Not just housing, but also other core services. However, durable goods inflation is back to normal.

By Wolf Richter for WOLF STREET.

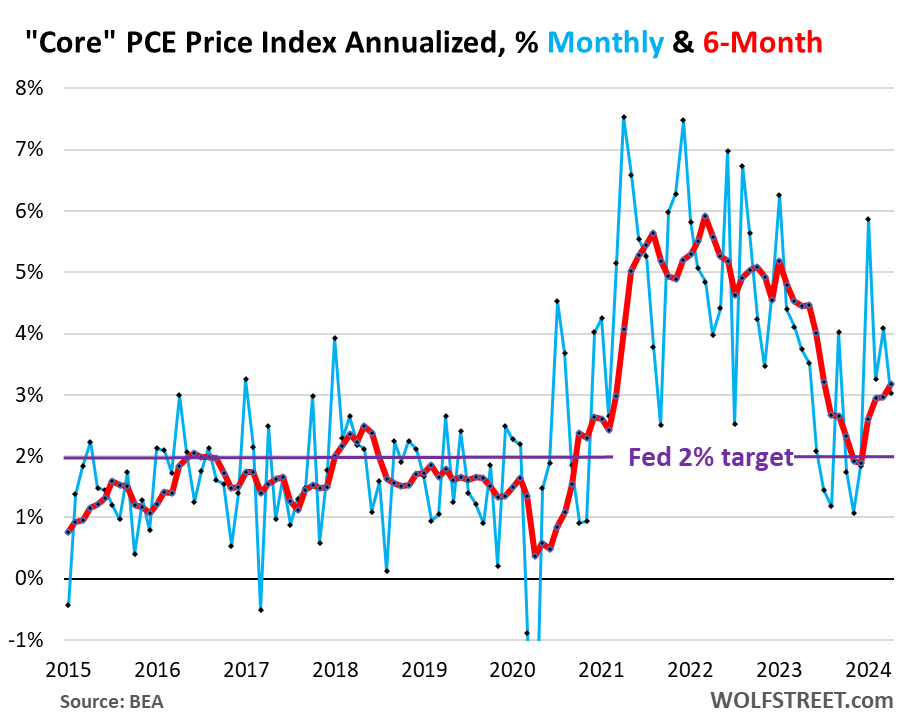

The Fed’s favored “core” PCE price index, which excludes the volatile components of food and energy, jumped by 3.0% annualized in April from March (not annualized, 0.249%), well above the Fed’s target of 2%, according to the Bureau of Economic Analysis today. But it was a smaller increase than in the prior three months, though far hotter than in late 2023 (blue in the chart).

The six-month annualized core PCE price index, which irons out most of the erratic monthly squiggles, and which Powell cites a lot, accelerated to 3.2%, the worst increase since July last year (red).

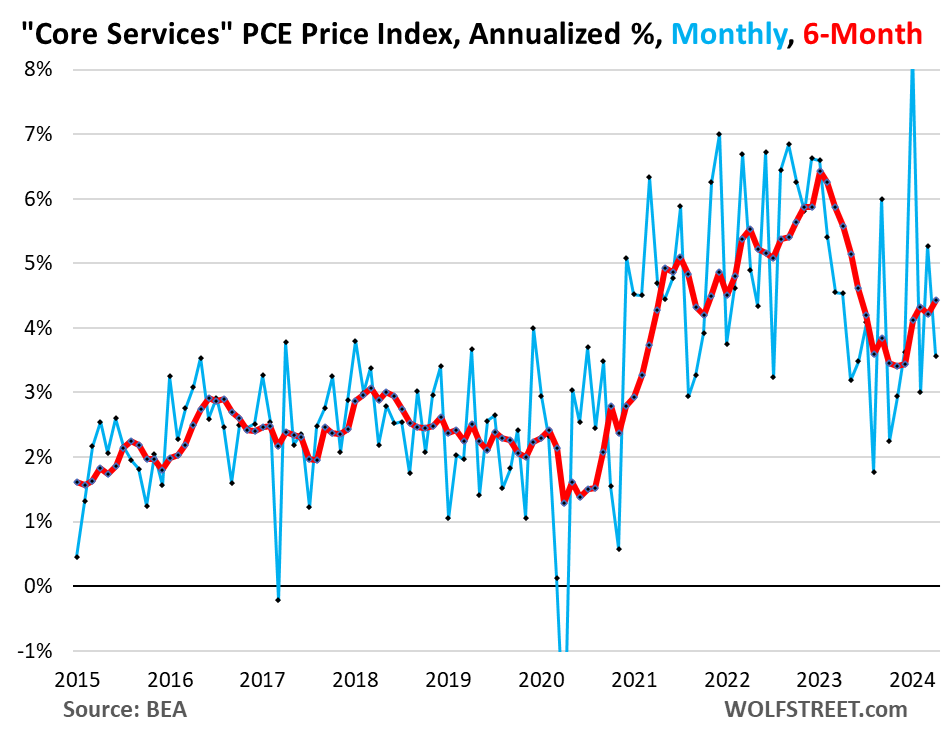

“Core Services” PCE price index, which excludes energy services, rose by 3.6% annualized in April from March (blue in the chart below).

The six-month core services PCE index jumped by 4.4% annualized, the worst increase since June last year.

Core services is where inflation has gotten entrenched, and it’s where the majority of consumer spending goes. It includes housing, healthcare, insurance, transportation services, communication services, entertainment, etc. Fed speakers have been pointing at core services incessantly.

In the month-to-month squiggles (blue), you can see how core services inflation had cooled from the peak in late 2022 (in the +7.0% range) to August 2023 (+1.8%), which had been the low point. But since then, it has re-accelerated in a disconcerting manner.

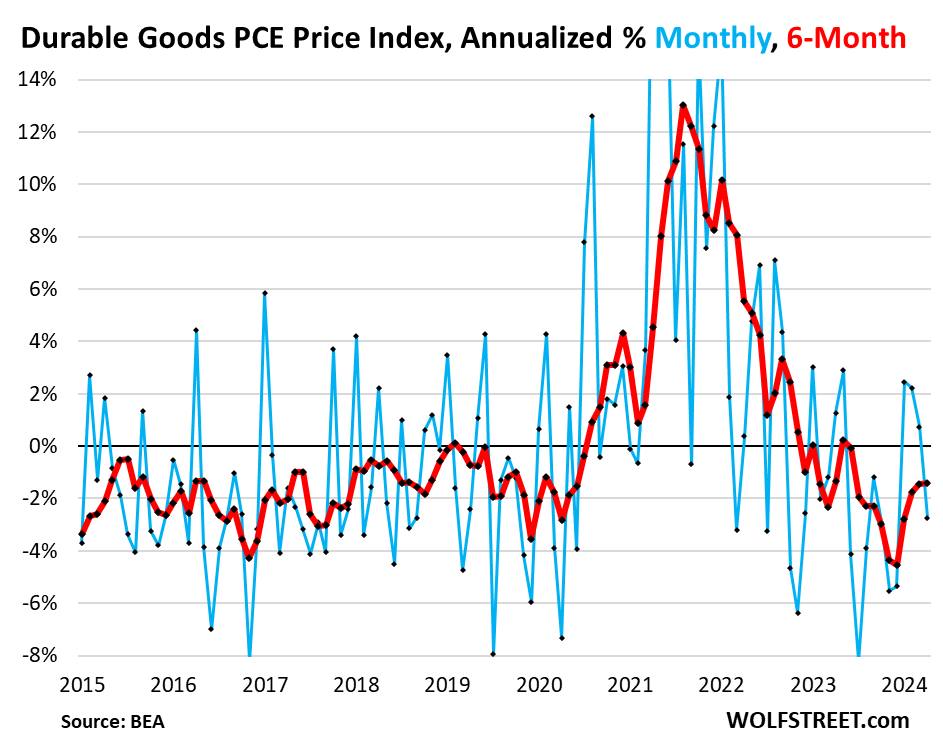

Durable goods inflation has vanished. The PCE price index for durable goods fell by 2.8% annualized in April from March (blue).

