Maybe house-flipper Zillow saw something in its data when it decided to stop buying houses.

By Wolf Richter for WOLF STREET.

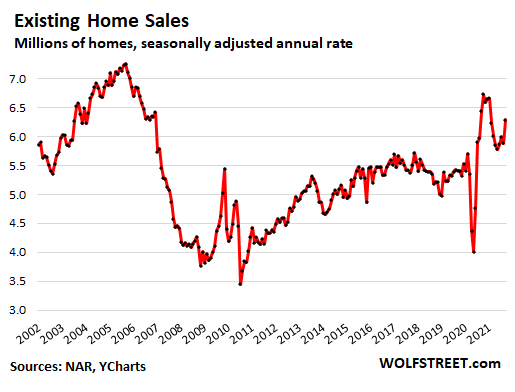

Sales of existing homes of all types – single-family houses, condos, and co-ops – were down 2.3% year-over-year in September, the second month in a row of year-over-year declines, and were down 6.5% from the peak in October last year, according to data from the National Association of Realtors today. But compared to the prior month, sales rose 7.0% to a “seasonally adjusted annual rate” of sales of 6.29 million homes (historic data in the chart via YCharts).

Year-over-year, single-family house sales fell, condo & co-op sales rose. Sales of single-family houses, at a seasonally adjusted annual rate of 5.59 million houses, were down 3.1% year-over-year, the third month in a row of year-over-year declines, and the biggest year-over-year decline since May 2020, and down 7.0% from the peak frenzy in October last year.

Condo sales, at a seasonally adjusted annual rate of 700,000 condos, were still up 4.5% from last year, but it was the smallest year-over-year gain since June 2020.

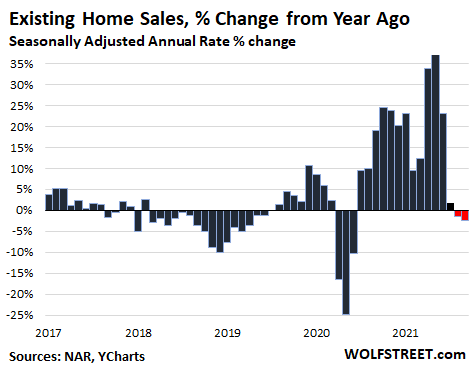

The chart below of year-over-year percentage changes in total sales shows the blistering boom in home sales last year and earlier this year, and how this boom in sales has now lost steam:

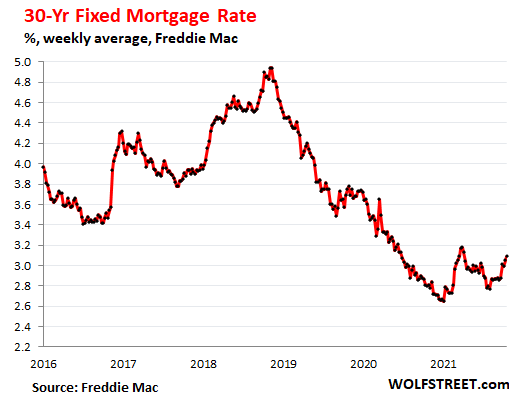

Fear of higher mortgage rates. There is a well-established phenomenon at work. According to Freddie Mac, the average 30-year fixed-rate mortgage in mid-August came with a rate of 2.87%, and at the end of September with a rate of 3.01%. In the latest reporting week, released today, the rate rose to 3.09%.

During the early phases of rising-rates, such as now, buyers try to lock in a rate before they rise even more, which leads to a rush in home sales that then turns into a decline as rates rise further. But even with this rush, sales were still down 2.3% from a year ago.

This will be particularly interesting this time around since prices have shot up so far so fast last year and earlier this year that even small increases from the record-low mortgage rates will put even more affordability pressures on the market, and sap some demand.

Seasonality returns, pandemic frenzy begins to fizzle.

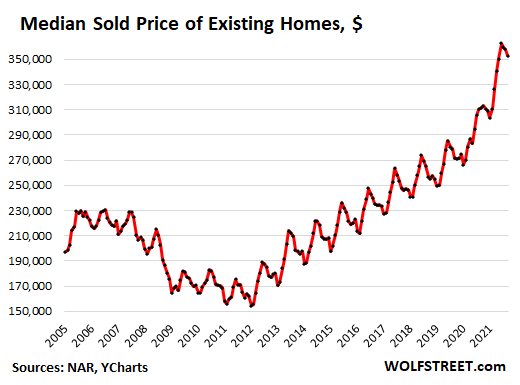

The median price fell for the third month in a row in September from August, to $352,800 for all types of existing homes combined.

