Seems, inflation prospects jangled some nerves today.

By Wolf Richter for WOLF STREET.

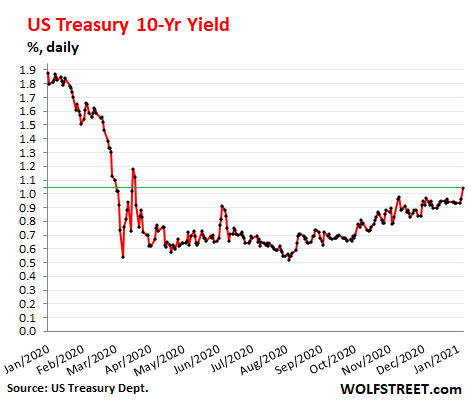

The 10-year Treasury yield jumped 8 basis points today and settled at 1.04%, the highest since the wild panic days in mid-March 2020. As the yield rises, the price of that bond falls. This yield has now exactly doubled from the historic low of 0.52% on August 4, when folks were still betting that the 10-year Treasury yield drop below zero:

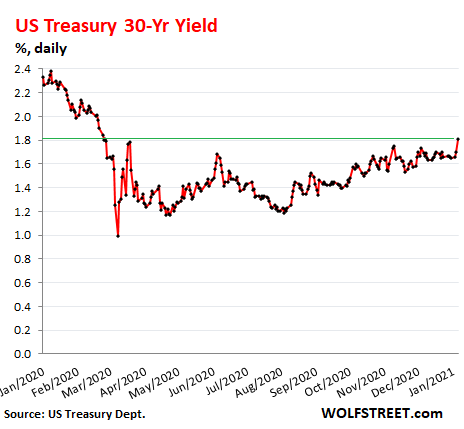

The 30-year yield jumped 11 basis points today to 1.81%, the highest since February 26. On March 3, as all heck was breaking loose, the yield had briefly plunged below 1% for the first time ever, and days later it was back at nearly 1.8%, in some wild and volatile panic trading. But this time, the upward trend started on August 4 and has been systematic:

Might the bond market be smelling a rat?

Yes, inflation. The bond market is smelling it. Everyone is smelling it. The Fed is touting its new philosophy of letting inflation run hot for a while – whatever “hot” and “for a while” might mean. The Fed’s inflation measure is “core PCE,” which nearly always runs below “core CPI” which always runs below whatever inflation people are actually experiencing in real life.

The prospects of inflation are further heightened by the possibility of additional big-fat stimulus packages, on top of the big-fat stimulus packages that Congress already passed in 2020. In addition to possibly firing up inflation as this money gets spent — and we have already seen some of this in real life — these stimulus packages need to be funded by debt issuance, putting more upward pressure on yields.

Chicago Fed President Charles Evans, a voting member this year on the FOMC, explained yesterday at a virtual meeting that “frankly if we got 3% inflation that would not be so bad” as long as it is not accelerating uncontrollably.

So, 3% as measured by core PCE. Something like 3.5% to 4%, as measured by core CPI. That would be a hefty dose of inflation for those who bought 10-year securities at a yield of 0.6% in the summer, or even those who bought them at a yield of 1.04% today, or worse, those who bought longer-dated Treasuries, looking at the next two decades.

Inflation destroys the purchasing power of bonds. The yield is supposed to compensate for that risk. But in this scenario, with current Treasury yields, it’s not even close.

And mortgage rates got nervous over the past couple of days. For example, the average jumbo fixed-rate 30-year mortgage rate jumped by 13 basis points today, from near record lows, to 3.25%, according to Mortgage News Daily. Maybe just a blip, but it shows some nerves got jangled.

But clearly, bond markets are only getting a teeny-weeny bit nervous because yields are still extremely low. Left up to its own devices, the Treasury market with these Fed-inspired visions of inflation, might react more strongly. But the Fed is still buying Treasuries and mortgage-backed securities, and that is keeping a lid on the upward moves. And holders of those securities at those yields will just have to eat the inflation.

Weirdest Economy Ever, as 20 million people still claim unemployment benefits. Read... How Will This Unwind? Amid Stimulus, Forbearance, Eviction Bans, Consumer Bankruptcies Dropped to Lowest in Decades. Commercial Chapter 11 Bankruptcies Highest in Years

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I smell and taste inflation whenever I put a piece of Cheetos into my mouth. My McCheetosh index is never wrong.

Mini bags of Cheetosh went up 50% last year, I am scared to think about the consequences of Cheetosh hyperinflation.

A sirloin steak was up 25% today in UK

I get your point. Fed core PCE is so divorced from the world most of us peasant folk live I’m scared I might need to see 30% inflation in my world before the Fed sees 3%.

NO NO NO NO NO

can’t have that – 10 year at 1.00%

really – no one wants devaluing(quickly) merican bond/treasury

say it ain’t so

well guess what I’m all in – on gold

Gold got whacked. It’s too important an indicator to let it go up.

The way the system is set up, gold will not rise until the system breaks and all people will want then is food.

PCE allows for items that rise too much in cost to me rotated out.

Tell me that is not a low measure bias.

So, we will start hearing..

“Hamburger Helper? Heck, its good all by itself”

I eat a lot of organic beans. What’s the rotation for that… sawdust?

“PCE allows for items that rise too much in cost to me rotated out.”

DC’s measure of inflation is always ex-inflation…just as its measure of unemployment is ex-unemployment.

Basically DC’s entire philosophy of life is to piss down your leg and tell you it is raining.

The MSM’s role is to give it a shake.

(Not your leg).

I’ve heard that using insects as food or filler has been tried, even if it is not mainstream yet.

Since insects are abundantly available and easy to raise they could be the next hamburger helper or meat extender to cut your grocery costs (if attractively presented and flavored).

Who has not salivated at the thought of savoring a delicacy such as roasted grasshopper?

Since it appears food costs are ready for big, permanent increases this could be the next big thing.

As far as I know some lignin in your cellulose is still good fiber, and not harmful. But I don’t think there’s anything in your gut that can digest it.

Maybe use a termite derived probiotic?

I’m don’t think I’ll I’m going to ever rotate out of my peanut butter….90% peanuts by law and they sure fought that law. Unchanged as far as I know.

Just stay away from “peanut spreads”, they can do what they want with those.

Here in Oz, live beef prices are at $8 dollars a kilo, predicted to go to $10 before the end of the year. We have the highest priced beef in the world.

Oops, forgot to say thats live price, on the hoof.

Quit eating beef be a vegetarian! He he!

Eat bugs like the ISB and WEF recommend.

Actually grasshoppers are OK if stir fried properly. I always wondered what the locust plagued farmers were complaining about. Just eat the buggers.

I got tricked over some canned silkworm cocoons once though – I was told they were nuts. Horrible things.

Joe-

Lobster and crab are just big bugs…all good protein.

Wish I could find out if silverfish had good protein. They are damned easy and cheap to raise.

I know, I raise them on 500 sq ft with zero effort. Have found they like small 3×5 notebook paper best. Know they are into glue, too, so my books are all in sealed plastic boxes. So far it’s just good coordination practice squishing them, fast and tricky little critters.

Cattle rustling is a young man’s game, but if I was younger at $10 a kilo it would be a consideration. Yeeeeee-haaaaaaw!

Don’t laugh, rustling is still a thing!

Yeah, but they don’t post Help Wanted signs so it won’t put a dent in the employment problems.

Alright, time to put money into PEP. Cheetos going up 50% means PEP is making more profits.

And one more thing, bring back my SALT deductions.

Dear Monkey,

The best way to prove inflation is with your phone…just take a few photos of staple goods and their prices(that are clearly on display) at the same supermarket every few months and then look back…. It might just scare you, (who knows?) but they will make great facebook entries lol

Like Wolf, my wife is Japanese and she’s like the Terminator going through the phone book when she gets the shopping docket. Can’t be bought, bribed or reasoned with. She said supermarket prices definitely increased by 20% in 2020.

Their first strategy is to reduce the number of specials that they always have on rotation and then to raise the price on Deli items that are harder to quantify like olives, cheese, etc. None of this will show up in any CPI measure which mostly has items that are govt price controlled like milk, bread, yada yada.

