The purpose of MBS purchases was to repress mortgage rates and inflate home prices. That process has already started to reverse.

By Wolf Richter for WOLF STREET.

A date for history: Today, September 15, the Fed stopped buying mortgage-backed securities altogether. It had been tapering its purchases since late last year. Since June, when the phase-in of QT started, it still purchased MBS to replace some of the pass-through principal payments from mortgage payoffs and mortgage payments that reduced the balance of its MBS faster than the cap of $17.5 billion. The idea was to keep the run-off of MBS within the cap of $17.5 billion in June, July, and August. But this circus is finally over.

On today’s release of scheduled purchases by the New York Fed, there were zero MBS purchases scheduled:

The Fed’s final trade in MBS.

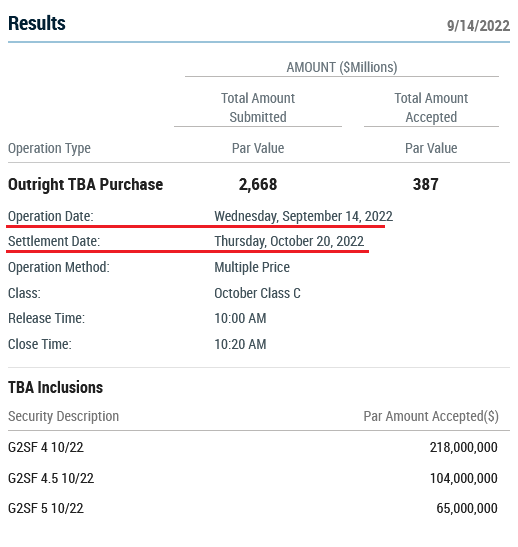

Yesterday, September 14, the Fed conducted its final purchase of MBS. The Fed bought $387 million in MBS in the To Be Announced (TBA) market, which is a minuscule amount by the Fed’s standards. It went out with a whimper, so to speak.

This is a screenshot of the trade that the New York Fed posted on its website. I underlined the operation date (Sep 14) and the settlement date (Oct 20):

Trades in the TBA market settle after one to three months. As you can see in the image of the trade info above, this particular trade will settle on October 20.

The Fed books these trades when they settle. So, it will book this trade on October 20, which is a Thursday. Its weekly balance sheets are always as of Wednesday evening, and are published on Thursday. This trade will show up on the next balance sheet after October 20, which is the balance sheet to be released on October 27.

So halleluiah, the balance sheet on October 27 will show the final purchases of MBS. And then it’s over.

A trickle of trades haven’t settled yet.

The MBS that were purchased over the past two months will still trickle into the weekly balance sheet until October 27.

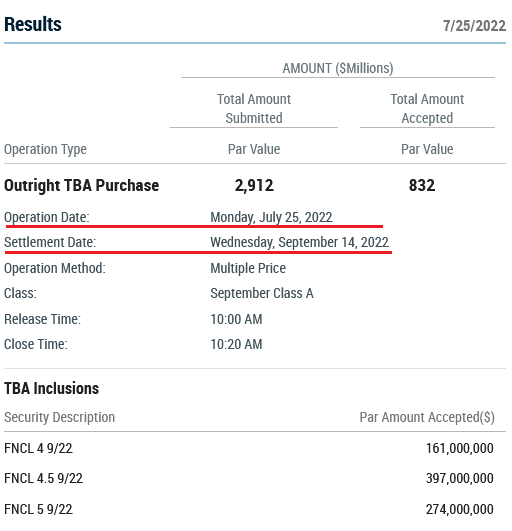

This includes a batch of MBS trades that the Fed conducted on July 25 and that settled on September 14, and that showed up on today’s balance sheet. Here is one of the trades that settled yesterday and was included today:

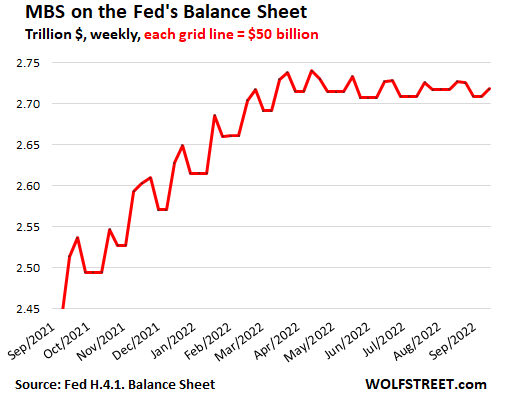

In total, $9.2 billion in MBS trades showed up on the balance sheet today. It is these trades, when they settle, that cause the balance of MBS to rise in the jagged manner.

MBS come off the balance sheet mostly through pass-through principal payments. When the underlying mortgages are paid off because a home is sold or a mortgage is refinanced, or when regular mortgage payments are made, the principal portion is forwarded by the mortgage servicer (such as your bank) to the entity that securitized the mortgage (such as Fannie Mae), which then forwards those principal payments to the holders of the MBS (such as the Fed).

The book value of the MBS shrinks with each pass-through principal payment. This reduces the amount of MBS on the Fed’s balance sheet.

These pass-through principal payments are uneven and unpredictable, and do not match the purchases in the TBA market. So the MBS balances form this jagged line of increases when TBA purchases settle, and the decreases when the pass-through-principal payments come off.

The upticks are the purchases from one to three months ago, when the Fed was still phasing in QT and was still purchasing MBS to replace pass-through principal payments. The downticks are the pass-through principal payments. Sometimes both coincide, and the net moves are smaller:

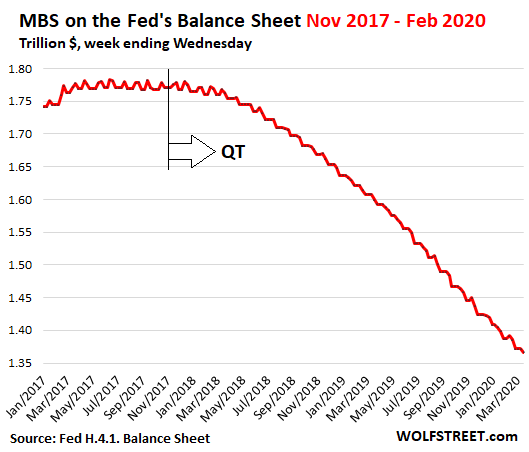

The last time the Fed did QT Nov 2017 – Feb 2020.

During the last episode of QT, the Fed shed MBS from November 2017 through February 2020. The chart below shows this phase of the MBS reduction. During the phase-in, it took about three months before the first declines became recognizable. QT back then was much slower, and the phase in was much longer, than in the current era of QT.

Note how the upticks essentially vanished as the Fed bought fewer or no MBS to maintain the cap of the runoff, and the line smoothened out on the way down:

Going to zero?

Going forward, after October 27, 2022, after the last MBS purchases have shown up, the upticks will disappear, and the line will smoothen as it heads down. But this time, the decline will be steeper and faster.

The Fed has said many times over the years that it wants to get rid of its MBS entirely, and that it wants only Treasury securities as assets. So if everything goes according to plan, the MBS balances will go to zero. And this might require that the Fed starts selling MBS outright later in the process to supplement the pass-through principal payments. The Fed has already put this option on the table.

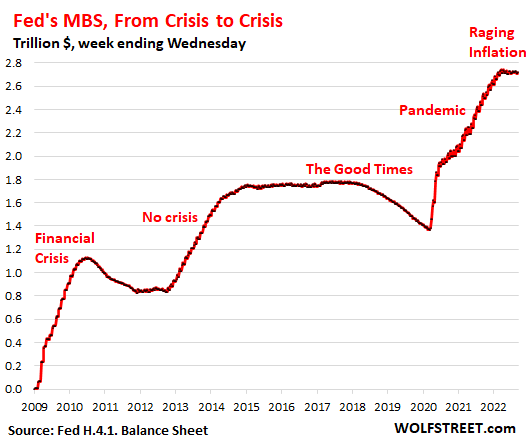

The entire episode of MBS on the Fed’s balance sheet started in late 2008, when the Fed for the first time started buying MBS as part of QE-1. By the peak in April, 2022, the Fed had $2.74 trillion in MBS on its balance sheet.

The purpose of MBS purchases was to repress mortgage rates and inflate home prices. That process has already started to reverse.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So what would this mean for MREITs such as NLY or AGNC?

America is going on sale. Cash is king.