Condo median price fell for the 3rd month in a row, to $297,900 down 4.2% from peak:

- Sep -2.2%

- Aug -0.5%

- Jul -1.5%

Single-family House median price fell for the 3rd month in a row, to $359,700, down 2.8% from peak:

- Sep -1.4%

- Aug -0.5%

- Jul -0.9%

Declining prices in September are not unusual. But last year, seasonally was totally upended when prices spiked no matter what, as you can see in the chart below. Reverting to seasonality is the first step back from craziness toward what is now called “normalization” or “deceleration.”

This price decline further reduced the year-over-year price gains for all homes combined to 13.3%, down from a year-over-year gain of 23.6% during peak-frenzy in May.

Maybe Zillow, when it decided to stop buying houses for its flipping business, saw something in its massive pile of data: algo-driven house flipping is a lot harder when the frenzy is gone, and when it bought many of those homes at peak prices (historic data via YCharts):

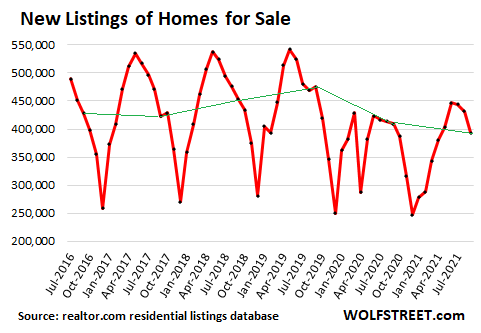

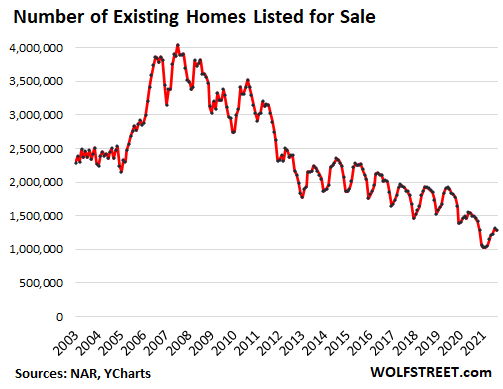

New listings normally peak in May and then drop off through December or January, after which they begin to rise again. The pandemic has totally upended any seasonality last year. This year, new listings rose from very low levels in December through June, flattened in July, and started dropping in August and September. The green line indicates the movements between Septembers (data via realtor.com residential listings database):

Supply of unsold homes on the market dipped to 2.4 months, and homes for sale dipped to 1.27 million homes (seasonally adjusted), as inventory for sale remains low, but has come up some this year (historic data via YCharts):

The share of all-cash sales rose to 23% of total sales in September, but roughly in the same range as during the summer. Cash buyers include institutional investors that can borrow at the institutional level, plus individual investors and second home buyers that have the cash, or can temporarily borrow against their portfolio and get a mortgage later.

The share of sales to individual investors and second-home buyers dipped to 13% in September, from 15% in August.

Mortgage rates rose as the 10-year Treasury yield jumped. The Fed has now made clear that it will taper its asset purchases after the FOMC meeting in November, and end QE entirely by mid-2022. There are already Fed governors that are considering to speed up the pace of tapering to make room for sooner rate hikes.

The $120 billion a month in QE, which includes $40 billion a month in mortgage-backed securities, was designed to repress long-term interest rates, including mortgage rates, in a massive manipulation of the credit markets. And the end of QE, with the single biggest relentless and predictable buyer gone, will give credit markets a bit more leeway to respond to surging inflation with higher yields.

The 10-year Treasury yield has surged by over 60 basis points since early August, to 1.67% at the moment. Mortgage rates, which generally lag Treasury yields, have risen 32 basis points since early August, to 3.09%, according to Freddie Mac’s data released today. But as you can see, mortgage rates remain extremely low, with a lot of room left to rise, and the Fed hasn’t started the rate-hike cycle yet:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

oof

from what I’m seeing after 1200 mile trip to colo, new mex, ariz

I’m seeing lots of SPEC buying in vacay area’s

many are doing airbnb, vrbo, etc.

doesn’t seem to be care about making any $$ just 1% buying to put money in physical asset

and of course TO MANY FOREIGNERS from commiefornia who don’t even bother about price

one homeowner had commiefornian come knock on door and person said

we WANT YOUR HOUSE – name price – he did and now has to move

few months back in Tucson, realtor representing GOOGLE exec bought site unseen tri-plex for over market price

again – had some $50,000,000 to spend and was just buying everything

maybe if we can crash stock market – reality will sink back in

but by then the everything inflation prices are going to hit 90% very hard

right now diesel jumped $.50 cents TODAY to $4

yah, guess I NEED TO RAISE RENTS AND PRICES ALSO 30%

Commie? What is this 1950?

Tucker Carlson….is that you?

It’s still amazing to me why some people choose to humiliate themselves like this on the internet.

It’s like when these buffoons called Obama a “Socialist”. A real Socialist would laugh hysterically at that since Obama was basically a Republican.

