Bailing out its crybaby-cronies on Wall Street, even when there isn’t a crisis.

By Wolf Richter for WOLF STREET.

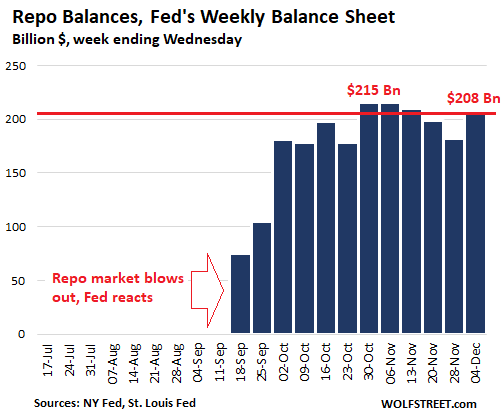

The total amount of repurchase agreements (“repos”) on the Fed’s balance sheet as of December 4, released today, declined to $209 billion, from $215 billion a month ago. These repos included:

- $70 billion in overnight repos, issued on Wednesday morning that unwound today; all prior overnight repos had already unwound.

- $88 billion in multi-day repos with maturities of up to two weeks;

- $50 billion in 42-day repos; of which $25 billion were issued on November 25 and $25 billion on December 2. They will unwind early next year.

Before the repo market blew out in mid-September, the repos on the Fed’s balance sheet were zero. This chart shows the weekly balances of repos on the Fed’s balance sheet as of each Wednesday:

In these “repo operations,” the Fed buys Treasury securities, mortgage-backed securities issued by Fannie Mae and Freddie Mac, and government “Agency” securities, under an agreement whereby the counter parties have to repurchase those securities on a set date at a set (higher) price. The interest rate is determined by the difference between the price the Fed buys the securities at, and the pre-set higher price it sells the securities back to the original counter party.

Via these operations, the Fed effectively lends to the repo market at rates that are within its target range for the federal funds rate. Today’s overnight repo operations had a rate of 1.55%. This is a way to push all repo rates down into the Fed’s range. And it guarantees that companies that borrow in the repo market, including mortgage REITs and others, can borrow at these ultra-low rates.

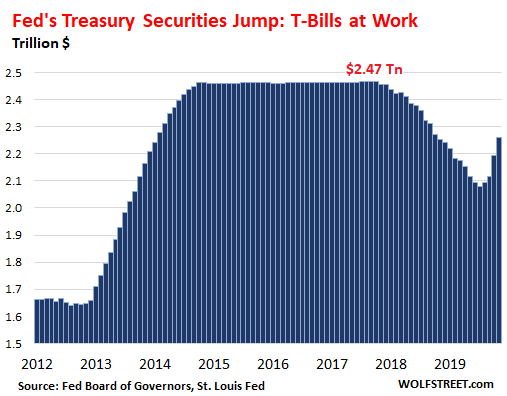

Fed goes hog-wild with T-Bills.

During the month of November through the balance sheet as of December 4, the total amount of Treasury securities jumped by $65 billion, mostly short-term Treasury bills (T-Bills) with maturities of one year or less. This raised the balance of Treasury securities to $2.26 trillion.

There had been no T-bills on the Fed’s balance sheet for the last few years. But earlier this year, the Fed changed strategy and switched to replacing some of its maturing longer-dated securities with T-bills. Then following the repo market blow-out, it decided to douse its Wall Street cronies with cheap cash. Under this program, it said it would add $60 billion a month in T-bills. Since July, it has piled on $179 billion in Treasury securities, including $77 billion in October and $65 billion in November, the biggest monthly increases since the depth of the Financial Crisis.

Only this time, there was no crisis. All that happened was that the repo market had had a hissy-fit and that rates spiked. And instead of letting the market take care of it, and let some risk-takers eat dust for taking these risks, the Fed is bailing them out. When it comes to bailing out its crybaby cronies on Wall Street, even when there isn’t a crisis, the Fed stops before nothing:

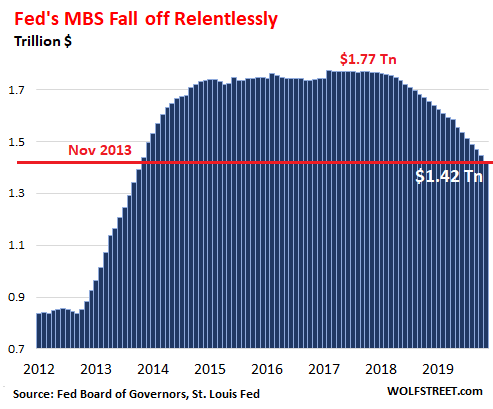

Fed continues to shed Mortgage-Backed Securities

The Fed has stated many times that it wants to get rid of its holdings of MBS. And it’s progressing with the plan. In November, the Fed shed $22 billion in MBS, exceeding the self-imposed cap of $20 billion per month for the seventh month in a row. Over the past seven months, it has shed $160 billion in MBS, or about $22.8 billion a month on average. Its holdings are now down to $1.42 trillion, below where they had first been in November 2013:

Holders of MBS, including the Fed, receive pass-through principal payments as the underlying mortgages are paid down or are paid off. About 95% of the MBS on the Fed’s balance sheet mature in 10 years or more, and the current runoff is almost entirely due to these pass-through principal payments.

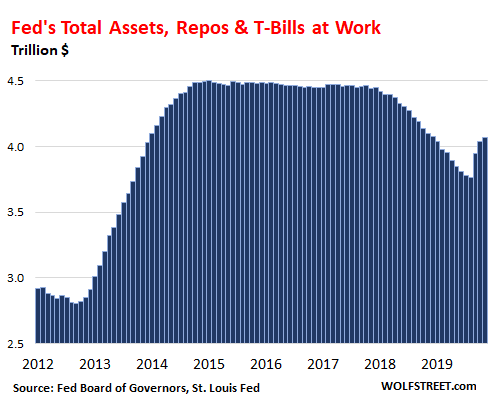

Total assets on the Fed’s balance sheet

The net effect of the surge in Treasury securities, the drop in MBS, and the small decline in repo balances along with some other factors, is that total assets rose by $26 billion from the prior month, to $4.07 trillion, having jumped by $304 billion in three months, the fastest since the post-Lehman months in early 2009:

Even though the Fed is dousing its crybaby cronies with cash and is bailing them out in the repo market, it is not targeting long-term interest rates, which it had done during QE. Instead, it is unloading MBS with long maturities and is piling on short-term T-bills, which has allowed long-term rates to tick higher from the lows last summer before this freak show began.

