Biggest COLA since 1982 already eaten up by inflation.

By Wolf Richter for WOLF STREET:

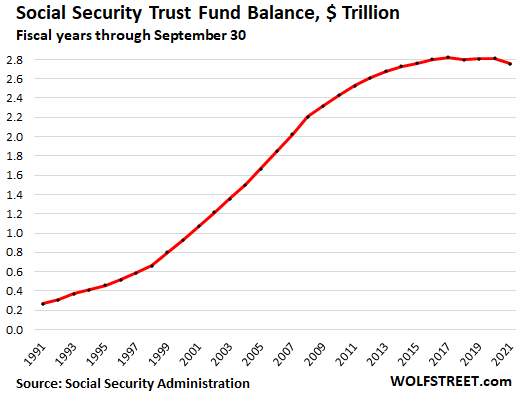

The Social Security Trust Fund – the Old-Age and Survivors Insurance (OASI) Trust Fund – closed the fiscal year 2021 at the end of September with a balance of $2.76 trillion, down by 2.0% from a year earlier ($2.81 trillion), according to figures released by the Social Security Administration. After large increases in the prior decade, this was the second annual decline of the Trust Fund since 1990; the first occurred in 2018 (-0.8%).

The Disability Insurance Trust Fund is by law a separate entity from the OASI Trust Fund, and is not part of this discussion here.

The OASI Trust Fund invests exclusively in Treasury securities. At the end of the fiscal year, it held $2.73 trillion in interest-bearing long-term special issue Treasury securities and $22 billion in a short-term cash management security, called “certificates of indebtedness.” These securities are not traded, and so their value doesn’t change from hour to hour, and they don’t need to be marked to market because the Trust Fund purchases them at face value, and the US Treasury redeems them at face value.

By investing on autopilot in Treasury securities that are not exposed to the market, the Trust Fund follows an ultra-low-risk strategy and operates with ultra-low administrative expenses, amounting to just 0.14% of the assets in the fund.

This strategy keeps Wall Street and its shenanigans away. For decades, Wall Street has been lobbying to “privatize” the Trust Fund in order to suck juicy fees out of those trillions of dollars.

According to the 2021 Trustee Report, 55 million people drew Social Security retirement benefits at the end of 2020: 49 million retired workers and dependents of retired workers, and 6 million survivors of deceased workers.

During 2020, the pandemic year, 175 million people paid into Social Security via payroll taxes – down by 3 million from 2019.

There are some real problems.

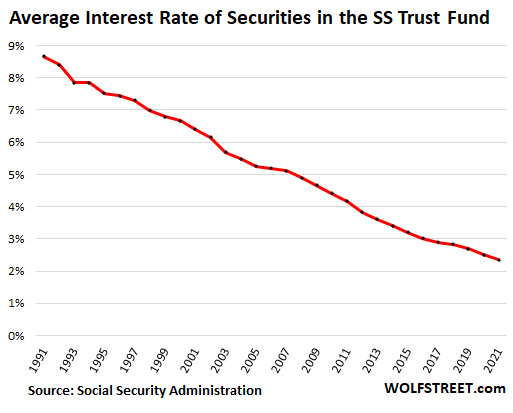

The Fed’s interest rate repression. The weighted average interest rate earned on the securities in the Trust Fund dropped to 2.40% in September. Before the Financial Crisis, the Fund was earning over 5%.

The effective interest rate earned from the Treasury securities in the Trust Fund has been declining for three decades: At first, the rate of inflation was coming down from the early 1980s, and yields were dropping across the board; and then, with the Financial Crisis, the Fed used QE to force down long-term interest rates.

The Trust Fund invests in long-term securities. There is a lag of many years before the replacement of higher-yielding securities by lower-yielding securities pushes down the average interest rate.

The Fed’s interest rate repression since March 2020 is just starting to be reflected in the Trust Fund’s average interest rate and will hound it for years to come, even if long-term interest rates rise.

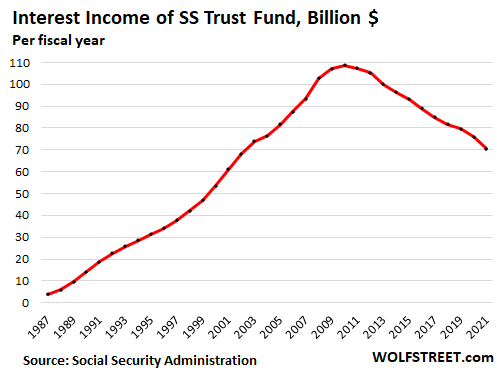

As a result: despite the 13% growth of the Trust Fund assets since 2010, annual interest income has dropped by 35%, from $108.5 billion in 2010 to $70.5 billion in 2021:

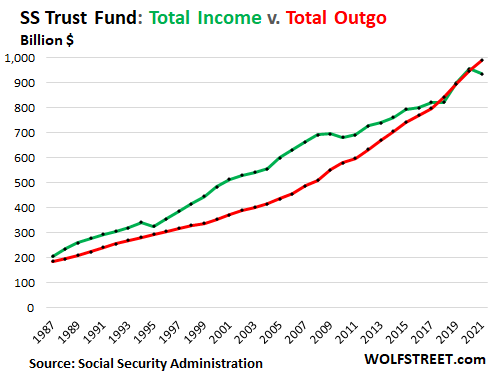

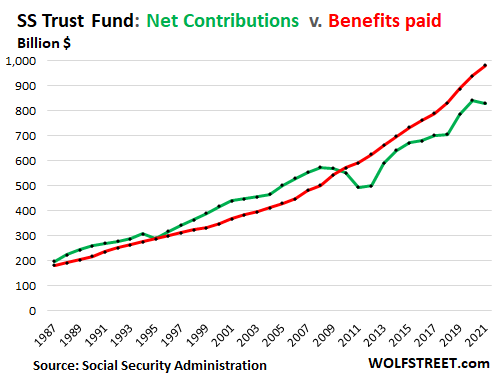

Total income fell below total outgo in fiscal 2021. Income from contributions ($831 billion), interest income from securities ($70.5 billion), and income from taxation of benefits ($34 billion) generated total income of $936 billion, down by $20 billion from the prior year.

Total outgo of the program (nearly all of it in form of benefits paid) rose to $991 billion.

The deficit generated by the lower income and the higher outgo reduced the Trust Fund balance by $55 billion.

When the green line (total income) was above the red line (total outgo), the Trust Fund accumulated assets. When the green line fell below the red line, the Fund shrank:

Employment fell off. Contributions to the fund depend on the labor market, and when people in high-paying jobs lose their employment, contributions sag. This happened during the Financial Crisis when banking, real estate, and many other sectors with high pay shed lots of jobs.

During the pandemic, those people switched to working from home and continued to make money and pay into Social Security. But people on the lower wage scale – such as workers at restaurants, retail stores, and service establishments – lost their jobs, and contributions dipped, but by a smaller amount than during the Financial Crisis:

What has filled in the gap between 2010 through 2020 were the two other sources of income:

- Interest income peaked at $109 billion in 2010 and then steadily declined to $71 billion in fiscal 2021;

- Income from taxation of benefits rose from $21 billion in 2010 to $38 billion in fiscal 2020. But in fiscal 2021, it fell to $34 billion, the lowest since 2016.

Demographics. The huge generation of millennials is entering their peak earning years. They’re replacing the huge generation of boomers (now between 55 and 75) transitioning out of their peak earnings years, and older boomers retiring. The two generations were similar in size. So that balances out. But the generations following the millennials are smaller. And then came the pandemic that jostled all assumptions.

Beware of Vicious Dog: Inflation.

