The largest three-months fall “since at least the 80’s”: CoreLogic

“Can we still describe this as an orderly slowdown in housing conditions?” mused CoreLogic Asia Pacific’s head of research Tim Lawless about the Australian housing market today. Over the last three months, the index for Sydney dropped 4.5%, and the index for Melbourne 4.0%, the “largest rolling quarterly fall since at least the 80’s.”

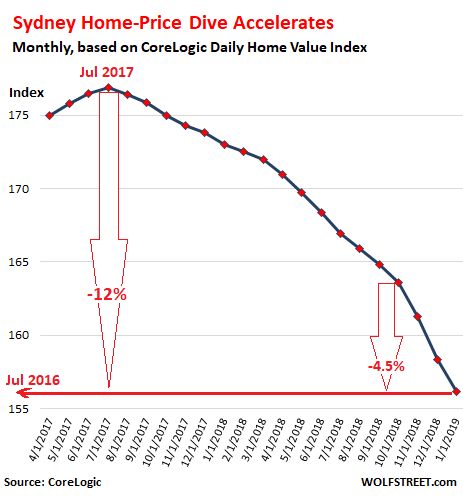

Across the metro area of Sydney, prices of all types of homes combined, according to CoreLogic’s Daily Home Value Index, fell 1.35% in January from December, the third month in a row with a monthly decline of over 1%. The 4.5% decline over the past three months pencils out to an annual rate of decline of 17%. The index is now down about 12% from its peak in July 2017. Note the accelerating decline over the past three months:

The 12% drop from the peak in July 2017 pushed the index back where it been in July 2016 – which shows how crazy and unsustainable the price boom had been on the way up. Now it is getting unwound at a slightly slower pace on the way down.

Over the 12-month period through January, the index fell 9.7%, with house prices down 10.9% and condo prices down 6.9%. At the same time, the number of homes of all types listed for sale in the Sydney metro jumped by 24%.

Prices of more expensive homes are falling faster than the lower end of the market: In the top quartile of the market, prices fell 10.8% over the past 12 months and are down nearly 15% from the peak.

“Buyers are now in a position where they can negotiate harder, take their time in making a purchase decision and be selective in finding a home that is right for their budget and lifestyle,” the CoreLogic report said. “On the other hand, vendors are clearly facing more challenging selling conditions.”

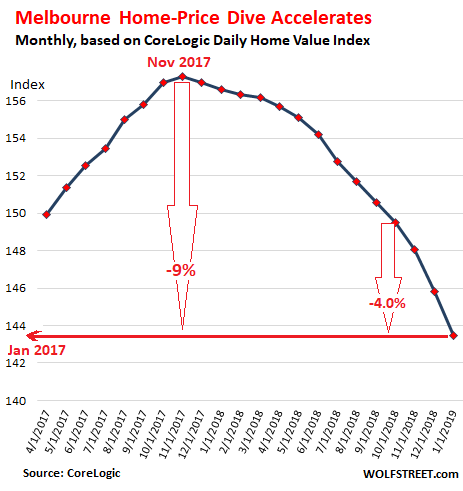

In the Melbourne metro, the second largest market in Australia, the housing bust is also taking on momentum, instead of slowing down, but started about four months behind Sydney’s. According to the CoreLogic Daily Home Value Index, since the peak in November 2017, prices of all types of homes fell about 9%, which pushed prices back to January 2017 levels. Note the acceleration over the past three months:

In Melbourne, too, the more expensive end of the market got hit the hardest: prices at the top quartile dropped 12.4% over the 12-month period and are down nearly 14% from their peak.

And supply is growing: the number of homes listed for sale in the metro jumped 34% from a year ago.

Across all capital cities, the picture is mixed, with some still booking year-over-year increases, such as Hobart, though its 7.4% rise is down from the double-digit increases last year. This list of the capital cities shows the percentage change of the CoreLogic Home Price Index for each city for the 12 months through January and the median “value” in Australian dollars:

- Sydney: -9.7% ($795,509)

- Melbourne: -8.3% ($636,048)

- Brisbane: 0.0% ($494,345)

- Adelaide: 0.9% ($430,711)

- Perth: -5.6% ($441,920)

- Hobart: 7.4% ($457,785)

- Darwin: -3.5% ($412,940)

- Canberra: 3.8% ($596,933)

The national CoreLogic index has dropped 6.1% from its peak in October 2017, largely driven by the vast Sydney and Melbourne markets. This pushed the index back to where it had been in October 2016.