I read a great article where this bond analyst basically is telling JPowell to come clean. The Fed and all the powers at be know that we can’t have an FFR much above 4%. As it rises towards 5% and drags the short-term treasury bills’ & notes’ yields higher, our interest expense on the national debt is going to explode. The Fed will be forced to pivot for this very reason.

While he didn’t give an exact timeline, I believe the Fed will be forced to pivot by the end of 2023. Rates will end this year about 3.5 to 3.75%. We’ll then see 25 basis point moves early next year after a 2-3 month pause. Once the FFR rises towards 4.5%, there will be a chorus of pundits, Congressmen, bond traders etc calling for the Fed to pivot. JPowell’s hope, of course, is that we’ll actually be in a minor recession by them with no more than a 1% uptick in unemployment.

My hope is that the labor market does its best to not fold for at least 6 more months, keeping at least 6% inflation on tap. This will create enormous pressure on the Fed. I truly believe that before they pivot, they’ll announce that the new inflation target is 4%.

FYI – our total interest on the national debt of $30.9T is already $678B with one month to go in FY 2022. This is up from an average of $545B over the previous 4 years.

You’ve just eloquently explained why the Fed needs to hike the FFR by 1% next week, but we already know they won’t.

BenW,

The Fed will “pivot” when inflation goes down, not before. People need to get this concept into their heads. It doesn’t matter what “bond analysts” say – they’re talking their book, and they’re losing a huge amount of money when interest rates rise, like right now. They’re screwed in this environment, and they’ll say no matter what to manipulate markets their way. These “bond analysts” have been dead-wrong about this for over a year.

Worth adding that anyone who cares to do the math on Federal debt rollovers and budget can work out the effect of sustained higher rates.

A lot of the Treasuy debt is longer-term and the higher rates only affect things as those bonds mature and get rolled over.

Bottom line is that the Fed can jam rates up for years before it’s a serious issue for Treasury Dept.

And even then, it’s not an end-of-world scenario … just a long overdue belt-tightening scenario, and an opportunity for Congress to relearn how budgets were done from ~1899-2000 or so.

The Fed does not have “fine tune” control over global inflation. The Fed will most likely break the entire world economy in the process of raising interest rates initially way too slow, then way too fast, without foresight to the real world impacts due to the 6-8 month lag of effects. Finite limits do exist to how high the Fed can raise FFR before they create more damage than 4-6% inflation over the next 2-3 years.

For example, if the 30 year mortgage goes from 2.5% to 8.8%, the monthly payment on a $1,000,000 home at 2.5% is exactly the same as the payment on a $500,000 home at 8.8%. Yes the Fed can deflate housing and destroy a large part of the economy in the process, but that mostly wipes out the middle class, and leave the top 10% wealthier as the top 10% don’t have 80% of their “wealth” tied in their main residence. And if this happens, the damage to the social and political system becomes even worse thus more gridlock in getting larger issues addressed for society.

Thus the Fed at some point will pivot due to the unintended consequences of broadly raising rates for “everything” concurrently versus having a more fine tuned interest rate regime that is more progressive versus regressive.

If the Fed does not pivot by the end of 2023, I know this sounds insane, but I’m predicting massive deflation by EOY 2024/2025 due to the unintended consequences of using the blunt force interest rate sledge hammer to our debt loaded global financial house of cards…

Yort,

“Yes the Fed can deflate housing and destroy a large part of the economy in the process, but that mostly wipes out the middle class, and leave the top 10% wealthier as the top 10% don’t have 80% of their “wealth” tied in their main residence.”

1. Nah, it won’t destroy “a large part of the economy” — the economy is: jobs, wages, consumption & spending, capital investment, etc. Home prices have relatively little impact on them.

2. With a 50% decline, many homeowners in aggregate would just be giving back the ridiculous casino money-printing gains of the past 3 years. Those gains weren’t earned. Those gains were the result of central bank money printing and interest rate repression. And now they may have to give some of them back? So what? Easy come, easy go.

OMG, the pivot crowd is still crowing. It’s like that roach that just won’t die. You stomp it with your shoe and it squirts out from under you like you did nothing. You chase it around stomping it it but nothing works. You finally take your wife’s hairspray and a lighter and use it like a torch, nearly burning your house down, but then the roach just shoots off at warp speed and disappears like it had a turbocharger it was saving for moments like this, and you think it’s gone, only to reappear and annoy you beyond belief.

Exactly the interest on the National Debt (increased by $7 Trillion by biden in 19 months) forces the FRB to monetize 50-75% of what they are draining with the unwind of the FRB investments.

I always pictured the Fed trying to start QT, like a kid removing the first block in a giant game of Jenga. Go very slow, close your eyes, and hope.

I like the question about NLY – Passthru Cash flows from principal repayments (refinancings) cloud be reduced on MREITs.

The effective duration of mortgages (viewed as bonds) increases quite a bit when rates are rising vs falling, and when house prices are falling vs rising, and when house sales are slow vs fast. Etc.

Housing speculators, hold on to your butts…

actually the private lenders are doing very well these days

rates back to double digit with great fees

I specifically asked about flippers – they are getting funded

it’s the hedgies of 1% kind getting de-liquified

A little guy, around the corner from us, bought a teardown shack on a 30 foot lot for about 2 million including permissions, severances, and municipal taxes etc earlier this year. The plan was to build two new semi-detached houses, each on a 15-foot lot, each about 1500 sq ft and sell them, for what? – 2 million each?

Despite what many people think, margins can be tight on small builders’ projects even in good times. Then there are the surprise variables.

Nothing is happening yet, and won’t until ‘maybe’ next year; project on hold. At the recent mortgage rates buyers would have to pay 10,000+ a month after a 400,000 down payment to carry one of these places.

Times have changed. Back in the golden days, I went expat and was allocated a housing allowance to fund an equivalent house to what I had in the states. I got a small apartment instead and pocketed over $1Ok per month. Now you have to PAY that much?

I have no debt now, so most of this goes over my head Except for taxes, which are the coming backbreaker.

This is going to get ugly for Banks. Banks will run out of liquidity; borrowers lose their jobs and can’t make payments; banks will review their portfolios for high risk and start cutting credit, very stringent credit terms to get a future loan and the economy will feel the pain. Here we go – rollercoaster ride.

Credit standards are a “moonshot” away from being anything close to tight now.

What most people call “tight credit” I call historically lax.

I’m 57 and there hasn’t been tight credit standards my entire adult life, back to 1982 when I graduated from high school.

“The purpose of MBS purchases was to repress mortgage rates and inflate home prices. That process has already started to reverse.”

That last sentence sent a shiver down my spine because I never looked at it like that and it will punish the FOMO “real-estate always goes up” crowd.

Debt can be a two edge sword.

I find it sick that despite promising tightening, Fed was still buying MBS to maintain the balance sheet against pass through payments.

A class action lawsuit against US fed should be in order. Here is the probable text:

1. Fed MBS purchases artificially raises house prices and consequently raises rent expectations.

2. These higher rents resulted in Tillions of dollars worth of cumulative financial losses to 45% of all American households that rent over the last decade.

3. These artificially higher asset prices also resulted in higher property taxes for home owners causing them to lose billions of dollar cumulatively. The asset price gains that they received were reversed by QT.

4. To hold the Fed accountable for losses to a majority of Americans, we the people will like to Sue the US Federal reserve to recover our losses.

5. We would like the US courts to decide the matter and uphold the rule of law.

What do you guys think about this?

We also call on our representatives, the senate and congress accross all political parties to launch an investigation to validate our case and hold the Fed accountable.

What good are the courts when we live in a Kleptocracy and rule of law has gone the way of the Watusi twist?

The global central banks, including the Fed, have changed the business cycle to the “Liquidity Cycle”. Personally I think essentials such as food and shelter should not be subject to financialization schemes, yet all we can really do at the moment is ride the liquidity waves as they rise quickly to the best of our abilities… and try not to get caught up in the liquidity wave inevitably crashes…

Note that when you include gold and housing into the “All global wealth” chart, it has a very high correlation to global liquidity. Perhaps Wolf can allow this single chart that shows Global Liquidity (including housing) & World Wealth as it visually simplifies what is happening with global housing and other “assets” across for all humans…not just Americans…

Per Jesse Felder:

https://pbs.twimg.com/media/FcXHBUhXgAAVzH7?format=jpg&name=medium

Well apparently if you talk bad about the connected oligarchs you will get pulled over by the FBI at a fast food joint and your phone taken away.

WA

“our representatives, the senate and congress accross all political parties”

They ALL are complicit in this crooked game, like complaining Foxes about hen houses.