Social Security payments to beneficiaries are adjusted annually for inflation via “Cost of Living Adjustments” (COLA). The percentage of the COLA is the average CPI-W inflation rate in the third quarter, and is applied the following January for the whole year. The Social Security COLA for 2022 is 5.9%, the biggest since 1982.

But CPI-W for October jumped by 6.9%, and the COLA for 2022 is already underwater. And the COLA for 2021 – a lousy 1.3% even as inflation started to rage – has been horribly underwater.

The Fed still has its foot fully on the gas, printing money and repressing interest rates, thereby creating more fuel for inflation. The Fed will eventually react, but it will be too late and too slow to bring inflation down quickly. And the 5.9% COLA for 2022 may not cover even the official rate of inflation as measured by CPI-W.

Each year that the COLA is behind actual costs of living increases, it affects all future years of benefits because inflation and COLAs are compounding, and that gap between them is compounding as well. Even small gaps year after year compound into big differences after 10 or 20 years.

In addition, depending on where retirees live and how they live, actual costs of living increase faster than CPI-W.

The gap between actual increases in costs of living and the COLAs for each year causes Social Security benefits to lose a significant part of their purchasing power over the years.

Depletion of the Trust Fund — if unaddressed.

The Trust Fund, after years of flat-lining, declined in fiscal 2021 by 2%. Relying on estimates for future demographics, employment, wages, retirements, mortality, births, immigration, and the like, actuaries attempt to estimate how income and outgo of the system will impact the Trust Fund.

The Pandemic has shredded the prior estimates in both directions and has created a lot of uncertainties about future estimates.

Employment, earnings, and interest rates “dropped substantially” in 2020, the 2021 Trustee Report pointed out. This lowered the income into the system.

But the report also assumed that the pandemic would “lead to elevated mortality rates over the period 2020 through 2023.” This would lower the outgo.

The 2021 Trustee Report only covers data for the year 2020. The report for the 2021 data will come out next fall.

In October 2021, despite the labor shortage, the number of working people was still down by 4.7 million from pre-pandemic levels, and by 6.5 million people if the pre-pandemic trends of working people had continued. This translates into lower-than-previously-projected income for the Social Security system.

The lower number of working people was in part caused by the surge in early retirements of people old enough to draw Social Security that then started drawing Social Security earlier than they would have otherwise. This increased the outgo.

The 2021 Trustee Report estimated, based on the new assumptions for the pandemic era, that the OASI Trust Fund reserves, now at $2.76 trillion, would become depleted in 2033.

Social Security won’t “go broke,” but adjustments will be made.

It simply means that workers will have to pay more, or benefits will get trimmed, or both. Social Security has been fixed before. So adjustments will be made before the depletion date.

Contributions could be increased by raising the income cap or by increasing the percentage of contributions, or both.

Benefits could be reduced, including by trimming benefit payments by perhaps something like 2% or 3%; or more insidiously by changing how the COLA is calculated.

COLA changes are insidious because they’re technical and people don’t understand them. But they have a large impact disproportionately on people who can least afford it, when they can least afford it – lower-income people, late in life.

The purpose of COLA reductions is to cause a faster loss of the purchasing power of the benefits, while inflation increases wages and thereby increases contributions on the income side.

Proposals have been floated over the years to replace CPI-W for COLA calculations with a chain-type price index, such as the PCE price index, which pegged inflation in September at 4.4%, compared to CPI-W in September of 5.9%.

If a change of the COLA calculation lowers the COLA adjustment by 1 or 1.5 percentage points on average per year, compounded over 20 years, it would have a very large impact on the purchasing power of those benefits. It would doom the lower-income elderly.

So the Social Security system won’t “collapse” or go “broke” in 2033, but benefits will be trimmed or contributions will be increased, or both, before then. The shortage this year was $55 billion, in a system that takes in and pays out nearly $1 trillion, in a $23-trillion economy.

Social Security will be there for you, but…

Social Security benefits will be there for you, but they’re guaranteed to lose purchasing power year after year, even if the COLA calculations are not changed, and much faster if they’re changed.

This is not an accident. Inflation measures are carefully engineered to not capture the true increases in the costs of living.

Retirees relying exclusively on those benefits might not feel the loss of purchasing power for the first year, but it compounds and eventually becomes painful. If it is tough to live exclusively on Social Security early on, it will be brutal after 20 years of retirement.

Social Security was never intended to provide adequate retirement on its own, and it’s not going to. Some people are trying to deal with this by moving to a cheaper location in the US, or to a cheaper country, such as Mexico or Thailand, which can be a great adventure.

A hedge against inflation in retirement is to keep working.

My patented solution is twofold: Build a nest egg while working, and work for as long as possible, either doing what you’ve been doing, or doing something new and interesting and fun. Full-time is great, but even a part-time gig is great, and for all kinds of reasons, not just money, and even if you have plenty of money and don’t need to work.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s nothing that Tom Selleck and a reverse mortgage can’t fix.

Hahahahaha….what about the renters?

Lots of retired folks will be moving south of the border soon enough.

Before I jiggled my portfolio a bit, financial repression was robbing me of about $35,000 per year so government could afford to pay me $20,000 per year in social security. When you control the printer you can do stuff like that.

Or east of the border WAY east I’m on the Med in SW Turkey within sight of Rhodes Greece and inflation is out of control, even in dollar terms

My cousin and her husband (age 70s) were both becoming increasingly mentally incompetent. A lawyer “friend” talked the husband (who was on the cusp of descending into Alz) into doing a reverse mortgage.

The husband had become pretty much incompetent about having a budget and paying bills. When he forgot to pay taxes (resulted in instant loss of residential rights), the reverse mortgage owners swooped in immediately and gave them one week to vacate. It was shocking how fast it happened. Relatives had some political connection and a grace period extended the eviction to about two or three weeks. This was a house they had lived in for 25 years or so.

U.S. is a culture where many sharks are legally allowed feast on many sardines.

When he forgot to pay *real estate* taxes.

At a dinner conversation a realtor brought up similar scenario. It seems if someone pays property taxes on a place they can legally claim it. Maybe a civil war is indeed what’s needed to clean up cr@p like this.

In FL, paying delinquent taxes for someone is more of an investment…

You buy a tax certificate that charges an interest rate…

After two years, the owner of the certificate can force the property to auction for bid by anyone…

At any point in time the property owner can stop the process by paying the certificates plus the interest…

Gives the property owner every last chance to save the property, if they want…

The auctions are on line in real time vs the courthouse steps…

I am not a fan of reverse mortgages… in fact I find them disdainful. BUT… in my experience (in New Jersey), the mortgage holder (the lender) pays the property taxes as part of the reverse loan. I do not know if this is standard, but this has been the case with reverse loans I knew about or was involved with. In fact I believe the law in New Jersey provides a minimum of one year grace period after a reverse mortgagee goes delinquent before a mortgagor can foreclose.

Just an anecdote/opinion from living in over 62 low income apts. That Selleck ad has got to be aimed at old ladies with some equity.

One of the few here with a car, was putting a Ben Carson sticker on her car, maybe even before the first GOP debate. I asked her how she decided so soon, and she said, “Because he is such a nice man”.

The sharking comes in many forms, the “good doctor” was worth $11M at the time. That is one HELL of a lot of brain surgery, even at his normal fee-for-service…maybe that is why he seemed so tired all the time.

The first chart covers my employment period (actually started in 1980) and show the over accumulation of funds the the SS Trust account. I’m just starting to draw SS Retirement benefits and do not feel bad at all that the Trust funds accumulated over the past 30 years will be drawn down. It was funded with my money. If the next generation wants to have a fund to draw on, they should start a new round of “over accumulation” just as we Baby Boomers did.

So, instead we get.

Anyone retiring today at age 65 who worked all their lives will never get back what they put in.

The self employed, who pay the full social security tax of 12.4% are truly generous.