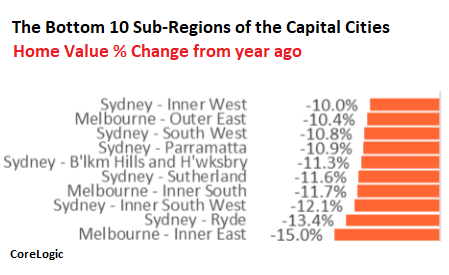

But there are large differences, with prices in some sub-regions plunging, while rising in others. On CoreLogic’s list of the 10 weakest performing sub-regions of the capital cities, seven are in the Sydney metro and three are in the Melbourne metro (image via CoreLogic’s report):

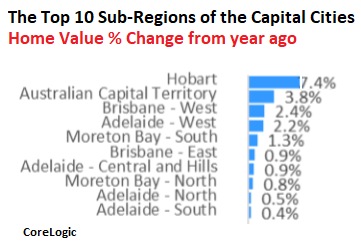

In some other sub-regions of the capital cities, prices rose, but none of the top 10 are in the metros of Sydney and Melbourne (image via CoreLogic’s report):

The report blames the “the worsening conditions” of the housing market primarily on these factors:

- “Tight credit conditions”

- “Weakening consumer sentiment”

- “Less domestic and foreign investment”

- “Higher levels of housing supply.”

Note the absence of interest rates on this list of factors. The Reserve Bank of Australia cut its policy rate to a historic low of 1.5% in August 2016 and has kept it there. Mortgage rates are hovering near historic lows. This would normally stimulate a housing market. But no.

Sky-high prices that have become unaffordable are reason enough to prick a bubble. Part of the reason the bubble even inflated this far is the now widely disclosed scandal of banking and mortgage shenanigans, along with crazy levels of investor speculation, supported by the same banking and mortgage shenanigans. After a lot of media coverage of these shenanigans, and after continued revelations about them by the Royal Commission, there is now pressure on banks to clean up their act, and this results in — to use CoreLogic’s phrase — “tight credit conditions.”

And CoreLogic adds: “Housing finance conditions are likely to remain tight after the hand down of the Hayne Royal Commission report which is due on Monday.” Hence, more revelations and more pressures on the banks to clean up.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

– A LOT OF australian mortgages are resetting from “Interest Only” (IO) to “Principal & Interest” (P&I) between 2017 and (at least) 2021. That reset means that the holders of those mortgages have to pay some 60 to 70% more in mortgage costs every year.

– A LOT OF mortgage holders with a IO mortgage are already now struggling financially. So, when those mortgages reset then those households won’t be able to survive financially.

– It strongly reminds me what happened here in the US after 2003 in the housing markets with the subprime mortgages.

I find your statement:

“That reset means that the holders of those mortgages have to pay some 60 to 70% more in mortgage costs every year.’

Kind of hard to fathom as in early years of most mortgages the interest component of the payment actually makes up 90% or so the total payment and payment on the actual principal about 10%.

Look at it this way.

An interest only loan must be replaced. The borrower must now justify a loan which is much harder to get. There will probably be mortgage insurance thrown on top.

Then the borrower May only be able to achieve a mortgage on 80% of the properties revised value – bank value (not actual value).

The interest rate will be higher due to a perceived higher risk on the loan.

Some of these IO loans were 100% of asset value.

My local bank ( one of the big 4) will not write a mortgage on an inner city apartment unless you have 50% equity in it.

It is about a 60-70% increase. It’s been quoted often in Australian media. I think the reason is that the period of the loan is not changed from a standard P&I arrangement so there’s a time compression for the remaining years. Also, the interest they’re paying in the IO period is not off the loan itself but just for the time delay before the real repayment starts.

Welcome to USA 2007!!!!

