The real worry is the economy in the Eurozone.

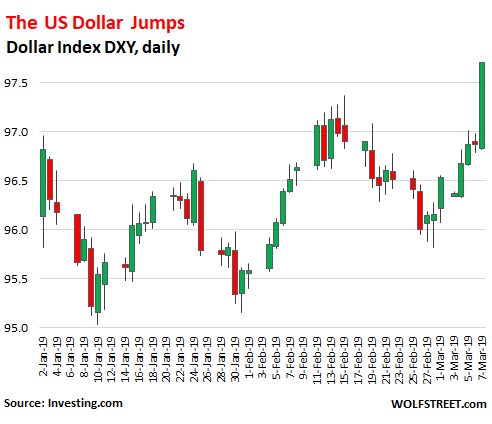

The Dollar Index (DXY), which tracks the dollar against the euro, yen, pound sterling, Canadian dollar, Swedish krona, and Swiss franc, and which is dominated by the euro, jumped 0.83% to 97.71 at the moment, hitting at least briefly its 52-week high, as the euro slumped 1.1% against the dollar, following the ECB’s announcement earlier today. But it wasn’t just a one-day event for the dollar, but an eight-day rally in an uptrend that started in early February (data via Investing.com):

The real worry is the economy in the Eurozone – despite the fabulous stimulus the ECB has heaped on it for years, including a brutal negative-interest-rate policy and massive QE that has inflated the ECB’s balance sheet to over 40% of Eurozone GDP (by comparison, the Fed’s balance sheet is down to 19.5% of US GDP).

The Eurozone economy is deteriorating rapidly. In the post-meeting press conference today, ECB president Mario Draghi announced that the ECB had slashed its economic growth forecast for the Eurozone to 1.1% for 2019, a sharp cut from its forecast of 1.7% growth at the December meeting, and down from its 1.9% growth forecast last summer.

“Incoming data have continued to be weak, in particular in the manufacturing sector, reflecting the slowdown in external demand compounded by some country and sector-specific factors,” the statement says.

Instead of admitting that its radical experimental monetary policies were a colossal error as the economic growth is now dwindling despite or because of the stimulus, and instead of gradually raising its policy rates above the rate of inflation to end its brutal “financial repression,” and instead of shedding the bonds on its balance sheet to push up long-term interest rates and force a restructuring of the bogged-down European economy so that it would liquidate or restructure the debts of zombie companies and lighten the load of restructured companies to allow them to have a fresh start – all of it at investors expense – the ECB does the opposite.

It promises new bank liquidity programs in the Eurozone which is already drowning in central-bank liquidity, to get banks to lend more to these zombie companies and keep them from restructuring their debts.

These targeted longer-term refinancing operations (TLTRO-III) are loans by the ECB to banks at a rate indexed to the ECB’s “main refinancing operations” rate, which is currently 0.0%. The idea is that banks would lend this free money aggressively. In the past, banks used these loans to aggressively buy the government bonds of their countries, such as shaky Italian banks buying shaky Italian government bonds, and collecting the difference while getting everyone worked up about this “doom loop.”

There will be unspecified incentives in these programs to discourage this type of thing, but good luck. The loans would start in September 2019 and end in March 2021, with maturities of two years.

But the last thing the Eurozone needs is more liquidity after having been doused with ECB liquidity. The negative-interest-rate policy and QE have repressed yields and have made dirt-cheap credit available to just about all comers. So the problem in the Eurozone is not a lack of cheap credit.

The ECB has named this program “TLTRO-III” because it’s the third such creature of liquidity injections since 2014.

But at least pushing the ECB’s deposit rate further into the negative and restarting QE are off the table. There appears to be no appetite for them.

Markets were spooked – instead of levitating due to the promised bank liquidity programs. Stocks in Europe sold off, particularly European banking stocks, with the shares of favorite piñata Deutsche Bank – now, there’s something that needs to be cleaned out at investor expense – dropping 5.1% (to €7.75) since the announcement earlier today. The Stoxx 660 bank index, which includes banks outside the Eurozone, fell 1.1%.