All that money, put in a simple SP500 fund, would be worth an order of magnitude more than what the government will give back to you if you play by all their rules correctly and will take it all if you die.

“This strategy keeps Wall Street and its shenanigans away.:

2banana,

“Anyone retiring today at age 65 who worked all their lives will never get back what they put in…”

BS. On second thoughts, a vicious lie actually.

1. It’s like an annuity that pays for the rest of your life and dependents and survivors.

2. For example, if you and your employer put in $160,000 into the fund over 35 years, and you start drawing benefits as late as possible, at 70, you might get $40,000 per YEAR out of the fund.

So after 4 years, you got out MORE than you paid into it. And it will increase with COLAs over time: you get $40,000 out the first year, $41,000 the second year, $42,000 the third year, etc. After 20 years you got something like $1 million out of it.

“All that money, put in a simple SP500 fund, would be worth an order of magnitude more than what the government will give back to you if you play by all their rules correctly and will take it all if you die.”

BS on all counts.

1. SS is an annuity based on Treasury bonds, you’re not going to make 100% a year, but you’re not going to lose 50% a year either.

2. If you die, your spouse and dependents get survivor benefits.

3. As mentioned above, if you and your employer paid in $160,000, and you draw at 70, you get $40,000 out the first year, and with COLAs, after 20 years, you got out something like $1 million – unless inflation is very high, and then you’ll get out a lot more.

4. You’re supposed to be diversified. If you put all your stuff in stocks, when stocks crash, and you’re 75, you’re screwed.

SS is a TAX, not an annuity. Please read your latest newly reformatted SS statement. An annuity can be bought, sold, redeemed, transferred, not so for your SS.

If you have dependents at age 70, then it sucks to be you.

I’ll take all I paid into SS now and invest as I see fit.

The fund lost 2% with inflation at 20% and a raging frothy bull market (I understand SS doesn’t invest in stocks, but with the FED controlling the market they should)

As usual, anything managed by .gov is a major loser.

JM

You mean like the Military Industrial Complex ?

You mean like management of all those nuclear warheads ?

You mean THOSE losers ?

JM,

Your vitriol aside, SS never should be gambled with…

It is supposed to be one portion of an overall retirement plan…

Even with the best investing period of the last 40 years, many boomers pissed their extra investable incomes away not worrying about their retirement years…

Without it, a lot of people would barely able to survive…

You can’t play a coulda shoulda game when your game is almost over…

While I understand you’re venting, things happen in life that can’t be predicted…

While I hope it never happens to you, the choice between being able to have a place to live and the overpass may just come down to the SS that wasn’t gambled away by the predators on Wall Street…

Think of pension contributions as an insurance policy for aging and retirement if it helps. It certainly is not a tax. I obviously do not participate in SS being Canadian, but we have our less generous version CPP which is also mandatory. It is sure nice to get that monthly deposit when retired and know it is untouchable. I also paid into a private pension plan which my employer matched and is also untouchable and protected by COLA. Now retired, I sometimes get the ‘must be nice’ comments and I simply reply that I paid in $1,000 per month into it for almost 20 years, and yes it is nice. It is freaking awesome. Our additional private investments are gravy, which is exactly what 401Ks were designed to be, simply add ons, and not the survival foundation. My neighbour/friend down the road relied on private investments for the bulk of his retirement and lost most of his nest egg during the GFC. He then had to sell off land investments to make up those losses.

My Dad was American and a WW2 vet. He collected SS as a result and when he died my mother transitioned into the survivor benefits for almost 20 years. It was more than enough to live on because her house was paid for. It is a very generous plan compared to others. Plus, it is not managed by Govt, it is mandated. The reason? Any Govt does not want a bunch of starving old folks demanding help after the Madoffs and Sellecks of the World finish their suck.

regards

@cowg,

“SS never should be gambled with”

Keeping retirement savings in cash is a gamble, keeping it treasury bonds is a gamble, keeping it in index funds is a gamble. Trusting the government to keep its promise when one’s game is over is also a gamble. Nothing is gamble-free.

Nacho Bigly Libre,

There is a well-understood and well-documented spectrum of risk. Low risk = low potential rewards and low chances of loss. High risk = high potential rewards, and high chance of big or total loss. It’s a choice every investor makes every day for a variety of reasons.

Gambling is at the very high-risk end of the spectrum, investing in Treasuries is at the lower end. SS is far lower risk than Treasuries because SS is adjusted for inflation.

Inflation applies to all assets the same. You can lose 50% in the stock market and lose another 10% to inflation, no problem.

Or you gain 50% in the stock market, and lose 10% of your total purchasing power to inflation.

Or you can earn 1.6% on your Treasuries that you buy when issued at face value, and can be sure to get your money back when they’re redeemed, but lose 10% of their purchasing power to inflation.

No one escapes inflation except to some extent Social Security benefits are adjusted for inflation at least partially (other investments fall into this category as well, such as I-bonds).

One of the reasons why SS needs to be fixed is because it’s such a good deal for people who live for long past retirement. Lots of people live to be 95+. SS is an immensely good deal for them.

When LBJ was setting up Medicare, he insisted it be a payroll tax deduction, like SS was.

His reason, “I don’t want some politician getting rid of it”.

Same reason Bernie and others want single payer health to be a payroll deduction.

Contract law with proven individual payments is hard to get around.

And keep it out of the casino, as Wolf and Paulo have said.

Hi Wolf.

With respect to social security, what’s the break-even age for retiring at 62 vs. 67 ? I thought it was around 81, but don’t recall where that came from.

Thanks

I have seen two different approaches. The traditional one says that the break even is roughly 80 if memory serves me correctly.

I have seen another analysis that says the break even is around 90 because the traditional analysis does not factor in that you might croak before you get a dollar if you delay.

There’s a free detailed retirement planner on line called Optimal Retirement Planner (ORP) that allows you to input everything and it will tell you at what age drawing social security is optimal for your situation.

I like it because it’s got the tax system programmed in and will spit out beautiful graphs of your drawdown plan. It also can do some Monte Carlo analysis if you desire for getting statistical solution if you are a math geek.

Sorry Wolf, that math looks very faulty.

That math ignores inflation, real dollar value and most importantly, the magic of compounding.

If someone had contributed $1000 thirty five years ago, in real dollar terms that’s equivalent to about $2500 today; not $1000.

If the same $1000 was invested in S&P500 35 years ago that would have become about $50000; not stayed $1000.

If the same $1000 was invested in Berkshire Hathaway, 35 years ago that would have become about $130,000; not stayed $1000.

If that same $1000 was invested in real estate, well, you can guess.

Above are the returns from just one investment of $1000, not cumulative over the years.

We need to remember every $1000 that was taken forcefully from a worker and put into this SS fund was the $1000 that the worker could not invest by herself/himself.

Nope, that wasn’t the statement that I responded to. You changed the topic to “which investment is best.” The statement I responded to was:

“Anyone retiring today at age 65 who worked all their lives will never get back what they put in…”

I show that they “get back” what they put in after four years.

I don’t feel SS was taken FORCEFULLY from me in my 45 years of working but you can word it any way you want. It’s actually a chicken s**t way of saying it.

I would say too many people wouldn’t have saved a dime for themselves and with SS plus Medicare, everyone comes out way ahead.

As I said before here, Social Security was born during the depression where countless forgotten elderly starved and/or froze to death. I heard the stories directly from the people who saw it and experienced it.

When I was a kid in the 60s, nearly everyone grew a garden and talked about where they put their savings accounts (which actually paid interest). The depression had left a taste of fear no one could forget.

I can only imagine what the next one will be like.

Best to done what Chili did. Privatize it!! Proven record with the right People handling it.

Chris,

Do you mean Chile?

There is a big difference in:

1. Letting people manage their own money.

2. Government taking their money and having private parties manage it.

Option 1 is what I am (and many others are) proposing.

