China, Japan, other foreign investors, the Fed, US government funds? Nope.

Foreign private-sector investors and “foreign official” investors – central banks, governments, etc. – whittled down their holdings of US Treasury Securities by $21 billion at the end of July, compared to a year ago, to $6.25 trillion, according to the Treasury Department’s TIC data released Tuesday afternoon.

Over the same period, the US gross national debt – fueled by a stupendous spending binge and big-fat tax cuts – soared, despite a booming economy, by a brain-wilting $1.468 trillion, in just 12 months.

So, with foreigners having shed $21 billion over the 12-month period, who bought this $1.468 trillion in new US Treasury debt?

Here’s who didn’t buy:

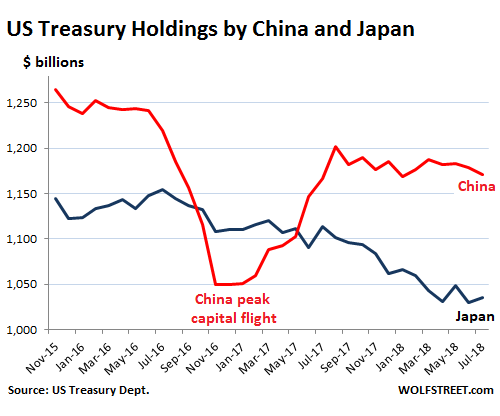

China’s holdings of marketable Treasury securities have remained roughly stable despite the arm-wresting match over trade, with its holdings at the end of July, at $1.17 trillion, up $4.7 billion from a year earlier.

Japan’s holdings fell by $78 billion year-over-year to $1.035 trillion, continuing the trend since the peak at the end of 2014 ($1.24 trillion):

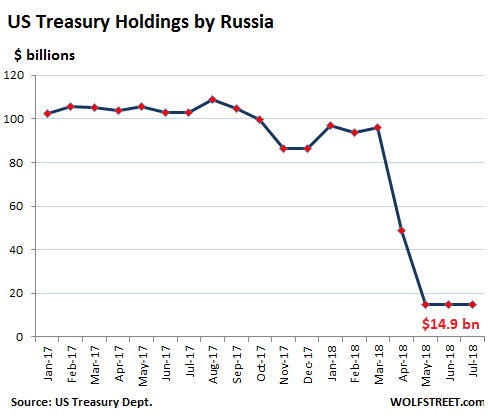

Russia, always a smallish holder of Treasuries compared to China and Japan, has liquidated 90% of its holdings, bringing them from $153 billion in May 2013 to just $14.9 billion in July:

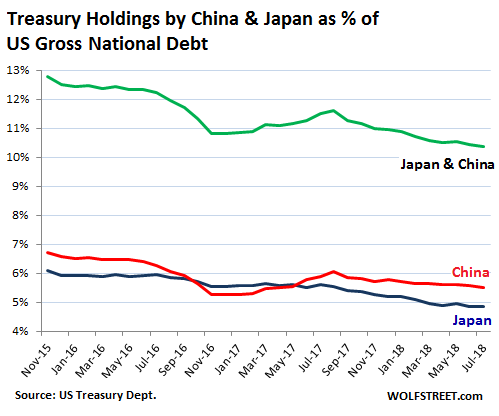

China and Japan have long played an outsized role as creditor to the US government. But their importance has been declining for years due to the growing pile of the US debt, and the simultaneous decline of their holdings. This caused their combined holdings (green line) to drop from nearly 13% of total US government debt at the end of 2015 to 10.4% in July, with Japan’s holdings (blue line) accounting for 4.9%, and China’s (red line) for 5.5%:

The Runners-up

Of the 12 largest holders of US Treasuries, after China and Japan, seven are tax havens for foreign corporate and/or individual entities (bold). The value in parenthesis denotes the holdings in July 2017:

- Ireland: $300 billion ($312 billion)

- Brazil: $300 billion ($271 billion)

- UK (“City of London”): $271 billion ($230 billion)

- Switzerland: $233 billion ($244 billion)

- Luxembourg: $222 billion ($213 billion)

- Cayman Islands: $196 billion ($240 billion)

- Hong Kong: $194 billion ($197 billion)

- Saudi Arabia: $167 billion ($142 billion)

- Taiwan: $164 billion ($184 billion)

- Belgium: $155 billion ($99 billion)

- India: $143 billion ($136 billion)

- Singapore: $128 billion ($112 billion)

The Americans are the only ones left.