The six-month index fell by 1.4%, roughly the same as in the prior month (red). It tends to run in the slightly negative range during normal times amid manufacturing efficiencies and globalization. Durable goods include motor vehicles, appliances, electronics, furniture, etc.

So durable goods inflation is back to normal and in line with the Fed’s 2% target. The inflation problem is in services, as we’ve seen above.

Year-over-year…

The overall PCE price index, which includes food and energy, rose by 2.7% in April from a year ago, roughly the same increase as in March (blue in the chart below).

The “core” PCE price index rose by 2.8% in April from a year ago, roughly the same increase as in the prior two months (red). The Fed’s target for this metric is 2%.

The “core services” PCE price index rose by 3.94% in April from a year ago; it barely changed over the past five months. In December it had risen by 4.03%. As we’ve seen above, the six-month core services index has risen by over 4.2% over the past three months

Core services inflation in detail.

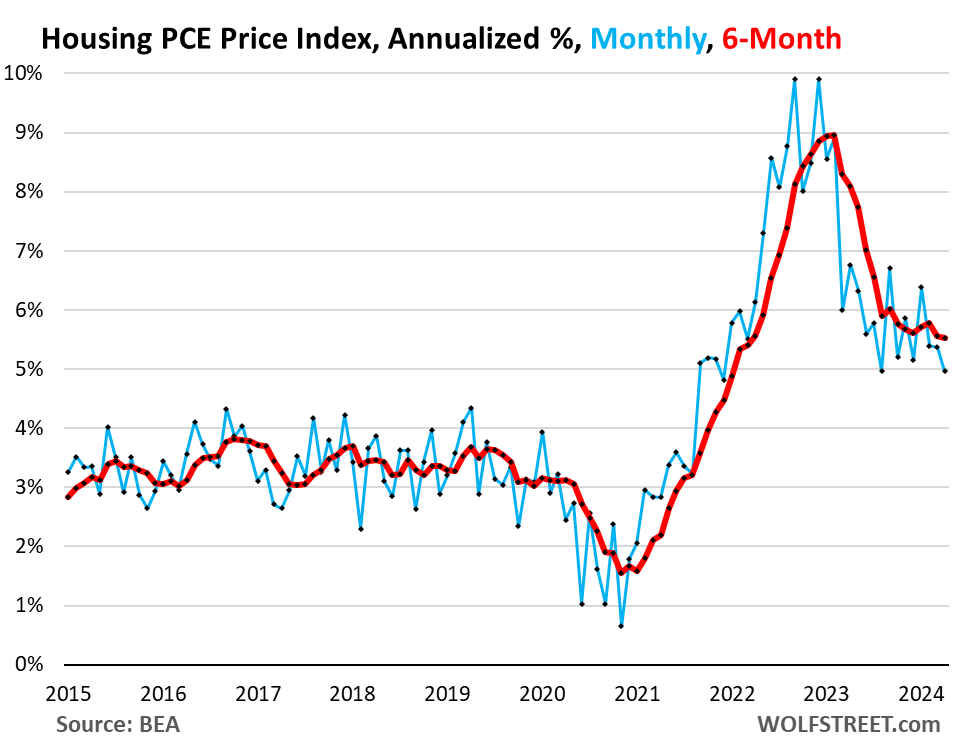

Housing PCE price index jumped by 5.0% annualized in April from March, a deceleration from prior months, but above where it had already been in August.

The six-month index jumped by 5.5% annualized, roughly the same as in the prior month. It really hasn’t significantly changed since November and remains sky high.

The housing index includes factors for rent in tenant-occupied dwellings, imputed rent for owner-occupied housing, group housing, and rental value of farm dwellings.

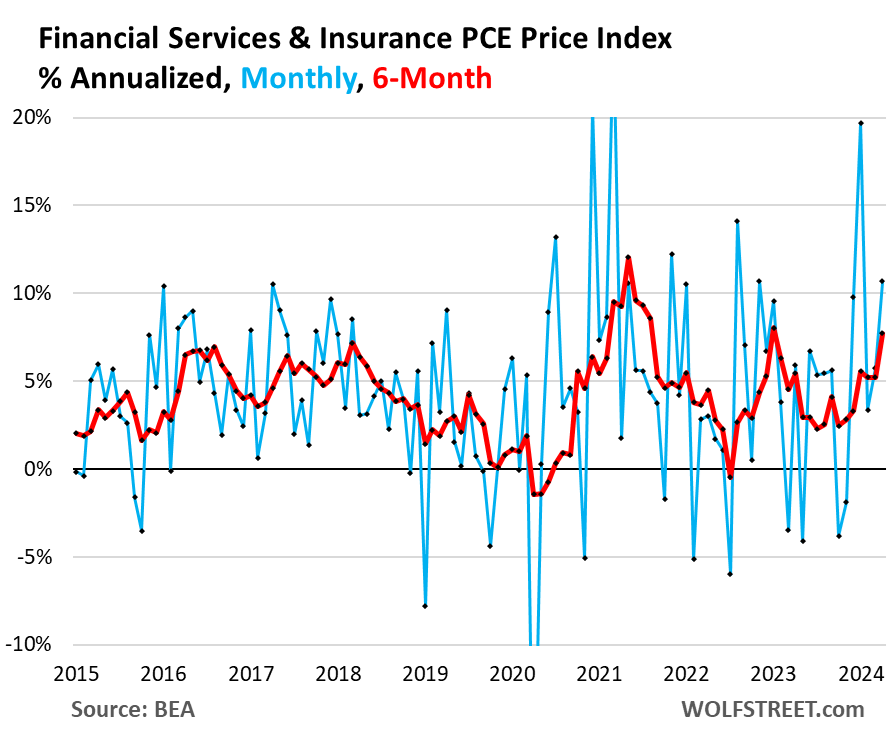

Financial services & insurance:

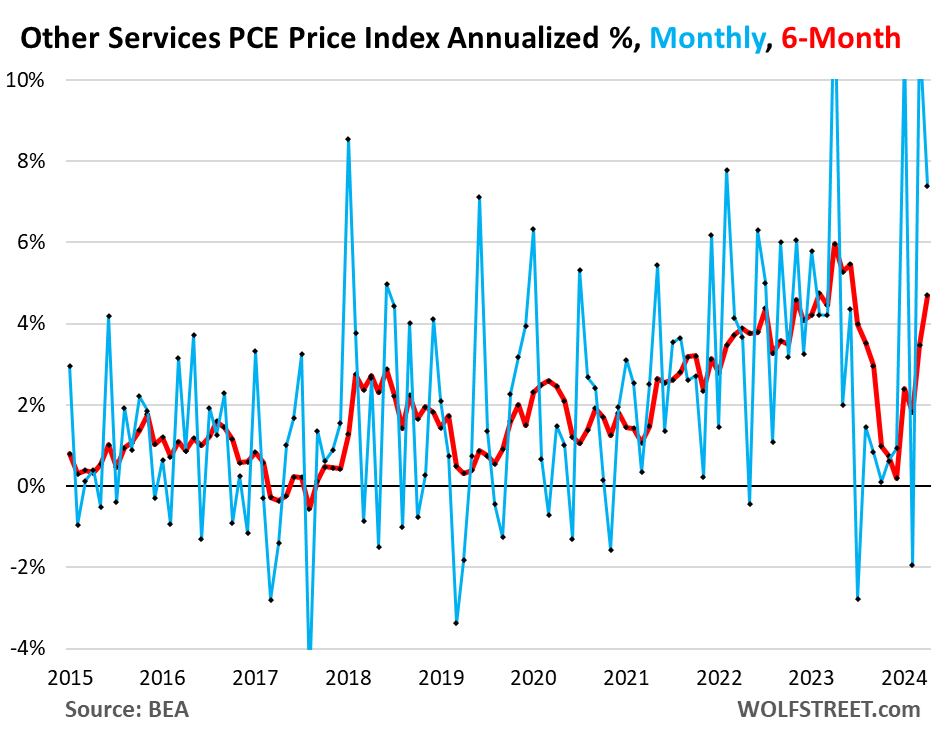

Other core services PCE price index (Broadband, cellphone, other communications; delivery; household maintenance and repair; moving and storage; education and training; legal, accounting, and tax services; dues; funeral and burial services; personal care and clothing services; social services such as homes for the elderly and rehab services, etc.):

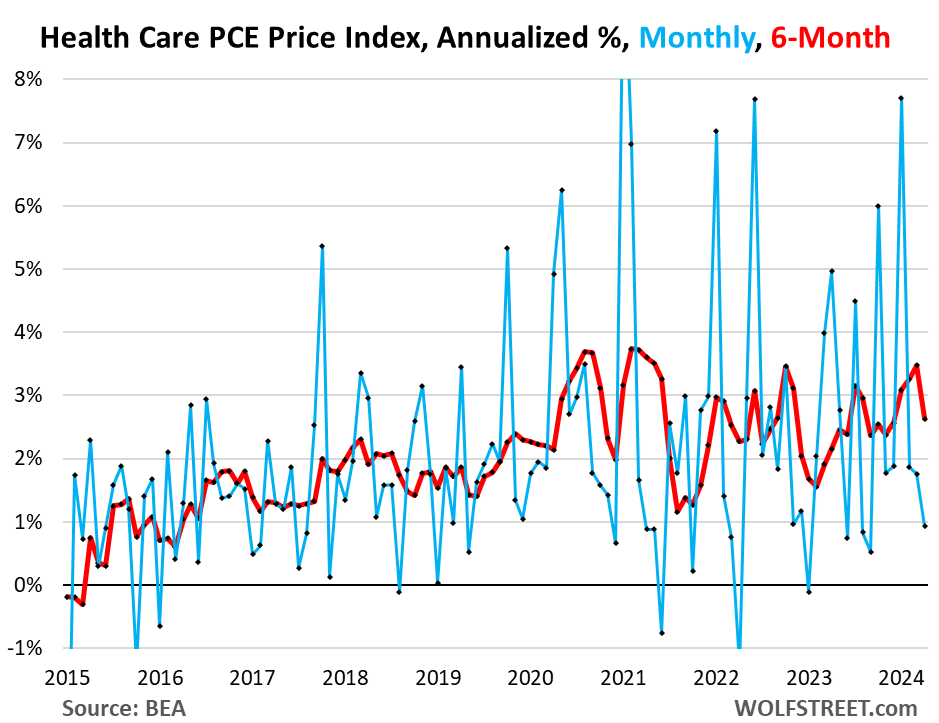

Healthcare PCE Price Index:

Transportation services PCE price index (motor-vehicle maintenance and repair, car rentals, parking fees, tolls, airline fares, etc.). A bit crazy-volatile month-to-month, eh?

![]()

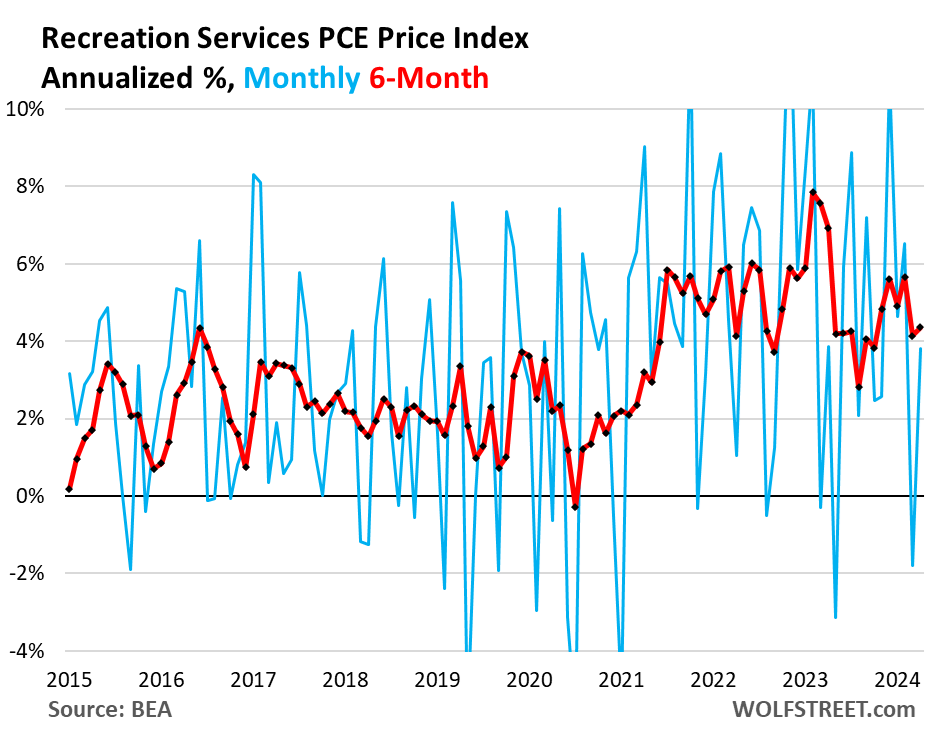

Recreation services PCE price index (cable, satellite TV & radio, streaming, concerts, sports, movies, gambling, vet services, package tours, maintenance and repair of recreational vehicles, etc.):