Option 2 is far more prevalent in USA – you might not have even realized that. Most big cities and states manage their pension programs this way. Check your own city’s employee pension program – you might be surprised.

Mandatory contributions and the funds managed private companies or fund managers. Those funds all have unfunded obligations.

Thanks Wolf, your’ commenters are loaded with a lot of bumper sticker (echo chamber b.s.). Thanks for being logical and reality based.

Agree. I’ve ignored all the alarm porn about SS until I could read Wolf’s calming facts instead. Much appreciated.

Wolf, also S.S. has dependent benefits for children that add to the benefit that can be paid. A young earner, with a family who puts very little into the S.S. funds dies, S.S. pays a benefit for each child until they reach adulthood. Many have claimed that benefit that would have drained a young workers stock retirement fund.

Thank you Wolf, for,

at least trying to straighten out the total mess,, of the stories,,, as in lies, damn lies, and statistics… re SS programs now and always…

Good luck combatting the lies that some parties,,, wallstreeters et al, who want to make the case to take this program ”private” to harvest the fees, etc., as you cite in this article.

Grandpa went back to work in order to pay into the SS system, and pledged to do his best to ”live” on his $100 per month and not yo touch his capital,,,

and did so for many years,,, mostly,, ”on the hook” in his home made sailboat,,, and then in his mid 80s, similarly in a home made house/home until his death…

Certainly, living on one’s SS income alone can be done these years,,, but, the kind of ”frugality” might be very challenging for the boomer types, not to mention the ”me too” types of subsequent younger folks…

Though it’s true many people do get more out of SS than they put in (even accounting for inflation) the math on your example is pretty far off unless you’re using some crazy, convoluted situation that isn’t typical. A 4 year payback IS possible, but only for somebody receiving a benefit of only ~$12K/yr, not someone receiving $40K/yr.

Even waiting until 70, a $40000/yr benefit is pretty close to the max which means the retiree & employer has paid in close to the SS max for 35 years. And that’s going to amount to a lot more than $160K, even if you don’t correct for inflation. And if you do (which you should), it’s WAY more than $160K.

Also, regarding being an annuity – it’s true it pays out benefits like an annuity, but the “cost to purchase” is not really like an annuity at all. Though there is some relationship between how much you put in and the benefit you get out, it’s not even close to linear and is highly regressive – the first dollar you put in each year is worth ~5X more than the last dollar (if you make more than ~$70K)

You’re describing another Ponzi scheme, the same one we have with the current asset mania.

If Bush the younger’s proposal to “privatize” social security had become law, it wouldn’t improve aggregate retirement security one bit.

Asset inflation is not real wealth. An individual can spend this fake wealth at full value if they get out early enough, but this is no different than their position in line to receive social security benefits from the “trust fund” or who receives “printing” money first either.

The real long term problem with social security is the lack of real economic production to pay current benefits at anywhere near current nominal value. That’s why these gimmicks are used with the COLA to supposedly make the program more sustainable.

Augustus Frost,

“You’re describing another Ponzi scheme, ”

Nonsense. It’s like an annuity. It’s a form of insurance. It has done very well for 80+ years it has been in existence. Wall Street is just envious because it cannot suck fees out of it.

Look up the definition of a “Ponzi scheme” and then read the article above so you can actually learn what SS is and how it works.

SS has done well up until 10,000 money-lusting boomers retiring every day. Now things have changed. How about we carve $300 billion off that $800 billion annual military budget and easily fund the shortfall for next 10 years? Or maybe get AAPL and AMZN to pay taxes? Happy Veterans Day.

Wolf,

To be fair reading the definition of a Ponzi Scheme and An Annuity, Social Security to me seems to be something in between

Ponzi Scheme:

a form of fraud in which belief in the success of a nonexistent enterprise is fostered by the payment of quick returns to the first investors from money invested by later investors.

This analogy fails because the underlying enterprise is well known to all. >investing OADSI taxes in US govt bonds to pay old age and disability payments. As Interest rates are now below the rate of inflation, I think the comparison to a Ponzi Scheme is more apt given that it better resembles using current investor funds to pay previous investors. That said, no one believes SS is a get rich quick scheme.

Annuity:

a fixed sum of money paid to someone each year, typically for the rest of their life.

This analogy fails both because SS is inflation adjusted (positive for recipients) and because as you point out in the article benefits can be reduced by the SSA, or halted altogether (negative for recipients).

As you point out it has worked on average reasonably well for 80+ years, as when it was initiated there were 20 people paying in for each recipient. Now there are around 3 and the strain is eating away at the SS trust fund, along with heavily manipulated govt interest rates starving the fund of returns.

For what its worth, to me, an employed person of 41, who first paid into SS in 1995, it does seem like like a bit of a gamble to get back what I have paid in.

More taxes, reduced benefits and unknown lifespan. Given the choice I’d walk away from what I’ve paid in to not have pay in any more.

The stock market is the real ponzi scheme, it’s massively overvalued. For decades people have been putting more and more money into it, because it can only go up. Eventually, more people pull out than put in and the value crashes. One of these times it won’t just fully recover in a couple years either. That magic money tree will be over. The stock market has real value, but will become stagnant and can only long term grow at the rate of the economy/global economy.

In order to protect the stock market and other forms of asset inflation, the government has massively skewed the economy and allowed such things as offshoring of critical manufacturing.

Social security has never caused anything like that. Once people eventually come to the realization that all services and products produced in a year, come from the workers, working that year, and not savings. And that the stock market isn’t a tenable retirement solution for the masses. Directly transferring money from workers to retirees will be the only practical solution. Over time, the amount paid into social security will have to be upped by the general public (the average jo will have to pay more) as it becomes the main form of retirement.

If the stock market bubble didn’t have to be protected (and other reasons), real competition might exist in America and inflation would be much lower. The total economy would be larger and so whatever percentage of an average worker, a retiree would receive from social security would go much farther.

The entire Healthcare system has to be redone as well.

Like most other things, change cannot happen, until the everything bubble bursts.

It keeps the shenanigans continuing. What is going on again here is like what was done to Japan and Asian economies to allow foreign “investors” (meaning the trillionaire families) to buy up their banks and companies for cents on the dollars. Read “Princes of the Yen” and watch documentary of same name as to those shenanigans and the “Federal” Reserve’s sister, bankster cartel, the ECB.

Cui bono? I predict the trillionaire families will end up owning even more of the US and world economy. With more inflation soon, your social security will be worth little. Be a good little sheeple and bend over yet again for them.

Curious they can print money for all the social programs, SNAP, food stamps, child credits, etc…

but never a word of doing same to support the SS system…which has been robbed.

They’ll print the money to keep SS current.

While they may move up future retirement years again, they won’t remove benefits.

Politically it would be a disaster.

Wolf I have been toying with this idea, maybe an article to educate folks on this if this is a good idea. My company “match” for 401k is 3%. What happens if I stop contributing to 401k but instead put 10% of my post into a ROTH. Seems to me like we keep feeding the beast and then complain the beast is eating us. Time to stop feeding it.

Full social security tax 2021: 12.4%

Full social security tax 1950: 3%

“The huge generation of millennials is entering their peak earning years. They’re replacing the huge generation of boomers (now between 55 and 75) transitioning out of their peak earnings years, and older boomers retiring. The two generations were similar in size. So that balances out.”

“…or to a cheaper country, such as Mexico or Thailand, which can be a great adventure.”

If only the Euro — as the dirtier shirt in the laundry — would hurry up and tank vs USD, the French riviera or Liguria could be in play. Count me in for that.