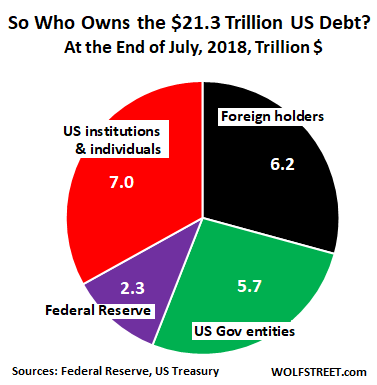

By the end of July, the US gross national debt had reached $21.31 trillion, up $1.47 trillion from July last year – as I said above, a truly brain-wilting increase for a booming economy. Here’s who bought or shed this paper over those 12 months:

- Foreign official and private-sector holders shed $21 billion, reducing their stake to $6.23 trillion, or to 29.2% of the total US national debt.

- The US government (pension funds, Social Security, etc.) shed $44 billion, reducing “debt held internally” to $5.70 trillion, or to 26.7% of the total.

- The Federal Reserve shed $128 billion through the end of July as part of its QE Unwind, reducing its pile to $2.337 trillion by the end of July, or to 11.0% of total US national debt.

- So if everyone shed, who bought? American institutional and individual investors, directly and indirectly, through bond funds, corporate or state pension funds, and other ways, owned $7.05 trillion, or 33.1% of the total US debt at the end of July, having added $1.66 trillion to their holdings over those 12 months!

And here’s how that rapidly growing elephantine US debt is now divvied up:

American private-sector investors are buying with a new-found passion. Yields have risen quite a bit, though they remain below the rate of inflation for everything up to three-year maturities: The one-month yield closed today at 2.05%, the one-year yield at 2.58%, the two-year yield at 2.81%, and the 10-year yield squiggled over the 3% line again, to close at 3.05%.

The fact that the 10-year yield is still so low, compared with short-term yields, shows that there is huge demand for long-term maturities. If there were less demand, the yield would have to rise to lure new investors into buying (prices fall when yields rise). And anytime the yield rises just a little bit on the 10-year, these new buyers emerge in force and that demand pushes the price up and pushes the yield back down. And this demand for US Treasuries is not coming from foreign entities, the Fed, or US government funds, but from American investors.

And investors are buying anything to get higher yields. Today’s megadeal, the ninth-largest ever, is one of the riskiest, and reminiscent of the deals in 2006 and 2007. And they’re still blowing off the Fed. Read… Just How Wildly Exuberant is the Junk-Credit Market?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So enough of the silly Chinese or Russians will sell their Treasuries and crash the American economy or American Government meme?

We put that to bed a long time ago :-]

In his new book, Ray Dalio alludes that if a country can fund its own debt internally it will not have a problem running fiscal deficits as long as nominal income is greater than nominal debt plus interest i.e., the ability to sustain and service credit. This was accomplished during World War II. As of to date, our debt (%GDP) is very close to the debt load of World War II.

During that time the total fiscal debt was financed internally.

On another note:

Prior to the war there was a huge influx of gold to the US because of the instability in Europe as gold (seeking a safe haven) was still convertible to currency. FDR initially sterilized this influx of gold deposited in the US (fear of inflationary pressure) but later reversed course.

RE; comparing today to WWII era.

The GDP stat today is so full of froth it is a very dubious measure of the economy. The old term Gross National Expenditure was more honest in that it told you it measured spending.

No matter how little benefit spending creates it adds to GDP.

If the govt builds a pyramid it adds to GDP.

If there is NO product (govt studies etc.) it adds to GDP.

In the WWII era, being a cop, fireman, or bus driver (50K where I live) was not an instant ticket for a twenty-something to the middle class, with retirement at 50, it was just a job.

Nor had Federal and state govt bureaucracy expanded to their present size in % terms.

The insane growth of (legal) drug use and prices means they are now 12% of total wholesale. Medical spending is devouring the economy, but it adds to GDP.

Prior to WWII there was virtually no consumer debt, student loan debt, or credit card debt (the latter not invented yet)

The mortgage market was much smaller as a %, as was corporate debt.

So in the emergency the economy was in a position to finance the war.

This is very interesting. I wonder if we can tell if some of the net ‘American’ purchases are in fact foreign capital that has been moved into the United States and then used to push into treasuries in an attempt by some foreign entities to get out of the way of the EM currency steam-roller.

Capital is flowing back into the US: that’s part of the reason your economy is overheating. However it’s very hard to find out exactly how much of this capital is domestic, flowing back into US Treasuries and the like after abandoning risky markets such as Turkey and Indonesia, and how is foreign, looking for a safe place to be and a scrap of yield.