The dollar index, against this background, jumped to its 52-week high, a sign that the US economy, including its manufacturing sector, is currently seen as the “cleanest dirty shirt” among the major economies.

More and more voices, including those from current and former Fed governors, are trying to prepare the markets for a Fed rate hike or two later this year — or one later this year and one next year. Yes, they say, the economy hit a soft patch in Q1 due to the government shutdown, delays and lower tax refunds, and some other factors, and Q1 GDP will be lousy. But these voices warn markets that the pace will pick up in Q2 and Q3 to a decent but not exhilarating pace, and that in this environment, the Fed isn’t quite done yet with its rate hike cycle.

That the dollar has been building up momentum since early February and is now at a 52-week high against the DXY basket of currencies is a sign that at least the currency market isn’t totally dead set on a dovish U-turn at the Fed.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Lael Brainard just said that the balance sheet reduction will come to an end in 2019. Some others hint at rate hikes later this year. What exactly are they trying to convey? Or is it confusion by design?

It seems as though the 1-year Treasury has been leading, and the FFR following its lead. The 1-year is getting awfully close to the FFR. If it dips much more, then my prediction is that the Fed will cut the FFR to make it appear the FFR leads.

I guess this could be a Q theory, whatever that is. (And why “Q”? Why not “X”? I won’t fill up Google’s storage of my searches with that, so maybe I’ll never know…)

I think you really should compare the IOER rate currently at 2.4%.

If the short-term Treasury (4 or 13 week) goes well beyond this, then the IOER is no longer the real floor as banks will buy Treasuries instead of holding excess reserves.

Did y’all see the 4-wk market yield this morning?

2.461 %.

Maybe June meeting is the latest date of the next increase.

What about the HQLA that goes into their RWA? I thought reserves are regarded as of superior quality to Treasuries? If this is correct, then I don’t think banks will be encouraged to move into Treasuries if short-term Treasury rate goes above IOER. Or am I wrong on this one?

Is “different” policy.

They are trying to see if another adrenaline shot to the economy is going to work.

It worked for 10 years. Now 2019 is looking like an inflection point. Market earnings potential is near record lows, with historically 95th percentile in stocks.

So in summary, they are confused due to the confusion that is the market. They see the indicators of a deep depression without the bust moment, see China’s GDP infusions, see Draghi’s EU QE’s, and cant seem to get a bearing at the moment. At least that is how I see it.

BTW, BTC is the new indicator for upcoming QE. Its literally pegs to it quite nicely. Nothing says growth in the most speculative of speculative investments like a bunch of ZIRP cash floating around.

She is the closet globalist on committee, Clinton’s choice, she would have implemented Yellen’s request to buy “a broader range of assets” . I would not call her an automatic in case of regime change, but she does represent a consistent global monetary policy alternative, although Powell has praised Yellens day-to-day handling of 2016 mini-recession.

“Ignore the man behind the curtain” Wizard of Oz

Ignoring all the economic mumbo-jumbo for a sec.

With exports decreasing, is it possible to maintain economic growth with a declining population? Japan, South Korea, and Europe need an answer stat.

Yes. People over-estimate declining populations’ effect on the economy. Japan is actually a lot stronger than most people think. It has extremely low crime rates, a very highly educated populace, and population decline has actually trimmed the expenses of their ubiquitous social programs. South Korea has some of the world’s largest companies, so they are actually doing quite well. Europe has issues though, but more related to horrible austerity measures and the abomination that is the EU/Brussels.

“Horrible austerity measures”. Is there a single Eurozone country other than Germany not running deficits?

Germany

“According to our calculations, the German govern- ment saved almost EUR 260 bn in interest payments between 2008 and 2016. However, the current fiscal surplus, which is to a large extent due to these spe- cial factors, should not be used to justify permanent expense increases or cuts in taxes and/or social security contributions.”

That from DB though it is speculative to say exactly what would be without CB monetisation . That interest saving takes away the surplus btw, and deficit is said due also.

Why does a shrinking populace need a growing economy?

I’m in the school that they know what they’re doing, and what they say they’re doing is rarely what they are really doing. I suspect the stimulus isn’t in cheap bank loans, it’s in devaluation to stimulate exports. And the EUR did drop strongly vs. the rest of the world currencies.