This would be hilarious if it wasn’t so very true.

In the pre-internet days they used to say American trends would reach Australia a few years later, it looks like that is happening again…

That is because when your con-artists flee from there, many of them come here and run the same scams.

Hands up who bought a house in Sydney during July of 2017.

It wanted some attention, the web he say…

“Will the impending changes to the first home owners grant and stamp duty help level the playing field for first home buyers? July , 2017, is the magic date for first home buyers in Melbourne and Sydney….”

Hands down.

We sold at end of 2015 for end of 2016 price.. were bit lucky as a millionaire old lady wanted to downgrade fell in love with the house.

Now we are just waiting for the prices to collapse before we buy.

So you’ve paid three year’s rent……………

Have prices gone down that much plus the stamp duty and moving costs times two…………….

Dishonest. Would’ve made three years 90%interest mortgage payments at a higher price, so the math on opportunity cost is more complicated than you’re making it out to be, but then re fans are almost always innumerate.

how many are selling the shirts off of the very backs that they had them on when they where dumb enough to buy homes when they where scorching on the way up?

Any way to break out how much of this slide is domestic pullback/bank lending issues/evaporation of Oz demand vs. the global issue of hot money (from mainland China) and it’s retreat?

As a Bay Area resident, I have always seen Vancouver and Oz as a bit of a canary in the mine when it comes to the offshoring of cash and distortion of the RE market. Their housing markets went steroidal a little before ours did, and now they’re starting to pay the price. But I am not sure if it is an Australia-specific downturn, or can we use it as a blueprint for what some of CA will look like in about a year re: disappearance and retreat of offshore money.

As much as people love to talk about 1% moves in interest rates, the CA real estate market has been turned upside down by a constant flow of Chinese all-cash bids. If we are to deduce that that is really gone, we may see some quicker pain then reading into Powell’s monthly FOMC statement and consumer sentiment numbers. You’re talking about gap downs in price expectations.

The Australian bubble was popped when our banks stoped lending to Chinese investors with 5% deposits and made up foreign incomes.

We allowed the Chinese to leverage their hot money 20:1

Mother of all bubbles is in China.

China being a communist country they can continue to blow that bubble (or stimulate their economy) for much much longer than any democratic nation can even imagine. When this bubble bursts, consequences are going to be very severe.

OPEC controls Oil prices and China controls Commodity prices – Canada, Australia and Brazil are very dependent on China buying their commodities and if China goes under, these countries will be impacted the most.

“China being a communist country they can continue to blow that bubble (or stimulate their economy) for much much longer than any democratic nation can even imagine.”

Right, here in the U.S. thank god we the people run the economy, as opposed to that backwards communist country China whose economy is run by the elites.

OH. WAIT.

Wolf reported housing prices in various cities, and it included the SF Bay Area (and Seattle). At least for residential homes, my impression was that these homes were bought for intergenerational purposes — that is, so that the children of wealthy Chinese mainlanders could attend American universities (eg. Stanford). These houses won’t go back on the market any time soon, and their demand is inelastic (a wealthy family that can afford a house *and* university tuition can afford a more expensive house!). No idea about business-related real estate investments.

Except if they are scared that money will be repatriated or exposed. The arrest of Huawei exec in Vancouver exposed the property she owns in Vancouver and the fact that she at least partially resides there (and her children reside there).

The US started a database tracking cash purchases above $300k (every purchase must have a individual responsible now). This means that they can track Chinese government officials with US property more easily (and repatriate these properties at a later time if needed). It also makes it harder to hide ill-gotten gains and launder money.

We live in the South Bay and the demographics of open houses have radically changed since June 2018, when US regulators added “money laundering” rules.

Yeah so good point there. Recently two of the banks CEOs have come out and said that actually the mortgage applications are down. Apparently they are still wanting to lend but demand is down. There’s a tug of war in the media right now with the RE spruikers saying banks are being too tight and banks saying “carefully” that they are only appropriately tight with lending (not lose!) but there aren’t enough applications coming through to them.

