This cannot possibly happen to US markets because US markets are special?

By Wolf Richter for WOLF STREET.

Most major stock markets globally rose in 2023, some by a lot, but a bunch of them are still below their all-time highs 15 or 20 or 35 years ago, while others are barely above those all-time highs from a generation ago.

It was a funny year for US stocks, with the magnificent 7 stocks carrying the markets, with the Dow and the Nasdaq 100 setting all-time highs, while the S&P 500 ended a hair below its all-time high two years ago, while the Nasdaq ended somewhat further below its all-time high in November 2021, and while the Russell 2000, which tracks 2000 smaller stocks, ended where it had been three years ago. We discussed all this on Friday. I bring this up because US markets have been among the exceptions, not the norm in terms of global stock markets.

First a ground rule here. Stock markets are valued in local currency. When that currency’s purchasing power plunges due to inflation year after year for decades, then stock market indices are a reflection of inflation more than of corporate performance. The 1,700% spike in Argentina’s Merval Index in three years, from about 51,000 in January 2021 to 930,000 now is a sign of the collapsing peso, and not of corporate performance. We’re going to ignore those markets. We’re going to stick to the major markets of the largest economies that have had relatively stable currencies and relatively low inflation – 6% year-over-year inflation being relatively low compared to 160% year-over-year (Argentina).

Huge bubbles led to long-term declines.

Yes, we all know, this cannot possibly ever-never happen in the US markets because US markets are special. It did happen in the US markets though, when the Nasdaq plunged by 78% during the dotcom bust from March 2000 to October 2002, and then didn’t get back to its March 2000 high until 15 years later, until October 2015, and it only did so because of huge amounts of money-printing and 0% interest.

Money printing and 0% were an option back then because inflation was below the Fed’s target; inflation was low in all developed economies. Now inflation has resurged in all developed economies, there has been an inflation shock, and we’re in a different ballgame.

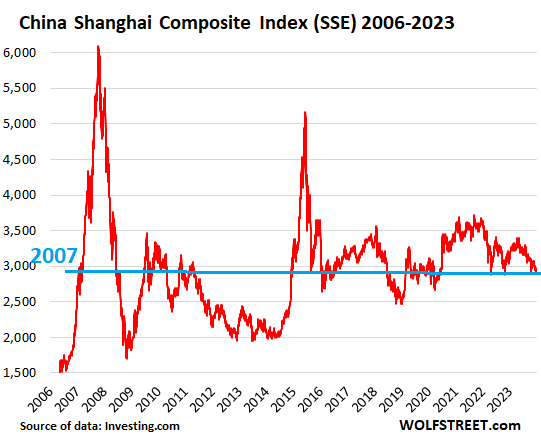

China’s Shanghai Stock Exchange (SSE), back where it had been 17 years ago:

- Closed the year at 2,974

- Year-over-year: -3.7%

- From October 2007 all-time high: -51%

- Back where it had first been in January 2007

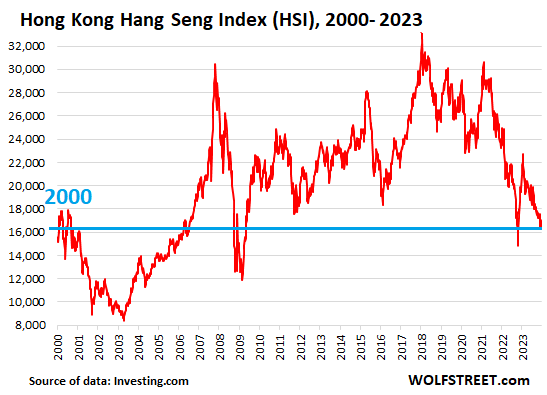

Hong Kong’s Hang Seng Index (HSI), back where it had been 24 years ago:

- Closed the year at 17,047

- Year-over-year: -13.8%

- From January 2018 all-time high: -48.6%

- Back where it had first been in January 2000.

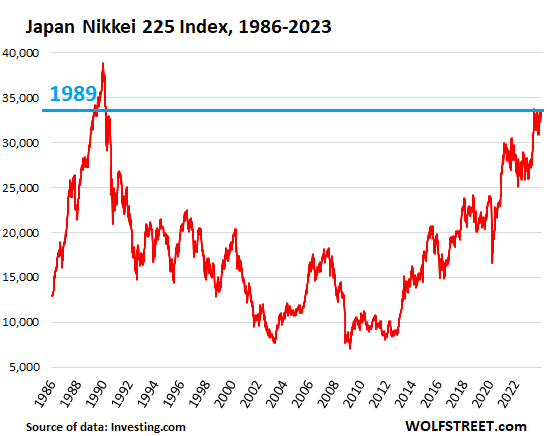

Japan’s Nikkei 225 (NIK), back where it had been 35 years ago:

- Closed 2023 at 33,464

- Year-over-year: +28%

- From December 1989 all-time high: -14%.

It took the huge amount of money-printing from 2012 on under Abenomics to get this index to recover. Now inflation is back in Japan, and QE has been systematically dialed back and will likely end entirely in 2024:

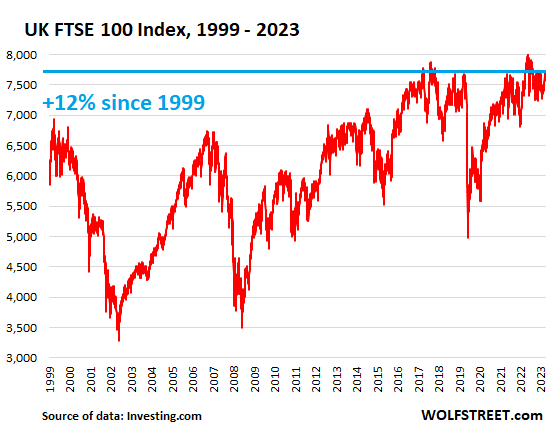

UK’s FTSE 100 Index (FTSE), +12% in 24 years.

- Closed the year at 7,733

- Year-over-year: +3.8%

- From all-time high in February 2023: -3.6%

- From December 1999 high: +7%

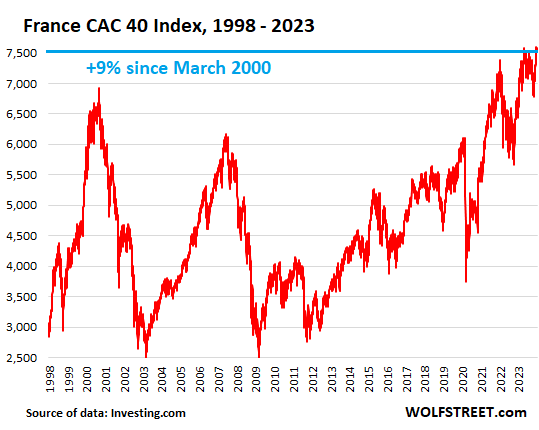

France’s CAC 40 Index (PX1), + 9% in 24 years.

