Most other regions in the UK cling to price gains.

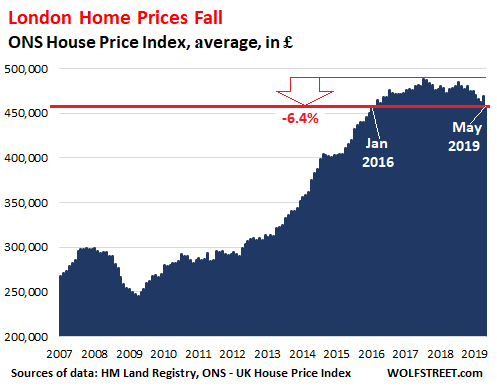

Home prices in Greater London – all types of homes combined – dropped 4.4% in May compared to May last year, the biggest 12-month drop since August 2009, to £457,471 ($569,000), the lowest since January 2016, according to the UK government’s Office for National Statistics today.

The average price has now fallen 6.4% from the peak in July 2017. The central areas of London have for years been among the most magnificent housing bubbles in the world, but the hot air is now decidedly coming out of the market:

Unlike US home-price index providers, the ONS is not squeamish about calling its House Price Index what it really is: a measure of “monthly house price inflation.”

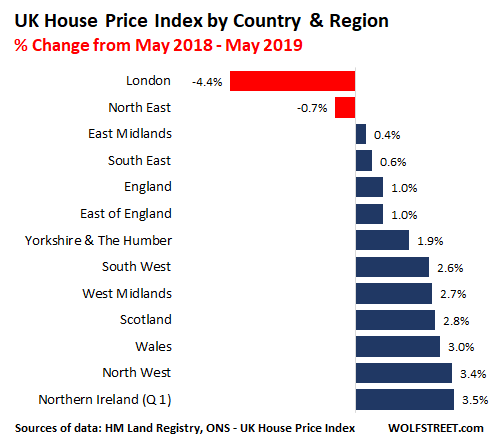

But these types of home-price declines prevailing in London have mostly not spread around the UK. A different picture emerges for each government office region and country. On a year over year basis, the House Price Index declined in only two of them: in London and the North East. Everywhere else, prices rose on a year-over-year basis:

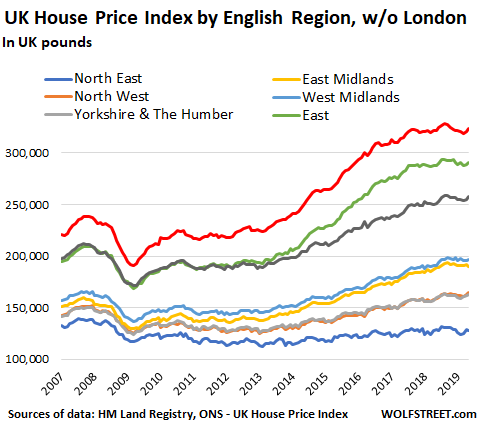

The long-term chart of England’s regions, with the fabulous London whale removed, shows some interesting splits:

The North East (blue line tagging along at the bottom in the chart above) is the only region that has not yet reached its prior peak of 2008.

The North West and Yorkshire & The Humber (the two lines just above the blue line that are so close together you can barely keep them apart) have surpassed their 2008 highs, but only by a small margin.

The South East (red line at the top), the second most expensive region in England behind London (removed from the chart above), peaked in August 2018 but remains within a hair of that peak:

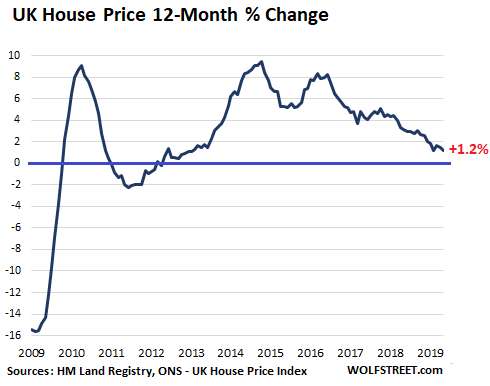

Overall UK home prices, after also peaking in August 2018, have inched down since then. On a year-over-year, they eked out a 1.2% gain in May, weighted down by the decline in the London housing market. May showed the lowest home price inflation, along with February, since January 2013 (by comparison, the UK’s consumer price inflation rose 1.9% through June):