Wolf stating the obvious hours late! or some investors thought this and others thought that! Really! Not an investment guru!

What is your point? Is that who you are looking for -“an investment guru”; good luck!

Not sure why you would consider Wolf any kind of guru rf?

IMO, he is the very best ”reporter” of financial and economy news, and, unlike all the others I have tried to listen to or read over the last 40 years or so since my uncle, a SM whiz, died and I got out of that market and began to concentrate on the RE mkt, Wolf makes very clear when he is opinionating rather than, ”just the facts” reporting.

Wolf also makes it clear that he will ”moderate” off his site anyone who is overly rude, etc., etc., and so this site has the most enjoyable commentariat on the web as far as I have found so far.

Another good chart would be selling price of TIPS at auction….buyers started having to pay above par for them quite a while ago with a stinky low coupon.

Don’t know where it’s charted, though.

Here’s the best I could do, but if that isn’t inflation fears, I don’t know what is. And you get taxed on the CPI-U adjustment plus the 0.125 coupon or whatever it is.

https://www.treasurydirect.gov/instit/annceresult/annceresult_query.htm?cusip=912828ZZ6

At least there are I-Bonds for us small savers.

You lost several ounces on orange juice about a year ago. Car insurance, home owners insurance goes up a bit each year. Food up. As a landlord, I buy stuff at Home Depot and building materials have gone up.

I recall my Mom telling me when they immigrated to America in the later 1950’s, they were able to buy so much with the dollar. Look at it today. Easy 100 bucks and that’s just for me. If you got a family, either one is a big bread winner or both must work.

The cost of a garage door opener installed in January of 2020 was $450. This January my quote for one is $600 installed.

Stop eating that junk food. Mght save you some big med bills down the road

Since I don’t eat junk foods, may I ask if the cost actually went up 50%, or they reduced the quantity by 50% , or a combo? You know, so called “shrinkflation”.

Also, on inflation in general, here are some thoughts and hopefully someone can help me out as I may be missing something. So comparing to last year at this time:

1. Most observers were commenting on the weakness in the economy, basically driven my monetary magic and, that many wrote about how it rolling over…overall data was not good.

2. No pandemic/shutdowns were in sight yet.

3. I believe approximately 6 million unemployed…unemployment numbers were “good”, at least by gov’t definition.

*** yet, Fed could not get inflation according to their definition….which after all, is what determines raises in Social Security , etc.

A year later:

1. We have had the shutdowns, so wealth has been destroyed and much else as well, so general economy even worse.

2. The pandemic and shutdowns are on going.

3. Depending on whom you talk to, anywhere from 18 to 22 million unemployed, many underemployed.

??? So now were are going to get inflation under these conditions when we could not before???

Could it be that the Fed and gov’t putting too much pressure on dollar? However, all the other currency are no pick nick either. Same boat.

Ok, stimulus? Should be renamed…”here is some phony money so the roof doesn’t cave in”. The “stimulus” doesn’t cover the damage that has been done. I read that millions are behind in mortgages, rent, car payments and so on. The velocity of money is very low…

Can someone shed some light on my thoughts? Thank you.

They are even packaging food in smaller portions, to hide the fact that the effective price, per ounce, is changing. Inflation is definitely occurring in the things that consumers use. Of course, it already occurred and is occurring in real estate, stocks, etc.

My own bag of groceries and expenditures had dramatically increased this year. Part of it may be the tariffs, which reportedly started after December 31, 2020. However, inflation tends to accelerate when more and more people and businesses feel that inflation is occurring and thereby, they better charge more for services or otherwise raise prices, when they can.

I would raise my own prices, but my law practice has quietly, mostly died. The restaurants whose disputes with landlords were being litigated, so they could keep their leases, changed their minds and decided to not dispute their landlord’s termination notices to abandon their leases.

I suspect that a lot of business people are in that same situation. No one that I know wants to file a legal action, because of their inability to afford substantial fees. These are very hard times now and will only get harder when the evictions start if the government does not act.

I do not see how all the businesses can be bailed out, so we will probably lose huge numbers of small and midsized businesses that could not continue providing services. Unfortunately, the news is that not enough vaccines will be available for various months to create herd immunity given the highly contagious virus infections and three new virus variants (three new ones from the UK, South Africa, and Nigeria reportedly were detected and our borders are partly open) may cause the infections to spike from levels that are already overwhelming to hospitals.

Civil insurrection in states would just be the rotten cherry on top of that pile. Those riots will be superspreader events.

The lesser talked about complement to that is Shrinkflation and lower quality ingredients.Soups have been taking away protein and adding salt.Other products take away amounts and increase prices.Noticed this in 2008.Added to this is the less beneficial rewards programs from various retailers.Return policy is also much more stringent.

As long as you have your nice government job with yearly raises, excellent benefits and a lovely COLA pension after 25 years…

“frankly if we got 3% inflation that would not be so bad” as long as it is not accelerating uncontrollably.”

please please ask retiree’s

how much HEALTHCARE(with govt medicare taking top 80%)

how about long term care/extreme care for severe medical

remember 90% widows are broke after hubby took entire savings to pay for care – ie nothing left for grandma

Hey Joe, my wife has COPD (among other ailments). Yesterday, her Spiriva drug, which keeps her breathing, cost me $455.00 using our Part D drug plan under Medicare. Between our drugs and Medicare with a supplement insurance plan, we shell out $14,000 (out of pocket) a year at ages 75 and 77. And it’s going up every year!

I guess we are living the American Dream?

Oh, if we were broke and on Medicaid, our health insurance and drugs would be “Free”

Heck, we can’t even afford steak anymore, especially imported from Oz!

I hear you. Just trying to stay alive is getting hard.

But with medical mistakes being the 3rd cause of death in the US, if you cannot evaluate your health care professionals, “free” health care is not worth much.

Best of luck.

Anthony You need to bone up on vitamin C as the information you can find just might help to reduce your costs.

We take a bunch of vitamins too! They don’t seem to be doing anything for old age though.

It’s kind of like putting racing fuel in that car Wolf presented in the American Debt Slaves thread!

Price in Mexico, roughly $80- don’t you love America and how it screws you ovah.

So many people make their run every three months around Phoenix to San Luis south of Yuma and get their drugs.

I do wonder how long it is going to continue to allow people just to walk across with their scripts and cash to survive. I also know of tons of people going for dental work as well.

Anthony-

My mom had COPD, and vehemently insisted she had asthma, so she used steroid inhalers. Spiriva has a different mechanism, maybe it’s better. Anyway at least one doctor (I was there) tried to get her to use oxygen at home instead, but she refused to do that that along with using her breathing exercise machines, except when actually in the hospital. My sister and I who took care of her at my sister’s house in her final 1 1/2 years said people using oxygen had always visually disgusted her and that’s why she wouldn’t use it….vanity. The steroids eventually trashed her kidneys and she died of renal failure age 87 when she got the one-two punch of c.difficile and norovirus.

I don’t know if she would have lasted longer with better life quality on oxygen (I kinda think so) but just wanted to mention it. She was more than ok with her CPAP machine for sleeping.

Everyone makes their own decisions.

Anthony, find an Indian Pharmacy. one tenth the price.

> how much HEALTHCARE(with govt medicare taking top 80%)

how about long term care/extreme care for severe medical

The assumption that every American will have to waste $ on healthcare is blown out of proportion. Both of my parents used tiny amounts of healthcare.

> remember 90% widows are broke after hubby took entire savings to pay for care – ie nothing left for grandma

Women are better off not marrying and working/saving for themselves. Even a kid by themselves is easier than with a man-child to then have to be a free nurse for after having to be a free maid and cook for. That time should go towards their own goals instead.

Women don’t benefit from marriage. All the time wasted in being a free maid, cook, nurse for a man should go towards their own careers and savings building.

Depends on the marriage and the benefits may be non$$! :-)

Each marriage is different. Marriage isn’t for everyone. Who you choose is a pretty important factor to state the obvious.

“frankly if we got 3% inflation that would not be so bad” says the well heeled Fed creature who is set for life no matter how badly inflation will screw the working class.

What an amoral piece of work these scoundrels are.