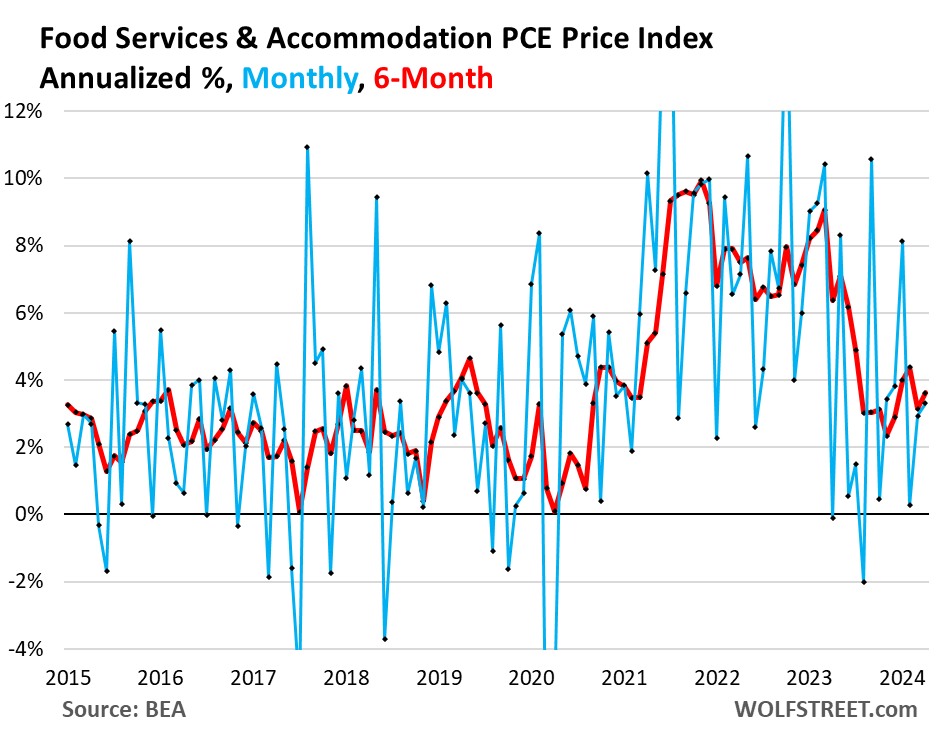

Food services & accommodation PCE price index (restaurants, hotels, motels, vacation rentals, cafeterias, cafes, delis, etc.):

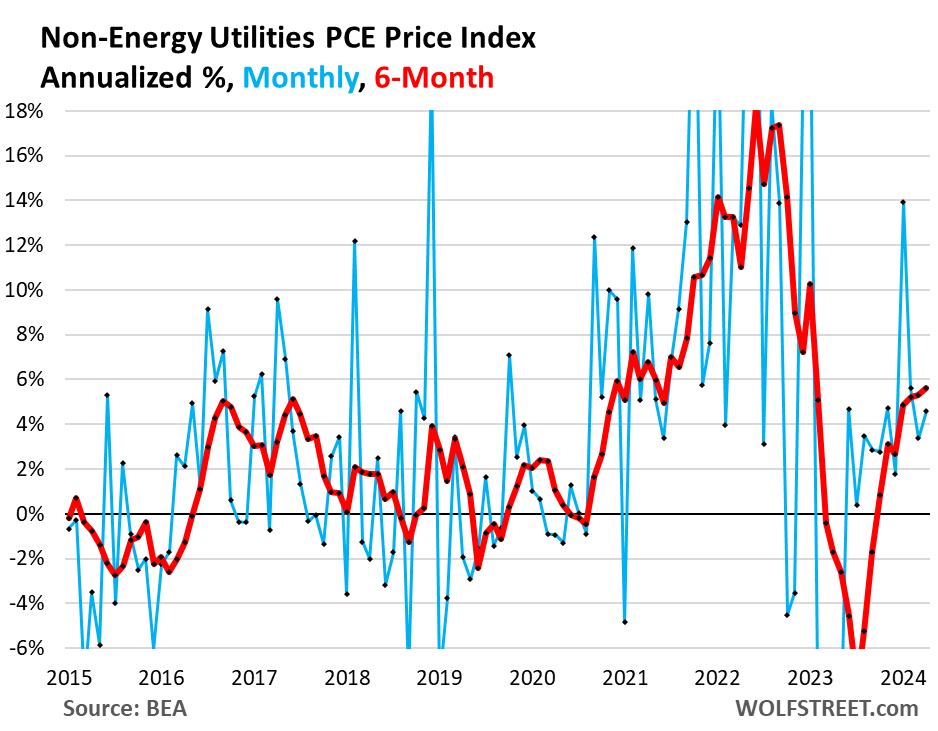

Non-energy utilities PCE price index (sewer, water supply and sanitation, trash collection):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Of course the financial media are rounding that 0.249% MoM number down to 0.2%…

Every one with an honest bone in their body rolled their eyes when they saw that .249 number, lol.

Great article, again. When you call it quits, the dispassionate, cold hard facts may not be available.

The data suggest that inflation, the enemy of the everyday person, is being managed in a manner designed to maintain the current wealth structure.

Free markets, be damned.

The FED eased again. Money supply up sharply in April

BS. You can say correctly: “M2 rose because the metric is screwed up (see below), even as the Fed tightened further (see below below).”

1. Since the beginning of April (your reference period), the Fed’s balance sheet has plunged by $155 billion, not including today’s roll-off of Treasuries.

2. Money supply (such as M2) is a bad metric that doesn’t measure money supply, as you know. For example, M2 includes CDs of less than $100k, but excludes CDs of over $100k. So if someone has a CD of $120k that matures, and the cash goes into a bank account, or into to two $60k CDs, then money supply increases. There are other problems with M2, including how ON RRPs are handled. M2 is meaningless, which is why I don’t cover it, and why the Fed no longer mentions it.

This is the best measure indicating the direction of money supply — and whether the Fed eases or not, LOL; it’s down by $1.68 trillion from the peak:

Innocent but basic question – are there any other monetary statistics that are better in your opinion than m2?

The federal reserve graph is great but unfortunately doesn’t tell the whole story as for example we know money supply increased fairly substantially between 2015 and 2020 despite fed assets decreasing.

Or is the alternative to look at other metrics alongside fed assets?

1. in terms of 2015-2020: The Fed’s assets stayed roughly flat from 2015 through 2017. QT-1 started at the very end of 2017 and took on momentum in 2018, and ended in August 2019. In Sep-Dec 2019, the Fed bailed out the repo market and its assets surged, thereby undoing a big part of QT-1. Then in March 2020, mega-QE started. So there were really four phases in this period of 2015-2020 in terms of the Fed: flat, decline, re-surge, explosion.

2. Yes, the banking system automatically creates money as part of the growth of collateral values in a growing economy.

3. There may be a better tracker of money supply than M-2. But I really don’t care.

4. What you cannot say is that because money supply rose (by whatever measure), the Fed “eased.” The Fed’s balance sheet will tell you if the Fed “eased” or not, not any measure of money supply.

Monetarism fell apart, well, basically in its Volker heydays, because it’s terrible at predicting inflation. Over the long haul, money growth and inflation match up pretty well, but what can anyone glean from a 50 year chart chanting mean reversion, mean reversion with a shaking fist? The newer, better measure sounds neat and pretty (Divisia, publicly available and for more than just USA) and try to rectify the issues with M2, but still don’t hold up in studies on predictive abilities. 1 big caveat worth pointing out, however, is the predictive value of monetarism breaks down in low inflation environments. We aren’t in that now.

WTS, I find a bit of value in M2 these days as a sort of anecdotal measure to see how close we are possibly getting back to pre-Covid trend. Take 2019 M2 and compound 6% into it, plus some unknown inflation adjustment for the spike that is now baked into our economic cake. We’re gonna have to find a new baseline normal money supply in here somewhere. I also find it unlikely to be a coincidence that the reversal of M2 and CPI declining line up pretty well. Both bottomed around the time of the 2023 bank bailout, or shortly after. CPI has been on the rise since June 2023.

