“Two steps forward, two steps back”: Fed’s new song and dance, no?

By Wolf Richter for WOLF STREET.

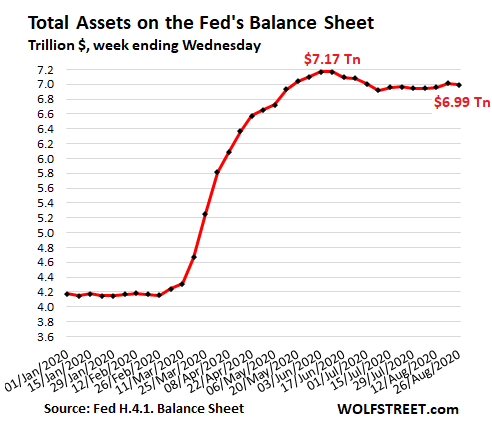

Total assets on the Fed’s balance sheet for the week ended August 26, released this afternoon, fell by $20 billion, to $6.99 trillion, after two weeks in a row of increases, which had followed two weeks in a row of declines, which had followed two weeks in a row of increases, which had followed four weeks in a row of declines. Two steps forward, two steps back — the Fed’s new song and dance? With the effect that total assets are now down by $179 billion from their peak on June 10:

So here’s how that happened by the five major QE-related categories on the Fed’s balance sheet: repos, central bank liquidity swaps, special purpose vehicles (SPVs), mortgage-backed securities (MBS), and Treasury securities.

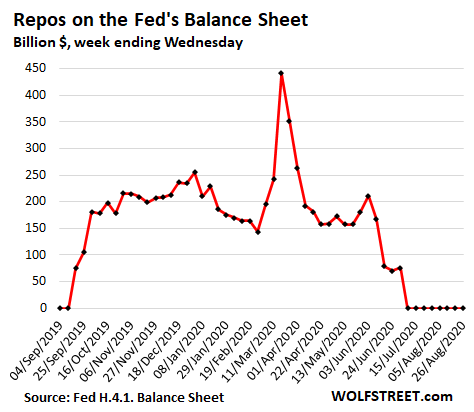

Repurchase Agreements (Repos) remained at zero for the 8th week:

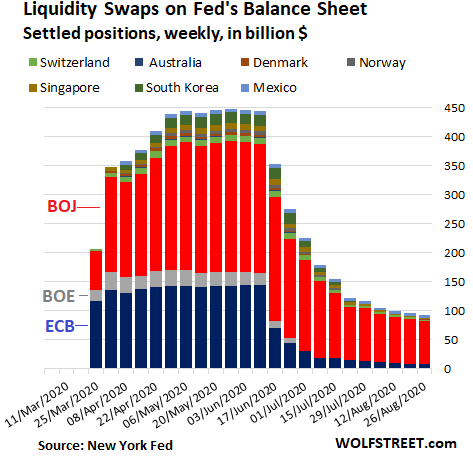

Central-bank dollar liquidity-swaps dropped by $4 billion.

The Fed’s swap lines, by which it provides dollars to certain other central banks, fell by $4 billion to $92 billion, from a peak of $448 billion in early May. The Bank of Japan accounts for 81% ($75 billion) of the total. Swaps with the ECB fell to $7 billion. Swaps with the Bank of Mexico have been unchanged since the beginning of July, at $5 billion. The central banks of Switzerland and Singapore had small balances left. The rest were gone:

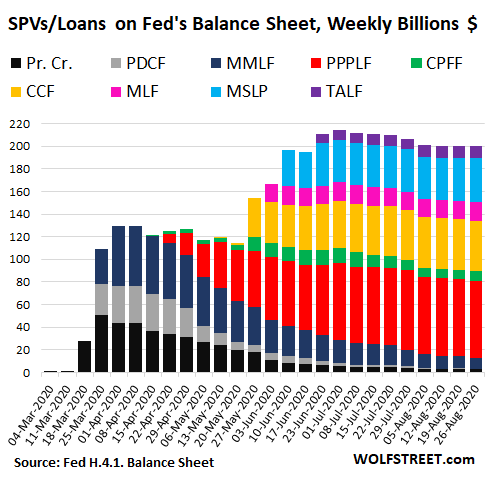

SPVs unchanged at $200 billion, -$14 billion from 8 weeks ago.