2-given human nature and the literal extinction of long-term pensioned general employment in American business (what’s the ‘average number of jobs an American will hold in their lifetime’ index up to, now?), little wonder that one might look at ‘a nice government job’ as an attractive and secure contemporary career path.

(Departed my last suit-and-tie job in 1986 when the president/CEO of the firm, who had personally recruited me and closed the deal with his company’s pension plan, abruptly ended that plan for non-vested employees. After too-many years of 10-14 hour days, by golly, I was short 30 days. Similar scenes have occurred in myriad U.S. firms then and since, resulting in our new reality of general mistrust and lack of loyalty among the workforce (…Paulo’s immortal: “…you pretend to pay us and we pretend to work…”). Have lived on what many here might consider the financial margins since, but not having that slight itch between my shoulder blades lets me sleep at night…sorry for this still-bitter rant).

may we all find a better day.

I have not been following these stimulus payments closely. I erroneously thought they were only going to the unemployed, but I now realize they are going to folks who are employed, or as the payments are based upon the most recent past IRS filings, that were employed during the last year that taxes were filed. But why are employed people who were not affected by the COVID19 policies that caused economic devastation and who remain gainfully employed receiving these checks? In many states, spending the money at local restaurants or bars ain’t happening. Spending on airline tickets not happening. Ordering Chinese crap from Amazon – happening. What is the logic at work here?

How dare you… why shouldn’t China receive its share of the US stimulus. It’s only fair… after all, it’s the freedom of choice, who are you to judge other Americans for buying their LONG LASTING, HIGH QUALITY, AND BEST VALUE CONSUMER GOODS from China.

Are you some kind of socialist or communist? ?

Or… are you one of those NATIONALISTS that insist on buying MORE EXPENSIVE, POORLY MANUFACTURED, SHORT SHELF LIFE PRODUCTS a because of some made in the USA slogan.

?

MCH, Crush needs to look at it this way……China shared the virus with us so our government (using the term lightly) is sharing the stimulus with them in a round about way.

I asked myself the same question. The answer is to help spur inflation. Any money they can get into the hands of people that will spend it on everyday things, will help their “cause”.

Much of the stimulus ended up in corporate bank accounts; some of them foreign because so much of what we ‘consume’ is made offshore.

These stimulus packages should be aimed at cohorts who are going to spend the money. What cannot be avoided, however, is that private debt is so high, a lot of the money will go to pay down debt. As Michael Hudson observes, two negatives (running up debt, then paying it down which suppresses demand) does not make a positive.

Anyway, stimulus is required. We haven’t got the distribution effects down, however. Aussie economist Bill Mitchell estimates the demand ‘gap’ that needs to be filled is $5.267 trillion.

“(running up debt, then paying it down which suppresses demand)”

So you bought something you couldn’t afford at the time (increasing demand) and then pay it off later( suppressing demand). Doesn’t that equal out to you? Seems neutral in my mind

Sounds just like France just before the French revolution. Once they started down the road to driving the economy by money printing, they kept having to do more and more until they did too much. Poorest get hurt the most when it collapses.

My millionaire friend who retired and residing at another country is enjoying his stimulus check just because he files to report only his SS income.

Go figure.

Reward for Chinas military?! :-)

I wonder what happens when the new $1 trillion in debt is issued in the next few weeks. Will the Fed buy all of it? If not, rates will come up even more.

Goodby real estate boom

Why wouldn’t they at this point? Nobody really cares about moral hazard right now because there is no wide recognition of the downside of current federal reserve policy. The dreaded inflation of the 2010s never showed up like the hurricane many feared. So where did the money go? What’s the big deal?

Minus the “h” I see you are up to $15K!

I have been tracking inflation and de inflation for some time. We have been slowly going up on some items for some time.

It’s not a matter of moral hazard, it’s a matter of destroying the dollar.

Exactly!There are no noral hazards as that implies anyone has any kind of morals and if they do,whose morals? :-)

“The dreaded inflation of the 2010s never showed up like the hurricane many feared.”

It showed up, in assets.

Yes, to the point that most young people will NEVER be able to buy houses, because all of the wealth has been transferred to the older, top 1%

Yes, that’s why my ‘storage space’ is larger than my ‘livable space’. ?

And college tuition. And healthcare.

There is no law requiring Congress to create debt to ‘pay for’ deficit spending. It’s a ‘gentleman’s agreement’ that allows us to pretend the debt actually funds Congressional spending. It doesn’t. Debt is not intrinsic to funding Congressional spending. That said, the Fed could buy all the debt and not sell it into the market. Left pocket, right pocket, same pants. Direct injections are far more efficient, and fast acting. No debt required. I believe the Federal Reserve is actually working on an operational capacity to do just that.

Funding of gov liabilities due to the lack of earned money for taxes, coupled with large trade imbalances due to a similar lack of USA work made things results in capitalism ripe for fraud, income disparity, and loss of freedom.

Every Ponzi scheme has it’s day. The more income disparity that occur the further in debt we go.

They will need to control everything when the protests get more violent, like China.

Draw the analogy between the power/energy to do work (joules) and the ability to make this work continue in healthy capitalistic fashion. The velocity of money, and the joules creating the velocity, lack power due to the absence

real earned long lasting work money. This could get very depresioning for a lot of people if it drags on for years like in Japan.

What an absolute disgrace central bankers and politicians are. These ivory tower hacks couldn’t run a lemonade stand.

I think you are misreading the situation Wolf.

The yield is up not because the markets smell something, but because the Fed thinks it’s ok for now. They can bring it back to 0.5% within a week if they wish so.

You are implying that the markets are functioning normally and there is price discovery out there.

We haven’t had free market in the treasuries since 2008.

With the temperature on the thermometer constantly manipulated;

one doesn’t know whether it is freezing outside and to turn on the furnace

or whether it is too hot utside and to turn on the air-conditioning!

Yes, as you imply, one thing is for sure, if the Fed wanted to, it could bring the yield back down. So yes, the Fed is still thinking that these yields are OK, or else it wouldn’t let that happen.

Can they? My sense is that they have to do so gradually, because if they buy enough to bring yields back down, more people will sell as prices drop, creating a positive feedback loop.

I got the sense that yields have increased because people no longer want to hold Tbills at .5%, and what the Fed is doing is more of a symptom, not the cause.

That’s the question I have. Where does the ‘FED controls the yield curve’ break down? At some point the market will fear that more monetization will cause yields to rise even faster and the more the FED prints the more yield investors will demand. In the end the FED would have to own the entire market to still control the yield curve.

We have not seen it. For now the treasury market is controlled by a supply/demand equation of treasuries alone, but there is another factor which is the supply/demand equation of the underlying currency. To me it looks like monetary policy and theory in the US is increasingly dependent on the premise that the USD is the reserve currency so there will always be a buyer for USD. It’s completely taken as a given because it has been for a lifetime. If this premise will ever start to break we will see some true market fireworks.

Yuan

My question too, for a long long time.

But the dollar seems to have some extra magic that I don’t understand. Why are people willing to hold 10 yr treasuries at less than 1%?

Or do they think they are smart enough, and fast enough, to sell them before everyone else notices the crash? Or their computer can sell faster than the other computers?

Yuan

Or is it this diabolical:

The guys with the ten year treasuries at 1% figure that the Fed with the magic money machine has the FASTEST computers, who won’t allow the price to drop TOO fast in case of a possible crash. So sellers of treasuries assume their computers will at least have enough time to sell to the Fed computer before getting hurt too badly.

The cash then will be held by the former treasury holder in place of the treasury as wealth at zero velocity not being spent–so inflation won’t happen too fast because that cash won’t likely immediately go into circulation–as long as inflation hasn’t yet been able to accelerate in the rest of the economy for other reasons.

Then my head begins to spin….

Wolf,

A retrospective post of the “Taper Tantrum” of 2013 (2014?) might be very, very useful.

Considering how absolutely supine the Fed has been about inflation (both patent and invisible) for 20 years, the *very” rare occasion of when (and why) the Fed felt it necessary to throw a scare into the mkt might provide some valuable insight into future Fed actions.

Yes, at this moment they would probably get away with that. But when the Fed finally gets its wish and succeeds beyond its wildest dreams in generating surprisingly high inflation in the CPI, the game is up.