I meant “means-of-payment” money. That was delineated by the G.6 Debit and Deposit Turnover Release which was terminated by President Bill Clinton’s “Paperwork Reduction Act of 1995”

https://fraser.stlouisfed.org/files/docs/releases/g6comm/g6_19961023.pdf

M2 is mud pie, always has been.

re: ” The Fed’s balance sheet will tell you if the Fed “eased” or not, not any measure of money supply.”

Dr. Richard G. Anderson said banks were unbound by reserves in 1995. That is especially true in an ample reserve’s regime.

By mid-1995 (a deliberate and misguided policy change by Alan Greenspan in order to jump start the economy after the July 1990 –Mar 1991 recession), legal, fractional, reserves (not prudential), ceased to be binding – as increasing levels of vault cash/larger ATM networks, retail deposit sweep programs (c. 1994), fewer applicable deposit classifications (including allocating “low-reserve tranche” & “reservable liabilities exemption amounts” c. 1982) & lower reserve ratios (requirements dropping by 40 percent c. 1990-91), & reserve simplification procedures (c. 2012), combined to remove reserve, & reserve ratio, restrictions.

This was the direct cause of the GFC, the boom in real-estate (as predicted in May 1980 by Dr. Leland J. Pritchard, Ph.D. Economics, Chicago 1933, M.S. Statistics, Syracuse).

He’s a Powell ball Wizard 🧙 doo doo dooooo

Powell ball Wizard! Doo doo doooo

Perhaps. You didn’t state your position beyond an absurd outburst.

Looks like those rate cuts believers is going to have to wait just a little longer..same goes for those deep in hopium that bought a house at high rates hoping for a quick re-fi to lower rate soon as part of their grand plan having their cake and eat it too, might just have to wait a little longer…

Kind of feels like Pow Pow’s wait and hold kind of not working in taming core PCE and rent inflation, maybe even a stronger signal of a coming rate hike might do the trick and he can even just jawbone without actually lifting rates..just sayin

This is the payback the economy needed for those benefiting off of 2.5% mortgages. 7.5% is a 5% rate with that missing 2.5% tacked on.

So basically the new buyers are having to pay for all those discount mortgages that happened.

Fill that piggy bank 🐷 🏦

There’s a person at the fed with their feet up and a phone. In front of them are 2 gigantic fish bowls, empty of course.

One fish bowl is filled with poker chips, this represents the old 2.5% mortgages.

The other fish bowl represents the new mortgages. Everytime a bank calls with a new 7.5% mortgage, the person throws a poker chip into this bowl.

Higher for longer until they are both even.

😆

There’s still a lot of cash buyers out there.

I’m not sure I would want to tie up the cash in real estate.

People are so wishy washy these days about where they live. Retirees might see a post on Facebook and decide to move to that place. By 11 am they have a realtor coming by, their husband scraping drywall and painting.

The churn and burn baby.

I know this is anecdotal and just one location but rents have cratered in Austin. My daughter rents out a small 3 bedroom SFH and she used to get $2500 a month. She had to go down to $2000 a month to get tenants. That’s a 20% drop.

I own 14 units across California, Wisconsin and Florida. Raised the rents 9% in California, 14% in Wisconsin and 5% in Florida. No one moved out.

How long between rent increases?

Big landlords have been saying similar things: 5-7% rent increases on renewals, but they’re having a hard time raising their asking rents to fill vacant units.

Yes, the majority of people are having to deal with the transition from QE to QT. Sky high asset prices supported by the ability to pay of most people.

It is an unstable disequilibrium. When I think about it, there is probably only one way for it to slide, and it ain’t up.

Maybe hard to say stagflation is an option except for maybe foreclosures etc

“Kind of feels like Pow Pow’s wait and hold kind of not working in taming core PCE and rent inflation”

That’s putting it mildly. But wait-and-hold is about as hawkish as we can expect from Powell & Co. in 2024. Reckless when easing, cautious when tightening.

Doesn’t look like a rate cut before the election.

I love Wolfstreet. No spin. Wisdom dispensed daily.

I still think no rate cuts at all this year.

I agree. There’s no compelling reason for cutting rates this year.

I’m expecting rate cuts, but not ones that will benefit stocks. The covid shock really threw government numbers for a loop. Their models are now wrong. They are updating their models to account for the changes, but that means they are trying measure changing variables and not getting valid data. This always happens at turning points. The data is most useless when you need it most.

I suspect that before end, revisions to the current data (which always occur) will show that the economy is weaker now than realized and employment is not as strong as folks say.

The nominal wage charts on FRED are showing wages are starting to flatline or decrease. This is rare. It’s only quarterly data, and the dip is only for a single quarter, but if subsequent quarters show the same, we’re in for a sharp ride down.

Real wages, even using government understated calculations for inflation, are down since early 2020. That is hardly indicative of a strong economy and labor market. Now it’s starting to look like even nominal wages are on the decline.

If you haven’t gotten wind of the Business Employment Dynamics Summary, it’s right up your theory’s alley.

What I can’t wrap my head around is how the much more accurate, complete BEDS report is showing a jobs discrepancy from the CES reports in the million+ range during 2023, yet demand is acting like the CES jobs growth numbers are accurate.

First – quarter GDP estimates just adjusted downward from 1.6% growth to 1.3% growth.

Who knows-higher for longer may be working!

MM,

There probably shouldn’t be. Trump wants the WH to control the Fed, I read. Conceivably to enrich himself?

Seems like we cannot guess what will happen due to any sort of logic or reasoning. This is why people call investing “the Casino”.

Howdy Harry. YEP, he backs his truth with their own data too.

An interesting comment in the sense that it stimulated my internal analysis of why in the world would the Fed cut rates in the over heated economy that we have now.

People buying imports with high priced dollars forces the USG to run a budget deficit to compensate so that the GNP doesn’t fall into depression territory of – 7%.

Wolf,

Thank you for your clear, cogent, and unbiased analysis of what is happening!

By the way … I sent a small anonymous donation to the mailing address you listed previously. I hope you

got/or will get it.

Haven’t you all seen narrative like ‚hopes of rate cuts due to weakening inflation in April’? These fucks have no shame…

I’m suck to death of that crap.

Oops, sick to death.

Desert – thought for a moment, there, that you were rasslin’ a vampire squid and losing….

may we all find a better day.

@Desert Rat

“I’m suck to death of that crap.”

I know it was a typo, but it sounds pretty bad just as is!

;-)

Too me, the rate cut mania is emblematic of the celebratory mood of a clan that is about too lose everything unless they call in their ownership rights of the USG. Like 2006,

Howdy Lone Wolf. THANKS again. Every place else is still preaching rate cuts because inflation is cooling.

Wolf is the best guy if you want a reality check on all the BS by many financial media talking heads. Wolf tells it straight, and provides the data to back it up.

Regarding the endless speculation about rate cuts, people neglect to consider that there may be other factors that affect the Fed’s policy moves, other than just the rate of inflation. Personally, I am not sure that the Fed is in control of this narrative anymore, or that they will be in the future. Another bank run, shaky Treasury auction, or some sort of other financial implosion (stock market, hedge fund blowup, etc) could lead the Fed back to rate cuts and balance sheet expansion (i.e. money printing).

