Retail sales amid record worst inflation in durable goods and red-hot inflation in nondurable goods.

By Wolf Richter for WOLF STREET.

February and January are the worst months of the year for retailers, after the huge holiday season binge. Large seasonal adjustments attempt to iron out the plunges in those two months from the November and December binge.

And for the past 14 months, we’ve got a new biggie in the mix: a record rage of inflation in durable goods and a huge bout of inflation in nondurable goods.

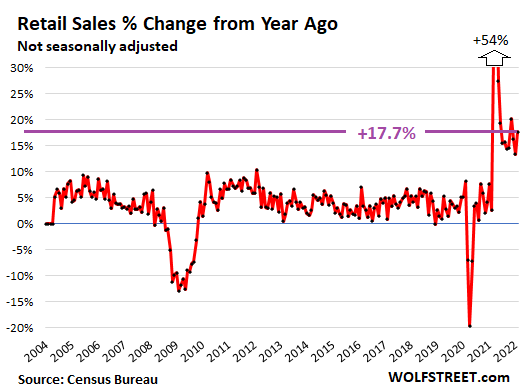

Not seasonally adjusted, retail sales, at $577 billion in February, were up a stunning 17.7% from February last year, according to the Census Bureau today. This was a huge massive gain, showing that Americans are spending hand over fist to keep up with price increases:

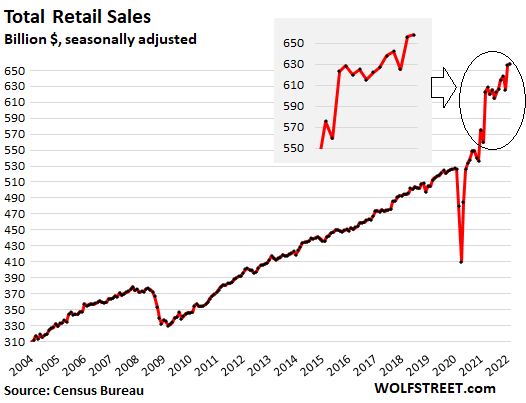

Seasonally adjusted, retail sales ticked up in February from January by 0.3%, to a record $658 billion, on top of the spike in January, and were up 17.6% year-over-year:

But then there’s the biggie: Raging inflation.

Retail sales are sales of goods, both durable goods (such as cars, electronics, and tools) and nondurable goods (such as food, household supplies, and gasoline). Retail sales do not include services such as healthcare, rents, and plane tickets. The retail sales here are not adjusted for inflation.

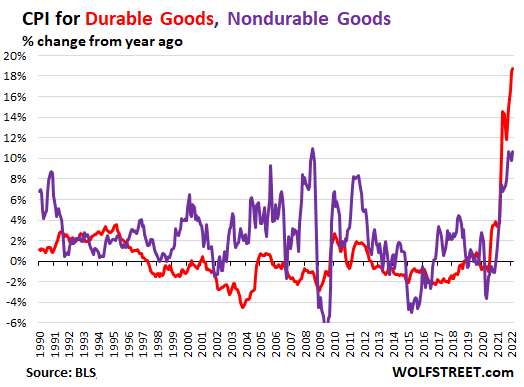

The Consumer Price Index for durable goods spiked by 18.7% in February (red line in the chart below), by far the highest in the data going back to the 1950s. A big part was the ridiculous spike in prices for used and new vehicles.

The CPI for nondurable goods spiked by 10.7%, the highest since July 2008 (purple line). The current spike in gasoline prices since late February has not yet made it into the index.

So the year-over-year jump in retail sales of 17.6% needs to be seen in light of price increases for durable goods of 18.7% and nondurable goods of 10.7%. Which means: Consumers are making heroic efforts to spend what they have and earn and can borrow to keep up with inflation, and maybe spend a little extra on top of inflation:

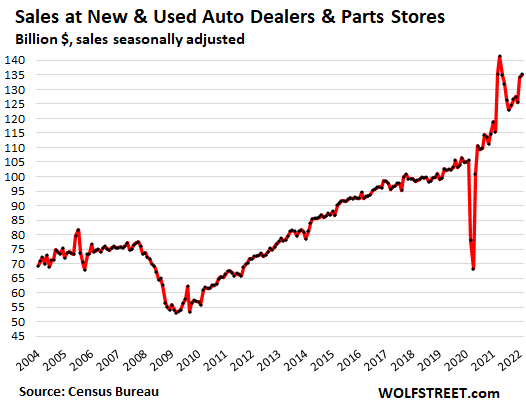

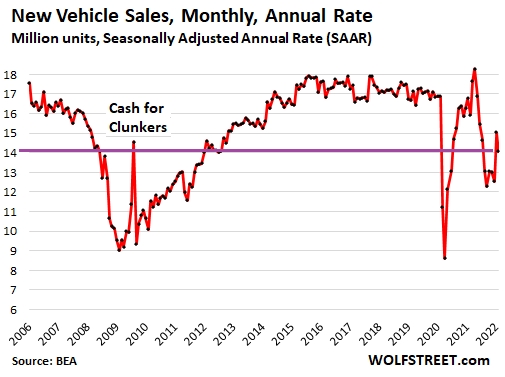

Sales at New and Used Vehicle and Parts Dealers: Spiking prices, declining unit sales.

In dollar terms, sales at new and used vehicle and parts dealers, the largest category of retailers, ticked up 0.8% seasonally adjusted in February from January, to $135 billion. Not seasonally adjusted, sales rose by 2.6% month over month to $121 billion. Compared to a year ago, sales jumped by 17.7%, a huge jump.

But used vehicle prices exploded by 41% year-over-year, according to the CPI; and new vehicle prices spiked by 12.4%. So the dollar-sales gains were all based on higher prices and a shift to higher-end and more-loaded models that the manufacturers have been prioritizing.

But the number of vehicles delivered to end users dropped. The number of used vehicles sold to retail customers in February dropped by 7% year-over-year, according to Cox Automotive. And the number of new vehicles sold dropped by 12% year-over-year, to a seasonally adjusted annual rate of 14.1 million new vehicles:

The other retail categories in order of sales volume.