The interesting thing about the currency wars is that oddly enough, for all the “trade war” and “currency manipulator” talk, the Chinese Yuan vs. US Dollar has been incredibly stable for the past 10 years. That exchange rate has stayed in the range 6.55 +/- 0.45 yuan/dollar. That’s a variation only about 7% around the midpoint, and with basically no trend. The Euro and the Yen have moved a lot more than that, with the Euro trending from almost $1.50 to only $1.10 in that same time period, a slip of over 25%.

So today Europe printed itself another percent or two of devaluation in order to stave off the inevitable reckoning. And perhaps its feature-not-bug that the extra bank credit comes just before the Brexit hits the fan, and financially-constrained banks might need a bit of extra flex?

Seeker: Central bankers are doing the only thing they know, printing money!

The only thing they change is what they call it! ZIRP, NIRP, now TLTRO!

I have long lost faith in the wisdom of central bankers. They sure think they know what they are doing and try crazier stuff when things don’t quite go as per the plan.

I am very happy with:

– my DXY position

– recent fiscal policies in US that freed the economy from reliance on the Fed stimulus.

– The fiscal policy implemented by the Trump administration is going to be the final straws on the back of the camel called “US economy”.

No, you should read more about what the central banks did in, say, 2008-2011. They have a lot more tools than just printing. The fact that the ECB is doing this policy adjusting using, say, 2-year loans rather than some other policy option is significant. Wolf clearly pointed out that they didn’t do deeper NIRP or more QE. One might ask why? I don’t know, but I know there’s a reason.

BTW, another side-effect of the EUR dropping vs. USD and CNY is that now the US and Chinese have cover to not raise rates (US) and to simulate as needed (China).

LTRO is a form of QE according to

https://voxeu.org/article/ltro-quantitative-easing-disguise

where the monetisation passes through weaker banks into their weaker national sovereign debt lowering yields. So this provides some asymmetric assistance that keeps the negative balance registered in the court of the weaker nations, albeit under the wider amperage of the ECB balance sheet. Lower negative deposit rates are just going to sink everything more without directing the process. “Classic QE” entails purchasing equal amounts of sovereign debt per country, several countries already have negative yield on the short end I think, which is perverse.

Something like that anyway…

That the markets gave a thumbs down is harder to figure. The GDP downgrade was well advertised beforehand. So we single out the TLTRO…was it ECB putting its policy where its mouth was…or not enough of that. I don’t think further easing was written in, but it could be the market leading the way by speculating on a bigger easing, those that did got caught short. Remember a lot of lending in european countries is variable rate, so if rates go up banks don’t nescessarily make a bigger margin, investors in them do, but only if the books stay whole – if borrowers go under they show up negative on the books of banks. So any further easing should be positive for banks in their known circumstance… basically it’s all managed though, so when Draghi said “we’re all screwed” markets just decided to agree this time as he didn’t come up with any new ideas to lift them. I don’t see where they are going to get any real new activity in EU, and if they do try to cash in on any then raising rates will squash it. So short of bringing down more than delinquent structures by raising rates early, using external inflation shocks for example as pretext, it looks to me that EU is going to remain a swamp for quite a while… but people aren’t supposed to consider that I think… so it’s all just a bit of a permanent delay.

Having said all that, I don’t have any real certainly about what will actually go on.

The economy is on steroids, and it will end the same as for athletes, as a wreck. There is no end game, no plan B, and that is the biggest obstacle to the way out. The markets sank because it wasn’t as generous as prior TLTROs, which says it all.

Max-Min: Or as Wolf says “Zombies”!

Maybe Wolf can create a metric to measure our Zombie state!

No doubt the Zombie trend is terminal!

The new Zomb-O-Meter, similar to my Hawk-O-Meter? Hmmmm…

Future Fed Rate Hikes indeed ! Global debt has been growing faster than global GDP for a long time. The Fed tried to tighten money at a snails pace. It backfired.

=>Global debt has been growing faster than global GDP for a long time.