It shows you the childish slang some people like to toss around. They don’t know what the words mean.

They can’t explain their real criticism of the person or policy so they just parrot some garbage they heard on the Rupert Murdoch Propaganda channel’s professional liars or ridiculous clowns like Alex Jones.

Perhaps growing up and thinking for yourself is in order instead of flying your Q flag and running around calling everybody a “commie”. Have a just a tiny little bit of self-respect. Please.

WOLF

A couple typos:

1)

Fear of higher mortgage rates. There is a well-established phenomenon at work. According to Freddie Mac, the average 30-year fixed-rate mortgage in mid-August came with a rate of 2.87%, and at the end of September with a rate of **30.01%**. In the latest reporting week, released today, the rate rose to 3.09%.

I think you meant 3.01% ??

2)

Mortgage rates rose as the 10-year Treasury yield jumped. The Fed has now made clear that it will taper its asset purchases after the FOMC meeting in November, and end QE entirely by **mid-2020**

I think you meant mid-2022 ??

Yes, thanks.

And MBS purchases are $40 billion, not million.

Long night, LOL?

I come here for comments honestly :-)

It gets worse. I initially made the edits and saved them to the server. And maybe 30 minutes later, in another tab where the same article had been open with the old version (dozens of open tabs, I lost track), I made another unrelated edit, and saved the article to my server, which then superseded the prior saved article with the prior corrections. And the 30.01% and million and the 2020 were back!!!

But I didn’t notice it until I got ragged about the same stuff again, and when I looked at it, there they were, in all their beauty, and I had another WTF moment.

In the good ol’ typewriter days, we didn’t have those problems ;-]

For the Wolf:

My first office job was typing specifications for an architect, because his ”secretary” was his girlfriend and didn’t know how to type, and really didn’t need to do anything at all in the office, etc.

Pay was $1 per standard (8.5×11) page, but with no errors and no corrections!

Had the ”pleasure” of retyping hundreds of pages.

MUCH better when we got word processors, not to mention all the additional technology these days.

Certainly would not want to go back to that old typewriter, though it was electric, so much better than the ”standard” we learned on at school at the time, early ’50s.

This site is much more well written and edited than almost all the others I am reading these days, some of them truly shameful.

I haven’t noticed any wrong within you write.

Perhaps aside from a missing /s tag here and there.

Typos are typos less today electronically then with my 1927 black ribbon machine used perfectly while at anchor meandering certain thoughts to type.

guess I’d have to NOT SPEED READ and skip things

10 year yield jumps to what 1.66% – woo hoo

I am a bit depressed – getting paid off on loan(just 12% interest)

I’ll miss my 1% month income on note

but if flipper can find another – I’m ready to fund again at 12%

I always am willing to own the property as I’m in 1st position

and with rents exploding – I hope some days

When it becomes harder for people to qualify with the higher rates they buy less home, so that’s why the median price goes down not because that same size home was down 3 months in a row it’s because they’re buying less home each month

The median price is not going down. A few months showing yoy decreases is meaningless noise. The trend is higher forever.

With mortgage rates hitting an unimaginable height of 3.09% (yes that is what Mr Wolf said – the Fed is now charging over 3% interest for mortgages – outrageous!!!!!!!!!!!!!!!!!) the chicken littles are out talking about price drops – never gonna happen.

Cheapskates that want to buy more houses are just going to have to cough up ever more dollars (Fed tokens), it’s not like money is difficult to come by these days (read Mr Wolf’s last article regarding sky high increases in incomes).

Just get off the fence and buy some more houses. The monetary politburo (the Fed) and the government will continue their policy of dollar devaluation.

Borrow money to buy anything today and you will be glad you did in the future when the dollar is in history’s dust bin. The price of everything becomes meaningless when the currency used as a gauge is falling like a stone down a well.

silly comment. incomes have not come close to increased enough to pay for the housing price increases. also you’re making a mistake in thinking people will get to keep their assets bought if the currency collapses.

There is no imminent USD collapse. The post to which you replied is nonsensical, believing the asset mania is a one-way street forever.

i didn’t say that the collapse was imminent. what i meant is that if it does collapse and is replaced with another currency, there will be social unrest like no one has ever seen before, and wealth, including houses, will be forcibly redistributed.

Nothing like an article on real estate would attracts real estate agents from all over. Then under pseudonames, they will start advertising their usual FOMO. Don’t pay attention to the noise.

Fed has screwed up with 20 years of short term solutions and now is in trouble. It’s hard to know what decision they will make.

1. Kill inflation down to 2%.

2. Let inflation run and try to get more people into labor force.

It want to take much of an interest rate hike to start recession. Maybe 1% it f they can even get through taper.

An good old fashioned recession wouldn’t be such a bad thing. The alternatives could be a lot worse.