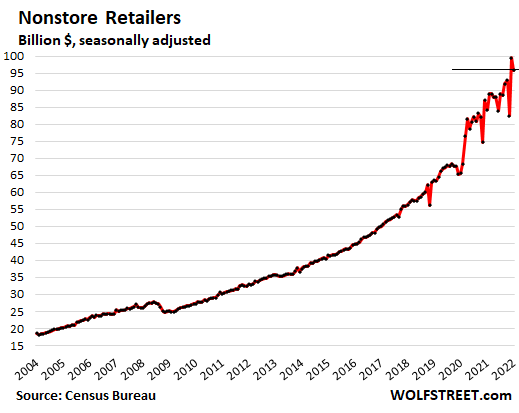

Sales at ecommerce and other “nonstore retailers,” the second-largest category, jumped 13.8% year-over-year in February, to $96 billion, seasonally adjusted, down 3.7% from the record in January:

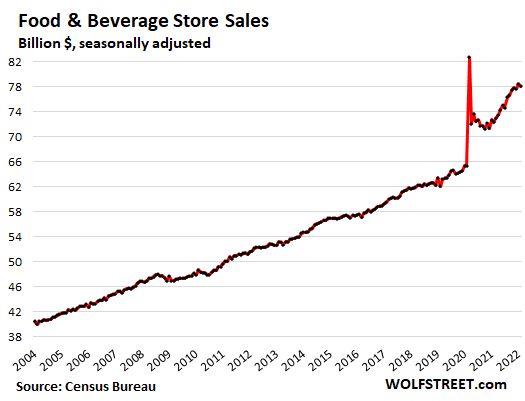

Food and Beverage Stores: sales dipped 0.5% for the month, seasonally adjusted, to $78 billion. Year-over-year, sales jumped 7.9%, while the CPI for food-at-home spiked by 8.6%:

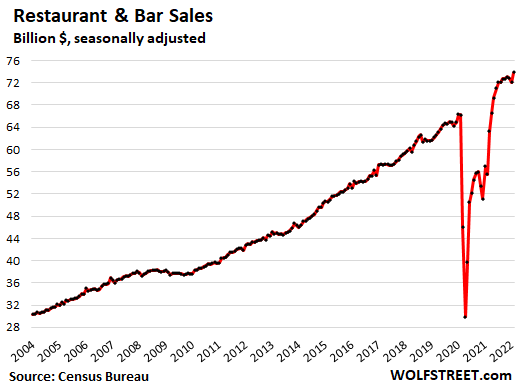

Food services and drinking places: Sales rose 2.5% for the month seasonally adjusted, to a record $74 billion. Year-over-year, sales were up 33%:

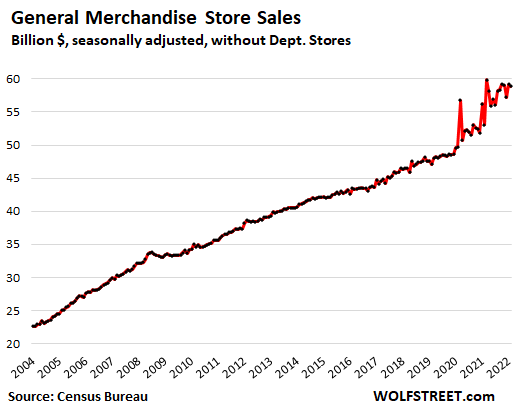

General merchandise stores: Sales dipped 0.6% for the month to $58 billion, seasonally adjusted, and were up 10.9% year-over-year. Walmart and Costco are in this category, but not department stores.

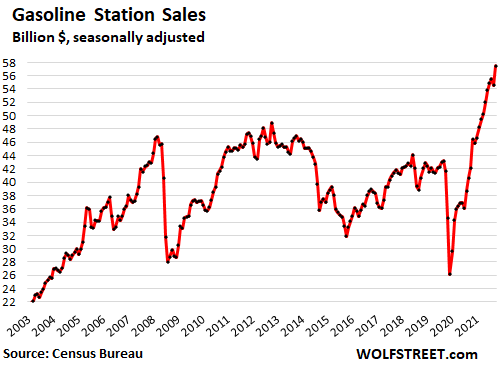

Gas stations: Sales spiked by 5.3% for the month, to a record $57 billion, seasonally adjusted, driven by the 6.6% spike in gasoline prices. Year-over-year, sales spiked by 36%, driven by the 38% spike in gasoline prices. In other words, the sales growth at gas stations is all due to higher prices:

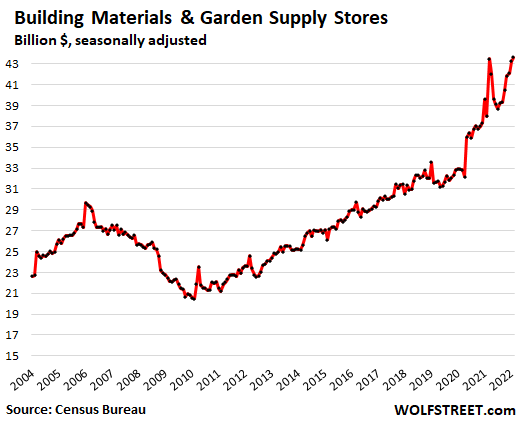

Building materials, garden supply and equipment stores: Sales ticked up 0.9% for the month, to a record $43 billion seasonally adjusted, up 14.8% from a year ago.

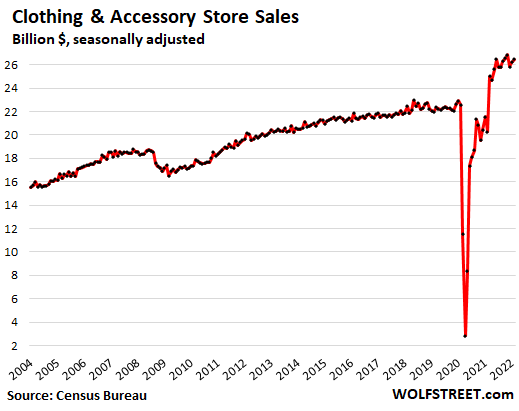

Clothing and accessory stores: Sales rose 1.1% for the month, to $26 billion, seasonally adjusted, and were up 31% year-over-year:

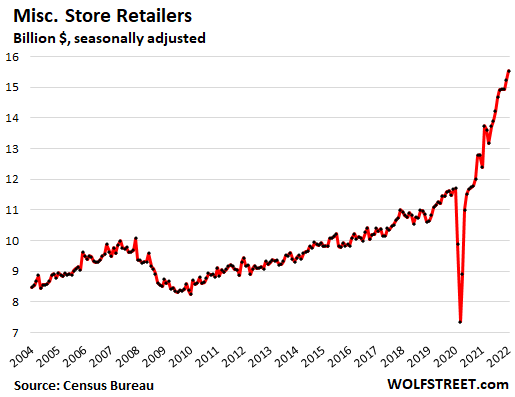

Miscellaneous store retailers, which include cannabis stores: Sales jumped 1.9% for the month to a record $15.5 billion (seasonally adjusted), up 25% from a year ago. This category tracks specialty stores, such as for cannabis products, beer brewing supplies, telescopes, art supplies, etc.