It might be, but what is happening here is bond ownership is being changed hands. It looks like the narrow capital, cash, is flowing to the sellers, abroad. In effect they are being returned the dollars they once invested in treasuries. Clearly that will also be returning to US some way to puchase something, even just own currency…it doesn’t get hoarded abroad, bonds are an interest paying method to hold US dollar value abroad. As bonds are “high quality” assets that pay more than reserves, and with excess reserves still at hand I think, US institutional investors will likely look to buy up what is offerred?

This will have effects on money supply, fx rates, trade etc., but I think you need a very big computer and insider knowledge to guess the outcome.

If you bought any new, callable bond issues in California during the Meridith Whitney bond scare (about 2010), you are probably an indirect owner of US Treasuries. Virtually all of these bond issues have been advance refunded to their first call date, with the proceeds invested in a class of Treasuries known as SLUGS (state and local government securities).

“American private-sector investors’ are picking up the slack, well I’ll be watching for the slaughter. This is like betting against the FED, duh they have the power until they don’t.

Who in their right mind would buy U.S. debt that’s going to be printed (inflated) away by the Fed?

If the yield is high enough, it becomes a good deal for investors seeking near-zero credit risk and good liquidity.

It’s mind melting for sure.

But if the financial crisis taught me anything, it’s that extend and pretend works, at least for political time frames. This applies to national debt, too. It’s mind melting now, but today’s figures will seem mild once we reach 2x-3x GDP. And who knows? Maybe the global reserve currency can tolerate 5x! Uncharted territory is no longer a policy constraint.

I’d like to think a recession would bring discipline. But recessions cause flight to safety. And nobody loses their job by piling up balance sheets with cash equivalents when ill economic winds start blowing.

The calculus is simple: you have to put you capital somewhere. Do you buy into the equity market bubble, or do you buy somethhing that everyone flee to during a market panic? Everyone wants short term treasuries during a market panic.

Yeah, but there seems to be no shortage of cash to go into equities either. Where does all this money come from??

So why do 401K’s offer returns in money market funds at about 0.71% when you can get 2.5% in CD’s?

That’s THEFT. Why haven’t we scene a class action law suit against the criminal fraudsters?

Why can’t we sue the Fed for stealing our retirement and giving to their ULTRA RICH friends and RICH GIGANTIC CORPORATIONS?

Because the Fed wants to force us to give our retirement to their ULTRA RICH FRAUDSTER FRIENDS.

After all, various Fed chairman have explicated stated their actions were intended to steal our money and give it to their ULTRA RICH FRIENDS.

To be fair, the fed is trying to destroy everyone’s pension savings because there are simply not enough young workers in the pipeline to deliver the retirement you were promised. The only difference for the rich is they can whine at the govt about this process and get exemptions and compensation to help them out because they are ‘job creators’ after all.

Frankly I believe these efforts at a soft landing are simply destroying the incentive system that drives capitalism forward and will make the problem worse in the future. They should have used QE and the GFC to train more skilled workers and build out infrastructure so that when the demographic crunch really starts to squeeze we can fall back on that capacity. Instead a whole lot of folks will turn to their bubbly assets for help when they need medical care or want to enjoy their final years and discover that you cannot fix a busted hip with numbers on a spreadsheet.

To be fair, the Fed was trying to prevent the banking system from collapsing back in 2008 not destroy your pension savings or mine. Of course, its efforts had unintended consequences. Savers saw their interest income shrink, even as stocks recovered from their 2008-09 crash and went to all time highs.

The Fed is not in the business of building bridges or training welfare moms to join the work force.

Matt Tiabbi sums it up quite accurately:

“The deal those bankers cooked up was to save the banks FROM capitalism.

Losers must be allowed to lose. It’s the first and most important regulatory mechanism in a market economy.”

https://www.rollingstone.com/politics/politics-features/financial-crisis-ten-year-anniversary-723798/

BS on this: “To be fair, the Fed was trying to prevent the banking system from collapsing back in 2008 not destroy your pension savings or mine.”

The Fed made explicit policy decisions to save the banking system by penalizing savers, rather than choosing other means. The right thing to do would have been to decapitate the mismanaged banks (replace the leadership) and then recapitalize them (zero out the shareholders and bring in fresh ownership). The federal bailout at taxpayer expense, ZIRP and QE at savers’ expense, deliberately stole from the innocent to reward the guilty. It was the greatest bank robbery in history – many trillions of dollars – and the banks robbed the people.

“Of course, its efforts had unintended consequences.”

No, they had easily foreseen consequences that those in power only pretended were unintended. The injustice of TARP was a big trigger for those watching to start grassroots protests from both wings, what later become co-opted and corrupted as the “Tea Party” and “Occupy Wall Street” movements.

Anton 1970. The Fed is the cause of all the booms and busts. All they do is inflate and cause prices to rise with the illusion of debt creation. Or should I say delusion. Read “Debt and Delusion” by Peter Warburton from 1999 revised in 2000 and 2005. But it may set you back $100 to get it.

