Hitting all his hot buttons today with the month-to-month PCE price index.

By Wolf Richter for WOLF STREET.

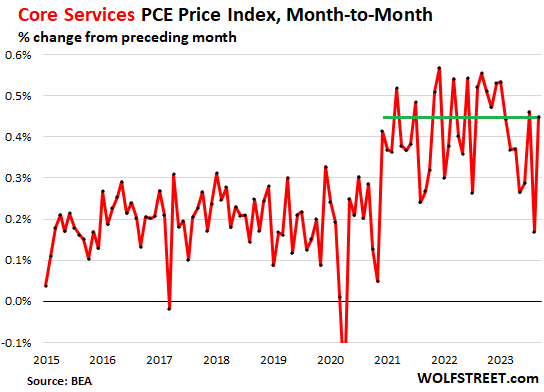

The spike in inflation in “core services” (all services except energy services) was the big nasty surprise – inflation is infamous for dishing up nasty surprises – in today’s release of the PCE price index for September. “Core services” is the index that Fed chair Jerome Powell has been hammering on, especially “core services without housing” because housing inflation is already coming down, and it’s just lagging etc., etc., and so the other core services were in his focus because their inflation rates sort of refused to come down.

But in today’s installment of our inflation soap opera, the nasty surprise was driven by – fake laughter in the background – a spike in housing inflation. And it came on top of some nasty spikes in some of the other core services.

So the “Core Services” PCE price index spiked by 0.45% in September from August (5.5% annualized), driven in part by the spike in housing, and in part by even bigger spikes in three of the remaining six core services categories. Note the head-fake deceleration in August:

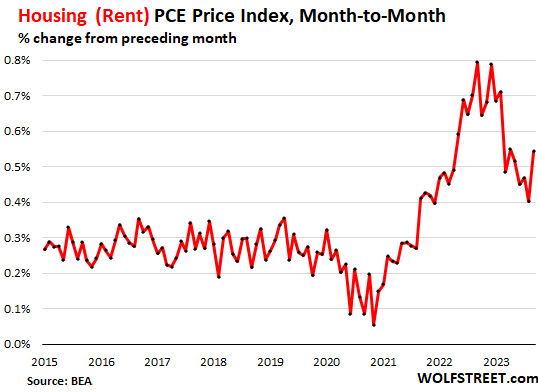

Housing.

The PCE price index for housing, which is composed of various rent factors, spiked by 0.54% in September from August (6.7% annualized).

This brought the 6-month average to over 6% annualized. That’s still down from the red-hot raging rent inflation in 2022 which topped out at 10% annualized! But 6%-plus annualized is far hotter than hoped for. Year-over-year, the PCE index for housing decelerated to 7.2%. All of it confirms what big landlords have been saying this year, that they’re getting 6%-plus increases on renewals and new-lease signings. So that’s where we are, 6%-plus rent inflation.

The seven “core services” categories.

Housing inflation was a big driver in the core services spike. But that’s only one of the seven core services categories. Three categories had even bigger month-to-month spikes than housing; two rose more moderately, and one dipped:

| Core services categories | MoM | Annualized | Includes |

| Transportation services | 1.80% | 24.0% | auto repair & maintenance, auto leasing & rentals, public transportation, airfares, etc. |

| Food services, accommodation | 0.84% | 10.6% | meals & drinks at restaurants, bars, schools, cafeterias, etc.; accommodation at hotels, motels, schools, etc. |

| Recreation services | 0.64% | 8.0% | concerts, sports, movies, gambling, streaming, vet services, package tours, etc. |

| Housing | 0.54% | 6.7% | rents |

| Finance & Insurance | 0.31% | 3.8% | fees & commissions at banks, brokers, funds, portfolio management, etc.; all kinds of insurance |

| Non-energy utilities | 0.23% | 2.8% | water, sewer, trash |

| Other services | -0.04% | 0.5% | a vast collection of other services |

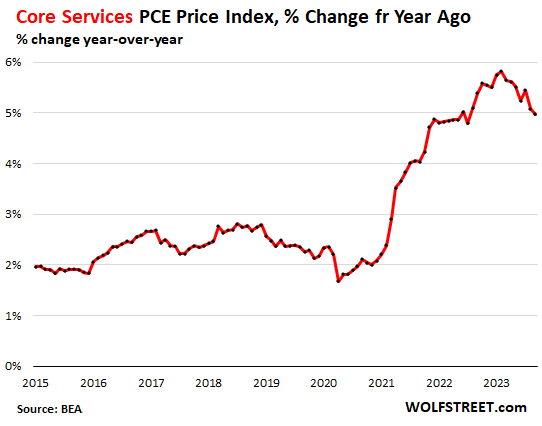

Year-over-year, the core services PCE price index decelerated to 5.0%, in part due to the base effect, given the red-hot spikes last year at this time:

Powell is going to talk about this at the press conference.

That’s exactly the data he is looking at and talking about. He has been talking about it for over a year because the index for core services without housing has been one of the frustrating elements, where inflation has gotten entrenched and is hard to dislodge from.

And now housing refuses to do what it was supposed to do and was expected to do – vanish as a source of inflation.

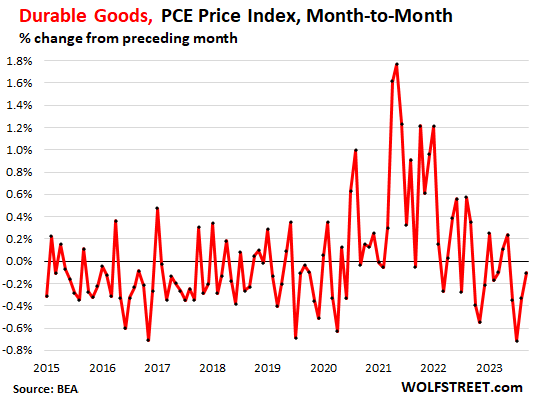

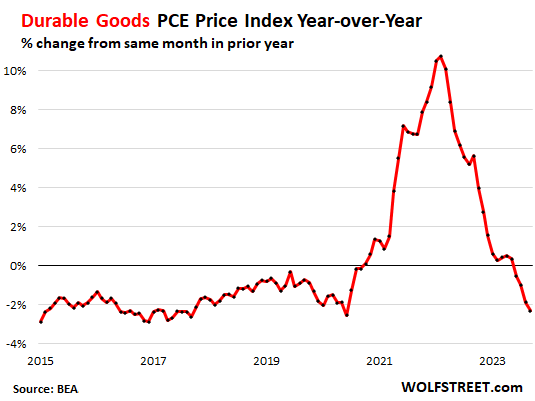

Durable-goods PCE price index is normalizing.

But the durable-goods PCE price index changes are still negative, driven by motor vehicles which dominate durable goods:

- Durable goods: -0.1% MoM; -2.3% YoY

- Motor vehicles 7 parts: -0.84% MoM; -1.4% YoY

- Furnishings, durable household goods: -0.38% MoM; -2.7% YoY

- Recreational goods and vehicles: +1.2%; -4.3%

- “Other” durable goods: -0.81%; +0.6%.

Year-over-year, the durable goods PCE price index fell 2.3%. The natural state for this index is with negative values – as we’ve seen in the years before the pandemic. This is a result of manufacturing efficiencies, offshoring, competition, and “hedonic quality adjustments” that remove the costs of improvements, on the principle that consumer price inflation is the change in dollars to buy the same product over time, and the costs of improvements to the products are not inflation. Here is my explanation of hedonic quality adjustments.

Prices of durable goods are still high but are coming down from the ridiculous price spikes of 2021. The dynamics are particularly driven by used vehicles, whose prices have been dropping for over a year, though they’re still way too high:

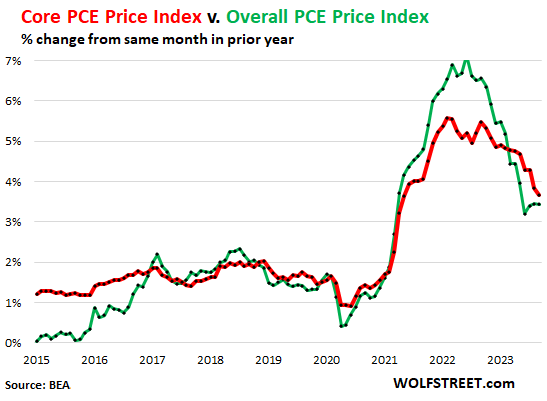

The core PCE price index re-spikes.