I for one am all for it.

WA

You might have opened up a can with that question.

Wolf might have to hire another moderator haha.

I’d love to answer sincerely, but it wouldn’t fly.

Ricky, I’ll answer sincerely by way of hopefully a short anecdote: When I first entered the world of small municipal administration (permit tech 4 yrs ago after 27 yrs as builder) I somehow ended up at a meeting of some random committee of managers, during which some new “issue” came up, and, without irony, a new committee formed, and regular meetings were scheduled.

I’m sure your elected representatives will be thrilled with another such opportunity!

We need to have Wolf write up the suit and see if he can use “smoothened” and “smoothed” in back-to-back paragraphs, accurately, again. In all seriousness, while we all accept that it will (probably) never be a thought in reality, this makes infinite sense. They pumped the bubble almost endlessly for nearly 15 years and now are going to revert back to letting the market fairly price?! Imagine the supply and demand side for bonds–the Fed is going to run off $60B in treasuries/month, which will have to be absorbed somewhere, and then completely stop buying MBS altogether. Granted, MBS volume is down, but still, where is the investor pool going to come from to absorb upcoming bond issuance? It’s crazy to think that homes have been used as an asset in this scheme–when people wonder how a bubble pops, look to the underlying financial instruments and those who manipulate them

“smooth·en v.t., v.i. to make or become smooth” — Random House Webster’s Unabridged Dictionary.

At a high enough rate, they will be flooding in from all over the world.

A legal problem: sovereign immunity. Government is immune from lawsuits unless it has waived sovereign immunity for that type of claim.

or the judge (politicians in black robes) will utilize the oft abused ruling that the Plaintiff has not standing and then dismiss the case.

The old trick that the Courts learned from the King is the trick of proving “standing”. Beautiful sentiment is displayed at the US Supreme Court. Approach and be heard. The trick of the courts and the King is that both will kneecap you in the approach. The king or an Empire are served by its courts. Beware of demanding “justice”.

How about the government encouraging the idea that every first time buyer should be able to buy a house, even in a lousy neighborhood, with no down payment, no closing costs, and even if they have essentially a zero credit rating, but have a history of paying rent on time?

Bank of America’s Community Affordable Loan Solution, a ‘trial’ program set to expand if ‘successful’, is like 2007 all over again.

Presumably all these mortgages will end up in MBS’s.

How’d that work out? Is there no learning curve?

/sarc

BAC needs to go big with this program. Even though the FED is not buying these MBS, all they need to do is to convince the GSEs to back the MBS they will bundle these loans into.

They need to go big and collect a lot of fees and if the program fails, the FED will come in and buy the MBS to prevent contagion.

No way does the FED ever let a TBTF bank from taking a loss.

The real problem is that the Fed caused a bubble, which will cause massive pain as it unwinds.

The mandate of the Fed needs to be cut back. No more dual mandate. A single mandate should be to hold prices steady and manage the banking system’s finances. We should also regulate the shadow banking system, so it cant get out of order.

Agreed gametv. The central bank’s tools don’t have control over employment. I can’t for the life of me understand why they’ve been tasked with handling it. They have control over the cost of debt and thus some control over inflation in a economy built upon debt. Currency stability and low unemployment are often totally conflicting goals anyway. A central bank should only be worried about the stability of the currency. Job programs and decisions on how to spend public money are up to congress. Unfortunately, Ds and Rs alike in our deeply dysfunctional congress have pretty much dumped their duties on the Fed, the courts, and the President’s executive orders. Except for when they pop their heads out every half a year or so with some unfathomably massive and unfocused omnibus spending bill without a way to pay for it.

The bubble itself caused VAST amounts of pain to the working class. Unwinding the bubble will cause pain to the lower parts of the investing class. The top few will continue to gain from every change and move because they are designing the changes and moves.

I find it sick that the Fed is openly creating bubbles for the benefit of asset holders on the premise of ‘wealth effect’ without a legal mandate or even evidence. It’s a completely rogue institution.

Your logic is sound but the problem for home owners, very difficult to overcome in the courts, is their John Handcock on the mortgage contracts.

Greenspan began pushing this “wealth effect” SCAM 40 years ago. I am glad that reality is finally asserting itself because, throughout all that period, people who did not own homes were defrauded by Fed caused inflation (consistently low-balled by the BLS). Thus, while home owners were enjoying the ride, they, and EVERYONE ELSE, simultaneously got the inflation shaft (i.e. loss of buying power) on just about everything else people need to buy just to live, never mind optional and luxury goods and services.

The Government computed cost of living was correctly computed before Greenspan began gaming it during the Reagan Administration. He kept ‘improving’ that game to steal from pensioners and COLA linked wage earners all the way to late 1990’s.

Shadow Stats still provides the pre-Greenspan COLA numbers, which are always at least 10% higher than BLS published numbers. If you want more detail on how we-the-people, particularly those who do not own homes, have been massively defrauded by the Fed gaming of the COLA formula for over 40 years, check out the Chapwood Index.

Shadow Stats is a joke. A few years ago, Williams admitted as much. He just ads some number to the BLS figures. He has made a living doing that.

I agree shadowstats are a joke but the inflation number produced by governments are also not true

Yes, and the problem with inflation is that everyone has their own inflation rate, depending on how they live and how they spend, and where they live, and whether they have kids in school, etc.. So coming up with a national average is always a compromise, and a political decision on top of it, and no one is happy with it.

the Fed is a private company, so the suit would fail.

Joe bob,

“the Fed is a private company,”

Either the “not” is missing or there’s a misconception here. So Just in case:

The Federal Reserve Board of Governors is a government agency, and all its employees are federal government employees with a government salary and a government pension, including the seven members of the Board, including Powell and Brainard. These seven members of the Board of Governors are appointed by the President and confirmed by the Senate. The Board of Governors has lots of employees, and they’re all employees of the Federal Government. They’re working in the Eccles Federal Reserve Board Building, the main office of the Board of Governors of the Federal Reserve System. This is a federally owned building on 20th St. and Constitution Avenue in Washington, DC.

The 12 regional Federal Reserve Banks are private organizations that are owned by the largest financial institutions in their districts. They include the New York Fed, the San Francisco Fed, the Dallas Fed, etc. All their employees are private-sector employees.

The FOMC – the policy-setting committee that makes the decisions – consists of the 7 members of the Board of Governors (federal employees) who have permanent votes on the FOMC. The New York Fed governor (private employee) also has a permanent vote. The other 11 regional FRBs (private employees) rotate into and out of 5 voting slots annually.

The FOMC is designed to give the 7 government employees a voting majority over the 6 presidents of the regional FRBs

Why does this sound like a bailout to me?

Hah! Yeah that last sentence caught my attention too.

Yes. Exactly why the Fed was founded and one of its core principles.

“The purpose of MBS purchases was to repress mortgage rates and inflate home prices.”

Leveraged Debt, such as used in real estate, works both ways.

And, on the way down, acts like a guillotine.

Greed and panic are different emotional responses and the tightening will not be the the reciprocal of loosening.

Trust (or complacency) is built gradually. Its withdrawal (up to panic) happens quickly. All for sound biological-survival reasons.

I construct my longs and shorts accordingly.

“Leveraged Debt, such as used in real estate, works both ways.

And, on the way down, acts like a guillotine.”

—————————————

not when it’s inflated away ……………..

My guess is Fed is playing with a money system that they don’t understand. There is more brainpower outside of the Fed than inside it, plus different incentive structure. Remember Great Britain selling gold at the very bottom.

Martin Armstrong (fwiw) observed that the Chinese central bankers are experienced traders, and the US central bankers are academics.

I try to look at the FED’s actions, not in the manner of ‘the FED wants the markets to do this or that, but as what do bankers in general want. They want to minimize their exposure to risk(s) and pass those risks on to others.

That poses the question: is the FED steering the markets to where it wants them to go (which mostly seems to go wrong), or is it reacting to the waves the markets make?

Most of the times it is difficult to answer that question. But looking at risk aversion, the FED’s actions doe make sense a lot of the times. They have front row knowledge of things happening and can take positions accordingly, before others do. We could all see what’s happening, but the FED sees it just a bit earlier. And most ‘investors’ just look at the FED to see what has happened.

CRV, I like your point about the FED’s concerns over risk. But, in spite of their timing advantages, they were completely blindsided by the 2008 collapse which they should have seen coming for about 3 years. Same for their obliviousness regarding savings and loan deregulations, shadow banking, asset bubbles from yesteryear, and currently cryptocurrencies, to name a few.

