An entire generation working on Wall Street has never seen Treasury yields this high.

The one-month treasury yield rose to 2.0% yesterday at the close and is at about the same level today, the highest since June 10, 2008. It is starting to price in a rate-hike at the Fed’s September 25-26 meeting. This rate hike, the Fed’s third this year, would bring its target to a range between 2.0% and 2.25%.

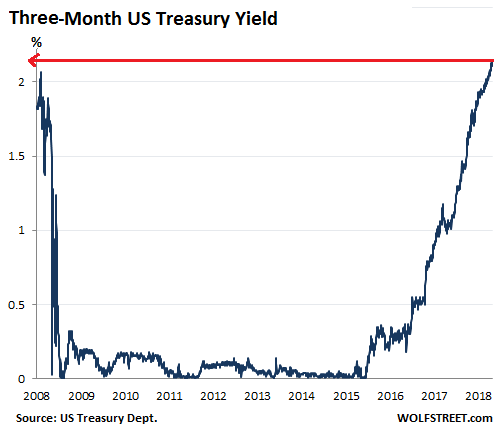

The three-month yield, currently at 2.14%, has reached the highest level since February 26, 2008. Back then, as the Financial Crisis was taking its toll, yields were going through enormous volatility, as the chart below shows. During that volatile period in mid-2008, the three-month yield spiked for a day to 2.07% on June 16, but never got back to the 2.14% in February that year:

It hasn’t been exactly a whirlwind rate-hike cycle with one-percentage-point rate hikes per meeting, à la Paul Volcker in the early 1980s, but in their “gradual” – as the Fed never tires to point out – easy-to-digest, no-surprises manner, the rate hikes are starting to add up. There is an entire generation working in the finance industry and on Wall Street who has never seen Treasury yields this high. They’re in for a learning experience.

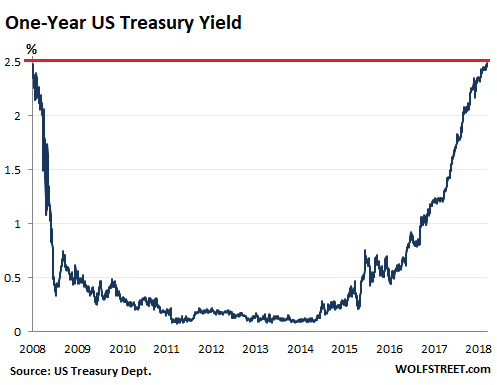

The one-year yield rose to 2.49% at the close yesterday, and remains at about the same level today, beating the 2.48% on June 25, 2008:

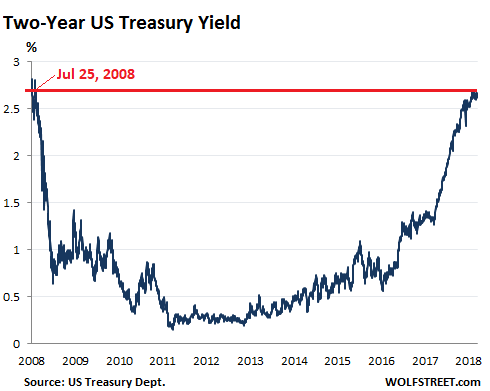

The two-year yield closed at 2.66% yesterday and trades at the same level today, the highest since July 25, 2008 (when it closed at 2.70%):

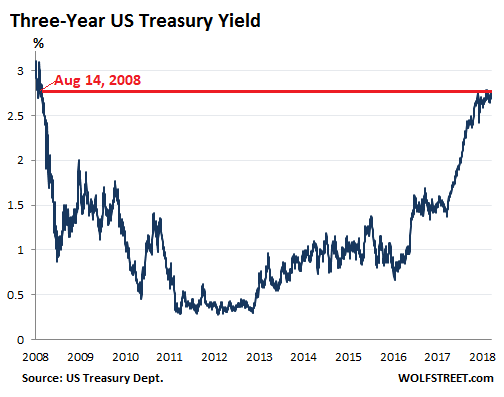

The three-year yield, at 2.73% yesterday, and edging down just a tad at the moment, is at the highest level since August 14, 2008:

All US Treasury yields through three-year maturities are now at 10-year highs. But the yields of Treasuries with maturities longer than three years still have not reached 10-year highs. For example, the five-year yield at 2.77% today is still way below the 4.16% on September 5, 2008.