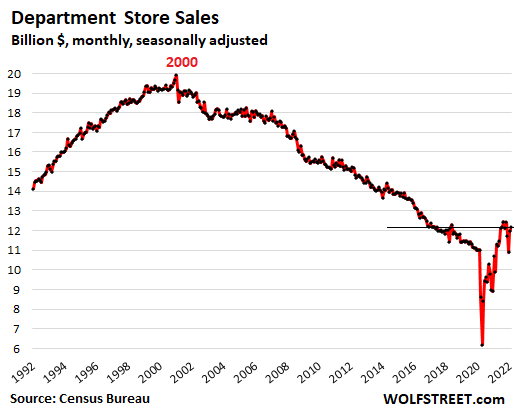

Department stores: sales rose 1.6% for the month, to $12 billion (seasonally adjusted) and were up 23% year-over-year. Compared to the peak in the year 2000, sales were down 39%, as Americans have abandoned that type of retailer. Innumerable department stores were closed over the past 10 years, and many regional and national chains were liquidated, with only a small number of survivors left:

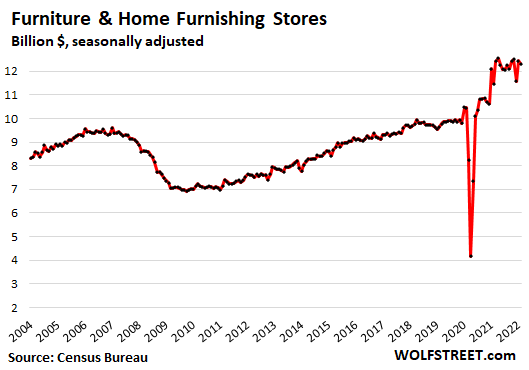

Furniture and home furnishing stores: Sales fell 1.0% for the month, to $12 billion (seasonally adjusted), but were up 7.4% year-over-year:

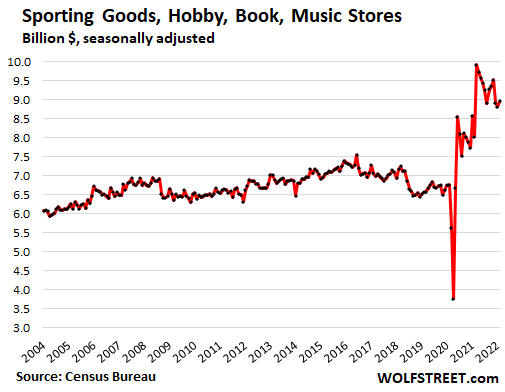

Sporting goods, hobby, book and music stores: Sales rose 1.7% for the month, to $9.0 billion (seasonally adjusted), and were up 11.7% year-over-year:

Electronics and appliance stores: Sales dipped 0.6% for the month, to $7.3 billion, seasonally adjusted, but were up 2.6% from a year ago. Sales of consumer electronics and appliances are huge, but are spread over many types of stores, such as Costco, Walmart, and Home Depot, and a lot of the sales have wandered off to ecommerce. This category here covers only the sales at specialty brick-and-mortar stores, such as Best Buy.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I get so depressed when I see these charts…

Well, the Fed just gave green light to run inflation “hotter for longer”. As they promised. And the 2% inflation was in fact “transitory”. Again, as promised.

Yes, the 0.25% lip service is just what was needed to make inflation go higher.

It seems we will continue racing donkeys in horse races and bail them out when they keep losing.

God, please help America face whats to come.

“God, please help America face whats to come.”

It is time to start thinking about what comes after the “USA” because nations that behave like this don’t survive.

The “USA” is simply a form of political organization, not an immutable geographic fact.

In theory, the USA has the Constitutional, political, legal, and organizational tools to reform itself…but the empirical reality of the last 50+ years prove that DC has absolutely no will to do so and will in fact use every tactic (including the dirtiest) to defeat reform.

And the factions among the states, ensure that DC leadersh*t stays in power.

So the higher probability is that rampant inflation (the “fix” for DC’s cancerous debt/corruption), the accompanying devaluation of accumulated personal savings, and the inevitable partial default on “entitlements” will break the “USA” into two pieces along ideological lines.

California will be head of one new nation and sooner or later be forced into junior partnership with an overseas power (China most likely) in order to reconcile its economic policy failures.

That will be an issue for the “other America” successor Nation, which has never really had to concern itself with a powerful neighboring military power occupying the same continent.

Countries that behave like the USA for the last 50+ years don’t survive.

Are we seeing a pattern here?

People are complaining we are being lied to but reality, we were not. We just interpret things incorrect when we hear them.

Transitory: correct; transitory to hyperinflation.

pelosi’s ‘more government spending will down the government debt.’: correct if you expect hyperinflation that will make the government debt worthless (and also your savings and your USD’s)

love everyone – INFLATION INFLATION INFLATION

but in REALITY it is simply – GOVERNMENT THEFT by DEVALUATION of fiat $dollar

only 30% of purchasing power in 2021

can’t wait to see final numbers of 2022

I read these charts as proof the economy is roaring. No sign of recession. The fact that so many readers of sites like this are pessimistic must be some sort of selection bias. Meaning more readers are having trouble vs the “real” world average.

The markets will have to adjust to higher interest rates. Higher and higher as long as inflation is out of control. I’ll wait to buy dips until there is light at the end of the tunnel. It may mean paying more, but I’d rather do that than catch a falling knife.

You sound like a reckless gambler who has totally lost touch with reality.

So par for the course with today’s investors.

How do you read charts that say consumer spending is at record levels and be pessimistic? Do you read them upside down, or do you not understand most of the economy is based in this?

20-30yr yield curve inversion. 7-10yr inversion. Yesterday, 5-10yr inversion. 3-10yr is within days of inverting and the 2-10yr doesn’t look all that far away at this point.. the reality is that the readers on this site are seeing not just the flat nature of the yield curve, but it’s trend toward inverting across the board.

For fun, look at the US10yr Treasury note chart for the last 40 years and tell me if you can spot the trend channel. It’s practically sloping downward at a perfect 45 degree angle. Every time the 10yr spikes above the trend channel there’s some sort of major market correction or recession. Now, look at where rates are in that trend channel and it’s pretty plain to see what’s about to happen in the next year or so.

That light at the end of your tunnel is the roaring train called Inflation, and it’s towing War, Death, and Pestilence, along with a few other things…

Good luck with all that buy the dip business…

There’s a huge generation gap on how inflation is affecting households. It might be a big deal to boomers and older.

For the young though, with remote work, moving to LCOL areas has become possible which fixes housing inflation along with lowering taxes permanently, maxing ACA credit for healthcare… It’s the gift that keeps on giving and with internet services like Starlink real mobility is now a reality.

I’m still enjoying severe deflation thanks to remote work.

none of these charts mean a thing…

unless they mean something to the ultimate authority…the unelected, unaccountable FEDERAL RESERVE

SO…nothing to see here…..move along.