Driven by the spike in core services, minus the drop in durable goods, the core PCE price index, which excludes food and energy products and services, accelerated to 0.30% in September from August, the biggest increase since April,

Year-over-year, the “core” PCE price index, decelerated to 3.7% (red line). The overall PCE price index remained at 3.4% year-over-year, as food and energy prices ticked up moderately:

- Energy prices: +0.20% MoM; +1.8% YoY

- Food & beverage for off-premise consumption: +0.30% MoM; +2.7% YoY

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Gutless Powell isn’t going to raise IMO. Not with so much debt being issued. Remember, his main job is protecting the currency/govt and the banks.

We need deflation big time, not just disinflation but this country is committing suicide in every way conceivable so a collapsing economy might hardly be noticed when we get to the point that over half the population is either playing a video game, hooked to a dialysis machine or a homeless fentanyl zombie.

If he doesnt raise that will mean long term rates might move above 5%. I have seen written elsewhere that if the 10 year moves above 5%, that will be a line in the sand for markets and equities will plunge (even more).

I actually think that Powell is doing the right thing here. He doesnt want to raise too aggressively, see inflation fall, reverse course and cut rates and then see inflation rebound. This is kind of like oversteer for a car, you have to be careful about over-adjusting, or you just get into a fishtail where things go up and down rapidly. Slow and steady tightening.

The longer they are able to keep rates high and continue QT the better in the long run. They really need to liquidate at least another 2 trillion from the Fed balance sheets.

What will tell me if Powell is doing his job is if once recession starts, he keeps QT going, even while lowering interest rates. He needs to come out and say that if long term bond rates are going wildly higher, the politicians need to balance the budget, that is the solution, not more Fed purchases.

Japan might be hitting a wall finally with their policies. I’m looking at the Japan carry trade as potentially getting hit hard and the Yen reversing higher as they finally allow interest rates to rise.

My bottom line is the more central bankers lose control, and admit it, the more stable our will eventually become (after initial turmoil). Let the markets sort out all prices and focus on true price stability (not these fake inflation numbers that include hedonic adjustments on everything).

One has too consider at least two scenarios about the current long rate.

Firstly, is it the free market rate that would be, in the world that I was led too believe, was a perfectly competitive market or secondly, a manipulated market ?

Thanks Wolf for presenting the components of the Keynesian macroeconomic measurement of the wealth of the American nation.

The atrocious trade deficit being hidden by the deficit spending by the drunken congressional sailors. Not exactly a bill of health for the future even though it feels good today.

dang…

Indeed.

What would long rates look like with 2.45 Trillion of MBSs not hidden on the balance sheet and out there looking for a bid? Not to mention the other long term paper held by the Fed.

The Fed’s “thumb” on the scales since 2009.

Why are everybody’s eyes fixed on the FED’s balance sheet?

Yes, some thing are hold to maturity and go of the books in oblivion. But most things are sold in the market. In other words: are now on somebody else’s ledger and are still a liability, although most think they own an asset. If the FED is shedding them, they are probably liabilities.

“Let the markets sort out all prices and focus on true price stability”

Hmmm….whether to laugh or cry. You, like I, learned Free Market Capitalism, competition, many buyers and sellers, from a textbook.

America is a nation of Monopolies and Oligopolies, seeded and supported by control of money by a few hands, and/including the Fed.

No where in the real world are funds available for increasing competition, for all money flows to more and more control and less and less annoying competitors.

GameTV

I don’t have arguments against what you are saying other than the Fed doesn’t create money, it just encourages the creation of it by lowering the rates. Money is created by new loans and as you can see from the Fed’s own M2 that isn’t happening.

This is a psychology thing. It is like that old saying that you can lead a horse to water but you can’t make them drink, inflation is partly psychological but borrowing is also mathematical. The high prices of real estate and vehicles was already at extremes where many (maybe most) people couldn’t afford to purchase them even at the low rates.

What needs to happen IMO is for the prices to come down a lot. This then affects the money supply which will continue to create a liquidity problem. That will continue to put pressure on interest rates. So higher for longer may actually be out of the Fed’s control at this point.

econnicminor..

“the Fed doesn’t create money,”

What do you call it when the Treasury issues new debt, and the Fed goes in and buys that debt? That is new money in the system, money that wasnt in existence prior, created by the Fed absorbing the cost of the security and putting it on the balance sheet.

economicminor

“the Fed doesn’t create money, it just encourages the creation of it by lowering the rates. Money is created by new loans and as you can see from the Fed’s own M2 that isn’t happening.”

There are two concepts in this sentence. The first is totally wrong; the second is mostly correct but requires some elaboration.

I normally just delete this BS about the Fed not creating money with QE. That stuff is just complete BS, and everyone knows this by now. But because it’s you, I will explain it to you with the forced patience of the exasperated, and your next comment with this statement will go into the auto-shredder.

1. The Fed creates money every time it buys anything or pays for anything; and it destroys money every time it sells something or gets paid for something. Period.

You can see this by the simple fact that the Fed’s balance sheet doesn’t have a “cash” account. Every balance sheet, right at the very top, has a “cash” account, except the Fed. It doesn’t need one because it creates and destroys money (cash) as a matter of routine; and does not put this cash into a cash account, and doesn’t draw it out of a cash account because it doesn’t have a cash account.

So, when the Fed spent $4 trillion in cash in two years to buy securities from the primary dealers, it created these $4 trillion in cash and sent this cash to the primary dealers by depositing it into their reserve accounts, and they then took this $4 trillion in cash from their reserve accounts and bought more securities with it; and so this $4 trillion was out there getting shuffled around endlessly between buyers and sellers of securities, driving up asset prices.

And now under QT, as it gets paid for the securities that are maturing, it destroys the money it gets paid. And since it buys hardly any securities back, and only when the runoff is over the cap of $60 billion for Treasuries, it therefore destroys most of the cash it gets paid.

Since the beginning of QT, the Fed has destroyed $1.1 trillion.

2. The banking system as a whole creates money based on rising collateral values (asset prices) and more collateral (new homes and factories being built, for example). It’s rising collateral values and more collateral that drives rising loan amounts which become deposits for the recipients. Which is how money is created.

Assume that a homeowner paid $300k for a house 10 years ago. Now he sells it for $500k. He gets the $500k cash from the sale, including the $450k that the buyer borrowed by pledging the house as collateral. The seller deposits $400k of the $500k into his account, and deposits $100k into some lender’s account to pay off the existing mortgage. And then the money moves from there. Rising home prices made it possible that the collateral values are higher, and that the loans are higher, and that the amounts that get deposited into accounts are therefore higher. Which is how money is created.

Money creation turns into money destruction in the banking system when leveraged assets (homes, CRE, etc.) decline in price substantially enough for long enough.

So, the banking system as a whole creates money and destroys money automatically with the ebbs and flows of collateral values (asset prices) and the rising amount of collateral (such as new construction), that the system as a whole lends against. Higher asset prices create bigger deposits when the assets are sold, and that money comes from the buyers’ loans. This is how loans turn into deposits in the banking system overall.

Individual banks do not create money when they lend money. They have to have cash to lend. When they run out of cash, they collapse, as we have seen with SVB, etc. Or the borrow the cash from the Fed of the FHLBs, to avert a collapse. Simple as that.

Wolf.

Sorry, it is to easy to get lost.

OK #1 accepted, the Fed can and does create and destroy money in the system.

The Fed is the entity that created inflation thru QE and is the entity that has to eliminate it using QT.

I thought their mandate was to stabilize the monetary system, not a funding mechanism for the government?

Still as the money supply declines unless the demand for borrowing also declines at the same rate, doesn’t this drive interest rates higher? Supply and demand?

And because of this relationship, when the Fed pivots, if it increases the supply of money above demand, interest rates will go back down.

It appears that if he doesn’t raise rates again, getting the stubborn core inflation is going to be tough to lower. Certain energy prices are coming down because demand for gas is going down and this winter, natural gas is supposes to stay in the 2-2.50 per thousand cubic ft vs. 10.00 last winter after the bans in Europe took place on Russian oil. Powell has to keep course or all of this pain may be for naught.

Nintendo is coming out with a combination mobile gaming console and dialysis machine with optional fentanyl iv drip attachment.

The hedonistic quality improvements of the fentanyl IV drip attachment will result in deflation even though the console is pricier, since the attachment is priced below cost. We can finally lower rates again!

Lol, good one! Give that man a raise – but make sure it’s well under inflation!

If Powell and other central bankers aren’t unionized, they really should be. What about their livelihoods. Those poor bankers…

Exactly.

The 2% self authored Fed goal….for the past 2.5 years would yield a 5% increase in prices.