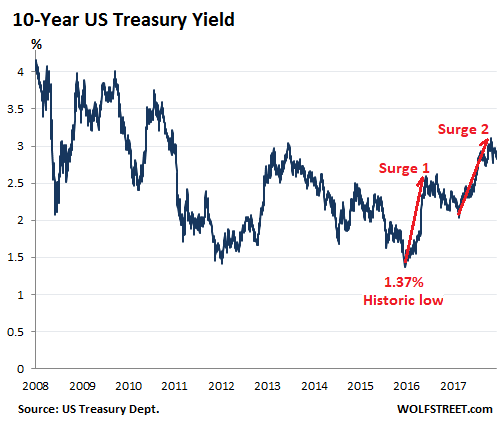

The 10-year yield has risen as well so far this week. It closed at 2.90% yesterday and trades at the same level at the moment. On September 5, 2008, the 10-year yield was 3.66%. So it will take a while before it hits a 10-year high. But note the two surges in this rate-hike cycle, each took the 10-year yield up by over one percentage point. The 10-year tends to move in these surges. And in this scenario, “surge 3” would push it over the 10-year high:

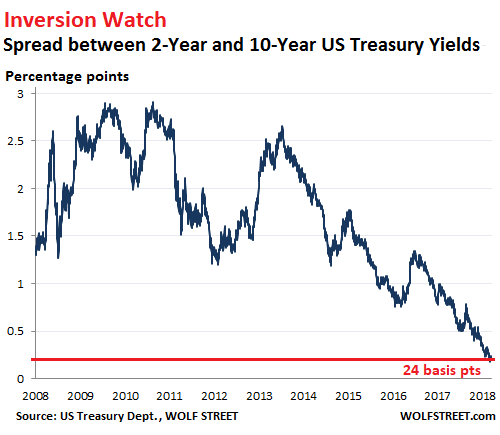

The yield curve has been on “inversion” watch since last year, where long-term yields would be lower than short-term yields – a phenomenon that in the past has been followed by a recession or worse. In recent days, the yield curve has steepened a tiny bit, and everyone is expelling an equally tiny sigh of relief. In that spirit, the spread between the two-year yield and the 10-year yield widened to 24 basis points, a smidgen off the 18-basis-point spread on August 27, a low not seen since before the Financial Crisis:

When QE 3 was announced, Wall Street called it “QE Infinity” to create the hype that the Fed would never end QE. And those folks also said that the Fed could never raise interest rates again. When the Fed tapered and then stopped QE, those folks said that the Fed could never unwind QE and could certainly never raise rates. When the Fed raised its target range by 25 basis points in December 2015, those folks said that the Fed could never raise its target range over 1%. And in the first three quarters of 2016, the Fed flipflopped and these folks seemed to be right. But then in December 2016, the Fed raised again, and has since been raising with clockwork regularity. Late last year, the Fed started unwinding QE. And the Fed’s rhetoric has become increasingly hawkish.

Five economists at the Fed’s Board of Governors published research results that encourage the Fed not to wait on tackling inflation because, in the current dynamics, “outsized deviations of inflation from its target are a plausible outcome.” Read… Fed Economists Deliver Ammo for Hawkish Approach to Inflation

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So who will crash first due to these “crazy” rates? Make your bets everyone!

1) Iran

2) Turkey

3 Argentina

4) South Africa

…others waiting in the wings

Replace “Iran” with Sweden.

Iran is sanctioned so it is harder for them to get into trouble with USD.

Sweden, OTOH, powering ahead with interest rates of -0.5%, sinkning SEK and no end in sight. Poky 3-room flats in Stockholm in nowhere really nice now costing several millions of SEK.

Except that …. come after the election where “Sverigesdemokraterne” will probably do well, there will now be a “politically unstable environment” and then they’ll raise and blame SD.

– They should have raised 2 years ago but no one dared do anything for fear of being blamed for the rise of SD. So much for the independence of central banking.

