Prices fall year-over-year in San Francisco Bay Area & New York condo market. Seattle below June 2018. Chicago nearly flat year-over-year. Other markets lose steam. Phoenix, Tampa, Charlotte surge.

By Wolf Richter for WOLF STREET.

Powered by the innumerable millionaires and multimillionaires that the mega IPOs would be suddenly printing in 2019, home prices in the San Francisco Bay Area would be doomed to surge this year, thus exacerbating the “housing crisis,” as it’s called locally, even further, the media have promised us incessantly earlier this year, having fallen once again for real estate industry hype. Now we got another data point that demolishes this myth.

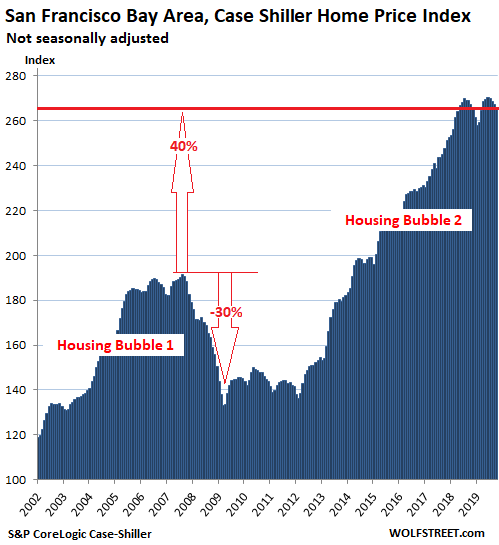

San Francisco Bay Area House Prices

Prices of single-family houses in the five-county San Francisco Bay Area – the counties of San Francisco, San Mateo (northern part of Silicon Valley), Alameda and Contra Costa (East Bay), and Marin (North Bay) – fell 0.4% in October from September and were down 0.4% from the same month a year ago, and were down 1.5% from the peak in June, according to the S&P CoreLogic Case-Shiller Home Price Index released on December 31. This put the index back where it had first been in May 2018. Note the double peak in 2018-2019, and note a similar double-peak in 2006-2008:

The Case-Shiller Index is a rolling three-month average. This release includes closings that were entered into public records in August, September, and October. The index was set at 100 for January 2000. San Francisco’s index value of 266 means prices in the metro have soared 166% since January 2000.

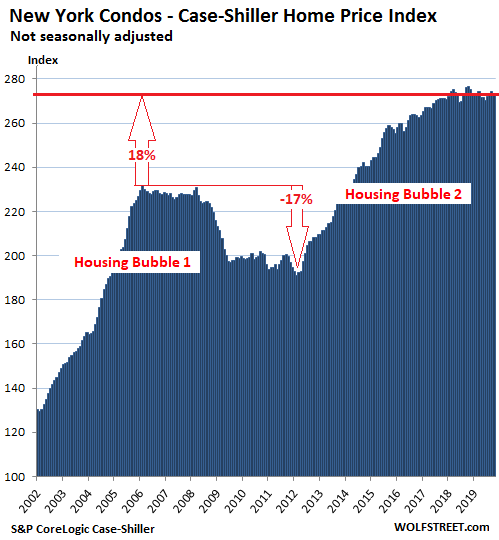

New York Condo Prices:

Condo prices in the vast New York City metro ticked down 0.3% in October from September and were down 1.3% from a year ago, and below where they’d first been in February 2018, and were up only 0.7% from October two years ago.

The Case-Shiller Index, which mostly uses standard Metropolitan Statistical Areas for its city indices, uses a custom area for New York City that includes numerous counties in the states of New York, New Jersey, and Connecticut “with significant populations that commonly commute to New York City for employment purposes.”

All charts in this series are on the same scale, with the vertical axis going from 100 to 290, which has the effect that there is more white space above the curve in markets where house prices have not soared as much as they have in Los Angeles, San Francisco, Seattle, or Miami. These charts show that there is no “national” housing market and no “national” housing bubble, and that all markets are local, with different dynamics, price levels, and price changes, and that the bubbles, where they exist, are local too.

The Case-Shiller Index methodology is based on “sales pairs,” comparing the sales price of a house that sold in the current month to the price of the same house when it sold previously. This method avoids some of the problems other indices have, such as “median price” indices, which are skewed by “mix”; and “average price” indices, which are skewed by a few big outliers.

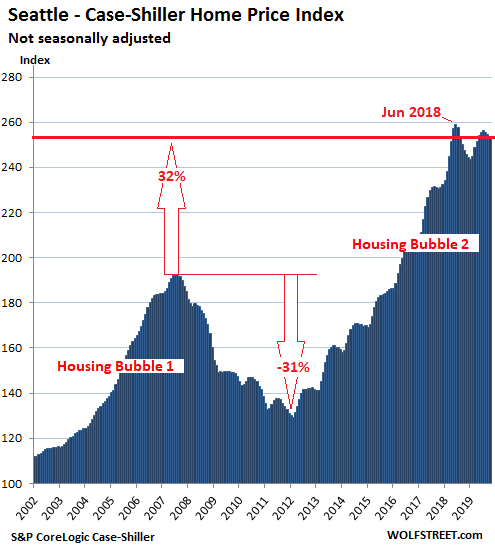

Seattle House Prices:

House prices in the Seattle metro declined 0.3% in October from September, and where down 2.0% from the peak in June 2018. This put them below where they’d first been in May 2018. In a testament to how steep the declines were last year from August through December, and that were followed by a bounce, the index in October 2019 was up 2.5% from a year ago. Note the double peak, with the lower high in June and July 2019:

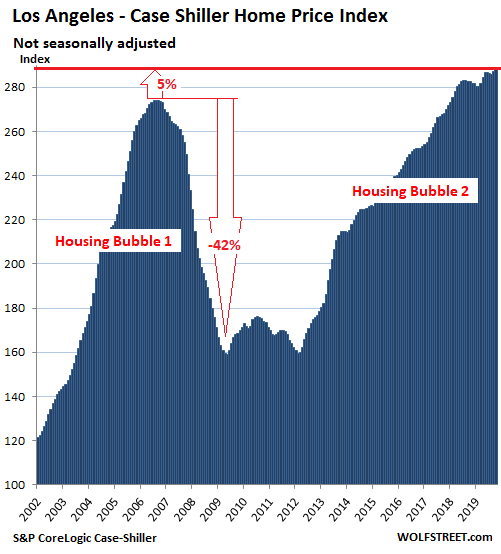

Los Angeles House Prices:

The Los Angeles metro is now the US market where house prices, according to the Case-Shiller Index, have risen the most since January 2000: With the index at 288, house prices are now 188% higher than they were in January 2000. In October, the index rose 0.4% from September and was up 2.0% year-over-year:

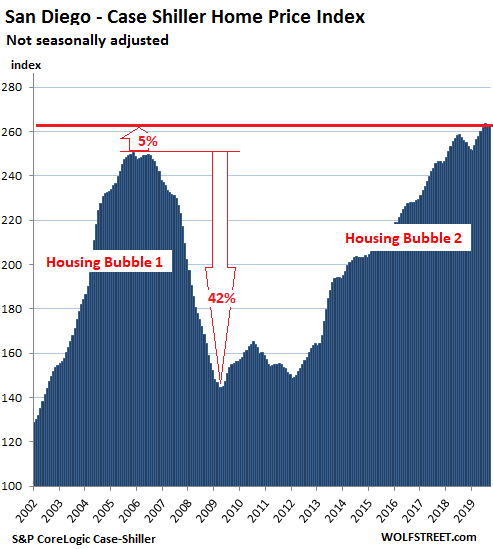

San Diego House Prices:

House prices in the San Diego metro edged down 0.2% in October from September and were essentially flat for the past five months. They’re up 2.9% year-over-year:

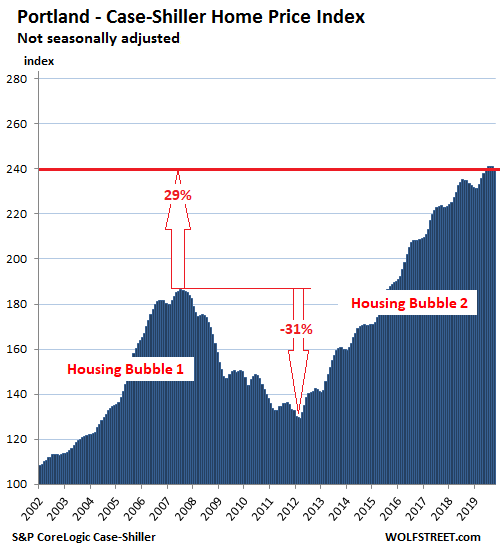

Portland House Prices:

House prices in the Portland metro fell 0.5% in October from September but were up 2.7% year-over-year. The index has been essentially flat for the past five months. At 240, the index is up 140% from January 2000:

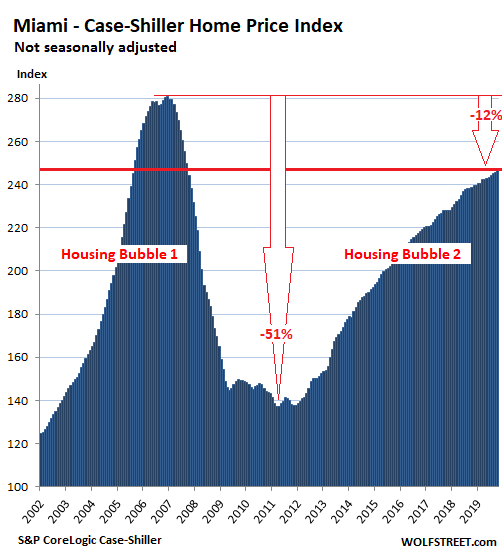

Miami House Prices:

The Case-Shiller index for the Miami metro rose 0.3% in October from September and 3.3% year-over-year, but remains down 12% from the most splendid craziness at the end of 2006:

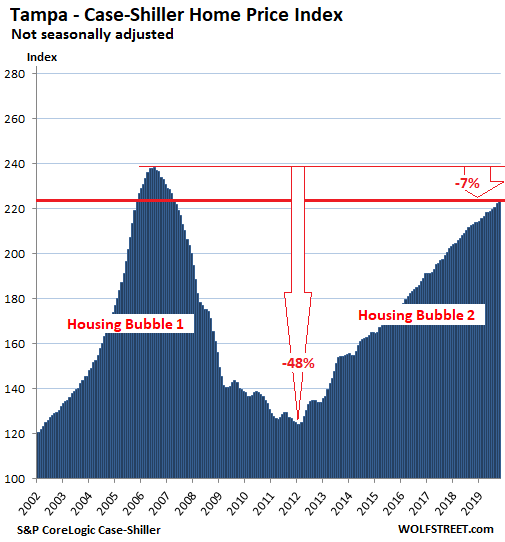

Tampa House Prices:

House prices in the Tampa metro rose 0.6% in October from September and were up 4.9% year-over-year, the second largest year-over-year increase of the metros in this series, behind Phoenix (+5.9%). The index is closing in on the craziness in 2006:

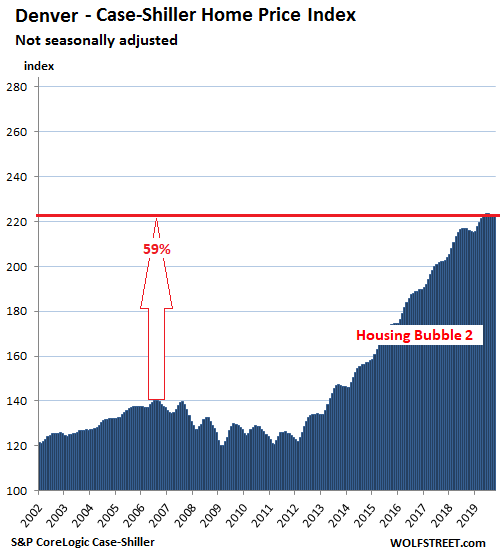

Denver House Prices:

House prices in the Denver metro remained essentially flat in October for the fifth month in a row (down a smidgen from June), but were up 3.0% year-over-year:

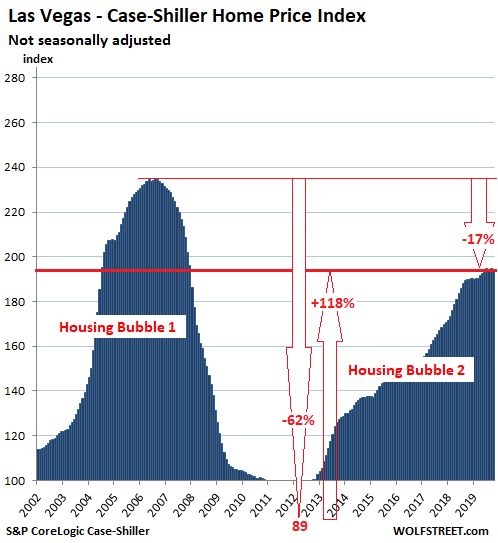

Las Vegas House Prices:

The Case-Shiller index for the Las Vegas metro ticked down in October from September and was roughly flat for the past four months. This whittled down the year-over-year gain to 2.3%, the smallest such gain since August 2012, when prices began to emerge from the collapse. House prices have skyrocketed 118% since March 2012:

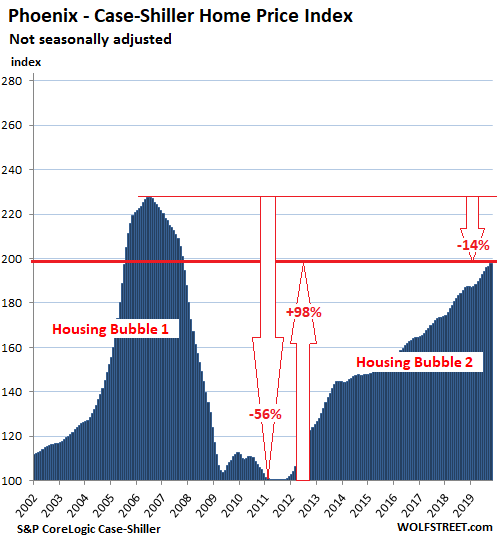

Phoenix House Prices:

House prices in the Phoenix metro rose 0.5% in October from September and were up 5.8% from October last year, the fastest year-over-year growth among the metros. And it’s closing in on the craziness of 2006. House price have nearly doubled in the eight years since September 2011:

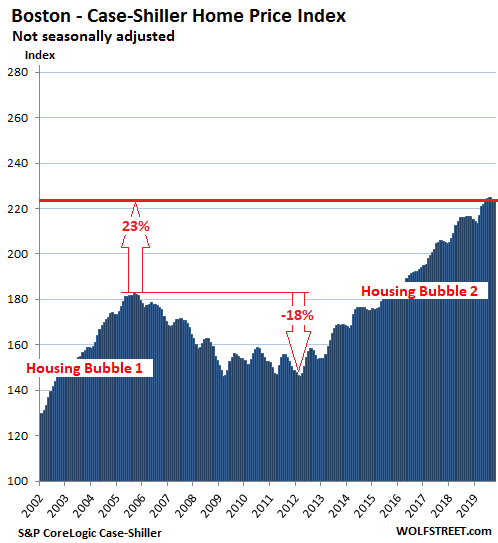

Boston House Prices:

House prices in the Boston metro were flat in October compared to September, and were down a tad from June, which trimmed their year-over-year gain to 3.4%:

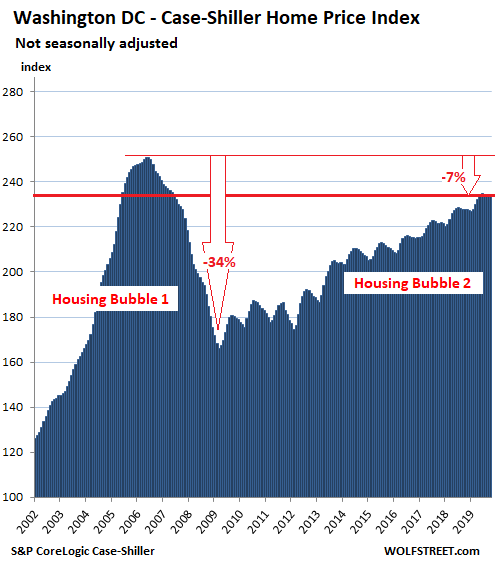

Washington DC:

House prices in the Washington D.C. metro ticked up 0.3% in October from September and were essentially flat for the past five months, but were up 3.0% year-over-year:

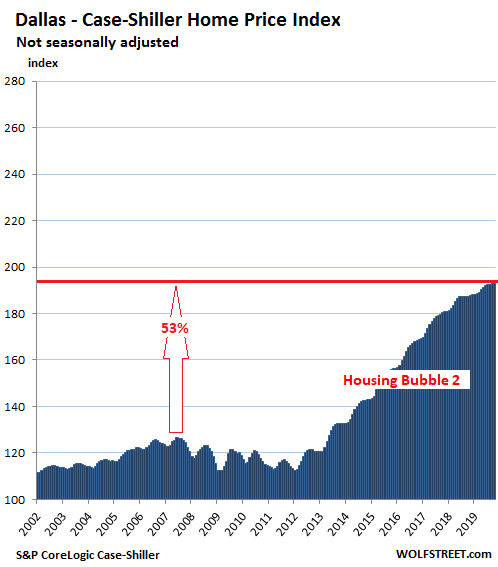

Dallas-Fort Worth House Prices:

In the Dallas-Fort Worth metro – counties of Collin, Dallas, Delta, Denton, Ellis, Hunt, Johnson, Kaufman, Parker, Rockwall, Tarrant, and Wise – house prices ticked down a smidgen in October from September, and have been about flat for the last four months. This whittled down the year-over-year gain to 2.9%:

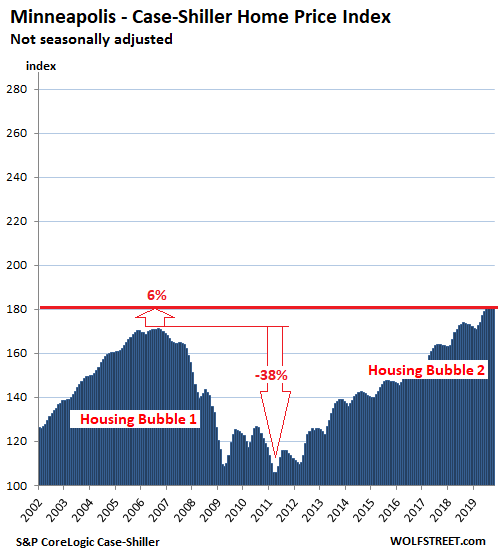

Minneapolis house prices:

In the Minneapolis metro, house prices dipped 0.2% in October from September and have been flat for the past four months. On a year-over-year basis, prices rose 4.2%:

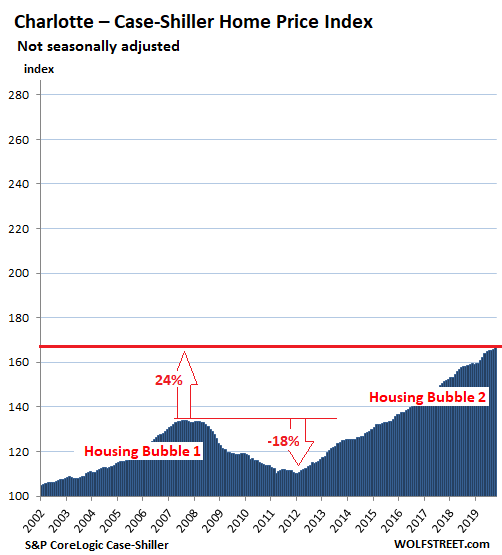

Charlotte house prices:

House prices in the Charlotte metro rose 0.4% in October from September, which increased their year-over-year gain to 4.8%, the third highest gain on this splendid list, behind Phoenix and Tampa:

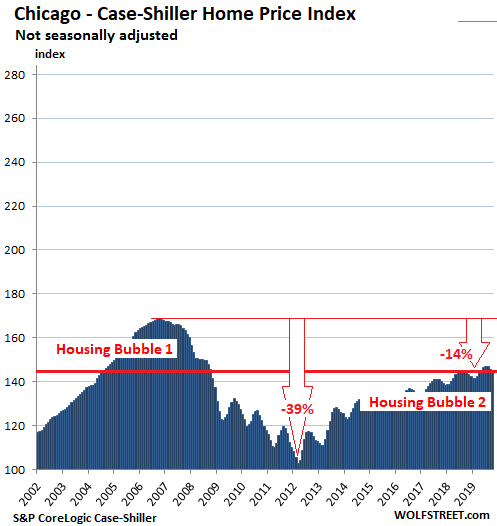

Chicago House Prices:

In the Chicago metro – the counties of Cook, DeKalb, Du Page, Grundy, Kane, Kendal, McHenry, and Will – house prices fell 0.4% in October from September, whittling down the year-over-year gain to just 0.5%:

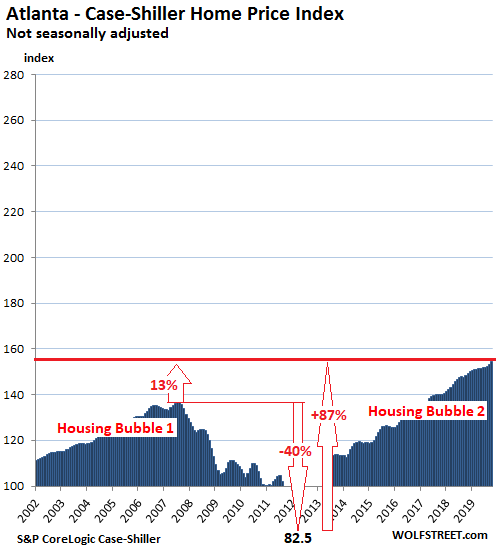

Atlanta house prices:

The Case-Shiller Index for the Atlanta metro jumped 0.7% in October from September and rose 4.1% year-over-year. Note that during Housing Bust 1, the index had plunged 40% to a value of 82.5 in March 2012, back where it had been in 1996, but in the 7.5 years since then, it has surged 87%, including at year-over-year rates ranging from 10% to 20% in all of 2013 and through mid-2014:

This is house price inflation.

The Case-Shiller Index, by comparing the sales price of a house in the current month to the price of the same house when it sold previously, tracks how many more dollars it takes to buy the same house over time, thus tracking the purchasing power of the dollar with regards to houses in various markets. This makes the index a measure of local “house-price inflation.” When the index shows that prices in Los Angeles shot up 188% in 19 years, despite the plunge in the middle, it doesn’t mean that houses have nearly tripled in size or opulence, but that in that metro, the dollar’s purchasing power with regards to houses has gotten crushed.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Fantastic!!! Now, let’s pump it up a little more for the next 5 years. The biggest and greatest housing appreciation in modern times all Thanks to our Lord Donald Trump.

After Trump regime, apocalyptic debt slaves.

But no worries, Debt will be erased for those joining the war. In the end, with debt comes leverage.

Does your TDS make your eyes unable to comprehend the plethora of charts above?

The current housing bubble started in 2012. Accelerated through 2016. And is leveling off through 2019.

And, amazingly, corresponds nearly directly with interest rates and QE policies in those periods.

The one consolation of your ideology is that it will prevent you from ever realising that it is destined to be your undoing and that of countless others. You know not what you do and never will. In the meantime you can trust him to bring those housing bubbles down while blaming his methodology on your adversaries. HRC would at least have been survivable.

Un-something,

Multiple administrations/congresses of both parties have been running the ZIRP scam since 2002-2003.

The “two” parties are really just two well heeled, polished mafias battling over the protection racket money from the other 320 million of us.

They pretend to have ideologies other than utter self interest in order to preserve their power by playing us off against one another.

The power of the near infinite printing press will never be yielded without a near endless ocean of lies.

To be sure, both parties are terribly venal, but the similarities end there. The differences between them are crucial, and you do yourself, your compatriots, and your country a grave disservice by failing to distinguish between them and to recognise those differences for what they are, how they affect you, and what you can do about them. I have no interest in debating the fine points of whatever political course you prefer to compass your ruin.

HRC’s wars would at least have been survivable?

Seriously?

“Why some of the Smartest Progressives I know will Vote Trump over Hillary” by Naked Capitalism.

Let’s do what we wanted to do 3 years ago, before Hillary (not Russia) stole the nomination from him:

Elect President Bernie Sanders

It’s not a presidential phenomenon it’s just monetary event(s).

The massive late-2008-2009 save-the-world flood of money reinflated ALL markets resulting in the 2012+ housing market re-inflation. It takes a while to work through; thus the debate on when the bubble ends.

The ‘printing’ of all this money can be debated forever but has been a recurring event throughout history, particularly since 1913 which resulted in inflation and then collapse in 1921. But the first bubble and crash (and scandal) occurred a year after Hamilton’s Bank of the United States fiasco, 1792, and many times since. The Federalists did win, regardless of party affiliation.

The dream of all governments is to create money from nothing and define its value, and the recurrent results are intermediate prosperity and periodic disaster. It will always be. Meanwhile, either capitalize on it, or go broke in the mania; your choice.

@timbers

Great article from Yves Smith. I’ve always liked her blog.

Thanks for the alert.

Don’t know about DuDu, but yeah, I’m so blinded by my T Disgust syndrome I do fail to comprehend all the wonderful things he alone has accomplished for all of us. Maybe a med will be invented to help out lost souls like me?

I’ve always heard that “real estate is local”. So, it was somewhat fascinating (to me at least), that in every single chart above the bottom and new trend up-words, in every single city shown, started at EXACTLY the same time! The end of 2012/beginning of 2013.

So, I went back and compared the Fed Funds rate and the Freddie Mac Average Mortgage rate charts during that period. They were not correlated at all, in fact, mortgage rates were actually rising at the same time the new housing bubble was starting in early 2013.

Can we talk about this instead of Trump? He’s a train wreck, HRC is cancer. 2 parties at the wheel, but people wanna blame only one? Genius. Moving on…

The recurring indication seems to be that the bubbles are (freshly printed) money desperately seeking returns. That is independent of mortgage rates at the levels they’ve been at, rising or not.

Trump 2024! Two terms is not enough. The new Supreme Court will concur, and ensure this. Then comes Don Jr.

This will ensure MAGA into eternity!

You have made me feel truly blessed. Thank God for this great family!

Is that a joke? Trump is the last nail in the coffin.

First, you cannot blame Trump for the new housing bubbles. Blame the ultra-low interest rates.

Second, it must be said that all house-price indices have one problem in common: home improvements (as opposed to maintenance) give the indices a slight upward bias.

No offence, and I apologize to everyone. Both parties are responsible, but Trump seems to put more fuel on the fire. In my opinion, he only cares on short term (his presidential term) which is not good.

Trump is like a bad grandpa that gives candies to be liked.

I severely doubt that upward bias: most “improvements” are useless or even counterproductive down the line. Just think of all the expensive improvements from the nineties that had very little lasting value later on like ISDN lines, ethernet networks, granite countertops and all kinds of other bathroom/kitchen applicances that were out of fashion some years later.

The Dutch “Herengracht index” (on which much of Shiller’s work about house prices is based) shows that it is perfectly normal for home prices to track income/inflation, although with fluctuations due to good and bad times; there is no real appreciation in the long run despite having to spend money on upkeep and sometimes on taxes. The last 30-50 years (depending on country) are the exception to the rule thanks to the grand central banking experiment with unlimited fiat money and debt.

Ethernet networks have no lasting value? What do you think this blog runs on?

My apologies to everyone. Dudu’s comment somehow got through. And it being the first comment, it is now derailing the comment section into political squabbling. That’s what happens when I fail to do my job for brief periods.

My apologies Wolf, and everyone! I will keep the comments related to the article on future posts.

My intent was not to blame or take sides.

Cheers!

Thanks!

Thanks, Wolf. I enjoy your blog and I even read the comments because they tend to be intelligent. I’ve followed some other blogs (Dr. Housing Bubble and thehousingbubbleblog come to mind) that started out that way, and over time the comment sections gradually descended into nonstop stupidity. Your blog and Nakedcapitalism (your posts there being how I found out about this site) are two that remain readable, but it’s gotta require constant maintenance on your part and I appreciate the work.

If I’m not mistaken, Japan is the country with the longest running period of ZIRP…So I’m curious if real estate market crashes have happened in Japan during the period of ZIRP? I can’t seem to find info on it.

