USD-denominated debt outside the US hits record – even junk bonds.

China announced today that it would sell $2 billion in government bonds denominated in US dollars. The offering will be China’s largest dollar-bond sale ever. The last time China sold dollar-bonds was in 2004.

Investors around the globe are eager to hand China their US dollars, in exchange for a somewhat higher yield. The 10-year US Treasury yield is currently 2.34%. The 10-year yield on similar Chinese sovereign debt is 3.67%.

Credit downgrade, no problem. In September, Standard & Poor’s downgraded China’s debt (to A+) for the first time in 19 years, on worries that the borrowing binge in China will continue, and that this growing mountain of debt will make it harder for China to handle a financial shock, such as a banking crisis.

Moody’s had already downgraded China in May (to A1) for the first time in 30 years. “The downgrade reflects Moody’s expectation that China’s financial strength will erode somewhat over the coming years, with economy-wide debt continuing to rise as potential growth slows,” it said.

These downgrades put Standard & Poor’s and Moody’s on the same page with Fitch, which had downgraded China in 2013.

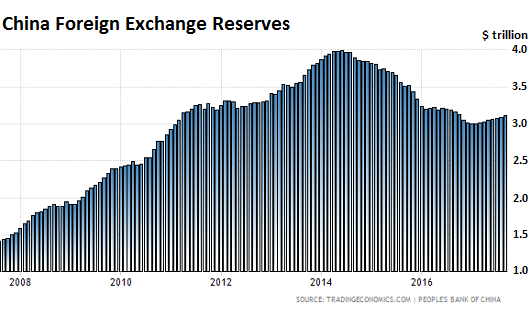

But the Chinese Government doesn’t exactly need dollars. On October 9th, it reported that foreign exchange reserves – including $1.15 trillion in US Treasuries, according the US Treasury Department – rose to $3.11 trillion at the end of September, an 11-month high, as its crackdown on capital flight is bearing fruit (via Trading Economics):

So why does China want these $2 billion in US dollars? For one, they’re still cheap, given the low yield, which is expected to rise as the Fed has started to unwind QE. And two, China might be interested in creating a benchmark for dollar-bond trading in China that could help set prices for Chinese corporate debt denominated in dollars. And there’s a lot of it.

Other emerging market governments and companies have jumped on the same dollar-bandwagon. Among them Tajikistan. It sold $500 million of 10-year bonds in September, its first foreign currency bond sale ever. S&P rated the bonds B-, six notches into junk, one of the lowest sovereign bond ratings out there. Yet at a yield of 7.125%, there was strong demand from European and US investors.

“Investors are very bullish on bonds from emerging markets and very keen to diversify into new names,” Peter Charles, a Citibank managing director who handled the bond sale, told the Wall Street Journal.

In June, even the Maldives, a minuscule nation of atolls in the Indian Ocean, was able to sell $200 million in five-year bonds with a 7% coupon.

In total, emerging market governments and companies have issued $509 billion in dollar-denominated bonds so far this year, a new record. Dollar-denominated junk bond issuance in the developing world has hit a record $221 billion so far this year, up 60% from the total for the entire year 2016, according to the Wall Street Journal:

Investors’ thirst for income is enabling governments and companies in some of the world’s poorest countries to sell debt at lower and lower interest rates.

Buyers reason that the debt pays a healthy yield and carries few immediate risks. The global economy appears robust and emerging-market defaults are low. Bankers say they expect emerging markets to sell tens of billions of dollars in new junk bonds by year-end.

The euphoria is worrying some investors, who warn that frenzied buying of risky assets sometimes presages market turning points. The average yield on speculative-grade corporate bonds in emerging markets dropped to 5.53% late last week, the lowest on record, according to J.P. Morgan. Two years ago, that yield was over 9%.

In previous times of market stress and economic weakness, junk bonds and emerging-market debt were among the asset classes that suffered sharp price declines as investors dumped riskier holdings for safer ones. The recent tightening in spreads raises questions about whether investors are getting adequately paid for the risk they are taking on.