I really wish folks would stop describing the current Fed (in the context of comparing it to the Yellen Fed) as “hawkish”. The current Fed is has been following the policy path set by Janet Yellen to the Tee. There has been no change in Fed Hawkishness.

Wolf,

As the debt crisis starts gathering steam…

Is it at all possible that once the EM dominoes fall by the wayside one by one and the EU joins the party that the Fed will continue to raise rates?

What happens if the Fed stops and ECB, Japan and China start printing with gay abandon?

IMO, both are not a zero probability event.

Even if you think the above is not likely could you provide some insight on what could happen in the above scenario. I (and many of your readers probably) would really like to hear your views on this. Thanks

A currency collapse here or there in a small-ish country that borrowed way too much, stupidly, in a currency it doesn’t control, well, that’s no big deal for the vast US economy. See Argentina, Turkey, et al. Let bondholders bite their nails, and let the IMF bail them out. The Fed is going to do a lot of “closely monitoring,” and that’s about it.

But all bets are off if something really BIG happens in the US, for example, if credit freezes up, as it did during the Financial Crisis. Credit freezing up brings a credit-based economy to a standstill. So this is serious business. But I’m not seeing any signs of this scenario yet.

A stock market drop is not a huge deal for the real economy. The Fed has been lamenting high asset prices, and as long as they decline in an orderly manner, they’d follow the Fed’s playbook. The Fed wants to bring down demand and nudge up the unemployment rate in order to tamp down on inflation, and a 40% stock market drop spread over a few years (without credit freezing up) would likely accomplish that.

The Fed will monitor and do nothing because the IMF does the heavy lifting (US controlled although a couple of tweets could fix that). LIBOR is breaking out, and the notion that a 40% stock market decline won’t hurt? Your posts about PMs are appreciated and well timed. We can read between the lines ;)

A liquidity crisis seems highly unlikely. It is much more probable that high-yield bonds and leveraged loans will plummet in value, which would set of a cascade of very unpleasant credit-market events. This would hit the stock market hard, but the financial system would not be in danger. However, the economy would certainly take a major hit.

Asian contagion wasnt any big deal? The Fed can stop allowing short rates to raise at any moment by selling the balance sheet? Waiting for the yield curve to invert and not having any luck? Well bucky i could sell you a gold or silver bar to add some flavor to your adventure (safe trip)

“The Fed want’s to bring down demand and NUDGE UP the unemployment rate in order to tamp down on ‘inflation’ ..

Well ain’t that grand .. I’m sure the FedHeads are not worried in the slightest with regard to THEIR OWN unemployment prospects, whether in the present Or the future. They take care of their own, after all .. No, Those concerns are designated to the lowly shlubs who have no power over their poor fate, caused in large part by the high-tone policies of the Banksters Supreme !

Well ain’t that grand .. I’m sure the FedHeads are not worried in the slightest with regard to THEIR OWN unemployment prospects, whether in the present Or the future. They take care of their own, after all.

Bernanke & Yellen better hope the oligarch billionaires who have been the sole beneficiaries (by design) of nine years of Federal Reserve “emergency measures” and $15 trillion in printing press QE save them seats on their Gulfstreams when they flee to some off-shore hidey-hole as the pitchforks and torches close in.

The next financial crash is going to be cataclysmic, thanks to the Keynesian monetary madness of the Fed that enabled the most insane Ponzi markets and asset bubbles in human history, while tripling corporate and personal debt levels. True price discovery, held at bay for ten years by the Fed and its distortions of the economy and markets, is going to wipe out trillions in make-believe valuations and expose the true magnitude of the Wall Street-Federal Reserve Looting Syndicate’s swindles against the middle and working classes in this country.

+10

Wolf, are you familiar with Jeff Snyder’s “Eurodollar University” podcast series published at the Macrovoices website? There are two “seasons” worth of content, both seasons are well worth a listen.

Hurrah for wise global large caps issuing substantial quantities of bonds denominated in Euros, etc..

I am loving watching Jerome drive a dagger into the heart of Trump’s vampire economy. Watch the USD soar to new heights! Watch the trade deficit explode! Meanwhile the market keeps going up but the cliff gets nearer and nearer. 1929 here we come!