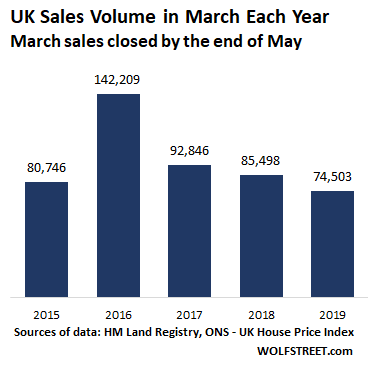

Sales volume in the UK overall has plunged in March every year since the pre-Brexit-vote spike in 2016. According to the ONS, March sales data are transactions in March that closed and were registered by now. With 74,503 such transactions in March 2019, sales activity has fallen below the March 2015 level and has plunged:

- 47% from March 2016

- 20% from March 2017

- 12% from March 2018:

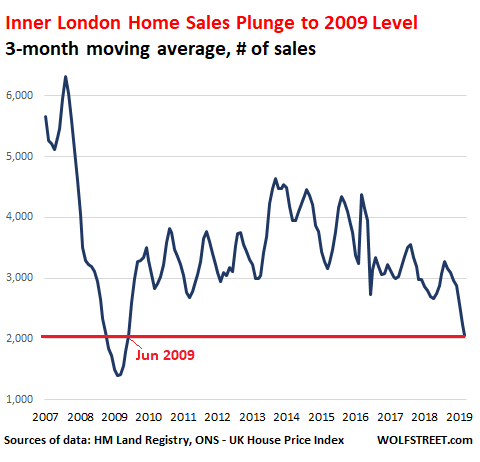

In Inner London, sales volume has plunged by 50% from the mid-range prevailing in the three years from mid-2013 to mid-2016. And it’s down about 65% from the peak in sales volume before the Financial Crisis. These numbers are very volatile from month to month. So, to smoothen out some of the sharp month-to-month ups and downs, I used a three-month moving average. At 2,057 transactions, sales volume has now fallen to levels not seen since the depth of the Financial Crisis in June 2009:

As the low number of transactions show, everyone has a wait-and-see attitude, with buyers and sellers far apart on price, and with most sellers largely in no hurry to cut the price, and with buyers reluctant to step up to the plate.

Prices and activity in London are subject to broader dynamics, and have been falling despite the ultra-low policy rate of the Bank of England. Leading up to the Brexit vote, the BOE had cut its policy rate to a historic low of 0.25%. It has since hiked this rate twice, to a whopping 0.75%. Currently, mortgage rates are among the lowest in the UK’s history. But the London housing bubble is deflating nevertheless.

Factors beyond interest rates have been piling up in the London housing market, particularly the simple but powerful factor that home prices had risen so far in past years that fewer and fewer people who live and work there can actually afford to buy a home there, despite low mortgage rates.

The problem of home prices outrunning what locals with even good jobs can afford stimulated the government over the past few years to act and, among other things, increase the stamp duty particularly on high-end property transactions. This, in addition to the uncertainties of Brexit, has pulled the rug out from under the blind enthusiasm of foreign investors.

The possibility that some of London’s finance industry might move to other parts of Europe after Brexit is also pouring cold water over the once hot market. That some hot air is now hissing out gives rise to hopes – and fears – that a modicum of sanity might gradually return to the market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Assets will deflate. What’s wrong with that?

It just can’t go up in a straight line.

Housing doubles in ten years? What’s wrong with that picture?

6.9% annualized appreciation – less than the expected return of many pension funds … why not!? The Weimar Republic and Venezuela have managed much greater returns.

Oops 7.2 %. Funnily enough the fake math worked out closely.

The Venezuelan stock market soared, but people were hungry and bread disappeared from store shelves.