Yet, by the least of measures, we have 18% in that time frame, so a return to 2%, if it ever happens, still leaves the circa extra 13% baked in….

Yes we need DEFLATION to remove the 13%.

I don’t want deflation of fixed assets (commodities are ok) that can be much worse than inflation . Reason is that’s what debt loans and salaries are based on return on investment. Deflation can be more difficult to control than inflation . Banks housing vehicles land businesses salaries the list goes on .

Price stability please.

The main problem, 50% worse in Canada, is the inflated price and rent of the key ‘fixed asset’, real estate. Without a substantial deflation of RE, to make up for the excess inflation of the last few years, rents will continue to strangle the young and not so young. I say ‘rent’ instead of mortgage payments because most middle- class younger people have given up on owning.

The lowest real interest rates in centuries…one UK banker said in 5000 years!, have created an addictive price bubble in the main thing people need, a place to live. There is no alternative cure but deflation in RE. No one said ‘cold turkey’ was fun.

“I don’t want deflation of fixed assets”

Easy to say for one who already owns said fixed assets, while having total disregard for those who are in the market to acquire said fixed assets (ie. a house) but are locked out due to obscenely inflated prices.

Price stability is only useful if the prices are already low. Let’s have price stability after the crash.

Actually, deflation is the goal of the competitive market hypothesis. The Great Depression was not caused by deflation. It was caused by the collapse of a speculative financial asset bubble that resulted in the deflation of asset values.

In that version, the fall in price of overvalued asset values is defined as deflation while the increase in price of products is defined as inflation.

Carlos,

“Easy to say for one who already owns said fixed assets, while having total disregard for those who are in the market to acquire said fixed assets (ie. a house) but are locked out due to obscenely inflated prices.”

Easy to say for someone who doesn’t own anything yet, and didn’t have to scrimp and save for a couple decades. Sounds like you have total disregard for those who have.

If you only ever let prices go up, no matter how catastrohically, and never allow them to deflate even a little bit to compensate, that’s not exactly price stability.

Price stability has been lost.

Housing for example went up by 60 percent in last 3 years.

If you are talking about price stability then let the prices go back to 2019 level.

Yes for price stability.

Bs ini-

“Deflation can be more difficult to control than inflation.“

Price stability, by definition, means short-circuiting the market mechanism by direct (price fixing and government market participation) or indirect (e.g. subsidy, regulatory controls, tax policy).

Such activity, with 12-year rate repression fiasco at the top of list, is what got us into the price bubbles and debt problems in the first place.

Are you (and others here) seriously arguing that more stabilization policy is the route you support?

Sheesh!

“Deflation can be more difficult to control than inflation ”

Who has EVER seen deflation? And , who says it is difficult to control?

Inflation and deflation are both positive feedback loops.

Prices are going up? ” Buy now, before prices go up more!” Prices go up more.

Prices are going down? “Don’t buy today because things will be cheaper tomorrow!” Prices go down more.

There’s a limit to how much money people have so there’s a limit on the positive inflation feedback. But there’s less of a limit on how much people can delay buying so there’s less of a limit on the deflation feedback.

That’s why a deflationary spiral is worse than an inflationary spiral.

On top of that, deflation makes debt more expensive so governments really, really, really try to avoid it.

“Yet, by the least of measures, we have 18% in that time frame,”

No, not very close.

The PCE price index, which is not even “the least of measures,” is up 13.3% over the 2.5 years.

The core PCE price index is up 12.1%.

In return, you got wage gains, SS COLAs (higher than PCE inflation over the 2.5-year period), and interest income (also now higher than PCE inflation.

Careful what you wish for: If there is prolonged consumer price deflation, of the type you want, such as -18%, your wage will go down, and your COLA will be 0%, and your interest income will be 0%, and your stocks crash, and you may lose your job.

Asset prices (housing too) can deflate just fine without causing too much trouble in the economy; rents can come down too as long as other prices rise to not cause a long period of deflation. There are always some prices that decline, and rent could fall into the category, in theory. But right now, rents are not at all in the mood of declining.

Rents aren’t going down, even if we have a recession. Free month’s rent, free cable tv for a year… maybe. nd that’s a big maybe, and maybe in a year or two.

For the last year Ive been saying we need minimum 7% to kill inflation. Real estate has a fatal bullet through the heart and is running on adrenaline, soon to drop dead, but everything else is out of control.

Look back to the 70’s/80’s. When inflation was 14%, it took 18% fed funds to kill it. With inflation at 5% we need minimum 7% fed funds to cause a recession and reset. This may take a year or two also, or a big stock market reset.

“you may lose your job” etc.

I don’t have COLA, my wages don’t matter because I can’t afford anything anyway, doesn’t really matter if my stocks crash and I’m sick of my job!

Actually this sounds great! Pull it!

😍 I knew I’d get a response like that

Generic COLA for All!

And you’re gonna like it.

Have you thought much about the massive disconnect on PCE expenditure growth for shelter and the values? And the fact more than 2/3 of all mortgages were originated at these values 2021+? I think there is more risk here than officials appreciate. Lenders / investors appreciate it, the 300bps spread over the 10 year proves it.

“No, not very close”

Going by the CPI, a very flawed metric as noted here (what I meant by “least”)….inflation is up 7% in 2021, 6.5% in 2022, and 3.7%.

I did not suggest that prices roll back 18%, but said 18% minus that 5% representing the Fed’s “goal” leaves 13 % overshoot. A resumption of 2% inflation, leaving that 13% in, hardly seems a “victory”.

“Least of measures” may have been misleading. Many feel the CPI understates REAL inflation. That is what I meant.

CCCB says rents are going down.

They already ARE in many places from what I just read. Is Google misleading me ?

Washington state down 7% July 2022 to July 2023 I read. Seattle area more so.

Austin, Jacksonville, and a number of other large cities down YoY. Typically 3 to 4%.

Too much misinformation throughout US media. Or is it disinformation ?

You’re citing “asking rents.” Asking rents are the landlord’s hope-and-wish-list. Few tenants actually pay asking rents. In 2022, asking rents spiked by 18% nationwide, while actual rents that tenants actually paid increased by 8%, which confirmed what the big landlords were saying in their earnings reports (+8%). So that tells you. Now asking rents are coming off that fictitious spike, while actual rents that tenants are actually paying are increasing in the 6%-plus range.

Yes, agreed, lots of misinformation being circulated by people who don’t know better, and who REFUSE to read my CPI articles where I explain the difference between asking rents and actual rents.

I meant to write

“CCCB says rents are NOT going down”.

Deflation is order of magnitudes worse for an economy than inflation. Ideally perfectly balanced prices are best, but since deflation is so much worse, the central bank aims for %2 inflation as a way of adding a margin of safety to avoid deflation.

The reason that deflation is so much more insidious than inflation is that true deflation involves people having to take a pay cut to do the same work. No one wants to go through that. Employers don’t want to have to tell employees that their pay is being cut. Lowering pay is bad for morale. Plus, it screws borrowers. Imagine the millions of people who took out mortgages on their house having to pay back those mortgage payments with deflated dollars. That is just brutal for an economy. Economy wide deflation is just bad all around.

It appears that you think that since past inflation targets have been missed (on the high side) that deflation is needed to make up for it.

That may naively sound good, but it will never happen. Never. No central bank will ever flirt with economy wide deflation. It is that bad.

The past is the past. Let it go. It is not going to be undone. It can’t. Just do the best that you can looking forward.

Wow half of the country thats impressive and wrong

So, when will they pivot, like next month? QT has done the job, no need to tighten further. Please? Pretty please? I say 6% 10 years before I nibble.

“Turn those machines back on!”

-Mortimer, Trading Places

HH, didnt you read that “transitory” and “pivot” are no longer in the fed vocabulary?

Patients pilgrim, the 6 % interest rate that you desire is more likely to be, only, the opening bid. Stay short treasuries.

“And now housing refuses to do what it was supposed to do and was expected to do – vanish as a source of inflation.”

I continue to think housing prices are a little stickier than people want to believe and there won’t be a drastic reduction in prices without mortgage rates significantly higher than historical averages for much longer.

Wait a minute… these are NOT prices, but RENTS. There isn’t a lot of connection between prices and rents.

Here is my infamous chart of the Case-Shiller home price index and the CPI rent index OER. See?

LOL, you got me on that one….but I think the sentiment remains for rents too. Home prices may be more volatile, but there is an obvious correlation and it has to be a factor, same with increasing interest rates. Add in increasing demand and increasing property taxes, I don’t see how or why rents would not be inflationary.