No collusion (a small laugh on a ugly day!) I WROTE THE OP-ED!

It was a “vampire economy” long before Trump got to it.

Their real goal is to somehow slot Pence into the God-Emperor position and begin the ritual that – according to the voices in their preachers head – will summon God!

“There is an entire generation working in the finance industry and on Wall Street who has never seen Treasury yields this high. They’re in for a learning experience.”

Wow. I never even considered that. But right you are.

I wonder what they would think of the mortgage rates of the eighties and early nineties? Savings bonds?

But go back to the year prior to 2008, and check out the rates from 12 Feb. 2007 and 31 Dec. of the same year.

3 month from 5.18% to 3.36%

1 year from 5.10% to 3.34%

2 year from 4.94% to 3.05%

3 year from 4.84% to 3.07%

10 year from 4.80% to 4.04%

In mid February of 2007, we had an inversion to say the least. Then, the 3 month beat the 10 year by 38 basis points, but in ten and a half months as 2007 closed out the 3 month lagged by 68 basis points.

Wolf, is there a reason that you begin looking at the three-month yield from February 26, 2008 and not a year earlier? Short term rates really dropped in 2007, and the 10 year eased up 3/4 of a percent.

The housing bubble had begun bursting during 2007 I believe (please correct me if I’m mistaken), but most pundits will say that Great Financial Crash is now at the ten year anniversary; which probably is true for Wall Street.

To me the most telling sign of what was to follow was published in The Economist back in mid August 2006: “Total aggregate value of USA residential real estate on 1 January 2001 = $14 trillion. In just five years on 1 January 2006 it equaled $23 trillion!”

I am not alone in being glad that these gradual rate hikes are adding up. Capital should have a price. If I could wave a magic wand as the world’s central bankers seem to be able to do, I would set rates from 2% for 1 month on up to 5% for 30 years. Somehow I doubt that anything close to that will ever happen as we are too indebted from global QE to see capital fairly priced again.

Dan Romig,

“…is there a reason that you begin looking at the three-month yield from February 26, 2008 and not a year earlier? Short term rates really dropped in 2007, and the 10 year eased up 3/4 of a percent.”

This was a post about a big milestone: 10 years. I can go back 11 years or 14 years or 15.34 years, or whatever. I mean, in 1982, rates were so high that a 40-year chart would show today’s rate as barely distinguishable from the zero line.

But 10 years is a big milestone. And that’s what this was about. Kind of a CHEERS!!

I have posted multi-decade charts of the 10-year and the 2-year to show where they overlap. And I’ll post them again. But that’s a different topic :-]

Oh, and concerning the charts, I have been using the same time span (back to 2008) since 2017 when I built these charts to document the rate-hike cycle (I used different charts before). So a year ago, you would have seen the same charts going back to 2008. But at that time, the yields were a lot lower and so the charts were lopsided. Now they’re sort of symmetrical. For me it was an interesting moment that the current yields have finally outgrown the charts :-]

My first clue as to why you began where you did should have been seen in the title: “… Hit Ten Year Highs.” The cliche, “Can’t see the forest for the trees.” pretty much sums up my question that you’ve answered, eh?

Looking back at the rates at market close on 1 August 2006 shows a one day spike in the 1 month of 18 basis points to 5.20% and the ten year at 4.99%. To my eyes, that’s the inflection point of what was about to happen. And, for a few months all yields were basically flat at around 5%.

Thank you for publishing WolfStreet and letting us comment on your site!

Exactly.

This is why china is such an issue, they have no experience of dealing with, let alone controlling, a major, internally produced, financial shock.

When they finally drop some of those huge bubbles they are juggling, and it is a when, planet beware.

The scary part of this for stock investors is that the 2 year yield now matches inflation. Unlike the past, now you don’t lose any purchasing power by sitting in cash (i.e., and equivalents). At some point, people will view cash as a viable alternative to stocks, assuming they weigh upside and downside potential. Of course, only the first few that move fro stocks to cash will get out alive. The exit door will close fast at today’s elevated stock prices.

Let’s pretend the real inflation rate is 2%. Anyone who needs housing, food, medical care, insurance, is putting a kid through college, etc. knows real-world inflation is much higher than our Soviet-style CPI data indicates.