Are they proactive (steering the market) reactive (to waves) or reactive (to waves)? I think they’re busy with three-martini lunches followed by long naps, way too often.

To my comment re: the 2008 collapse that “they should have seen coming 3 years earlier”, is this reference to Robt. Shiller’s revised book:

“The second edition of Irrational Exuberance was published in 2005 and was updated to cover the housing bubble. Shiller wrote that the real estate bubble might soon burst, and he supported his claim by showing that median home prices were six to nine times greater than median income in some areas of the country.”

It’s not as though they didn’t know who Shiller was or whether or not he knew anything about the housing market… Shiller was at Yale; Bernanke was from Princeton.

Sorry about over-participating, but I’m quite pissed. I forgot to mention the .com bubble which popped in 2000. Shiller’s book was first published to warn about THAT bubble.

I just cannot excuse the FED, with all their friggin’ PhDs, for watching the market madness that went full throttle in the late 90s, with them having valves and switches to tamp down stock market activity (I can’t blame them for the entire mess!), and they just watched. Just let it rip.

CRV, your comment about them having a timing advantage just set me off…

After 60+ years of watching RE mkts in FL, CA, OR, and various flyoverstan locations, I AGREE TOTALLY How!!!

Even in the mid ’80s, many folks in CA were displaying ”End the FED” bumper stickers due to the bad timing and bad to very bad for WE the PEONs activities of the FRB.

The FRB is a tool of the banksters and the oligarchs that own them and the corrupt puppet politicians.

NOT an institution to help WE PEONs by providing ANYTHING for us.

Great stuff How Now, I just can’t help thinking about how the irrational exuberance has morphed into the Plandemic Jubilee! Yeah, the FED doesn’t have our backs, well only in one way I can think: Dolchstoß, stab in the back.

What is the Fed supposed to do about cryptocurrencies? I’m no defender of the Fed but they seem to be an easy punching bag because our expectations of Congress are so low. Surely, it falls in lawmakers domain to… make laws about such things.

All sorts of projects are underway at various agencies, Congress (and some state legislatures) on crypto. Part of the issue is, crypto straddles various traditional regulated things. Is it a commodity? A security? Banking? The answer is yes, in some cases for each. We start in a free country with the premise that something is legal unless a law declares it illegal. There is a lot of fog there. Thanks to the open Internet, people just started hawking stuff like some guy selling steaks off the back of a station wagon in your local parking lot. Somebody in government had to see them, then figure out what they were doing. From a standpoint of individual risk, do you buy pills from people on the street you don’t know? It is buyer beware unless the stuff is regulated, especially with all the opacity in crypto. A seller could just do a rug-pull and disappear,or be “hacked.” People in the crypto business are openly awaiting a wall of regulations.

And there are offshore sellers, including very large crypto exchanges operating right now. Some of these operations may be illegal, but hard to police and enforce when people just buy the stuff on the Internet. It is like Internet gambling; it is simple to evade location screening, and some crypto businesses have tutorials on how to do it. Enforcers have had to come up with new tools, like creatively applying sanctions to prohibit any dealings with a particular business entity, which may now be a smart contract platform without a locatable operator.

phleep, as you know, some of these crypto entities are publicly traded, so it isn’t limited to selling stuff from the truck of a car. The SEC is involved. I guess that a company selling snake oil could go public, but the FDA should weigh-in if it’s making fraudulent claims or is a danger to health (post tobacco, et al…. :)

And it’s not as though the FED is sealed-off from Congress or other agencies to advise them that there’s something funky going on. They police money-laundering… the FED controls the money supply and crypto is a direct threat to the dollar.

No, I’m not suggesting that it’s the FED’s responsibility. But they shouldn’t be deaf, dumb and blind to it, either.

Why make anything about crypto? Let it implode on itself, if that’s what it’s going to do …..

To regulate is to give legitimacy, no? I see any regulation as a prelude to bailouts. Do you want to bailout the “cryptobro’s”?

“:Surely, it falls in lawmakers domain to… make laws about such things.”

No, it doesn’t. Really

No need to fix stupid.

Crypto is nothing. The only reason it exists is due to the asset mania. If the asset mania is allowed to collapse as it should, it will disappear where it came from, which was also out of nothing.

Why does nothing need regulation?

@ HowNow –

The FED is very smart. What they do, they do on purpose. They serve their owners, the Banker/Wall Street class. The goal is an indebted worker class to provide lots of servants and service and protection if war is waged. They want your productive capacity to their benefit.

It is all very purposeful. It is all very simple. Keep a good stock of wage slaves and debt slaves. Sprinkle around some BS about patriotism. Rah, rah, rah.

Fed has hundreds of PhDs in economy and other related field on their payroll, mostly from big schools. Fed making mistakes consistently speaks volumes about the quality of these ivory tower educational institutes.

I think it was Wolf who pointed out the Fed uses indicators that are lagging. No choice but be late.

I imagine this gives the privates (so to speak) a chance to use their leadings to prepare for what is coming.

Is lagging part of the Fed charter? What would it take to change it?

“can take positions accordingly, before others do”

As could anyone listening in to their meetings in real time. I’ve wondered what kind of information security they have considering the value of advance knowledge of their meetings would be and from a look at the FOMC meeting room with huge windows shown in the WSJ article “Go Behind the Fed’s Closed Doors,” I’d say it was close to zero and the furthest thing from a SCIF one could imagine.

Commenters here forget to mention the FEDS dual mandate. Employment and Inflation. The fed pushed rates down yes to inflate home prices but to also stimulate the cash out refi market. I took advantage of this “gift”. It was hard as a retiree to do a CO refi but the proceeds went 100% into a whole house renovation of our 27 year old home. Our P&I went up barely $300. It has been a much better return then investing in the Market or Treasuries. We got in early before The chip shortage hit appliances and the escalating cost of materials.

It did help stabilize the employment market especially in the home improvement industry. First time home buying Millennials who were employed and working from home did buy houses or took advantage of lower rates to refi reducing their monthly payment and freeing up money for daycare. The Gen that definitely went “wild” were Gen X with stable jobs and no day care requirements with pools and cars.

I do agree that the FED waited to long to remove the cookie jar. But no one could predict the increase in inflation from the war in Ukraine, the ridiculous zero covid policy in China with its continued effect on the global supply chain, and the long term global drought from climate change that continues to ravage the agricultural sector.

Blame the Fed for Everything is the permanent everyday cheap shot in comments here.

The failure of the American people through Congress to decide a lot of important things has dumped a lot of weird rescue jobs onto the Fed.

Agreed on Congress, the “broken branch” of government. But calling out the FED’s repeated negligence is not a “cheap shot”.

They have loads of resources. And ignoring warnings from someone like Shiller, regarding TWO bubbles, is genuine negligence. He’s one of the foremost economists on “economic behavior”, a Noble Prize winner, the author of the Case-Shiller index, and an esteemed professor at an Ivy League university. Those f’in’ PhDs should have given it much more consideration. Shiller said in a talk that in 2005, only one paper had been written on the possibility of a housing bubble at the FED. When he contacted the author, a researcher, that guy “walked back” his critique – didn’t want to make waves. (sorry if you heard this from me before)

I agree that the Fed is not solely to blame. There is also plenty of blame for the US government. Reckless spending is the other side of the coin.

But government is basically to blame for the WHOLE ENCHILADA!

The function of government should be to enact and enforce laws that maintain stability, spread wealth and negotiate trade deals that benefit American citizens. Nothing more, nothing less.

If the economy

Phleep said: “Blame the Fed for Everything is the permanent everyday cheap shot in comments here.”

—————————————–

What is cheap about it? The FED deserves much more criticism than they get.

Cheap shot? How can you respect a central bank that employs emergency measures for 14 years. Why was the central bank buying MBS when housing inflation was running at 20% per year nationally and 30-50% on the West Coast?

Also, don’t forget that we are in our third massive monetary bubble in 25 years.

Inadequate legislative policy does not justify absurd experimental monetary policy.

Toute nation a le gouvernement qu’elle merite.

Each country gets the government it deserves.

~Joseph-Marie, comte de Maistre, 1860.

A Frenchman for today. And Germany, imploding for the third time in 100 years?

When you manipulate interest rates then you own whatever happens.

@ Sailorgirl –

spoken like a true FED apologist …………..

Stimulating the economy and reducing unemployment by inflating bubbles is peak insanity in monetary policy. Managing the economy and labor markets is Congress’s job, not unelected bureaucrats. Not that Congress is less of an abject failure these days.