It seems like ZIRP/NIRP puts a floor (at least a pretty solid one) under real estate. It seems like the most likley place to allocate capital when you millions (or billions) to place and aren’t chasing big returns.

Curious what the brilliant people on here think.

“seems like ZIRP/NIRP puts a floor (at least a pretty solid one) under real estate.”

Everything may be ok until rates are ever allowed to even twitch upwards towards truth -then you get a massive asset value/housing implosion (because the ZIRP inflated prices are utterly unaffordable under even slightly higher rates – because real salaries have stagnated or worse).

See the 2008-9 implosion – small hikes had started in 2006 (getting nowhere near historic norms) and within two years had triggered the implosion of trillions of ZIRP driven bullshit loans.

And the Fall 2017-2018 hike of MTG rates from 4 to 5 caused a 15 pct fall in CA home sales (as a 2 to 3 hike in 10 yr Treasuries triggered a 20 pct collapse in stock values).

DC has steered the country into the Dead Zone.

Some day rates will have to increase because alternatives around the world will yield 2 to 3 times more in yield for comparable risk – draining true capital from the US.

The Fed will print more to make up the difference but more and more productive capacity/legit assets will exist outside the Dominion of the dollar (with its history of debauchery). China will have/has more productive capacity and a less fraudulent currency.

So all the Fed printing will yield is wildfire inflation. There is no free lunch and DC’s empire of bullshit isn’t magic – it is just as*holery.

People like to point to absence of US inflation (ignoring many categories of prices…and the Fed confiscated price cuts – vilified as deflation

– that would have been the US consumer’s had the Fed not operated to defeat them)

SiliconValleySkeptic,

To answer your question: “So I’m curious if real estate market crashes have happened in Japan during the period of ZIRP? I can’t seem to find info on it.”

So here is some info on it: Tokyo housing prices started falling (sharply) in the early 1990s and fell more or less straight through 2013/14 when they hit bottom. In smaller towns away from the big cities, prices continue to fall to this day. This has been one of the hugest stories in global real estate. During this time, home prices in Tokyo fell from the most overpriced in the world to one of the cheaper ones among top cities.

And it happened despite ZIRP.

It also imploded the Japanese banking system along the way, which has received a long series of bailouts. The Japanese bank share index TOPIX Banks is still down 80% from Jan 1990!

Worth noting that Japan has an ageing (30%% over 65) and shrinking population not unlike parts of the US and Europe. This is going to create lots of vacant property in the years ahead.

Might not affect Tokyo or other major cities right away but eventually it will. There will be no one to buy real estate at the current valuations.

Already in America’s underclass ruled cities one can buy what was once luxury housing at 1960’s prices if one is brave enough to live there. I suspect the big problem for the children of today will not be ‘affordable’ housing but ‘safe’ housing.

Unit472

Astute observation:

“… I suspect the big problem for the children of today will not be ‘affordable’ housing but ‘safe’ housing…”

As a Midwest inner city real estate investor, I could not agree more. I buy houses at $30K (less than what they were 60 years ago) and fix them up so they are worth “a little more” than they were brand new. No value appreciation whatsoever. Were it not for the ability to charge 3X what the rent would have been 60 years ago, the real estate is worthless due to security concerns and zero appreciation.

Japan’s ageing population is a story in itself. Usually a declining birthrate signals a loss of hope for the future. The declining birthrate is also happening in the U.S. If it weren’t for the optimism of Wolf’s readers I’m afraid I’d be overwhelmed by the pessimism of my fellow workers. Happy New Year everyone!

They are already giving away free houses in many outer areas in Japan in an effort to repopulate. You just have to commit to live there.

Thanks for taking the time to respond, Wolf! Truly appreciate your writing and research!

Re the apparent “success” of ZIRP in Japan:

Japanese cities are well occupied, but there are thousands of towns and villages that are now ghost towns. As in zero residents. The young moved to cities because they couldn’t find a job or a mate in their village. The old moved on to the next world. Ergo, villages became ghost towns

Failing demographics may be the story (or they couldn’t afford big families in their credit bubble?) … but whether demographics are cause or effect, ZIRP is not helping Japan at all.

ZIRP has not worked anywhere, and that was obvious more than a decade before bernanke’s failed experiment… obvious to any true scholar who bothered to look anyway

On a per capita GDP basis, Japan has been doing quite well. If the assets are smaller, but the population is even smaller, everyone left actually has more for themselves. Which group is better to be in: share $1,000,000 among 5 people or share $600,000 between two people? Yes, $1,000,000 and 5 are bigger, but not necessarily better.

It doesn’t matter if you have 600k or 1mm, if there are fewer (in some cases zero) vendors supplying what you want to buy. One person in your example has 400k more in useless trash because he can’t buy what does not exist.

Central planners (that is what the hucksters at fed are) can print currency, but they can’t print products and services.

ZIRP was a mistake brought to life by academic arrogance. It’s easy to balance a budget if you always raise tuition 3-4x inflation and then blame the student debt crisis on anonymous forces. No student debt would be needed if college didn’t overcharge for a shoddy product. Yup, the student debt bubble is irrefutable evidence that college is overpriced.

Yes, I know that questioning the great and powerful professors goes against church dogma. But the student debt bubble shows the professor is wrong.

And ZIRP proves Keynes was wrong, no matter how many tuition busting quacks indoctrinate their students with Keynes rubbish.

Japan has a declining population. People are dying creating housing vacancies. An isolated mountain hamlet was abandoned as people moved closer to town. Commuting long distances is not efficient.

I am NOT brilliant, but following is what I think. The difference between Japan and US is NOT economics. It is guns. Japan needs protection from US, so when the G5 gets together and agree that one of the country need to strengthen exchange rate while weakening others, the sucker has to be Japan in the Plaza Accord. US can be in the same economic situation as Japan but US can use carriers around the world and say do what I tell you to do economically or you will get hurt. This is where US is different from Japan, and this is the difference between Japan and China. US does NOT have enough fire power to tell China what to do.

I think the analysis should NOT be economic or demographic, rather, goes deep down to the geopolitical power, AKA, military organized violence power.

Have lived in Japan during the great bubble of the late 80s when the land around the Imperial Palace briefly was worth more than all the real estate in California.

The biggest issue there as opposed to hear is a disastrously low birthrate, lower than any other country except I believe South Korea and maybe Malta?

And no real immigration.

The US has a birthrate about twice as high and has always had significant immigration. Japan is in a very long decline and is already a shadow of what it was economically on the global stage in 1989.

But it is a wonderful country to visit and very close to my heart

– A LOT OF (if not ALL) people need credit to buy a house. And take out a mortgage.

– But one also have to factor in demographic developments. The age group that is the most likely to buy a house or move to a larger house was the largest in the (late) 1980s (for Japan). Hence the japanese real estate bubble of the late 1980s.

– Similar story for us here in the US (between say 1995 and 2006)

– Similar story for South Korea right now (2015 and say 2020 (??))

Chicago is doing amazing considering the acceleration of the exodus of productive folks from the long time dem control (70+ years) of ever increasing taxes and crushing regulatory burdens in this people’s workers republic paradise.

A thinly-disguised creeping corporate totalitarianism is neither a peoples’ republic nor a workers paradise. It just looks that way to you in the gas light.

If by corporation, you mean gov.inc, then yes this describes the situation of Chicago. And Ill.

No complaints here. Residents fleeing from Ill. have created a very nice backlog for our business. Will keep the excavation equipment going until winter finally shuts us down.

Stop it, you two. Don’t make me stop the car.

Team Blue and Team Red are not opponents; they’re rivals They compete for the right to serve our oligarchs*, and to accrue favors therefrom.

Rooting for the either team is like rooting for the Harlem Globetrotters or the Washington Generals.

“The smart way to keep people passive and obedient is to strictly limit the spectrum of acceptable opinion, but allow very lively debate within that spectrum….” – Chomsky.

“It’s a big club, and you ain’t in it.” – Carlin

*Wall St and the big dogs in the FIRE sector, the military-industrial complex, chemical mfrs, resource extractors, et al. .

“A system founded on genocide and slavery”

Do you bring this point up about the numerous not so indigenous Americans and the Africans who enslaved southern Spain and parts of Italy, or do you tend to stay on script and only decry the acts of European founded states.

The 1960’s called. They want their anti-Anerican revisionist history backed.

Suit yourself, Mr. Rogers. It’s up to you how to rationalise the loss of your chattels.

Excellent comment, two beers. And when someone gets out of line, they get brought down one way or another. They bring themselves down. I’m just finishing off the book, ‘The Irishman’. Not a bad read, but it reminded me of past fixed elections and what happens to leaders when they paint outside the lines and forget who put them in ‘power’.

It’s always about money and the power it brings. Taking Chomsky’s comment into today, I think of all the nonsense and time wasted by people posting on Facebook and other platforms. (mentioned by a guy who doesn’t even know how to turn them on). Regardless, it keeps people talking, occupied with trivia, and dumbed down with false choices, electronics, and the right to consume drugs coming to a State/Country near you. As long as the hamsters on the wheel get off once in awhile and buy stuff, all good. Apparently.

As for the article, it works for individuals to purchase housing and live in a declining area as long as one develops marketable skills that are needed. You might have to work away once in awhile, even on a regular schedule, but it beats the hamster wheel of never getting ahead. I live in such an area. The funny thing is that our declining valley has now attracted young families and folks with cash. Many work away and earn a very good salary.

One can only hope they found the true freedom they so rightfully deserve elsewhere.

Chicago is a tale of two cities. Downtown and river north and a few other neighborhoods surging with wealthy move ins, everywhere else in decline. Government debt there will require bankruptcy in short order. I love Chicago but taxes will have to elevate to catastrophic levels to pay their pension obligations. Owning property there will probably not be a sound long term investment.