The Treasury Department provides the equity capital to these Special Purpose Vehicles (SPVs) and the Fed lends to them. The sum of the two is what the Fed shows on its balance sheet for each SPV. But not much has happened yet after months of hoopla: Most of what we see in these SPVs is the equity capital from the Treasury, and not much lending from the Fed – because these SPVs have barely bought any assets. Here are the SPVs:

- PDCF: Primary Dealer Credit Facility

- MMLF: Money Market Mutual Fund Liquidity Facility

- PPPLF: Paycheck Protection Program Liquidity Facility, with which the Fed buys PPP loans from banks

- CPFF: Commercial Paper Funding Facility

- CCF: Corporate Credit Facilities: Buy corporate bonds, bond ETFs, and corporate loans.

- MSLP: Main Street Lending Program

- MLF: Municipal Liquidity Facility

- TALF: Term Asset-Backed Securities Loan Facility

For example, CCF has only bought $12.3 billion in corporate bond & bond ETFs.

The CCF (Corporate Credit Facilities), yellow in the chart, holds the Fed’s corporate bonds and bond-ETFs. The balance of the CCF has been a notch above $44 billion since mid-July. But in a separate report on August 10, the Fed disclosed that it held only $12 billion in corporate bonds and ETFs at the end of July. The rest was mostly the unused equity capital from the Treasury and some interest income earned on the bonds.

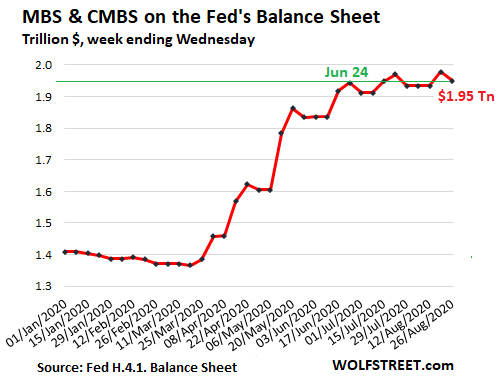

MBS fell by $29 billion to $1.95 trillion, about level with two months ago.

The zigzag shape of the chart tracking the balances of mortgage-backed securities (MBS) is due to two factors that move the balance in opposite directions: Holders of MBS receive pass-through principal payments when mortgages are paid off, which has turned into a torrent in today’s refinance boom. It reduces the MBS balance. And the Fed’s MBS purchases take 1-3 months to settle, which is when the Fed books the trades.

What this shows is that since June 24, the Fed has roughly replaced the pass-through principal payments and nothing more:

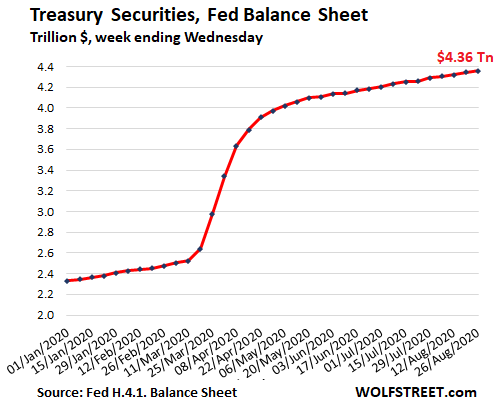

Treasury securities rose by $13 billion to $4.36 trillion.

Since mid-May, the Fed has increased its Treasury holdings in a range between $6 billion and $29 billion a week, following the 10-week period, starting in mid-March, when it had gone hog-wild, buying at the peak $362 billion in the week ended April 1:

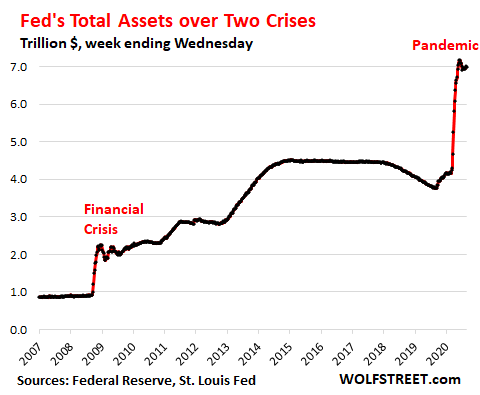

And finally, another crazy chart, to document these crazy times.