Well, you might be right that the Biden gang will keep handing out free money and the bubble will just continue.

But the blow off tops in Bitcoin and Tesla sure look like a good time to take a short position. Tesla with a market cap of $906 Billion and $42 Billion in sales has insane competition looming, the electric F150 is sure to hurt Cybertruck. VW, China, Cadillac; everybody is coming which is sure to cut everyone’s margins. The only way out for current Tesla stockholders is to find a greater fool.

Market historian Jeremy Grantham knows no one has a crystal ball as to when the stock market crash will happen, but the odds have shifted to an asset crash.

MLH is correct (do you really think they will ever even attempt to deflate the bubbles?). If you look at our monetary policy as a game, then MLH is showing you how to play game. This is what all the newly wealthy from feds goosing are doing.

Make funny money on stocks/bitcoin , convert to tangible goods.

The more pronounced the trend becomes the more dystopian our future appears

Except, in an inflationary environment, home prices continue to rise even as mortgage rates rise. That was the lesson from the 1970s they teach in college econ classes. That is the beauty of inflation.

The wage inflation in this instance is doing more for renters than home buyers. The demographics then supported young people starting families. They went to work in construction and bought homes with the money they made. It was almost that virtuous cycle Henry Ford had in mind. Home buyers who had locked in 3% mortgages when rates blew off were sitting pretty. But, those wage gains,and pensions based on them, were eaten up during the decades after that, health care costs especially, and most of them came to their end hat in hand.

There are two big differences between now and the 1970’s. The first is that as a whole the population was much less indebted than they are now. Most people did not have a credit card and mortgages payments as a percent of income were much lower. This put headroom in place for people to pay more for a home regardless of income. The second thing is that a much greater portion of people had incomes that were being adjusted up right along with inflation like union jobs. Though we have some wage increases now they are not really widely spread throughout the economy like in the 1970’s. We also have a much higher portion of the population that are on some kind of fixed or investment based income now. Inflation is not boosting the home buying income of those living off savings, pensions, annuities etc. So there might have been a bit of a blip from meme stocks, crypto etc., we are settling in for a long cold winter were most peoples income to spend on housing will be on the way down after expenses. That will reduce mortgage payment amounts. Higher energy prices will also hit hard and crush home prices in the exurbs and outer suburbs now that the WFH wave has crested.

He is incapable of seeing the differences. Or given his posting history, doesn’t want to because the outcome is contrary to his personal preference.

Given the prices versus incomes, believing residential real; estate will be minimally or not affected from much higher higher mortgage rates is ridiculous.

People who are invested in real estate tend to think that real estate can never go down.

We all are biased in many ways. It’s difficult to have an objective/unbiased thinking process when you are personally invested.

Under inflation, incomes rise, as they are now and you have to include that in your prices vs income analysis. Rents are also rising fast which draws yield buyers.

It really is that simple. The average homebuyer cannot afford the average house and it is going to get worse when rates go up.

Eventually, this housing rally will end and prices will fall back. In my opinion, this rally continues for at least one year, but with much lower price growth.

After that, it could go either way based on the 2022 midterm results as well as future FED appointees.

> Inflation is not boosting the home buying income of those living off savings, pensions, annuities etc.

Those sound like retired people, they sell homes.

The young are the homebuying population.

I wonder what would happen to housing market when and if the mortgage rates are 5-7% instead of 3% today.

I doubt we would see this high rates as FED sees no meaningful inflation.

jon

The last time we had inflation anywhere near this level was 1999 and 2006

30yr was 6%

so that is how abnormal the Fed has made this world we live in

Like someone said the other day, house builders are going to try to build at a price people can buy even if they have to build it smaller, on a smaller lot and use cheaper materials.

History means nothing economics 101 went out the window forever since Bernanke was in power. Anything that makes sense is usually a losing position as the central bankers take the opposite sides of the trade and push everyone into a losing position with all their money. The bankers have the playbook and usually take what would seem like the wrong trade but with all their money they push out everyone on the other side of the trade. So the wrong trade makes all the money. That’s how the bankers work things today. Go go by history or you’ll end up broke.

T:

I really thing you meant, do NOT go by her or his story or you will go broke…

While many of us older than boomers would really and truly prefer to have this situation and the inevitable crash following sooner and later FOLLOW ”history” the facts so far seem to imply that we are in a literal ”wonder land” of intervention, invention, and the clearly happening ”invections/lies/lies, and statistical fornications” that have almost nothing to do with reality on the dirt.

In spite of all of that, some of us older folks keep hoping and praying that, sooner and later, we will be able to get at least SOME decent income from our savings, etc., etc.

Also, QE ending mid 2020? There are so many crazy financial events to keep track of, I can’t blame Wolf for being distracted.

The potential buyers are too busy buying Bitcoin!!!