Whose Bets are Getting Bailed Out by the Fed’s Repos & T-Bill Purchases? Read... What’s Behind the Fed’s Bailout of the Repo Market?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Price stability and maximum employment… they say with a huge grin.

Maximum employment, in the short term, could be accomplished by handing everybody $1M worth of new $100 bills. Why don’t they do that?

That would go against their mandate of “rob from the poor and give to the rich.”

Great reporting Wolf,

I look at that chart of the Fed balance sheet and Little Prince comes to mind.

Is it the drawing of a hat or a boa constrictor that has swallowed an elephant?

Funny.

Actually, it’s just the start of a drawing of a Bactrian double hump camel but it won’t be completed for a few years!

Likely, your not all all far off, although have you considered a boa constrictor swallowing its second elephant?

First thing in the morning and coffee deficient.

“Likely, you’re not at all far off, ….”

Except the second wont be an elephant. It will be a brontosaurus.

I just read that 95% of trading is algorithms. If that is true then they are efficiently following central banks every move. Not sure the end result but this is probably how you get a stock market at 3100 on $136 of Gaap earnings. What’s going to happen during recession when earnings are $30 – $50?

This reminds me of the story of the town with the tower clock and the cannon firing at noon thinking that they were keeping accurate time because they agreed with each other not knowing they were using each other for accuracy.

In machine learning algorithms, like the ones used in HFT, there’s a problem called overfitting which is when the model ‘memorizes’ its training data and gets stuck in a set of local minimum or maximum solutions, failing to find better global minimum or maximum solutions. It’s like the algo only has ‘eyes’ for that particular solution not being able to look around. When I see what’s happening with S&P500, FANG’s and responses of indexes to specific headlines, it seems the algos are overfitting.

So did turkey before thanks giving.

I wouldn’t call it overfitting as it’s more the case that you have your machine learning model operating outside the boundary conditions established by prior data. I used to have to run over a week of compute when adding in a new quarters data to an existing ML package I had written in order to make sure that it would come up with an accurate model for those previously and newly seen conditions.

Interesting side note: over on phys.org, there’s an article about using ferro-electric ternary content addressable memory at the node level to drastically speed up, and reduce energy requirements, to address exactly this problem. Be interesting to see when/if the Wall Street Rocket Scientists pick up on it.

Maybe swallowed Deutsche Bank when nobody else would even take a bite

Fed is monetizing everybody, it’s pretty scary

Which central bank is not monetizing debt?

Better get used to it. Fiat money will be monetized.

“Fiat money will be monetized.” What is that supposed to mean? Fiat money is in the process of being digitalized- meaning you do not even get the small comfort off being able to burn a wheelbarrow’s worth when it gets cold outside, but the banks still get to chip a bit off of it with negative interest rates.

What is that supposed to mean?

Simple: The Central Bank will buy government debt. Just exactly what the Fed is doing.

In fact, if you are watching carefully, the Fed is buying up a lot of T bills especially in the 13week to 52week (slanted towards the longer ones) that were once the mainstay of Money Market Investing. Wonder what the the MMFs would do now?

Repo is cash for collateral, RRPO is collateral for cash. They are working with both hands to monetize.

Did anyone notice that FRB “sold” $0.05B = $50M in FRN (Federal Reserve Notes, meaning dollar paper currency, aka. greenbacks/banknotes today). Some entity, probably a foreign bank, converted some of their reserves to currency, which in they in turn probably will take out of the country to use as cash payment elsewhere (bypassing crazy banking sanctions is a popular use of US banknotes :))

I got the following email :

Federal Reserve Bank of New York

11:21 AM (8 hours ago)

to me

New York Fed sells $0.050 billion in FRNs

Anyway, thought this was interesting.

How else would reserves leak out?

There are only a few factors that reduce reserves in h.4.1. Currency is one of them.

Getting permission from the Fed to buy and pay for Treasuries is another. But a bank just paying another bank only moves reserves.

Foreign Repo Pool which does reverse repo reduces reserves, too.

Yes, currency is a huge part of “factors that reduce reserves”of H4.1. But think there is no official published statistic as to how much of currency is physically located abroad….

I read a fed circular stating more than 70% of our US currency is overseas.

We slap a tariff on Argentina, which needs our dollars to pay the interest on its 100yr US dollar denominated bonds? Am I missing something?

@Ambrose

Hopefully, you missed buying Argentina’s Bonds.

Reference (may take some time to get out of moderation)

https://www.newyorkfed.org/markets/pomo/operations/index.html?05122019

Were you referring to these:

(Auctioned by the treasury)

1-Year 11-Month 0.300% FRN

https://www.treasurydirect.gov/instit/annceresult/press/preanre/2019/A_20191206_1.pdf

or these?

(SOLD by the Fed)

Outright FRN Sale 12/05/2019 Total Par Amt Accepted (mlns) : $50

Neither of these are currencies. These are Treasury Floating Rate Notes.

They start as 2 year and then are re-opened.

One of the CUSIPs, 9128287G9, the Fed SOMAed $794,508,600 on 24-Jul-19, so I guess they just wanted to test the sale of securities because this looks like a small amount operation.

You’re right. FRN stood for Floating Rate Notes. My mistake. Live and learn (that’s why we are here, right?)

When will Mortgage-Backed Securities explode?

Became it definitely looks like it’s heading that way. The question is when not why or how.

Which is exactly why I think housing bubble 2.0 is on its way. Just because the causes aren’t the same, doesn’t mean this echo bubble doesn’t need to pop.

Jeffrey Snider made an interesting point at his Friday RealClearMarkets column a weeks ago about Repo. I’m a layman at this but as I recall the issue went like this. In order to arbitrage, e.g., the spread between US and JGB , an investor would need to hedge Fx risk. The problem is that a repo is a loan and requires a bank to account for it on its balance sheet as a loan and this requires balance sheet capacity and sufficient Tier One capital. OTOH the Fx hedge is a derivative product and only requires the nominal VAR of the trade on a banks balance sheet.