1. For millennials and genZ, there will no social security. There may not be a society or security either.

2. Even if SSN stays, they pay very less or pay peanuts. Inflation will eat them away

3. Given the rate of obesity, lifespan may be reduced or people will be severely diseased.

4. With Virtual reality and meta, most people prefer to live in the VR as characters rather than real life

5. Wiseguys already full on stocks and $it coin will be able to retire earlier and comfortably.

6. At this rate of inflation, houses brought today will be paid easily. But there will be no buyers either

7. Happy veterans day…

Cobolt– you claim:

” For millennials and genZ, there will no social security.”

How do people get and believe this garbage. Unfortunately, one person starts this kind of BS on the internet, and gradually a lot of others start echoing and repeating it without any evidence or logic.

I’ve written the following on how Social Security works, taken from the SS administration, and also from a Stanford economics course I took very many years ago.

I hope it is helpful for those who are interested in really understanding it, rather than for those ready to believe and spread more BS. Yes, it’s based on a reference document from the government, which of course some will also declare it therefore must be just lies.

It doesn’t deal with the important comments made by Wolf about the inaccuracy of the Social Security COLA, but does explain something about how it actually works.

Inflation does not matter as long as FED keeps printing money and pays for the gap in social security system

Not true.

If this were true, then government’s everywhere could prevent declines in aggregate living standards.

And don’t forget the sky rocking costs to carry a single family house ie Insurance, property taxes, maintenance, HOA fees, Somehow I’m not terribly bullish on American housing as I once was

To millennial voters, AOC is a centrist. I’ll bet social security payouts are doubled when millennials retire. They’re going to vote in a whole government full of Bernie Sanders clones once boomers and dead and gone.

I’ll bet by 2060 tax rates are high while millennials collect fat SS checks and free healthcare in retirement.

Correct me if I’m wrong on this, but I understand the SS Trust Fund to be all an accounting gimmick. That is to say, it holds nothing, it simply is a ledger that states what the US owes it. The actual funding day-to-day and year-to-year comes from the US Treasury through the CURRENT sale of bonds.

So no true savings account in the usual manner that is thought of.

READ THE ARTICLE.

Generally, you should read the article before dumping garbage here.

ROFL

Agree strongly with your statement above about carving 300 billion off of defense. We spend a ridiculous amount on defense and that would be the perfect funding mechanism to help out SS Social Security is a good program that does a lot of good for people.

That seems a bit of a harsh slapdown considering in the article is this

“The OASI Trust Fund invests exclusively in Treasury securities.”

Which are certificates that state what the US owes it. How is the comment garbage?

Not unusual either, I know this is a US site but for anyone interested the UK has a segregated tax called National Insurance which supposedly pays for pensions (and health) but just goes straight into government income while the liabilities are just listed as IOUs. In fact in the UK case they aren’t even listed as part of the government debt because they only become due in the future. The UK government -could- hand some notional pension authority sufficient gilts to the value received but what would be the point?

And so, the US system which does this, why not describe as an accounting gimmick?

I responded to this part in his comment:

“….the SS Trust Fund to be all an accounting gimmick. That is to say, it holds nothing, it simply is a ledger that states what the US owes it.”

This is truly garbage.

True. Before the Trust Fund can pay for any benefits the Treasury bonds in the TF have to be paid back by the Federal government to itself – out of future Federal tax revenue – which is already sadly insufficient to cover other existing Federal spending commitments.

Read the section about the assets of the fund. The fund holds long-term Treasury securities that it doesn’t sell. And short-term cash management securities, called “certificates of indebtedness,” that is uses for cash management to manage the inflows and outflows.

You can do a similar thing when you set up an account with Treasurydirect.gov

Does the Social Security Administration provide weekly or monthly data on withholdings/contributions?

I would trust that to give me a better view of employment and wages than the BLS surveys. Contributions are a direct and real-time measurement – no room for fudgery.

It’s a misleading figure because it doesn’t include quarterly and even annual payments by the self employed, such as lawyers and the like.

“All that money, put in a simple SP500 fund, would be worth an order of magnitude more than what the government will give back to you if you play by all their rules correctly and will take it all if you die.”

>……

4. You’re supposed to be diversified. If you put all your stuff in stocks, when stocks crash, and you’re 75, you’re screwed.

In other words you may be doubly screwed If you bought into the 401k equities myth that was not originally intended to replace defined benefit pension plans. Next up Medicare, an even more dire situation.

@Boomer,

If that same money is all invested in treasury instruments which pays less than rate of inflation, how will you ever come out ahead? Aren’t we scr***d?

That shortfall has to be covered somehow. So far the shortfall has been covered with:

1. With new payees

2. Tax increases (rate and tax base)

3. Reduced benefits

4. Taxing ‘excess’ benefits

None of these are sustainable.

Thanks for this awesome post – nice collection of data.

In the long term, never taking a risk is the biggest risk. The Treasury has been paying less and less interest – zero or near zero interest. That’s not being risk free.

When the same entity (government) decides the interest rates, is in charge of CPI and COLA, decides the tax base, decides maximum benefit, there are multiple conflicts of interest. That never ends well. I would never willingly put my money into such a disastrous annuity program.

By nature SS is a Ponzi scheme. Any adjustments made will be temporary and can not hide the reality for long. One solution is to kill the program now and eat the loss. Whoever has contributed already, can be made whole. If left in place, the problem will grow too big to solve.

“By nature SS is a Ponzi scheme.”

Look up the definition of Ponzi scheme, and then read the above article about the finical facts of SS.

Wolf,

I also get frustrated with the nonsense people post about SS.

It is not a “Ponzi scheme”. SS is like insurance, NOT a savings or investment program. In fact , the cards when it was originally started said “Social Insurance” on them. Sometimes you are going to get more than you paid in. Others will not. That’s how insurance works.

Since I have never had an auto insurance claim in the 40 years I have been driving, maybe I should call State Farm and ask for a refund of all the premiums I paid due to the fact it was a “Ponzi scheme”.

There are many who pay in for decades and never draw a dime in benefits. It’s also provides survivor benefits to people with families who have met an early demise. Same with disability benefits. Critically important program these days partially as our average longevity declines due to the Pandemic. Those who would trash the system better be careful what they wish for.

‘Wall Street is just envious because it cannot suck fees out of it.’

This…..

‘ For millennials and genZ, there will no social security. There may not be a society or security either.’

Lordy, I am over 70 and I heard the exact same thing when I was a teenager. Easy to predict the future. Hard to be correct.

doug,

Me too. The dad of my high school sweetheart told me when I was 17 that SS was a scam and that it won’t be there for him, and that it won’t be there for me. He retired many years ago and then for something like 20 years, he drew SS benefits, and then he passed away, and his wife continues to draw the survivor benefits to this day, and I could draw SS if I wanted to.

This nonsense has been propagated my entire life. It’s just hilarious how the same nutty stories survive for so long, copy and paste.

So many of the commenters here have listed the reasons why it’s an unsustainable model.

One can only take a horse to the water, rest the horse has to do.

I once asked a social security representative if I could sign a paper where no money ever would come out again of my paycheck to social security. In exchange I would forego the money previously put in. He laughed and said he gets that question asked at least once a day and the answer is no. The US is the absolute worst country except for all of the other countrys which are just as bad. I actually have no solution. I wish I did

Lay flat, black market, or start a business and take most of your pay as owner earnings rather than wages so as to avoid social security deductions?

Ida May Fuller,teacher of Brattleboro,VT was the first beneficiary of recurring monthly Social Security payments.

The first Social Security check number 00-000-001, was issued to Fuller in the amount of $22.54 (equivalent to $416 in 2021) and dated January 31, 1940.

During her lifetime, she collected a total of $22,888.92 in Social Security benefits and paid in $24.75.

Lately these numbers IN $24.75 & OUT $22,888.92 ceased to look good,much less inspirational…

Ida Fuller is still mentioned at ssa.gov website but the second number $22,888.92 was quietly edited out.