Timbers you can buy treasuries direct with your retirement money.

You just need to withdraw it from your 401K (10% penalty to discourage withdrawal, for your own good), pay all income taxes due, then enjoy 2.9% (less than real inflation) returns on the remaining half of your money.

Vanguard has some sort of treasury-backed vehicle you can put 401K funds into. I got tired of reading the fine print, but the gist of it I think was that you could potentially lose money!!

You can invest your funds in a self-directed IRA with brokerage custodianship in Treasury securities, but only as a secondary holder; the primary holder is the brokerage house and you can be sure that they are leveraging your supposedly super-safe funds to the hilt. If you can find a Treasuries-only money market fund to hold your pre-tax savings, the custodial fee is likely to make your effective yield unattractive or negative, and there is always the possibility that in a crunch your liquidity could be reduced and the buck could be broken. As our financial situation worsens, taxes have no place to go but UP and the government will likely be tempted to force you to invest in certain areas which will be unattractive except to them and to limit withdrawals. For people nearing the end of the game, with plenty of capital left to burn through, the best approach for safety and liquidity is to cash out of their pensions and place the money in a laddered reasonably short-term Treasury Direct account and reduce roll-overs as needed to cover living costs. Transfers to a linked bank are free. Of course, the siren stock market becons and many of us regret not going in whole hog in this most unusual period, but sooner or later stocks will be priced to market and risk will be recognized. It does seem that the game has gotten long in the tooth and the longer it is played, the more violent the snap back will be, unless “this time it’s different.”

Yes, lots of those examples for sure. Vanguard govt Moneymarket pays about 1.95%, which is reasonable. Fidelity’s equivalent is about 25 basis points less and higher management fees. Look around.

Some 401k plans use investment vehicles with very low fees. Others, especially those offered by smaller employers are burdened by much higher fees, which include the costs of administering the plans. It is up to the employees to know their investments and understand their 401k plans. Many do not. If you are in a lousy 401k plan with high costs and poor investment choices, you may even want to think about changing jobs.

Stealing your retirement? You are being very naive. Every government law has unintended consequences. Some people receive windfall benefits, others end up paying up. You can’t sue the government for passing a law that you don’t like.

I don’t think Timbers sounds naive…I think he sounds justifiably pissed off.

Tell me, what would be the ‘unintended consequences’ of a ‘government law’ that would allow everyone to allot 401K monies directly into treasuries without management fees and not through a “fund” with a bunch of fine print saying that even the return of my principal is not guaranteed!

I’d gladly pay a buck or two per month to cover mailing of the statement.

In 2014, the Obama administration announced a program similar to what you are talking about (myRA) aimed at small savers whose employers did not offer retirement plans. But I don’t think it attracted much money and was recently shut down by the Trump administration. Don’t expect the Trump administration to come to the rescue of small savers.

401k what a scam. Save taxes now and in 30-40 years pay less in tax. Problem the taxes you saved, that money becomes part of that 401k account and they also grow. And in 30-40 years your income also grows pushing you into a higher tax bracket. I know I did it. Wait until you want to cash in and then you will know how little you actually saved. Besides that money is locked until your 59 1/2 except for a few instances unless you want to pay a 10% penalty. So if you think it is a good investment vehicle have at it.

In retrospect, I probably would have been better off putting less into my 401k and buying more zero coupon non callable munis. But hindsight is 20/20. Overall, I am quite satisfied with how my retirement plans turned out. When I got laid off at age 57, I received a generous severance package and started to make IRA withdrawals soon after I reached age 59-1/2. What I didn’t anticipate was a big bump up in my Medicare premiums. The Doc fix passed by Congress in 2015 (?) which took effect in 2018 made things worse. My Required Minimum IRA Distributions starting in 2018 will bump my Medicare premiums up again in 2020.

Timbers, “why do 401K’s offer returns in money market funds at about 0.71% when you can get 2.5% in CD’s”?

My 401K’s money market fund is paying about 2%. I think the answer is that either your data is stale (rates have been rising) or that your plan sucks for some reason. You’re trapped in a captive market – the same situation as when you’re hungry inside an airport, movie theater or amusement park. So you’re getting ripped off. Your company should negotiate for a better deal on your behalf and you and your coworkers might be able to gently raise that issue with management (or at least warn new hires)…

America is in a boom economy, HARK, what is that I hear BOOM BOOM BOOM tis nought but the genteel dropping of love and affection from 30000 feet to country not near you

What happens when there’s not enough money to buy all the government bonds? (say, the stock market fake wealth-effect is drained and there’s not enough real money to buy bonds)

We will print more ;-)

James,

“What happens when there’s not enough money to buy all the government bonds?”