Inflation was raging high ever since last year or so.

A lot of people, rightly so, predicted the inflation tsunami.

Fed somehow found a mantra and was parroting ‘transitory’ for quite some time.

Problem with dual mandate is peak labor happens after the landing whether it’s soft or not. If you wait on labor market to turn down you are too late.

Fed is in a mess. With mortgages at 6% plus they probably have done enough real world slowing, but they can’t stop because of saying inflation was transitory when it was not.

The FOMC does not operate outside of the same world everyone else does which means they have been infected by the same manic psychology over the last quarter century. It’s the best explanation of their hubris where they could actually believe their central economic planning (monetary policy on steroids) would actually work as they claim.

As for your analogy, as the supposed captain of the ship, the FRB can only steer where the current will let it.

When market sentiment (the current) turns decisively against them (where they find themselves with inflation sentiment now), they can either change course or sail the economy and financial system into disaster.

No, they aren’t masters of the sea, much less the universe.

“They have front row knowlege.” This is really rich. These guys have been blindsided by every crisis of the past 50 years. All they know is what bankers and politicians tell them. And those guys only lobby for what benefits them personally.

Not sure I’ll get past the censor on this, but here goes. You know how “quiet quitting” has been in the news for a few weeks now. Well, it’s always been a thing, especially in the public sector in which the fed resides.

Out of interest, in the chart entitled “Fed’s MBS, From Crisis to Crisis” and for the period 2013-2015, it is clear there was some sort of crisis. Something broke.

I’m not suggesting it’s your responsibility, but without a crisis label, there is no accountability for a USD one trillion money print, and that’s just for MBS.

I heard the news today o’boy.

+1000

My first reaction was George Jones:

“He Stopped Loving Her Today”

anon, me too. I wonder whether Wolf’s title was based on that song, or just a sigh of relief: “They stopped buying MBS today”, words and lyrics by Wolf Richter.

Correction: music and lyrics…

My first thought as well and I have been reading the comments to make sure that someone mentioned it. “Great minds, … etc.”. LOL!

Djreef,

Indeed.

I also noticed this yesterday that the Fed scheduled no MBS operations for the period betwen Mid September and Mid October. On the other site, that is also a sign, that no or much less principal payments can expected from MBS. No wonder when the 30 year mortgage rate is at 6.33%.

I think this would be (very) difficult for the Fed to roll off the entire MBS portfolio, mainly when the mortgage rates are so high. The only solution could be outright sales, but in this environment and the primary dealers will only buy MBS when theyself have a buyer.

The Fed makes the mistake buying MBS too much and too long. The better way was when the Fed start to sell off MBS in the second half 2020 and in 2021 where the real estate market was in good condition and the hunting for yield was high.

Clearly this pushes debt costs up but does it spark a trend? I mean when interest rates are going down, debt gets cheaper you can expand production (itself deflationary), but when debt costs going up then more expansive to expand production which is a reinforcing cycle the other way.

What I mean, the big question, is whether as we go through this inflection(?) point on real interest rates and its global its not just the US, does this become a decade of ever increasing debt costs i.e. is the trend self-reinforcing? For example, I mean 2or three years of high interest costs on a mortgage isn’t really that much of a pusher because they are 25 years in duration. In the US they are usually long term fixed rate as well, immune to Fed actions.

If the interest rate cycle really ended in 2020 after 39 years, it won’t be two or three years of “high” (actually still ridiculously low given the actual credit risk) interest rates.

It will be several decades of increasingly higher interest rates, at minimum. It just won’t be a straight line up. The prior cycle lasted from the 1940’s (1946 I believe) to 1981 but rates weren’t noticeably higher until the late 60’s or early 70’s.

The actual fundamentals are now a lot worse than either the 40’s or late 60’s.

Debt burden is too high and economic growth too low. Unless you are going to default, real rates are still in long term trend lower.

Who has been expanding production? Most income goes to stock buybacks, right?

JeffD: I was thinking the same thing. I wonder how different this situation would have been if stock buy backs were illegal and all the cheap money had to be used for production related enterprises.

Agreed. Look at the current buyback activity, even in light of the current interest rate/economic backdrop. These reckless executives still spending billions on buybacks before the new tax legislation hits. One last C suite bonus extravaganza before the whole thing implodes. These guys are simply Brilliant !

Thanks for all the solid information, charts and commentary Wolf. You nailed the landing on your rate hikes and inflation calls. Inflation is a huge issue(and sticky). 2023 is going to be a very tough year, especially for US citizens who are on the lower rungs of the economic ladder.

People know they have been screwed and see how the cream floated to the top over the last few decades (while they struggled with low to no wage growth). The wheels of the machine are greased with the blood, sweat and tears of the populace.

.Gov and the Fed created this monstrosity

You are a daily “go to” site for me

Agree completely. The plight of most of our rail workers is very disturbing. The “deal” it it holds isn’t an answer either – it’s little breadcrumbs. These unions aren’t really representing the workers.

2023 is going to be a year of growing unrest and if wildcat strikes become a significant thing, I will not be surprised at all. There’s only so much people can take.

LOL – railroad men have been the worst eggs in the “labor” movement in my experience, which included; paying dues to Teamster, UAW, and Carpenter bureaucracies back in the day.

Drove 4-man rail crews to and from the Kansas City yards in 1983 and hearing the highest-paid industrial operators of the time, bragging about hiring non-union labor to roof their houses and fence their horse areas brought their hypocrisy home to me on a regular basis. These crews worked trains in from Nebraska, Kansas and Missouri and most of my trips were taking them home. They were the ‘kings’ of their podunk towns and their hubris spilled-over into every conversation I ever heard; often with two crews in the stretch-van. So cheap that they’d stall me up to an hour regularly at the diner, for the purpose of making overtime on the ride home; which was more than I made on a round-trip; a lot more as I recall. They knew I wasn’t paid by the hour and they didn’t even buy me a cup of coffee, much less breakfast. They turned a potential (realistic) $8-an-hour job into $5. Unbelievable pathology: insert 4-letter words here for railroaders.

“The purpose of MBS purchases was to repress mortgage rates and inflate home prices.”

Because history has shown that central planning is always the best way to go.

Looks like the Realtors(TM) will be jingle-mailing in the keys to the leased Lexus/BMW over the next few weeks. Guess they should learn to code, or find some skills other than unlocking a door, pointing out a furnace, and handing you a 10-page contract and pointing where to sign.

I received a voicemail from a Realtor asking me if I want to sell my house “while the market is still hot” just a few weeks ago. No thanks. Why sell and get rid of my very comfortable 2.625% mortgage rate? To hope to time the market and get in a bidding war for a rental in the process? To buy another property and get twice the interest rate?

The fed has created such a debacle in housing. They had no business buying MBS whatsoever past September 2020, when it was clear COVID alone was making the market hotter than it was before. Yet they decided to keep pouring fuel on the fire for another two years. Powell never should have been re-nominated.

The real travesty is a healthy housing market shouldn’t have such boom and bust cycles. I feel for anyone stuck in a rental going up 10-20%, yet priced out of housing, lest they buy a house and catch what is obviously a falling knife. It might be years before the interest rate/price balance comes back to a place where affordability returns to where it was even a year ago. It is unfortunate that the American dream of “work hard, save for a house, buy when ready” is effectively dead, thanks to the fed.

“The real travesty is a healthy housing market shouldn’t have such boom and bust cycles. I feel for anyone stuck in a rental going up 10-20%, yet priced out of housing, lest they buy a house and catch what is obviously a falling knife.”

Amen. I’ve been stuck in a paid off starter home since 2019 with 3 kids because I can not fathom how inflated house prices have become. What scares me even more is buying a house and being underwater by 50%+.

Just not worth it.

Damn, you’re stuck in a paid off home. Gee, that must really be tough

You must not have three kids. Gets a little crazy when raising them in a 1400 SQ ft house when they are teens.

Consider yourself blessed congrats

Does the Realtor send the same email to prospective buyer, like umm, “Do you want to buy a house while market is still hot?

We were looking at the very beginning of the Bidding Wars, which we didn’t know about at the time, and thus got outbid on the two we made offers on. Several months ago, I started getting emails from realtors and mortgage originators I hadn’t corresponded with in over a year. I politely declined, and the calls/texts have stopped again, thankfully. My guess is that layoffs have begun. The sales volume around here (non-Boston New England) is a trickle nowadays, inventories still tight, and median sales price is STILL rising in my small, fairly grubby city. I can’t wait until we start to see what’s happening elsewhere.