- Closed the year at 7,543

- Year-over-year: +16.5%

- From March 2000 high: +9.0%

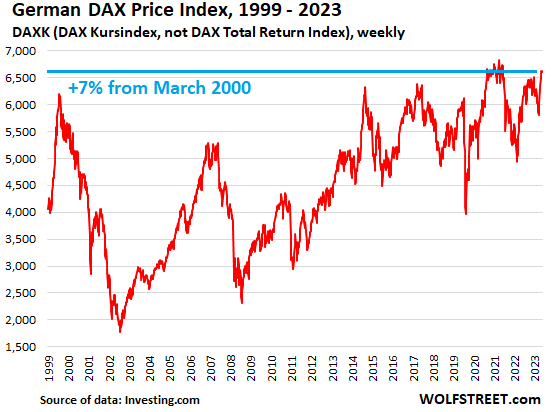

Germany’s DAX Price Index (DAXK), +7% in 24 years.

The most widely cited German stock market index, the DAX, is a “total return index” that includes dividends and is therefore not comparable to a “price index,” such as the S&P 500 Index, which does not include dividends.

The DAX Kursindex (DAXK) is a price index, and does not include dividends, and is comparable to the S&P 500 Index and all stock indices here. So that’s what we’ll use.

- Closed the year at 6,628

- Year-over-year: +15.2%

- From all-time high in January 2021: -3.6%

- From March 2000 high: +7%

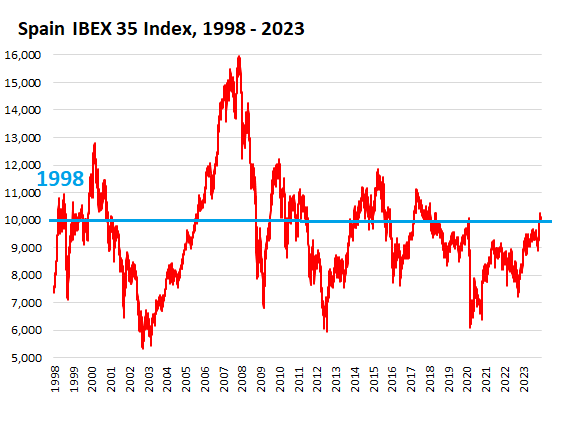

Spain’s IBEX 35 Index (IBEX), back where it had first been 26 years ago:

- Closed the year at 10,102

- Year-over-year: +22.8%

- From all-time high in Dec 2007: -36%

- Back where it had first been in 1998

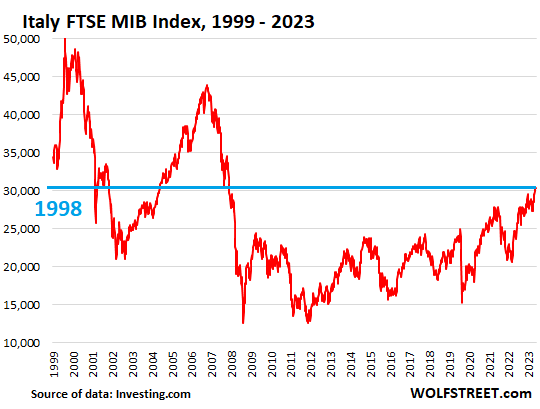

Italy’s FTSE MIB Index, back where it had first been 26 years ago.

- Closed the year at 30,352

- Year-over-year: +28%

- From all-time high in March 2000: -39%

- Back where it had first been in 1998

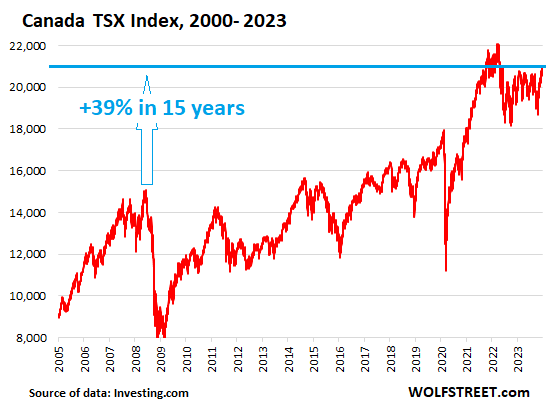

By contrast, Canada’s TSX Composite Index (compromise between the German DAXK and the US S&P 500?), +39% in 24 years:

- Closed the year at 20,958

- Year-over-year: +8.1%

- From March 2022 all-time high: -5.1%

- From March 2000 high: +39%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Do these countries have the same automatic inflows into stocks that the US retirement system generates?

The automatic 401k investment idea was a narrative used to prop up the 2000 bubble. Be careful.

When people see things dropping, they can move all their money out of 401k stock funds into money market funds, starting a downward stock price cascade.

The dot.com bust destroyed 2M jobs & was exacerbated by the 9/11.

The difference today is $1.7-2T in federal deficit spending and falling 30YFRM rates that will help to stabilize the housing market, meaning higher seasonally adjusted sales. And, we’ll probably see existing home prices rise and could see an end to falling new home prices.

Add to this lots of local spending via high property & sales taxes, and you get a VERY LOW probability of a recession in ’24, outside of a black swan event like 9/11. Certainly, we enter ’24 with a geopolitical landscape that easily could meet or exceed 9/11.

And by the way, where’s the CRE apocalypse? Amazingly, it still hasn’t show up and probably won’t at least through the first part of ’24. Nobody’s talking about it anymore, despite being all the rage 5 months ago.

When 1st-time unemployment claims get up to 250K and stay there for at least 2 months, then we can say for sure that the labor market is softening.

‘Nobody’s talking about it anymore, despite being all the rage 5 months ago.’

The people in the biz talk about it. It’s not headline news, i.e., ‘the rage’ because it’s old news and everybody knows office buildings and of course malls are worth a fraction of their previous and in many cases, less than the mortgage. The stalled new Frisco towers are still stalled.

Frisco office building sales after repos went for less than half appraisal from 3 years ago.

Tallest tower in Canada is still in bankruptcy, half finished. This news is less than 3 months old. Simon Group, largest US mall owner isn’t trying to get back the 10 or so malls it’s walked away from, etc. etc. Canadian Van Dyk group, also building in Washington with thousands of units under construction, petitioned into bankruptcy in last two months.

Old news so not headlines. But HUGE opportunity for someone who thinks it’s over, and doesn’t need financing.

Nick Kelly,

Agreed. The Office and retail CRE bust continues at full speed. Investors and lenders continue to take huge losses, default rates keep soaring, and office properties are selling at 50% to 70% below their 2015-2018 prices. It’s a huge fiasco, but investors are losing money mostly, not banks, and so the Fed doesn’t worry about it. Maybe I should write another article about office towers to quash these kinds of comments about CRE somehow not being in trouble anymore.

But I’m a little confused. Frisco is in Texas. If you’re referring to the city on the West Coast with a $2-billion megaproject that has barely reached grade, stalled years ago, and is now in bankruptcy, and whose Chinese developer is now in bad shape in China, well, that city is variously called San Francisco, the City, SF, or stretching it, San Fran.

Point taken re: “Frisco’. You have to watch yourself around a local. But ‘the City’ I’ll reserve for the London Financial district. So SF from now on.

From the business pages of my local newspaper on 13 December 2023:

“After months of negotiations and uncertainty for the tallest and most valuable office tower in Minnesota, the owner of the IDS Center has negotiated a three-year extension for its loan on the 57-story tower.”

“Today, many Twin Cities building owners and their lenders are finding themselves in a state of financial purgatory, with both parties searching for an exit strategy that best minimizes their losses.”

“I view it as a bit of a staring contest between office borrowers and lenders. Neither party wants to blink.”