I think the bigger take away from your graph is that rents will continue to rise even if home prices don’t.

Agreed.

There is tools to deflate the real estate. Double the taxes to 2nd or non residential property, vacant properties, investment properties. IRS must do better job chasing hidden rental income, believe me where I live everybody is renting out cottages and no one is declaring this income!

Junkmail, those are good starts. Additionally, Congress should retroactively adjust all 3% mortgages to 6%, and simultaneously remove the power of the judiciary to rule such an action unconstitutional. That would cause a wave of foreclosures, and a housing correction, fast.

“Additionally, Congress should retroactively adjust all 3% mortgages to 6%”

Congress doesn’t have that power. There’s this pesky thing called “contract law” that interferes, Comrade Einhal.

Contracts don’t constrain Congress. Contracts are voided as contravening public policy ALL THE TIME.

Congress arguably didn’t have the Constitutional authority to guarantee mortgages, but it did it, and here we are.

Einhal…just speculating: I don’t think that would be salubrious for the health and welfare of Congress critters.

Again, Just thinking out loud, but it was my take-away that the prevailing consensus was “let market price discovery govern” – not gov’t interference that is demonstrably incompetent.

Let’s be honest here: first there is irresponsible Fed policy for years (ZIRP, QE). Then there is atrocious accumulation of debt by the Federal gov’t for years up to the present.

Does anyone seriously believe this hasn’t been intentional – vice mis-calculations?

Consumer “drunken sailor” behaviour is an outcome…not an input.

ChS,

I think you missed the fact that housing prices influence rents, but rents do not influence housing prices. If the cost to purchase a home decreases below the cost to rent the same property, rents will begin to decrease. Not immediately, the vacancy numbers may increase first, and there will always be those not in the market to purchase.

I’ve been leasing single-family homes since 2011, and have yet to rent to someone looking to purchase a home in this area.

Remarkable, and apparently convenient, that the Fed uses such a lame “survey” when hard data is available.

BS. The red line (rents) is survey based (OER) for rents. Rents that are actually paid by tenants is based on a survey of tens of thousands of rental units across the country, with tenants coming and going. Each unit receives the survey every six months, and whoever lives in it says what the current rent is. So that’s how actual rents are being tracked. That’s the CPI rent measure. OER very closely mirrors it.

Don’t you ever read my articles? Or do just read the comments? It’s really a waste of time to have to re-explain all this in the comments.

But you said

“these are NOT prices, but RENTS. There isn’t a lot of connection between prices and rents.”

I said “Remarkable, and apparently convenient, that the Fed uses such a lame “survey” (referring to OER to determine house prices), when hard data (Case Shiller) is available” referring to determining the cost of home prices. I think that is a statement of agreeing WITH you. I could have been more clear.

And I do read the articles.

Wolf,

If the CPI rent value is based on surveys… begs the question…why a separate OER survey ? What value does it provide beyond that provided by the CPI surveys ?

CPI attempts to track the cost changes in housing as a service (“shelter”), for everyone, renters and homeowners. The CPI Rent tracks the cost of rents. OER is the method that tracks changes in costs of “housing as a service” for homeowners.

Canada’s CPI uses mortgage rates and an index of home prices to track housing cost changes for homeowners. But Canada has mostly variable mortgage rates, or mortgage rates that are fixed for only short periods, such as 2 years or 5 years, so they change for current homeowners, unlike the US where 30-year fixed rates dominate.

Wolf:

One has to catch the other (like around 2012). Which one, we don’t know. Perhaps house owners can convince themselves that the price will inflate further (and overall inflation) so that they can forgo some rent today. It is happening in many developing countries.

Looks to me like case schiller and OER should meet around 260, which is about 30% higher from here for rents

From the chart in Wolf’s response, you can see that the ratio of Case-Shiller to CPI Home Owner Equivalent was 1.5 at height of sub-prime boom in 2006-07 (i.e., 180 Case Shiller and 120 CPI Home Owner Equivalent) – the same ratio as today (i.e., 300 and 200 respectively).

Interesting that we are back in same “over pricing” of homes as during sub-prime.

What a sec here. This is a classic “marginal pulling the average” chart. OE rent is based on housing prices. Specifically “If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?” How could my house be worth $1.3M? Well, I guess if someone paid $6k/mo… People drink their financial bubble Kool-Aid.

I believe your thesis; I don’t think this is the right chart

That said, Case-Shiller is totally flawed in that it attributes all sale price gains of tracked pairs as price gains and ignores improvements. In the classic fix & flip, it assumes just a flip, but the flippers typically put real money and improvements into the house; they don’t just pull out the clutter and stage the place. As prices heat up, the fix & flip activity does, too, which pushes up CS figures. I suffer from this with my property tax assessment as I live in an old house in a wealthy area with older homes that have over multiple 6 figures put into then before sale. The assessor then comps my house to them despite my aged kitchen, baths, deteriorated windows, etc.

.

1. “That said, Case-Shiller is totally flawed in that it attributes all sale price gains of tracked pairs as price gains and ignores improvements.”

This is ignorant bullshit and a lie. Read the CS methodology before spreading lies here. I linked the methodology a gazillion time here, and I discussed how the CS accounts for improvements.

2. CPI OER tracks CPI Rent closely, and I could use CPI Rent just as well, but OER weighs more in CPI, which is why I use it. Maybe I will switch, and then we don’t have to have these discussions. Over the longer term, such as the above chart (Case-Shiller v OER), it won’t change anything materially.

Rents respond to prices in this way (I was a landlord once). If interest rates are high, you may pay more for your mortgage, or second mortgage. If adjustable, you’re in trouble.

Rentals require maintenance, lots of it sometimes if people vacate and leave the place a mess. You do what you can yourself, but that isn’t always feasible. In any case, you will be hiring electricians, plumbers, painters, roofers and etc. Here is where service inflation hits; those guys all want more money. If you don’t want to pay their high rates, you are a greedy capitalist ripping them off. You don’t want to operate at a loss; you must raise your rent. Then the prospective young tenant feels you are a ‘greedy capitalist’ ripping them off.

Good comments CH.

Regarding the last comment: I hadn’t read anyone point out this apparent non trivial shortcoming of CS, increased house cost basis ignored, if I’m understanding.

CS concern,

The reason you haven’t heard this “shortcoming of the CS” is that it’s ignorant bullshit and a lie. Read the methodology of the CS. Or at least read my article about the CS where I discuss this.

While I understand your right to be wrong. I point out the 50 pct reduction in house prices that occurred in the first ten years of this century.

Whether it could happen again ? I think it has too.

Nobody can afford these prices

If no one could afford these home prices, they would have already plummeted. There are plenty of people who are buying houses at these prices everyday (just got outbid on an overpriced fixer upper this week). Americans are swimming in money (at least on paper). Mountains of home equity. Swollen nest eggs courtesy of QE that are currently being rotated into 5+% risk free fixed income instruments. Tens of trillions of wealth about to be handed down from one generation to the next (at least the lucky ones). If RE prices fall 10% there will be a feeding frenzy. If mortgage rates fall a percentage point or two there will be a feeding frenzy. If we get a 20 percent drop in prices, large corporate investors will have an absolute field day. Unemployment is going to need to rise dramatically before you see any real movement in RE prices.

A 50% downturn in RE will take a Great Depression level event coupled with WWIII. I sure hope that doesn’t happen but you never know…

Actually from a study I just saw, you need to be a person or family making at least $163,000 a year to afford to buy. On average across the country.

That’s quite a high bar and mostly shuts out non 4 year college degree holders. And it may take 2 of those together in a family unit to own.

In summary, it’s brutal for the minority.

Agree. People are awash in wealth from asset bubbles. People are paying cash for real estate, more than 20% down when financing, and have been for years. To those, 8% mortgages don’t matter. US household wealth exceeds $154T. There are only 124M households. Do the math. The 90th percentile of HH wealth is $1.9M in 2023, up $500k from 2020, after a “tough” 2022. Annual wealth gains exceed income for millions.

“If we get a 20 percent drop in prices, large corporate investors will have an absolute field day.”

No, because they have to make those prices and interest rates work with the rents they can get for the properties. There is no shortage of rentals, and lots of new-built rentals are coming on the market. And corporate entities are borrowing via the bond market, either by issuing regular bonds, or by selling rent-backed structured securities (ABS). If they have to pay 8% interest, on still higher prices, the rents they can get will create losses for years to come, and Wall Street won’t go for that, and they won’t be able to sell those bonds, and their stocks will be crushed.