Read of facade pieces falling off a New York building and has the inspectors out in force.

Wondered how many other cities have the same problem.

This will definitely effect buyers of older condos.

This will definitely effect buyers of older condos.

If the buyers of older condos are careful and agile they could mostly avoid being affected at all, except for having had a close call.

Met a guy in Detroit once and his son was a building surveyor. Me living in a town with one 5 story building, says what is that? Evidently certain cities require a licensed person to physically inspect side of tall buildings from top to bottom to make sure they are not safety hazards. I think he said it was required one a year.

Let me know when the everything bubble is over. These charts don’t show any evidence of that.

Let me know when the everything bubble is over.

Alas, we may never see you again.

“They fly so high, nearly reach the sky

Then like my dreams they fade and die

Fortune’s always hiding

I’ve looked everywhere”

Housing prices in California maybe colliding with other ‘issues’. I’ve read that fire insurance cannot be cancelled for one year in areas that were declared ‘fire emergency areas’ last year but if that is all its a bit like saying wind insurance can’t be cancelled in Mexico Beach, Florida ( population 1200) but Miami is exempt!

Then there is auto insurance. Car breakins in San Francisco were already out of control but with the new DA refusing to prosecute unless the owner can ‘prove’ the car was locked its going to be open season on your car windows. Auto insurance maybe a picayune expense compared to a mortgage but it was already about $500 more per year in California than in other states and more in San Francisco and LA. Toss in the expected $500 deductible for annual car window repair and even higher rates to come and it adds up.

Then there are the looming black outs and utility rate hikes to say nothing of spending days and weeks in choking smoke. Got to believe, if Berkeley won’t allow you to have a gas stove in your kitchen, the state air quality folks aren’t going to allow you to run a generator for back up power and good luck with your solar panels when the sky is thick with smoke or you are under a mandatory evacuation order.

I have lived in CA since age 6, so my ability to suffer living here is beyond your comprehension. Weep not for me, and be grateful you are not here.

But I was.

Don’t know how old you are but I lived in San Francisco from 1966 to 1988 and in the REAL San Francisco. 2814th Clay St. then at a Maybach house at 2015 Pacific Ave.

Look them up! Doubt you could afford them. Then, as an adult I lived in San Rafael and Sausalito. What piece of the Bay Area do you occupy/

All around Haight St. 66-67, but mostly lived in Mendo and Sonoma countys. Glad you escaped, don’t know if even I could handle Marin.

I’m sure I’ll manage to tough it out somehow. :-))))))

PS: there are lots of things I “can’t afford”….so what?

Not allowed a gas stove!! Sorry but I had to look that one up & verify it.

I’m guessing they would prosecute that offense.

What? No wood stoves? :-) hey, my folks bailed out of Walnut Creek CA the summer of ’68. My dad walked away from his business, a nice rancher with a pool and olive/fruit orchard, and the riots and unrest. We’ve never looked back. Long time CA folks will remember the riots and threats of the ’60s. I do, even though I was just 12 the day we left. One day around 1967 my folks had enough. It took them a year to get out and I was instructed to say we were moving to the Pacific NW, (Seattle) because some of my folk’s friends were pretty strident about that old Domino Red Theory. We hit Seattle that Aug and kept going to the border, arriving as accepted landed immigrants.

You know what I noticed as a kid? No Pledge of Allegiance at school. Rugby instead of football. Hockey. And after I had the required fist fights under my belt and behind me, great friends who never even thought about the military, or being drafted. It seemed normal, actually. No wars and no one cared if you were white, native, east asian, whatever. It just wasn’t thought of. I will say this, there were always a few fights. You move to a logging town from the Bay Area and you had better be prepared to stand your ground a few times. All good.

Governments tend to be big and clumsy. Inflate housing so much that it’s not rational for first time home buyers and the the gray market for shelter will blossom. Shelter is low tech. Many ways to have it and many places.

I had a thought on people living on the street as well. Most people do it because it is a choice. If they go to shelter they are going to have to follow rules like in school. Most adults do not want that. Maybe just say then living on the street is price of freedom. It’s the low cost solution. If you really want to clean them up and provide all services society is going to spend probably a $50,000 -$200,000 per year per person to do it. Better off spending money on children than someone that does not want help.

I have some experience here. Many people on street have family and have already burned through their family’s kindness and love. Many are addicts that have rejected family’s attempt to help. It is sad situation, but as we get older it gets really hard to change our behavior. I do have sympathy for vets as Uncle Sam does owe them excellent care.

I’m a Viet vet, and I have always felt the VA should be a full blown part of our total military. Kind of a “you break it you fix it” normal Pentagon National Defense budget expense.

Makes a lot more sense than a “Space Force”…..or “Star Wars defense”, by a similar self styled “visionary”.

I am in San Diego. IN my neighborhood, the home are on an average 1 mil USD. But the neighborhood streets are clogged with cars parked on the street meaning a 3 bedroom home is housing may be 6-7 adults…

here goes our quality of life and it is worsening..

I was a UPS driver in So Cal and you could tell those neighborhoods by the fact that there was no place to put my Brown truck. Got out of there to Idaho. Good luck. San Diego County was pretty nice in the early 80’s. Not so much now.

Kids are in high school

I intend to bail out on CA as soon as they are done

‘When the index shows that prices in Los Angeles shot up 188% in 19 years, despite the plunge in the middle, it doesn’t mean that houses have nearly tripled in size or opulence, but that in that metro, the dollar’s purchasing power with regards to houses has gotten crushed.’

It almost sounds as if investors are including a currency crash into the value of real estate.

The World dumping the SWIFT payments system because it is an instrument of US foreign policy and punishment could start the ball rolling.

The swift system was built on confidence with recourse and a history of integrity. The new payment system China, Russia, Brazil, and Iran are now launching will collapse in no time from all the cheating these guys will pull on each other. I doubt it will last 18 months.

At first they will blame problems on the infrastructure not being mature enough, then one of them will get kicked out for outright fraud. Then another and another until there are no more kids to play with in the sand box.

I hope you’re correct. I doubt you’re correct.

It is obvious to me that much of Europe sees the need of an alternative to SWIFT that is outside US control, because of the outrageous US extortion and spying policies with respect to SWIFT in the last few years. That says a lot, because most EU politicians are totally clueless when it comes to US influence on EU politics and finance/economy.

Maybe SWIFT only worked for so long because all these countries were under total control from the US all the time. I agree that the new China/Russia payment system may not be smooth sailing, but if they can show that it works well for some time I expect many others joining them – it could be a very nice complement to the Chinese “New Silk Road” project.

Collapse because cheaters. That part made me chuckle. The current systems in place are full of scammers and cheaters, both systems would collapse if cheating was punished.

Quite right Petunia: AOROL – absence of the rule of law is why the pretensions of the Iranians, Russians and Chinese, etc, are mostly nonsense.

But, as in all things, we shall see: this might apply less to a payment system than to, say, actually doing business or owning property in such places.

Even thieves may show some honour when it suits them to do so, and the political manipulation of Swift is too crude and irksome for too many parties.

I would agree the swift system has been a tool of politics since its inception, maybe to its detriment. It is actually better than the blockchain for tracking where the money goes. As for the alternate payment system, I’ll only say I’d rather use bitcoin and I think bitcoin is a scam.

I usually agree with Petunia, but in this case it is wishful thinking. Unfortunately the US has weaponized what was once an international payment settlement system. The number of countries desiring an independent alternative system far exceeds “China, Russia, Brazil, and Iran.”

If New York and SF get rejected at the top for a 3rd year in a row in 2020 and can’t break out I predict the bubble will start deflating by this time next year.

Here’s the steps of a housing bubble (or any bubble for that matter).

1. There is an appearance of a lack of inventory so prices go up for a while

2. Prices form a top and stop going up, causing a chain reaction of events

3. Sellers de-list their inventory figuring they’ll wait to list it once prices go up again. Because this inventory is unlisted, everyone still thinks there’s an appearance of scarcity in the market – “surely I’m the only smart one waiting to list, there can’t be others like me”

4. Buying dries up after a top is formed for 2 of 3 years. Buyers don’t feel a need to rush like they used to because prices are flat, they can take their time and wait for a deal

5. Some sellers start to crack. After paying property taxes on an empty unit for 2 or 3 years they cut their losses and sell at a discount

6. Buyers start to wait even longer to buy because they start seeing houses sold at a discount – buyer behavior changes from getting their dream house to getting to “win” buy getting a cheap “deal”.

7. As prices fall every month sellers panic – there’s a fear if they don’t sell soon they won’t be able to sell at all. All that shadow inventory hits the market and everyone realizes they’re drowning in supply

8. Prices crash as there’s an obvious appearance of way too much supply for the demand.

To me, it looks like we’re at stage #3 right now.

What about property owners simply renting out the vacant homes instead of selling it being a contributing factor? All the hype with being “landlords”.

Rental unit investors, young and old have been flocking to the real estate “passive” income investment game and buying up inventories for renting or short term rentals such as Airbnb.

There is no urgency to sell if the rental income pays all their PITI. I hate that this leads to lower housing inventory or higher home / apartment prices (big cities being affected far more), but if cash-loaded private investors can just swoop in and buy up all the properties and turn them into rentals, there are pros and cons.

In my personal opinion they’ll be the ones selling at the bottom.

Being underwater on multiple mortgages is an awful place to be. I really don’t understand these middle class wannabe slum lords. It’s the kind of investment strategy that only works in a bull market and when things go bad they go very bad.

“I really don’t understand these middle class wannabe slum lords.”