Accesso, based in Florida, was several months late in financing a $151.7 million loan to make a balloon payment, which was due in this past fall. Will things change in downtown Minneapolis in the three years that Accesso has on the loan extension? My guess is probably not much.

The IDS has 1.4 million square feet and is at the center of downtown Minneapolis @ South 8th Street & Nicollet Avenue. Ten years ago, Accesso paid $253.5 million for it, and at that time it was “valued” at $256M. Earlier in 2023, it was valued at $180M.

Yes, when the bubble collapses many will stop contributing. That will end much of the automatic investing.

The biggest bubble in history is likely to have a pretty bad hangover, at some point. No natural population growth and little to no productivity growth means a slow growing economy. Probably around 1%. That should produce a lot different market return than the past 10 or 12 years. Other countries experiencing the same problems.

“When people see things dropping, they can move all their money out of 401k stock funds into money market funds…”

This is not true of all 401(k) funds.

The default my company offers is a 401(k) thru Vanguard, which only offers ~20 choices of funds, all of which are stock or bond funds. I had to request my 401(k) be switched to a self-directed fund, which is now with Schwab and lets me buy any listed stock, ETF, or fixed income product.

But most people at my company would not be able to “move their money into a MMMF” as you suggest.

Most 401k plans have a stable value fund that is similar to MMF. It will be cash and short term bonds

Bobber,

Sure people can shift to MM funds within a 401k.

But 401k “Auto-Invest” (or “Auto-Destruct”…) might be responsible for the goofy valuation levels obtained pre-2009 and post 2015…

In other words, in the same way there can be mindless 401k panic (triggering runs to MM accts), there can be mindless 401k booms (absurd valuation levels enduring for years, based on blind auto-buying).

Even today, way too many people (way, way, way too many) really only look at recent-ish price trends to determine “how safe/valuable” is the “market”.

There are tons and tons of better (much, much, much better) valuation metrics…but 85% of investors are ignorant of them or too greedy to act on them (“lemme squeeze out that last 10% of a 100% overvaluation…” ends up under the train, not on it.)

So much for “buy and hold” theories.

Looks like money managers make more than their investors.

In a very important way, the US is special. US assets are the safe haven investment for most of the world. It has very little to do with 401k auto investments, or ETFs, or any other reason I’ve seen in these comments.

If you are well off person from China or Venezuela, or even the EU countries — you get your money off shore to the US to protect it from local autorities. Will this happen forever? Of course not. US leadership is making investment here worse every day. But it’s still better than the alternatives, which is why you see charts like this today.

Next time there is a recession and stocks go on sale, buy. The rest of the world will ensure you will make gains.

“you get your money off shore…to protect it from local authorities”

Feel the exact same way.

Only problem?

I’m here in the US…

Fred Schwed’s query is evergreen: “Where are the customers’ yachts?”

US is different. These rules don’t apply to us. With the press of a button, I not only print a few trillion dollars, I also print cars, food, gas, oil, houses, apartments, utilities, hospitals, doctors medicare. This is what you are made to believe by the media.

My club can enjoy riches only as long as the majority slogs to make money for them. To ensure this, I run high inflation so that you must slog to make ends meet. We also play this number game that keeps confusing you that you are making more dollars as your living standards keep decreasing.

I took the Everything bubble and blew it to a mega bubble with my first President. With my second president, I blew this mega bubble into a giga bubble. With the next president, I will blow a Tera bubble!

1. Other way around? US retirement moneys flow into these foreign markets because a lot of diversified funds and global funds invest in foreign markets.

2. There is nothing “automatic” in terms of the inflows in the US. People with 401ks CHOOSE the funds they want to invest in. Pension funds CHOOSE the stocks they want to invest in. Like everyone.

3. The same choices exist in those countries, and their pension funds and life insurers have very diversified portfolios, including local stocks, as do individuals in their retirement portfolios.

But….

are there not things in play that require investment in plans prior to April 15? Hence the strong seasonal “Up” in the first quarter?

index funds get the inflows…

And the money managers seem to know who ever spends first spends best….which might explain the late year run up in stocks….expecting this influx.

“are there not things in play that require investment in plans prior to April 15? Hence the strong seasonal “Up” in the first quarter?”

The first conspiracy theory for the New Year? Happy New Year, we’re starting out on the right foot.

No, what’s required is that you do your taxes by April 15 and pay them by April 15, and some people get refunds during tax season, so the used-car industry hopes that people use their $1,200 refund for a down payment on a used car. But other people owe taxes and they have to send the IRS the cash that they’d saved for a down payment. So these hopes for used-car tax season don’t always work out.

In terms of stocks, no one has to buy anything by April 15, you have to fund your IRA account by April 15, but you can let the cash sit there in the account as cash and think about it for a while, or you can buy bonds or CDs or money market funds. And 401ks are funded with every payroll throughout the year.

With stocks, Q1 is a very mixed bag:

Q1 2018 was down

Q1 2019 was good

Q1 2020 was terrible

Q1 2021 was up

Q1 2022 was bad

Q1 2023 was up

Over those years 2018-2023:

When there was a strong selloff into the end of the year (end of 2018 & end of 2022), the following Q1 was up (Q1 2019 and Q1 2023).

When there were big gains into the end of the year (end of 2017 and end of 2022), the following Q1 was down (2019, 2023)

Based on this, the strong rally toward the end of 2023 suggests a bad Q1 2024.

Wolf wrote:

“1. Other way around? US retirement moneys flow into these foreign markets because a lot of diversified funds and global funds invest in foreign markets.”

According to the BEA, the US international investment position at the end of the second quarter 2023 was -USD18.94T and at the end of the third quarter was -USD18.96T, which suggests that more foreigners are investing in the US than US citizens are investing in foreign countries. Although I grant that it has been going up and down since the start of 2022. Interestingly, the net position looks a little like an inverted SP500.

See https://www.bea.gov/data/intl-trade-investment/international-investment-position

Happy New Year fellow Wolfstreet posters!

May 2024 be a great year for all of us!

Happy New Year, Manzana and others! Thank you Wolf!

Everyone, all the Best for the New Year!!!

Thank you, Wolf. Wishing healthy and wealthy 2024 to you and yours. Happy New Year!!

Back atcha, Prof Richter.

Charts on different markets all shown the effects of money printing. With tonnes of freshly print monies flow into these casinos around the world, we see asset bubbles building up AKA wealth effects that highly promoted by Benanke, so do his successors.

Will it be better off if these central bankers do not have printers at their will?

I agree with Simonyoosen, where would these funds be without the artificial inflation? Are these funds equivalent to the US Nasdaq?

Happy New Year!

Happy New Year, everyone. Let’s see what happens next!

Happy New Year to all!

“Huge bubbles led to long-term declines.”

“Yes, we all know, this cannot possibly ever-never happen in the US markets because US markets are special. It did happen in the US markets though, when the Nasdaq plunged by 78% during the dotcom bust from March 2000 to October 2002, and then didn’t get back to its March 2000 high until 15 years later, until October 2015, and it only did so because of huge amounts of money-printing and 0% interest.”

“Money printing and 0% were an option back then because inflation was below the Fed’s target; inflation was low in all developed economies. Now inflation has resurged in all developed economies, there has been an inflation shock, and we’re in a different ballgame.”