But it is carved in stone (i.e. can be found in the book “A History of the American People” by Paul Johnson).

Cute fact.

But do you have an actual point ?

SSA has an actual point:

“Coping with the Demographic Challenge: Fewer Children and Living Longer”

Long research paper posted on SSA website.

Taxpayers to retiree ratio:

1950: 18 (When Ida Fuller enjoyed her 10000% ROI)

2018: 2.8

SSA admits if this ratio is less than 3 system becomes unstable.

Now with people dropping out of the workforce and living like Lilies of the Field (they dont spin,neither do they toil) – what is the ratio now ? How stable is the system ?

True we are having fewer children. This will be something for the next few generations to make choices about. Immigration has helped keep the SS system stable in the past.

We aren’t living longer. Life expectancy has dropped due to covid. :(

Covid is the #1 cause of death in my State, Az.

Biden made a campaign promise to SS recipients receiving payments under the poverty level to increase their benefits to 125% of the poverty level. This would bring those people to about 1300 a month minimum, not a lot of money. Many older voters believed him when he promised to do this and so far he has forgotten all about his promise.

Also, they have yet to announce the medicare premium and deductible for 2022. This is sure to eat up the rest of the 5.9 increase.

These issues highlight why I had no problem taking the stimmy money and spending every last dime. I’m taking my SS early too, because money now is worth more than money later.

These kind of political promises are kind of why I think people shouldn’t worry too much. A politician (either party) will just promise a big raise if things get too out of whack. I wouldn’t count on it but seems like a good way to get a bunch of votes. If the monthly SS check is only covering the average rent, millions of voters could easily be convinced to help the poor retirees even if it results in SS taxes increasing which are enviable either way.

Petunia – “Also, they have yet to announce the medicare premium and deductible for 2022. This is sure to eat up the rest of the 5.9 increase”.

The part B premium was 148.50 in 2021 and will be 158.50 next year, or $10 higher. The part B deductible was 203.00 in 2021 and will be 217.00 next year, or $14 higher. Makes a total of $24 higher.

However, the medicare supplement insurance is what can get us. Mine goes from 123.66 per month to 136.05 for next year, or 12.39 per month increase.

My part D drug plan actually went down for next year, but I usually don’t meet the deductible anyway.

If the average SS monthly annuity payment is 1,500 (insert your number here) and we get a 5.9% increase, that is 88.50 per month increase. 88.50 – 24.00 – 12.39 = 52.11 increase per month which whittles that 5.9% COLA down to 3.47%. Therefore inflation is more than eating up the rest of the increase.

So yes, we are going backwards because of inflation. Social Security was never designed to provide full retirement income, but to supplement what was saved up during ones lifetime. I think that is what is being lost in this discussion. People need to save for retirement themselves as their main source of income, or find a sugar daddy as another option to Wolf’s options.

Charlie,

The medicare premium rates you cite for 2022 are only estimates, the real figures have not been released. So you really don’t know yet what medicare will cost you next year. They are estimating a 6% increase so far.

Also remember your increases in supplemental insurance amounts hit recipients with lower benefits harder than they hit you.

Charlie,

Just read the updated numbers for medicare part B for 2022. The premium is going up to $170.10 and the deductible is up to $233. A total of $51.60 per month. A SS beneficiary receiving $1000 in 2021 would have gotten a COLA of $59.00 – $51.60, for a total increase of $7.40 a month. The real COLA increase is 0.074%. The SS thievery continues.

The deductible of $233 is an annual deductible, not monthly.

I believe that if you have your part B premiums come out of your SS payment (which most people do) then the max increase percent of the Medicare premium is limited to the SS benefit payment increase percent. As such, the numbers you cite would only apply to new Medicare beneficiaries.

Taking SS early worked out well for me. At 65 I had a widowmaker heart attack and then two small strokes two years later.

I will take out more than if I had waited until 67. And I had a few years to travel and enjoy before health issues.

The least obvious way to get more money in the trust fund (raise revenues) is to crash the stonk market, and force those Wall St mongrels to buy treasury bonds. And I think I know a way to start the salivating, just one teeny quarter point.

Thanks Wolf, best summary I’ve read to date.

Keep it up, you’re an asset — and an appreciating one too!

I think the children of social security recipients benefit too! Would you want to have to take care of your fully broke parents? Even if you have to care for your parents it helps you that they get a SS check.

Dan

Excellent point !

Always forgotten !

Virtually everyone derives some benefit from SS.

I totally disagree with your ~3% reductions in benefits projects for the 2033ish come to Jesus moment. Will it be the worst case scenario 20-25% doom & gloom, probably not. We really won’t know until we see the next 3 years annual reports as to how quickly it’s going to run out.

For the most part, SS being able to pay near 100% of its future benefits will depend largely on the SS taxes paid by the high earners once the adjustments are made. The problem is that it could take Congress at least 8 years to do anything meaningful. Right now, the DEMs are salivating over raising all sorts of taxes on the rich. Well, if that happens, it’s going to get much harder to force the rich people to save SS with these down-the-road adjustments.

Like most things, it’s really going to take a while longer to see how things shake out. And don’t forget, America will run at least $1.5T deficits over the next 5 years. Medicare Part A’s trust fund may run out in that time. Part B will be at at least $1T deficits by then.

The bottom line is all of this is connected, and the risk to America with Congress’ incompetence grows greater every year.

Where ubeen rich don’t pay taxes remember Leona went to jail for running her mouth got made a example

Wolf server has been down for hours.

Yea, we’re all effed, Ludwig von Mises was right.

42

He’s also dead.

So there’s that…..

So where do we from here?

“Inflation measures are carefully engineered to not capture the true increases in the costs of living.”

Wolf, what are your thoughts on TIPS?

The US Social Security program, setup by the Old Age, Survivors and Disability Insurance Act in 1935, was never a retirement program. It was designed to transfer income from upper income to low income people to prevent them from starving in retirement. We all know about the 12.4% SSA tax and 2.9% Medicare tax on the first $147,000 of our income, with W-2 employers paying half. Few will check the Social Security site to see how their benefits will be calculated.

If you search for “social security pia” there is a page with many links describing a curve with 2 bend points. The lowest income retirees get the highest payout. For 2022, the monthly income credited and percentage used to calculate your benefit are:

$0 to $1024 worth 90%, $1025 to $6172 worth 32%, $6173 to $12250 worth 15%, over $12250 is no credit as no tax paid

For people at the $147,000 end, the benefit is about 30% of income credited. With luck they could do much better in the stock market. However social security is a government backed annuity for life with COLA and disability and family survivor benefits. For most people (the lower 90% in income), SSA is an important backstop to their other retirement savings in case they suffer financial loss.

Great review, Doug, One has to wonder how the max cap & bend points will evolve over the next 8 years or so as we march towards Social Security’s day of reckoning. I for one am not nearly as optimistic about Wolf’s 3% reduction in benefits. Certainly, Congress will act eventually. The question is how will they act and to what extent will the rich be forced to see their benefits drop.

One idea that’s always been floated is aggressive means testing….for those fortunate to have other income and cash positive assets, less SS for them….boo hoo, but we paid in, we deserve it….sure, but it’s a fascist corporatocracy and they have to be made whole before anyone else…the one’s on tbe bottom are screwed anyway..

Maybe there’s a simple answer, but why is the SS limit so low?

Sure, it goes up a little every year, but why not say all sources of income are subject to SS taxation? It’s not fair for people of modest means working a W-2 job to have to pay taxes on all their wages. Just add a few more more bend points and adjust the percentages. Maybe even lower the % collected in the last coupe of bend points down by say 1/2 each, so it drops to 8% paid on and then down to 4%.