ZIRP has gutted returns in numerous asset mkts (many/most asset classes are implicitly priced to a spread against riskless Treasuries – when the Fed prints enough to cut rates by 50 pct (long end) or 80 pct plus (short end) almost all less risky (fixed income) asset class returns are going to fall dramatically.

People have been herded into over-leveraged, pyramided real estate slumlordism thanks to two decades of Fed interest rate repression – in the name of stimulating….slumlordism, to judge by actual results rather than lofty intentions.

I’m no real estate expert like Petunia, however I do know quite a few people with real estate holdings in New York city. They started buying a few units in the 80’s and when the crash came in 08 they sold all their stocks, but they couldn’t sell the real estate. They were sweating bullets for a while but it turned out to be the right move. They did age quite a few years in the process and are doing quite well now. It all depends on when you buy, at what point in the cycle. Sometimes it’s just luck.

“…but if cash-loaded private investors can just swoop in and buy up all the properties and turn them into rentals, there are pros and cons.”

From the little I can see and understand, it is the investors who are the problem. Small investors from overseas buying a house, condo, or a small apartment building and the large investors like Bain Capital (I do not know if Bain itself is doing this.) that buy up thousands of units, but they often do not necessarily rent them to anyone.

It is either an investment for the future or that they want too high a price even for this market. That means all those units just goes away. It is hard to find out who is buying what now as the buyers are not locals buying individual homes and registering them at city hall.

I think that this is a result of effectively shipping all the jobs and taking all the wealth from the bulk of Americans to either China or the uppermost wealthy class. The 1% or 5% enriching themselves by impoverishing the bottom 80% and most especially the bottom 40%.

So all the money printed, all the wealth created, has been diverted to a small group given exclusive access to the almost free money; they are not looking at productive, long-term investments but at an almost immediate profit anyway possible without a care for the consequences to anyone.

There is also the fact that the jobs are mostly in the cities with wages that have not kept up with inflation; much cheap housing like single room rentals (SROs) were destroyed and what housing that is being built is for the apparently glutted upper income bracket and the owners do not want to reduce their prices.

It is almost like some evil cabal planned this economic storm although I know that it was not conscious planning, but plain greed.

I’m just a 500 sq ft apt renter in a hotel style 3 story 200 unit complex (only one exterior wall, big utility savings) and other than buying two bare off grid parcels (from a friend’s mother directly and then BLM) and two mobile homes from the dealer), I know virtually nothing about realtors or real estate.

But your analysis of the present data for this area makes sense to me, for what it’s worth.

Most people have too much real estate. I have found about 400 – 500 sq is great for a single person. Probably twice that for two adults is plenty. A big home will eat your cash flow up and unless you get property appreciation is a sink hole for money.

… but reality is that in a housing bubble many buy the biggest home they can afford (with the most reckless mortgage etc.) because that increases the leverage and is the only way to get ahead in the housing game; especially if you know that any financial downside can be shifted to others, and assume that you can time the top of the bubble ;)

Incidentally I’m hearing more often these days about high income homeowners who are trying to downsize for home and garden while staying in the same area and keeping a similar luxury level. That now often means paying even MORE than for the bigger homes. In some remote parts of the country big monumental homes are starting to look relatively affordable too despite still increasing bubble prices, because for e.g. 3x the cost of a very small apartment you get a 10-15x bigger and more luxurious home. In the housing hotspots such big homes are split up nowadays but in other areas this apparently doesn’t pay off. I don’t think owner maintenance cost and taxes are the big factor there, probably more that those who can financially afford more than a very modest home at current bubble prices (usually boomer couples or people close to retirement) don’t want a mansion that is way too big for them and try to find the “perfect” home instead.

My partner and I are in LA and we are solidly on stage 4. Just extended our lease for another year. No rush. Very clear the houses we want are lingering on the market for 200-500 days.

Interesting, thanks. I think I will copy A’s analysis and save it to my W. St. folder. Glad to hear it made sense to someone else.

From here it appears that residential real estate bubbles have two root causes:

1) A shortage of housing, in general created artificially, one way or another.

2) Predatory lending practices.

Interestingly enough, depending on who you ask, in the CA Bay Area there appear to be five to ten times as many unoccupied residences as there are homeless people. Many of those homeless people are well-paid professionals, which just goes to show how extreme such bubbles can be when market conditions are aggressively manipulated.

I’d spend a few minutes providing context and filling in the details except that I’d rather have some schnapps and read Henry James. That said, I have absolutely no objection to those who may be inclined to do it for me.

Translation: You’re going to shut the hell up for a while. Outstanding.

Take over me me, drggie. Owl be bock.

Guess he wasn’t kidding about using his beer mug for hard stuff…

I would add to the reasons as number 0 a compelling Ponzi story, pushed all over the MSM, that mixes greed and fear; like fear of being priced out forever while seeing others reap huge profits from flipping homes.

We have much of the same problem in Netherlands: surging house prices (for three decades already) with a steady increase in vacant properties that aren’t even rented out because the home values increase so much (average 8-10% yoy for three decades!) that most “investors” don’t bother collecting the pity 2-3% ROI from renting out. In some cases properties are rented out a few months per year through Airbnb etc. which creates untaxed income that easily exceeds what one could squeeze from a renter in one year and of course drives up home prices in the area even more (in Netherlands, having an Airbnb suite in your home will provide an additional 100K euro or so mortgage).

Result: nowadays 40.000 citizens are homeless (a significant chunk of them people who are still employed) and over 1 million are stuck in the housing market (like living with their parents, with their ex, way to far from their work etc. or in otherwise horrible apartments with high rent) with no way to go due to surging rents and surging prices. In much of the country households with median income can only afford 1-2% of the homes that are for sale now, and of course those homes are usually POS. So basically all sales are now to the speculators, the elite and people who inherited loads of money from their wealthy parents (parents can shift much of their wealth totally taxfree to offspring if it is used for buying a home).

Valuations and ROI for rental properties are irrelevant because you cannot loose money in the Dutch housing market. Our last housing crash was in 1981 – nobody believes that housing will ever go down more than the proverbial dip before the next surge. ECB and politics are doing everything they can to keep this epic Ponzi going.

Hi nhz,

I try to remember the words of Charlie Munger when things look screwy which is to ‘invert the problem’ to see if it looks different. I guess that could mean different things. If you are home owner, imagine if you are renter. Or if seller, imagine if you were a buyer. If you are a saver, imagine if you are debtor.

Yes, that sometimes works. However, not in the current situation.

Despite significant savings I’m just as stuck as some people in the opposite situation like those on social security, in social housing and with zero savings: they usually don’t qualify for a mortgage and when they leave their current rental home they would be on the waiting list for another home forever. I had interesting discussions about that with some of them last year. Some of these people have nice homes for next to nothing that would be almost unaffordable to me; they will probably never leave. But many others have homes with serious problems or terrible neighbors that they would love to escape from, but they have zero options.

Politics is managing the bubble for the benefit of the elites and the countless debt slaves; others (a voter minority) no longer matter. In my country the game is now basically rigged against all new players except those who get a free pass from the government (like new migrants). If you are not in the game yet the only option is to wait until the bubble bursts or leave the country.

Read some Conrad instead. James can be depressing and sometimes just wierd.

Now what? A few years back we could have guessed the FED would assist the limp economy by reducing rates. But now that the rate reduction is virtually spent, now what?

Money printing. Debt forgiveness. Helicopter money. Down payment assistance. Tax rebates…

All that is a good guess, and possibly massive infrastructure spending from congress…

just look at Netherlands:

– full mortgage cost deduction from income taxes and zero-down mortgages for everyone

– free government-provided guarantee against any financial loss when you have to sell your home (for all homes up to at least the median home price), plus of course zero tax on any gains when selling the home: home buyers can never loose!!

– add even more ridiculous zoning, rent control etc. etc. politics so available land for building is limited to the max and land prices increase even more than home prices, making it impossible to build affordable homes.

– have a huge buyer in the market who doesn’t care at all about price/cost, like a government that provides free homes to the flood of new migrants (plus later on their extended family etc. …) and other disadvantaged groups. This cuts available housing supply and drives up prices even more.

In my part of the country in the last 5 years over 90% of social housing went to newly arrived refugees, the other 10% to special cases like single moms; normal citizens have zero chance and waiting lists for social housing are 10-20 years in much of the country. If your income isn’t sufficient for buying or renting in the extremely expensive free rental market you are basically stuck forever, as home prices increase much faster than anyone could save (while living with their parents etc.).

Mortgage rates in the US are still ridiculously high compared to Netherlands (1.0% for 10y fixed, 1.5% for 30y fixed), I’m pretty sure the FED will go there too before this grand experiment ends. Price gains in most US markets are also quite moderate compared to Netherlands (up 10-20x in 30 years with very little income gains).

I have a low limit now to how much I will fight a bad situation. I don’t have much power to restructure work or local or national government. It’s obvious the Netherlands is rewarding certain behaviour and giving you the stick. Probably should just vote with your feet. We have a lot of migration right now from high tax to low tax locals. Let’s face it, if you are average Joe Blow in some places you are working to fund a unionized person to retire early while you bust your butt.

The southern states culturally have problems with unions and most of government unions are fairly weak so the drag on private economy is small.

@Old-school:

I would like to vote with my feet yes, because as long as I’m staying I’m subsidizing the housing market gamblers and all kinds of other irresponsible policies.

The US has the advantage that it is very easy to move to another state and I think that limits average price increases for the whole country. In EU you can theoretically move to another EU country, but in practice it is difficult even if you have money and a job that is in demand in other countries; education or other job qualifications may not count in the other country and some of cheaper countries make life difficult for newcomers (I can understand that …).