When the bond market prices that in and the Fed buys bonds in an attempt to suppress yields (i.e. print more money), that would be throwing oil on the fire and therefore might actually increase yields. While the Fed has a gargantuan $5T of treasuries on its balance sheet, this is still only a small fraction of the $20T or so of the total. It won’t be able to absorb all supply.

The usual way to suppress rising yields for long maturities when inflation rises is to raise short term interest rates and remove liquidity (i.e. reverse QE). Nobody currently expects that, so expect carnage in the markets should this come to pass.

For some strange reason, everybody now seems to believe that the central bank can backstop government spending. But it is the other way around: government is the backstop of the central bank. Base money is created by buying Treasuries, i.e. it is these Treasuries on the other side of the balance sheet that give the money value. And Treasuries are valuable only to the extend of the value the government can realistically extract from the economy by taxation.

So how long is this still credible? Well, it’s been going on for much longer than I thought it would. But this is a very unstable situation. Investors are comfortable holding bonds because other investors are too. But when some start to bail, this could snowball very quickly. Nobody knows when will happen but it cannot go on forever. Ask Argentina.

Good summary…loss of faith in the USSA government will occur slowly at first (last 20-30 years?), then all of a sudden. Kind of like Hemingway’s summation of bankruptcy. Although many countries print like the USSA, no developed country runs a trade deficit like we do, courtesy of having THE Reserve Currency, i.e. TRUST that we’ll make good on our debts.

Would you trust the government to pay back everything it owes, especially to foreign enteties?

I don’t either.

Government as operated in Washington DC is Organized Crime, plain and simple. Perhaps sloppily organized at times, but crime nonetheless.

Don’t forget the primary dealers who “earn” their cut every time the Treasury pushes the goods to the Fed.

Indeed, well organized.

YuShan, exactly. The Fed can’t simply buy all treasuries. What it can do is buy enough to force prices up (and yields down) but ONLY to the extent that other investors are willing to hold the remainder IN SPITE of this price interference.

At this point, both parties have succumbed to MMT, and there’s no credible argument we’re ever going to increase taxes on ourselves to pay for this spending binge.

Also, I don’t find the “But we’re the reserve currency and the cleanest dirty shirt” argument credible. While that may be true, our levels of taxation are much lower than our European counterparts and our levels of spending/printing much higher.

It’s more likely that foreigners are dumping treasuries gradually so as not to tank the value and make it unlikely that they’ll book losses.

Prices are set at the margins and 5 trillions out of a total outstanding 20 trillions is not tiny, its 25% and the Fed is currently buying 120 billions each month.

They can instantly increase it to one trillions if need be or reduce it to zero for that matter.

Yields will raise only if the Fed decides to let them do so. All other players are midgets compared to unlimited printing power of the Fed.

Yes, but this is ultimately controlled by the value of the dollar relative to foreign currencies and assets. The Fed CAN’T control that

So why is Argentina not doing the same?

True, but the Master Forger Theory of Governance breaks up when DC can’t hide/frame somebody else for the related, inescapable inflation that results from how it “governs”.

Once the USD breaks, DC’s power will cease to exist.

I’m sure DC will perform some summary executions in a bid for continuation (see worthies like “DC has Nukes” Swalwell) but in the end, the political class that profits from the status quo is tiny in relation to 325 million other Americans, terminally hardened against DC’s horsesh*t.

YuShan, exactly. It only appears to “work” right now because we can print and not have the money stay entirely within the U.S, which would cause rampant consumer inflation.

But foreigners have made it clear that they don’t want our dollars at the prices they did just a year ago, and it’s rapidly getting worse.

Good analysis of this exciting game of inflation brinkmanship Fed and Guv are playing.

It is indeed a con (confidence) game with authorities as the inside operator and public as the mark, or victim.

This monetary/fiscal game might implode on itself unpredictably (straw that broke camel’s back is a good analogy), or a black swan may appear ‘out of nowhere’ to do the honors and put paid to the charade.

My vote is for a black swan event. Timing is unknown, but if our spot in countdown timeline is like a clock I would say it is 11:30 pm.

The US Treasury (Government) creates the “assets”. The Federal Reserve creates the liability.

That’s why I don;t buy anything with more than a 1 year maturity.

I agree.

Have we had market driven bond yields, 30Y and 10Y treasury yields would trade much higher.

I agree with your comment/thoughts. I’ve felt this recent steady rise in rates is Fed/Treasury driven to strengthen the dollar a bit. It will end shortly as they don’t want to go too far. Let’s see.

Maybe the Fed thinks more money should go into government debt, verses trying to handle the debt all by itself?

We are in a economy divorced from policy hence inflation. Fed tries to raise rates to counter inflation, they will find it makes the situation worse, (higher cost of money translates to higher costs). So let it run hot, (or lukewarm). Downside is that rates rise faster, omnipotent Fed falters, and inflation lags because of economic sluggishness. Bad news for everybody, not enough yield return in bonds to reallocate from stocks. Rates high enough to squelch lending.

What most people are missing is that dealers/banks/funds all over the world have been rehypothicating collateral to back everything else… there is no CB that can control this once the chain reaction starts… feb/march 2020 was just a warm up…

Watch the US dollar’s foreign exchange rate!

Foreigners always figure it out before anyone in the affected country do!

Tell me about it! GBP =$1.36! It’s a race to the bottom, alright.

What is the reason the 2 year hasn’t budged?

If you look at the yield curve, every maturity of 3 years of less is at 0.2% or below (near zero). So the yield curve is essentially flat in that range. The Fed, with it various mechanism, has a tight grip on the short end. And these yields are all within the Fed’s federal funds target range of 0%-0.25%. After that, the yield curve steepens.

Got it thanks for the explanation Wolf.

Mr. Richter, Mr. Daniel Tarullo, former NY Federal Reserve board governor, was on Bloomberg this week and made some very interesting statements. Tarullo was the man behind the scenes during the 2008 financial crisis and was actually running the show. His involvement was not made known until several years later. Yes, there’s definitely something very unusual going on behind the scenes in the US Treasury market.

“made some very interesting statements”

Don’t be a tease (or make me Google)…what did he say?

Powell would have started to normalize rates, but political pressure kept him beholding. Fed can allow markets to set rates, especially in the context of reduced economic growth projections. The bond market is really too big (globally) to move as quickly as naysayers assume. Those new treasury buyers will be mostly offshore cash, and once the government policy toward the dollar is bolstered they can buy bonds and monetize our spending without running deficits. The stock market sees a lot of blue sky with the assumption that real economic growth and consumption improves and earnings. Once rates normalize and GDP resumes the wealth disparity gap should close.

AB,

“once the government policy toward the dollar is bolstered they can buy bonds and monetize our spending without running deficits”

You are going to have to step through that, because it doesn’t make a lot of sense on its face.

If there were some secret sauce “dollar bolstering” (definition?) that allows dollar dilution monetarization (hooray?) and makes fiscal deficits disappear (after 50 years)…where has it been for 10+ years?

Go through and describe each of the steps individually.

Election is over. Now the pain is to be let lose on economy so it is forgotten before the next.

The thing that really galls me is the Fed is intentionally making savings and retirement planning more difficult by manipulating the price of assets. People on Wall Street know how to front run Fed policy and people on main street get deceived by the asset manipulation.

It’s a club. And you’re not in it. It’s the penalty for choosing the wrong career – or more precisely, the wrong parents.

> The thing that really galls me is the Fed is intentionally making savings and retirement planning more difficult by manipulating the price of assets.

Depending on your age. Tech is allowing remote workers to relocate to LCOL areas shifting their healthcare and fed tax burden on the shoulders of the middle class living in HCOL areas.

The BEST way to plan for retirement is to play this game crushing fixed costs like housing, healthcare, taxes and transportation. It’s a massive geographical arbitrage that finally one can enjoy without having to wait for retirement. This way, savings rates above 70% are possible without that much effort.

It is not about making savings and retirement more difficult, it’s about stealing your wealth and making it difficult for you to see it. There is one way for main street and people who don’t understand wall street: make savings in gold or real estate. Measure everything in gold terms. Fiat is a lie, you don’t want to use a lie to measure investments. This doesn’t mean one should avoid wall street, but just to look at how much gold you have at the beginning and at the end of each investment. If it doesn’t make gold, it doesn’t make sense. Of course, it’s a bit old school.