But it did all start mid-2017 when banks realised all these overseas Chinese people they have been giving loans to with foreign income have been on fake documents and cannot be verified. There was also a leak that those Chinese had actually borrowed the 20% deposit from a local bank in China and then used that to borrow the other 80% here. In my mind, that was the first nail in the coffin and the house prices have not increased or “plateaued” ever since.

Not so much that they realized the Chinese documentation were fake and unverifiable (you’d have to be gullible beyond belief), but they realized with additional scrutiny coming down they couldn’t get away any longer with pretending they were real to justify profitable hog-wild fantasy loans.

Also, don’t forget that one of the things the Hayne RC uncovered was the rampant (criminal) use of the HEM (70%+) to asses expenditures of mortgage applicants. The HEM, for the non-Aussie, is a statistical measuring called the Household Expenditure Measure, that actually only estimates the expenditures for the lowest %tile of the population.

Folks the incomes to support these (still) high prices aren’t there, they never were. Don’t believe me, go check the ATO per post code incomes, the incomes aren’t there.

And don’t be fooled with the whole, “yeah, but Oz is a full recourse”. Correct, it is, on LEGAL mortgages. Almost every mortgage for the past 5 years is ILLEGAL due to the fact that the used the HEM to improperly asses the applicants expenses. Never mind the also rampant ILLEGAL act that the brokers/bankers would have the applicant sign and fill out only the minimum on application, with the banker/broker filling out things such as income, expenses (see above), etc. post applicants signature. They are all FRAUDULENT. If applicant can prove this post signature, you can walk from the mortgage, house is yours.

Won’t be long until the lawyers get a whiff of this, I can see the billboards and hear the radio adds now: “Did your broker/banker get you in over your head? Did they use HEM on your application? Are you underwater? Want your house for FREE? Call me, Bill Buttlicker of Dewey, Cheatum and Howe, 1300 BITE ME.” Oh, and how long to you think its going to take Mr. Institutional Investor who is holding these now proven ILLEGAL MBS to ring the BIG 4 and tell them “I want my money back, 100%, NOW!” First one might get there money, 2nd-X maybe not so fast…And the elephant in the room is that these now ILLEGAL mortgages (and remember, they were ILLEGAL at origination, they didn’t become illegal) are also on the books of the Big 4…they’re TOAST.

Boom goes the dynamite!

There’s an old saying around here: “À Rome, fais comme les Romains”.

Are we absolutely sure this is a case of gullible/overeager Australian banks allowing themselves to be taken in by shifty Asian investors?

Or is this perhaps a case of Asian investors merely taking advantage of pre-existing conditions and local banks trying to pass on the blame for their own actions on somebody else?

I’ve seen quite a few real estate bubbles around the world in my life, and these bubbles tend to be overwhelmingly domestic in nature: foreigners merely inflate them even further, only to be blamed for everything afterwards so locals, starting from banks and regulators, can play the part of the naive victims of Johnny Foreigners’ treachery.

I can assure you that if you saw a block long line of people of same demographics before the sales office whenever a hole in ground is announced, you would succumb to the same impression. Saw it many times with my own lying eyes.

I heard exactly the same argument in Southern Florida (God help me!) about Brazilians when I lived there.

According to common lore each time a condo came up for sale Brazilian buyers would immediately converge upon it and “line up around the corner” to buy it, thus bidding the price up and pricing locals out of the market. Sometimes there was a slight change in flavor: “Brazilians” was replaced with “Colombians” or “Chileans”, all patiently lining up to use their hard-earned dollars to bid up real estate prices.

When that bubble started hissing air it transpired that “foreign nationals” accounted to a respectable but far from incredible 14-15%. However, and here is the funny part, the largest group of foreign buyers by a wide margin were those dastardly Canadians, closely followed by “EU citizens”, chiefly from Germany, The Netherlands and Italy. These two categories together accounted for a massive 46% of foreign buyers during the Southern Florida housing bubble which largely coincided with the Dotcom Bubble.

Brazilian nationals were down in sixth place, behind even Israeli citizens… how could people have been so wrong? Had statistics been tampered with?

Robert Shiller, him of Case-Shiller fame, famously said that most asset classes are chiefly media-driven, with real estate being the most egregious example of the lot.