That was basically the gist of my comment posted here yesterday but for some mysterious reason it never appeared Of course you are spot on

You cannot promote this guy on my site. He uses government data and just adds some numbers to it. His site is a hoax at best, and people keep falling for it.

Turkey has the kind of inflation he is talking about, not the US.

Pro-Tip: Short any bank where >10% of traders are <35 y.o.

That’s probably every bank. But the entire premise itself is false. In the age where the shareholder is king, Chuck Prince put it best: “But as long as the music is playing, you’ve got to get up and dance.”

Let’s say one bank tries to do the “right” thing i.e. use experienced traders, that bank WILL be punished by their shareholders. Supply of capital will be cut off and its carcass will be divided up by their competitors.

Policy makers are the real problem. The repeal of Glass-Steagal by Bill Clinton and the deregulation of the banking industry by Reagan and Bush set the stage for the 2008 financial crash. And then there’s our captured and complicit regulators and enforcers.

The entire country is the real problem. Not enough people interested in history to object to the repeal of Glass Steagal. Whenever the government says: “Do YOU WANT A PARTY?”, I’ve never heard a single no from the populace.

Goldman, please throw muppets to the wall.

Slightly off-topic, but I noticed a local savings bank, Salem 5, starting to give away free streaming services to new customers.

I think this type of offer is a result of rising interest rates. Has anyone else noticed similar behavior from banks?

A couple of days ago, I received an advertisement from HSBC in the mail offering a $400 bonus if I open a checking account with $10,000 and maintain that minimum for 90 days. Thereafter, it takes up to eight weeks for HSBC to close the account. It’s rather tempting, although I’ve been with BofA since 1983 and I have no interest in switching my main account to HSBC.

For the last 6 months, I’ve been getting roughly the same offer from Chase.

Wolf-

Why do you suppose that Treasury isn’t managing the yield curve better? That is, they could easily issue more 10 year bonds and fewer short term ones. Indeed, given the current yield curve that would be the smartest thing to do, locking in low rates for the taxpayer for 10 or 30 years.

Could this represent a fight between the Fed who wants to raise long term interest rates to deflate asset bubbles, and Trump’s treasury sec who would want to keep asset prices high at least through the next election?

Lune,

Yeah, I would think they’d start selling lots of 10-year notes. They do sell a lot of them but maybe not enough of them.

That said, these decisions are made months in advance to allow the market to prepare for absorbing these things. So the 10-year yield may be lower today than Treasury thought it would be some months ago. It might have figured that the 10-year yield by now would be around 3.5%. At this rate, 10-year debt gets pretty expensive, compared to 2-year debt at 2.67%. So to reduce costs at least over the near term, it might have decided to not exaggerate on the long-term debt side.

There are all kinds of guesses that go into these decisions, but I don’t think it’s any kind of battle between the Fed and Treasury.

Wolf, there are two ways, that I know of, to get out from under an extreme debt load. Obviously, one way is to default legally (Which the US government cannot do).

The other way is to default on the sly, through inflation which could be done by selling long term treasuries ( 10-30 year) at low interest rates before a rise in real interest rates. As you know when doing bond calculations from par to discount on 10-30 year treasuries there are significant losses of principal when interest rates rise.

Incidentally, the treasury department has not followed this process to date as Lune stated. This would minimize interest expenses for the US government.

One reason why they may not want to exercise this option too quickly would be the losses that institutions such as pension funds etc. could incur since many have large treasury positions. I suppose these institutions could use derivatives to protect their downside risks.

As for your previous article on gold, just a reminder that all central banks hold gold for hypothecation.

That makes sense. I don’t think anyone expected the 10 year rates to be as stubborn as they’ve been. That said 2 year rates of 2.67 isn’t very cheap when the Fed has stated loud and clear that they expect to exceed that within the next 18 months…

Sadie-

The thing with pension funds is most of them hold bonds to maturity so they don’t face principal losses per se, although they certainly face inflation losses as you mention

well, wolf you were right when almost everybody else was wrong. where’s peter schiff now?

the big question now is what kind of event would cause the fed to stop or reverse? european banks are in deep sh*t. what happens when taxpayers have to pay real rates on gov’t borrowing?

the other elephant in the room is pensions. if rates don’t normalize, what happens there?