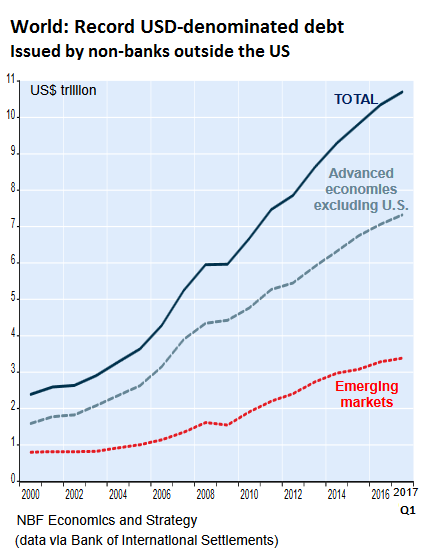

Total dollar-denominated debt owed by governments and non-bank corporations outside the US has risen to a new record of $10.7 trillion, according to the Bank for International Settlements’ last Quarterly Review, cited by Krishen Rangasamy, Senior Economist at the National Bank of Canada, Economic Analysis. In the Emerging Markets, dollar denominated debt amounted to $3.4 trillion:

Dollar denominated debt owed by governments and non-bank corporations in advanced economies with currencies other than the dollar has reached 26% of their GDP, nearly three times the level of the year 2000.

Borrowing in foreign currencies increases the default risks. When the dollar rises against the currency that the borrower uses – which is a constant issue with many emerging market currencies that have much higher inflation rates than the US – borrowers can find it impossible to service their dollar-denominated debts. And when these economies or corporate cash flows slow down, central banks in these countries cannot print dollars to bail out their governments and largest companies. Financial crises have been made of this material, including the Asian Financial Crisis and the Tequila Crisis in Mexico.

But today, none of this matters. What matters are yield-chasing investors that, after years of zero-interest-rate-policy brainwashing by central banks, can no longer see any risks at all. And the dollar remains the foreign currency of choice.

Betting against the dollar remains a favorite sport. Read… The Hated Dollar Resurges. But Why?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“central banks in these countries cannot print dollars to bail out their governments and largest companies”

So what? Isn’t that what the new “swap line” system takes care of?

Gary, PBOC was not part of any swap lines with the FRB, at least not according to Wikipedia. But I have another possible explanation: PBOC is trying to drain the USD reserves of Chinese banks by selling them USD-denominated debt in return for payment via USD-denominated reserves.

Just wait until the Chinese start their oil for Yuan (convertible for non-China gold) futures contract and let’s see how the good old 20+trillion dollar indebted dollar fares. The contract is supposed to start trading by the end of this month.

“let’s see how the good old 20+trillion dollar indebted dollar fares.”

And therein lies the conundrum: if this is a move to drive the value of the $US down, why would they embark on a program to *increase* their exposure (holdings) to the $US?

Not an expert on FX, nor even a dabbler in the field. I can only imagine that this might be a move to help push for the SDR where the renminbi (Chinese Yuan) would hold more weight as a percentage in the “basket” of currencies that would be used to form the SDR. If the (current) world reserve currency is suddenly destabilized, then the push to calm world trade and maintain the commodities markets viable may force the issuance of the SDR. Create a crisis, and then propose a solution. Once you’ve got your proverbial foot in the door as a part of a world reserve currency, like the camel nosing in under the edge of the tent, you can gradually take up more and more space in the SDR. A simple plan that would be a peaceful end to decades of a single reserve currency dominance.

It’s irrelevant. Eurodollars control global trade.

I think that dollar-denominated debt will cushion the economic shock, if the U.S. dollar ever loses its world reserve currency status. I think that is already in motion.

As a country, we should encourage it as being in our financial best interests. After the major oil producers and the goods producers, e.g., China, decide to require more dollars for their oil or goods (which may not happen soon as to China, because it is trying to put out its own, huge financial fires and cannot engage in any financial wars), we will be happy that debtors will still seek U.S. dollars to repay such debt.

I find it amusing that we are being rescued from the consequences of the massive corruption in our country centered in the financial system and the “Federal” reserve bankster cartel, by the mistakes, corruption, and fears of the rest of the world. It is further confirmation that god has a sense of humor.

My thoughts along the traditions of Mark Twain: The reports on the death of the USD has been greatly exaggerated.

I have explained on this theme a few times before, but its bears repeating that the USD will retain its vaulted reserve currency status, as long as the US can maintain her world’s most powerful and effective military-industrial machinery.

I’m not an American but I can see that USA is a surprisingly resilient country with very well developed institutions and a certain “can do” spirit that is both competitive and inspiring. Few can bet against the US economy and win. I know many Americans think their country is in a mess right now, but sometimes it takes an outsider view to have an objective perspective without the emotional biases of being immersed within the cauldron.