The Fed multiplied its total assets since 2008 by 8, from $875 billion to $6.99 trillion:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf…

There is something going on “off the books” IMO.

If the Fed is allowed to deviate off their mandates of stable prices and moderate long term rates..

If the Fed can deviate from their dealing only in federally backed securities..

If the Fed partners up with Blackrock…

anything is in play…including out of sight, off the books maneuvers IMO

When China dumped a large number of Treasuries a young fund manager offered to buy most of it in the secondary market, but first he wanted a private meeting with Bernanke. What would BB say to him, that he had not already said, publicly?? Sure, Fed wanted an audience with him as well. (They like to know who holds their bonds). There are quid pro quos. The sales are made public, you just don’t know the conditions. Fed has gotten more cozy with hedge funds who are short Treasuries. If they can control the clawback in rates, they will provide liquidity and every pig gets fat, none are slaughtered.

I really wish to know more insight into this possibility. Everything in the stock market to me reeks of corruption. I’ve watched the price action pretty closely through this entire rally, including overnight futures, and to me, there’s no other way to explain the activity other than corruption. Basically a team of people with limitless amount of digital money saving EVERY SINGLE micro dip in the markets. It simply makes no sense that any type of big money, especially after hours on low volume (this is not retail traders buying when cash markets are closed) continually buy every micro dip and never sell into any of these declines to lock in profits and look to buy much lower. It makes ZERO sense.

To me, whoever is behind all this unlimited buying power on every pullback, has stopped caring whether it’s obvious and blatant manipulation, because the price action repeats the exact same trends every single time. How many times have we seen the market rally into close at cash day’s highs? How many times have we seen a morning decline followed by a sharp V within minutes or hours, finally with again, a rally to highs of day right at close. How many times have we seen the market rally on low-volume as soon as the cash market closes at 4PM – ALWAYS rallies 10-30 bps in the hour or two that follow. And then always ends up with a massive head start by the time cash market opens at 9:30 so that IF there is any pullback, it is just the manipulated pump that was done overnight, ie. net zero loss.

It’s insane how there are no media stories or any big money that has been blown up short, calling out this suspicious price action. I wouldn’t be surprised if years from now we find out the depths of what went on…

At least things are leveling off, albeit in ping pong fashion.

Hmm. I’d have expected the Fed to start unwinding the extraordinary, barely-legal exotic hedge-fund SPVs. But maybe there’s a strong bias not to do anything between now and November 3, to avoid being accused of biasing the election…

P.S. The monthly H.8 report on commercial bank assets came out last Friday and is also quite interesting. That, together with the Fed’s balance sheet here in this article, should pretty much summarize the formal banking situation in the US. Total bank assets have contracted through June and July. With the crazy annualizations used, some have declined more than “100%” (annualized)… though really not so much. And loss provisioning is surging.

“Hmm. I’d have expected the Fed to start unwinding the extraordinary, barely-legal exotic hedge-fund SPVs.”

No, they will keep that, possibly forever. It makes the “fed-put” explicitly visible, so the jaw-boning is even more effective.

YuShan,

They didn’t keep the SPVs last time either. They sold those securities or let them roll off when they matured, including the hated TALF.

I’m not convinced this time. Remember that in 2008 there was still talk about “moral hazard”? (That’s why they allowed Bear Stearns and Lehman to fail). This time however, there is no such talk and they appear to be actually encouraging moral hazard. To me, this seems to be the whole point of the SPV. They have not been buying all that much, as you yourself have been highlighting on this blog. They just engage in cultivating moral hazard by having the SPV ready should any downtick ever happen and keeping the Fed-put in plain sight. I hope I’m wrong.

YuShan there’s a lot of talk about moral hazard; if you can’t see it you’re not looking. The phraseology has changed since “moral hazard” is out of style now, but the underlying idea is all over the place.