If I’ve got this right, and I may not, the problem lies in this distinction. A bank will have to value a repo at its full market value of say $1 billion while hedging a Fx contract for that would only appear as a minor liability on its balance sheet and not impair its ability to make more lucrative loans.

Maybe Wolf or another person with more expertise ( and clearer prose that Snider) can go deeper into this but it sounds plausible as to why Repo markets can freeze up but Fx markets do not.

Read the BIS article on the missing money. Currency Swaps, which are derivatives, are accounted for differently.

unit472,

Remember that banks are LENDERS to the repo market. The problem that has by now been well established was that they didn’t lend to the repo market when they should have.

Banks have options where they want to borrow short term. Yes, they can and also do borrow in the repo market. But the repo market is secured funding. Banks have to have collateral. Banks have the unsecured market available (federal funds market). And banks can borrow at the Fed’s discount window (currently at 2.5%). So when the repo rate spiked to 3% of 5% or 8%, banks would have been nuts to try to borrow at those rates when they have the other options available.

During the blowout, and even now, the borrowing pressure in the repo market came from other sources, and banks weren’t lending enough.

Which are these sources?

https://wolfstreet.com/2019/11/06/whats-behind-the-feds-bailout-of-the-repo-market/

But banks borrow from the Fed and then lend to the repo market, yes?

What a wonderful legal and horrible way to make easy money, until something goes wrong.

How do banks intermediate between the Fed and others in Repo? There is more to this.

The fact is, as of today, we don’t know who really needed to borrow badly, who did not want to lend who, and to whom is the Fed lending on repo. But it’s fair to assume that something is very wrong in the repo market since it needed massive intervention from the Fed.

raxadian,

Banks could do that, but that’s a money losing proposition unless the repo market blows out. Currently, they can borrow at the Fed at 2.5% discount rate and lend to the repo market at 1.55%. So no, they’re not doing that. But if the repo market rate spikes to 3%, it would make sense to borrow at 2.5% and lend at 3%.

Wolf,

Many thanks for keeping score. Appreciate the ongoing efforts.

Also loved the ‘tude in this segment.

Is no financial entity allowed to assume room temperature anymore? Who would really care if a few hedge funds and REIT’s went Tango Ultra? Seriously, the Fed acts as if every last non-value added, flimsy, financial business model that relies on CB money laundering must be saved.

Indeed they do! Could they be afraid of even the teeniest weeniest downturn?

…and I remember Reagan howling about welfare queens. What an unjust world!!!

I suspect that it’s because our overleveraged parasitical financial system lacks robustness, and that a significant failure or even broadening uncertainty at any point can plausibly set off some sort of disorderly unraveling.

The system bases its ever growing size on promises that the future will be much bigger and better than the present, and since it’s politically much easier to maintain such a stance, participants have willingly kept on increasing those bets even as the response to ever growing debt infusions grows weaker. It doesn’t bode well for when people broadly wake up to that we’re being told fibs.

It’s becoming increasingly apparent that central banks are trapped in a ponzi system with only two modes, so the need to paper over any cracks has now become an imperative, it seems, irrespective of whether the office holders individually see through it or not. They have to quickly stop any small thing from developing, as once a snowball starts rolling downhill it might quickly gather too much mass for our central planners to readily roll back.

Thank you for the great work and sharing it

the FED and other central banks are all in

they act like during a crisis and war

but have we ever gotten out of the crisis after 2008?

It look like it is permanent and they have to increase the liquidity on regular basis to paper over insolvencies

the debt monster cannot be stopped and needs to be fed always more and without any pause.

Peter Schiff has been saying this for years That we never got out of the crisis just papered it over with more debt Hes usually early about things but ultimately spot on

Peter Schiff has a great observation in his latest webcast. The Fed always said it needs 2% inflation to create a buffer against deflation. This was the sole justification.

Now, they say the 2% target needs to be symmetrical, meaning they will run it at 3% in the future to make up for past periods when inflation ran less than 2%. However, if the point of the inflation goal is to create a buffer, and we successfully avoided deflation in the past, the goal setting process was successful and there is no reason to increase the inflation goal. Thus, new symmetrical inflation target is a ruse.

The Fed’s real motivations are becoming clear. They are now in panic mode and want inflation to accelerate to avoid a debt crisis. The creation of a deflation buffer serves only as a feeble excuse.

The Federal Reserve is trying hard to present things as normal. When they do this by deceiving the public, however, they lose credibility in the end.

Is their any way to be able to see the rate of Repo Failure (repayment failure from the borrower) since the Fed started Repo in September?

The Fed will make details about the present Repo operations available starting Fall 2021, starting from who’s taking advantage of it and down to eventual defaults.

That’s something very very strange which has given raise to all sorts of theories and even crazy conspiracy theories, especially given we are now over two months into it and the Fed shows no sign of slowing down.

My two favorite ideas (not mutually exclusive) are that the Fed is giving a big helping hand to one or more likely more foreign banks facing a “sudden” dollar crisis (what broke the Thai banking system in 1997) and/or that this is all part of the present scheme to inflate US financial markets even further before the 2020 elections.

Either way the Democrats are losing another golden opportunity to publicly grill Trump and Powell thanks to their obsession for irrelevancies.

The Democrats’ “obsession for irrelevancies” is a feature, not a bug.

There’s only one oligarchy, and it “hires” (or honey-traps) and promotes clowns on both sides of the aisle to put on a show and distract everyone from the real issues at stake.

“…clowns on both sides of the aisle to put on a show and distract everyone from the real issues at stake.”

Huey Long had this figured out back in 1935

Thanks!

… yah fall 2021 is a long time away, that is very weird. I see why it is spawning conspiracy theories, the less that is allowed to be know for longer the worse the mind is forced to imagine the reality being hidden could actually be.

I shouldn’t add to the conspiracy theories, but my personal concern is that the rate of Repo Default might actually be relatively high. This could explain why the Fed had to step in, all the banks that would normal partake in repo started to back off of it a bit when they realized the rate of defaults was growing and that continuing to cover 100% of the market’s daily repo needs was going to slowly drain them of their liquidity and then leave them with a giant pile of former repo-collateral that would suddenly become hard to unload. At this point Fed-run repo would basically be a fantom bailout that we wouldn’t know about until fall 2021 apparently.