So Powell raises by a whole quarter point. Ya, that’s channeling Volker alright. Three more quarter points and we’ll be up to one whole basis point.

Inflation, watch out, the FED’s out to get ya.

10% PPI is how many quarter points? 40?

and Powell does ONE?

The Fed has been hijacked…they are not the Fed anymore….something very very different….and answering to whom?

I think he’s trying to not get elected again ,walk into sunset with80 million nice retirement

If people like Dr. Lacy Hunt are correct the high prices create demand destruction which leads to deflation. Even the hyper inflation during the Weimar Republic only lasted about a year. High rates of inflation isn’t the same as slowly raising the temperature on a pot containing frogs

Yet Powell is still talking massive sh*t. He is “acutely aware” of the need to return to price stability, and he “sees inflation coming down later this year,” yet it rages on. A quarter point rate hike and he’s fixed it – A MIRACLE! This guy stands up and lies his asz off every time he says anything, and somehow never loses his job. He is getting re-confirmed today.

Yes, the working-class that hoped that finally Government and Fed would save them from inflation are so disappointed today. God bless them.

In the bag, a 1/4 point hike. A brave start, and only 39 more needed. By August. Getchur’ popcorn.

If you stand back and consider everything that is happening and the FED’s response to it, it is painfully obvious what their goal is. This is 100% intentional. When the stock market started cratering in 2020, they were in front of the cameras in a day, hammering rates to zero and talking about trillions upon trillions of QE and other programs to levitate the stock markets so that the rich didn’t have to suffer the horrors of paper losses on their assets.

But now when we have raging inflation which is destroying the standard of living for 90%+ of all Americans, they are sitting back, carefully considering for months whether they should do a measly quarter or half point rate hike. C’mon, folks, they are intentionally “letting inflation run hot” because they want to reprice everything.

They want these prices to STICK. They are desperately attempting to maintain all asset price bubbles into perpetuity, meaning the bubble prices become the new prices at the expense of the future of the young people. They are spending your futures away to pad their own net worths. These guys should be fired and arrested. They were personally day-trading their own policies, front-running the markets, and were busted for it.

The markets are a part of the war effort IMO. They prop them up to give us false confidence in the country and it also sucks in foreign money. It’s a giant black hole that does indeed cannabalize future generations.

Death of our money mirrors the death of the culture and the country.

“death of the culture”

The US does not actually have a ‘culture’.

Instead, it has ‘marketing’.

No culture? It’s worldwide, you absurd snob.

It’s pre-recession inflation.

It won’t last, they’ll do a few 0.25pc rises and then have ammo for relaxing policy in Q3/4 when it’s statistically a recession.

Then they’ll blame it all on covid/putin/bogeyman xyz, and again, people will accept it rather than point their angst at the real perpetrators.

Rinse repeat, and each time people think it’s a new game.

Why change the game when the current one works so well?

yep

intentional

the quick to save markets but slow to protect the citizen from inflation is the tip off

The Fed has been hijacked

Those WHO KNOW the Fed wont do their duty make all the $$$$

People have commented at times “the FED are idiots.” I don’t believe this at all, because they’re not. These people are educated and know exactly what they’re doing. Their plan is to “let inflation run hot” for as long as they possibly can. They don’t believe pitchforks will ever show up at their doorstep.

They know that the longer they allow inflation to run hot, the higher the floor in asset prices. You can’t take it back. So they’ve made a policy decision to actively destroy the currency and the standard of living to levitate asset prices. That’s the plan, and they are sticking to it.

Jerome Powell and Co. to the working class and the poor:

“Can’t afford a house? Can’t afford rent? Can’t afford a car? Can’t afford health insurance? Can’t afford good food? Too f***ing bad. You lost. Suck it.”

Powell was asked a question about the differential between the current interest rates of 1/4% and the inflation of 10% . He could not answer the question and there was no follow up. He just started rambling about the tools that the Fed had and would use them in the future if needed. What a bozo clown.

Right. Because he’s not fighting inflation, he’s encouraging it. They know EXACTLY what they’re doing. It’s intentional. The young people need to understand the FED, and share with each other that they are the enemy stealing their future.

Powell seems to care more of government cavalier spending and his debt floating venture capital buddies than the working/earning/saving people of this nation that turn the lights on , drive the trucks and fill the shelves each day.

From the incubated Northeast elite, prep school, Ivy League, Venture Capital, then fast tracked to the Treasury and ultimately the Fed. Isolated. Removed from real life in America. No hourly wage in his resume, no elbow rubbing with the great unwashed….ever touch a shovel? Break a sweat? Save for a purchase or for unforeseen events?

Punishing saving….as he promotes inflation. Theft..no other word for it.

Please tell me what happens after they destroy the currency? What happens to the value of those assets they have been pumping up?

Can’t afford half of what you did!

Recession, depression, deflation.

How would the economy work?

What you’re suggesting is like giving people 10% pay cuts every year.

It’d kill the economy.

The Fed aren’t idiots.

They’ll crash it, but causing deflation is just as risky as too much inflation.

People need to be able to buy “stuff” for the wheels to stay on the bus.

We don’t have raging inflation…yet.

Then you haven’t been paying attention to Wolf’s charts.

The inflation which matters most is each individual’s personal rate which varies, a lot.

If you have semi-fixed housing costs with a moderate sized mortgage and good medical insurance with a (reasonably) stable well-paying job, you’re probably doing ok to “great”.

Otherwise, you’re potentially staring at double digit rent increases and housing appreciation and other costs.

The only reason most American households are solvent or “middle class” now is because of government transfer payments and access to (relatively) cheap credit.

Even before 2020, real median income and net worth had flatlined for 20 years. That’s an entire generation and probably the worst performance in American history.

Powell actually said he’s protecting the stock market…

It went by real quick…

He also said the FOMC did not operate on what is happening today, but is making policy based upon what they think will happen in 12 -24 months…

Understand that…

Financial policy is issued today for a fictitious economy in the future and not the economy that exists now…that’s why they are always wrong and behind…

Oh, and blame it on Russia… how convenient…

Since all the data with which they allegedly make decisions is from prior to the invasion…

Maybe a coincidence when the harder questions were interrupted by a zoom failure…

Pitiful, just friggin’ pitiful….I turned it off when I couldn’t stand the hems and haws and the “ you know” any longer…

He kept looking down and reading from a script. He had canned answers for every question. When he couldn’t answer a question he just didn’t answer it. I wanted to smash the TV set watching this crap.

Theatre.

No Wolfstreet.com questions

No Zero Hedge questions

No Mises.org questions…

just lap dogs….dishonest really.

He always has “canned answers.” That’s how it does it every time. Some things he adds freely. Other things he reads.

are you referring to this?