@Wisdom Seeker

Perhaps I’m reading the wrong media then, but I cannot recall anybody in power (Fed, politicians, etc) discussing this in recent months, while this was a very big thing at the start of the GFC. If “moral hazard” is out of style, what is the new phraseology?

YuShan,

I think they renamed “moral hazard.” It’s now called “moral virtue.”

I see Janny Yellen was down in DC, browbeating Congress critters to hand out more bailout money. Have these people no shame? Bet she doesn’t part with a dime for charity, but with the taxpayers money she’s all ink and printers.

I still remember some of the comments from this site that should really belong in the Hall of Fame.

– “The Fed’s trying to torpedo the current administration”

– “The Deep State’s trying to torpedo the current administration”

– “Your favorite villain (insert here) is trying to torpedo the current administration”

In the meanwhile, we are at 7 trillion.

The Fed does not care about you, me or the current administration. It only cares about the rich.

Monkeybusiness:

That’s the only chart I understand…..the “7T” one…….the rest is all Martian…….

Remember what Alan Greenspan said: “I was wrong!”

It’s what they call ‘building a base’, for the push to $15 Trillion. Then $25T not out of sight.

10 trillion by the end of the year for sure.

20 trillion by end of next year.

From now on it will just double every year. Wait till interest rates go sky high.

I remember reading that once the Fed is at zero they have for lack of a better word a cheat sheet that converts quantitative easing to an equivalent drop in interest rates. So expect to see the balance sheet grow and grow every time they need to drop rates but can’t.

Just remember there is reason the long end of the treasury curve is so low. It seems foolish to buy a 10 year or 30 year but it’s big market and it might mean stocks aren’t go to do anything over the next 10 or 20 years.

All this ‘zig-zag’ going no where with no statistical significance to conclude any thing conclusionary! What does it signify for an ordinary investor?Why bother?

Why bother posting your comment? Cant people cover things for information in of in themselves? Or must you need someone to steer your mind for you?

‘TO EACH HIS OWN’

All the best for you and yours!

see my comments below.

The Fed doesn’t do extreme policy unless we are in an extremely bad situation. My opinion for ordinary investor is keep adequate cash, plan for zero returns for next ten years if you are fully invested in stocks, bonds and cash. Don’t let low rates fool you into going out further on risk curve than you would normally go. Try not to make a fatal investing mistake by letting the Fed get you off your normal game.

FED balance sheet is keep inflating decade over decade. The amount is increased at an quadruple fashion and the current ballooning is on going with no end in sight. If you cannot pay down your debt during booming period, how you expect it would somehow reduce during the bad time? Perform new magic and trick the world? I doubt the modern world will buy into it this time around. Something major set to change down the road. Create new $ from left hand and hand over to right hand is officially witness by the world.

‘Create new $ from left hand and hand over to right hand is officially witness by the world’

Yep. You are right!

But where is the OUTRAGE? by the concerned citizens, regulators or MSM!?

Business as usual, next day!

Sunny129:

“Why is there no outrage?”

Because most people have no clue what the FED or Treasury have been up and plan to do into the future!

I commend Mr. Richter (and others) who post these blogs and I take great care to carefully read them and enjoy the comments….but most ordinary Americans would look at this information and get the “Thousand Yard Stare”!

I’ve been “following national and global economics/politics (etc) for more than 60 years and what is going on now is totally “out of whack”!

Many Americans believe that the economy pre-pandemic was the greatest in history. (Personal contact with some)

I personally believe it has been a total disaster since the “Grand Give-Away” beginning in 2009.

“No Pain No Gain” was the former mantra.

Not any more!

Not only do we have a “people opioid crisis”; our whole system is now in a, “opioid” one…….

Wow!

As an aside comment:

Mr Richter:

Just talked to my granddaughter who lives and works in SF…..couple weeks ago she and her roomies tried to re-negotiate their rent (Dolores Park area) and were turned down flat. They just moved to an upscale place up in Corona Park with less rent; their landlord called them yesterday and wanted to talk lessening their rent where they were…..needless to say what their response is/was.