Foreign bank dollar shortage as you propose also makes a lot of sense.

Repo are the “best” kind of default, as the lender is immediately left with full possession of a highly liquid asset (US Treasuries and similar ultra-prime assets) he can immediately sell for cash or use as a high quality collateral. No messy bankruptcies, no credit recovery, the only thing the lender stands to lose are the interests but it’s a risk worth taking.

Albeit expensive there’s really no shortage of US Treasuries in the world, meaning the Repo machinery suffers no risk of bogging down.

The big story here is why repo rates shot to over 8% pretty much overnight, forcing the Federal Reserve to douse the system in even more liquidity. And it shows no sign of slowing down: a sudden crisis would have been over by now.

I am yet to read a satisfying explanation or analysis, and compounded with the Fed’s shocking lack of clarity makes me curious. Very curious.

The dollar shortage is still my personal favorite, and the scattered evidence around seem to point towards the Middle East. It could be a false lead, but so far is the most convincing I’ve found.

Not so far removed is a “manufactured crisis” to ostensibly force the Fed’s hand into providing even more liquidity to the US financial system than it does. It would fit into the pattern of non-sensical rate cuts we’ve seen lately.

The two are not mutually exclusive and would raise all sorts of questions, hence the need to keep them under wrap for a couple of years.

Obviously it remains to be seen if the Fed will be able to stop Repo operations from here to Fall 2021 so as to allow everything to fade from memory: easy liquidity tends to be pretty addictive for all parts involved, no matter the damages it causes.

Money printing is like a drug addiction, it’s very hard to stop once you start.

The printing will continue, and increase until something breaks.

Lots of tears and shaking and looking deep in the mirror…takes guts. They ain’t got any.

Wolf Said:

During the blowout, and even now, the borrowing pressure in the repo market came from other sources, and banks weren’t lending enough.

The bank in question is JPMorgan (currently under federal indictment for PM rigging) not entirely unexpected as Jamie “Fine Me” Dimon’s leadership buries this corrupt institution under scandal upon scandal with impunity. It bears repeating that when JPM withdrew from the repo market to fund its own stock repurchase agreement, it demonstrated no regard for the destructive fall out it would cause. And what does the FED do? Fills the hole that JPM created in the repo market and it’s business as usual.

How did the USA become so corrupt so fast? What a shame.

Jamie “Fine Me” Dimon

Neat. Haven’t seen that one before. It says it all.

AIUI, it was in an interview with Elizabeth Warren I think. Anyway, DuckDuckGo ‘Jamie “Fine Me” Dimon’ and you’ll get hits related to the incident.

Regulation doesn’t work if the regulated are too big to fail, obviously. If breaking the rules pays why would you not break the rules? So much better are systems in which cheating doesn’t pay. Systems in which breaking the rules mean you automatically lose out.

Quote:

According to the most recent 10-Q that JPMorgan Chase filed with the Securities and Exchange Commission, from September 30 of last year to September 30 of this year, the bank reduced its cash position that was predominantly held at Federal Reserve banks by $145 billion from $344.66 billion to $199.8 billion. During the same period, to meet its required level of High-Quality Liquid Assets (HQLA), it increased its securities holdings by $147 billion.

JPMorgan’s Capital Return Plan (2019):

Under the new plan, JPMorgan will hike its quarterly dividends by 12.5% – from 80 cents now to 90 cents a share beginning Q3 2019. This works out to total dividends of $11 billion assuming average outstanding shares of 3.1 billion for the next twelve months.

The bank will also repurchase $29.4 billion worth of its common shares over this period.

So, where is the corruption here?

So, where is the corruption here?

Are you referring to JPMs criminal complaint? They got caught rigging the gold and silver desk and other charges actionable under the federal racketeering statute. The FED is also committing Federal crimes related to their “not QE” intervention in the repo market.

The topic is and was the Fed Repo and the T bill purchases which both expand the Balance Sheet. It was not about manipulating the gold or silver market or price.

Quote:

It bears repeating that when JPM withdrew from the repo market to fund its own stock repurchase agreement, it demonstrated no regard for the destructive fall out it would cause. And what does the FED do? Fills the hole that JPM created in the repo market and it’s business as usual.

As far as I know, JPM Holdings is bank and a dealer-broker. They only have an obligation to serve public banking and to bid on Treasuries. What legal obligations do they have to provide liquidity in Repo ???

Imafan:

They don’t have any legal requirement to fund repo. Where did I say that? JPM created moral hazard by withdrawing from repo funding to commence stock buyback. This plainly illustrates their blatant disregard for the destructive impact their actions had on the repo market. This should come as no surprise given CEO Jamie Dimon’s long track record of scandal, driven by his lustful, despicable greed. What’s worse is the FED’s stonewalling with excuses thereby enabling what appears to be an interest rate arbitrage. I submit the FED is out of regulatory compliance on this and more. oh well.

JPM topic: I think what JPM did was making a big bet on longer-term Treasury bonds, using their reserves to buy them, in anticipation of renewed round of QE at the long end to bring the price still higher.

Fed and Powell responded to JPM by saying: No QE for you! We (Fed) won’t do QE and buy long end, we will only buy the short end. Screw you and your front-running, JPM!

Don’t fight the Fed? Even if you are mighty JPM?

Who knows how short the short end really is.

I would welcome insights to better understand Fed actions, as I am not a financial expert.

Given that the US government continues to run significant deficits and that balanced budgets do not seem likely in the horizons, why is the Fed moving into short term financing?

It might seem more sensible to lock in ultra low rates while we have them

This approach seems to make the US very vulnerable to any spikes/increases in interest rates.

Of course, balancing budgets and living within our means also seem sensible to me.

Thank you in advanced.

Clarification:

The current Fed’s approach (of moving its debt to shorter term from longer term) seem to make the US vulnerable to spikes/increases in interest rates

Don’t hold your breath for an answer. The FED is trying to pass off the lame excuse that it’s part of its open market operations so it doesn’t have to disclose to shareholders and the public who they are. Add to that, the loans are 42 day loans and open market operations don’t last 42 days.

There real question is what/how many financial crimes has the FED committed and will it get away with it?