The Netherlands has an epic housing bubble, has been like that for over two decades and the introduction of the Euro in 2001 and ZIRP/NIRP after 2008 only made things worse. While the most remote rural corners are more affordable than the big cities they are still very expensive and probably more risky financially. Current prices there are even more elevated compared to local income or past price levels, due to people from the big cities (with high income and/or lots of home equity) who moved there to escape the bubble.

How to short housing?

I don’t think the VNQ is just housing.

A quick perusal of homes listed on Zillow within about a 1 1/2 mile radius of my place in Union City, CA shows nineteen listings. Nine of them are foreclosures. The outcome of having so many people in over their heads can’t be good.

That used to be blue collar. Freemont also had a sort of renaissance didn’t it? All the homeboys moved to SJ? In 2008 the foreclosure bug hit mostly higher end homes I think.

Mixed collars in my neighborhood. My own collar always had more blue in it than white. I like being around people who can fix things with their hands instead of with a phone or a check.

SF, NYC, DC and Chicago are all millennial cities….

Not long ago, a 24 year old GIRL (as in female child, not an adult woman) has a blog explaining how she supported herself living in NYC working at a magazine… after a few people questioned her math, she acknowledged her parents paid her rent, her cell phone, and gave her money toward food and clothing — and being female she got free drinks at most bars… other than rent, food, clothing, cell phone and entertainment she was totally self sufficient. Yeah, right.

How many people living in NYC or SF or DC could indulge their fantasy lifestyles if they truly supported themselves?

As a former New Yorker, I agree with your assessment. Many women or men for that matter who live in New York are subsidized by their parents until they have been at the job enough years to be self sufficient or until they are married. This is another barrier of entry for people who move to New York to find work, you better have someone backing you financially or else you can’t make it (unless you work on Wall Street of course).

This girl happened to post an absurd note on her blog that demonstrated how clueless she is/was, but a newspaper ran with her story (before it was ridiculed) because many people were complaining about the cost of living even with a half dozen roommates. And the math check / rebuttals happened because she simply could not afford her city lifestyle without substantial subsidies.

I doubt her story or her post college allowance was unique. Adults should be able to support themselves, especially a college graduate.

It isn’t just NYC. Another widely repeated situation (and 60 minutes story) told of new employees at google living in RV while making six figures, but still not being able to afford the fantasy that is San Francisco.

These are the same people who vote for Bernie Sanders and his free stuff program. It only appears “free” because mommy and daddy are paying the bills. Without mommy and daddy, one ends up in a living situation closer to Caracas Venezuela. That “Bern” these children are feeling is called Peter Pan syndrome

Six figures and not able to afford housing? There is housing for new people who want to pay 3k for a dump in San Francisco or, if you are lucky, something halfway decent for 2.5k outside usually outside the city.

Although buying a RV probably is cheaper right now though and for anyone making less than 100k it might be the only option available.

Cold Water:

“How many people living in NYC or SF or DC could indulge their fantasy lifestyles if they truly supported themselves?”

Many are trying. Mightily. And, that is why we have so many young that are the, “working homeless.”

In addition, there is absolutely nothing wrong with getting “help” from parents, grandparents, etc. Isn’t that what family is all about? Have we forgotten what “society” is supposed to be about??????

I own a house in the north Silicon Valley area and my house went down from its (zillow estimated) high in Sept. ’18 (of $1,910,000.) to its present est. price of $1,312,000. So what is that, down almost a third?

Funny that would happen in the best economy ever, and, while stocks are still going up thru the stratosphere.

Someone needs to short the markets!!

That would get you a nice ocean front beach house and a nice mountain house in NC with about a half a million left over.

4 years ago, January 1st, 2016,

the Fed started raising its “Funds” rate.

Interest rate spreads are so narrow,

it’s covering a multitude of sins;

not even the Fed knows what’s going on.

12 months ago, right before it started

lowering its rates, it predicted that

its “Funds” rate would be 3.1 % today.

However, here’s a hint:

> A growing company issues shares;

> an aging company buys them back.

I don’t have a lot to add really. But next year I’m gonna start seriously looking at those new condo developments around Millbrae BART. I work for the City of SF at the reservoirs along 280 and all our offices are in Millbrae and Burlingame. Been commuting on BART and its killing with and hour to an hour and half rides plus a bus connection in Oakland.

I hope it all comes down to a reasonable mid-50]k range for the new buildings.

I know Facebook AR/VR is moving into the area. But I also know someone that is a manager at FB and the cost cutting and leaving positions unfilled has begun.

Make sure the new condos are insured and premiums locked in for quite some time. I understand that there is a growing trend of insurance companies failing to insure condos all over North America. After all, the Bay Area is in an active earthquake zone, a fire zone, and property values have skyrocketed. All the boxes are ticked.

snippet: “After the 2016 Horse River wildfire that burned down more than 2,400 structures in Fort McMurray, residents of the 40-unit Winchester Greens condominium building considered themselves among the lucky ones.

Their apartment-style units didn’t burn, but the condo board did claim $246,000 of smoke damage on its insurance.

Three years later, the condo board is struggling to find insurance coverage, in part because of that wildfire claim.”

https://www.cbc.ca/news/canada/edmonton/fort-mcmurray-condominium-insurance-1.5318750

and: https://globalnews.ca/news/6237709/bc-strata-insurance-surge/

Zillow’s price estimation algorithms are terrible. Use redfin instead. You will see lower highs and less decline because redfin actually estimates more accurately.

The value of my home in Florida has risen about 33% in less than four years. HOA fees and utilities were rising, but at lower rates. Wages are not rising much. I think Walmart pays $12 an hour. When I worked my first summer job at 15, the minimum wage was $2.10 an hour. People were afraid the stock market might crash. It rose.

I hold onto an index stock fund. I always thought it might crash. It crashed last year. I held. It rose through 2019. In 2020 I hold. The stock market might crash someday. If I live 15 more years, it will probably be worth more, if I hold. The S&P 500 outperformed gold over the long run.

The S&P500 only outperformed gold in specific periods, the opposite is also true for much of the past decades. It really depends on the starting date you pick. Said otherwise: most of the “gain” is just inflation and not real; when more people realize these stockmarket gains are not real the bottom could fall out and it will not recover in 15 years (most EU stock markets are still lower than in 2000, even nominally; I think most of them will never recover if you correct for inflation).

More interestingly, in my country the prices of homes measured in gold has changed hugely (up and down) over the past three decades; don’t know about the US but probably similar.

One of the truest things that Al Gore said and it applies today, “Everything that ought to be down is up. Everything that should be up is down.” I think it is true with regards to financial markets and has been true since 2008 regardless of party affiliation.

yes, regardless of party affiliation and in most cases even regardless of country as long as we are talking about the Western developed word.

Would you agree with the claim that Japan hasn’t seen much change in home prices in US dollar terms since the market peak around 1989? The Yen started out around 150 Yen to a dollar in 1990 and bottomed around 75 Yen in 2012. Since then it has strengthened again, but so has the housing market. Since apartments in big cities lost a bit more than half their value from peak to trough, the two seem like they cancelled each other out.

The Australian dollar, on the other hand, lost about 40% of its value from peak to trough during the last decade, so it looks like the Australian housing bubble imploded in US dollar terms.

The yen was 110 to the USD when I went to Japan for the first time in 1996. Now it’s 108.74. The USD-JPY exchange rate has been in the same fairly wide range for decades.

Wolf:

1950 360 yen to the dollar…….of course as a young 20 year old in the Navy I had no clue as to any “exchange” rates…….Little did I really know!

That’s back when everyone smugly said, “Jap Junk”.

In the 60’s everyone was buying damned good Jap motorcycles.

By 1971 in Detroit I saw lots of bumper stickers that said, “Hungry? Eat your Toyota”.

Then things got even worse.

Here in the DFW area, I see constructions in progress everyfreakingwhere! They are popping up all over the place. It never ends. Growing growing growing.

I haven’t been following prices, but this area is *STILL* growing.

I have heard, new constructions are having many problems. Plumbing is a big one. From what I am hearing , unqualified labor, is the cause of the poorly built homes.

This won’t end well. I know at least 3 families right now having big issues with their new house.

The bad news is that, rent is outrageous as well, they keep building houses and overbuilding apartments, yet, rent is still ridiculous.

We still have companies moving here, mostly from California and people from all over. 45% of our new comers in the last 10 (I think) years, came from abroad.

Yes, homes are not just outrageously overpriced in a bubble, you usually get the worst possible construction quality as a bonus. I don’t think this is primarily because of unqualified labor but more due to the huge financial pressure in finishing homes as fast and cheap as possible (rising demand, rising prices of building materials and worker income), and because in a bubble buyers will accept anything in fear of “missing out”.

With the highest home prices ever (also relative to incomes) my country now also has a strong increase in newly build homes with such bad construction quality or other problems that they are officially uninhabitable, with no financially acceptable way to cure the problems. These unlucky “homeowners” will be spending many years of their future income for owning a garbage dump.

Some new constructions are doomed! We rented a brand new apartment, and we had mold growing inside the wall, visible spots on the outside of the wall, plumbing issues in bathrooms and kitchen, the same problems happening in several buildings and many other issues. Outside and inside. Poorly built. Poor design, especially outside where the rain water is supposed to drain away from the building the slope is reversed and water drains towards the entry way, staying ‘flooded’ for months.

I’m not sure how wide spread this is, but in my area, the small group people I talk to and my own experience, it’s a sure thing. And many people are just finding problems a year or 2 after moving in.