Also have family in business, Santa Clara V.; they tried the same thing last week with office/warehouse. Landlord says, “nothing doing”. They found another smaller but good enough size in a much better area and are moving…..same thing with their landlord trying to re-negotiate too late.

Some “Chickens” are coming home to roost.

I suspect that the month of October is going to be very revealing for the whole nation.

Good luck everyone!

sierra7,

Your granddaughter and her roomies are smart.

We call it a “free upgrade.” If you’re a landlord and you’re trying to keep your units filled, or want to fill your units, you have to make deals. Smart landlords have figured this out. Everyone is talking about these free upgrades now.

@ Sierra 7

I completely agree with you. I have been in the mkt since ’82.

I am now, happily retired with ‘enough’ for my future livelihood. This is the most SURREAL market of my life time! This won’t end well, when (not IF) the inevitale DOWN cycle begins!

The way I see it the economy was ready to roll into a recession when Trump took over. They took a risk by big deficit spending at the end of business cycle and did get total employment looking pretty good, but really it was debt fueled growth.

What’s the problem with deficit spending at end of business cycle? If you have economic shock like the virus you are just going to pile on more a lot more debt which at some unknown point will put us in the doom loop of economic activity.

However, efficiency gains in manufacturing and energy and even in service sectors have allowed for the same capital to produce more. As long as we can keep producing goods and services, debt can balloon. The real problem is when we are only buying and not selling.

Massive injections of liquidity earlier in the year will wear off in due course and wildly distorted junkie markets will be back for more. If they don’t get it credit will seize and a deflationary collapse will begin. The Fed will comply with new and ever greater injections. The Fed isn’t managing the economy they are merely distorting it, in much the same way a substance abuser distorts their state of mind. Cloistered fools at the Fed don’t understand that. The game ends when markets finally lose confidence in increasingly junky currency. Tangible assets offer refuge.

Wonder when the protestors will visit J-Pow? I would not want to be the person responsible for minting billionaires while the bottom 80% struggle daily. Perhaps J-Pow should reduce that $7 Trillion given to Wall Street billionaires by a few trillion over the next few months and give it to the bottom 99% instead?

Protesters set up guillotine in front of Jeff Bezos’ DC home

Of all factors that can be controlled, central bank policies are by far the biggest cause of rising inequality.

Unfortunately, very few people understand how this mechanism works. They know they are getting screwed by the oligarchs, but don’t really understand how. So you see riots (more to come in the future) but they won’t be aimed at central banks.

Also, don’t expect mass media and celebrity economists to educate people on this because we know who owns them. So often I hear/read “liberal” celebrity economists fulminating against inequality but they never touch the elephant in the room.

Yep. That’s why Pelosi said in March that the plummeting stock market was “disturbing.” She’s one of the oligarchs, as is Biden, and anyone who thinks that they’re going to make any changes is deluding himself

This says it ALL

“The much deeper problem for the US economy is the asymmetric impact of Fed policies on households and businesses. The Fed’s monetary and regulatory policies have contributed to a form of capitalism where the rewards are going to the 1% and the risks are borne by the 99%. The current crisis response has made it painfully clear again that the Fed’s policies benefit high income individuals and large corporations, while small businesses and low income individuals bear the burden. While the Fed likes to see itself as part of the solution to America’s economic problems, it should ask itself whether it is also part of these problems.”

–Rabobank’s Philip Marey who in his Fed post-mortem “The Wrong Kind of Symmetry”

h/t ZH

“The Fed’s monetary and regulatory policies have contributed to a form of capitalism”

This is not a “form of capitalism” it is socialism. Wealth distribution is being decided and manipulated by the Fed and the Federal Government.

The country is living under an illusion of capitalism and freedom, neither of which actually exist. We are living under a socialist government with a socialist economy and that will not change until people understand the situation for what it is…

Do you know the level of financial literacy of an average American?

There is no hope there!

This is a CRONY CApitalism where the DEBTS are socialized and the profits are privatized.

Coming class wars (among 10 sub classes)

‘Class wars are the inevitable result of an economic system in which ‘anything goes if you’re rich enough and winners take most’.