Or like SocalJim, they finally came to realize that this country is corrupt!!! And the corruption started only last year!!!

ROFL.

Zillow’s cites unit and labor shortages as the reason for pausing their home purchase program. That just does not sound convincing. If prices are going up anyways, why not just mop up anything and everything now?

they’re basically saying that they don’t think the unit and labor shortages will fix themselves in time for them to get out before the housing market crashes.

Busy buying bitcoin – using one type of worthless tokens to buy a different type of worthless tokens.

Humans are just the dog in the middle of the room chasing his own tail, it seems important to the dog while he’s doing it, but it’s really not.

Who even knows anymore. Goldman Sachs says housing appreciation of what? 16 percent through next year? How? God only knows.

Shortages in everything? Labor shortages? Empty shelves? Companies bring forced to raise wages constantly? Bad inflation? All that means is wall street setting all time records every day! How? God only knows.

I’m still sitting on the sidelines watching. Of course all the people with a vested interest say nothing bad is ever going to happen. NAR says home prices can only go up. As per usual.

I think I smell smoke in the breeze.

A watched market never boils over.

It’s usually due to the condos taking a larger share of the sales. They have a lower average price.

Also, 2020’s Spring home buying season occurred in the Fall due to the lockdowns.

Les,

Condo median price fell for the 3rd month in a row, to $297,900 down 4.2% from peak:

Sep -2.2%

Aug -0.5%

Jul -1.5%

Single-family House median price fell for the 3rd month in a row, to $359,700, down 2.8% from peak:

Sep -1.4%

Aug -0.5%

Jul -0.9%

That is because families tend to buy more expensive homes and most of those family sales happen such that the home is closed in mid summer. Nothing to see here.

A) what advantage do those institutional investors have over retail mortgage buyers?

B) Zillow got out of the market when the supply of houses which suited their purposes dried up. Maybe they’ll get into new construction.

C) If you want to understand home prices (and stonks?) you just need to look at a chart of Bitcoin. A sound money regime would label this counterfeit and prosecute the cretins. However it suits their purposes (nicely). The problem arises when you add the size of the monetary base, to the float of Bitcoin you have the most hyper of all inflations. Natural thing is to unload their bogus profits and buy real assets. Anyone who sells a house right here, is a damned fool.

The only houses for sale are mostly junk right now.

I would attribute the decline in sales to lack of product entirely.

Here in SoCal if smth decent comes up, its gone within days with bidding wars.

Case in point, a house I saw last week came for sale at 1.6m.

It went immediately pending on zillow.

I saw today on zillow that it sold for 2.37m.

House was in a good location but still a 1970 construction that needed a lot of work, full renovation.

The amount of money out there is insane.

With the materials inflating…the house price inflates.

And people in an inflation want to hold on to their largest hard asset.

The Fed has everything effed up…. but they dont seem to notice.

they notice. they just don’t care.

Ambrose…

indeed.

What is Bitcoin worth if the Fed Funds were at historical norms….ie even with inflation?

Who would hold Bitcoin if you could get a fair return on your money.

I often wonder if any Fed Governors own Bitcoin.

But as long as people can get 30 yr mortgages well below inflation, housing will hold in there.

The question is “Why are 30 yr mortgages at his level, and why is the Fed supporting the mortgage industry and suppressing rates with record housing prices?”

Last time inflation was near this level, 1999 and 2006, 30 yr was 6%….now 3% …why?

Fed has got everyone trained that the way to wealth is to leverage up and go for it. Fed’s out of ammo. Who is going to save everyone the next time there is an economic shock?

Many people invested in Bitcoin made huge amounts of money when they sold Jim Cramer brags about it on CNBC

Global sovereign debt bubble is bursting for the first time in 100 years IMO.

There’s a reason why the BTC chart looks like the gold chart in Weimar papiermarks.

I contacted Zillow about selling my house just to see how it worked. After a week they called and said that since I live in a gated community my house isn’t eligible for their program.

I cussed them out for discriminating against me just because I’m in prison. :-)

Too funny

As everyone knows a Canadian mortgage rate is set for a certain term usually 1 to 5 years, rarely more but 7 can be had. Having had many and done some weird renewals. you don’t reapply or requalify, you just pick a term and type, open, closed. variable. Lately of course, they’ve been going down.

I don’t get how a bank can offer 3 % fixed for 30 years. With inflation well over 3% it looks like a death wish. Is this all govt guaranteed or are banks on the hook?

no bank is holding this stuff on its own books. it’s immediately being sold to fannie or freddie and then packaged into mortgage backed securities, which the fed is buying.

Fannie Mae is worth a whole 85 cents a share now, it’s nice to see there is deflation in some things.

It was 20 cents in ca 2009, when I bought some of it (I sold it years ago). So there is still 300% inflation.