Then yields go up (prices fall), and these bonds become super attractive, and investors will deploy their cash or sell everything they have and buy these bonds until yields come back down.

And at the end of the day, there’s always the Fed that can buy these bonds, and everyone knows this and counts on it.

Wolf’s right. Having a buyer of last resort creates an artificial market. And artificial markets can be whatever we want them to be.

But if more and more money gets tied up in US treasury bonds, wouldn’t that leave less money for other liquidity seekers? (like corporate bonds which are rolling out of control)

James,

Yes, this is already happening with Emerging Market debt and equity securities, which is one reason why they’ve been falling this year.

Bill from Aussieland,

Greetings from the US empire. I struggle with Americas foreign policy quite often. There was a time when I felt we should close every military base, pull all troops and prioritize democracy over empire.

I also wonder who would fill that void if we did.

The middle east would be a proxy war between Iran, Saudi Arabia and Isreal.

China would quickly expand its sphere of influence over the asian geographical area.

Eastern Europe, Western Europe and Russia would be interesting. And Russia China as well.

And what would Turkey do, bit of a wildcard there eh?

So yeah, not a big fan of a lot of the stuff we do. Not a big fan of the other possible scenarios as well.

China is welcome to sorting out Vietnamese, Koreans, Japanese Thais and all the rest. without DC, Riyadh and Jerusalem are busted you talk to people in Basra about how sick they are of Iranian influence.

The EU would become a superpower especially so with Russia which is why DC loves the Brexit debacle and messes round in Catalonia and the EU creaky old financial system

If you have been all in on stocks during the last decade, its time to transfer gains into treasuries. So boomers balancing their portfolios are buying treasuries heading into retirement.

This. Where else are you going to go for reasonably safe yield? There’s no such thing as a dividend paying stock anymore. Remember when sound corporations issued Preferred stock that paid a nice dividend yield? Now if you want yield from stocks all you can find are maybe utility stocks and REITs. Corporate debt looks worse than ever, two decades worth of levering up balance sheets to fund stock buybacks is going to end very badly so corporate bonds aren’t the answer.

Nope. It’s pretty clear that Treasuries are finally coming home to roost.

You guys are smart.

Berkshire Hathaway only issued a dividend once since Buffett built it and the divi was small. Jabba-the-Hut of Omaha has withdrawn from stocks knowing that most are overvalued. Even GE is a bad buy these days.

Treasuries will get dark money for quite a while yet but it won’t be Buffy buying it.

MOU

I believe the Fed’s primary dealer banks are required to be the buyer of last resort for the treasury market. It would be interesting to see what portion they are buying.

After the fed GIVES them the ‘thin air’ fiat to purchase T’s….off book altogether

When you can get between 2 and 2.5% yield on risk free securities, why investing in the stock market you believe to be at the peak. Same thing is happening in the UK. Banks have revived their notice accounts, increased rates on short term deposits while the stock market has lost money since the start of the year. A no brainer in my opinion.

Wasn’t this posted before? Yes it was. Only the difference is that even more Americans bought American!

Isn’t that good for the country?

Only if the America being bought is worth buying.

Cliche, but is true…US = best house in a very bad neighborhood.

I asked a well known economist 4-5 years ago how we could get to 4% GDP. He laughed at my question and then said it would NEVER happen again. So as bad as the house is, few other houses are doing as well.

My thought also.

What I see besides that is that the direction of flow of investment is also centrally managed. I am sure that the fed scrutinises the effect policy decisions will have before they make choices, that they prepare the road. For example, if cheap dollar funding saturates emerging markets for yield, raising rates will pressure those markets also, the US then being a safe haven in comparison. The sale of treasuries by foreign holders might also be to supply dollar liquidity to own financial needs . Being reserve currency allows a lot of leverage, just as long as the larger international framework remains credible, and US management and economy remain within reason.

The (some say needed) problem now would be if that position were lost. How would the US pay its trade defict if co-sponsors unpegged ? What would happen to the US economy on a “national debt as reserve” devoid field, to its currency ? For now those that work with the US accept its tune as the better direction, but this will likely sooner or later change, either by rebalancing and reaching a greater understanding, or by separation of ways.

The US is a big and dynamic country, unless it went to war with itself or turned full communist, I think it has all the ability and resources it could need to prosper well, even in isolation. So for now it enjoys a privileged global trading position and more choice of option than most countries. The difficulty is maintaining that, tendency is always to let slip once reaching a certain level… same goes for in Europe and so on…and not always in ways that are immediately obvious, sometimes contrary to first impression.