What caused the corporate buying in 2011 and 2021 was 0% interest rates, collapsed home prices when they bought out of foreclosure, and direct encouragement by the Fed for PE firms to buy those homes from the banks. This was an entirely different scenario than now. And even a 20% drop in home prices will just get them to where they’d been a couple of years ago, and they will still be too high to make large-scale rentals work.

For the umpteenth time, no money is being “rotated” into risk free fixed income instruments. If someone is buying fixed income bonds from someone else, they’re giving that cash to the other person, who then has to do something with it.

What’s keeping asset prices high is psychology.

Here in the Coachella Valley, perhaps not indicative of other communities due to resort and tourist activities, prices and rents have gone out of control. Up until just a couple of months ago, the majority of buyers were hedge fund/corporate real estate management companies (long term rentals), corporate and mom & pop short term AirBnB buyers, cash buyers from the ocean cities moving here due to the work from home phenomena, and wealthy second/third home buyers. Prices have increased by roughly 60% to 80% (neighborhood dependent) over the past 4 years.

Average families and individuals seeking to purchase have been effectively squeezed out of the market. Until a recession comes, if ever, that knocks out the long-term and short term rental buyers and forces them to sell, I don’t see any relief on the horizon. Post 2008 once the party started, rental properties and second home properties flooded the market. At the depths of the Great Recession, there were over 1,000 foreclosure listings at any time in cities with populations of around 40,000. The net result was a 50% off sale.

I’m desirous of purchasing a primary residence while sitting on the sidelines by renting for now, and hoping that prices will come my way. This places me in the camp of wanting a recession that produces deflationary forces in residential real estate. Regarding future COLA increases or not, they are insignificant compared to the monthly cost of ownership that runs in the thousands of dollars per month.

Illegal immigration/wide open borders and it’s effect on rents and inflation are not a talking point of the corrupt sewer dwelling dnc, as well as a select group of slime in the rnc. Best pos government money can buy!

Lol immigration is deflationary.

Immigrant gardener is cheaper.

Immigrant doctor is cheaper.

Immigrant programmer is cheaper.

People who don’t want immigrants (e.g. doctors / AMA) WANT HIGH WAGES!!!

It’s barrier to entry my man.

@WaterDog It is true that immigration will lower the cost of a gardener and programmer so most rich software company owners that own one acre Atherton estates are in favor of immigration (both legal and illegal). Immigration (both legal and illegal) is not so great for working the class guys since the millions of immigrants in CA push down wages at the same time they push rents up.

Well said WD

I live in the immigration capital of the US – Miami. Illegal immigrants are living three generations in one rental to survive. Theyre definitely NOT running up housing prices – sales or rentals

And Apartmentinvestor, I cant reply to you directly but unless you are pure blood native american, your family at some point were immigrants to this great coutry as well, as were mine in the 1840’s

Wolf, do you allow such blatant political comments on your blog? It’s a bad path to allow this kind of stuff.

I saw another chart that showed asking rents were declining, although actual rents paid has increased. Is there a typical time period of how long it takes for changes in asking rents to hit the actual rent payments?

@gametv More and more landlords are using software to set “asking” rents (like airlines have been using for decades) that set prices based on supply and demand so when demand is high (and supply is low) the “asking” rent at some Bay Area apartments will spike $1K in month, but it can go down as fast as it goes up (just like the price of a round trip ticket to Denver will quickly go up before the holidays and then back down again).

Do rents ever actually fall? I’ve never seen that anywhere in my lifetime. I’ve only seen concessions, like a few months free rent, utilies paid for, etc.

They fall locally, and stay down for decades. Happened in many cities, including Tulsa.

In San Francisco, rents began crashing in 2000 and didn’t get back to 2000 levels until 2012.

But how do you take advantage of less rents?

You have to move right?

And negotiate?

I think that is what a good strategy might be.

“Do rents ever actually fall?”

Happened in Houston, TX in the late ’80’s and at the same time home prices plummeted as the S&L fiasco played out. It was also happening in many other cities in Texas at that time based on conversations with others that I knew from college as foreclosures were rocketing up in numbers.

Also happened in Denver, late 80’s early 90’s. My wife’s rent was reduced upon renewal.

It’s happening in my zip code here in Austin, TX. The For Rent signs cropped up like mushrooms after a mist all around my block starting in June. Only in the last month I’ve seen about half of them removed.

Perhaps we can have an extremely dovish

raise!

J.

————————————————-

I suggest that in order to signal just how

dovish this raise is, the fed drop the rates

it pays on RRPs and reserves, while going

for a 1/4 point raise. “We raised this,

lowered these others, it’s kinda a wash.

Almost like the hold you were expecting.”

Can’t wait to see him gaslight us on Nov 2nd and tell us it will be data dependent and that’s why we will be holding and not increase interest rates…

The higher and quicker they raise rates, the sooner they’ll probably need to cut them. I don’t see any problem in not oversteering and holding at levels never imagined at the start of this year. Meanwhile they let QT run silently in the background while the market sorts out long term rates to the upside (QT doesn’t actually run silently – it makes a loud sucking noise). If they don’t cut rates for a year or so and can run QT that whole time without any major banks imploding who knows; they may even grind the S&P back down to pre-pandemic all time highs while putting a 6 handle on the Fed balance sheet and giving RE a ten percent haircut. That’s my soft landing.

What is the rationale behind the government’s use of owner’s equivalent rent, instead of simply extrapolating actual rents in the neighborhood to the owner-occupied properties, as weighted proportionally? Most owners have no clue about market rents because they’re not landlords. Also, how are outliers treated, eg if a homeowner says his OER is $50,000/month (or $50/month)?

I have a better idea. Why doesnt the Fed create an asset inflation measurement. So when stocks rise without commensurate increases in earnings, or home prices inflate without improvements in the housing stock, that is another type of inflation that they use to measure the stability of money?

The problem is that over the past decade the Fed has stoked asset price inflation with easy money. This was possible as technology and globalization were deflationary forces.

I still dont buy that deflation is bad. It does dampen consumption. Quite frankly, many types of consumption are just waste. Technology is the perfect example of an industry where products improve every year and costs fall. Why are healthcare, housing, higher education exempt from the forces of efficiency that drive technology? Which is the healthier industry, tech or healthcare?

Jackson Y,

Only CPI uses owners equivalent rent (OEr). PCE’s rental factors are somewhat different and broader:

Rental of tenant-occupied nonfarm housing (Tenant-occupied stationary homes, mobile homes, and landlord durables)

Imputed rental of owner-occupied nonfarm housing (Owner-occupied stationary homes and mobile homes)

Rental value of farm dwellings

Group housing.

The reason for including “imputed rent” (similar concept as OER) is to come up with a figure for the costs of “housing as a service”(rather than an asset) that covers the whole population, not just renters.

gametv

“Why doesn’t the Fed create an asset inflation measurement.”

We already have asset price inflation measures, such as the S&P 500 index, the NASDAQ, the Case-Shiller home price index, etc.

Stock indices are a mix of asset price inflation/deflation and changes in earnings. So you could look at indices of earnings multiples, for example.

“Indices of Earnings Muliples” search resulted in these… related to the drunken retiree splurge? Top 10 as of March 2023 via Eqvista.

Industry Name PE Ratio

Beverages – Wineries & Distilleries 68.1724

Software – Application 56.6311

Internet Retail 54.7509

Health Information Services 49.0714

REIT – Specialty 48.1218

REIT – Healthcare Facilities 45.5218

Medical Instruments & Supplies 43.1705

Consulting Services 39.5976

Medical Devices 38.0792

Wolf, I agree that S&P and other stock indexes measure asset price inflation. What i believe gametv was getting at is that the Fed should take asset inflation into account when judging the effects of its policies. In other words, S&P going from 666 to nearly 4,800 in 12 years, when income and productivity hasn’t increased by anywhere near 700%, should have been judged as inflation.

But then every time stocks drop 20%, the Fed has to step in to prevent that? That would be insanity.

First of all, the stock market is the closest thing we have too an actual “free market”. Yes, I know, the stock market has been corrupted by the Fed’s insane QE policies and excessive reserves.

When the asset bubbles collapse, then maybe you will understand the extent of what they have done. Today, the stock market and housing price bubbles are still intact, drawing unsophisticated buyers into a quagmire of overpriced assets.

Off topic, but used car auctions (think Manheim, Adesa, etc.) are the free market in action.

Can be a bit overwhelming; a vehicle rolls by for 15 seconds while 20 or 30 men flash hand signals, then the unit has a new owner, or not.