\\

Viewpoints | August 31, 2022

Entering the Superbubble’s Final Act

By Jeremy Grantham

“The current superbubble features an unprecedentedly dangerous mix of cross-asset overvaluation (with bonds, housing, and stocks all critically overpriced and now rapidly losing momentum), commodity shock, and Fed hawkishness. Each cycle is different and unique – but every historical parallel suggests that the worst is yet to come.”

“We’ve been in such a period, a true superbubble, for a little while now. And the first thing to remember here is that these superbubbles, as well as ordinary 2 sigma bubbles, have always – in developed equity markets – broken back to trend. The higher they go, therefore, the further they have to fall.”

“Why are the historic superbubbles always followed by major economic setbacks? Perhaps because they occurred after a very extended build-up of market and economic forces – with a major surge of optimism thrown in at the end. At the peak, the economy always looks near perfect: full employment, strong GDP, no inflation, record margins. This was the case in 1929, 1972, 1999, and in Japan (the most important non-U.S. superbubble). The ageing cycle and temporary near perfection of fundamentals leave economic and financial data with only one way to go.”

– Mr. Grantham is a student of asset bubbles. I’m sure this is fine. /s

It would seem that Grantham is suffering the same dilemma that both Keynes betting against the mark and Newton betting, before the collapse eventually came to pass. Lost their shirts by betting against the time that the current market price would reflect their perception of where the price should be. In both cases, a liquidity fuel rally did them both in.

Like now.

“Like now”

Did you forget where the casino was just a couple short months ago? How quickly people forget and turn to denial. Do you really believe the gains of the last two months, based on what the Fed will do, are sustainable? I think our ability to paper over the disaster that is the US economy and the stonk casino is coming to an end. I don’t believe they will be able to continue the charade much longer.

I’ve been saying since about 2009 when I realized what was happening to America that I thought we could continue the game until 2030 or so. I still stand by that prediction.

That and 5 bucks will get you a cup of coffee.

JD:

Legend in your own mind? Lol

Einhal,

I hope you are right in your prediction but hope it is much sooner than 2030.

I wish coffee was only $5.00. I paid 7.50 for a smallish mocha frap over christmas at Starbucks.. it was made out of bottled chocolate milk, ice, whipped topping and a dust of cookie crumbs. no coffee could be found! I stopped “starbucking” years ago, make my own at home, but it was Christmas and I was travelling. Starbucks is now off my radar permanently.

Liquidity won’t come along until the wheels fall off though, as we’re currently seeing QT and too-high inflation.

History shows the pivots don’t mark the end of the mess, but the start of it.

I have a gut feeling participants using MMF is going to cause some kind of “issue/event” when people decide they don’t want sticks/bonds and the FDIC aren’t going to cover cash.

Huh? Surely you aren’t under the impression that Newton was shorting the South Sea company and lost his stake in a ‘liquidity fuel rally’? He was a believer like the rest and lost 20,000 pounds or about 3 million US in today’s money when the South Sea Bubble collapsed.

That’s my understanding too. If I recall correctly though, Newton sold his initial stake for a profit, but as the rally continued higher and other investors were getting rich he reinvested close to the final collapse. He was initially correct, but FOMO got him in the end. A cautionary tale.

Happy New Year everyone and thank you for all the great insights this year Wolf!

After losing money in the South Sea Bubble Newton said something along the lines of: “I can calculate the motion of heavenly stars with precision, but, not the madness of people”. Thus, hinting at consensual hallucinations in finances.

another economist that keeps making predictions about the future … with absolutely terrible track records. but hey eventually he may get lucky and be right.

nobody knows nothing about what’s in store for 2024 and beyond.

Would be interesting to see an analysis of these markets that comprehends dividends

The ultimate gauge of market performance is surely either total inflation-adjusted returns with dividends reinvested, or remaining inflation-adjusted value at a given draw down rate (including dividend yield)

“…inflation-adjusted”

What does consumer price inflation have to do with asset price inflation? Nada. There are times & places where there is lots of asset price inflation and little or no consumer price inflation; and there are times when there is asset price DEflation and lots of consumer price INflation (such as 2022 in the USA).

You wouldn’t adjust consumer price inflation (CPI) by asset price inflation (S&P500) either. So CPI went up by 10% over x years, and over the same period, the S&P 500 went up 10%, and so on an asset-price-inflation-adjusted basis, CPI actually went up 0%? Sure, you can do it, you can calculate anything. But see how this doesn’t make any sense?

People look at their brokerage statement, portfolio, 401k, IRA, or whatever on an inflation-adjusted basis? That would be a hoot. “I lost a lot of money, but after inflation I lost even more?” Makes for a great conversation at your watering hole. Wait till your broker sends you the 1099-INT adjusted for inflation, LOL

If anything, convert all indices to the same currency, such as the USD, and this must be done daily with the exchange rate in effect on that day, going back for all years. So now it shows a mix of exchange rates and stock prices. For local investors, this is useless. But for example, as a US investor in Japanese stocks, you’re betting simultaneously on these two things: the yen/USD exchange rate and Japanese stock prices. So stock prices can go up and the yen drops (2022-23), and in USD terms as a US investor, you may not have the hoped-for gains.

Americans bear witness to the greatest economic gains in equities, crypto, real estate, and now money market in history . If the end is near or coming most have wet their beaks and continue to prosper. Dynamic growth as I think back to March 2020, AAPL $45/share. I will miss the wisdom of Charlie Munger, and all his quotes. I welcome 2024 with open arms and optimistic view for the most resilient economy on earth.

You are correct from the perspective of a libertarian, winner, posing as if they were WW2 veterans. Neither Munger or Buffet are veterans, only the recipients.

The story of the American aristocracy who forgot who payed the price for this miracle stock market. Not one of them are enjoying the inequality.

Munger served in WW2.

“I welcome 2024 with open arms and optimistic view for the most resilient economy on earth.”

What are you drinking? Most corrupt, fake economy ever. I can’t believe anyone could look at the last two months with the casino only rising due to hope Fed will cut rates and maybe even start QE as optimistic and resilient. This house of cards will collapse, and many of us who don’t celebrate this corruption will view it with mixed emotions. If you think the next few years will continue like the last few, think again. I never understood the ability to live in that kind of denial.

Sorry your life is miserable. Hoping 2024 is a better one.

Sorry you missed the ride. Permabears never win.

My life isn’t miserable, and I’m doing well. Only problem in my life is the corruption in this horrible country and greedy permabullz like you who are complicit. You are the problem. Your ride will be ending soon, like it was only two short months ago, and I can’t wait to watch it consume you. You truly disgust me.

You don’t have to be a permabear to not like the direction the country is moving on. Some of us have children and are concerned with their future, and not just living in the present. Are you childless? Or just very selfish?

“It was a funny year for US stocks, “, is a phrase, worthy of a prize for understatement of what actually, happened. Which brings us too the obligatory new year wish (hope) so here goes

Being that there is only one way that our Darwinian, winner take all impulses haven’t destroyed us yet and that is the pollination of mankind, love.

May this year be full of the stuff.

Market prices do not reflect value. They reflect the integral over time (in the mathematical sense) of the difference between the weighted frequency of participants who believe that the marketed entity is a superior asset to all the alternatives and the weighted frequency of participants who believe that the marketed entity is an inferior asset to one or more of the alternatives. Bubbles develop and are sustained by that underlying belief being founded in a relatively recent history of price appreciation. In other words, the absolutely lunatic, capitalism-destroying notion of momentum.