“In making decisions about interest rates and the balance sheet, we will be mindful of the broader context in markets and in the economy, and we will use our tools to support financial and macroeconomic stability. “

There might be a reason the FED want asset prices to stick. Disputed, because it is about the perceptions about the monetary and banking system.

The keyword is mortgages and other loans in exchange for taking title of the debtor’s property where the title to the property is the counterpart to the money issued by the bank to pay out the loan.

If the sum of the value of these assets and the banks other assets go below zero the bank is technically insolvent. Now the FED do not want insolvent banks, that quickly leads to bankruptcies.

If you’ve listened to the Powell press conference and think this guy is going to reduce inflation then I have a bridge to sell you.

He looks like a man who is stood in front of millions of people who know he is lying through his teeth.

georgist,

Powell hiked by a quarter point, and lots of people here said that the Fed would never hike. So here we go. Now the Fed is looking at 7 more hikes this year, and more next year, and maybe bigger ones, and lots of people here are now on the one-and-done track. And then they’ll be on the two-and-done track, and then on the five-and-done track, and then on the 11-and-done track… You gotta go with the flow, no?

Wolf –

Why does a quarter point even matter? You damn well know it’s not doing anything. It’s a token to try to pretend like they are taking this seriously. They’re not. You know it. I know it. Everybody knows it. You said it yourself – if they were serious they would have done something long ago, and if they were serious today they would have raised at least 100 basis points.

They are doing it precisely because they know it doesn’t matter. Even if they hike 5% at a time, they are doing it because inflation is much higher and real yields are negative.

Wolf, did you forget that last time the Fed interest rate was above real inflation rate was 15 years ago in 2007 and it caused GFC. Since then fed has been talking about raising it but makes U turn on first sign of market tantrum. Enough will go wrong before year end that Fed will use as excuse to backtrack again and marketswill celebrate again and inflation will eat all our lunch.

Raj,

” last time the Fed interest rate was above real inflation rate was 15 years ago in 2007″

Almost but not quite. Nov 2018 through Nov 2019 was the last time:

Wolf, Thats why I used the term “real” inflation rate. One that includes housing and not shelter, one that does not account for hedonci quality adjustments and one that is weighted on where people actually spend their money. You know this better than me as I learned these from Wolfstreet.com.

I’ll agree we have to wait and see what the next two meetings bring before outright condemning them, however they deserve huge criticism for the mess they have made. They’ve put the west back decades.

Marketing/media have programmed Americans to consume beyond their means to look fashionable. It’s an addiction.

Producers have concocted every more complex products, either physical/ intangible/financial, that hoover up more consumption while providing questionable value.

Add in cheap borrowing, free money and government bailouts – all without negative consequences – and you have a self re-enforcing cycle.

This could go on for a very long time due to USD dominance but world events may trigger more rapid change. My intuition tells me that Americans will hoard more stuff, not less, as conditions deteriorate.

As for today’s announcement of a 0.25 percent rate increase, a slow/prolonged increase in rates will only result in more panic borrowing to buy more stuff before rates go higher.

I cannot tell a lie,

but if keeping up is absolutely necessary,

Ladas are now a bargain buy…

🤫

I’m Stanley Johnson. I’ve got a great family… I’ve got a four bedroom house and a great community… Like my car? It’s new. I even belong to the local golf club… How do I do it? I’m in debt up to my eyeballs! I can barely pay my finance charges… Somebody help me?

And Jerome Powell puts on his cape and flies to the rescue of Stanley Johnson and his bloated debt lifestyle! He leaps over a speed bump in a single quarter point, so Stanley can continue to do his part to stretch the y-axis on Wolf’s charts.

No, only super heroes wear capes. I see Powell as a villain, specifically the Joker in that Batman film where he and his goons throw money into a greedy crowd. Or in the other Batman film, where he sets a warehouse full of cash on fire.

Did Jerome Powell wear a purple suit today at his presser? Was there a tint of green in his hair? Did he laugh maniacally?

Always a borrower and never a lender be

is that the old saying?

“High inflation takes a toll on everyone but really, especially on people who use most of their income to buy essentials, like food, housing and transportation.” — Jerome Powell, today

Yet the NASDAQ closed up 3.77%. This shows the obvious falsity and wilfulness of the Powell quote. The Fed punchbowl, asset prices, and inflation are a party still in full raging mode.

No actions or remarks were made, designed to actually fix things. Powell’s bully pulpit opportunity was lost. No leadership here, just misdirection and fake sympathy.

These are merely carefully crafted soundbites to make this evil man appear human, like he has a conscience when he is really a demented, filthy, perverted soul.

Those who KNOW…the Fed will not stand to their post….will make all the money.

Those who expect responsible action and a mandate following Fed, will be passed up like stopped car on the highway.

If only there were some rules…..oh, wait, there are!

Just no cops.

In a system that boasts of “checks and balances”, who checks the Fed?

stop all the negative posts ! .25 kills inflation in its tracks ! ” Mission Accomplished !” lets have a wrap party with some MMT to the tune of a few trillion $$$ newly printed /key stoked dollars ! all sarcasm aside this is – was – and continues to be one hell of a party !

Powell plays the guitar, they say. Dresses impeccably.

Jerome Powell stated that the Fed Funds Rate would be below 2% to end the year, with “official” inflation running 8%, and nobody questioned him. Nobody pointed out that to stop inflation you need the Fed Funds Rate to be ABOVE it. Jerome Powell is allowed to steal from the young, the working class and the poor with impunity. He is a protected class, above reproach.

amen brother

greatest theft ever perpetrated in world history

taxation without representation

The world will leave the dollar

Maybe thats why Russia created this mess, so they can change the USS worldwide reserve status.

They only needs China´s support, maybe with the Taiwan answer

Yamo,

Russia isn’t going to do anything to the US dollar. Russia’s economy is smaller than the economy of Texas and New York, and is half the size of the economy of California. And that was before Russia’s economy crashed. The ruble isn’t worth the paper it’s printed on. Russia is going to default on its debts shortly, and that will strangle its finances for years to come.

China is the big kid on the block, not Russia.

Wolf,

But maybe oil is a more “real” international currency than fiats, because 1) oil has direct utility (unlike “paper”/”legal claims upon theoretical tax revenue”) and 2) oil’s value cannot be diluted at the will of corrupt governments (“QE”).

Oil’s value derives from its ability to make machinery move.

Fiat’s value derives from the reliability/capability of political promises (heh).

International governments know this in their bones – it is the foundation of petrodollar military alliances and the reason why DC cares infinitely more about Middle East “unrest” than say, Congo unrest.

And Russia is one of the three giant oil producers/reserves on the planet (comparable to Saudi, and somewhat greater than US until recently).