And renting such places is outrageously expensive. I’m not sure it makes sense to rent versus buying anymore. I guess it depends on the size of your family and the location you need to be.

I know a family who bough a 900K brand new house and the house is falling apart, the frame is rotten due to water damage and they have mold everywhere. Second floor flooring, is cracking.

In my country renting (outside the social housing market) is now several times more expensive than “owning”, most people buy with a no-money-down mortgage at extremely low rates and assume the property will appreciate forever. And if the value goes down, most of them have no ability to pay so what is the real downside risk?

In a way the premium for renting makes sense: you pay extra to avoid the risk of negative equity from falling prices or shoddy construction – but only for those who have something to loose, e.g. because of significant savings. If you have no savings and decent income there probably never was a better time to buy because “owning” is relatively cheap on a monthly basis. The real bill comes in 30 years or so and most people don’t want to worry about that and just assume that whatever happens the government will bail them out or more likely richly reward them for buying.

In my country those very shoddy new homes are still an exception but I’m sure the problem is on the rise. Another development is tiny homes that are almost as expensive as big homes (because something like 3/4 of the total cost of a home is the land and government fees). Those owners are probably in for a big shock once the government finally relaxes the zoning laws for building in agricultural areas, which is inevitable due to serious problems with CO2/NOx emissions caused by too much livestock farming and other bad agricultural practices. Even the very “dense” Netherlands uses only 7% of the total area for cities and roads, if they increase this to 8% by allowing building on just a few % of current farmland the whole “land shortage” would magically disappear. I think that will happen at some point, but not before the next elections in 2021 ;(

Much less government interference with developers, contractors, and by those pesky building inspectors, etc.

Low taxes, though……

No free lunch?

Houston, the overlooked 4th largest city in America is more of a measure than Dallas by a stretch.

Not “overlooked.” Houston is not included in the Case-Shiller Index for reasons related to how difficult it was for Case-Shiller folks to get the public records data.

Houston has been under a unique situation due to Harvey.

I’m not sure if that affects the housing market data. Maybe not?

Post Harvey period, many workers from the DFW area left to go work in the Houston area, causing labor shortage in the DFW area and material cost increase.

We are certainly in a bubble in Dallas, however, part of it is due to population increase (rapid increase and significant). So, I’m curious to find out what percentage of our price increase will remain after the bubble burst. It won’t go back to what it was. But the current level is ridiculous.

Hey Wolf,

Seems like everyone trying to make a buck. I myself don’t want the headache. Trailer homes in Maine, three years ago at 20k now 40 and 60. Land from 50 to 60. I don’t want to hold dirt, wouldn’t help me at all. Thanks for writing, you have kept me cautious, and I’ve learned a lot.

This massive Bubble can’t bust soon enough! Insane asking price below indicates we are past peak.

https://m.sfgate.com/realestate/article/Empty-Oakland-lot-with-Shen-Yun-billboard-asks-14933309.php

My father used to take us to his friends and relatives who lived in Upper Piedmont (overlooking Oakland and the “bay”) about the 70-early 80’s. Those were the days when old folks bought krugerrands and just tossed them on the dining table.

Some of the houses or mansions there made most of Oakland look like a ghetto (in fact, it really was). I still have relatives and family friends from Los Gatos and Los Altos area. They have unbelievable stories. I am glad I didn’t stay in No. Cal.

When you live in a part of the country with affordable housing, and live in a small house there, and have been putting your savings into the markets rather than into local housing payments, the plots of your total assets look quite different from all those plots.

Quite different because the stockmarket went up more than home prices in much of the US? Don’t forget that most homeowners are using huge leverage (mortgage etc.) with their “housing investment”, something that isn’t possible for the average small stock market speculator.

For sure in my country it would be extremely difficult to beat the gains in the housing market by investing in stocks; over the last 20 years homes have appreciated many times more than the stock market index. Add the huge leverage and it is obvious why most citizens feel the need to play the game, for most there is no other way to keep your head above water.

I think it is getting ready to come to an end and I think the Fed ought to be spanked for allowing it to go this long. You have a lot of regular people saving for retirement or are in retirement who have been lulled to sleep as far as risk assets.

Higher asset prices every year make you think it’s going to go on for ever but if you have been around the block a few times you know assets have to eventually be supported by real income.

Unemployment in December 2008. In December, the number of unemployed persons increased by 632,000 to 11.1 million and the unemployment rate rose to 7.2 percent. … The number of long-term unemployed (those jobless for 27 weeks or more) rose to 2.6 million in December and was up by 1.3 million in 2008.Jan 13, 2009.

…….2020 unemployment rate under 3%.

This bubble scenario just doesn’t make sense when you compare this economic fact

david cooper,

I’m not sure, but it seems you’re conflating two things:

– A housing bubble inflates: prices rise faster than incomes for a long time and rise beyond a certain level (however that may be defined);

– Then a bubble deflates and prices fall.

In December 2008, the housing bubbles around the country were in the midst of deflating.

Now the housing bubbles are still inflating in many markets, and just started deflating in a few markets, as the charts show.

Interestingly, the bubble started deflating in the Bay Area DESPITE super-low unemployment.

What I find particularly interesting about residential real estate bubbles is the lack of risk aversion among buyers. It’s yet another sure sign that people can be and have been successfully manipulated to act in a manner contrary to their own interest so as to enable their profitable exploitation, economically, politically, and personally.

That people have an unfortunate tendency to ignore warnings is a subject that’s been well-explored by any number of risk management experts, for example, Geral Wilde, who first proposed Risk Aversion Theory in 1983. Naturally this tendency has also been well-explored by marketing consultants for over a hundred years, even before Edward Bernays turned it into a framework for the arts and sciences of mass abuse for fun and profit.

People in general have never been very good at making assessments of danger and safety for the same reasons they also tend to be poor at evaluating risk and reward, also as described by Wilde and others. Now that culture has been replaced with marketing, and science has become inconvenient to ideology, and critical thinking has been replaced with wishful thinking, and narcissistic irresponsibility has replaced reasoned judgement, it’s only going to get worse.

But probably not for housing bubbles. Those seem to have been pretty much optimised already, and people simply may not have the money to be even more foolish.

It helps a lot if people see that others (those who do not play the game) bear most of the downside risk of the players, making buying a home basically heads-I-win-tails-you-loose. At least in my country with its massive government intervention in the housing market, probably less so in most of the US but still … Especially after 2008 financial responsibility has been heavily punished and reckless speculating has been richly rewarded (both for small and very big speculators). Just like in the runup to 2008 many are making more (untaxed, but often virtual) money by playing in the housing market than with their official job; the difference with 2008 is that they now KNOW that the government will bail them out because otherwise the whole economy will implode.

People can always get more foolish if politicians give them access to OPM for buying an even more expensive home.

In USA we have bill of rights that protects basic freedom. Government has basically used money to induce people’s behavior. For example, you can home school your kids, but you are going to still pay taxes to educate your neighbors kids. The constitution allowed states to retain most power, but because Fed can tax they suck much income out of states and then give it back to the states with strings. Our tax code is 70,000 plus pages which is just behavior carrots and sticks.

A few people still can find maybe 99% freedom by being off the system in rural areas or by being RV nomads out west. For the most part if you want to participate in official economy as an earner and a buyer, you are dragging government regs along with you.

In USA we have bill of rights that protects basic freedom.

Your ‘rights’ can be alienated fully or by degrees by privilege, and those of many people in the US always have been.

A few people still can find maybe 99% freedom by being off the system in rural areas or by being RV nomads out west.

Exile may sometimes be preferable to captivity but it’s almost never sustainable.

Nice try though.

Now with computers and big data you’re not dragging government regs as much as the government is actively chasing you.

I think you’re bored and just want to be entertained.

Can’t wait for Housing Bubble III! I love LA (sits in a basin) and SD (isolated by ocean, mountains, a foreign border), that bump in the chart, early in the recovery, puts the shoulder into it. Vegas, Phoenix and Miami all have “water” problems. GT is only 16, she will be waving her finger at you for a long time. A lot of housing markets are going “underwater” literally. Thriving urban environments have strong physical borders.

Location is the real deal. At beach where I like to vacation an empty beach front lot is about $275,000. Cross the road to second row you drop to $175,000. Cross the bridge and go 1/2 mile from beach a lot is $25,000. I guess the convenience of being to walk down your steps to the beach has a market value of about $250,000.

SoCal is still going strong. Dont expect a crash here. Everyone wants to live in San Diego. We are special!

We are not seeing any depreciation or slow down.

Got advice from a baby boomer that moved here to SD in in like ’72 to buy now, “Prices have only ever gone up” he said.

Heard the same thing from a Carlsbad real estate salesman recently.

At the taco truck this was also stated “San Diego wasn’t hit by the housing crash”.

Speechless.

Famous last words. Has anyone bothered to see the prices for housing in San Diego? What kind of job market do they have down there to suppose 2 million dollar 1500 sqft condos and old houses? Please go on zillow and see some of the shenanigans they are pulling. Buying and then putting house up for double their buy in price to catch a ponzi. It’s pretty incredible people would still be buying in this env down there.

Home prices in the DFW area are flat if not on a slight decline. I attribute this to iBuyers who are now flooding the market with homes they bought, threw on some paint and want them off their books. They are making all of their money from fees charged to the seller, not from home prices so if they are charging 7% on a typical $300,000 home they are pocketing $21,000, so they can afford to slash the price a few thousand dollars and dump it. Prices should be on an actual slight increase based upon demand driven by the influx of newcomers and low interest rates in the DFW market. No bubble in the market, but no further near term gain for Dallas metro area. Flat prices still make owning a home better than renting if you are not moving in the short term, but is becoming less attractive.