Pump & dump?

Thanks Wolf!

Happy New Year and best wishes for 2024!

The index value across time are not weighted so there is no way to compare what the message the index is conveying by it’s existence.

The world monetary policy is walking on ice, afraid of withdrawing liquidity too fast and induce a heaviside dislocation in the prices of assets.

The index values are all extraordinarily overprice so it is difficult to be optimistic about capital asset prices as reality catches up with perception.

I had an “ah ha” moment with this article, thank you. It’s not that the stock market value is so high, as much as it’s that the local currency is worth less.

So where do we go from here? Any predictions?

Thanks.

Excess liquidity in the financial markets lends itself to a process of grift and graft that becomes an acceptable economic environment, predatory by it’s nature.

Markets are now unmoored from reality and the actual economy. But where are the printed piles of fiat paper Central Banks have created out of thin air? Maybe the obscene trillions in derivatives with only one counterparty. Check out David Webbs, ” The Great Taking”.

1) The BOJ raids bank accounts for deflating IOU, control the long

duration, invested at zero rates in US treasuries and AAPL.

2) Japanese houses used to be pressed paper and wood. They didn’t last long. After the Plaza Accord, Tokyo RE became the most expensive in the world.

3) The NIKK reached 39K in 1989. Sony, Toyota…Japan’s mag7 – dominated the world. In Nov 2023 the NIKK reached 33.8K.

4) India is shadowing China. China sent Japan to the back of the line.

Exogenous events might send us to the back of the line in 2024/25.

5) Happy new year.

How do the young people navigate this market ? Of course the market itself disqualifies most of the wannabee home owners on the likelihood that they will be able to afford the monthly interest payment.

There is a suspicioun that support of the housing market is a tentacle of the Fed’s operation, below market loans.

It is more likely that owners of below market loans will eventually have to sell into a market with a paucasity of buyers.

They chase meme stocks and crypto in the hopes that they have a winning lottery ticket. It’s sad and there’s no discouraging them because giving up that dream destroys their last hope of being middle class

Epic crash will come sooner than later. Fools buy at the wrong time and sell at the wrong time.

Typecheck-

Your comment about an “epic crash will come sooner or later” reminded me of a simple chart put out in the mid-1980’s (paraphrased from my memory):

DJIA declines: Occurred, since 1900:

10% from recent peak. Every 1.5 years on average

20% “ 3 years. “

30% “ 4.5 years “

40%+ “ 10 years “

I might have the numbers slightly off.

Good lesson for all investors, and especially sobering for newer participants… and perhaps drunken sailers, too.

My chart didn’t format well. Apologies.

The source of the paraphrased chart information was Marty Zweig/Zweig Funds.

Marty was like the first day trader back when if you didn’t have a seat on the stock exchange commissions would kill you. Strategic switching certainly worked out well for Martin.

The Real Tony-

Two of his many well know trading tips, often retold on Wall Street Week with L Rukeyser:

#1 “The trend is your friend”

and

#6 “Don’t fight the fed (less valid than #1)”

I saw this chart with a roller coaster explanation in the 1980’s. I was a child, and the roller coaster caught my eye, but it stuck! It reminds me that finances around stocks operate like a roller coaster. My grandparents (silent generation) warned to score stocks like a roller coaster. Stay away from ones that have no seatbelt unless I am okay with the money flying away. When the stock market is high, it will come down and never in a straight line (Wolf). Now, I am trying to figure out what to invest in, because this bubble is deflating slowly.

If the bankers are running the stock market without consequence then the other side of the trade at some point in time will be all but wiped out. When the bankers can take either side of the trade and push the other side of the trade into losing positions with their vast sums of money right or wrong, something is wrong with the criminal system in America.

We are witnessing a slow correction of asset price bubbles of both equities and property. The reckless creation of money out of nothing has resulted in the value of money decreasing, in other words inflation, with a

consequent price increase in these assets The fact that these prices are are no longer increasing despite the decreasing value of money would indicate that we are entering a new negative trend in the market How long this will last is anyone’s guess.

Financial assets are priced by discounted cash flows. 0% rates for many years resulted in significantly over-valued assets. Massive money printing finally resulted in high inflation. Inflation finally pushed up interest rates.

The return of higher interest rates, to combat inflation, means assets should be priced lower. Debt, demographics, and de globalization are inflationary.

The bigger the bubble the bigger the crash.

Exactly. As I’ve said many times on here, the last 3 months of asset appreciation would only be justified if we return to ZIRP and QE. Merely dropping the FFR from 5.5 to 4.5 ain’t gonna do it.

I believe that everything is overpriced, housing, ,meds, food, car etc. I am by no means a trader or money guy, just a working blue collar trying to figure this out. What i figured out is the game is rigged and by that, I mean when things start going south I will be the last to know. Best to pay off debt and invest money you can afford to loose. But who can afford to loose money? ARG!

Happy New Year, y’all!

RFW. I agree that there’s some “rigging” going on. I also think that the stock market is a casino, but it’s one that favors the players rather than “the house”. It’s closer to Liar’s Poker than five-card poker.

But collectively we have been led to believe that the market is safe if you just hang on to your investments over time. Is that true, going forward? Maybe not. People underestimate risk in the stock market and all other investments. Are treasured art works really worth millions?

People pay dearly to get other people’s opinions about where to invest: financial magazines, advisors, subscription advisory newsletters, etc. We’re all sniffin’ around, trying to know which way is up when it comes to investing.

But the BEST times to invest, in my life, were times when the economy scared the crap out of me and everyone else. When you think that the economy or our currency is in a state of collapse, it’s probably prime time for investing.

Like Robert Frank Walker I see a lot of things that I think are “overpriced” but I don’t know if the things will go down in price or if inflation will just keep pushing wages up. Six years ago today the CA minimum wage went from $9/hr to $10/hr. In 90 days the CA minimum wage for fast food workers will be $20 (and the Redwood City In’nOut Burger already has a sign on the door that says starting wage from $21-$24/hr).

The same thing happened to Vancouver, British Columbia when the Chinese bid real estate prices to the moon. If companies can’t pay for buses or trains to ship workers to and from work from far abroad then the minimum wage soars.

In ‘n Out always pays well above min wage. Nothing new here though there is definitely upward pressure now by a new artificially high minimum wage.

Of course it is rigged but as a society we aren’t ready to recognize the importance of society in taking care of food, water, shelter, retirement, healthcare, employment and other needs.

One could argue that moving past slavery, feudalism and related models is progress. History shows the “land owning classes” and related have little interest in society as a whole but they will make small reform changes when forced to. A push for more will occur again but these take time, organization among other things.

Stock markets were becoming the people’s widespread wealth builder. There was the American Century where if a youngster survived the obligatory wars, a decent prosperity beckoned. Now I wonder have the zillionjaires reached liftoff where they can pass around the truly valuable assets and power amongst themselves, leaving the peasants in the low reaches of the casino (nickel slots) where payoffs are perpetually microscopic and meager? The state asks little, dispenses vapor-money plus bread and circuses (marijuana permissiveness, identity esteem games). Glad I got a sliver of a few actual assets. Hope everything goes better than my perceptions here. My portfolio and my mind’s aperture are small.