Sandy Toes,

The US Treasury Department (US taxpayers) is in charge of financing US deficits. It does so by selling bonds. It sells all kinds of bonds, from T-bills to 30-year bonds. These bonds are purchased by investors all over the world. This forms the US national debt, now at over $23 trillion. So it is the Treasury department that is “locking in ultra-low interest rates” when it sells long-dated bonds.

The Fed is one of the buyers of these bonds. It buys these bonds with money it creates, and thus it puts new cash into the market that then needs to go somewhere and drive up asset prices (hence “money printing”).

The Fed’s actions impact the bond market by pushing down the yields of the bonds it is buying. So now the Fed’s focus is on short-term T-bills, and yields are in the 1.5% range on those. The Fed’s shift away from longer maturities is allowing longer yields to rise (10-year now at 1.84%).

Wolf

Thank you for taking the time to clarify how the US Treasury and the Feds work and why the Feds are pursuing short term debt.

It helps.

Wishing you well… and keep up the good work!!!

The fed is anchoring the short end of the yield curve to control where it goes and doesn’t go. They are trying hard to keep it above zero. The low end of the yield curve impacts the high end by containing how far away from the bottom it gets. If the low end is 1-2%, the high end will never be 15%+, too nonsensical a curve historically.

This and dumping MBS points to them wanting to be on the short end of the yield curve.

Fed policy is Reverse Repo at a lower rate than EFFR. They are able to keep a bid on rates, at a lower benchmark by adjusting the volume, while the excess spills into the stock market. YC is not their real concern and by evidence that measure has lost momentum. https://www.brookings.edu/opinions/for-the-fed-is-it-1998-all-over-again/ Fed rates then were 5% but at the low of the 94 bond massacre they had dropped to 3%. By analogy we might guess the Fed today is also afraid of a violent reaction in long term rates, and a vacuum in liquidity at the short end. They are basically trying to suppress a rise in yields of longer maturity bonds which would have devastating effects.

We will reduce the balance sheet and normalize rates when unemployment dips below 6.5%…Ben Bernanke 2009

The Fed suspends supply/demand price discovery by providing fake demand for government securities.

A tenet of Socialism is economic decision making and planning by the unelected behind closed doors. This is Central Banking.

Central Banking is Socialism and backdoor Globalization.

What a complete 100% reversal of what the Fed was doing about year and more ago!

Today we have QE4.

Today we have falling interest rates.

Today we have bigger asset bubbles.

We have bubbles that are bubbling more with the Fed firmly in the Pro-bubble corner.

And nothing bubbles up in a straight line!

Hawkish gradualism has been replaced by hawkish dovism.

And the implication for real estate bubbles are obvious: real estate over all will bubble up again, but this time face head winds from exiting Asian money and the always there demographics of baby boomer downsizing.

The dome and gloom real estate prophesizers will be disappointed as long as the Fed is on it’s present course.

Wealth and assets will just continue to do just what they have been doing: concentrate more and more to those who already have it and most others will fall steadily behind them.

” and the always there demographics of baby boomer downsizing.”

Is that a real factor nowadays? In my country baby boomers hold most of the RE wealth but most of them are NOT downsizing because there are hardly any suitable properties for them to buy (smaller but high quality, adapted to old people with good nearby services etc.). Most of the luxury housing for older people is in practice only accessible to those without money or people with severe medical problems, others are on their own.

I see countless examples of this in my area, old people who are living in huge homes, bought for close to nothing long ago and now on the market for ridiculous asking prices that no younger person could ever afford. The boomers “deserve” these asking prices and most of them will probably never sell. If a home is sold it is usually to some equity locust from an even more expensive part of the country, or to a developer who splits it up into tiny city apartments with hugely inflated prices, which further increases the bubble.

While it is nice for the boomers that this makes/keeps them all RE millionaires on paper, in the end I doubt it works out. I know several of them who are getting too old for their huge homes and huge gardens and would like to move, but they have no options. The government only allows building of huge family homes in the suburbs (targeting the typical younger two-income family, and for government this means they get the highest price for the land) or social housing, but almost nothing new for older people. I spotted an apartment complex with a golf course though in a nearby city, with pretty modest apartments priced for millionaires – maybe they are onto something?

If the FED is easing, it’s under legal obligation to disclose to the public all of the institutions it’s providing these funds to. The FED has transgressed against the governing authority it is subject to. Where is Congress? Oh yeah- busy engaging in self serving political witch hunts.

Except it’s not a witch hunt. It’s a legitimate abuse of power but I guess that’s not really important anymore.

Objection, conclusion. :-p

Wages up, employment up, unemployment @ 50yr low,

Let the clown show continue. Keeps their attention away

from working America. But of course the sky is falling.

Real estate is down in NYC due to factors having nothing to do with interest rates. The majority of real estate in Manhattan is not financed through traditional means, if at all. The new tax law affecting deductions is one factor, a new higher millionaire’s tax affecting closing costs is another, and more importantly a new law not allowing buyers to hide behind a blind company name is scattering the rats away.

There are other cities which are doing things to contain the housing bubble. I think it was Minneapolis which recently restricted the building of single family homes.

Umm… restricting building new homes for no other reason than to contain prices doesn’t sound like a good plan to me.

agree, in my country this works great for driving UP prices ;)

They are restricting single family home builds in favor of multi family housing with a minimum of 3 units per lot.

Buildings are assets, not commodities, goods, or services. When you feed an asset bubble (by either providing more of the asset and/or cheaper money), assets go up. Supply & demand theory is completely unable to model asset bubbles. Only when the asset bubble pops, does S&D theory begin to to be applicable. Real estate, especially primary housing, is highly illiquid and “sticky” on the way down, so even then, S&D theory doesn’t work like it did in that nice, simplistic graph you saw in your Econ 1 textbook that most people exposed to it erroneously think is a universal “law” of economics.

Communities that are trying to slow down skyrocketing housing prices by restricting assets that feed that bubble are on the right track, despite the simplistic nonsense taught in Econ 1.

@Petunia:

OK, a selective restriction might work indeed.

It might even work in my country, especially if instead they start building cheap homes or apartments for small families. In my country a small home can be build nearly everywhere for 75K euro including land (very small garden included). But despite one successful experiment (with 100x more potential buyers than homes available), no politician wants that because without such options even the worst possible old home can sell for about 300K (which is the amount for which the average worker can get a very cheap an risk-free mortgage).