Morningstar (Markets) has US large caps 10-11% undervalued, small caps 25% undervalued.

Does Morningstar have incentive to claim the market is undervalued ?

I dont know.

I was surprised to see that the Vanguard Value fund was down 3 to 4% ytd. Its P/E end of September at 15.5, a little less today.

Some international funds P/Es are now in single digits. Overvalued … I guess they could be if earnings fall going forward.

Deflation is just the less fortunate using “begging” to get what they want.

Hey I get it “squeaky wheel gets the oil”.

But it is kind of a cowardly tactic

Whatever works tho right?

/s

Thanks Wolf for reminding me with the Case-Shiller Home Price and equivalent rent chart.

I guess housing prices explain the rising rents. Renting is often cheaper now I have read.

I saw an interview with a distressed debt guy today. He was licking his chops and not only for commercial backed real estate. He used the metric net debt/ebitda (net debt to earnings before interest depreciation and amortization) and said there are many many companies where this metric is above 4, his safety top.

I checked my stocks and had one with a 7 and immediately sold it after I could not get information from the company. All they would give me was ‘adjusted ebitda’ and a lot of financial talk.

The rest of my companies appear ok on this financial leverage measure. A companies financial leverage could become very important as they begin refinancing at higher rates.

Yes, the rising home prices explain the rising rents as the most egregious of the effects of the QE bubble. Taxing the least able to afford it with high prices has become acceptable, without regard for the moral regard demanded by the constitutional commitment that every US citizen undertakes.

And the health insurance adjustment bullet hasnt hit the index yet.

Health insurance is figured differently in the PCE price index.

Cow prices are up, too. I stopped buying steaks.

Quit the steaks.

Buy the cows.

Lol

/s

Powell is most definitely raising again in November/December. Book it Danno.

After this Core PCE, it is certainly more likely.

QT: Woefully Inadequate.

Rate Regulation: Woefully Inadequate

Policy Discipline: Non Existant

Inflation: Progressing Nicely

I too am losing my hair Mr Powell

I’ve raised that same point to deafening silence. Not sure how Wolf feels about this invasion. Yeah, where do they live? They didn’t suddenly build two million housing units in the time four million+ streamed across the border.

I generally don’t like to have this stuff discussed on my site because people then quickly start throwing around made-up numbers, or manipulative out-of-context numbers, and the bigoted BS starts flying, and then I have to delete the whole thing.

So let’s how long it can last before I have to delete this whole thread.

So a huge increase in GDP yesterday and core PCE today and the labor market is still tight. If the fed funds rate has anything to do with inflation and slowing the economy, maybe Powell has to think about higher for longer.

Many commenters on this board have suggested Powell raise more aggressively, despite going fast historically. But note that he is coming off of over ten years of historically low interest rates (ZIRP), so he does not really have any past experience to guide him. Maybe he needs to be even more aggressive. He says he makes decisions based on “data”. Well here is ****load of data which says he is not doing enough. He is clearly flying by the seat of his pants, and that seat is getting hotter and hotter.

William Leaked,

Yeah. I guess we are all flying by the seats of our pants. I’m fact, Yellen said something to that effect yesterday and Paul Romer (Nobel) today. The dismal science….

Romero further said he thought hiking again would be a mistake. Mentioning that ought to get me shouted at….

That being well said, there is no rational reason why the FOMC wouldn’t raise the rate by at least 25 bpt. The economy is running red hot with the ultimate future depression to be worse, given their lax monetary policy.

I live in Mill Valley and am trying to move to Corona Del Mar. I have it a snag in you have to give a home in Mill Valley away for much less than the peak price while it is next to impossible to get any kind of a deal in Corona Del Mar. I bid 5% under the ask on two entry level Corona Del Mar homes that are scraper quality and lost. I am talking 4 million dollar money here. The longer I wait the more my Mill Valley home drops and the higher the Corona Del Mar homes go.

Just enjoy Mill Valley. What’s not too like? Who wants to move to Southern California when you can have Bay Area fog? Down there, you may have to use A/C, god forbid.

Lots of Southern Cal homes have no A/C, and many can go through an entire winter without firing up their heater. Northern CA has always looked down on SoCal. Just snobbery.

You missed the sarc?

When I lived in SoCal, the secret sauce was an attic fan. The temp drops so fast after the sun goes down (except during the rare Santa Anna) that all you had to do was blow out the hot air from the day and then your were good to go.

Certainly not unique to Cal.

Many eastern and western Washingtonians look down on each other. Especially if in politics.

Quite pathetic.

Never lived in west Texas but you can bet they think they are better than Dallasites or Houstonians.

You’ll find it in every state.

(I did live near Dallas for 11 years).

At the $4mm price point more people looking for a CDM or Tiburon address so it will be harder to sell a typical $4mm home in Newport Beach or Mill Valley than a typical $4mm home in CDM or Tiburon (or Ross)…

Patience MV. Your time will come

First world problems.

“you have to give a home in Mill Valley away for much less than the peak price”

Give away? I’ve always loved that expression with RE. MV is still super premium priced, and you ain’t giving anything away at those prices. And don’t get me wrong, I love Mill Valley. Might be the best place to live, period.

Hey Wolf, a/c along the coast? Nah, like maybe, maybe a couple times/year. And BTW, Mill Valley doesn’t get “Bay Area fog”…that stuff gets blocked by Mt Tam.

My A/C kicked on at 3:00 AM to get the house down to 75 here in Florida.

I feel your angst, dude. Waiting for overpriced condos in California is a gnarly example of guts.

All the while totally unaware of the majority of citizens that have real problems.

Stuck-

The first part of your hoped-for trade makes Wolf’s repeated point that owners are extremely slow to accept price drop realities on their own properties.

That said, I sympathize with your reluctance to overpay in Corona….

Best of luck on solving the price differential enigma!

John H. – for sake of clarity, there’s a significant geographic difference between the locations of Corona and CdM…

may we all find a better day.

Well then….shouldn’t Fed Funds be at 7% ?

I vote Mike for next Fed chair ;P

William Leake

Something in my software keeps adjusting my typing: Leaked

And then Romero for Romer

Always proofread if you have any spell check that assumes it knows what you want more than you do. Hmmm, do you have Grammarly perchance?

I use a Samsung Galaxy A11.

Bought it 4 years ago I think.

Couldn’t believe how good the picture taking quality is. But the spell checker for text messages and other places interferes much too often. If it was a doctor I’d be sick with something all the time.

Very annoying. To its credit it usually doesn’t try to modify

“and” and “the”.

Yes yes. My Direct TV subscription just increased 12%. I pushed back, threatened to leave. They gave me a sports package that has no Football – junk. But seriously, people are just paying. As long as people pay, prices will increase. So everyone blames the fed or someone. After all we in America are expert at complaining. What if people saved more and spent less? Meaning we are the cause of inflation. Cheap money made us bolder but we are the ones buying expensive concert tickets and unnecessary pickup trucks.

We cut cable TV 15 years ago and lived just fine. All we have at the house is broadband, now $25 a month after I switched providers. You have to fight inflation where you can.

Rates are just approaching “normal” and are actually historically low. We will march higher with a pause to placate Wall Street etc. every now and then.

The price of distorting the economy for so long with ridiculously low interest rates that may take generations to mend.

2% inflation target? Check the last 100 years and you’ll find that inflation has almost never been at 2%.

More evidence that rents are too low, and will continue to be pulled up by inflation / overpriced houses. No landlord wants to rent at a loss.

The landlord can sell and book a profit.

Again, landlords don’t have a god given right to rent at a profit. This situation is not evidence that rents are too low, but evidence that sale prices are too high.

And tennnts don’t have a god given right to be rented a property below its carrying costs.

Asset prices are still too high, but rents are currenty too low based on these asset prices. Both can be true. The correction will involve declining asset prices and rising rents untill an equilibrium is reached.

I’d like to see what the costs of landlords are. What their profits are.

I think our country could use more transparency…especially in some industries.

Mutual fund annual reports have five statements disclosing considerable detail about their investments and costs.

I believe something similar should be required for landlords… detailed list of revenues and expenses. I have absolutely no idea if my landlord’s profit is, say 10% or 40%, of his revenue.

Sadly this kind of thing is not discussed by MSM nor politicians.

It, in fact, has absolutely nothing to do with rent inflation. To think it does is simply delusional.