Believe it or not, the government of Chile is actually a net creditor, supposedly because the socialists who have mostly run the country since 1990 don’t let the financial system run the government. They also have a national health care system, although their privatized pension system did get mostly blown away in the 2008 meltdown and has little hope of ever recovering. It also really really helps that it’s by far the world’s largest copper producer, which could put it in a precarious state if its customers have to cut back.

Somebody tried to promote Chile in another thread today as some sort of predatory corporatist success story, and this seemed a reasonable opportunity to mention it.

Look at the 10-year yields in Euroland. I’m surprised Uncle Buck hasn’t gotten much stronger already.

– US interest rates are higher than in the Eurozone because the US is running a Trade and a Current Account Deficit.

So where does all this fiscal profligacy leave poor ole gold and all the bedraggled gold bugs? Is gold really a buggy whip? Anybody buying any PM coverage? I have none…but am wondering if it’s “recognition time”, finally, for gold

Gold is a touchy topic round here because we havent settled the “physical vs. paper” debate. we started to have it, but im still waiting on Wolf to address it (hint hint). IMO gold is going to the moon. And then pluto. That price will not be reflected in the spot price and an ETF will not go along for the ride. go buy some eagles and maples and krugs and buffalos and watching this will not be (as) painful.

Stick with buffaloes and maple leafs, .9999 is what you want, seriously.

If you notice, gold collapsed with Trump’s election in 2016. Everything he has done since then has strengthened the USD and this won’t stop until he end of his term in 2024 maybe longer. Eventually gold will be the beneficiary of the debt collapse but this is easily 10 to 20 years away.

This is what happens when bank bailouts, tax evasion, and other financial scams regularly take over a third of Europe’s economic production, year after year, suffocating the real economy.

The solution is to have European governments tax the rich and regulate the banks instead of the other way around. That’s never going to happen, so instead they’ll devalue the euro, try to cover their collective asses on Brexit as best they can, and hope the coming economic meltdown starts in China or the US so they can deflect some of the blame and keep the plunder going.

Don’t worry about me. I’ll be just fine.

The former artist formerly known as Prince wrote a song about this …

“This is what it sounds like,

when Doves cry.|

LOL

The bottom line is it doesn’t work. They tried stimulus & 0%. The same as the U.S. & Japan. The U.S. has printed trillions & 0% for barely 2% Inflation for 10 years. Japan has been in a deflationary death spiral since the late 80’s. They’re demographics are falling over a cliff. It’s a structural problem that can only be solved by hitting the “reset” button. A lot of pain back when they should have done it. Insurmountable pain the result now of their foolish monetary policies.

Germany is weak & Europes biggest bank – Deutche bank – is up to its eyeballs in derivitives (bad loan) exposure. Italy’s banks are insolvent. France is in a social crisis. It’s a bad time for Europe.

The dam is strating to crack with weak underlings all around and it’s scary as hell. Yes the U.S. is the cleanest dirty sheet but the world is intertwined economically. The USD is getting stronger for a reason. We’re still at the bow of the Titanic busilly rearranging deck chairs. The rest all already scrambling for the too few life boats..

I liked this analogy, it was quick and pertinent!!

With the EU booming [sar] maybe Brexit is in the long term is a smart move for the UK Maybe the people got it right ? Not the Elite.! I wish them well.

So the desired result is for banks to “lend this free money agressivley”. Is there a high demand for loans in these economies thats not being met? If they truly are zombie companies why would a bank lend them anything? Is the gov. gonna garauntee the loans or something?

They gonna find theyselves “pushing on a string” one day.

Wondering what this latest move from Draghi means for the SNB?

The Swiss have worked hard to debase the franc in order to maintain parity with the Euro. US$ hit a new 52-week high against the Euro today. Does the SNB continue to tag along in the race to the bottom? The way they’ve been operating in recent years was something like print francs, buy Euros, convert Euros to US$, buy U.S. equities, sit back and collect dividend checks.