Nice to see your name on a comment, phleep. Eloquent, as ever.

As Zuckerberg is building a 100$ million home in Hawaii with a 5000 sq ft underground bunker .

I think you really hit the nail on the head here. Buying into the stock market in the past meant you were buying into America’s prosperity and growing economy. Now you’re just buying into a bubble. America is no longer really growing in the traditional sense, and I think on some level, people realize it.

The pie isn’t getting bigger, the only way to get ahead is to get a bigger piece of the pie.

Happy new year Wolf & commenters!

I just want to say that thanks to your insights I was able to reduce my parents variable debt prior the rise of the interest rates.

I cannot be more grateful to you in this 2024 start.

Keep doing your thing! I love your narrative, your exactness and your humour ( yes, that kind of strange but funny ASF humour)

Cheap energy (Shale oil and gas), the growth of tech globally, perceived low inflation with globalization of the labor force , and the ability to keep inflation at bay (low energy) has provided the USA with tremendous economic growth opportunities. I did not throw healthcare into the mix but private healthcare has been a growth engine as well . Though everyone did not benefit equally from the past 60 years I still believe opportunities exist and freedom to benefit exists in the USA economy . Welcome to 2024 and I’m optimistic about the prospects for prosperity for my grandchildren. Up to them to navigate this world path they are embarking on . Happy New Year!

Great perspective article, Wolf. Seeing the anomalous performance of the US equity markets compared to rest of world suggests a “safe haven” effect.

How has foreign ownership of US equities fluctuated over last several decades, I wonder?

Your question: “How has foreign ownership of US equities fluctuated over last several decades, I wonder?” prompted me to do a little sniffing. It turns out that foreign investment in equities and debt hasn’t fluctuated; it’s only increased over time.

Here are some tidbits I came across: The U S markets are valued at ~$45.5T, 4 x the size of China’s markets. And foreign ownership is ~$5.3T as of the end of ’22. But one chart showed foreign ownership to be on a steady increase since 1985.

The largest foreign investors in order are: Japan, UK, Canada.

As of 1/21, the US owns 56% of the stocks of the entire world, Japan is second with 7.4%, China 4.4%, and the UK at 4.1%.

Warren Buffett: “Never bet against America.”

Then check out US ownership of foreign equities… That’s the other half of the issue here. US asset managers have forever been touting their foreign stock mutual funds or their global mutual funds to Americans. Financial advisories have been pushing American investments into foreign equities. For US investors, these foreign equity funds are often marketed by themes, such as emerging markets, frontier markets, Japan equity funds, European equity funds, etc. For example, US investors, including hedge funds, have been ALL OVER Japanese equities in recent years.

Then check out foreign companies that IPOed on US exchanges as ADRs… that’s a lot of US money going into foreign stocks, such as the Chinese ADRs (BABA, etc).

Then I wonder why Buffett is sitting on so much cash if he truly believes never bet against America?

The cash he’s sitting on are US dollars, not another country’s currency.

I agree on principle not to bet against America markets. The economic wealth and military power of the country ensure they remain dominant. The US can probably deficit spend for a long period of time and maintain that position.

I haven’t run the numbers, but I expect the US stock market over-performance is largely attributable to a concentration of technology stocks in the US? If technology stocks were removed from the indices, wouldn’t the charts be more comparable?

The US has done a better job supporting large innovative corporations via low regulation, IP development incentives, IP protections, low effective tax rates, weak anti-trust authority, attraction of qualified labor, etc. As a result, the most valuable companies in the world are US companies.

But…..fantastic stock prices doesn’t mean life in the US is necessarily better. Roughly 10% of the population owns 90% of the stock value, so stock market performance isn’t meaningful to society at large. Other countries may be doing a better job dispersing wealth and supporting labor.

”Other countries may be doing a better job dispersing wealth and supporting labor.”

Might be some countries doing so Bobber, but with millions from all over earth ”voting with their feet” and flooding across borders and filling up all legal venues to get to USA, it certainly appears most are not.

Since I am well aware that all the families in my background have folks who immigrated into USA at some point, I for one welcome all folks who want to come here and work hard and reap the benefits of that work, as my ancestors did.

BTW Wolf, you forgot ”Baghdad by the Bay” in your various names above for SF, a Herb Coen favorite IIRC…

Happy New Year to all here!!!

”Baghdad by the Bay” LOL that guy must have never been in either place. It’s 120℉ in Baghdad in the summer, while it’s 58℉ in SF, which changes everything, including how the city is built. Baghdad has over 8 million people, SF 1/10th of that. Between these two cities, nearly everything is vastly different. Whoever said that was an idiot.

The coldest winter I ever spent was a summer in San Francisco.

Are the long-term charts a true indicator of each country’s economies and price discovery? We can’t say so for the U.S. with 0%. Japan’s chart seems believable. China’s chart looks a bit mysterious with a continual fall after 2015. A country with 6% average growth per year until now? Go figure.

China is well known for its ability to produce fake/imitation products at a low cost. The best example of this is the country’s growing, robust economy.

I would buy anything ‘fake’ and ‘imitation’ Chinese if the price is right. The only difference between the ‘real’ thing with the imprimater and the ‘fake’ is which door of the factory it came out of, the employee entrance or the back dock.

Central Bankers seem hell bent on never letting things really decline….they prevent free market “cycles” that flush excesses and the poorly leveraged…which actually leave markets “healthier”

IMO, this became the mission since the 2008 debacle…and the beginning of QE in 2009. A complete change of attitude and mission.

The argument that 5% interest rates are restrictive seems to have fallen by the wayside with the stock rally, as well it should.

“The argument that 5% interest rates are restrictive seems…”

If they’re not restrictive — and there is a good chance that they’re not — inflation will take off again, and all the hype and hoopla about the gazillion rate cuts in 2024 are then kaput, and all this stuff has to be repriced. We’ve been through that before.

There are not many people who will alter their way of living because the rate of interest has fallen from 5 to 4 per cent, if their aggregate income is the same as before…

Perhaps the most important influence, operating through changes in the rate of interest, on the readiness to spend out of a given income, depends on the effect of these changes on the appreciation or depreciation in the price of securities and other assets.

– John Maynard Keynes, The General Theory of Employment, Interest, and Money

Friedman was only good at math.

In 1932, Milton Friedman “stopped Jacob Viner in his calculus and finally went to the blackboard and worked the whole problem out, which Viner was unable to do”…

In Mints’ class “Price and Distribution” Friedman “discovered some of the errors in Keynes’ fundamental equations.

Mints wrote Keynes on Milton Friedman’s behalf – & for the class. That Keynes admitted the errors and this gave him, at least in part, the impetus to write the General Theory.”…

”Keynes’ subsequent repudiation in the General Theory of those parts of the Treatise on Money grew out of these criticisms.”

I have to wonder if the fed actually cares about getting inflation under control or if it’s more of a going through the motions sort of thing? With the massive amount of government spending which no one’s stopping, it seems to only way out that mess would be massive inflation and thus have our debt payments relative to GDP seem far more reasonable. Similarly, with the size of our national debt would the federal reserve actually raise interest rates to say 10% if needed or would it avoid it because the size of the interest payments on the national debt? Seems like smoke and mirrors. Our politicians on both sides will do anything to avoid a recession which has led to massive spending….and the fed just has to cope with it? On the flip side, a recession would give the fed an excuse to drop rates significantly and then we can fund our govt spending at ultra low rates again.