Read “America’s Metastasizing Class Wars’ @ oftwominds com

All of this reminds me of what the BOJ and banks in japan were doing in 1989… euphoria was rampant, while quietly (or not so quiet if you were paying attention, lending standards were tightening, BOJ encouraging the government to go more and more in debt… we all know what happens next… Kuroda on now QE 29 while still down over 50% from ATH 30 years later lol

They still seem to have an excellent standard of living? In which case , to play devils advocate, does QE really matter?

Ask someone who had a retirement account all in on the n225 for diversification… look up “Mrs. Watanabe” and ” Japan’s Lost Decade”

The reason that post-1989 birthrates in Japan have been so low is because their overall standard of living isn’t that great. They also have a very high suicide rate, as their working lives have become ever more stressful.

Low wages plus QE-driven high asset prices means workers have no hope of retirement above what the government offers, and they work crazy hours just to afford a tiny room to sleep in.

This is typical Fed, when they are giving out money they use a shovel and when they are taking it back a pair of tweezers. Just like the little increases in interest rates they did in 2018, first sign of panic, and it doesn’t take much to panic their masters on Wall Street, and the fed was all in sending interest rates to zero. Wall Street inspired panic attacks followed by bureaucratic penny counting. Sorry don’t see the significance, different day, same bad management.

Many years ago an Economics professor told us there were three ways to reduce federal debt.

1) increase tax revenues

2) reduce spending

3) monetize debt (print money)

A combination of all three would work as well.

It seems our government is not concerned about debt levels. They’re decreasing tax revenues (by shutting down the economy), increasing spending through trillion dollar giveaways while monetizing the debt (M2 up 20% in 7 months). M2 is now at 18.3T

It’s going to get ugly.

Even if shout at the top of my lungs that exchanging money that yields IOER and stays on bank balance sheets (M2V people ignore all the time) the more they do it, for long term debt is hardly money printing… at best, it is an asset swap… at worse… lol

truely “printing money” wouldn’t require the use of debt… nor would said “money” yield IOER…

You seem to be missing the part where the Fed Gov’s newly monetized “long term debt” translates into cash in the Treasury to spend on whatever Congress votes for and the Executive Branch follows through on…

Yeah, at the expense of there being less cash available for private market participants: banks/primary dealers buy debt that yields from the gov (instead of lending it to anyone else), then sell it jerome, and then get reserves that stay on their balance sheet and yield IOER or buy more treasuries…

Sounds horribly inflationary compared to jerome just conjuring reserves and giving them to the federal government with no increases in federal debt…

Yup… no distinction whatsoever… lol

You don’t lose many votes if you select option #3.

I wonder if markets are finally ready to top…

1. The Fed doesn’t want to do anything major before the election so they aren’t accused of taking sides.

2. It seems increasingly unlikely that any pre-election stimulus will pass. This will look bad in the next 2 months.

3. I watched some of both conventions and there is significant fear being spread by both sides of the other side winning.

This fear will grow to a peak in November, probably before the election but possibly after if we have the uncertainty of a close & disputed result.

Add to that the diverging advance-decline line and waning momentum we’re seeing combined with crazy bullishness on the put/call spreads.

This selloff will likely be a good buying opportunity as the fed will undoubtedly juice markets more by early next year.

I think that to get to a real generational bottom that is worth buying based on value should take years from top to bottom. Everything else is just speculation on even more P/E expansion. Projected investment returns over the next 10 years are extremely low (and likely negative) at current levels of the S&P500.

I can recommend John Hussman’s analysis on this.