Sweet….sweet irony! Strong dollar and the us consumer can buy more import stuff cheaper and have $ left for ummmm what you call it , oh yeah , savings. Corporate globalist will have that threat removed quickly as Their interests come first in DC.This strong dollar will be dealt with quickly,,,but one day it will not work and We will be left with a dollar that will not buy much . You only get a finite # of bites of the Apple.I do miss Larry Kudlow running around yelling KING DOLLAR

The drugs aren’t working anymore and never did much to begin with. Along with slower real economic growth there will also be a stagnation in productivity. I cannot believe all these smart economists don’t understand this. Everyone is just kicking the can down the road and doing “whatever it takes” with other people’s money. Draghi wants to exit and retire on a high note….a note that might very well be elusive.

You said it well Wolf:

“Instead of admitting that its radical experimental monetary policies were a colossal error as the economic growth is now dwindling despite or because of the stimulus, and instead of gradually raising its policy rates above the rate of inflation to end its brutal “financial repression,” and instead of shedding the bonds on its balance sheet to push up long-term interest rates and force a restructuring of the bogged-down European economy so that it would liquidate or restructure the debts of zombie companies and lighten the load of restructured companies to allow them to have a fresh start – all of it at investors expense – the ECB does the opposite.”

Smart economists eating jumbo shrimp with honest politicians.

Forex is going to blow up. Armstrong says a ramp up in the dollar will be the final act. (Then Plaza Accord II?) Half of all derivatives are written on currency, and almost none are registered. Europe holding the line at ZIRP represents a more hawkish stance than NIRP?

The price of crude will collapse, and interest rates, as US reverts to the global MEAN. We can’t escape their policies, look at the dollar! Gold is waiting patiently. End of times.

Obviously, the roll out of the stimulus and the behavior modifying negative interests rate has not had the desired effects. But I think we can attribute this to a poor communications effort, better marketing is needed to make people believe. Free money is no good if people just don’t understand what it means to not take up this free money.

There are ample models that Mario can find within Continental Europe to launch such campaigns. But if he is unable to find the right examples, then, let me speak to you more directly, Mario, my friend, simply come to Wolf Street, there are plenty of people here who can give you marketing tips.

Consider for example the program name, you call it the TLTRO-III.

Seriously, what is that? No one can even pronounce this correctly. One would’ve assumed you had TLTRO-I and TLTRO II as well, both probably so uninspiring that nobody even bothered to look up what the great program was all abou.

You could call it TITS-III and make up the words to the acronym and that’ll get people’s attention, well, at least the male half of the population. Then set up a website to explain it. People might click on the link out of curiosity or simple misunderstanding. Yes, it could be called clickbaiting, but that’s just such a negative thing to say.

But we can make this even easier, let’s assume you are too laz… overworked to come to Wolf Street for advice, let me suggest a different naming scheme at least, one that you can base a campaign of understanding around. It’s been applied successfully elsewhere, and the acronym is even a real word and makes people think big.

MEGA “MAKE EUROPE GREAT AGAIN.”

@MCH

It goes way beyond marketing.

See this paper as well as Wolf’s article on the same.(see below) And it goes far deeper than the citation below. Structural issues with debt and excessive leverage are not being dealt with for obvious reasons. The withdrawal of stimulus is and would become ever increasingly painful. It is classic addiction behavior and classic procrastination and “kicking the can down the road.” They’ve clearly chosen the easy way out and there’s about a decade left until monetary policy, which is becoming increasingly less effective with time, will become impotent. There’s talk of nationalization of our corporations to support outright purchasing of equities. This would be one such solution to continue to keep the equity market amd sentiment afloat.

The other alternative is to allow a complete reset and allow price discovery to clean out all the debt and bond structural issues and clean out the zombie corporations. We would emerge far more productive and eventually realize that long term sustainable real economic growth that global economies are yearning for. But no one wants to go through the pain.

The US is a global leader and Powell had the opportunity to lead by example. He did this, but in the wrong direction……..

Here’s that article. Wolf summarized it in an article….

https://bfi.uchicago.edu/sites/default/files/file_uploads/BFI-MFRI-2019-09.pdf

The whole European banking sector is still in an enormous mess ten years down the line. Greek banks still sitting on 60% non performing loans. Spanish and Italian banks being supported by 350bn ECB funding still. Deutsche Bank merging with Commerzbank to try and save it. Also the news stories ref the banks money laundering. Complete mess.