The bubble should burst or at least partially deflate, but will either party be willing to be the bad guy and let it? Or will they just send everyone checks?

Lastly, a sign of a top is when individuals with no real investing or financial background all seem to think they’re market experts (dotcom, 2008). The number of people this past year who aren’t very financially literate who basically told me they were a real estate investing genius and their plans to buy more and more properties because they seem to think real estate will always return 20% annually is pretty significant. No understanding that buying in late 2019 was more than anything luck because without COVID and 3% mortgages prices would not have inflated the way they did. When I run the numbers in my head for their plans (former CPA and current SE so this math is easy for me) they’re just terrible ideas. I’ll ask about their current job which has done a few rounds of layoffs, and they have no concern about buying when their company is struggling because they’re just gonna buy a second property and be rich. Make another $100k real quick. I’ll ask about the fact that here in Denver there’s tons of new apartments coming online and rents are actually projected to drop, and I hear that it doesn’t matter if rents drop because the price of the property will more than double in 5 years (not realizing how rental prices will directly impact valuation) and also that while rental units used to rent is just days many of the older units are now sitting 1-2 months before renting and this is in a “good” economy. And I get blank stares like why does that matter? I also seem to get stock tips from everyone, I’ll ask about the fundamentals and get blank stares. It’s basically buy it, it’s a cool company and therefore will go up.

So should it pop and soon-ish? Probably. Will the fed or govt actually let that happen, especially in an election year? I’m skeptical.

It’s amazing the government was able to monetize $5T of government debt and register 20% inflation in three years, while keeping future inflation expectations at 2% during a time of $2T deficits.

Either investors have lost touch with reality or Jennifer Lawrence is about to kick open this Boomer’s front door.

MB-

Good comments. Many of your questions have troubled me, too. What is an “SE,” if that’s not a stupid question?

Bobber-

“ It’s amazing the government was able to monetize $5T of government debt and register 20% inflation in three years, while keeping future inflation expectations at 2% during a time of $2T deficits.”

Excellent point. Didn’t the 1960’s experience a similar “simmer” stage of inflation. Reported inflation would kick up, then recede. The inflation didn’t get on to a full “boil” till the mid-70’s. In both the 60’s and 70’s, inflation expectations became progressively more “cooked” into market participant’s psyche each time inflation hit new highs.

And I believe this was the era where COLA’s came into common usage, or at least got lots of press. “Inflation expectations” in a contractual covenant…

Bobber, that’s a great point. It’s almost as though investors buy the “Yeah, the 20% in three years was due to a once in a lifetime pandemic, and it’ll never be repeated again.”

I agree that it won’t be repeated again because of a pandemic, but I’m sure the Fed and Congress can come up with some other “emergency” to justify a helicopter drop of money and consequent printing. So if investors are willing to buy 10 and 30 year bonds at 3.8%, they’re basically saying that they have confidence that no other “emergency” (again, using scare quotes) will manifest itself in the next 10 or 30 years.

That seems like a risky proposition to me.

Happy New Year Wolf and fellow readers!

I believe the correct lens to view market index for countries is to ask the following:

1. How are demographics trending? Is the population increasing consistently? Look at Canada. They are getting a lot of qualified immigrants that are highly educated because of their targeted immigration policy. This will generally lead to long term growth in GDP and prosperity in the country. In general, this should lead to higher stock index over the long term.

2. Does the country have the freedom to issue large quantities of debt? Look at the US. As long as this capacity exists, it is hard for the economy to tank and remain low for long periods (decades for example). Business cycles are normal and we will see recessions every five to fifteen years. That is totally expected. US is also growing in population although it is arguable if the immigrants are as qualified as Canada.

The capacity for the US to issue cheap debt is not unlimited. I understand that when that changes, things will quickly go south in the US. I don’t know how far we are from that point though. It may be decades. I say this because I don’t see a viable replacement for US treasury in the near future. At least this decade.

Canada may have qualified immigrants but Canada’s job makeket sucks big time.

Canada is doing OK all because of natural resources.

“Look at Canada. They are getting a lot of qualified immigrants that are highly educated because of their targeted immigration policy.”

McDonalds, Tim Hortons, A&W, 7-11, thank the Canadian Government for all the MBA’s, MA’s, PhD’s with entrepreneurial skills to expand the taxable economy?

The Canadian Economy, like most Western nations, have depended on borrowing against assets and “the full faith and credit” of future taxpayers.

More immigrants to live in the shrinking spaces in the Vancouver Lower Mainland and Southern Ontario, because very few want to live in the freezing cold.

Winning/s

This will generally lead to long term growth in GDP and prosperity in the country. Are you kidding me? Every GDP report that comes out of Canada that puts the GDP at 0 or positive 0.1 percent is a negative report doctored for whatever reasons that be. Canada is predicted to have the worst growth rate out of all G7 countries for the next decade. The productivity rate in Canada is in a perpetual freefall until we end up with countries like Grenada in the near future.

So why are you sticking around?

I tend to agree. Being in my mid 50s I don’t expect too many changes from now through the rest of my working years and into retirement. That isn’t to say there won’t be periods as always have ups and downs but corrections will recover. Even my teenage son might be okay. Kicking cans down the road seems to be an American specialty. Given all the economies that are struggling hard to see a different option. That said, while the US markets and treasuries seem safe I wouldn’t say that translates to quality of living of US citizens however. There is no appetite to significantly reduce military spending or tax more to invest in the overall health of the society. Not investing in healthcare and education, for example, only hurt a society over time.

If you are economically successful and ambitious in Canada then you move to the US. For a number of reasons this is easier for Canadians than for people from other countries (specifically: the TN visa category makes it cheap/easy to get a work permit, and is part of USCMA and therefore only available to Canadians and Mexicans; and if you want to move permanently, the most-common EB-3 green card category has a per-country cap that tiny Canada can never fill, vs China and India whose caps are filled for the next several decades).

Canada is also a fairly rich country and culturally seems to look down on the US, which is completely unjustified but discourages Canadians from moving south if they don’t think too hard about it.

All this to say that there is a pretty-big braindrain from Canada to the US, and this includes braindrain of recent Canadian immigrants. So I can certainly believe that the average Canadian immigrant is more successful or valuable than the average US immigrant, but this value will find its way to the US eventually.

(This is all somewhat anecdotal. I grew up in Canada and everyone ambitious I know is either in the US or chafing at the Canadian system. I could pull out stats about how “1% of everyone in Canada has a work permit for a Bay Area company” or “16% of all Canadian scientists move to the US at some point in their lives” but I’m not aware of any real statistical smoking gun describing this dynamic.)

Joined the drunken sailors for a night out on the town. I’m helping boost the GDP. Noticed the place we went to (Clydes) was packed and you needed reservations to get a table. We sat in the bar and watched all the football games. Based on my anecdotal evidence, I don’t see any recession in sight. 2024 will be more inflation, deficits, wars and same old, same old. The more things change, the more they remain the same.

Happy New Year!

Howdy Swamp Creature. How dare you enjoy life and do exactly what you want to do…….