We will see what lies ahead, but I am not optimistic that the Fed can manage this anymore. I hope I am wrong, or things could get really, really ugly.

There is nothing ‘ugly’ at all about wages and prices falling.

If wages and prices fall at the same time then everything remains equal, and the “ugly” is still equal. But prices are not falling and wages are not falling, and they won’t. They might give a little here and there on their way to the “big ugly”.

That is not the way it works. People spend their money on products produced by the Communist Chinese Party monopsony on labor. In direct competition with American labor.

American labor was it’s own worst enemy.

Ok, raging inflation is a problem. And probably we will have higher rates.

Is that so so bad? I Will try to reformulate: It is worse than QE?

I have no doubt that millenials being the first generation having less wealth than their parents has a lot to do with artificial rates.

If your company was in a bad shape in 2012 well, it should have died but central banks extended the agony .

Also salaries were trash.

Riich people are richer than ever. If you have money and they lend you free money , were is this going?

Last week I read that amazon make his first year generating a positive cash flow in europe, after 6-7 years behind losses.

As they usually say , It is the market folks!!!

I dont really know and all of this is just an opinion based on my perceptions but nowadays the only way to return new generations their power seems to be a raging salary increase due to inflation. or a good deprecation of durable goods due to higher rates and less money for those companies . Companies which are not even providing anything people are willing to pay for ( social media, Bitcoin , buggy AI , Netflix , prime)

I really hate the “giant tech” way of doing things. Buy the competence or smash the price having losses year over year and ruin those who cant compete for 7 years with companies like Amazon. Then start collecting and raising the prices of everything…

And the final boss is laughing at us while visiting the space.

I dont know a better system. But QE has destroyed the future of those starting to have some money to invest, to buy a house, or whatever.

I really miss when people were able to gain their bread through their honest work and investment was only for a few ones that really believe in the company and their numbers.

Just look at tesla and Bitcoin, this is just so so stupid. But people keep It Up.

I leave my parents farm to be an engineer in 2012. Until COVID, salaries were fucking Frozen since 2012.

Now I’m going back to farming because inflation is even worsening the balance. Farmers here , as well as companies who provides real assets, are doing well.

Engineer work, real engineer work is mostly related to investment.

Farmers works are different. Everyone has to eat.

QE tries to create wealth for the penniless which is the wrong policy. Loaning money to the penniless at near zero interest rates just creates a ponzi like the housing market in China that recently imploded. The rich should be made richer and the poor made poorer that’s why we need higher interest rates not lower interest rates.

Tech is what I consider a harvester industry, cleaning up what’s left of the ore body that we have been mining for 250 years. AI can never be wise or loving.

dang – I appreciate that observation, but prefer the term ‘gleaner’ or ‘scavenger’ (‘harvest’ the product of repeatable (done responsibly) reaping of time&resources invested in the planted crop). Best to you.

may we all find a better day.

Engineers are needed to allocate capital . You will provide those engineering skills in the food production process as well helping feed the world at reasonable prices. Thanks for not falling into the financial engineering world we don’t need more of those.

DM: You won’t believe the home you can buy for $2M in the tech mogul haven of Palo Alto

Real estate fans shared their shock after viral footage showed what $2 million will get homebuyers in affluent Palo Alto. In the Instagram video, realtor Olivia McNally shows viewers around a rundown three-bedroom 1950s ‘fixer-upper’ located on a quiet cul-de-sac in Palo Alto’s wealthy Barron Park neighborhood – complete with ugly shag green carpets and a shocking lack of amenities.

Those ugly carpets are a dealbreaker.

MW: Kashkari says ‘many months’ of good inflation data needed before a rate cut

From my own work with multiple businesses, the most regular pattern of price increases has historically been either annual increases or ad hoc (less than annual). However, during 2021/2022 this increased to 2-3 times a year. Including many increasing prices because their competitors were, not just because of costs. Its a mixed bag. But, now in 2023 and 2024 I have seen many switch back to annual price increases, but at higher levels than they would have done pre-2020.

Just thinking aloud whether my anecdotal experience may be what is happening elsewhere in the market, that companies have stopped multi-year price increases, but are increasing more once a year, showing the stickiness of 3-4% service inflation, but also how inflation statistics are now weighed heavily in the first few months of the year, as most still operate on a calendar year basis.

If that is the case, unless the labor market stagnates significantly we’ll have to be waiting till Q1’25 to see whether there has been any meaningful debt in current inflation levels. Price competition just doesn’t seem to be intensive enough to indicate otherwise.

The labor market has been stagnant for decades, and that didn’t stop in the past four years. In a strong labor market, wage increases should exceed inflation. That has not happened in most cases. Even looking at government data that understate true inflation, the “strong” wage gains during 2021 and 2022 at best kept up with inflation (and in many segments wage gains were less than inflation). From Q1 2020 to Q1 2024, nominal wage gains have underperformed inflation in virtually all broad segments of the economy. That is not a strong labor market.

My definition of inflation is an increase in the quantity of currency. That happens in two ways: QE from the fed that monetizes deficit spending (what we saw post 2020), and bank lending (which normally creates more inflation than the fed). The fed stopped QE and initiated QT. So far, that has been more than offset by running down ON RRP (ON RRP kept some of the newly created money post 2020 from entering the market and driving up prices, and now that is being unwound and is offsetting QT). Lending standards for autos has tightened, and the low turnover in housing is limiting loan growth there (though refinancings are starting to occur again as desperate people tap expensive equity in their home, giving up a 3% mortgage for a 7%). Thus I think inflation is over (though prices take awhile to respond.

Businesses are already reporting pushback from customers when they try to raise prices. People are being forced to trade down or go without. The covid bonanza is largely gone. There may be pockets where businesses can get away with price increases, but many cannot.

” Fed speakers have been pointing at core services incessantly.”

If they are really concerned, may be they can do a tease rate hike of 25 bps to surprise the market and show everyone that they are serious.

Financial conditions are still very loose.

Lol, the gorilla in the room is housing, look at the chart , 2021-2024 of 5-10% increases. My biggest bill every month is shelter and it was before this craziness. JPow said it right off the bat that housing needed to come down, hasn’t happened. He should have kept up with narrative and told the other fed heads to follow suit, instead we get the will they or won’t they cut.

Markets to the MOON!

If rate cuts are to stimulate the economy, why would the Fed cut the rates even if inflation went down? I don’t understand why there’s constant talk of cutting rates. It doesn’t seem to be needed.

“I don’t understand why there’s constant talk of cutting rates. It doesn’t seem to be needed.”

I agree, no rate cuts needed. Inflation is here, the economy is doing OK, labor market is doing OK too, so what the Fed needs to do is push down inflation.

But the reason why Wall Street and its minions in the financial media are clamoring for rate cuts is that they want to make money off their bets, and prices might go higher if the Fed cuts a bunch of times, and the cost of leverage will go down if the Fed cuts, and more Wall Street deals might be happening if the Fed cuts, these people get rich on fees. I’ve for years called them “Crybabies on Wall Street” and “Wall Street crybabies.” You can google that, 🤣

When Biden is down in the polls later this year, Powell will cut rates. Period end of story finito basta.

I’m not saying Powell is political or has a political position. It’s solely that he will have pressure he can’t resist. And he wants his job not to be hell on Earth until May 15, 2026 when his term end.