Meh. Could’ve written this article two months ago, last time there was a “new since March” “high” in the yields. They’re still historically awful yields.

But the Bond Market can’t smell a rat properly because the Fed policies have the same effect as COVID does to real people – wipes out the sense of smell… and all the bond vigilantes are dead.

“all the bond vigilantes are dead.”

A whole series of posts could be written about what might happen “After the Dollar”.

Hint hint.

The stimulus money should go down once most people get vaccinated, because they could pull money fron the stimulus to pay the vaccines and to pay the public health system. Then again this is the USA so who the fudge knows…

Not a chance. First, there will be a lot of long term job loss from this pandemic as many industries have been restructured. Second, now that politicians have seen that they can outright buy votes without having to raise taxes (read many comment threads on political blogs, people actually think MMT is a legitimate theory), that’ll continue. I expect a UBI very soon, even after COVID is but a bad memory

I’ll give you $2000 if you vote Democrat in Georgia – J. Biden. And that’s just a start.

MMT = More Money Today. (Tomorrow will take care of itself.)

> I’ll give you $2000 if you vote Democrat in Georgia – J. Biden. And that’s just a start.

Isn’t this ultimately a transfer to people with super low fixed costs living in LCOL areas?

Rent-wise it goes 3 times as far in the Midwest than in the coastal expensive cities where it doesn’t even cover 1 month of rent.

> I expect a UBI very soon, even after COVID is but a bad memory

Same! It’s basically a transfer from HCOLs to LCOLs.

I’m all for it!

We’re seeking Equality here. Eventually HCOL for everyone. I’m old enough UBI won’t bother me too much. The young, however, will have to live through the resulting horrors.

Well, here is the thing about MMT…it is so transparently stupid and infinitely gameable that it can more or less be discredited in three or four short paragraphs (“Of course inflation could ruin the country…but you said “bankrupt”…).

In the era of the internet, those paragraphs can be cut and pasted…infinitely.

So the only places that MMT ends up going unchallenged are

1) 100% insulated Left wing circle jerks and

2) Among the Baghdad Bob Meat Puppets of the MSM.

Wholly shameless deceit is in vogue so MMT will be habitually pitched…but, being challenged everywhere, it will convince very few who haven’t already huffed the paint.

The internet has altered the dynamic from the days when “Doomed from Inception” DC policies could be Leni Riefenstahl’ed through, against the common sense of the 95% of the public who have to live under said policies.

In case you did not notice, stimulus money did not win Mister Trump the election.

Not everyone wants the vaccine.

Inflation is the hidden tax that consumers don’t seem to understand. Place a 3-5% tax on fuel to fund highway projects and taxpayers get angry at the pumps, yet the Fed advertises “good 2-3% inflation” on EVERYTHING, and taxpayers seem happy as it is hidden, and does not print out one their fuel receipts as “Fed Stealth Tax”. Perhaps time to place a line item on every product and service receipt that contains “Fed 2% Inflation”, and then lets see what happens?

Sure we can all pay less taxes, get loads of stimulus, and pay for it all by debasing the currency Such ultimately drives up our Fed mandated stealth EVERYTHING inflation TAX that makes the entire construct a zero sum game of winners and losers that is based more on luck than hard work and responsible human activity…

Yes, if the central bank wants higher CPI inflation, just stick a federal 2% sales tax on everything and increase that tax by 2% per year. It is nice and transparent, unlike the stealth inflation tax. It would also encourage the discussion whether we actually want inflation, what purpose it serves and who is most affected by it.

Sales taxes actually depress spending because they affect the low income buyers the most, who wait for sales, substitute, or don’t buy.

I have a high sales tax in my area and never buy any discretionary item unless it’s on sale for more than the sales tax. Usually, I wait for the discount to be at least twice the sales tax rate. I am pushing the tax burden back on the seller and lowering his eventual income and tax basis. The govt is actually losing more as they increase the tax.

Check out FairTax, they advocate a national sales tax with the abolition of income tax.

Regressive taxes are as bad as MMT.

The net effect of raising the sales tax is a drop in consumer prices. Vendors absorb the tax rate hike. In effect it is a corporate tax. The immediate cause of the demise of brick and mortar was the sales tax waiver on internet purchases. The loophole was grossly unfair and never should have happened. Now the red lumpen want to blame China. CC rebates and other box store discount programs are effectively zero sales tax gimmicks. Walmart buyers beat up vendors on pricing, its all deflationary. That’s how the average joe can fill a house with junk while personal income is flat. To get inflation drop the sales tax and put the bite on shipping. With $50 oil in a 25 cent economy you will see more CPI.

I like that. A FRB 2% tax line item on every single consumer sale receipt.

> Inflation is the hidden tax that consumers don’t seem to understand.

What people don’t understand is that tech and aging demos are highly deflationary. The fact that somebody using a ton of healthcare is affecting a few who spend a ton of healthcare doesn’t affect me when most of my purchases are tech-related.

Housing inflation used to be problematic, but with remote working, there’s no need to live where the NIMBYs live. Move away from them and place the healthcare and tax burden on their shoulders: make them pay for your ACA and lower your federal tax burden like there’s no tomorrow. Once you crush housing, healthcare and taxes… you shouldn’t be worried about inflation.

Tort

Exactly and wait till they raise taxes. Market trying to outrun both.

What are people doing with the helicopter Stimulus checks? Paying down debt? Buying stocks? As Jim Rickards points out, the money printing doesn’t cause inflation when the velocity of money is at record low levels.

The sales of trucks and large SUV’s increased as the price of gasoline dropped. Saudi Arabia recently announced a million barrel/day production cut. Electric vehicles are becoming more popular in Europe. They are about 2% of U.S. sales.

Bond prices fell yesterday. I suppose the assault on Congress on Capitol Hill did not inspire confidence in the bond market.

My dad told me story of someone in his small town having a two mule team to work his small farm. FDR public works program was doing a project in the state and wanted to rent his mule team for a few months. The farmer was afraid that his team would get hurt so he told them he would only allow it if his son got hired on to work the mules.

What is the lesson? When government sprays money around it changes things. In this case a farmer got paid to give up his means of production to build a government make work project. For him it was great as the government paid above market rates. Did the government help the over all situation? Probably not but the statistics showed they created a job and increased GDP.

If they were digging ditches then filling them in, of course that is useless. But what if they were digging ditches to irrigate crops or improve cropland drainage? What if they were building the Hover Dam? Would any of those changes have been positive for society?

Yes a corrupt government will mostly fund useless, even harmful projects, and that is what we now have. Perhaps the problem is the corruption, rather than the idea of people pooling resources to fund projects for the common good.

Govt has a history of funding things that aren’t needed, with interstate highway being a notable exception. See high speed rail in CA.

RE: helicopter stimulus checks:

People in my family and extended family are either paying bills or buying food/staples.

Step Daughter-in-law is unemployed (oil co. layoff) since about last February and is still collecting unemployment. She is divorced from my stepson but still a family member per se, with an unemployed grandson at home. This is not going to end well. She will lose her house unless she ends up with a really good job (unlikely). Her skills are related to oil & gas accounting and she is over 50 years old.

Other grown children have spouses that have been furloughed and still collecting unemployment insurance. They are “two worker” families and are laying low and not spending unnecessarily.

Adult grandchildren (2 of 3) are “getting by” with entry level jobs and are careful spenders. Both have college degrees (non-technical).

Pretty much everyone in the family is in a holding pattern and not buying Chinese junk. They had plenty of it in-place before 2020 went nuts.

Since so many here are concerned about deficits, I’m sure you will all be happy to know that the CBO recently state that Medicare For All with single payer would reduce the Federal deficit by $650 a year.

Other studies show similar proposals to save about 100,000 lives a year

S/B $650 billion a year

If they are going to make numbers like that why just say it will erase all budget deficits and make people immortal? If you are going lie through your teeth, go whole hog.

The problem with government “estimates” is that they always assume that no one changes their behavior in response to the new law, tax, regulation, or whatever.

For example, New Jersey proposed, and ultimately passed, a cigarette tax some years ago. They “estimated” it would bring in X dollars per year, where X represented the tax per pack multiplied by the number of packs sold in the state the year before.