IF you have lived any length of time in one of the many “flyover countries” that compose most of the world, you are bound to have read in the newspapers (or on the Internet) or heard on the radio (or on a podcast) how “foreign investors” are interested in this or that project in your area. Usually it’s nothing more than smoke and mirrors, but you’ll notice that soon afterwards people will start talking about how Mr X is in talks to build a new development with “Australian investors” or how some “Chinese tycoon” is about to pour huge capitals into some ailing local firm. How much truth is in there? Very little, if any.

There’s a good reason why our mothers told us never to lend any credence to rumors but, sadly, these days the worldwide economy seems to run on them. See the inexistant “Fed fold” last week.

Wasn’t a large component of the Bay Area housing bubble also from rising stock prices of Silicon Valley companies?

With the recent “dovish” stance of the Fed, stock prices (and the resulting confidence to buy a $1.5M shack) should go up.

Cabaries in coal mines not chirpin’ much no mo’…

Daddy? What is a full recourse loan?

Quiet kid! I am working only for cash now…

Got to love how they try and portray Hobart as some sort of beacon of housing hope.

Its a town of 200k, with less than 1% of the country’s population in a backwater state with no employment opportunities.

And pretty much everything is poisonous there and in the rest of Australia too!

The appraised value of my house in n.silicon valley (according to zillow) has been in decline since the beginning of Nov. If prices are heading down here, after about 6 years of soaring upward dramatically, I would think it’s got to be bad news everywhere in the U.S.

In Boston, the market is very strong with many homes getting multiple offers. In coastal LA/OC, the market is slower, but prices seem to be holding up. Decent deals are selling quickly. With the strong job market, hard to imagine any significant price decline.

I’m in Boston area too, and have similar impression – real estate is doing fine, no dents yet.

Boston area has a big medical mix and maybe different tech companies? And if you take a bike ride in the Cambridge MIT area, one can fantasize about all sorts of secret Dept of War and Aggression projects juicing dollars into the economy inside all those mysterious storage like buildings. And I walk my dog with a retired Raytheon worker who has a puppy in desperate need of letting off puppy energy. He tells me stories of the “expense is not object” reality that exists amongst war contractors.

Medical and War spending both going up up up…maybe that’s what helps Boston area?

Orange County here. Anything over $900k is sitting. Delisted and relisted constantly to hide DOM. Price cuts galore. Still, nothing is moving. Under $700k moves, but slooooowly.

Ladies and Gentlemen, there is absolutely nothing to worry about. Enjoy your wonderful dinner. Enjoy the fabulous music. Enjoy the very expensive and elaborate decor. I assure you that your safety could not be in better hands because, as you all know, this modern ship (our global economy) is absolutely unsinkable. ~ The Captain, right before the Titanic hit its Waterloo.

“FONGO replacing FOMO” was my favorite line in yesterday’s paper. Says it all.

What about HIMO as the mnemonic opposite of FOMO ?

Wasn’t it Hemingway who said you become bankrupt slowly then all at once?

He got to observe this up close and in detail as the 1920s turned into the 1930s.

In other news, I clicked on a vape ad because I was not sure what the heck the beautifully sculpted item displayed actually was. Now I guess I’m gonna see a lot of vape ads on here.

And maybe “your” credit score will go down too. Who knows what they are using their online measurements for.

Did Ernest have a premonition about Deutsche Bank ?

This is only just getting started, wait untill some momentum gets behind it, and it will! The whole Real Estate game in Australia is one big crime scene, from Core Logic right through government and the Real Estate whores, whom I may add, are doing deals behind closed doors, and making people sign a non-disclosure agreement. My support for hanging the lot!

These are the vested interests plus the MSM who are talking up the market and massaging the figures.

I would suggest these figures Wolf has listed are extremely “optimistic”.

Reality is probably far worse.

The RE market outside the two cities of Melbourne and Sydney is not doing as well as quoted.

There are a lot of “ghost apartments” in Melbourne and Sydney. – Owned by foreigners with no occupants. Land banking.

It’s not just foreigners who have eased up on the lending market. I live in an upmarket inner eastern area. Foreigners aren’t allowed to buy used property. My local bank had three mortgage lending managers in early 2018. Now there is one.