So Russia’s influence on the international economy may be somewhat greater than you make out.

When the Russians pump oil, the foreign buyers know what they are getting.

Can the same be said when the US pumps dollars?

Misconception here. Oil is a commodity that gets consumed. It’s subject to supply and demand. But in the end, it will be consumed and disappears. It’s not a currency. And it’s not an asset. It’s a consumable. The asset is the oil field.

If people keep spending like the charts here say then why would the FED be motivated to stop doing what they are doing? People may be going into debt, reverse mortgaging their homes, opening new credit cards and spending the grand kids inheritance but the FED don’t care.

Honey badger don’t give a..

DC

They did ask him that question, but he dodged it and started talking about “tools” that they had and could use in the future.

He did get a few questions about that… Can’t remember who asked. And he was asked twice about being “behind the curve.” There were a few similar questions.

So… what ever happened to the Taylor rule? Lol

check out the Feds own Rules of Monetary Policy

at the Cleveland Fed website

Taylor Rule is one of 7 calculations

Median Fed Funds rate among the 7 is 3.25%

They ignore their own rules and they ignore their mandates and nobody says a word

China’s in a new lockdown. Is Covid retreating or just mutating for another surge? He has to keep policy loose, no choice.

They chose to tighten. Rate hikes every meeting this year, more next year, details on QT in the minutes (3 weeks). QT plans to be announced at the next meeting in May. QT will be “faster and sooner” than last time. They have lots of choices.

Then why are they stalling, Wolf? What’s taking so long? They show up in a minute to throw trillions on the market, but wait months to do something about inflation? C’mon, this is a tired old act they’ve got going. The people who just had their rent jacked 35% don’t have time for the FED to act, do they? But heaven forbid rich people have to suffer even a day of paper losses on their stocks.

LOL. Depth Charge. Why are they stalling. Good question. QT has been going on for 13 years.

It is always hard to put a fiscally challenged person on a budget. I think the FED is no exception?

I just head an interesting comment. Europe will probably just send checks to everyone to combat commodity price increase but use the “War” as an excuse.

Wall St. loves Powell’s dud today. They know he’s never going to take away the punch bowl.

If he takes away the punch bowl that will do

way more than any interest rate increase.

Wm. McChesney Martin coined that phrase about taking away the punch bowl. Check the Feds rate hike program in the 50s after inflation spiked, and a recession after the Korean war. They were also trying to work off a pile of accumulated debt from W2. They kept raising rates however, and it didn’t become inflationary for two decades. We’re still in the early innings here, and by analogy maybe the punch bowl is still being filled.

As long as Americans keep spending big money, nothing matters. It does not matter if they are in debt to their eye balls.

I don’t see spending slowing down by any measure at all.

Our road might be paved with good intentions, but it really is paved with raving showy excess, phony status displays, press release emoting, until the whole train careens off the tracks.

“I don’t see spending slowing down by any measure at all.”

There’s a ceiling. Some, like me, have slowed down spending. Different people have different tipping points, but eventually most people will pull back.

My opinion, anyhow.

I see they have been building Dollar General and Family Dollar stores. Is there a chart for online stores?

A rate hike will not fix sanctions, export bans and boycott related supply chain disruptions. Ukrainians need water, bread, insulin, heated shelter, etc.

Mortgage rates are rising. A CNA was getting $13 an hour last year. She gets $14 an hour this year. The rent was raised again.

Gonna need more tents.

Don’t know where you are at but here CNAs went from 16-17 to 20/hr

“I see they have been building Dollar General and Family Dollar stores.”

Two new ones near me opened this past year and only six miles apart.

So Americans are just ignoring inflation? That is not what the political polling says. Maybe they are taking note of it but unable to change their spending patterns (for now). Maybe the wage increases we have seen are insulating them (for now).

Something has got to give and I don’t think 0.25% Fed rate increases is going to do the trick.

People I know are slowly changing their spending.

I think the rise in interest rates will have a huge effect on real estate sales this summer.

SpencerG,

“So Americans are just ignoring inflation?”

No. They’re NOT ignoring it. They’re hating it. And they’re trying to OUTSPEND it, as you can see in the charts.

OH… I missed that part of your argument. Americans are trying to frontrun the inflation that is to come. I guess that I can buy that.

Price inflation is easily handled simply by increasing everybody’s debt peonage, er, credit limit.

Problem solved. Next!

It is starting to mirror the 1970’s. I am not sure there is an easy fix. If they prop up interest rates then companies cut employment, people are out of jobs and can’t afford anything. If they do not stop inflation, people cannot afford food, gas, and shelter. The only answer is to find a way to deflate inflation without killing income. One solution is to deflate the everything bubble. Can they do that and lose part of their portfolio for the good of the Nation? Are they selfless? History states no. However, Marie Antoinette would caution Powell it is better to lose a little padding from your portfolio then from your suite should Main Street revolt.

This is way, way worse than the 1970s. This is inflation on a level never before seen in the US. 30+% rises in rent? 40+% in used vehicles? We are in totally uncharted waters, with an economic terrorist Jerome Powell calling the shots.

DC

Agreed. This is the 1970’s on steroids. The Inflation figures are deliberately falsified to understate the real inflation rate. I believe it is close to Stockman’s figure of 13.8% and going higher.

It’s worse still. Back then unions managed to negotiate wage increases near the inflation rate. Today the majority of employees are not covered by a union and will not receive wage increases to compensate for the increasing cost of living. Outcome will be a deep economic slowdown.

The stock market is not going to deflate alone.

A deflating stock market will be caused by changing sentiment, not the piddling changes in the FFR contemplated in the FRB announcement today.

When sentiment changes sufficiently (whatever that is) not only will the stock market deflate, the credit markets and housing go with it too, though not necessarily simultaneously.

There is no “soft landing” in store for the economy from the greatest asset, credit and debt mania in the history of civilization.

If there was, it concurrently means there is something for nothing.

I watched Powell’s full press conference. Yes, central bankers kicked and dragged their feet up to this point. But judging from today’s remarks, at least he finally seems to understand the magnitude of the problem. The FOMC consensus is now

– 1.75% of tightening before year end (that’s an average of 0.25% for each remaining meeting) It was 0.75% in the December SEP & analysts were predicting 1.25-1.5%.

– a 0.5% increase at one meeting isn’t ruled out

– balance sheet reduction (QT) to begin as early as the next meeting

– above-neutral federal funds rate by 2023/24

It could have been worse. In a different time, a geopolitical disruption like Russia/Ukraine would have been used as a reason to cancel/postpone rate increases or even expand QE. Instead, Powell said we’re at full employment, that the economy is very strong and could withstand the rate increases as well as supply disruptions from covid & Russia/Ukraine.