John – I concur with your theory. The hard part is where it reverses, and when. The next levels in my opinion will be SP500 at 3638 (+3.7%) by mid September, 3820 (+8.7%) mid October, and 4,011(+13.7%) EOY if we do NOT have a blue trifecta after elections. Without the fed involved, we would have hit 1500-1800 range over 12 long months, with the average 1000 day (3 year) recovery instead of only 100 short days due to fed printing. The fed changed the game, to benefit the top 1% above everyone else. Yet even if we get election volatility, how far would the Fed allow the markets to fall? 10%? 20%? We know 35% was the last limit. The game is rigged, and will seem to work as planned until it falls apart due to unintended consquences in which the top 1% are simply not smart enough to calculate. Yet that could be years or decades from today as the 99% have no clue what is really happening, they just “feel” that the American dream is becoming an American nightmare…

“just speculation” oh you mean modern investment. Ha! I can’t help but think that there has to be at least a 30% market decline at some point. However, I also can’t help but think that there is also some degree of permanency to this stupidity. A 50+% drop returning the stock market to long-term cyclical lows and typical p/e ratios could be very unlikely. Reading Piketty actually convinced me of that to some degree. Historical asset valuations to aggregate income ratios in low growth economies tends to top out at fairly high levels. Since that’s the u.s. now and the rich have grown all the richer beyond the other classes, stocks may stay quite high relative to stock prices over the last century. However there’s still a lot of current speculative excess to blow off.

I loved Tramp’s speech last night:

“I’m going to lower taxes and make sure Medicare and Social Security are well funded.”

Another 5 Trillion in Debt?

Corporate, Government , both State & Federal, and consumer debt has never been higher. And yet, every day I see recommendations to buy stocks and get in on the ride to the top and make money or you’re missing out on getting wealthy. I look at it as the snake oil salesman coming to town to take your money and leave town. No one can say when the top will happen! Next, their will be tons of suckers left holding the bag when the traders owning super computers take the stock market down in one day. The rich will win again, and the rest will be impoverished. This is the height of wealth and greed. I just step back and buy more gold and gold stocks.

The Fed doesn’t know where it is going because it is caught between a rock and a hard place. Reduce interest rates to negative? That’s not working to well with its affect on Treasuries and other bonds. Now they are talking about increasing interest rates to 2% or a little more. The current USA debt will go higher, but the average guy holding CD’s will still get nothing. IT”S ALL ABOUT DEBT! WE CANNOT GO ON AD INFINITUM!

‘Now they are talking about increasing interest rates to 2% or a little more’

NO!

2.0% is the inflation rate they are trying to aim at! The REAL interest rate after considering the current inflation rate (1.5 to 2.0%) is Minus 1.5%!

The Mkt will get seizure if they increase from the current 0.25 to even 1.0%!

The FED is in a bad situation. It has maxed out its balance sheet, and now has little or no ammo left. This is how I see this playing out. There is a crash coming, they are trying desperately to postpone it until after the election, but it is coming.

At present, the FED is following the bond market which is pushing interest rates lower due to massive demand for Treasuries. That demand is only going to last until the crash comes.

When the crash comes and asset prices go into free fall, it will draw money out of Treasuries and into assets as their prices become more in line with their intrinsic value. As the interest in Treasuries declines, the interest rates will have to rise on Treasuries to accommodate the auctions and the governments massive need to finance their out of control debt. The FED will not be able to replace the trillions of dollars flowing out of Treasuries because its balance sheet is already seriously over inflated. In addition, the crash will effect bonds across the board including municipal funds . This all adds up to a major emergency for governments at every level and their need for cash to service their debts in an environment of rising interest rates is going necessitate massive tax increases, and possibly even bail in’s as we saw with gold in the last depression…

“It has maxed out its balance sheet” emmm not sure about that… they can double it and still be miles away from complete destruction of the currency. I’m short, but must admit the epic crash some expects might never get here as along as FED remain shameless.

The balance sheet can go from the 7.1 Trillions to 10 and even 20 Trillions and no one cares until the rate of growth debt exceeds that of GDP aka the interest payment on the national debt, in competition with defense/Medicare/Social services in the annual (recurring deficit!) budget

Even if the Fed’s balance sheet remains stable, it could be argued the level of the balance sheet is very relevant to the current levitation in the stock market.

A bank could continuously buy new agency debt using recurring cash flows, which the Fed continuously buys, adding cash debits to the bank’s reserve accounts at the Fed, which then grow over time. These reserve accounts could then be used to provide loans to leveraged Wall street firms to buy stocks.

Wolf..

something going on off the sheets..out of vision..