It is not just residential areas that have “ghost” occupancy, check out the industrial and retail districts. Once you get past the highly trafficked main street, most units are empty and have been empty for the past decade or so.

Sold our groudfloor apartment of a three storey complex in August 2018 in western Sydney. In November 2018 an identical apartment sold for $65,000 less, despite the better views being on the top of the complex. No sign of the decline bottoming out either.

Sold our inner eastern 3 bedroom townhouse in May 2017.

New owner would get 20% less now if he put it on the market and this is after he renovated.

Gold!

I am a sydney-sider and know numbers…..panic is yet to set in from what I see.

Graph’s are awesome, thanks!

Clearly, Australia is falling into a recession.

That’s right – your bubble is ‘different’.

Has to be, doesn’t it?

Strangely, exactly like the Australians/Canadians though theirs was…

“So, time to catch up, and here we go. The median prices of new single-family houses that sold across the US in November 2018 fell 11.9% from November 2017.”

And:

Sydney: -9.7% ($795,509)

Melbourne: -8.3% ($636,048)

So should people be in awe of how fast the price of new houses in the USA have fallen?

It appears that they have fallen more than in Sydney and Melbourne.

Here is a chart of how much some ares of Melbourne have fallen:

Bottom performing suburbs – median house prices

Suburb Median house price YOY

St Kilda East $1,068,000 -18.00%

South Yarra $1,482,000 -17.70%

Clayton $950,000 -17.40%

Abbotsford $1,040,000 -17.10%

Flemington $881,500 -16.80%

North Melbourne $1,077,500 -16.80%

South Melbourne $1,250,000 -16.70%

Fairfield $1,169,500 -16.50%

Lower Plenty $942,750 -16.50%

Collingwood $950,000 -15.60%

Here is a chart of some suburbs that have gone up in price:

Top performing suburbs – median house prices

Suburb Median house price YOY

Kurunjang $442,000 17.40%

Gisborne $768,750 16.90%

Whittlesea $595,000 16.20%

Brookfield $490,00 15.30%

Eynesbury $557,000 14.90%

Harkness $480,000 14.80%

Middle Park $2,740,000 14.60%

Wollert $600,000 14.30%

Wallan $500,000 13.60%

Truganina $573,000 13%

Now if you look at the prices and changes you’ll see something interesting:

Prices in high prices areas generally fell; prices in cheaper areas actually went up. In fact the price falls in the high priced areas were almost half the price of some of the houses in the cheap areas. And you can add a lot more areas to that bottom data set where prices went up as well. They were also in the areas that had median prices lower than the overall Melbourne median price.

Those high prices areas in Melbourne have always skewed the data when prices were increasing, when prices are falling, and also influencing the median price overall.

So not all real estate in Australia is falling in price.

Those outer suburbs will have their fall in the future. Many are family outer edge estates far away from the CBD.

The housing down turn will mean less construction jobs. The outer suburbs are full of tradies and construction workers.

When they are out of a job…….

Population Ponzi. Oz is bringing in 250k migrants a year with a further 100k entering through study visa rorts. Most of them are in the lower-middle income bracket. You see a lot of Uber drivers from South Asia with accounting degrees. They’re driving the rise in cheaper housing.

Everybody expects a significant reduction in price.

Usual what happens is that expensive houses don’t sell because almost everybody that buys an expensive house has already a roof over their heads so waiting makes senses.

Cheap but nice sells somewhat because those are the first time buyers who need a roof.

Very cheap is in need of TLC don’t sell. The fix-um-uppers as business.have left the market (cashflow problems) and those that do it to save money can negotiated a great deal on cheap but nice

I think this is the explanation for what you see happening and that the price is in fact falling in the cheap neighborhoods but the median house price is going up because dumps aren’t sold anymore

There are suburbs in Australia where the price of houses hasn’t changed much in 20 years.

There are also suburbs where the prices of townhouses/apartments have only gone up 20% in 20 years too.