That is nutty talk.

Biden has never pressured the FED on rates. Only one president has done that in over 40 years.

On a financial podcast I listen to now and then, the economist being interviewed said the Fed’s concern is not inflation but more about preventing deflation. If deflation happens, the whole house of cards falls.

Do you agree with that statement Wolf?

Nah, another one spouting off deflation BS.

They are not crybabies. They are parasites that need to excised from the nation. Bring back labor camps only for wall street workers and no one else. The moment these guys slip up, make sure they never get to see their mistress or family again.

Butthurt bond traders who took a bath on duration don’t want to wait 10+ years to get their principal back.

Rate cuts are really desired to control the country’s debt.

It’s easier to control debt by devaluation, and that also keeps asset prices high so the banks don’t have to take losses on the loans against those assets.

Meanwhile in Canada….From Global News

snip: “Signs of slowing economic growth could set up “fireworks” at the Bank of Canada’s interest rate decision next week, one economist says, as odds rise for the first rate cut of the cycle.

“The Canadian economy managed to keep growing in the first quarter, but at a slower pace than first expected, Statistics Canada said Friday.”

And:

Canadian consumers now saving 7% of income after increases in disposable incomes.

We are also just above a ‘technical recession.

snip:

“Central bank governor Tiff Macklem has said a rate cut is within the realm of possibilities, but that the decision will be based on the economic data. Inflation has continued to cool since the central bank’s latest rate decision in April, coming in at 2.7 per cent annually in that month.”

Of course, if the US rates are unchanged, we must follow suit or our currency will suffer and it is usually manipulated/pegged to be around a 75 cent dollar to keep US exports up. I remember as a kid our dollar at $1.03, but that was when the Viet Nam war was raging etc etc.

Wage gains are through the roof in Canada and the province of British Columbia is raising the minimum wage again to $17.50 an hour as of today. Rates need to be hiked to prevent a wage price spiral like back in the 1970’s. This is happening against a backdrop of greatly increased emigration to Canada. When the Conservative party is elected in 2025 the immigration quotas will be reduced putting added pressure on wages in Canada.

Honest question. Is large scale immigration inflationary or deflationary? On the one hand there is less available labor so you can predict wage pressure. On the other hand there is less demand for goods and services. Net, what is it?

In both the US and Canada there has been plenty of immigration and plenty of inflation at the same time – though the “emergency monetary policy” of most of the last 20 years has been there to help inflate the bubbles.

I don’t think there is a clear answer on the inflationary/deflationary effects of immigration.

It depends.

For one, it greatly depends upon the current environment. An environment when there is low unemployment in unskilled labor (which is driving inflation) than immigration is probably disinflationary. There is no doubt paying unskilled immigrants less than the current market rate of labor is disinflationary.

However, if inflation is being driven by commodities or durable goods, then immigration is probably inflationary. Inflation still rises, but immigration keeps wages low.

It also probably depends upon the time frame. In the long run, there is no doubt that adding prime age productive workers is good for an economy, but in the short run if it happens too fast or uncontrolled, thrn it can be a bad thing.

Yes, I remember that too. For a long time the Canadian dollar had been pegged at 92 cents US but then it was allowed to float. What I don’t understand is why the Canadian dollar had a premium for a while but has declined ever since. What happened to cause this?

The Canadian dollar was roughly at parity during the summer of 2011. I have friends who moved from Vancouver to Chicago at the time and made a significant sum on the sale of their house and then converted at a great exchange rate. Though I think Vancouver real estate kept going up after they left.

They’re probably crying today since the house they sold has gone up about 400 percent in the last 13 years. If it was on a fair sized lot then 500 to 750 percent.

So………here is my take which could be goofy

In 2014 there was little inflation.

Take the inflation rate since 2014 which was roughly 32%.

Apply to the FR balance as of 2014 which was 4.5 trillion.

4.5 trillion inflated by 32% is roughly 6 trillion.

Growth in the US since 2014 was roughly 62% less inflation of 32% equals 30% real growth from 2014 to 2024.

Apply growth to 4.5 trillion…….roughly another 2 trillion added to 6 trillion equals roughly 8 trillion.

So…….8 trillion vs current balance sheet of 7.2……means to me the balance sheet has been reduced in real terms……and more importantly will continue to be.

Factoring in the destruction of assets from CRE and bank balance sheets holding bonds below par means the reduction is more meaningful.

The factor holding us up has been DC deficit spending……

Both incumbents will be in their second terms so they may care less when they take office……and we are late enough in the first term so that more stimulus is doubtful.

The auctions recently have been less than ideal.

The feds game plan is all about making interest rates respond to their actions.

Since January interest rates have been on an upward trajectory.

The squeeze is starting……and the DC gang can’t do much since their auction friendly environment is fading away.

MCD, TGT, LOWE, HD, WAL, WMT have stated some sort of warning about sales.

The steam in the economy is still strong…….but the coal bin is starting to look empty.

Just my take.

I like the inflation-adjusted FR BS concept, but why should it rise proportional to economic growth? During the 20th century it rose only moderately it seems.

Look at the technicals of the 10Y treasury interest chart and tell me the market isn’t ripe for an upward explosion of interest rates around mid-July.

The S&P 500 is already up 11% YTD without any rate cuts, and market expectations for 7 rate cuts dialed back to 1.

Imagine if there were rate cuts. Markets would likely have gone parabolic like it’s 1999. I’m glad sanity prevailed at the Federal Reserve.

You mean the market hasn’t already gone parabolic like it’s 1999?

Bullishness is very high right now but it’s nothing in comparison to 1995-2000. The S&P 500 returned 32%, 25%, 26%, and 30% in back-to-back-to-back years. We haven’t had anything like that since then.

Ever since the S&P 500 broke through 5,200 in March, further net gains have been relatively muted over the last 2½ months. And as Wolf wrote in the article preceding this one, high-flying growth stocks are being punished for missing earnings in a way not seen since 2022.

Why would the FOMC cut rates before the BOE or the EU? Inflation in England in particular has dropped precipitously and the BOE will probably the first big central bank to pivot. The world’s going to watch what happens. If the BOE can pivot and inflation remains tame the canary in the mine says it’s safe to come in.

I still think this is a repeat of 2008, the FED raised the feds Fund rate to 5.5 and held it for a year and we had the Great recession fast forward over a decade and they’ve done the same thing, They have held the feds fund rate at 5.5 for a little over 9 months, so it would look like the recession will be here in a few months.

Quickest way to solve the inflation issue would be for the federal government to balance the budget. Deep cuts to social programs, and a reduction in the quantity of government departments would solve the problem, and set us up for long-term growth. De-regulate and spending cuts. While we’re at it, pass a constitutional amendment that required representatives to read at least 90% of what they sign, and sets a 30 year expiration on all laws, rules, and regulations.

Your prescription is screwed up, designed to squeeze the little guys that already don’t have anything, while enhancing the wealth of the already rich. So that’s not going to fly here. What the government should do to reduce the deficit is:

1. Impose a transaction tax of 0.1% on any and all nonfood transactions by any entity with at least one leg in the US, applied to all transactions from high-speed trading to corporate M&A, to repos, to stocks, to bonds, to home sales, to M&A. So that $100 billion corporate takeover generates a tax of $100 million. And the $5 trillion-plus in trading of securities, repos, etc., a day generates $5 billion in transaction taxes a day, or $1.3 trillion a year. Apply this transaction tax to futures, currency trading, credit default swaps, interest rate swaps… to all derivatives with at least one leg in the US. If you want to be serious about balancing the budget, you tax all these transactions one tiny bit (by 0.1%). This would have other benefits as well.