This was an easy choice for those of us with multiple homes to sell late 2021 or early 2022.

But for those folks without multiple homes people always get forced to sell for a wide range of reasons beyond their control. Divorce, loss of job, relocation of job etc.

SC7, I am sure you will be pestered with re-fi offers as long as you own the place as my father-in-law was. He bought his home at the previous low in mortgage rates and laughed at the bank’s re-fi offers as rates went into double digits in the 1980s.

“The purpose of MBS purchases was to repress mortgage rates and inflate home prices”

Translation: Not capitalism. A private company manipulating asset values for it’s own gain.

Agreed. And it went on for almost 14 years. As I said in another post, Congress should pass a law baring the Fed from purchasing MBS, but we all know they won’t. Even issuing / purchasing treasuries beyond what’s needed to fund the government needs to have parameters put around it. The Fed should NOT be able to throw such egregious amounts of money at the system, even when there’s a global pandemic. The mere fact that Congress let’s them do it shows how unrestrained the entire system is and benefits primarily the wealthy that risk management in a capitalist system is supposed to require. There’s a simple reason why Japan has negative rates. Their debt burden is so massive, they have to push rates negative, otherwise their interest on the debt would quickly swamp them. We’re rapidly approaching the same issue here in the US. By FY 2024 we could be interest expense @ $1T, and notably lower tax receipts from where they are today. It’s possible tax revenues will drop back to $3.8T 1/3.8 is 26% of our revenues going to meet the very first thing that must be paid, interest or we default. And don’t let people yack about it being so little relative to GDP. You can’t tax the country’s entire GDP, so IMO making that comparison is crazy.

All these mortgages originated and then wrapped up into federally backed securities is reminiscent of the Savings and Loan debacle in the early 80s in which S&L restrictions on investments were loosened. The S&Ls ventured out of their local purview and ended up taking way way too much risk in distant projects.

A question regarding the Fed and long maturity securities….

“Why are they involved at all in long maturities?”

The Fed did not dabble in MBSs until 2006, and now 2.7 Trillion?

Not to mention their ownership of Treasuries ten years and out.

Stimulating employment and maintaining stable prices …the famous “dual mandate” has little to do with long maturities.

It seems, the Fed is allowed to go “off the rails” whenever it benefits markets, stock or real estate. And now, here we are, and the Fed is in a box.

The S&L crisis was predicted in May 1980 in IMTRAC (Dr. C.Y. Thomas’ publication) by Dr. Leland J. Pritchard (Ph.D. Economics Chicago 1933, M.S. Statistics Syracuse). The DIDMCA of March 31st turned the nonbanks into banks by permitting demand drafts.

Dr. Pritchard also predicted the GFC, the domination of the GSE’s in the bond backed mortgage markets, and that M1a would end up approximating M3. I.e., the FED’s Ph.Ds. don’t know a credit from a debit.

Google “The housing market is on fire. The Fed keeps adding gasoline.”

That article on CNN is dated June of 2021. So if the mainstream media was reporting that in June of 2021, that means it was well known that Fed policy was inappropriate for at least 3 months before. That means that they knew in March of 2021 that they shouldn’t be buying agency MBS, and continued to do it for another whole year.

That was inexcusable. And they would have continued it too had the blowback not been so severe.

There are still plenty of economists that actually believe the Fed is making a mistake to execute QT, that they are over-reacting to supply side shocks.

Yea, they still believe that crap.

I do think we are headed for a very sick economy very soon. The Fed must hit the markets hard next week with talk and action. Before the Nov election they want to be able to claim that inflation is back under control.

So watch for an ugly couple of months.

Some of those economists probably claimed that the solution to the country’s financial problems is to let inflation run hot for a few years.

“Yea, they still believe that crap.”

That’s what happens when someone gets the hubris disease, in this case believing that their version of central planning will work longer term.

People talk of monetary “policy mistakes”. Some have claimed QE-2 was one and others will presumably claim the current rate hikes and QT are one.

No, the real and only policy mistake is the very existence of monetary policy. No one knows the “correct” price of money (interest rates).

“No one knows the “correct” price of money (interest rates).”

I agree, but whatever the correct price is I’m certain it isn’t zero or negative so those are blatant policy errors.

Sheila Bair and Brooksley Born are the only two honest, competent public servants who made it to high financial office since Volcker. I often wonder who in government F’d up and let these three people filter through.

PS If I remember correctly, Sheila Bair has recently been advocating an emphasis on QT over rate hikes.

It’s Nobel laureate Milton Friedman’s “Fool in the shower” metaphor. There is no “Fool in the Shower”. Contrary to economic theory, & Nobel laureate, Dr. Milton Friedman and Anna J. Swartz (“Money and Business Cycles”), monetary lags are not “long & variable” (A Monetary History of the United States, 1867–1960, published in 1963). The distributed lag effect of money flows have been mathematical constants for > 100 years.

Trying to process the effect this is going to have on markets, outside the obvious upward pressure on mortgage rates, credit tightening, and housing market.

Yes, the visualization of smoke billowing from my ears is accurate.

As someone, who started in the Loan Origination business in 2004 and exited in 2020, the current model of the FED being the final stop of the mortgage money train is all I’ve ever known. I know other MBS buyers are out there, but the FED must be the biggest. So:

The GSE’s publish the guidelines providing a framework the banks follow as they create mortgages that conform to those guidelines and then the GSE’s happily accept as they have/had a guaranteed buyer, more or less, that they could sell those mortgages to once they securitized them.

The other 35%, or so, of mortgages that didn’t conform to the GSE’s guidelines went elsewhere.

That’s my understanding of how it’s worked for the past 12 years, or so, or since Dodd-Frank.

Ok, finally to the sincere question.

Now that the FED (tentatively) is ceasing to purchase MBS, how does this impact the mortgage market in terms of lending, specifically?

Does the potential credit crunch make financing so difficult that the wealthy, inflation/recession, proof crowd emerges to gobble up the housing market Pac-Man style? (Creating higher rents and homes/apt’s packed with people?)

Are parts of Dodd-Frank repealed, opening the market up to some of the pre-2008 practices?

I’ll leave it at that since I have a habit of leaving comments the size of an additional article, sometimes.

Just trying to figure out, at least some, of the side-effects to this action.

Let me known when you get a response to your important question. Can’t really find anything online that I too was wondering…

I wouldn’t think that the Big Money types will “emerges to gobble up the housing market Pac-Man style?” They did that after the 2008 crisis when housing prices were already low and unemployment was already high. There wasn’t much chance of losing money on THAT strategy.

To do it now would be to try and catch a falling knife… the higher rents you collect have to outpace not only the higher interest rates you will be paying but also the drops in property values of the houses that you not only are buying now but also that you already own.

If Blackstone really does have 50 billion sitting in a fund just waiting for the prices to fall, interest doesn’t matter much.

We really need to get private equity money out of the real estate game. If people want to rent a home out, fine, but when Blackrock uses 50 billion to buy homes and then uses their massive influence to write government rules that turn people into debt slaves, isnt that a core part of our problem?

What we really want is for the system to flush itself out.

I actually have an idea that a very large tax on undeveloped property could ignite extensive home building, which is good for the economy. It would lower the portion of housing that is based on property value and make home values closer to replacement cost.

When people hoard unproductive resources that other people can put to good use, we should find ways of increasing the pain on those people.

game tv said: “We really need to get private equity money out of the real estate game.”

————————–

+ 10

and get the Government and FED out as well

@gametv,

We don’t need more laws/regulations. We need to take some away. Eliminate capital gains exclusions, mortgage deductions, depreciation schedules, and the ability to deduct property taxes and closing expenses and improvements. If you want homes to be priced as a place people live rather than an investment, you have to take away all investment incentivrs. And I do mean all.

Ricky,

“Now that the FED (tentatively) is ceasing to purchase MBS, how does this impact the mortgage market in terms of lending, specifically? Does the potential credit crunch make financing so difficult that…”

As the Fed steps away from the MBS market, it will make mortgages more expensive (higher interest rates) but not more difficult to get per se.

But a higher rate will disqualify a lot of people at a certain price level, and so prices will have to come down for there to be enough qualified buyers.

Wolf

I’m with you there… and thank you.

I guess I’m trying to get a sense of what may be happening behind the curtain as the FED steps away.