Don’t get me wrong: the Federal Reserve gets a solid failing grade up to this point, but there is reason to be cautiously optimistic.

“ – balance sheet reduction (QT) to begin as early as the next meeting”

I thought he said at “ future meetings”…

He will never commit to anything he can’t weasel out of….

Everything you heard today was couched in – possible, perhaps, if, maybe, we’ll have to see…

You will never pin him down…never…

“above-neutral federal funds rate by 2023/24”

This is unlikely. It assumes inflation returns to their supposed 2% benchmark.

If market interest rates (not the FFR) are neutral by then, it will happen because of “risk off” market tightening which completely disregards any attempt to prevent it.

The last time rates were somewhat neutral was in 2007.

“the economy is very strong and could withstand the rate increases”

The problem comes when their cumulative actions eventually affect the economy such that it’s no longer strong. At that point, I think the Fed will stop/bail on rate increases and QT. That’s what happened last time. What they should do is ignore that and keep going to clear the excess liquidity from prior actions. This is the reason nobody trusts them to fix anything, they are scared little princesses at the first sign of difficulty.

Let’s all be willing to take a nominal hit to our ego-pumping “wealth effect” jacked- up asset prices, in order to get general prices reasonably lower. I think Powell is playing to a straw man that is some hypothetical disappointed over-sensitive asset holder. Let’s cheer for a bit of deflation. The target should now be for zero inflation for awhile, to reverse, wring out and correct prices, just as Powell and company relaxed the 2 percent inflation target on the upside.

The reverse to wring out prices is just what we are seeing now except in the opposite direction of what you mean.

Oil companies, retail, landlords etc. making up for two years of losses and now enjoying the chance to reverse the losses.

Make sense, but then, I saw in the runup to the COVID crash, a lot of companies not investing in capital development or even building reserves, but sucking up cheap credit and doing stock buybacks with it.

“Powell insisted the Fed will do whatever it takes to squelch inflation, but he expects the process to take a few years.”

LIAR. LIAR. They could stop inflation dead in its tracks, TODAY. All they had to do was raise the Fed Funds Rate to 10% – 1,000 basis points. Immediately. Then announce that they would be drawing down their balance sheet to pre-pandemic levels within a year’s time. Inflation DONE.

LOL, running aground is the last thing we need. 25 basis points is a slap in the face of ‘already occurring inflation and a tug on our blindfold’. The truth is, the TPTB want to bleed us slowly, not kill us.

Wolf, as u know, I’m a big fan. After todays anemic announcement that “we have to tackle inflation”. Do you think JPow is going to try and quietly inflate the debt away? If so, what, if any, assets would do well?

Also would love your opinion on Xi “clamping down and regulating” Cayman island P.O. Box equities for the past 2 years and then suddenly announcing he was just kidding. Seems like he filled his bags to me, do u think US regulators will delist these companies?

Thank you

You CANNOT inflate debt away with low interest rates because low interest rates just encourage more debt. He knows that too.

Sorry to push back, but you definitely can with the fed todays metric for inflation.

They seem to pick numbers out of thin air and negate numbers they don’t like.

What I’m saying is that the burden of the debt won’t shrink and might even increase as consumers, businesses, and governments pile on more debt faster than the burden would be reduced from inflation.

And note, it’s not CPI (consumer price inflation) that matters when it comes to the burden of debt, but income.

Only borrowers with rising incomes have a lower debt burden.

Many borrowers face higher costs (CPI inflation) and that will make meeting their debt payments even more difficult. Consumer price inflation makes debt burdens worse; what you need is income inflation to reduce the debt burden.

I love the question of which assets would do well. Unfortunately this is a global mystery. Musk said “physical things”. Real estate has already hit stratospheric levels, so what else? If it’s stocks, these things tend to tank hard in a recession, so I’m a bit gun shy. Names that are on my list are VZ, MMM, PG, WMT, NEM, WU, IBM, INTC because they have decent dividend history, but depends at which price ppints ur comfortable taking on the risks. My XOM I’m just holding like others here are doing. Not financial advice, and interested what others have to say.

Persistent inflation will eventually make practically everyone poorer.

Asset wise, the difference now is that practically everything is either overpriced or insanely overpriced.

Stocks were cheap in the 70’s. Bonds were better values because credit quality was much better and interest rates higher. Real estate was far more reasonably priced.

Gold was a lot cheaper too. Silver is cheaper now adjusted for price changes but has effectively lost its monetary status.

Other commodities have been catching up to gold but are still quite relatively cheap.

Historically, gold has been very overpriced versus the commodities people need to buy which means that at some point, even when it goes up, it will almost certainly go up less which means those who own it will still lose purchasing power.

There is no escape for most people from this fiasco. They are either going to get financially bled to death slowly or get crushed by the end of the asset mania.

“gold has been very overpriced versus the commodities people need to buy which means that at some point, even when it goes up, it will almost certainly go up less which means those who own it will still lose purchasing power.”

Agustus,

How many people do you know who are real, committed gold bugs? Gold bugs who can afford living expenses rarely sell their gold…it is a security issue. Many will die with the hoard, and their unworthy heirs and assigns will then sell, and usually at distressed prices.

Just an observation…but I could be wrong.

“Americans Make Huge Efforts to Keep up with Raging Prices ”

Sorry, but I’m no of those folks. I’m checking out of this mania. I’m on a buyers strike. Not buying anything unless it is an absolute necessity. Not traveling anywhere unless its an emergency. Any extra I have at the end of the month I’m storing in my credit union MM fund, yielding 37 basis points. The only two trips out of the Swamp Metro area in the last two years were to get vaccinated and to go to the Truckers rally in Western MD. I’ve got plenty of productive things to do with my time.

The central bankers in the USA and Canada see no inflation, because they are the prime reason for inflation.

At least 99% of Canadian and American politicians own a home, have stocks and will retire in pension funds that rely on inflation and money printer go brrr.

My burning question I always have is where is all the money that the consumers are torching coming from?

Stimmies are done afaik and most people just let them pass through their hands and on to worthless consumer goods. Crypto has crashed. Most don’t have enough in stocks to have dividends paying and unless they are cashing out, stocks are just paper gains until sold. Credit cards still rake you over the coals if you’re dumb enough to not pay them off monthly. Is it cash out refi’s or continual increases in credit lines?

I don’t understand where the working class of America is getting all of this money to not only match inflation but stay ahead of it by spending more?

What percentage of sales are made by the top 10% earners? The top 20%? It’s a very large number, if I recall. That would partly explain this mess. The charts don’t illustrate this.

Many people are using their homes as ATM machines like they did in the Greenspan era in early 2003/2004. That’s where they are getting the money for massive consumer spending.