Now, I’ll be the first to admit that, on paper at least, the rich certainly pay their fair share of all taxes collected. What, the top 1% pay 50% of all the taxes, and the top 10% pay something like 70%?

And, the way Biden wants to raises taxes even more on the rich, well, I would say SS better hurry up and get in line and call their local Congressman.

There are several things that could be done to address the social security short fall.

First is to make the upper $12250 limit another bend point and collect the 12.4% SSA tax on all wage income above $12250/month. This the same as the Medicare tax that is applied to all wage income. All income above $12250 could be worth 8% toward your benefits. With the additional tax, it may be possible to increase the 32% benefit payout to 33% or 34% to help middle income retirees.

Second is to apply income, SSA and Medicare taxes to the gains in stock and stock options companies use to pay employees. Employee stock options date from the 1950’s when voters were unhappy with high executive pay. Congress stopped companies from deducting any salary in excess of a million $ from their expenses, but allowed employees to be paid with stock. This was a huge win for companies (pay in stock, not cash) and employees (deferred long term capital gains) and a loss for stockholders and tax payers. If employees are unhappy with a 35-40% tax hit, they can ask their company for more stock or a lower grant price. There could be a $10,000+ deduction on gains.

Well for some good news, at least USG series “I” bonds are paying 7.2% for the next 6 months. Gotta supplement that social security. Just opened my account today.

With MMT, you can just print any and every problem away. Enter Lael Brainard – the architect of the end of the USA. Full clown show coming soon to a bigtop near you.

The composite rate for I bonds issued from November 2021 through April 2022 is 7.12 percent. Perhaps J-Pow could make I-bond rates permanent at current rates with “the stroke of a pen” (joking).

Next J-Pow can wave his magic monetary wand and change the $15,000 I bonds maximum yearly purchase limit to his favorite number, infinity. And then he could repeat daily that the change is simply transitory and thus will not add to the long term interest costs of the Federal Govt…

So easy even a Fed could do it…

The most effective ‘adjustment instrument’ is not being discussed here – the retirement age. Obviously, that is a hot potato for politicians but it would be most effective nevertheless. Emotionally a taboo but rationally very justified: as people get older, the number of years people spend in retirement increases every year. What if the retirement age were increased to 70?

There is no real retirement age! You can retire NOW at 70 if you PLAN to at that age. People need to take responsibility in planning for their OWN retirement. The more hands allowed in this decision, then we can all start wearing the same color of clothes and eat meals picked by others.

I officially retired when I turned 69, but I “retired” many times in my 20’s.

1) COLA is catching up. If inflation moderate so will COLA, just slightly behind.

2) Since the eighties the average CPI is 3%. The peak was in 1990. COLA is historically lagging.

3) Since 2009 the CPI became negative twice and COLA didn’t respond.

4) If the high inflation switch to deflation COLA will have a change of character.

5) In order to save the fund from going broke COLA will have to turn to negative territory to some people. Squeeze SS as much as u can, especially if u are in the upper echelon. Retire as early as u can, if u care !!

6) Those who contributed the most have a target on their back.

7) The chart predicted that Crude oil futures can dive to deep negative territory and that Ford is $1.01 one day, but software ignored it, because human create AI.

8) Wake up software engineers, negative rates are here to stay. They are mean, crazy and stubborn. They can bite like a shark, which mean : serious injuries and slow recovery, if u survive.

9) In order to keep tranquility the gov will provide enough stimulus to

critical industries, at the expense of other plans, so they can be sold at lower prices.

10) Those who intended to play golf til their last breath will discover few holes : the golf course will be closed.

The simple fact is that a large proportion of Americans do not have ability or self-control needed to save or invest wisely for the future. Some people just don’t have the ability think rationally and/or act wisely about the future. If allowed, many would put that money into bitcoin, NFTs, or whatever. But they may have other redeemable traits that are good for society.

Social Security is a form of socialism designed to salvage something for those people, despite themselves. This in addition to people who would have done will, but have had bad luck at no fault of their own making.

CNN Business (Sep. 9):

“Between July and September, US household debt climbed to a new record of $15.24 trillion, the Federal Reserve Bank of New York said Tuesday. It was an increase of 1.9%, or $286 billion, from the second quarter of the year.”

So it’s not rocket science to know where most the money would go if people could opt out of social security. Competent people may be angrily critical of Social Security, sort of like a totally genetically superior healthy person being angry about paying for health insurance.

However, if those people are so competent and superior, they should be able to do well in the long run anyway, even paying into the Social Security system.

The Crypto gen acquire good trading skills. They use all kind of geometrical shapes that indicate targets. They don’t care if the trend are up or down. They look at targets produced by software, for which they pay fees every month. They imitating other gold members in their trading room and ignore the rest.

Some people, like the ones who wait on you at restaurants or ring up your purchases, don’t earn enough to save or invest. They also get the least amount of SS when they retire.

Some people, usually men, work very hard manual labor jobs and are disabled by age 40. They also get very, very little in benefits.

Dear readers,

If you couldn’t reach Wolf Street today for a few hours it’s because of a complete fiasco whose origins remain a mystery. My three-month old super-duper Linux server has been acting up for two months, getting increasingly ornery, and today finally decided to puke on everything. I have gotten no explanation about the issue or issues. They don’t know either, it seems. But they replaced the whole rig just now, and it seems to be running OK, knock on digital wood.

My apologies.

OK, I just noticed the time stamp is now completely off. Let me go down to the engine room and see if I can fix that.

It’s just a disrupted bilge pump supply chain effect..the problem should fix itself in say two, maybe three, years! Got life vests?

Phew! I was beginning to think they had arrested you for being too honest for being honest and accurate regarding the shenanigans of the US Fed.

don’t believe you don’t have a ssh access?

I worked for wages 20 years prior to retirement. As a high wage earner SS stopped my deduction around September every year. While I appreciated the extra money I was living just fine before. It would not have hurt me one iota if they kept deducting. Since then I make money which does not require me to make contributions.

It seems easy enough to me to lift the cap on when contributions are deducted as well as requiring non wage earners who make over 200000 a year to contribute.

1) Paul Volfer gave inflation a shark bite.

2) After 1987 bottom the CPI reached it’s peak in 1990, in the reaction zone. So far, this peak stand, but the 1987 low was breached. The current Nov 2021 spike might be a dead cat bounce (an UT ?).

3) Since the early 1990’s, CPI spent most of it’s time in the lower half.

4) PnF experts calculated accumulation for hyperinflation, in case of a breakout.

5) In the last 30 years CPI osc in the lower half due to it’s injuries.

6) The clogging, the hugging of the bottom and the sudden negative rates indicate that the risk of a large negative spike is still high. Bubble up/ bubble down.

7) Our children and grandchildren will not pay the price for our fancy retirement plans. They will have problems of their own.

QQQ & SPY built a new backbone.

The DOW, too.

Great post Wolf.

I have played around with Social Security “reform” calculators for about a decade now (the Committee for a Responsible Budget has a really good one) and it used to be easy to extend SS solvency with simply a couple of hedges… a half point more in taxes… a half point less in payments. Voilia!

But the delay in making the fix is starting to make the fix more difficult…. now it is more like one percent adjustments. It is truly weird to me that Baby Boomer politicians have not done what is necessary to extend the solvency… it is their generation that will bear the brunt of the problems if they don’t.

Not to be to ‘flip’ but SS is operationally a ‘pay go’ system based upon the stats Wolf details. That means Congress can put in or take out any Treasuries it believes will enhance the SS benefits. It could insert 30 yer Treasuries that carry higher interest rates, and do the same with the shorter term bills. The math will always be correct because the conclusion is pre-ordained and Congress has no need for debt to fund its spending anyway.

