger the burst of one of the bubbles that are still inflating.

What is really looming in Canada are mortgage term limits. I read the other day that 70%+ of mortgages in Canada will have to be renewed in in the next couple of years. Standard rates are 3 and 5 year terms here as opposed to 30 year fixed in the US. For example, my kids have around 2% mortgages. Going from 2.5%ish to 7.5% could hurt a lot of people on the margins. This could also drive a lot of property underwater. Luckily, my kids are well enough able to handle the increase because they bought 15 years ago when prices were cheap. I would guess that a substantial price drop for sellers is looming.

My in laws re financed their mortgage….three years ago? I know they are worried about it. They live across a lane from a waterfront property for sale That place has had just one offer in the last 2 months, subject to inspection. The deal collapsed because the chimney needs some work. For waterfront on Vancouver Island, that was just an excuse to ditch. A masonry chimney can be relined with a stainless insert in about 1/2 day at the most. Same for a bricky to repoint the exposed surfaces.

Mind you, the RE boosters here are still saying prices and sales will be rising this year. Don’t see how that is possible?

I definitely favor the opinion that the federal government is directly and indirectly supporting condo prices (don’t want prices deflating) through letting regulated mortgage lenders conduct blanket appraisals and the CMHC MLI program (linked to the government’s CMB purchases). Trying to keep an overly inflated condo market from correcting too far downward. Doesn’t seem overly fair to the younger generations and new Canadians. If it’s the fear of condo development and construction coming to a grinding halt and/or lenders getting burnt – doesn’t make sense to expect consumers to pay outlandish prices. However, not much makes sense currently with Canada’s housing market.

Most people will not believe me but I actually became a millionaire by 40 by saving aggressively and working 3 jobs, 75 hour weeks for 11 years before I got married. After 29, I work 45 hour weeks. I got married when I was 29 and have 2 kids now. When I say millionaire I do not count my home in that figure. I have $1.3 million now at 43 and my wife never worked out of the household. RRSPs and TFSAs is the key as the taxes every year are not included in my working annual income. Compound interest and debt reduction is the key. Our mortgage is 60% paid off and I made sure used spousal RRSPs to split income. If you vision something hard enough it will be your future.

I was one of the few who made over a million dollars by age 18 at the racetracks and betting boxing matches down in Las Vegas. Ron Waples senior made me most of the money at the racetracks. He went every other week with his horses and his local drives and always went if a horse came in from another track. Always went or went meaning didn’t stiff the race and purposely ran out of the money. Went means went with the horse no stiff. This was back before the slot machines at the racetracks in Canada. Virtually all the races were stiff jobs and everything was rigged just the major stakes races and drivers who were broke that was about it. After the slot machines showed up I turned into the master of the maidens and went with breeding the looks of the horses the trainers and owners and endless decades of street smarts. I never in my lifetime thought I’d ever see honest races but the slot machines changed everything as they didn’t want to chase the public away or the horse players as some might play the slots.

The gov’t thought it could drum up some positives to keep the leadership in place next election. Finding any falsified info to promote irresponsible financial decisions is what the Canadian gov’t does now.

I fully expect them to move the goal posts and say that 2% is no longer the target and that under 4% is ideal. Our currency will follow Japan, for no good reason.

Like in the twilight zone flip a coin a million times and one time in a million it lands on its edge. We just saw that with the Bank of Canada actually stating the inflation rate went up. The bond market believes it when the CPI and the inflation rate increase but not decrease. Huge runup in the 5 year yield on the Government of Canada 5 year bond and 2 days later the yield is up a lot more. When the CPI and inflation rate fall the bond market comes back in mere days or less to where it was before the CPI and inflation report came out. A one way street for traders as you can’t lose if you bet interest rates will rise. At worst you only have to cover for one or two days and if the impossible happens and the CPI and inflation rate come out higher you hit mega bucks.