Yep. This could last awhile. I read an article from an analyst last year that if we had another Home Equity binge, it could tap into several trillions of dollars.

So far, people have not down so like during HB1. But time will tell or some will need to because they like to live large.

In just 1 year, CoreLogic analysis shows U.S. homeowners with mortgages (roughly 63% of all properties*) have seen their equity increase by a total of over $3.2 trillion since the fourth quarter of 2020, an increase of 29.3% year over year. That is $55k per home.

That can buy a lot of Starbucks coffees and Chipotle burritos

Homeowners in California, Washington state and Idaho saw among the biggest average equity increases in the second quarter: $116,000 in California, $103,000 in Washington state and $97,000 in Idaho.

U.S. homeowners have $153K “tappable” home equity on average

Even a 5% drop in home prices would only equate to .1% of homes dropping into negative equity.

With 65% of families owning a home….there may be some cushion for the economy albeit they will need to clamp down on some spending? I say that because the hotel chains have been reporting record profits.

That is very interesting, thanks for sharing RU82.

The same analysis could have been made in 2006 or 2007.

We all know what happened next.

Augustus – In 2006 and 2007, people did tap the Home Equity big time. I had a neighbor take out two Home Equity loans. They did tap the equity and when things turned, people did not have much equity and many houses had negative equity value and that preceded jingle mail.

The point the person was making is people have not tapped their home equity this time and the amount of home equity as stated is very very large.

This is his post from a year ago. So the equity is more than 23 trillion now. He said that if the banks start offering programs to tap into this HE. But the banks may not offer programs to entice the consumer to tap into HE. Just a theory.

——————————————————————–

The present $23 TRILLION in Home Equity is so massive, timely, and opportunistic – 100%+ larger than in 2007 (11 Trillion) – it will soon be the central focus for homeowners; pure-play mortgage and housing companies; all directly and indirectly related companies and investors; and law makers and regulators, alike.

“Locked-in equity” is ‘the’ problem AND opportunity of the post-COVID era. With $23 Trillion in home equity vs $11 Trillion at peak bubble 2007 — while 10s of millions of homeowner families are unemployed or underemployed and living off savings, high interest credit, and Government aid – and with the backdrop of the average FICO for all mortgage originations in Q121 about 785 and less than 10% below 685, banks, credit unions, and non-bank lenders have done a horrific job getting credit to where it’s needed most, full stop.

In 2021, $275 Billion came from MEW. What did they buy? I don’t know. RVs, new cars, boats, home improvements, etc etc. They spent it all.

The unemployment number is low so people have paychecks. Living large baby!

Only spend on essentials. Stop playing into the game.

If the FED raises by 25 basis points in every meeting for the next two years, they would still not even be at HALF the current inflation rate. That means that by the end of next year inflation, at the current rate, would still be double the Fed Funds Rate. This is fighting inflation HOW? Anything short of getting ahead of inflation is doing nothing to curtail it, and Wall St. knows it.

Yep, Wall Street loves J Powell. He’s got their back. He doesn’t have yours. In fact, to put it bluntly “He doesn’t give a f$ck about you or your problems”

I finally concede this. The political class and their donors are just fine. I’m not in the club. Yeah, it could be worse. There are at least some crumbs for those falling behind, and this is a rich country. It troubles me to hear myself saying this. “It could be worse” is not a thriving country’s slogan.

I’m enjoying a macro hedge fund guy’s memoir centered around the 2020 crash, “Fed Up!” The guy gets the logic discussed here, and agonizes about the inequality, the crazy gains of the super-rich, and the vaporizing opportunity in the USA. But he isn’t giving up his perch, the posh London house and jet set life.

This is a rich country?

How rich is it without a fake economy, the one we have had since 2008? How rich is it without an asset mania, the one we have had this entire century)?

I don’t believe anyone really knows.

What I do know is that inflating stock values and housing prices aren’t real wealth and neither is increasing debt.

When people say the country is rich, they are looking at data such as the FRB report which states that household net worth keeps setting records and is increasing by leaps and bounds.

None of that makes a society wealthier. Only actual increases in productive capacity and human capital do.

If the Fed stays its course. inflation will double in 6 months. Better look at another plan Mr jay f’n Powell.

Fed lied through the teeth today. More inflation coming. Stock market is already rising again anticipating more printing as soon as the market falls.

Kunal,

You better sit up straight and pay attention: interest rates are going higher, a lot higher.

Today, the average 30-year fixed rate mortgage rate hit 4.5% today upon the news, the highest in years. And this has barely started.

Since you started this endless diatribe last September about the Fed lying, and QE will never end, and rates will never go up, yada-yada-yada, well, over those months, the 30-year rate mortgage has risen by 150 basis points.

The Fed is telling you what you’re going to get, namely much higher interest rates. And if you don’t believe it, and don’t adjust to it, and if you think the Fed lied today by telling you that rates will go much higher from here, it’s your own fault, not the Fed’s.

The Federal Reserve has been a complete failure, but what do you expect them to do at this point?

It’s not economically feasible to do a 5% FFR increase overnight. Even during the 1970s, the EFFR rarely rose by more than 2-3% over a year’s time. eg Mar 1977 4.69%, Mar 1978 6.79%, that’s the equivalent of a 0.25% increase at each meeting. Volcker only brought it up to 19% after inflation had been raging for over a decade. The current inflation problem is a year old, which arguably doesn’t justify such an extreme policy response just yet.

Today’s announcement was on the hawkish end of analyst predictions: rate increases at every remaining meeting for 2022, balance sheet reduction at next meeting, above-neutral rates in 2023/24, possibility of 0.5% increases after today, de-emphasizing Ukraine/covid as risks to the US economy.

I’ll give them the benefit of the doubt for the time being, until/unless they backtrack because the stock market sold off or some other reason unrelated to economic fundamentals.

Just got my valuation this week on my house. Valuation up 13% yr on yr. That means taxes up probably another 10%. No rest for the wicked and the righteous don’t need it. I’m tired.

Headline: “The Fog of War Is Providing a Smoke Screen for Trading Losses at a Dangerously Unreformed Wall Street”

…and will also be blamed for already in the pipeline inflation that have nothing to do with it.

Who cares?

Shit happens and people are harmed.

I don’t care that silly 21 first century cars are damaged.

The pussies of my generation will get what they deserve.

The year over year comparison is not appropriate because it obscures what actually happened in February 2022. The +0.3% increase of retails sales in February versus the 0.8% increase in the consumer price index, means for one month, retails sales, adjusted for inflation, declined.

One month is not a trend but it is useful current information. The year overt year comparison completely obscures what actually happened to retail sales in February 2022.

Look at the charts. That’s why I gave you the charts. The second chart, in billion dollars, shows the progression. February was a HUGE month because it was on top of the huge spike in January plus some!