“I don’t get how a bank can offer 3 % fixed for 30 years.”

The government buys and guarantees most of those mortgages. The banks and shadow banks (largest mortgage lender is Quicken Loans) that originate them get the fees.

Institutional arrangements reflect policy support of home ownership in the US that is different from Canada (mortgage deductibility, 30 year mortgage guarantees via govt agency as described by Wolf, etc)

Brother took out pledged asset line of credit to pull the trigger on a home purchase. He said he was given a credit line of 70% of pledged securities, mostly stock and bond mutual funds, and 96% of cash.. What may we infer from that?

The three charts in this article tell me there’s very little chance of a housing crash … or even a substantial pullback.

1. Housing prices are steadily INCREASING.

2. Inventory of homes for sale is steadily DECREASING.

3. Interest rates are at 40 year lows.

… AND wages & incomes are just now starting to take off.

It’s going to take years to turn this ship around, especially with builders building way fewer homes & condos than markets need. Until they overbuild rentals (much more likely) and the cost to rent drops substantially below the cost to own, folks will continue to buy, buy, buy.

BTW, for whatever reason, Zillow announced they have resumed their I-Buying program just one day after ending it.

You unlock this door with the key of imagination and a rather unlimited amount of QE money. Beyond it is another dimension: a dimension of rentals, a dimension of profit, a dimension of turnover. You’re moving into a land of both shadow and substance, of houses and values; you’ve just crossed over into the Zillow Zone.

Xavier…

good one!

Most Americans are dependent upon a substantially fake economy for their job and income. Same for much of their “wealth”.

The economy is built on sand. It doesn’t take much for it to deteriorate substantially, since it’s based upon unfounded manic financial optimism.

inventory of homes is low not because of population pressures, but because of people buying houses purely for investment, and i don’t mean as income properties. that never leads to sustainable growth.

wages and incomes are not taking off in the group that buys houses. it’s taking off in the low wages, so the $11 hour people are now making $15. they’re not buying houses at either wage.

Aptly said. Wage increase happening at the lower end of the spectrum.

Last time inflation was in this neighborhood, 30yr mortgages were 6%.

The Fed is holding the beach ball under water…..

Inflation does make the federal debt worth less, somehow. That seems to be the dreary conclusion that cowards posing as leaders will hand off to us.

Also, houses are tied up because if you were 75 or 80 would you want to go into an independent/assisted living situation and risk getting covid? In 10 years we will have a housing glut and no one to buy them.

And when people can’t afford vacation either—all those fancy vrbos—there will be another glut in previously desirable areas. The masses will have only worthless dollars to spend (see above).

@LM: you said…….”Also, houses are tied up because if you were 75 or 80 would you want to go into an independent/assisted living situation and risk getting covid?”

I’m 78 and living in my 2,000 square foot home. I don’t want to go to any assisted living facility because they are full of cranky old people.

My Uncle is ex marine 97 years young and lives by himself. Still drives and swims at the Y.

NO SUCH THING AS AN “”EX”” Marine OS!!

Once a Marine — after passing boot camp — ALWAYS A MARINE<<<

And may the Great Spirits of the WORLD, continue to bless them every one…

Thank you,

Curious what your uncle did in WW2? Not many of those USMC veterans still around.. My Basic School class is having a reunion in SF soon and will be having a ceremony for one of the very few 1st MarDiv WW 2 vets left.

Where I live in Vancouver Island it is somewhat opposite to the article. Available houses for sale are down 51% from last year, BUT prices are still rising due to this constraint. This seems logical as people still want to move here. Why? Fires in the interior, decent winters here, and all of the recreation opportunities. Universities, colleges, etc etc etc.

Direct quote: According to the British Columbia Real Estate Association, sales are returning to normal, while supply is hitting record lows.

One small example. My son bought a second home that closed on Jan 1. He renovated the downstairs and installed a suite for himself in the basement where he stays on his 2 weeks off per month. Last week his RE agent phoned to see if he wanted to sell? In the 9 months since his purchase the value has increased to 800K without any of the renovations, whatsoever. I would imagine the new suite adds another 100K. A 33% rise in value in 9 months is a pretty darn good return on investment. This is his home and he doesn’t plan to sell, but meanwhile the upstairs renters (2 single ladies in their 50s) are paying for most of the mortgage even though he discounted the rent because they are such great tenants.

On mid Island houses are selling as fast as they can build them. Apartments are rented out before they’re finished. And here is a quirk, the empty property that I used to cut Christmas trees on every year with my kids now has a full shopping plaza, theatre complex, and a 14 story apartment under construction. The place is booming. That is the reason I moved out 20 years ago. This housing boom has been going on for almost 40 years on the mid Island and the low interest rates acted like gasoline on a fire.

Somewhere I just read that average US wages from September 2020 to September 2021 actually fell for most workers. Things might be slowing down.