Most of those areas where the prices are going up in that chart have something other than ‘cheap’ prices in common. They are areas that have had and continue to have large population growth so your thesis about ‘dumps not selling’ is not correct. Those areas have had quite a population and house building boom.

I’m not familiar with all those cities/areas so I just picked one at random.

Wallan had 8504 people in 2011. In 2016 it had 11074. The number of houses/dwelling units in 2011 was 3109 in 2011 and 3996 in 2016. (Australian Census data)

Estimates for 2019 put the population at around the 13,000 mark. So roughly a 20% increase in population in the most recent 3 years.

Another item that I think many people in the USA don’t understand about Australian RE is that it is very expensive to sell and buy. The costs and fees are huge.

First you have the RE Agent commission. That can run from a fixed fee of A$5000 to $7500 up to 2 or 3% of the sale price.

Next if you do sell and have to buy the governments here at the state level take something called ‘stamp duty’ which is just a type of transaction tax paid by the buyer.

In Victoria on a $1 million property that is about $50,000.

Then you have all the other fees to the government such as mortgage registration and title transfer and the bank fees and costs if you get a loan as well.

Finally, moving costs. I read an article recently that indicated that movers are now the highest paid people in the ‘trade’ area beating out electricians and plumbers.

So I’d guess that to sell, buy, and move on a $1 million property here would cost you about $100,000 or so.

“Another item that I think many people in the USA don’t understand about Australian RE is that it is very expensive to sell and buy. The costs and fees are huge. First you have the RE Agent commission. That can run from a fixed fee of A$5000 to $7500 up to 2 or 3% of the sale price.”

2% to 3% would be a rip-roaring deal in the US for broker commissions. Most of them are around 6% of the sale price, though some are cheaper, and you might be able to negotiate a better deal.

I think you misunderstood me. I don’t mean all the houses in a suburb are dumps but the houses that are less nice than its neighbors are dumps. Take an apartment complex During the start of a price fall the apartments with a good view/nice kitchen still sell, with a not so nice kitchen etc. will only have lookers and those that need to be stripped and are normally bought by flippers don’t even have lookers This is why at the start of a price fall you will see the the median sales price rise in an apartment complex rise. It is fake because the bad apartments don’t sell.

Those Australian RE commissions may or may not include listing one one of the big RE listing sites, photos, ads, or the billboard in front of the house.

So a not ‘one size fits all’ when it comes to RE in the USA and Australia.

Another difference is that the principal place of residence is free from most capital gains taxes unlike in the USA.

So when selling in the USA the RE Agent takes a big cut.

When buying in Australia the state government takes a big cut.

Pity they don’t include the more affluent areas, it would be interesting to know what was happening on the north shore of Sydney.

Official RBA rates may be low but we’ve had a few rises regardless. Some say due to the cost of borrowing from OS – esp if we have a weaker dollar. Maybe it’s just the banks being greedy. Record profits and still sacking people.

Maybe the smart money is hopping off the train in-case it goes pair shaped?

Many thanks to Wolf for honest analysis of these issues over time and for allowing free comment on his website.

The Australian MSM pumped this bubble along with banks, politicians, etc and did not allow dissenting voices.

Most of the public bought into the dream lifestyle lock, stock and barrel and are, in more ways than just money, heavily invested in it. The forthcoming drop in confidence will be staggering.

I’m afraid I have little sympathy. Not the way to build a caring, prosperous and sustainable society IMO.

The main stream media didn’t tell them what happens when the Chinaman leaves the locals out to dry. This is the part when housing actually falls into line with incomes which would portend about a 60 percent decline from top to bottom unless the Chinaman comes back.

Moving to a cheaper area isn’t an alternative for most people because of a lack of jobs. The labour market may be strong where you are right now, but what if that changes? FONGO indeed…

My reading of the tone of consumer/investor/speculator comments on this excellent site: 0 % bullish, 100 % bearish with a highly articulate Wolf leading the parade. Is there a message here? (Just asking)

There are plenty of commenters who are bullish and disagree, but it’s kind of hard to be bullish in the classic sense about a housing bubble that has seriously started to deflate.