The world can be a complicated and unpredictable place.

It’s one of the things I track monthly because it’s important. Other things I track monthly are various housing market stats such as rents and prices, the transportation sectors (trucking/rail), the used vehicle market, etc.

The list of monthly updates also included new-vehicle sales, but now that GM has decided to not report monthly sales any longer, but only quarterly sales, I will have to switch to quarterly tracking of auto sales.

Other stats I track annually (international trade, movie ticket sales, Fed’s remittances to the Treasury, etc.)

So yes, you’ll see these things again.

Wolf, GM sales can be calculated since all other manufacturers report sales and JR Polk issues monthly new vehicle sales based on new US vehicle registrations (They sell this information). Total monthly US new vehicle sales minus all other new vehicle sales reported by all other US manufacturer sales equals GM sales. So, you have GM total monthly sales, however, you do not have GM individual model sales. This is just one of the reasons GM went to quarterly sales releases.

These GM figures are “estimates” when they’re used to “estimate” deliveries. Registrations are not equal deliveries (big timing differences, etc.) so they don’t match. I see these numbers too. Same as monthly numbers for Tesla; they are all estimates because Tesla doesn’t disclose monthly deliveries. So matching those estimates with actual deliveries as reported by other automakers is somewhat of an apples and oranges deal.

Wolf,

How is our government not reporting the 1.468 trillion deficit? I looked at Treasury.gov and for last 11 months of fiscal 2018, I believe they are reporting 800+ Billion. I am confused as to how they hide the real number.

Thanks.

I have written some articles why the growth of the debt is almost always more — and often much more — than the deficit. A big part has to do with how the “deficit” is accounted for. So even during the few years the government actually had a “surplus,” the debt kept growing.

The debt cannot be fudged. This debt is owned by others and is registered. It’s public for all to see. So the growth of this debt cannot be fudged either. This is the only real number about government finance as far as I’m concerned. The “deficit” (or “surplus” when there was one) — based on government accounting — contains a lot of smoke and mirrors.

Presidential administrations have been using accounting shenanigans to hide deficits going back to LBJ. Bill Clinton elevated the practice to a high art in order to produce some phony budget surpluses. Curiously, Bush 2 never made much effort to hide his deficits, but predictably, Obama picked up where Clinton left off. Trump is just following this well-worn path.

The “Myth of the Clinton Surplus” page has been on the web for decades, it explains it pretty well, you can find it here:

http://www.craigsteiner.us/articles/16

Buckaroo Banzai,

Much agreement here. But I like to separate Presidents from budget deficits or surpluses.

Congress has the power of the purse. Presidents can influence the budget debate, but the spending of actual dollars is ultimately put together and decided in Congress, which then tells the Administration down to the dollar how much to spend and what to spend it on, even if the President has opposed those items.

The exceptions being –

The Pentagon and the ‘back door’ boys (black ops)

Langley and the spooks both inside and outside

DHS, ATF, and a myriad other acronyms depicting bottomless money pits, that are tax payer funded by way of more debt.

OutLookingIn,

Yes, it may not show up in the budget, or in the deficit, but it shows up in the debt.

“Debt funded” means the government has to sell Treasury securities to get the money to fund these operations. Those Treasury securities cannot be sold secretly. EVERYTHING eventually shows up in the debt, even if it doesn’t show up in the budget or the budget deficit.

There is only one entity in the US government that issues this debt, and that’s the Treasury Dept. The Pentagon cannot issue its own debt. The Treasury Dept. issues the debt and sends the money to the Pentagon to fund its operations — whether or not this money shows up in the BUDGET is the matter you’re addressing. But it does show up in the debt.

That’s why the debt is the only reliable figure we have of the government’s finances.

To be more specific, only the US House of Representatives has the power to levy taxes and appropriate-spend at the federal level. There you have it credit (spending) and debt (borrowing).

Professor Michael Pettis (The Great Rebalancing) argues that a county must buy foreign bonds with its profits to run a trade surplus. Global trade and profits are down. Foreign purchases of US bonds are down. Too soon to call how trade surplus is going. My understanding is that currently Chinese trade surplus is largest ever but this might be pull-forward because of tariff rhetoric.

@ Nick Kelly:

There is a posted wage and then there are all ‘adjustments’ and titles/categories. :-)

For Campbell River

2017 Topping the list of top paid firefighters in 2016 were: Fire Chief Ian Baikie, who earned $144,410 in remuneration, Fire Captain Reid Wharton who earned $134,772, Fire Captain John Baker at $129,805, Deputy Fire Chief Thomas Doherty, who made $129,450, former Deputy Fire Chief Chris Vrabel, who earned $128,917, Fire Captain Ken Dawson, at $128,674 and Fire Captain John Vaton, who earned $122,076 in remuneration.