Would seem the simpler fix would be to just use the magic marker/eraser and take $1-3T off the books or add it to the fund. Call it national security, once in a lifetime un-expected event, stabilization of economy 3.0 whatever. The government has proved beyond a reasonable doubt they can create vast sums of money when it suits the system and players. This is like stimulus just by another name. If old folks begin to strain the system it will cause all kinds of other unexpected problems

20% kf the US is on social security.

25% of the US is underage and cannot vote

Elderly vote in greater numbers than the younger

So……approximately 35% of the voter base is on social security.

No benefit reductions. Somebody will either get taxed or defense is going to get reduced substantially.

Besides…..reducing benefits would probably create a depression. Imagine the reduction in spending.

They can’t reduce benefits unless they substantially increase interest rates. The pensioners on fixed income are going broke.

Just gut the Military Industrial Complex.

I would cut so deeply the Pentagon would become a triangle.

JFK tried that It didn’t work out so well for him though and I’m not seeing anybody in the White House that can even shine John Kennedy’s shoes frankly so don’t count on that happening anytime soon

This is instantly one of my favorite WolfStreet posts of all time. I finally feel like I have a basic understanding of SS and its troubles. Thanks, Wolf. Excellent prose.

Great article, Wolf. Many thanks for your good work!

“My patented solution is twofold: Build a nest egg while working, and work for as long as possible, either doing what you’ve been doing, or doing something new and interesting and fun. Full-time is great, but even a part-time gig is great, and for all kinds of reasons, not just money, and even if you have plenty of money and don’t need to work.”

Here’s my SS and working Record:

Started paying into SS in 1961 at age 18,

Stared collecting my SS benefit at age 66 (FRA) and still working, as the first leg of our retirement stool,

Continued to work in my small business and PAID IN TO SS at MAX until age 74,

Saved a chunk of $$ along the way for the second leg leg of our retirement stool.

The third leg of our retirement stool is my wife’s SS check as she worked all her life and retired at 66,

So we have a three legged stool of funds (no company or government pension): my SS, her SS, and a nest egg to draw from.

This result is by two kids who came from dirt poor families and made it on their own. Oh, along the way had successful children, paid off our house and have no debts.

Yesterday, I played in a veteran’s charity golf tournament and donated a nice chunk of $100’s.

I’m 78, my wife is 76, and thanks to periodic savings and SS, we are comfortable.

Could we have done this well along another route? I’m sure some posters here will think so, but looking back, I can’t visualize another path that we would have been comfortable taking.

AA

This is a nice summary / story. It also reflects how the times change. You and your wife had a strong work ethic. Right or wrong, SS was thrust upon you in the midst of your working years as a retirement “solution” but you understood it to be a supplement and continued working / saving. The world of working has changed dramatically, but so have lifestyle choices. You played the cards you were dealt and you are successful. It is a good story.

I have a feeling the Millennials and the generations thereafter will have a vastly different path, but I am confident they will also succeed in large numbers.

There’s a Country Western hit right now entitled ‘Buy Dirt.’ It is a tribute to the farmer or small rancher. Here’s some of the lyrics:

“Buy dirt

Find the one you can’t live without

Get a ring, let your knee hit the ground

Do what you love but call it work

And throw a little money in the plate at church

Send your prayers up and your roots down deep

Add a few limbs to your family tree

And watch their pencil marks

And the grass in the yard all grow up”

‘Cause the truth about it is

It all goes by real quick

You can’t buy happiness

But you can buy dirt”

Good article Wolf. I am 75 took my SS at 70 using the best assumptions at that time that I would have to live to 81 to break even vs taking full retirement at age 66 (my SS full retirement age). Assuming reasonable investment gains ~5/6% and my tax bracket ~25% do you think those numbers are reasonable? I am very healthy and active and did not need the SS at age 66. Even thinking about working part time to keep my active and social lifestyle ongoing.

Sounds great! Actually, you should be fine if you are clear of any big debts.

Just make sure you have enough to cover long term care, even if you have insurance as LTC insurance does not cover everything if you live long enough to get past the benefit provided.

This all comes to an end when the Chinese and others decide there’s no point in continuing to subsidize America’s Cargo Cult.

You mention two alternative fixes: reducing benefits and/or increasing contributions. It seems to me there is a third alternative: have Congress eliminate the regressive, anti-labor federal payroll tax entirely and fund the benefit payments via the appropriations clause directly from the federal budget.

Social Security is the most pro-labor program ever put in place. It pays out hundreds of percent more than anyone ever puts into it. I’ve never figured out the rabid complaints.

Good point. I should have said it was anti-employee, not anti-labor. Because businesses must pick up half of the payroll tax for employees, they have an incentive to convert them to 1099 gig workers, viz Uber. Also gig workers can not organize to raise their compensation, that would be illegal price fixing since they are independent businesses.

So true, Lampoon… and when the business does pay half the payroll tax for employees, it is a deduction for that business. BUT when the employee becomes “self employed” and must pay the full payroll tax (which is then called “self employment tax”). This tax is effectively doubled for the ex-employee and runs over 15% of the income. Of course, the self employed individual CANNOT deduct this tax as an expense as did his or her previous employer when he or she labored for someone else…

Sorry if someone already mentioned this, I have not read the entire comment chain. Social Security and Medicare are taxes on wages and compensation, i.e., labor has to pay for the costs of its own retirement; the earnings of capital are not similarly taxed. I.e., the regressive SS tax is part of the institution of a class structure in the U.S. favoring rentiers. The fact that almost no one ever mentions this in discussions of “reforms” to “save the system,” indicates how deeply this class structure has been internalized and accepted as “just the natural order of things.” Somehow, $ earned by investing are different from $ earned by working, and deserve special treatment.

If capital had to pay a share of the SS and Medicare taxes out of its interest, dividends and capital gains, the tax base would be vastly expanded, which means both the tax on labor could be reduced and there would be ample funds to pay retirees

SS has many flaws, but as many have pointed out, it is a safety net in a quasi-capitalist society which the poorer folks really need, whether because of their own poor life decisions or because of unforseen life changes (genetic illness / disease / accidents / injuries / casualty losses etc). Hopefully CONgress can find a way to keep it solvent and helpful to those who need it.

I had three uncles who paid into SS all their lives. They died before they collected one dime. They were single so they had no survivor benefits to pass on. Some Beaurocrat just logged on to a computer and they were deleted in a nano second, erased as though they never existed.

Medicare Part B premium jumps 14.5% for 2022. HMOG!

One important way SS benefits are continuously eroded is by having more of them (in real terms) be subject to federal income tax. That is because when Congress made them subject to income tax back in the early 80s, they set the sheltered benefits level at $25K fixed and unlike most other such thresholds, made it so that it does not get adjusted for inflation. As such, every year more and more of the benefits in real terms are subject to income tax. $25K was a lot of money back in 1983 and thus “protected” a lot of retirees. Nowadays not so much.

All this means nothing if the USA breaks apart. If Texas were to leave the union, do you think the federal government would offer them the SS funds for their citizens. And do you think Texas would agree to take on their portion of the federal debt? This is why if Texas goes, everybody goes.

The 1% wants the USA to break apart. 3 reasons.

1) there would be no entity to claw back the trillions they have acquired in the last decade or so

2) there would be no entity to pay off the USA debt.

3) social security and Medicare liabilities would disappear.

Do you really think the 1% holds assets in USA treasuries???

A corollary to this is that private pension funds, required by law to invest in USA treasuries, would nearly disappear. Retirees would indeed become the most endangered species.

And if the last 20 years is any indication, what the 1% wants, the 1% gets. What would happen to the USA dollar is of no concern to the 1%, because they will have acquired all the hard assets of any value in the country. And in other countries as well. Oh, the advantage of being first in line for printed money.

The “disease” aspect of COVID was targeted primarily at seniors. The vaxx at the general population. These folks are serious.