California alone will be responible for a 1% increase in the rent component of the CPI over the next two years, given current asking rent levels. Asking rent spiked by 31% in California since 2021-2022, but there is a 10% rental increase cap in place in California. The first 8%-10% rent increase has occurred in the last year on continuing leases, and there are at least two more of those sizeable increases to go over the next two years to bring continuing lease rents up to asking rent levels. Since California counts for more than one eigth of all housing rentals in the US, that is at least a 1% contribution to the rental CPI component for the next two years, before any consideration of contributions from other states!

If the tenant vacates, the landlord can set whatever rent they feel they can get. Rent cap is for continuing leases, as you pointed out.

Anyones guess what the Fed will do in November/December and potential government shutdown a factor too. I usually tend to see politicians ensuring it doesn’t happen but when a team can’t select a captain it isn’t a good sign. My prediction, which is worth zero, is that no rates increases and some weird rationalizations as to why not.

Are political shenanigans part of the “data driven” formula? Powell flying by the seat of his pants is more real than metaphorical.

My understanding is a government shutdown would mean no data and thus likely no decision as a result. I am cynical however and think that is involved but without evidence don’t want to push conspiracy theories.

The treasury has been borrowing a lot. How long would it last in a shutdown?

Revenue for the federal government would keep coming in.

Glen, I agree with Mr. Market that the chance of an increase at the Nov. meeting will be about zero, but for December I have a feeling there may be that one last increase due to core inflation being so sticky as Wolf explained at the start of this article.

I see an ad saying “pump where others dare not go,” featuring a buxom brunette. I didn’t click on it but I assume she’s recommending monetary policy to Chairman Powell?

You should see what’s on the iOS app here…

;)

/s

Since the Fed pays their pet banking project, they will probably hold the FFR rate at the current level.

The Fed is the last one to risk a collapse of the asset bubbles they tolerated during their unrestrained expansion of the monetary supply.

And to think the bankers in Mary Poppins used to scare me…

“Put it in the Bank, boy!”

This is what the F idiots need to do Feds- first end the Fed – 2- let rates go to market rates – why were they zero??? Never ever should there be zero risk. The rates should of been 6-7 in 2018.

To solve it you pull a Volkswagen raise rates to 12% let the economy crash

Yes it’s painful but 40 years of lower lower rates it’s a ponzi as the lower lower rates fueled this crap

Now after you crush it as 12-15% rates you bring it to 6.5 people are jumping with joy and you built back a solid foundation – you back the dollar with a basket of day gold, silver, oil, bitcoin and a few other commodities

I’d rather have 3.6% inflation and full employment.

I wouldn’t. I’d rather kill the psychology of spending money. Higher unemployment is needed for that.

Vincent:

Why were they zero? Because as soon as the Fed tried to raise interest rates pre 2020 the stock market swooned which TFG did not like so he said some bad words directed to them and scared them back to ZIRP.

That trained Wall Street to believe that the punch bowl would always be there.

Worse rate decision in the last 10 years in my opinion. It left no room for cutting in 2020, so $$$ was printed with inflation following.

Wolf, big fan of your articles! Thanks for sticking to the facts.

I’m a housing provider (a few hundred units) and am starting to see rents soften first hand. Not sure if this is due to absorption of a lot of new deliveries or other economic factors.

Our company’s theory is that, even if rents deflate a little bit, it will hurt developers significantly on top of interest rates (up 3x) and construction costs (up 40% from 2020).

With all of this at play, do you see a huge price correction of commercial assets? We think 20-40% from the peak regardless of asset class. What do you think?

Where are your properties located?

Sell AL sell

Al:

New deliveries. Here the SL Tribune reported a year ago of an existing inventory or rentals of 3k, another 3k under construction, and another 3k planned.

I have a feeling it would be hard to sustain rents when the population of school kids went up by only 280 kids or so for the entire state along with the number of apartments increasing by 200% to 300%.

Construction cranes and in-progress apartment blocks are still seen everywhere. Overbuilding perhaps?

The FED refuses to meaningfully bring home prices down. For most of 2023, home prices have gone back up after a puny % drop in 2022. Powell needs to get rates above inflation (no I do not believe the CPI) and sell MBS. Neither of which he will do. Inflation and home prices: “higher for longer”

Today i was looking at a house for fun since it was a open house where I was visiting

This is in souther ca 100 miles away from coast so quite inland.

The home was listed for 680k. The median income in this place is 45k .

To be able to afford this home one needs to bring in 150k plus per year .

No home in this town for below 600k.

The market has really gone crazy .

The housing market need to crash badly to bring some sanity.

This article says inflation is quite high and is sticky.

If Powell feels the same he’d raise rates.

But I am sure he won’t to protect his and his friends and masters wealth.

Home prices are gradually dropping. The housing market does not move quickly. It will takes months for the housing market to work itself out. Raising rates just to lower prices faster will just lock up the market more. Basically more pain with no real difference in the market.

The “demand for money” is fickle. It fluctuates more than the money stock. But the FED discontinued the G.6 Bank Debits and Deposit Turnover Release in Sept. 1996 for spurious reasons (for its intended use).

The sticky inflation is purely FED’S fault 100%. They didn’t have to print $5T during the pandemic. They didn’t have to print $400B in Spring 2023. Their multiple rounds of reckless money printing inflated the asset prices, which inevitably translated into persistent inflation.

It was fine to print $5 trillion, in theory, as long as the $5 trillion was removed as fast as it was printed. It never is.

Jason: 100% the FEDs fault? What choice did they have with ZIRP? Remember, the FED tried to raise interest rates (so they could be cut in a panic such as 2020 instead of printing $$$) but Mr. Market complained and TFG complied.

Housing has been a good investment for decades but I don’t think it will be for years and maybe decades to come.

I see this in Wolf’s Case-Shiller and CPI -Owners Equivalent Rent chart.

I listened to Howard Mark’s updated Sea Change memo last night. You can find it at Oaktree Capital. I think his ‘Sea Change’ memo alludes to this and many other investment thesi that are changing. Howard is one of the best.

I don’t think housing will fall quickly relative to other assets unless the Fed raises rates too high and sets off a recession and a housing crash.

I think there is a possibility of that for several reasons. First, their goal of 2 to 2-1/2% for the Fed funds rate is too low. Mohamed El-Ehrain has been harping on this for a year. Yesterday I heard Paul Romero (Nobel winner) say something to the effect that raising rates again would be foolish. Finally, I heard Summers say that the feds nominal rStar plus inflation is 2 to 2-1/2 while his is 3-1/2 to 4.

I hope the fed does not overhike and set off a recession and everybody who owns a highly inflated house should be concerned too.

Not Paul Romero, Paul Romer. This damn smart computer isn’t so smart in correcting my spelling.

It (or the programmers) still thinks it is smarter than you, hence the incorrect corrections. Always proofread before submitting. /s

“Housing has been a good investment for decades but I don’t think it will be for years and maybe decades to come”

Thomas do you own a home? Have you ever owned a home? Do you have any experience owning homes over the long-term? Ever been a landlord? I would be interested in hearing your real-world personal experience much more than what you read somewhere.

Housing has always been a long-term game, just like stocks. Sure, you can day trade or flip houses and make fast money, but you can lose big fast also. There are opportunities to make significant gains in housing just like there have always been. Everyone wants to get rich quick but I’m perfectly happy to get rich slowly and steadily.

Anyone remember when mortgage rates were 18%? That was a terrible time to buy a house, unless you did and held it.

DougP,

You said, “Thomas do you own a home? Have you ever owned a home? Do you have any experience owning homes over the long-term? Ever been a landlord? I would be interested in hearing your real-world personal experience much more than what you read somewhere.”

My bio is mine and I am quite proud of it. I strongly suggest you try to understand what I think I learned from Mohamed El-Ehrain, Howard Marks, Paul Romer, and Larry Summers and them make a rebuttal to my reasoning. You and all of us might benefit.

My rebuttal is that anyone who thinks a goal of 2% inflation is too low isn’t worth listening to on anything else.

Einhal,

Your understanding of economics is poor and your aggression keeps you from learning.

My understanding of economics is fine. there should never be an inflation goal. Stable prices should mean just that. You never want to encourage people to consume on the basis that their money is worthless the next year.

I understand math a bit. Here’s the math:

At a 2% inflation rate that is compounded, a dollar gets cut in half in 34 years, 8 months.

So, who out there wants to hand me a $100 bill for a $50 in return? I mean, why wait, I’ll be happy to speed things up for you, eh?

“I strongly suggest you try to understand what I think I learned”

Let me know when you are SURE of what you have learned, then we can talk.

Fed needs to hike more .

Never trust these so called experts although they are the policy makers.

Remember transitory word .