But very difficult to predict how the RE market responds to such changes given the huge incentives to play and to cheat.

Vancouver recently added a 5% tax to housing left empty, i.e. not being occupied by either the property owner or a renter (with renting required to occupy the property for something like at least half a given year and only counting tenants whose stays are no shorter than at least one month, so most Air B&B operations won’t count). This is in addition to the 15% additional sales tax on real-estate transactions for non-residents added about two years ago. The once bustling “Beautiful Empty Homes of Vancouver” blog that documented the entire towns worth of large rotting empty mansions in West Vancouver, has now been retired because those mansions owners are desperately renting out the bedrooms in these places to everyone and anyone who can possibly be used to fill them; even college students of questionable trustability: https://www.bloomberg.com/news/features/2019-04-16/college-kids-are-living-like-kings-in-vancouver-s-empty-mansions

That should mark the end of the current Vancouver housing bubble. But who knows how long it will take for it to bottom out now that it is deflating especially as a ridiculous amount of new space is coming on-line in the coming years and this bubble has been decades in the making.

Interesting, does it really work like that in practice or are there clever workarounds (like renting out on paper, to virtual renters?) just like with the sales tax for non-residents that apparently didn’t consider the possibility that speculators register and buy as a native company and skip the tax (don’t know if that is still a valid workaround?).

In my city the prices could crater if such rules were applied, because the amount of empty homes/apartments is much larger than the real market could absorb without huge (over 50%) pricecuts. But I don’t see it happening, the only new rule of the game that has been announced for now is a 6% tax for speculators that isn’t official yet. And knowing the Netherlands, it will be extremely easy for real speculators to skip the rules and again pay zero tax like they are used to, probably only some small house flippers will feel the pain. A tax for empty homes is even more remote possibility here, in fact an owner can save some taxes and other fees by keeping the home empty. And local politicians love empty homes (unfortunately, a big chunk of the better-off citizens too); admittedly, for the neighborhood empty homes may sometimes be better than having them turned into Airbnb rentals or student/migrant homes.

Its a good question nhz. Someone may find a work-around eventually, but it seems like it is working correctly for now as air b&b emperors, flipers, and lots of never-show foreign owners are both spooked and pissed.

one must remember that the fed is now the central bank to the world.Europe is where the problem lies as the banks are in such horrible shape that they don’t trust each other and won’t lend. They are insolvent if marked to market. How long this can go on is anybody’s guess. I’m guessing year end might be interesting as they have to square their books.

The Fed is out of control. And, as the 4th branch of our government has no checks or balances.

Good bye republic and hello “social democracy”.

B

The Fed is not a 4th branch of government, any more than the Post Office or the VA. All of them are legislative creations of the US Congress. If you want to fix the Fed, engage the legislative branch.

Wolf: Thank you for this site and insight into the FED and repo “QE(not)” bailout. I have so many more questions. For instance what happens if a repurchase agreement itself defaults and the collateral is released? Does this ever happen and if so what are the repercussions?

It seems to me that as the U.S. Dollar (U$D) seems to be the reserve currency of the current global economic system and that this can go on for a long time as long the FED is supported by foreign capital. It seems to be in everyone’s best interest to “keep playing the game” and not have a global audit of who owes who what.

“what happens if a repurchase agreement itself defaults and the collateral is released?”

A repurchase agreement is a “sale,” not a “loan,” so securities get sold for cash, and the Fed owns those securities. If the seller defaults and cannot buy those securities back, the Fed gets to sell them to someone else. This is generally structured to be a profitable deal for original buyer (in this case the Fed) and punitive for the seller (Fed’s defaulting counter party). So it discourages defaults. And if there is a default, the Fed would come ahead.

So if a foreign “repo-sellers” default, they lose the collateral they offered entirely. As many of these sellers are foreign banks it might export and accelerate contagion of a liquidity crises to other foreign counter parties? That could be bad, right? It reminds me of the Asian Flu of 1997. How could the Fed fix repo-defaults if they start happening? Perhaps discount the repurchase? Hey wait isn’t that a negative interest rate? Would the FED pay interest to sell repos?

Am I out of step here?

Well, let me say this, if any big bank, foreign or US, defaults on a repo or on anything else, all heck will break loose. None of the big banks defaulted on anything during the Financial Crisis, and look what we got. Now imagine what we might get if one of them actually defaults on anything? It will be brutal and sudden.

But I don’t think that’s the case here. I don’t expect a default from a big bank. Even foreign banks can get funding in a routine manner either from their central bank or from the Fed (“discount window”). If anyone defaults, it’s going to be a smaller non-bank player, such as a mortgage REIT that uses the repo market to fund its mortgages. They don’t have access to the Fed’s discount window. But even a default by one of those players could shake up the market and make some big ripples. I discussed this here:

https://wolfstreet.com/2019/11/06/whats-behind-the-feds-bailout-of-the-repo-market/

It’s more like a pretend sale of pretend securities and pretend interest rates while they pretend to obey the law. The reality of it is so dirty it makes Bernie Madoff look like fiduciary of the year.

I better skaddadle. I’m over my limit.

Relevant to this and my larger question is don’t these same firms have to buy these securities back at the end of the repo term?

and if they cannot ; is there some disclosure of this default or are they allowed to sell more to fed to “mask” their default or inability to buy back ?

I.e. isn’t there any mechanism by which these firms are estopped from selling more back to the fed?

Stan,

I just don’t think this is an issue. The issue is that firms that are borrowing in the repo market might not be able to borrow in the repo market, which could cause that firm to collapse. Its counter parties in the repo market would still be OK, owning the securities, but contagion from the collapse could spread far and wide, if the firm is large enough.

Re: “What happens if a repurchase agreement itself defaults and the collateral is released? ”

First of all, the Fed only does repo with PRIMARY DEALERS.

Second, in the Fed Repo, the Borrower (Dealer) pledges Treasuries or Agency, and promises to buy them back at the end of the repo.

But what exactly do you mean by “buying them back”.

In the first leg of the repo, the borrower is lent “money as RESERVES.

In the last leg of the repo, the borrower buys back his collateral with RESERVES.

If he fails to buy back his collateral, the Fed keeps his collateral (Treasuries and Agency) or sells them.