I don’t see that, in data or reality.

WES,

“…average US wages from September 2020 to September 2021 actually fell…”

That’s probably not a correct data point by itself. But the average wage figure you might have read about might have risen less fast than inflation, so that the “real wages” might have declined, and that is the case, because wages were rising slowly last year and earlier this year. They’re now surging, but inflation is surging too.

The expansion (or contraction) of the production of marketable goods and services under capitalism is mainly determined by the extent to which the executives of large corporations and Wall Street financiers invest profits in new productive facilities, especially those embodying more advanced (labor-saving) technologies. What drives capitalist investment is not the impulse to maximize output or labor productivity but rather to maximize the rate of profit (i.e., the ratio of profit to the market value of the means of production).

However, Marx, in one of his key insights, demonstrated that there is an inherent tendency for the rate of profit, the driving force of the capitalist system, to decline over time. By prompting capitalists to cut back their investments, a falling rate of profit generates periodic crises, usually triggered in financial markets. The result is a contraction of output and increased unemployment.

Marx’s explanation for the falling tendency of the rate of profit flowed from his understanding that surplus value—the unpaid portion of workers’ labor—is the source of profit, not the capitalists’ expenditures on the means of production (e.g., machinery and raw materials). Marx observed that especially in periods of economic boom, when workers can feel emboldened to demand higher wages, individual capitalists invest an increased amount of capital in plant upgrades and such in order to cut labor costs. By doing so, the capitalist gains a competitive advantage. However, as all capitalists follow suit, the total amount of surplus value generated per amount of capital invested—i.e., the average profit rate—declines.

Capitalists invest in expanding productive capacity on the assumption that they will be able to sell the goods produced at a particular rate of profit. However, as the profit rate drops, they find themselves unable to sell their products at the expected profit rate. They cut back investments and slash production, resulting in an economic downturn. Workers are thrown out onto the street; entire factories become rusted relics.

Bourgeois economic ideologues, from Keynesians to monetarists and supply-siders, identify the laws governing the capitalist mode of production with the laws governing production as such. Both liberals, like Krugman and Gordon, as well as centrists on the bourgeois political spectrum, like Summers and Levinson, insist that it is not possible to overcome the decades-long stagnation in the living standards of American working people.

Mr. Scott,

Karl Marx was married to the Baroness Johanna von Westphalen. So I guess your solution to our current financial problems is for each of us to marry either a rich Baroness or Baron.

I don’t believe that union brought Marx much economic security, Greg, since he had to rely on support from his rich buddy Engels for much of his life, Greg.

So rich friend rather than lower aristocratic orders.

Marx had a very early look at the various and sundry ”systems” of production, and came to some conclusions based on clearly ”insufficient information.”

While I do not denigrate those conclusions, in fact they were wrong then, and are wrong now…

What was not part of his conclusions then, and mostly not now if one listens to the apologists is that the corruptions of the systems then and now were not included…

IMHO, having been involved with very clear ”off the books” housing and work, etc., etc., is that these days,

NOBODY knows what is actually happening in the ”real” markets of labor availability, productivity from that labor, especially the black market labor, etc., etc.

Wolf does a really amazing job of presenting the ”official” picture of labor and productivity and so on and so forth, but his picture is based upon the official statistics, as it should be,,,

while to my clear understanding working with SO many folks who bought their tickets just below the border for $500 or so, that no matter what the official reports, most if not all of the real workers are not on any books anywhere or any when, not here, and especially not now.

Marx missed imagining Central Banks.

And he especially missed out Central Banks in Marxist countries.

“From each according to his* Central Bank, to each according to his* needs.”

* freely exchange with it’s or any other possessive you wish.

Might be the last year anyone bothers to carve a jack-o-lantern. Lots of people might be supplementing their dietary intake next year with a slice of good ‘ol pumpkin pie kicked out of the stupermarket factories. Now excuse me while I go celebrate Numerica with a triplet of burrit-dogs and a home brew that can kick a mule across the little-Riata.

Deja vu all over again. The behavior of people is virtually identical to what it was in the previous housing bubble. The underlying mechanics are different, but the psychology is identical. Even a small rise in mortgage rates will crush the market. But even if that doesn’t happen, the market will eventually collapse under the weight of its stupidity. A mosquito that has had lobotomy could figure this out.

SoCalJohn, are you the bizarro version of SoCalJim? I do like what you’re saying and do agree with you but we aren’t the one that are right so far and that hot hand fallacy mindset runs rampant in this cycle…

NOPE. In 2007, you had the media carrying water for the Dems in the middle of campaign season. They spread the housing bubble propaganda 24/7 and created a housing panic … just to help the Dems in November 2008.

The dumb money walked away from their homes and rented just to watch prices snap back. It will take generations for this mistake to be repeated.