We need much higher for longer .

Even if the inflation goes to zero the prices stay at those high plateau.

We need big crash in hosting for young and future generations.

People who are invested in housing are justifying that home prices won’t fall a lot

I sold most of my homes in socal but 2 last year so I am in it but not really invested

These are my homes I live in but I want home prices to fall so that people I know and future generations can afford a home to live.

All I know is my health insurance premium went up 22.7% for 2024, and I’m pissed.

I’m on Medicare, and my premium for Part B actually went down by 3% or so in 2023. And the small premium I pay for my Advantage plan (to get very low caps and maximum out of pockets) went down by about 4%. Everyone on Medicare is paying less this year than last year. Many millions of people.

My wife, who is covered at work, saw an increase of about 5%.

What is it I hear about someone on Medicare or a supplement can become locked into a terrible plan? Then the terrible plan can refuse procedures one needs.

I’m really going to have to dive deep into this at some point. A pile of books in my future, I see.

If I were living in a business-friendly (insurance-company friendly) but consumer-hostile state, such as Texas, I would NOT get an Advantage plan ever. I would stick to original Medicare, Part B, Part D, and maybe a supplement. I had insurance in Texas, and it taught me a lesson. I wouldn’t want to deal with a health insurance company in Texas again. Your state’s dealings with health insurance companies is the first thing you need to look at.

In general, Advantage plans are a huge taxpayer rip-off, and insurance companies are screwing the government royally, and all the executives should go to jail.

But as the insured, I don’t care about that. What I care about is what they do for me. In my opinion, if you have the right insurer in the right state, Advantage plans can be better for your health and finances than original Medicare, plus B plus D plus supplement.

I don’t ever make any recommendations about that; these decisions are very personal and depend on all kinds of personal things — including in what state you live, and crucially, if you move between states a lot (which is a huge issue with Advantage plans). The whole thing is very complex to figure out. I wish we had a simpler and easier-to-navigate healthcare system. But we don’t.

You can be locked into a terrible plan if you do not check not only your Advantage plan’s Annual Notice of Changes, but the providers covered. My current plan covers 95% of the providers, but I still need to call both UofU and IHC to see if it will be the same this coming year.

As a sales provider for Aetna I always recommend actually calling every medical provider you have to verify they will be affiliated with your Advantage plan next year. One provider I called said yes before realizing they forgot to turn in their renewal paperwork – such is life.

PS Don’t call your Dr., call the billing office. Also, if you have a tier 3 or 4 drug, call the Advantage Plan’s helpline to find out the cost for next year and if it will still be covered. Usually there is no surprise but I have had enough calls to know this can create a nasty surprise (or a good surprise – one lady found her drug went from $140 to $4/month – got a generic competitor).

Part B premiums are increasing $9.80 in 2024, from $164.90 to $174.70. That’s on the lowest level tier before IRMAA kicks in, of course, as you know. I have medicare advantage through United Healthcare, and it is a 22% increase when usually it’s about 7% or so at the most. According to one article, UHC is basing the increase on some BS modeling out of CMS. I’m glad for you that yours is better. I’m pissed about mine. I’m not experiencing what you are experiencing.

Read your response again. You are talking about 2023. I’m talking about 2024.

“Everyone on Medicare is paying less this year than last year. ”

That’s because CMS raised premiums prematurely in 2022 for some Alzheimers drug that they thought would cost Medicare more than it did. We were unnecessarily hosed in 2022, so 2023 was a correction for their miscalculation. I don’t feel they gave me anything extra in 2023, so the jump in 2024 is an outrage. I’m sure this risk modeling that UHC is basing 2024 premiums on is just as inaccurate. Therefore, I’m pissed and have every right to be so.

Airfare inflation is even devaluing frequent flyer miles–I am using more miles to travel an identical itinerary as I did last year during the same week.

That’s been going on for two decades. I finally gave up even trying to collect miles or maintain them because it was so hard to use them to book flights. What did it for me was in 2005, when Delta refused to let me book a direct flight (for my wife and me) with my miles from San Francisco to Narita (Tokyo). They wanted to fly us from SFO to Atlanta, and then the next day fly us out of Atlanta to Narita, a two-day monster trip. So I paid for the flight, and Delta flew us direct, via their partner Korean Airlines, in eight hours.

…anyone here remember the era of ‘S&H green’ or ‘Blue Chip’ ‘savings’ stamps? Recall ‘cash value one Mill’ imprinted on each. (Surely 100% devalued by now…).

may we all find a better day.

Wolf,

Is this setup giving you an eery feeling of a repeat of the early 1970s? Then inflation dropped to about 3.5%, refused to go below that floor and re-accelerated sharply on any economic or fiscal spending expansion. Then the pattern repeated until Volcker.

If the US military budget goes up big time (looking like it will given what is going on internationally), and the Fed is tasked with paying for it because Congress can’t get it together, what do you think happens?

I don’t think history will repeat. It will dish up something new, maybe similar elements mixed together differently, or something like that. Even in the 1970s, all this took years… into the 1980s.

Congress needs to get serious about the deficit, and not just with partisan grandstanding. That’s not happening though. All we have is partisan grandstanding. The fiscal situation will have to get a lot worse before it forces Congress to come to its senses. And this can take years.

The reason all you see is partisan grandstanding is that the American people, collectively, don’t want a cut in spending. Sure, individual people want cuts to things they don’t personally care about, but every bit of spending is SOMEONE’S sacred cow.

I’m all for the dictatorship of the proletariat but that won’t happen in the U.S. Most people see things through their own lens not realizing most of us share the same goggles.

“The American Republic will endure until the day Congress discovers that it can bribe the public with the public’s money” -DeTocqueville

History repeats.

Net changes in Reserve Bank credit, since the Treasury-Reserve Accord of March 1951 are supposed to be determined by the independent policy actions of the Federal Reserve authorities.

Treasury-Federal Reserve collaboration exists in its present state, because whenever in the past the FED’s responsibilities were subordinate to the Treasury’s, this country experienced intolerable rates of inflation.

Every comment I put in is now flagged for “moderation”. I don’t believe I violated the rules for comments every time, though I may have done so unintentionally at times.

I’m sick of your inflation BS. I’ve tolerated it enough, and I wasted endless hours shooting it down, but it just doesn’t end. So now your inflation BS ends right here. I hate it when people abuse my site to spread misinformation. Do that on X. All your other comments are welcome and appreciated.

I was in moderation for months – every comment – then one day Wolf opened the jail cell and I breathed the sweet air of freedom. I never did thank Wolf for that, so THANKS WOLF!!

It would be nice to get feedback as to why that happened to me individually (not just the general reasons he gives) so I could modify my behavior. Maybe he did tell me in a follow on comment but I never come back once I’ve read the comments, so I wouldn’t see it.

As they say, you can’t control how I feel but you can control how I behave. Good luck to all those misbehaving out there.

Oh well that was short lived. I’m back in moderation. This site is too funny sometimes.

LOL. If your comment bitches about “moderation,” it goes into moderation. Enjoy moderation in moderation.

Try to post something without bitching about moderation and see what happens.

Gee, those “FED pauses” look like such a great idea now, don’t they Wolf? I was right and one day – ONE DAY – you’ll acknowledge it – the FED never should have paused. :)

If the Fed stands by it’s word, it should be trying to create deflation to offset the excess inflation during the 2020 to 2023 period. You don’t do that by pausing. You do that by increasing rates and accelerating QT.

What good is the Fed if it will not stand by it’s stated inflation objectives?

The Fed answers to the banksters, not the American people.

You need to understand that it takes YEARS to get inflation back down and keep it down, not months. You can create a recession, and inflation keeps going, as we have seen, you can create stagflation with lots of inflation. This is not a simple thing. And taking some time to watch the economy react to these 5.5% rates, up from 0.25%, is a good thing.

If something big blows, inflation or no inflation, the 0% starts all over again. And that would be the worst-case scenario.

I understand that you’re pissed off because Powell hasn’t blown up the entire system already. And I understand that you’re pissed off about everything in general. And I appreciate that. But blowing up the entire system is not a good solution imho.

Wolf, please just remember that Powell is the arsonist, not me. Cheers.

This!

I am always surprised at how people carry grudges from the past so much that it clouds their view of the future. The past is the past. It cannot be changed. Do what is best going forward.

30 years of loose rates and 15 years of QE were dumb. No doubt. I genuinely wish it had never been done. But no matter what you think of it, it was done. No changing it. However, blowing up everything and driving the world into a deep recession isn’t going to undo any of that.

DC,