Do the GSE’s, banks, institutions, and HF’s resume holding the debt? There must still be a pipeline to push through the secondary, and you can’t just flip the sign on the MBS window from “open” to “closed” without a redirect, right? I know we’ve all been prepped for this and now that it is here, I feel I have Vertigo.

Maybe I’m making a mountain out of a mole hill? I don’t know.

Then we have the big guy over at BIS talking about fintech, global regulations, and supervisory capacity. FedEX… and on and on.

So much going on that I know there is an opportunity waiting, wide-open, for that financial touchdown. Too bad I’m spinning like a top.

Although, I’m sure the market lined with beartraps right now.

I personally believe that Blackrock and other PE firms have massive impact over government policy in many areas and have used this influence to the detriment of many people.

They were able to pay off Sinema to squash the carried interest provision in the latest Democratic proposal. Can you imagine that? There is literally ZERO reason for PE firms to get away with this tax scam, but it never gets changed.

The one big difference between 2008 and now is that there was no inflation back then. So the Fed could step in with cheap credit and put a net under the housing market.

This time, it goes down much further.

By the way, my new conspiracy theory is that Blackrock has massive influence on the Fed and wanted to create a housing bubble, so it would burst and they could do two things 1) buy homes cheap and 2) have plenty of renters with poor credit due to foreclosures. That allows them to turn those poor people into rent slaves. So those really rich guys used their influence to get the Fed to insanely pump up the bubble.

Wall Street loves boom and bust cycles. An economy that was very stable would not yield the same profits. Volatility is the friend of Wall Street insiders.

We really need to get some grenades (figure of speech only) and blow up Blackrock.

Number of homes under construction seems quite high, higher than the 2008 peak. Can builders sit on these partly built projects or will they need to be completed and add more inventory to a cold market in the coming year or two?

Houses will be on sale for those with cash. The price is the same if the higher interest rate equals the same expenditure for the same house. Price or terms take your pick, unless you are fortunate enough to have the cash to take advantage of the lower price that is caused by the higher interest rates that you don’t have to worry about.

I don’t know if this situation was actually planned this way, but nobody makes money when things are flat. Volatility makes money if you are on the right side of the trade at the right time.

I’m not but can see it coming.

Want a fix? End the Fed. And also end Congress, a malicious cesspool of corruption. Democracy ended in the US decades ago, all that’s left is the Circus.

Campaign finance is the problem. These political campaigns shouldn’t last more than a few months and contributions should be no more than $100, from living and breathing American citizens only. Corporations and businesses, of any size, do not serve the country – do not serve in the military – and should have no rights in respect to electing human beings for political offices.

“Does the potential credit crunch make financing so difficult that the wealthy, inflation/recession, proof crowd emerges to gobble up the housing market Pac-Man style? ”

Most of these people are about to lose their proverbial shirts if the credit cycle has actually turned. They mostly own absurdly inflated assets with limited if any substance with much of it bought on credit.

735 billionaires in 2021 according to Forbes versus 13 in 1982 or 1983. The country didn’t miraculously get that much richer in the last 40 years and it’s not due to price inflation either.

It’s due to the asset and credit mania. Look at Adobe’s acquisition this week, paying $20B for a software firm with $400MM in annual revenue. That’s insane .

Been in the industry for about as long as you Ricky. Trying to figure out the same thing….how do we make the best out of this? What to short….

1) Blame the Fed. Pray to God. The end is near. The Fed sucked liquidity, raised rates, provided plenty good collateral to prevent 2008 “event”.

2) SPX for fun and entertainment, in the bulls/ bears casino :

3) Option #1 : perma bulls : SPX to 6K/7K. Buy today, before it’s late.

4) Option #2 : Perma bears : not yet. Not before SPX reach 2,800 and test it twice, thereafter, in a sling shot to Mars & Saturn rings to extract rare commodities. 5)

Michael, do your comments come with a plain English translation? We in major bear market for stocks and bonds, what is not to like??

5) Ilan will build Noah’s ARKK on Mars.

The Fed’s wealth effect policy to dis/en/courage consumption is completely intact. That is the essence of central planning that enslaves people and subverts the rule of law under which the Fed was originally chartered. QT is just as tyrannical as QE.

Would we be better off if

*There was a formula for Fed Funds the Fed must adhere to…ie = to inflation?

*If instead of all the QE, Repos, RRP, QT and the Fedspeak that surrounds all that…..we had for the past 14 years had Fed Funds at 2% and 30 yr mortgages 5.5%….would we be better off and the markets healthier?

*If money supply could only expand via a PULL from an expanding GDP and at the appropriate rate to meet that pull?

*If the Fed only dealt in short term federally backed paper….like they used to?

Yes to all of the above.

It is a very legitimate question as to why we need a central bank at all.

It’s above my pay grade, but there have been higher level mathematicians that have ran analysis that can demonstrate the last decade of experimental Fed policy did virtually nothing for the real economy.

So an asset bubble with the coming hangover is all we got from the Fed.

“The Fed has said many times over the years that it wants to get rid of its MBS entirely, and that it wants only Treasury securities as assets.”

Congress should pass a law baring the Fed from purchasing MBS, and the Fed should forced to start selling its MBS holding immediately and to have them off their books by the end of 2023.

The Fed has absolutely no business manipulating the residential mortgage market to the tune of almost $3T over 13 years. Absolutely none. Any economist or bureaucrat who supports such actions does grave harm to our economy.

I live in NW ATL in a city called Woodstock. It’s a nice area. Just down the road is Alpharetta, a really high end city. There are 2,700 SQ 1-2 year old houses around downtown Woodstock that are selling for $850K which is just absolutely obscene. What’s crazier than the Fed’s actions is the fact that there’s so much money out there in Woodstock GA willing to pay these drastically inflated prices.

Now, I get the fact that a significant part of this new wealth is coming from people who’s baby boomer parents have started to die off, resulting in the biggest transfer of wealth America has ever seen. But, how do these people think these prices are going to sustain themselves? Everyone says this time is different. We don’t have the 12% of total loans that were subprime. Well, is very true, but we do have nearly 95% of all houses bought in the last two at astronomical prices at really low interest rates until June of this year.

In order to return some semblance of sanity to the residential housing market, prices will have to fall at least 30% over the next 2-3 years.

And as I’ve said many times, what does the Fed / Congress do when prices really start to fall off the cliff? Does rent & mortgage relief come back into vogue. These sorts of actions are criminal because it bails out the rich from the natural risk they take on when investing in mortgages or properties.

The taxpayer is on the hook for those mortgages, not any lenders or rich people. Once again, socialize the losses and privatize the gains.

The sooner MBS and long bonds are off the balance sheet the better for the middle class. Being priced out of homes and schools and cars, 2020s will go down as a travesty of a decade for the middle class in America.

Agreed 100%, but like I said above something has to be done to keep the Fed from being able to do this again.

That makes me mad. Leverage up a house at 33:1 and if it goes bad offload it to the taxpayer. Of course there is going to be a bubble.

I live in the metro ATL area and if I understand you correctly, you are referring to the neighborhood by the amphitheatre. I’ve driven by there because I like the condo building but I too think the prices are nuts. Some of those houses (with virtually no land) sell for about the same as the one my mother grew up in on Peachtree Battle Avenue in Buckhead, over $1MM

There is only one reason I can use to explain it.

Ever since the local riots and looting in 2020, escaping proximity to undesirable demographics and the potential crime that goes with it. That’s worth insane prices to quite a few people who can afford it, both now and in the future.

Forgot to mention, I don’t think Alpharetta is that great. It’s nice but there are other areas in metro ATL I consider better. It’s not an area I aspire to live in.

I agree here as well. If we did a deep dive into the Alpharetta area we’d get the same result in terms of whacked out prices.

Yes, prices are absolutely nuts. So anyone who’s acting like crazy high prices are really any different subprime mortgages are splitting hairs.

And to be clear, the house in question has a .05 acre lot with no garage. You park on the street. Yikes!

“Congress should pass a law baring the Fed from purchasing MBS”

I got a good laugh from this. I have no doubts that it was Congress that pressured the Fed into those purchases.

I give the wolfman a lot of credit for these three-times-a-week deep dives on some really hard-to-understand topics. Just terrific work.

AGREE,,, like totally dude or dudette KW!

And hence ”preparing” my twice a year support MO for the Wolfstreet.com GREAT HELP for this old boy who came on here at first just to see if WE, in this case the family WE, could get back into the SM that WE have been OUT of since mid 1980s…

NOT YET, but the education on here is SO worth the money that I am happy to send the Wolfster some dough, whenever I can, after the ”grands”,,, etc.