I wonder if the epidemic of “Knife Violence” has had any effect on these prices?

I have read that the MoD has stated that they are ready to step in to help deal with the problem…

If any readers are considering buying in London and dealing with their concerns about violent crime by buying the now popular “Stab Vests” ( Soft armor) be sure to do your homework first, the quality and efficacy varies greatly.

If you come from an old family check the attic for chain mail.

Whilst it’s terrible that knife crime is so high in london and its blighting the lives of parts of the community who live there, the vast majority of attacks are related to school arguments and gang issues. If you aren’t a teenage boy or don’t have teenage children, it’s really an incredibly small chance that you would be affected as an average professional.

In 15 year living in London, and going out to bars etc, I’ve only seem about 3 fights. If I went out in other areas of the uk, I would probably see fights on a monthly basis.

It’s clearly far from ideal that people are getting stabbed on a daily basis and we needs to work to sort this, but it’s not honestly something I ever found impacted day to day life there. Most young professionals move to London for work, and leave to become commuters from leafy market towns once they start a family.

It would be nice if London was a safe place for everyone who lives there, but the media around the violence is massively over hyped.

Riddle me this Batman.

What happens when the “rich” foreign buyers become desperate sellers joining the ever growing seller crowd?

“The foreign buyers have pretty much all but disappeared,’ he added. ‘I’m helping a lot of foreign buyers get their money out of this country as fast as possible.”

https://www.wsj.com/articles/foreign-buying-of-u-s-homes-suffers-record-drop-11563396472

They liquidate for what they can get – for many, encouraged to London by the UK’s ‘light touch’ regulation which ensures first-world countries become third-world countries, it’s an exercise in money laundering so it’s all free cash anyway as it’s al been embezzled.

Then they move on to the next speculative bubble.

Wealthy – corrupt – foreigners using London as their playground has become a political hot potato as more and more young Brits are priced out of the housing market by speculators. Measures have been taken to get some high-profile court cases going so that the masses are mollified and it’s back to business as usual, attracting these ‘wealth creators’ (ie they create minimum wage jobs in Harrods). But the masses haven’t been fooled.

PS to add – in other words it’s just the same as any other historical bursting speculative bubble. Tulip bulbs, coral, London apartments – the mechanism is exactly the same:

when there’s no bigger fool you get the heck out ASAP and for what you can get.

Hi MD, heard a saying the other day – ‘population QE’ in relation to Australia but the same applies to the UK also. Regards Steve.

Supply will skyrocket, and the most feverish demand that has been making the cash offers to drive prices up, disappears. Asset prices fall. Timbers’ boss cries for overpaying in his bidding war.

The 2016 spike in sales had less to do with brexit and more to do with the added 3% stamp duty for 2nd home buyers

In our area (Islington) where we have been watching the market for quite some time, the price for commodity 2bed 70sqm luxury flats has gone from about 800k to 700k in the last 2 years and is still very soft. However, these types of flats are still selling with these adjustments. Gross rental yield is about 4-4.5% on these things (rents are very soft but not falling anymore), but there are high taxes for investors and service charges can be rather spectacular, so if you’re borrowing at 2% you’re probably coming out even. Not a great investment, but if your thinking is diversification and you’ve already got a bunch of negative yield govt bonds, there is enough there to keep wealthy investors interested. It also amazes me how liquid this market has remained, which is what people have always said about these types of properties, and I guess that is appealing to a lot of investors as well.

By contrast, in the sub 500k range it is completely jammed up. Here there are a lot more owner-occupiers who seem intent on extrapolating out to where prices would have been if the boom had continued. There are a bunch of 1bd 45sqm flats on the market at 600k+. Almost nothing like this is moving, and you see flats in the same block go up for a few months then get pulled, with the cycle repeating every 6 months as the owners presumably hold out hope.

Moving out of zone 1 the picture makes no sense to me. Prices are completely nuts. Flats in Highbury (zone 2) are the same price as you can get in the City. Commute for 30 mins into a prime stabbing areas and you might save 15-20% over the same sqm in central London. In my view the outer suburbs (which experienced huge booms since 2014) are ripe for 40-50% falls. Central London is probably not going to fall much further now unless interest rates go up.