The eu issues are keeping the very dirty $, looking like a freshly laundered shirt.

Why would the fed do anything to change that.

After the $ the only other fiats possibly truly safe, are CHF and Yen, both of which have their issues, or if you live in the region Aud.

Only stupid people trade the cleanest dirty shirt, for thin ones, with holes in.

I was kind of curious about this topic again after reading a Canadian news article starting to fear the yield curve.

“Stephen Poloz says this time is different: There is unusually high demand for long-term Government of Canada bonds, and that’s causing investors to accept lower interest rates on those bonds, flattening the curve.”

Not good when someone as high up and as experienced as Poloz says “this time is different”, expect similar rhetoric to keep popping up everywhere as rate hikes keep coming.

greenspan started this way back in response to dot com bubble bursting and market went on to peak and crash. rates lowered to zero, increased slowly to 5 or so, then boom again now approx. 18 yrs of the 30 year pension bond ladders have bean destroyed as they cannot make the approx. 8% yearly return they need to survive. for them to recover 30 yr rates need to increase to 12 % and 10 yr rates to 8-9% over the next several years or so. [say 5 to even 10 yrs]. this is an impossibility. for all intents and purposes, all fed, state, local pension funds are essentially irreversibly compromised and are mathematically doomed to fail [ie, they have already essentially failed]. this does not take into account the gross underfunding of the funds. thus they are kaput. if they increase rates they will kill the economy off and cause a crash [10 yr yields at 5.5% will cause market peak and crash a year later just like all the other times]. the fed budget will get blown out as well. the politicians have really done it this time. wolf, love your sight—any possible solutions?

No one will ever see four percent again in their lifetime.

Oh boy, we’re doomed to die, all of us, by next year :-]

Agreed, first it will go to negative or close to zero, and then once it’s clear that the dollar has minimal value, it will jump to 5, 10, 20 then 40%. So yeah, no one will see 4% because it will fly by so quickly the human eye can’t catch it.

That’s a good point that will come as a “surprise” some day, or so they will say. I think the pension problem will really come to surface when stocks drop 20-50%. Most pensions have a decent allotment to equities, and that share has increased the past few years.

Of course, the biggest pension of them all – social security – has no chance of fulfilling its promises. They’ll have to cut benefits 30-40%. I imagine other pensions will have to do the same. The pensions won’t fail, but they’ll pass laws that reduce benefits dramatically. People without savings will face some retirement austerity.

The chances of nominal cuts to Social Security benefits are nil. When the Trust starts running out of money, Congress will make up for it with appropriations of either borrowed or printed funds. Don’t know how long that can last but the number of dollars paid out will never go down. This says nothing about what those dollars will buy, though.

Everyone should be considering the impact of the shrinking fed balance sheet on international banking, and lending.

The consider all of the leverage that will have to be unwound with higher interest rates, including all of these things that are derivatives.

Oh well, just watch what happens.

It will be fascinating, and it will take quite a while.

“It will be fascinating, and it will take quite a while.”

Unless somebody, in an important place, makes a mistake

The 10 year yield is 100 percent rigged to stay below the 3 percent threshold mark by the same criminals who rig the stock market the commodities market and the bond market.

I have no doubt plenty of individuals “try” to rig the market. However, there is zero chance that any group rigs “the stock market the commodities market and the bond market” to the degree implied by your post.

I’ve been hearing much Sturm und Drang on possible inversion, but I note the yield curve tracked very tightly from 1994 until it inverted for a short period of time before the 2000 crash. In other words, the current situation is not a fait accompli for inversion in the near term and traders would be well advised to consider this possibility.

As for the youthfulness of people at the trading desks, the same is true in the back office from line employees well up into middle management.

Back in the day, I could tell what the indexes were doing just from the background noise level in the room. Now, it’s crickets all day every day. The DOW could (and did recently) dump 750 and the kids were basically unaware if not utterly clueless. I suspect this doesn’t rate as anything more than anecdotal, but there it is…