Looks painless, right. After all the collateral is GOVERNMENT DEBT.

In other words the Fed Repo increases Primary Dealer’s (owned by bank holding comps) Reserves. They hope the banks will lend their other freed up cash in the other PRIVATE Repo.

In billionaires we trust.

We give them trillions of dollars if they fail;

should they win, they keep the proceeds.

Reversing this policy ( so Homer Simpson gets it instead )

would be disastrous: rising inflation,

rising interest rates, massive unemployment,

greater reliance on the government

— long lines for toilet paper.

Ever since the beginning of the ONGOING great financial crisis a decade ago, so-called TBTF banks have been ruling the waves. TBTF bank CEOs are TBTJail. The military-industrial complex has been TBTF ever since the end of WWII. The US’s perpetual wars are, if history is a guide, TBTF, because their failure would cause the US’s war-based economy to fail, and the US’s economy is, a priori, TBTF. The US stock market is now TBTF (or TBTDrop, whichever you prefer).

It is prefectly obvious that all of the above TBTF are literally holding the present whatever-you-want-to-call-it “economic system” hostage. The Fed is paying them ransom (“profit”) in order to maintain/sustain the present economic system — the “living end” of centuries-old “arrangement” in which a microscopic percentage of the human population owns or controls the vast majority of LARGE SCALE capital equipment, land and wealth, upon which the vast majority of humanity vitally depends.

What does the future look like? When, not if, the Fed outright starts buying shares in TBTF US corporations (instead of doing so by using foreign CB proxies), you’ll know the end of the present arrangement is near.

There is more to the repo market than what the easily available data suggests. First of all, the repo market is “private”. Some of it is Centrally Cleared, e.g. Tri-Party run by the DTCC. But a supposedly huge and growing part of it is Bilateral and does not necessarily use the Tri-Party clearing system which has only one clearing bank – BONY.

The bilaterals (like Tradeweb) are rather bespoke and do not have to report to the Fed. DTCC chooses to share their data with the Fed and that is where most of the alternative reference rate like SOFR comes from. DTCC runs the tri-party repo, GFC repo, and the tri-party clearing services (that some bilaterals and the Fed repo uses to clear their transactions).

The Fed repo is essentially bilateral because the Fed cannot allow the DTCC to be the “supra” party in the transaction. Therefore, the Fed repo is not net-able (like the GFC repo is) and counterparties settle have to settle each transaction itself, but they use the tri-party CLEARING system.

Rather than describe players (e.g banks) as borrowers or lenders; it is better to call them as Liquidity Providers because they often take both sides – repo and reverse repo – of many trades.

When the Fed wants to control interest rates; they actually have to influence the repo markets. Think about what I just said for a second. An un-elected body (backed by the taxpayers) is essentially becoming a huge part of the wheeling and dealing of government debt. The takeaway from this is that Private Money was not enough to accept the LOWER RATES that the Fed was comfortable with, so they had to step in and run the show.

Print baby print. Dow +30k on the way . The Big boys are taking it off the table in these side-way dips which are followed by an engineered re-bound. Pension,ETF money is on auto-deposit , Big Boys extract a taste and cycle repeats on the way to 30k and beyond. If Pesky Gold raises its inflationary head ,no problem-mo, a few billion of fiat naked gold future contracts will slay that beast. If the Stock Market tries to correct on fundamentals , I DO NOT THINK SO, the Plunge Protection Team armed with a trading desk at the FED will not allow that lucid twitch to happen. The really best part is that most of the western world Central Bankers are in the game, this gives it legs and staying power. Treasuries?, most people don’t even know what they are other than they must be safe or our government would not print them,therefore lets do more. Booze and circus and cheap gas therapy will mollify any reaction.Post WW 2 dominance by the US as the reserve currency coupled with the best scheme of all time , the petro dollar, has turned out to be good for those in the game. The rest not in the game can fight over politics while gamers are busy liquidating the non-gamers. So Print Baby ,Print.

You are right. Either you figure out how to play this game and then play it; OR, you will be left behind. It’s as simple as that, whether we like it or not.

Learning to adapt is part of living.

Yep- play the game and play it well and when it asks you to turn your back on your principled foundation, integrity, self-respect, respect for others, honesty and decency and replace these virtues with the empty promises of greed and naked ambition, that’s living. Isn’t that right?

agree, better to figure out a way for not playing the crooked game and still surviving; but it ain’t easy :(

Play the crooked game, sacrifice your sense of self and ensure your own destruction.

Pursue the things that can’t be bought or sold and these will never be taken from you. These will increase your chances of survival as well as those who follow your example.

Wondering when the Fed is going to make its next course change?

Strong employment report supports “no more cuts”. Maybe the time for tapering of the not-QE run-rate comes in January, after the year-end balance-sheet window-dressing needs? Or will it be pedal-to-the-metal through the election?

Since reserve levels are being managed by repos once more, when does the failed alternative (IOER) get trimmed back? Whose ox does that gore and what handout will they get in exchange?

Will we get a return to financial prudence in 2021? Ever?

How do we end the fed? I’m serious. These people are financial war criminals with their endless trillions in money printing.

If someone like Bernie Sanders were elected, do you think he could expose this and somehow bring about the political will to make a change? Do you think he would?

These are serious questions. If the political counterculture can’t do it, can anyone?

No way. The corruption is the system and vise versa. It’s beyond the scope of a POTUS, sad to say.

Why is this corruption?

Isn’t it just the U.S. way of life?

The GOLD standard left the station in 1971 and we have been in the FIAT bus since.

You might not like it or agree with it, but that’s they it is.

Who is to judge what is right or wrong?

Either you have enough money to live or …

Imafan:

Corruption is immutable, self-evident and defined by the things it produces. You really don’t know this?

No Empire pauses and self-corrects. The Fed is our Empire,our republic is their spoils . The Fed will go when it has depleted our currency by be-basement and the time value of money to zero.