SocalJim,

Sure enough, there’s always someone who makes their money in real estate who says that Democrats caused home prices to tank during the housing bust, hahahahaha. This stuff is funny every time I hear it, and I’ve been hearing it for years.

No, but you can blame Democrats for pumping up home prices afterwards by getting PE firms to buy hundreds of thousands of houses out of foreclosure… that was a Bernanke deal, fully supported by the Obama administration, and this caused home prices to soar and created some of the biggest and most avaricious landlords out there, and helped create to this day some of the big distortions we’re seeing.

Investment firms recognized we were in the midst of a media generated housing panic and they saw real value, so they bought them up. And they were right. The Dems had little to do with that.

The Fed specifically developed a program of cheap money for PE firms to fund their house purchases and discussed it publicly too. It was one of the ways the Fed bailed out the banks. The While House was totally behind it. This is all well-known by now — though perhaps already forgotten.

I know about the cheap financing. However, investment managers will not do a bad deal just because the financing is cheap.

I still don’t understand the whole 2nd home speculation and shadow inventory deal. I wonder just what percentage of homes are second or third non-rented speculation assets. The carrying costs on even a vacant home are pretty high. Not to mention it is a physical asset subject to the issues of it being an item and not just some numerical value in a computer somewhere like stocks and bonds.

And don’t get me started on the alleged 2nd home rentals or the BnB rental craze. I know the overwhelming vast majority of people aren’t cut out to be landlords.

I’m wondering what the real statistics on this narrative are. We have had almost a million (mostly old homeowners) kick the bucket in the past year but suddenly there is a massive drought of homes because people fled city apartments, yet supply will never catch up and this blip… Ahem astronomical rise in prices won’t abide yet will only go up, up, up? Mortgage rates are increasing but up is the only place the market can go? Supposedly rents can only go up as well and are steadily increasing outside of a handful of metro areas? I hope there actually is millions of homes in shadow inventory out there and the second the pendulum starts it retrograde descent the bottom falls all.

Guess that is what they call inflationary mindset. Doesn’t matter what anything costs, FOMO rules the day and we just pay anything blindly.

There had never been a point in US history where something catastrophic has happened and everything turned out peachy afterwards before. Why is it suddenly all different this time? I seriously doubt we’ve entered a new paradigm out of the pandemic. And if we have, it’s one that by all metrics will financially slaughter the young kids coming up now. Either it will burst like it has every single time since the inception of biological life or we will have a new age that pisses off the next generation enough to pop the bubble themselves.

I don’t believe anything other than the statistics. And statistics show 99.9999% of the time: Ebbs and flows rule the day in life.

I try to do the numbers on different investments.

It seems if you are in a thriving area that people who owned a second or third SFH and rented them out to good tenants made out really well the last decade With depreciation and low interest rates making it easy to carry the property, appreciation with say 4:1 leverage made a nice return.

Trucker…

VRBO changed everything…

People are leaping out of dollars into anything that can give them a fair return….

Buy a home, rent it out.

Why is it different this time?

Why does the Fed have interest rates 5% below the current inflation rate?

Why does the Fed buy MBSs (lend money) at 3% below the current inflation rate?

Why does the Fed promote any inflation?

Why does the Fed buy 120,000 MILLION (120 billion) of federal debt each month?

I think you see where I’m going and to whom I am point the finger for the upside down financial environment we are in.

In australia right now your home earns more in unrealised capital appreciation than you do. Almost without exception.

In nice areas (not the best areas) your home earns more than a surgeon.

In the best areas you house increases at the annual rate of a regular workers entire life time of savings.

No bubble here tho.

Straya’s different mate.

You’ve this tiny sliver on the coast that is densely urbanized and populated and the entirety of the remaining country is uninhabitable misery with a few trailer parks dotted about.

Any reasonably livable area in Australia has been built up. Much the same with western Europe which is why most of it is rental deals. The US and to a similar degree, Canada still have millions upon millions of habitable acreage to build on. There is no shortage of livable space in the US. We can expand like China. No reason for SFH to be an issue or scarcity. Especially with coming an infrastructure revolution with self driving vehicles.

people forget that. even in america’s densest cities, you can drive 50 miles outside and be in the middle of nowhere. people pack themselves in like sardines mainly because they like to.

Especially the western cities that are still young. East end of Denver and it’s suburbs is literally a wall. You have subdivisions you can’t drive a car between the houses and then literally nothing until you hit Lincoln/Omaha. 500 miles away…

The development just stops. Same with places like Vegas, Phoenix, Abq, etc.

Even the east coast still has a lot of breathing room to expand.

I don’t agree that any reasonable land in autstralia has been built up. Just few miles away from coast you have swath of open land, can be leveraged with either good public transportation and or self driving car ….

No one wants to sell their largest hard asset in a runaway inflation.