As you can imagine, the tax passed, and revenues were nowhere near estimates. Some people quit smoking (which is good!), and others started rolling their own cigarettes or buying them in neighboring states with much lower taxes.

In the case of Medicare for all, they simply assume that providers will be paid the same rate that Medicare is currently paying, but for all patients, not just 65+ people.

The problem is that the providers get paid substantially less for Medicare patients, and essentially subsidize their operations with higher payments from private insurers. If EVERYONE was on Medicare, they’d have to raise prices or they’d go out of business.

Additionally, consumption of medical services would inevitably increase, as people consume more of anything that is “free.”

All of this is not necessarily an argument against Medicare for all (there are good policy arguments for and against), just a summary of why these estimates are always nonsense.

Actually, studies on MedicareForAll do take into account change in behavior. That’s so many of these studies conclude not only huge govt spending changes, but about 100,000 saved lives a year because people change their behavior and get needed healthcare.

“people consuming more free medical services”

That’s exactly where triage comes in! Everybody in the military has to accept it. Why are us civilians so damned exempt from what “our heroes in uniform” face daily?

If I hear that meaningless and obligatory “thank you for your service” crapp again I am liable to lose my usual civility. In fact, I seldom mention I’m a vet unless asked, and don’t advertise it with a ball cap or bumper sticker. I just check the box when it truly helps me out somehow.

NBay-my ocassional surly response is: “…and what service may i thank YOU for???”. The oft-resulting blank look in return would be risible if it weren’t so damn heartbreaking.

(Somehow, with your dirt-moto background, i can’t help but feel i’ve crossed your path in my shop days here in Sonoma County. D’ya know BP?).

may we all find a better day.

The figures aren’t made up. It’s been known a long time Medicare and Medicaid are the lowest cost healthcare options vs employer based insurance & all others. About 40% lower and that’s before you account for additional savings with single payer. And state & local govt would save hugely. For every 1 dollar spent giving MedicareForAll, about 2 dollars are saved.

Did you bother to read my comment? I address the cost issue there.

Yes:

“The problem with government “estimates” is that they always assume that no one changes their behavior in response to the new law, tax, regulation, or whatever.”

Did you read my comment? It address that, also.

Single payer is used throughout the world. Saying one is assuming it works, is not accurate. It does work. All over the world.

No, I’m referring to the rates paid to doctors and providers.

Also, the rest of the world is subsidized by us in terms of drug development.

If “studies” are so darn accurate why are we in the mess we are in? Perhaps we haven’t been buying enough “studies?” Apparently “studies” are accurate before implementation and reality sets in.

Lisa-i’ve come to believe the constant generation of new studies addressing the failure to properly implement/complete older studies are a larger economic driver than one would initially think. (As a late physician friend of mine-he was in research-said: “If i actually had to practice medicine, i’d stick to pathology-one usually appears wise and the exposure to error or malpractice is small…”).

may we all find a better day.

Haha, yes!

You might be misunderstanding what the CBO report is saying (or I might be misreading it!)

It’s CBO publication 56811. It has a number of scenarios that it looks at.

In those scenarios it sees an *increase* in the federal budget from $1.5 to $3.0 trillion dollars by 2030.

However, spending on National Healthcare (i.e. by govts, companies and private individuals not just the fed govt) would see a range from a $0.7 trillion decrease to an increase of $0.3 trillion dollars.

All the usual caveats about assumptions and projections apply.

“Medicare for all”…. See the comment above regarding $14K out of pocket for a couple in their 70’s. In my case, it’s about $10K for my wife and I (and I take a $2 generic drug x 4 refills or $8 per year and go to the doctor exactly once per year. I do get an annual flu stab. That’s it.). My wife isn’t so lucky. Last visit to the pharmacy (for a 90 day supply) was $700 for her. One 5G tube of “ointment” was over $500 the month before that. That’s Medicare for you.

People are under the erroneous assumption that Medicare is “free”. It’s not. The monthly charge for those making less than $75K per year (as an individual) is in the realm of $150 per month…. or $1,800 per year and that’s if you don’t use it. The co-pay is 20% on Part A (hospital) and comparable on Part B. The deductible is @ $500. Then there’s Part D (I pay $34 a month and my wife is $90 a month because we had to find a plan with her meds on their forumulary) plus the co-pays. And, keep in mind, that the premier medical facilities (such as Mayo Clinic outside of MN) do NOT accept Medicare assignments. The patient eats the difference. We have Medicare supplemental policies that add another $285 a month to the tab – which cover the “gaps” between costs and what Medicare pays. Those rise when you hit certain ages – my gift for turning 70 was an increase of $40 a month.

So it somewhat baffles me why people think “Medicare for All” is *the* solution to costs of care. As my ex-doctor said one day: “If you think medical costs are high today, wait until they’re free.”

Correct Ei. My wife’s drugs on the best Part D plan I could find run us about $3,000 OOP, not including the $455 deductible or plan premiums.

“Medicare for all” will be a huge surprise if it comes to the masses.

BS

BS

Inflation….slowly then suddenly.

Corn, Beans, Wheat all up 20 – 33% in just two months..

Run that through the food chain….

Lumber, Aluminum….?

The bond market collapse will be geometric….and what of all those mortgages and the paper to back them up, when inflation and thus rates exceed 3%?

Inflation will punish and grind down the working families of this nation….and all to encourage investment in stocks.

This will put people (even more) in the streets in protest. IMO.

First…… it will be explained as welcomed and a sign of economic activity and recovery. The talking heads on cable are already at this stage. Just last month they were saying “no fear of inflation.”

Second stage … The averaging “back” to mitigate the reality of this current inflation. We will only see charts of the “rate of increase” but rarely if ever a chart of accumulated and compounded inflation.

Third stage….will be a weak reaction by the Fed, 1/4pt “cautionary” raises well behind the rate of increase. (remember when they cut 1.5% in just months?)

Don’t know how many times I’ve repeated this — 2 year treasury yield is a proxy* for where the 10 yr yield is headed, a year from now.

Today: 2 yr yield = 0.143 %

Looks a lot more like disinflation.

* Based on research related to treasury futures, from Ed Yardeni:

… previously served as Chief Investment Strategist of Oak Associates, Prudential. Equity Group, and Deutsche Bank’s US equities division in New York City

Well, Martha, you are wrong so far.

If you dont see the inflation, you’re not looking.

Look at Corn, Soybeans, Wheat, Lumber, Aluminum, Housing, Medical care…

ROARING!

I don’t disagree that some commodities are going up, due to pandemic related shortages, but overall, commodity stuff apparently is not exploding in price.

(a) Consumer Price Index for All Urban Consumers: Commodities in U.S. City Average, Index 1982-1984=100, Not Seasonally Adjusted (CUUR0000SAC)

Wheat as an example was significantly higher during the GFC, but lately the price has not spiked. Covid has obviously raised prices for some things because of demand, and that’ll continue for many months — and eventually price shocks will be offset be decreases in prices as we see more disinflation

I think we’ll see more inflation-related dynamics from a weaker dollar, but all this needs to be looked at in context, with global pandemic economics. Central banks aren’t likely to raise rates and future value of longer term debt isn’t a factor, because GDP has been weak for a decade and pandemic growth will be less than ever. I see no argument anywhere for overall inflation, except of course in food. Generally people have always assumed oil to be an inflation factor, but oil will be contained by virus. Home prices going up in many places are related to supply shortages and demographics, yet mortgage rates will bounce now and then but stay lower.

It also doesn’t take much imagination to think guns, ammo, liquor and fatty foods will experience inflation …

I think you have way too much faith in central banks. Ultimately, inflation will result when the demand for “stuff” exceeds the global ability to produce it. Printing money doesn’t change that dynamic.

Central Banks will be forced to react when the 95% who dont have enough stock in their account to make a difference get CRUSHED by inflation.

Strikes. Have you ever been through an inflation….like in the 70s?

No, most modern investors haven’t, and they haven’t experienced a real bond market, so they think neither can happen.

Also, bear in mind that stock wealth is illusory. As soon as people start selling, the value plummets.