” The national average salary for this job title is CA$106,426.”

I know a lot of these guys in CR and I’m sure none of the regular crew make any less than 100K. There are not too many fires in CR and the pulp mill has been shut for years which was one reason why CR FF were paid so much. 4 days on a 4 off, waiting around the firehall 24/7 would make me want to slit my wrists.

Every year they used to come around our worksite and do a complete inspection of all safety equipment until one day my boss/friend flipped out and threw them off the property. He just couldn’t take it anymore.

Where I live we have a volunteer dept which we contribute money to and we also have our own home fire pumps, etc. It works.

With permit fees, bylaw inspections, culture departments/ recreation, etc. local Govt expenses and required taxes to pay them are totally out of control.

You should provide something to back up the claim that American investors are buying bonds like fund flows, etc etc. You just throw it out there and say there it is. I assume without proof that government is self financing new debt with its own off balance sheet gymnastics. and so there IT is.

Ambrose, I think you have a good question.

When an overseas debtor nation like, say, Italy, runs a self-financed deficit by issuing bonds, typically one looks at the nation’s banks as “forced investors” of the bonds. In fact, Italian banks are frequently described as being unstable because they are so overexposed to Italian government bonds of dubious quality. Why should we assume that US “investors” were so eager to swallow all the new US debt?

In the context of Wolf’s post about the US, the pie chart says that “US Institutions and Individuals” increased their holdings of US Treasuries from 5.4 to 7$ Trillion. Which is it, institutions or individuals? Which ones? An allocation shift or growth of that magnitude should be obvious in pension asset data, mutual fund and ETF assets-under-management data, and so on.

Federal Reserve data on US government securities held in money market funds does NOT show massive growth in the past 12 months, although it does show about $1T in growth back in 2016:

https://www.federalreserve.gov/releases/efa/government-money-market-funds-investment-holdings.htm

I would look very closely at social security pension assets.

Whenever the governments over the years, required an infusion of “cash” the pension fund has provided it.

This money which is paid in by the workers and employers, is transferred out and replaced with a treasury note, marked as agency debt.

As a result the pension fund has been hollowed out.

Good luck to the younger tax payer in collecting it!

Social Security is restricted by law to investing its surplus cash inflows (from FICA taxes) in non-marketable US government securities. In its early years, SS had its own budget and the numbers were reported separately from the US government’s main budget. In the late 1960’s, Congress combined the two budgets for reporting purposes to help hide the true costs of the Viet Nam war.

SS, which started out as a government sponsored retirement plan for most private sector employees, has been expanded over the years to provide benefits to disabled employees and to surviving spouses (in the case of a covered employee’s death) and their minor children. From its very beginning, SS was designed to replace a higher percentage of low income employees’ wages vs. high income employees. Employees with non-working spouses and with minor children were not required to pay higher premiums for the extra coverage they received. SS was a better deal for early members than for more recent ones. In that sense, it operates like a legal Ponzi scheme.

Just listening to Ray Dalio “We have to sell a lot of Treasury bonds, and we as Americans will not be able to buy all those treasury bonds. The Federal Reserve will have to print more money to make up for the deficit, will have to monetize more, and that’ll cause a depreciation in the value of the dollar.” Are they buying treasuries with SSN trust fund money? Is that the question?

No the Fed doesn’t have to if it (and the USG) can stand the yields!

A 10-year Treasury offering 7% yield??? There would be unlimited demand, as investors would sell other bonds, stocks, commercial real estate, etc. to get the risk free 7% return. I would!!

Yield solves a lot of problems.

Ambrose Bierce,

Well, ok, we’ve got: 1. Foreign private-sector investors and 2. foreign official investors. Both are listed in detail. Those are the only two non-American type investors. 3. we have the Fed. That data is listed. 4. We have US government funds which are listed as well. 5. then there American institutional and individual investors. Those are the 5 big category of buyers. There are no other categories of buyers out there that are not already included in these five categories. Unless you believe in Martians :-]

Doug Noland documents flow of funds, maybe I can ask him the question? 1.2T is not something you sweep under the rug. That buying has to show up somewhere.

I was rummaging for a detail but could not find a transparent answer…just “private investors” etc. does not answer it in my book. So I am not judging one way or the other, the link Wisdom Seeker posted rings true to me though.

The first chart at

https://fredblog.stlouisfed.org/2018/04/whos-buying-treasuries/

is interesting. It shows foreign buyers increasing from 1/4 share before 2000 of ownership ex. fed, to roughly a 1/3 by 2010, now tapering off their share. What really stands out though is that US buyers have been on a real tear since 2008…and continue in that direction still, now taking up the slack of foreign purchase.