Howdy Folks and Happy New Year. A new years resolution tip ? Get out of debt this year and you will prosper. Have a Mortgage? Sell the house and purchase less of a home that needs lots of work. Bust your a$$ and get out of debt. Govern ment will also then hate you for doing that and that is a good thing. Invested in the stonk market? Don t…………

Agree with you!

Why buy a smaller house that needs a lot of work? Why pour dollars into fixing it up when you will mostly break even when selling it? Use your time a better way.

Buy a small, cheap house like I did and just pay utilities as all of the house is NEW!

Buy an electric car and keep it forever. Get a “Time of Day” utility rate like I did and pay only $0.04 per kWh for power. Then the EV runs on CHEAP electricity (charge on off hours).

My formula (now widowed) is:

Cheap, paid off house,

Low utility costs,

Paid off car,

NO loans or other debt,

No new wife (LOL),

Eat healthy.

Exercise regularly,

No Booze or smokes,

Get check ups on a schedule.

Happy New Year to all here!

Wolf, thanks a million for your hard work!

One more step, Anthony: cut out fish, meat and dairy.

Anthony A.,

You said, “Get a “Time of Day” utility rate like I did and pay only $0.04 per kWh for power. Then the EV runs on CHEAP electricity (charge on off hours)

This makes excellent sense!!!

Maybe even rig the car battery into feeding back into household energy use during higher rate times?

Thomas, my Chevy Bolt is not equipped to back feed battery power but I believe the Ford F150 electric pickup can do that, or at least power your house in a power loss event. Good idea, though.

For me to get Time of Day (TOD) rates, I had to have a “smart power meter” supplied by the utility, have a gas water heater, a gas stove and gas furnace. All of those appliances were in the house, including the smart meter. So, I applied, and was granted the TOD service. I would guess most large utilities off this lower power rate for folks that have EV’s.

Many people who have EV’s and charge at home look into getting this reduced rate service from their power provider.

Howdy Anthony. Some folks make a great living by rehabbing RE. You need to know what you are doing and why. Most are not willing to work that hard.

Alternate idea, along the same lines: buy solar panels for your home, and then your electricity is free. That’s what I did last year.

You can even charge your EV with your free solar electricity if you’re able to charge during daylight hours.

“Have a Mortgage? Sell the house and purchase less of a home that needs lots of work.”

Howdy DFB: I generally agree with your sentiments, but the problem with this advice is it will cost *more* to downgrade for folks with a low rate mortgage.

Case in point: I couldn’t even afford to buy my own home if I were in the market today.

Great article to start the year and stay grounded. Wealth is a passing illusion based on the time period one chooses. At the end one’s life experiences are the only true wealth.

Wish you all happy, healthy and prosperous 2024!!!

As a Canadian investor I’m confused by your data for Canada. You note the TSX is back to where it was in 1998. Your chart doesn’t go back that far but I seem to recall that the index was well below 10,000 at that time.

Perhaps dividends explain this, I have trouble accounting for them when looking at index data.

That line shouldn’t have been there. It got tacked on somehow, and I didn’t catch it last night.

Can you imagine where the TSX or former TSE would be today if an honest stock market was ran in America throughout the decades? The TSX would still be well south of 10,000 today. I recall Ben Bernanke saying something to the tune of “backstopping any losses in the stock market” when that made the news back in 2012.

2024 is starting out as the year of Earthquakes and Japan just had a 7.6 in central Japan a few hours ago and Southern California just had a 4.1 off the coast of the Palos Verdes Peninsula in this active Ring of Fire new year with lots more to come as the year progresses.

Yep, I live in Palos Verdes and my earthquake alarm went off quite nicely.

October 24, 2024 the 4 large planets square with Earth like 79 AD.

We had a 2.7 earthquake in NH on the Friday before xmas.

Hi Wolf, Happy New Year. Many thanks for the work that you do, your blog is the best out there. There was the conversation recently in this blog about “real estate for the long haul” (the comments included some bears sort of capitulating): could you do a similar post as this stock market post, but for real estate markets?

All of the Western markets with the exception of Spain have had big run ups from 2009.

My thoughts:

Don’t fight the FED remains in effect.

Picking sectors and individual stocks will be more important without zirp.

Hedging nimblely using puts and calls and or shorts will be more important if geopolitical conflicts increase in frequency as seems likely.

In total the markets will favor traders more than they did under zirp.

TC: I look forward to buying stocks when picking the correct ones will actually be rewarded.

Before exiting most of my positions, I did well with microcap companies – those with mkt caps so small that funds & pro investors couldn’t touch them. Its also much easier to get in touch with the execs at these companies to ask them questions.

It’s nice to see other stock markets around the world aren’t rigged and manipulated to the bull’s tits like the U.S. stock market. Hopefully other countries around the world will follow the lead of Iceland and lock up the bankers for criminal activities aka stock market and commodity rigging.

I once thought as you do Wolf. I was 10 yrs early and lost out on a lot of returns.

Funny reading this article as a Canadian. We usually think of the TSX as a crappy index because its returns suck compared to the S&P — but comparing to pretty-much any other major index, it’s pretty great!

TSX is a typical stock exchange, nothing but a corrupt old boys club.

Other stock markets don’t have the famed Drunken Sailors doing the paddling. That’s the biggest difference. Other drivers keeping the US stock market special include Reddit’s Wall Street Bets, punters like Chamath Palihapitiya pushing dodgy SPACs, (former) Madam Speaker making a fortune trading options that’s like mathematically impossible, and of course the Fed with its plethora of alphabetical schemes bailing out pretty much everyone.

May want to add the wall street crowd manipulating various and sundry stocks to pay off the corrupted politicians in our congress who can trade with impunity from prosecution for insider stuff the rest of us go to jail for, eh?

Wall street also seems to be able to pay ”advances” on yet to be written books by those same politicians when they need cash more rapidly than stock manipulations can provide.

Very interesting Wolf.

What about total returns? The UK FTSE for example has a very different long term returns chart when you include dividends.

A great article, from the viewpoint of currency devaluation. A pleasurable read, to start the out right!?!

Yes, we’re special. We have the Fed Put.

US stockmarket in 2023 rose on AI optimism.

This is a great illustration of why my international equity portfolio (which I have been averaging into for about 20 years now) purchased on behalf of my children has been performing so dismally. The premise was to maximize diversification, given that all of the non-equity assets are either Canadian or in commodities. Fortunately the other 50% of their equity position is in US markets, so the whole thing hasn’t been a complete disaster.

I suppose it’s possible that the diversification imperative could pay off in some unforeseen way, but right now with the benefit of hindsight it looks to have been a bad decision.

Hi.

Been enjoying the articles and discussions on this site. Great job!

The S&P500 and Nasdaq are near all time highs set in 2021. In 2021, the S&P500 had a P/E of I think 14ish. Today the P/E is about 25ish. I notice a few years ago S&P having envy of Nasdaq and started ripping out solid income generating stocks and stuffed it with high growth(inflated p/e) stocks. So the index is indeed back to that number but the number is inflated by its p/e. Do these gains hold weight? This looks more like financial engineering by wall st. I can see why the casino reference, oh and our friend 0dte. Trading going forward will be interesting we had zirp so long I don’t think anyone knows how to trade in a non zirp market. Market should rebalance since companies are paying dividends below new treasuries.