Faith isn’t really an issue, I’m more interested in supply/demand. I agree that production will play a role with output, but the game of bond yields, economic growth and future value are intertwined in complex ways.

In the most simple terms, a huge tsunami of debt supply and bond issuance will dilute future value, which will theoretically keep purchase prices lower — but, the only reason yields will go up, will be a shortage of bond buyers, but that doesn’t seem to be happening. Nothing makes sense these days …

Meanwhile at FRED, we see the explosion of debt issuance:

Assets: Securities Held Outright: U.S. Treasury Securities: Wednesday Level (WSHOTSL)

or

Federal Debt: Total Public Debt (GFDEBTN)

FYI: To finance this budget deficit, the U.S. Treasury will need to issue massive amounts of debt. At the quarterly refunding in August, the Treasury announced net issuance of $947 billion for Q3. This followed the record $2.753 trillion in realized borrowing from April-June.

Comparing pre- and post-COVID-19 funding requirements from coupons issued during the January to March 2020 quarter of $579 billion to the most recent quarter of August to October of $934 billion is over a 60% increase in coupon issuance.

==> I can’t see yields going higher with that supply flooding in. I was never trying to infer that I had faith in central banks, I just think the market will run the show, regardless of what the CBs do and I think rates will stay stuck in a low range.

The 2 year yield says there will be very little GDP growth going forward — and I have faith in that.

You see inflation related to supply-demand and gdp. You forecast low gdp and low demand, so low inflation. When there is strong demand, people and companies ask for credit, and the bank prints money (they don’t pay for credit with your savings, they hope you will pay back and cancel the money). So, strong demand=money printing. My point is, in sh*thole economics, take Venezuela for example, there is inflation without demand: people are broke, and prices go up. Why? Money printing. Money printing is the heart of inflation. Imagine a world with a stable amount of money and growing wealth and gdp: prices would go down. Complex theories are hiding the truth of something very simple: money printing makes you poor, prices go up and don’t care if you can pay for it or not. One silver dollar, changing hands :)

Except of course in assets including RE, equities (on a tear as we speak), bitcoin, gold, etc. Also education, health care, automobiles, etc.

Yes, I just bought, after a LONG wait, a box of 50 9 mm Luger ammo (not hollow points). I paid $65 with shipping. A year ago these were $30.

Grocery prices are going off the charts too.

I paid $9/box for 50 rounds of 9mm ball. That was a while ago. Ammunition keeps well when stored properly. A brick (500 rounds) of .22 LR used to be under $10.

As Admiral Acbar used to say…it’s a trap.

“Stimulus” money is more than offset by falling income Wolf. Another point is that stimulus even if one where to assume perfect economic conditions is nothing more than a three card monte game. No quantity of money is added to the economy, it only shifts money from one group to another even when CBs are monetizing debt. The only thing for now that could cause price increases in consumer goods is the trade war.. a significant shift in production capacity and costs.

You should factor in that poor/middle income people spend their money, and wealthy people generally don’t.

Money printed and given to the poor/middle class goes straight to spending, which increases consumer spending overall.

“Money printed and given to the poor/middle class goes straight to spending, which increases consumer spending overall.”

If that was the case then yes of course. But stimulus is not money printing. It’s more like taking money from one pocket and putting it in the other. It just shifts money from one group to another.

Forgot to add Bobber. The middle and poor class that receive this money have had their incomes decimated by the lockdown so any stimulus money while it is true that it goes to consumer spending it is not enough to offset the loss of income in terms of salaries small business revenues etc that would have otherwise also gone to consumption, and expenditures.

Yeah, but what kind of spending? Buying foreign manufactured goods does not have much of a multiplier, the way spending on domestic goods or services would.

“Inflation destroys the purchasing power of bonds. The yield is supposed to compensate for that risk. But in this scenario, with current Treasury yields, it’s not even close.”

One of my favorite analysts, Jim Bianco said a couple of months ago that ultimately the Fed does not have complete control over the bond market when there is a consensus opinion on the direction of inflation.

When there is a fragmented opinion on inflation (some say up, some say deflation), the Fed can control the bond market with a combination of jawboning and treasury purchases.

So,with the above in mind, it’s quite possible we could see yields well over 3% on the US ten year if the market decides there will be inflation. The Fed will not be able to control the curve anymore.

P.S- (I have no idea how true Jim’s analysis is, but it sounds right)

Robert

“when there is a consensus opinion on the direction of inflation.”

and Jerome Powell is very aware of “perceptions”….and has said as much.

The financial history of this nation, prior to 2009, was that Fed Funds equaled or exceeded inflation. This was the “norm”. This was “fair” to lender and borrower. The central bankers have rewritten that “norm” for a while……they have held the beach ball under water in good times and bad.

But markets have a way of seeking equilibrium….eventually.

We saw how healthy the market was in December of 2018 when Powell attempted to bring Fed Funds to equal the then 2%+ inflation.

5000 Dow points later, Trump jaw boned him into slashing rates.

When the Dow made its then all time high in July of 2007, Fed Funds were 4%…and in a market that had been rising steadily.

Todays market couldnt handle 1.5% Fed Funds.

Bloomberg macro technician William Maloney was quoted by Zero Hedge:

“Using the S&P 500 Index as an example, an increase of 1% in the 10-year US Treasury yield from current levels would lead to an 18% decrease in the price/earnings multiple (P/E), all else equal. For the Nasdaq 100 Index, such a rise would equate to a 22.5% decline in the P/E.”

From a technical and fundamental level there would be increased 10yr selling at 1.10% according to the Nomuro quant- Takada.

Beyond the repercussions rising rate cause from option selling backlash like stock selling, it is clear that the Fed will definitely try and control rates well before it gets away from them. There can never be normalized rates with all this debt.

Never say never to a swan trying to land.

Black swans matter.

Implicit, that means that the Fed is going to have to raise rates gradually, before the market gets away from them and causes rates to shoot up suddenly.

RightNYer: I don’t think they will be able to raise rates for a long while due to the large amount of money applied to interest already. They can’t afford to raise rates without creating more money at the same, a Ponzi scheme wrapped in a conundrum.

But they also can’t afford not to. If they don’t raise rates, debt becomes more and more unmanageable.

That is true. And the determination of the Fed to keep rates low even when inflation starts to heat up can actually have two very different outcomes:

Outcome 1) If you belief in the Fed’s omnipotence, you expect that the Fed will be able to keep yields low. This belief is underpinning the market at this moment (and has in the last decade at least)

Outcome 2) If you don’t belief in the Fed’s omnipotence but you do belief in the Fed’s DETERMINATION, this will reinforce your belief that inflation might run out of control because you expect the Fed to be behind the curve when it happens. After all, inflation past a certain point is highly self-enforcing. So investors start selling long maturities well before the actual inflation takes hold. Because if you expect the Fed to let things run hot, you really don’t want to own 30-yr bonds at 1.8%.

In other words, the Fed’s resolve to keep rates low even in the face of inflation may backfire.

The situation now is very different from the last decade with QE. This time around, the massive fiscal spending puts a lot more money in the hands of people who actually spend it. The Fed can buy what they want as long as the climate is dis-inflationary, but when inflation starts running hot, or even when investors start to expect that to happen in the future, it will be a completely different game.

Sorry, but the market has COVID and can’t smell a damned thing. There is a giant pile of dogs**t in the economy, and Mr. Market is oblivious to it.

Automatic first quarter investing by the automatons…

Then sell in May and go away.

That is the managed money game.

?

I sure was ripe for a little humor!

So, what is the consensus here? Wartime yield control or no?

That’s always an option. Japan has been doing it since 2016.

I’m curious to know if you think they will do it?

If yield control is combined with QE — is there any limit to how high prices can go? It seems like at that point “the market” becomes actually detached from the real economy — stock values simply being determined by how much QE money is attracted, rather than any underlying notion of “value.”

Hey Wolf, where are all your CCP trolls? They infest everywhere else.

Bitcoin up 10% today. It’s been sky-rocketing.

It’s a sign that the younger generation has little faith in USD and is expecting inflation.

If and when the Bitcoin price bursts, there’s going to be some upset younger folk. They were mad at central banks before. After a bust, they’ll be steaming.

Ironically, the Fed may find itself in a position needing to save Bitcoin in order to prevent a $2T asset class from exploding, which could lead to a broader crisis.