The only other article I found heads off into conspiracy of opaque funds, I have no idea if the site or theory is credible…enough to say the lack of transparency has people guessing. I’ll include it all the same

https://arcadiaeconomics.com/interest-rates/whos-buying-all-of-the-u-s-treasuries/

If the central bank has a format being used, as per Wisdom Seeker’s link, it should be made clear… mind you, in EU the similar is well known, and no one seems to give a hoot either !

Correction “Wisdom Seekers link” should read “Rich Bonderud’s link below”. My muddle.

A number of companies contributed to their pensions before the Sept 15 tax break deadline (35% to now 21%), which caused an uptick in the buying of stripped Treasury Bonds. As of Aug ’18, we already surpassed the total increase reported in 2017. Plus, companies with underfunded pension plans face higher insurance premium from Pension Benefit Guaranty Corp. These plans are paying a 3.4% fee on any deficit in 2018 and that will go to 4.0% in 2020. The numbers above don’t match the numbers you mentioned, though they are part of the total. In my opinion, that pull forward of demand caused yields to decline and without more buying, yields will probably go higher from here.

I think Trader Vic [Victor Sperandeo] has the answer in his article “The Rules of the Bond Game” https://www.theepochtimes.com/the-rules-of-the-bond-game_2600435.html

Thanks Rich for that link. I read the article, and here’s one quote from it I’d like to see vetted thoroughly:

“Not only can CBs create fiat currency from nothing, but they can buy U.S. government debt with that money and keep the interest to make a risk-free profit, which even adds to the CBs’ capital.”

I understand that banks “create” money when they make loans. Do banks “loan” money to themselves, somehow, in order to buy U.S. Gov’t debt?

Pls read the article for the full context. He’s making some very significant assertions. If he’s accurate, it’s a key piece, or a least a strong clue about how the debt pyramid evolves forward.

The core point we’re all struggling with is “who is buying the debt, and how long can that go on?”

I encourage all WS readers to ponder this and keep hammering away at it.

It seems that it is the linchpin around which the “monetary policy dominated” economies (like the U.S.) are rotating.

“Do banks “loan” money to themselves, somehow, in order to buy U.S. Gov’t debt?”

I say not quite. They “give” money created out of thin air to the government and “receive” U.S. Gov’t debt. Therefore, then, the Chinese government can dump however much of their U.S. Gov’t debt instruments they want and receive dollars, too.

Rich is right above, but one more point for Tom: the Federal Reserve uses the interest on its treasuries to pay its expenses, and then sends the remaining interest back to the US Treasury. So in effect the interest payments on bonds held by the Fed don’t add to the US deficit. Those bonds basically balance out the the base level credit in the financial pyramid, from which all other credits derive.

HOWEVER – new in this market cycle, the Fed now pays “interest on excess reserves” (IOER) to the banks who have “excess reserves” on balance with the Fed. And guess what! The excess reserves come from people depositing the cash the Fed gave the Treasury to buy the bonds… You can plot the data on the Fed’s balance sheet (both assets and liabilities) and there were no excess reserves to speak of before the Fed bought up a ton of bonds via QE.

Now, the IOER payments are part of the Fed’s expenses, so they reduce the amount the Fed sends back to Treasury. Without IOER, the Treasury would get the interest back, but as it stands the banks get that money instead. This was a huge backdoor taxpayer gift to the banks – or part of the bailout plan.

It will be interesting to see what happens to the excess reserve balances and IOER policy going forward

Wisdom Seeker, while I believe you are correct about the Federal Reserve, I must stress that Trader Vic is talking about commercial banks creating money out of thin air to buy Treasury paper. And boy, do they love all that free interest (and free principal at expiration of the paper?). Looks to me like printing press money on steroids.

If anyone thinks the bond market will not crash with the next crisis listen to Michael Pento on USAwatchdog.com on Sept. 19th. The whole world economy is in trouble with $250 trillion of debt, which is 2.5 times world GDP.

blah , blah , blah…. a ponzi works until it doesn’t. corrupt to the core.

burn baby burn, I can’t wait to see it blow like the hindenberg.

A hundred upvotes votes for you, whopper.

How can we afford the interest payments — a 1% increase in rates is costing $210 billion extra — where is that money coming from?

More bond issuance :-]

Yes – the very definition of Ponzi Finance as defined by Minsky and explained in Kindlebarger: when you can’t pay down the principal and have to borrow more just to cover the interest.

The U.S. is overdue for another major stealth default or devaluation, along the lines of Roosevelt revaluing the dollar vs. gold in the 30’s or Nixon closing the Gold Window in the 70’s.