2. Make “charitable contributions” over $1,000 not tax-deductible, so that will tamp down on a lot of scams that the wealthy are playing with their “charitable trusts,” etc. If they want to donate to a good cause, let them do it out of the goodness of their hearts, and not to dodge billions of dollars in income taxes (Buffett).

3. Make all real-estate capital gains fully taxed at the capital gains tax rate, no matter what.

4. Make corporations pay a minimum 15% income tax on their highest earnings that they announce, such as “adjusted” earnings, etc. If they say that they made this much in profits, let them pay taxes on it.

5. Fully remove any deductibility of mortgage interest and property taxes by homeowners.

BTW, Social Security is the biggest “social program” in this country, and it’s self-funded and over the past two decades generated a $2 trillion surplus.

Much to agree with here — it would be funny: “While we’re at it, pass a constitutional amendment that required representatives to read at least 90% of what they sign, and sets a 30 year expiration on all laws, rules, and regulations.”

Totally agree 👍

On more.. stop supporting endless wars by sending weapons and trillions outside usa to favor big military complex.

…But they have to read it BEFORE they sign it.

I wonder if #1 would make all of this slosh of cash a bit more rational or if it would just fuel more insane spending. Maybe both. I don’t love the idea of making transactions more complicated as capitalism and smooth low cost transactions in a non croney sense is my hope for the world… but maybe this would be awesome. Wolf for USA supreme financial leader I say! We could make a silly statue that looks like one of your mugs to commemorate our supreme leader. I just finished an overnight shift so sorry if none of that makes sense.

Wolf: in your points you leave out any curtailment on spending. The Government’s State & Federal have a spending problem they are unable to control. Your proposals above would only feed the beasts and encourage more unproductive spending. I’m shocked, shocked at this horse shed. You should know better. In fact, I think it must be a joke!

Spending is a problem, but not the biggest problem. You people always want to cut spending in a way that squeezes the little people. Start with cutting all corporate and housing subsidies to zero.

Not taxing certain capital gains is a subsidy of the wealthy. Allowing for charitable contributions to be tax-deductible is a subsidy of the richest. Etc. These subsidies are a form of indirect spending. Think a little about this stuff.

Luke,

The first problem to solve is not what our government should do, but get a government that is run by the people, not with special interests and lobbies. Part of this would be tearing down the two party system, which while Americans consider them very different, they essentially share similar interests.

To achieve this there first needs to be a recognition that the widespread disatifaction is rooted in the same causes. In this country large, organized trade unions could achieve that but requires a lot of educate and organization. The corporations and political parties are highly organized and know how to play the game and the rest are content with whatever the ruling class offers them as something to blame.

Then thst government can focus on the economy, healthcare, education, housing and so on instead of imperialism and enriching themselves.

Seems like a lot but the US and Europe have a strong history of trade unions so the key is education and organization.

Have you tried one of wolfs luxoburgers glen, I think he added an extra ingredient to enlarge the brain.

But to your plan of peace and prosperity for all wild beasts. I’m down with the plan… But first, the wolf luxoburger.

Howdy Luke and other folk. Yall will never find your answers through Govern ment. The forefathers knew ignoring a King was easier than the system they set up for US. Stay out of debt, live with in your means and save some of your earnings always. Squirrels are looking forward to more inflation if it comes and not afraid of it…..See how easy it can be??????

Bubbas been eating wolfs luxoburgers, now he’s turned to a squirrel.

It would be interesting to see these graphs as an index set at 100 at the beginning of the period much like the housing bubble graphs. On the other hand, it might be too depressing to see them in that format.

Go my CPI articles to see index charts. CPI is our primary inflation index, and I go into it in detail.

The PCE price index here is an index that the Fed uses as measuring stick, which is the only reason I discuss it — and I discuss it from the Fed’s point of view.

Here is the most recent CPI article with lots of index charts by category, such as rents, core services, durable goods, new vehicles, used vehicles, food at home, gasoline, etc. … All you have to do is read those articles, they’re a monthly feature on every CPI day.

https://wolfstreet.com/2024/05/15/beneath-the-skin-of-cpi-inflation-april-after-some-zigs-a-zag-but-6-month-core-cpi-hits-4-0-6-month-core-services-cpi-hits-6-0-both-highest-since-mid-2023/

Thanks, Wolf. I do read those articles too and the graphs are stunning. I guess I wasn’t thinking past this article. A similar graph would show how damaging the Fed’s 2% PCE target is over time as well as their miserable performance in achieving it.

This “imputed rent” (OER in CPI) is hot and is driving overall inflation rates. It’s hot because tenant-occupied housing rents are hot (“Rent” in CPI), and because it includes the costs of homeowner’s insurance, maintenance, etc. and all those costs have seen big price increases, which is why the imputed rent factors have been so hot. So be careful with your shopworn threadbare criticism.

I should have called the core of your comment “bullshit.” I was being nice.

People have posted the same BS about OER/imputed rent for over decade here. Copy and paste. I wasted countless hours shooting this stuff down.

JimK,

They seem valid to me. Currently I own a 24 year old home and it is paid for. However insurance is $1400 or so with a high deductible, flood insurance is $700, I have several windows which need replacing and an original HVAC, kitchen, and water heater. On top of that property taxes are over 6K a year. I know I indirectly pay for much of that if I rent but not on the scale I do as a homeowner. I could probably rent out for 3K or a little more depending on who pays water and sewer, and garbage which are also going up but the math of it hardly makes sense.

Admittedly these factors vary by age of home and state of residence. In California, even in my area, the costs are not insignificant and so a “paid for” house is probably $1,200 plus maintenance of which I just had 3 good neighbor fence lines replaced at going rate of about $45 per foot so add 5K just this year. Soon to be HVAC will be close to 20K more than likely.

I like having my own house now but can easily see being a renter once the nest is empty.

– No matter what the inflation is, Mr. Market is telling me that rate cuts are coming. The only thing that is up for dispute is the question “When”.

– Currently I am on the fence what the next move of the FED is going to be. Mr. Market is still not quite sure about that. Mr. Market thinks that either one rate hike is quite possible or that rates won’t be cut.

In a recent interview Powell stated the lags are longer than they thought for rents and owners equivalent of rent. He stated that current rent increases have been “low” but they haven’t shown up in the data. But according to the data in 2023 the graph indicates that it did fall. Apparently, something showed up in the data. I not sure if I am missing something or Powell is misleading the public.

https://www.youtube.com/watch?v=3TufaG29B7w ( timestamp 16:13)

Just wait a few more weeks, the fireworks will really start once Putin starts meddling in the 2024 election (likely through oil prices).

All of you are looking at this like it’s a 2-dimensional chessboard… when in fact, this is like playing 3 or even 4-dimensional chess with one tied behind every players back.

You people who think Putin has vast influence US politics make me laugh. He can’t even win a war on his doorstep with a massive advantage in manpower and material. People here vote for or against politicians for all kinds of reasons but “Russia” isn’t even in the top 10.