Of course, Bitcoin is not at $2T yet, but it will be soon based on the current trend line.

Bitcoin crashed from 20K to 7K last time with no crisis.

There will be no crisis even if it were to crash again to 2K, as long as stocks are up.

Now if all markets were to crash together, that would be a different story.

The government will start attacking Bitcoin before it gets to that point. They’ll try to label it a security, or something.

I don’t own any Bitcoin, but I do sympathize with it. Central banks are taking away peoples’ financial freedoms.

Financial freedom is a delusion. Freedom from what? In order for someone to have financial freedom, another person has to pay/work for it.

Can you please explain what does it mean really with everyone having financial freedom? Does that mean no one has to work? Congress will just print 100K for everyone? That’s coming by the way.

MB,

Financial freedom is being able to transact without government restriction and intervention, at prices determined by actual supply and demand.

When I am forced to subsidize somebody else’s home purchase, that takes my freedoms away. When I fund stimulus checks for people who don’t need them, that takes my freedom away.

How many examples do you need in order to understand you are getting fleeced by an intermediaries that are arbitrarily taking from some and giving to others?

Bobber, I think we are discussing about two different things. The commonly accepted definition of financial freedom is this: ”

Financial freedom usually means having enough savings, financial investments, and cash on hand to afford the kind of life we desire for ourselves and our families.”

Also your freedom is not being taken away. Those subsidies don’t come from your tax. We are way past that point. Just look at our national debt.

What rat? The rat that S&P just hit all time high?

J, or “Xi Ping” or “Q” or “Jason19” or “PJY,” or “Mike78” or whatever other alphanumeric combos you’ve been using to post here:

If you had read the article, you would have known that this was about Treasury securities (bonds) and not stocks. It helps to read the article, or at least look at the pictures if you cannot read, before commenting so you don’t have to make a fool of yourself in public.

Oh, and the 10-year yield today 1.08%.

There is a panic in the Real Estate Market purchase, sale, and refinancing here due to the expectation that interest rates will be going up. Vet Admin Real Estate sales and refinance transactions totaled 2,400 for the last month in DC alone. Rates are pegged by the 10 year Treasury note. Usually about 2% above the 10 year rate. I don’t believe the Fed has much control of these long Bond rates. I wonder how much of the QE money is going to buy these long term Treasury bonds? I think I saw a chart a while back.

My, my, my, the Omnipotent / All Knowing Fed is starting to get egg on its exalted face(s). The monthly buying of Treasuries and MBS by the money printing Federal Reserve is currently at ONLY $80 Billion for T’s and $40 Billion for MBS, a drop in the bucket in a sea of quaking DEBT of some $44 Trillion in U.S. obligations of all genre. Hard to move the needle with massive/ record-setting U.S. debt now, with the Governmental AND Corporate levels at all times highs.

Investors have always been the final determiners of Bond Prices, and hence yields, until the Fed decided it knew better than these key players in the allocation via pricing of U.S. capital. The suppressed, distorted, and manipulated yields of today will not last because the landscape is now changing rapidly to one of DEFAULT RISK, CURRENCY RISK (for foreigners holding a Crying George Washington!), and INFLATION RISK. These three horsemen of a Bond Apocalypse are riding in three abreast as in a spaghetti Western (Clint E. no longer rides!).

So it is not only a Fed Sanctioned Inflation Increase that is spooking all those that play on the Bond Railroad Tracks today to literally cover their own tracks of printing endless gobs of Dollars to fund Uncle Handout, but the growing reality that Defaults and Dollar Devaluation are sprouting like Spring flowers across the land. Only a proliferate Congress will be able to attempt to arrest the Government Defaults baked into the cake of an economy that got whacked into negative “growth” territory by mandated Lockdowns of businesses. THE FED WANTS THE DOLLAR TO GO MUCH LOWER IN ITS ATTEMPT TO SERVICE THE DEBT THAT IS ALREADY OUT THERE.

So your homework assignment today, Wolf, (if you accept this mission!) is to present to us eager & very erudite readers the evidence mounting in the jimmied U.S. debt markets that Pandora is out of the box, and the Mad Hatters of the Eccles Building are losing control of the joy stick they use to micromanage the once most self-sufficient economy in the world.

Just an update on corporate debt defaults will do and a recent graph of the Decline of the U.S. Dollar, wallet size, should cover that avenue. Keep a copy in your wallet or purse Fellow Readers to remind yourselves to spend it as quickly as possible, Weimar Style.

Schumer said yesterday for us peons to buckle up, but Betty Davis said it was going to be a very bumpy ride first. Haven’t bought a bond in 20 years.

Oh. 0.1% times ~5 trillion = 5bn. Per year.

Last stimulus package was 2.2 trillion? For until Biding’s inauguration?

Those who bought long bonds last summer are already down 10%. It could get a lot worse. USD is dropping hard, so import costs are rising. Commodities like oil, copper, zinc, lumber, etc. are rocketing higher. That’s going to roll into consumer prices pretty soon.

Housing prices are already up 10-15% YOY, partly reflecting lumber price increases.

They can always hold them 30 years to maturity at which point they’ll get face value :-]

Anybody who bought long term bonds has to have a few loose screws. The risks of a big capital loss are much greater than the minimal interest advantage of bonds of a much shorter maturity. I wouldn’t touch them with a ten foot telephone pole.

Or even just cash.

Commodities along with the broader stock market can nose-dive if the yields keep climbing. I am not buying the reflation trade for various reasons. I think the next few weeks, months will provide clarity on this.

I want to see those Paul Volcker Interest rates back. 18% Mortgage rates and 21% prime. This will give the savers a fair rate of return above the inflation rate, and make debters pay their fair share. No more subsidies for the top 1% or bailouts for Wall Street crooks like in 2008. If the stock market crashes then that’s the risk you take for investing in the casino.

Swamp Creature,

But I’m pretty sure you don’t want to see those inflation rates of that era again, though.

Even with those high inflation rates savers were making a positive return as opposed to today where savers are getting hosed big time.

Inflation is back. Just went to the grocery store and noticed double digit price increases on nearly everything I buy. Especially items which are imported from Europe. The figures on inflation you hear from the mainstream media are just fake economic news. I trust what I see right before my eyes not bull s$it from the government. Gas at the pump just went up 5% overnight. All this money printing will lead to Jimmy Carter era double digit inflation sooner rather than later.

The crooks are moving in for the kill. They have grandma on the plank of risk investments to get some yield. The inflation will drive her out on the plank to the end of the board.

Then……just as she starts to get comfortable…..with the fed screaming that rates will stay low for decades……..the emergency meeting in secret to bring rates up one point in one day…….and strip her of everything.

Meanwhile the fed governors walking around and being interviewed…..I’am shocked….shocked mind you….to learn that runaway inflation is being generated by the economy. Pick out the usual suspects.

I had a really horrifying thought. With all of the “stimulus” that is likely from a Democratic controlled government, GDP will be artificially high this year. But since each new GDP reading sets the baseline for what GDP is “supposed” to be, that means that $1 trillion in stimulus will be necessary every single year to maintain that number, because we can’t have 2022’s GDP number be smaller than 2021’s.

Even during the height of the Obama era government stimulus, we never had a deficit above $1.4 trillion.

What if the deficit needs to be $3 or $4 trillion every year just to maintain the bubble? How hard does this crash?

I don’t think “What if” is really right- it is no longer a question of “if”.

You are totally right. But this has gone on (to a lesser extend) for a few decades. With total debt (both gov and private) constantly increasing, what is seen as “trend”/”full capacity” was always overstated and therefore “growth” keeps missing targets, requiring even more “stimulus”, etc.

Actually, the real capacity now lies below what would have been realistic without the debt buildup, because the inevitable deleveraging of that massive debt will now subtract from growth. Even if deleveraging happens by “inflating away” debt, because inflation also lowers real GDP growth.

So I’m afraid we will keep getting waves of ever greater “stimulus” until the whole thing blows up. After which we will reset to a much lower standard of living.

Slowly lowering the standard of living is happening now, doesn’t require a blow up. Replace that pricey tinned cat food with the new higher-quality hedonisticly adjusted dry cat food.