Several ways to end the Fed:

1) re-elect Andrew Jackson and he will bully them until they are extinct

2) Congress revokes the federal reserve act

3) I frequently hear a rumor which I am unable to validate that the US Congress has an option to buy the Fed for a low price- interesting question who would they pay? I’d really like to know

4) educate enough people about the nonsense of fiat currency, reserve banking, central theft (aka central planning) and encourage them to only accept real money for their wages- if 300 million do this the Fed is toast

4) create a new polítical party that actually follows the constitution and drive it to dominate all federal offices and then use political might in all 3 branches of govt to end the Fed

5) wait for Jesus to do it when he returns

6) some other non-recommended way- I oppose any unlawful method

And really the trick is to End the Fed and also prevent the fedgov from replacing it with another fiat currency

Jerome Powell has dropped all pretense of being a responsible central banker, and instead has embarked on a counterfeiting spree set to exceed the deranged money printing of his inglorious predecessors, Zimbabwe Ben and Yellen the Felon.

No such thing as responsible central banker

End the Fed and end all central banking forever (and lots of other central things too)

Yes, looks like Jerome is out to steal the record from Rudolf von Havenstein or Gideon Gono (don’t know which of them is ahead in the official records).

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks…will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered…. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.” – Thomas Jefferson in the debate over the Re-charter of the Bank Bill (1809)

Unfortunately your quote is a fake, but I like the idea:

https://www.monticello.org/site/research-and-collections/private-banks-spurious-quotation

Did the research and read the article. Although the actual quote appears fraudulent, Jefferson is quoted (from a letter) as saying he believed that “banking establishments were dangerous than standing armies”

So there is little doubt as to where he stood on the subject.

The Democrats used to have dinners honoring Jefferson-Jackson. One thing both had in common was intense opposition to big banks. Jackson was the President who closed the first version of the Fed.

So, of course, in todays Goldman-Sachs, JP Morgan version of the Democratic Party, Jefferson and Jackson are both smeared and their new hero is the early champion of the big banks Alexander Hamilton.

\\\

Breakinng news: The jellybean market is colapsing, government is stepping to ease the situation. Senator P. has stated that all preacutionary measures are taken to stabilize the market. The jellybean securities market have since recovered 6 000%, and are projected to grow infinitely.

\\\

On an unrelated topic:

The general surgean is suggesting a steady diet of Jellybeans, indicating that it has health benefits.

\\\

On another unrelated topic:

Scientist show that consumtion of jellybeans increases test outcomes in school. Senate has already passed a bill to make jellybeans a staplefood and an integral part of lunch for every school kid in the country. The fears of high sugar causing liver failure or diabetes are missplaced as the jellybeans contiain only wholesome jellygar-saharose, which is not the same as sugar.

\\\

Breaking news: Global warming is caused by well informed readers. It has shown that a lot of correct information can cause elevated blood pressure and body temperature, affecting the climate adversly. Effective immediately all sites that provide information not dumbed will be shut down. If anyone approaches you and suggests getting informed, or you see someone reading please inform your local police station.

\\\

On an unrelated topic:

Congress has been informed that there is a wikipedia page relating to “standards” in Russian. Hence the phrase “emission standards”, or word “standards” are removed from English dictionaries as they are believed to come from Russia…or China.

\\\

If an economy depends on bringing future spending into the present by destroying savings, that economy is doomed regardless of NIRP, for eventually the cash runs out and spending declines anyway.

NIRP also says the economy that needs NIRP is sick unto death and doomed to an implosion of impaired debt, over-leveraged risk-on bets and asset bubbles generated by stock buybacks and central bank purchases of risky assets.

I have an unrelated question To MR.Wolf

The Index Funds rebalance in low-cap indexes without risking losses, Do they cause massive spikes in some stocks? and How do they prevent losses in illiquid market?

QE,

Yes, rebalancing small-cap indices impacts prices of those stocks (up for the ins and down for the outs). The rebalancing is announced in advance, so the stock price movement is not all in one day, but usually over time.

Thanks for the reply Mr Wolf, Always a follower of your website. (I have my adblock disabled).

Keep up the good content.

In reality, Central Banking = Parasites of Humanity like the fake governments !

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around [the banks] will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.” — Thomas Jefferson

“When it comes to bailing out its crybaby cronies on Wall Street, even when there isn’t a crisis, the Fed stops before nothing”

It amazes me how voters consume the propoganda that so-called “socialism” will ruin them and the economy so they must oppose any “socialist” program that could benefit them.

Meanwhile the conservative-run FED is going wild with socialist bailouts for the richest of the rich.

We live in a socialist country but it’s only socialist for the billionaires.

There is still no explanation as to why the Fed is in the Repo markets. Remember, the Official Story was that on one single day back in Sept bankers actually started having to pay real interest on their overnight loans. That was for one day. We were told a lot of bull at that time about how this had to do with the end of the quarter and some arcania about how banks had to hold on to their money during certain phases of the moon. Then, the Fed declared an emergency and started pumping $70 billion a day out in overnight money.

Furthermore, there is still not even a vague, fig-leaf of a cover story as to why the Fed started doing 2-week repos and now 42-day repos. (I take it that the number of 42 days was chosen by a Douglass Adams fan).

Why is the Fed having to loan out massive amounts of money for longer and longer periods? If anyone even bothers to ask, we are led back to the cover story of that one single day when interest rates spiked. Which was supposedly a unique occurrence due to the confluence of the end of an accountant’s calendar and phases of the moon.

Apparently, there is someone for whom “give me a loan overnight and I’ll pay you back tomorrow” isn’t good enough, and that its had to extend to “I’ll pay you back in a couple of weeks” and then extended still further into “I’ll pay you back sometime next month”.

Its still a likely candidate that its Donald Trump’s bankers at Deutsche Bank who are in big trouble. And they are apparently tied closely into other massive banks in counterparty derivative deals. The bankers are apparently scared bleep-less that the whole thing can come crashing down and that if they make overnight repo loans like they’d been doing they might be the ones without a chair when the music stops. Thus, the federal electronic printing presses are running non-stop, because of course in this fantastic version of capitalism is the public that has to carry the risks.

Doc,

Your last paragraph is kind of fun to imagine. But in reality, the US unit of Deutsche Bank (which would be the unit in the repo market) can borrow at the Fed’s discount window, no problem. No bank is forced to borrow in the repo market. They can all borrow at the Fed’s discount window.

The borrowing pressure came from somewhere else – such as mortgage REITS that HAVE to borrow in the repo market because they do not have access to the Fed’s discount window. What we do know is that banks weren’t LENDING to the repo market when rates jumped.