Seriously, probably saved us many thousands,,, SO FAR…

YES,,, please READ the article FIRST folks,,, thank you.

Three times a week? Wolf does 1 to 2 articles a day ,,,,,,,,,,,,, all deep and requiring deep background knowledge.

I hate-follow multiple 20-something year olds on social media who each own 5+ homes all on a mountain of mortgage debt.

Their entire worldview is real estate prices can’t go down so it’s illogical to do anything other than maximize your leverage.

Indeed.

There was an article in the WSJ recently how young professionals were buying homes on line, getting a management company, and renting them out. The example was a guy in NYC buying a place in Jackson MS. (how’d that work out? water issues.)

We speak of Blackrock and others buying up residential property to rent, but there are untold massive amounts of small pyramiding schemes out there involving highly leveraged sole proprietors or small partnerships.

I wonder what the banks are thinking.

I was also reading from a real estate article how a lot of young California Tech workers were doing the same thing.

I know of a couple twenty somethings that own a few homes they rent.

They did not go into this with the idea of being a landlord. Each time they moved for a job, they just kept the old house as a rental and bought a house where the new job was. One was just moved again during the past few months but chose to keep the old home as a rental but chose to rent a his next house because of the higher mortgage rates.

I think he owns 3 homes purchased in 3 cities over the past 6 years because of job changes. He probably now has a good $250k to $300k in equity on these 3 houses through price appreciation.

To add to ru82’s anecdote,

I know a youngish couple (30’s) here in central TX who have also accumulated multiple rentals over the last 5-6 years through the combination of moving and renting out their existing home, as well as directly buying SFHs and converting them to rentals. Thanks to the booming housing market in central TX over the last 2 years, they HAD almost $1mil in paper equity on what was a modestly leveraged balance sheet (2 SFHs with mortgages, 2 without).

But all that paper equity was burning a hole in their wallets and they decided to extract as much of it as they could in May this year to purchase a mixed-use property. Even then, these funds weren’t enough to complete the purchase, so they had to scramble and make use of a 5-year interest only loan with a balloon payment to close the financing gap. Now all of their properties are heavily leveraged, with the same equity as before (at the time of the purchase).

Look at recently sold in San Diego on Zillow. Has to be tons of loan fraud still going, 0 down ARMs where the seller is probably paying the straw buyer after close and then they flee to another state or even country without making a single payment. Saw it when i lived there in the last bubble, but this time its next level – tear downs in gang hoods going for 1m. Mariachi music playing all night, punctuated by gun shots.

But, don’t worry. This time is different! Just keep buying people!

To be fair, I was one of those 20 year olds in 2006. I only owned 3 houses, but they were 100% financed. I bought my first house in 2003, then refied that in 2005, took the cash-out to buy 2 more houses. I was going to be a real-estate mogul!

Lost 2 and was able to break even on 1. I learned my lesson. I was a renter until 2017

Glad you learned your lesson but all of these real estate dickheads should be Mao’d

I think that the Fed is going to have to SELL a large portion of its MBS portfolio this time. In the previous QT it took 30 months to drop a third of its MBS portfolio… but that was with mortgage rates still low. There won’t be as many people trying to refinance for a lower interest rate or to cash out some equity this time.

Refinance, no. Cash out? I think there is a possibility that could increase quite a bit, as home equity loans.

Home equity loans don’t have an impact on MBS. In fact the Fed will end up holding its paper for longer if people get HELOC’s rather than doing a total refinance.

Who will want to buy the Feds MBS that pay 3 or 3.5% when they can get a 2 year or 10 year treasury that is much safer.

Mish over at MishTalk firmly believes that the Fed won’t make it’s MBS runoff in the coming months now that it’s supposed to be full bore $37B a month. We’ll know by the end of the year, if he’s right or not.

“Believe” is something people should do in church.

I would like to see the Fed announce they are increasing sales of bonds to 200 billion per month next week. That would finally put a dagger in the inflation, probably killing the markets for a little while.

The Fed should unload all of its MBSs and accelerate unloading of their balance sheet and stop trying to peg interest rates. Let interest rate assume their natural level whatever that may be. Fire half of the Phds on the Feds staff and save the money for the taxpayers.

I agree with you but if this happened, interest rates would completely blow out a lot faster than will ultimately happen anyway.

Actual credit quality is so poor (the lowest in history) that most borrowers would be locked out of the credit markets.

Substandard or basement level credit quality is clearly evident for the USG (worst since at least WWI if not the Civil War) and corporates.

State governments, housing, and consumer only looks good because of the fake economy which is substantially due to suppressed rates.

Make that WWII, not WWI.

And they need to stop the BS reverse repos that are parking almost $2T in excess liquidity that the Fed is paying upwards of $100B a year to all the companies like Fidelity & the big banks to hold this liquidity. And, they ended reserve requirements back in March 2020. The Fed has literally gone rogue.

You’re funny. Reverse repos took $2.2 trillion in excess liquidity out of the market. Thank god!! Otherwise that $2.2 trillion would be chasing asset prices higher. They need to do $3 trillion in QT to remove that excess liquidity for good — that’s what they need to do at a minimum, and the reverse repos will go to zero on their own.

Colluders, counterfeiters, market-manipulators…

If you or I were to engage in behavior literally 1 millionth of the degree of these scumbags the “authorities” would swiftly lock us in a cage.

Tim R some will choose to believe Adam and Rebekah Neumann and their latest direct alliance and support, Andreessen-Horowitz, are completely reputable. Intelligence, ambition, and business-saavy should not be confused with honesty and actual ethical behavior.

Tim R

You are not the government. You are not in charge of guaranteeing others’ rights in an even-handed public way, or managing the dollar in a global economy. You are a privateer. Totally different categories.

Ha Ha. You are funny. “even-handed public way.” Do you work for the government?

Yes, that is hilarious.

Sorry, off topic, but when FedEx says packages are sharply down “in every segment”, I can’t imagine a more relevant SHTF barometer.

Also seems like an inflation barometer. Given the reporting lags that exist, one might say FedEx’s business is a leading indicator for what the retail sales portion of CPI is going to look like a few months from now. Product inflation has already begun dropping off, and service inflation can’t hold for long thereafter. FedEx is telling us their business is cooling.

You guys need to read beyond the headlines. Most of the FedEx issues were in EUROPE and ASIA. This headline reading is a huge factor in the dumbing down of America. It causes you to come up with wrong conclusions.

So I’ll just repeat what I said yesterday:

Most of it not in the US, but due to its troubles in Asia and Europe at its Express unit.

Its FedEx Ground in the US, which delivers the WOLF STREET beer mugs, also has problems, and I should write about it, and I might, because I have never seen such a clusterf**ck, something has seriously gone wrong there recently in terms of service, and I’ve been sending out the beer mugs for a few years, and I think it’s driving customers away to UPS and others. Nearly every mug I sent out over the past four weeks (there were lots on my Mug List for the past nine months) was delayed somewhere, often for days.

These endless constant delays, sometimes multiple delays for the same package, are NOT a sign of lack of packages to ship, but a sign of a huge operational problem. FedEx Ground is run by contractors, and those contractors are in dispute with FedEx, and FedEx is now suing its largest FedEx Ground contractor. This is really bad.

I noticed something similar with my FedEx deliveries. Packages seem to be stuck in facilities for days with no movement. I try to avoid FedEx where possible.

I’ve learned, when I’m expecting anything, via FedEx, to divert the package to a Walgreen’s nearby. However, their app won’t let me divert until the package is close to me. It’s an option that shows up later.

Otherwise, the FedEx folks will not make any effort to ring the buzzer to call me to the security door of my apt. bldg. (as I put in the delivery instructions). They just slap their stick-it “attempted delivery” slip to the outside of the security door and drive off was th my package. I’ve been told that their drivers are just extremely pressed for time.

I avoid FedEx whenever possible. I dread dealing with them.

USPostalService drops packages at my apartment door (inside the secured hallway) since they can access all of our buildings.

UPS presses my buzzer (as requested by me in the notes/instructions). On their app, it’s very easy to divert package to one of their local UPS stores, if I’m going to away or out of town.

Sorry I paraphrased from deep inside one of the many articles I read start to finish.

“We’re seeing that volume decline in every segment around the world, and so you know, we’ve just started our second quarter,” he said. “The weekly numbers are not looking so good, so we just assume at this point that the economic conditions are not really good.”

At least my conclusion was upgraded from “stupid” to “wrong”.