But if you’re young and wanting to buy a home in the future, this is the most bullish news anyone could ever hand you. There are always two sides to everything. Lots of people have waited for prices to move into their range. And gradually, this will happen. It will be good for a big part of the population, and they’re loving it. For them this is AWESOME NEWS.

“For them this is AWESOME NEWS.”

But then if the prices are just starting to drop, might be a good idea to wait and watch. Also this brings up a question – how low can it go? Given the CBs will meddle once the prices go southwards in earnest.

Rates will stay low for a long time and wage pressure will keep up with housing values and interest rates. (At least at the high end where most of the asset value is concentrated) I am inclined to agree, rates are not rising, and the wealth disparity gap is not shrinking. For home buyers in the sweet spot this is good, affordable will need to find subsidies, and renters will get rent control.

I am bullish on “well located” real estate in top tier cities. This bullishness is based on my belief that no recession will occur for at least a few years. But, I could be wrong, and I enjoy reading others opinions. This site has some decent well though out comments on both sides. Much better site than others.

We’re living in the end times meaning virtually all assets will be crushed. The last shoe to drop will be the all the wealthy or the world’s elites becoming penniless. Your theory about no recession couldn’t be further from the real truth.

Good luck catching a falling knife.

And….. this big fat cow…. There is also no wage growth…

Yes – Watch Out!

It’s hard to be bullish when we have so many games of Chicken going on at the same time: Trump vs. China, Trump vs. Congress, US vs. the EU, Iran, Venezuela and Russia, England vs. EU, Italy vs. EU …. Markets vs. The FED,

All it takes is some griefer jamming the controls at the right moment in one of those games and that smash will be a doozy!

After Brexit, 2019-11-29, I think is a more appropriate time to be bullish.

Don’t forget the reverberations when the biggest bubble of all times the U.S. stock market finally implodes. This will affect most of the foreign stock markets and consequently real estate markets for the morons who still have money in stocks.

The Australian Economy ( if you can apply that term to it at all) is but a fickle house of cards,

– No manufacturing

– No Industry.

-No Tangible Production!

If you discount the Mining & Primary Industry (the First basically wholly reliant on the Creator and the Environment, the second on , Yup you guessed it China and to lesser extent India, Japan and few other Asian players). You’d be forgiven to conclude that ( the Lucky Country!) is doomed.

That said what is holding the floor under the RE market are couple of factors;

– the immigration ( generous or otherwise, pick according to you political views) .

– the delayed and soon expected outflow of foreign Capital from Theland down under, this last factor will undoubtedly wreck Havoc and render ( and quote me on this at least 60-65% of mortgages unserviceable read the collapse of the banking sector ( by by the Big four & their little cousins as well)!

another great factor that’s playing on the dilemmas and protracting stagnation in the land of the Roos is the unbelievable stupid crop of politicians ( on both major parties) .., those are the real risk to what’s left over of yet another Economic Carcass the will find its way to the scrap heap that is until ( that Nation produce someone with Big “ Cojones” .who’ll start filling the empty coffers and invest in the great asset of the country “ The Australian People “!

Peace to all.

Off topic warning: Zero Hedge will no longer allow comments from people who use adblock.. I’ve had an account there for 7 years 5 months and read those kids when they were still a blogspot. No matter.

I have something to say – from the distaff side of the isle. I’m female, heterosexual and I want to see scantily clad cheerleaders – BOYS & GIRLS. They’re good dancers and much more interesting than beer ads.

There – I’ve said it.

Can we be charged if we use adblock we will be deemed political dissidents

The New Zealand residential housing market is only down 20 percent in the last 4 months. Obviously the locals don’t understand what happens when the Chinese can’t buy. It should be down at least 50 percent in the last 4 months. Hopefully Australia and Canada will follow the lead of New Zealand so locals can buy property again.

Hi,

Well, Australian media news tells us that the Royal Commission into banking is over.

For the nasty people that they are …. they have been billing the dead & buried for services not rendered.

There is no respect here.

Oh, & by the way, more than 200 & closer to 300 high rise apartments in Victoria are covered in highly flammable cladding ….

All you need is a cigarette butt & whammo – you have rows & rows of pyrotechnics.

Life is just one big bowl of cherries – hey !!