Well when you are paying hundreds of thousands of pounds for a one-bed flat – sorry, ‘apartment’ – in a ‘prime stabbing area’ then that tells you all you need to know about the London property market and its trajectory.

As with ALL bubbles (yours no different I’m afraid), once the bigger fool loses interest the whole chain collapses.

For future prospects, think Tokyo 1990 to around 2011 and you’re about there.

>Commute for 30 mins into a prime stabbing areas and you might save 15-20% over the same sqm in central London.

Hell 40 min commute into kings cross and I can get 3 houses with a nice chunk left over for that.

The London market is screwy.

I suspect there will be a downward presuree in November. There are more EU workers in London than anywhere else (and I think it has the largest per capita population too) plus those wealthy investors will no longer get an EU passport thanks to an empty london property.

That’s before we consider a lot of high end finance jobs moving for euro clearing or passporting.

The U.K. authorities will soon lose control over interest rates as the pound sinks,inflation takes off and the bond markets panic.

… The brexiteers will predictably rant about how this is a good thing and what the majority voted for.

Hi Fajensen, I am a brexiteer but whilst house prices going down in London is not a good thing they have been vastly overpriced for years. Brexit or no Brexit they were going to fall at some point. Regards Steve.

Art, cash, jewelry, gold, un-named benefial owners; where else can you hide hidden wealth that can be passed to generations without proper tax?

I guess you are referring more to the action in “The City”, it’s many tentacles and pirates, and some serious dynasty building, than recent changes in housing prices per se.

All these real estate investments only make sense in a world where bonds are priced so low that real estate provides a better risk-adjusted reward.

But when bonds revert to the average, a 4% risk-free govt bond is a lot more alluring than a 4% annual appreciation in risky real estate investing.

Billionaires cashing out their real estate investments to pivot back into bonds (all at the same time!) will oblityeratte prices worldwide. Just as billionaires shifting from awful negative yeild bonds into real estate pumped up the market in the last decade.

Risky real-estate investing that requires annoying and often very expensive building maintenence and tennant management. No thanks, I see little desire to own more than my primary residence at this point.

True, tenant management and building maintenance is a pain. I deal with that daily. And, I make good money from that, but it takes work. There is risk involved … like a non-paying tenant, They say, no free lunch. Right now, I am fixing lose pool coping … big job. Tomorrow, I have to put in a water heater. Going to Home Depot now. But, I actually like this life better than working for a company.

Real houseprices outside of London are pretty subdued but Prime in London is hurtling towards a distressed cycle

https://twitter.com/robhawcroft/status/1149708394619473920

I don’t see any bubble but I live in Canada where two-thirds of residential real estate in Canada doubled, tripled or quadrupled in price since 2007.

Where else can we put money (our savings).

4 week auction today: 2.090% high rate (taxable)

The banks make 2.35% effective 5/2/2019

Effective Fed Funds Rate is about 2.41%

SOFR overnight repo is about 2.47%

DTCC GCF Repo weighted ave is about 2.582%

1 day LIBOR 2.36275 %

Ah we people are getting robbed. We are making less than the banks who don’t have to do anything.

Over $200 billion of treasuries being auctioned in the next week. We’ll find out how much demand there really is just before the Fed meets and “must” lower rates to stop a worldwide recession

Got a flier in the mail that says that Union Bank in San Francisco is paying 2.50% on a 12-month CD, $10,000 min. You must go to the bank in person to open that account. They also offer a 2.25% money market account. So banks are still trying to attract new deposits.

The Tabloid methodology strikes again. Countered by the Independent (UK):

http://www.independent_dot_co_dot_uk/news/uk/crime/london-murder-rate-new-york-compare-worse-stabbings-knife-crime-teenagers-statistics-figures-a8286866.html

Similar populations, 1/3 the number of homicides, and a complimentary blurb congratulating NYC for getting their murder rates down to that level. Ishkabibble.

Instead of lowering the interest rate why don’t we just lower the debt itself?