The US strangely always manages to find a way forward maybe because of her diversity and tolerance for new ideas. Few other countries can match her speed in innovation, her capacity to absorb shocks of all types and then bounce back stronger.

The US will never default on her debts because she can print her way out, and no one else has the means to make demands on USA simply because she has the biggest guns on planet Earth. If you have the biggest guns and the most powerful military, no one else can ask you to return them their money.

Yes, money talks, power to print money talks even louder, but the guns backing the printing press is the grand daddy of all the GodFathers insuring the value of that printed money.

Believe me or not, the US military-industrial complex is one of the backbone of the US economy. Many, if not most of the practical innovations came from investments within the US military or related technologies, in their bid to maintain their killing edge. Examples include the origins of the internet protocols, fibre optics transmission, secure communications, drones, advanced sensor and digital signalling techniques, aerospace and satellite technologies etc. It is unfortunately, the weapons drive and the untold trillions poured into it that later leaked into the private sectors and morphed into industry “disruptive” technologies.

The US military-industrial complex has technologies now that are easily 30 years or more ahead of the general public, so don’t you think there are more disruptive tech that the US economy has up her sleeve?

Isn’t it obvious which country and currency is a better bet for the foreseeable future?

USD, Russian rouble, Chinese Yuan, Euro or Japanese Yen?

Russia and China are even more unstable and fickle countries dependent on the whims of their dictators and unpredictable internal power struggles. The Eurozone is a mish-mash of conflicting concerns driven in multiple directions. They can try to be the United States of European nations, but my bets are that their experiment is going to fail eventually and the Euro will go poof. As for the Japanese, they will probably commit collective suicide as they shrink and age into nothingness.

All currency pairs are RELATIVE in valuation. The economy that is least worse becomes the strongest measured in relation to others.

So again, now where would you bet your money on if not the USD and by correlation her economy?

Whats with the Y-axis on the first chart? I see two each of all values except 4.

Seriously, Wolf – is the death of the petrodollar fake news? There are multiple reports of China – Russia (per Nikkei) working on a gold backed Yuan purportedly for oil or other trade with China? So sell in Yuan and get gold back if you want.

I think that is an aspiration of the Chinese govt. Because having over 3 trillions of $ ; they don’t need any more. So if (As you suggest) they are using it as a testbed to allow Chinese companies to borrow in $ eventually – it can mean only one thing:

USD says “The reports of my death have been greatly exaggerated”.

The practical implications of this are the following:

1) US Fed can pump and dump for quite a bit longer than their jawboning otherwise.

2) USD is still a de-facto world reserve and continues to be even with Chinese/Russian attempts to undermine it.

3) No one is issuing sovereign or corporate debt in Cryptocurrencies

4) Gold is constrained to a certain threshold (What, i don’t know)

5) Despite the misgivings of folks like us on this and other forums – America remains the last port of trust due to reliance on the USD

6) American hegemony (even financial) remains unchallenged

7) With Catexit, Brexit and other exits, Euro would strengthen 6

8) Despite being a house of cards, the US economy has the strongest cards (or at least perceived to be)

9) Last but not the least:

It has 2 vector affects on US consumers:

a) Strong dollar would make imports cheaper for a long time to come

b) Potentially (continue to) reduce employment in US of work that can be done elsewhere. This may counteract to an extent the lower cost of imports

Viva, America

What’s wrong with the Y-axis? ==> I accidentally clipped the decimal when I cropped the image of the chart. Chart with complete Y-axis is now in place :-]

1) USG benefits when they issue debt in USD and use that debt to settle BIS trade accounts with China.

2) according to Rickards the dollar is not set on trade imbalances but on interest rates and policy. if there is a rush to liquidate these bonds where do they get the dollars? Might this call into question the reality of using T bonds as sterilized US dollars in payment of trade imbalances.

3) i mean i don’t get it, how can they issue THEIR debt in OUR currency. Trump ought to tweet something and make them stop

4) and yes the petrodollar is a zero sum game, however by issuing those bonds the USG funds its deficit spending. must find a workaround i suppose.

off balance sheet solutions come to mind, direct monetization, which is inflationary.

Ambrose Bierce wrote:

“”3) i mean i don’t get it, how can they issue THEIR debt in OUR currency. “”

As I see it:

They are borrowing money and are willing to pay it back in the same currency as they are borrowing.. IN THIS CASE they want to borrow USD and nothing else.

Why borrow only USD? Maybe they have a debt to pay that may be paid only in USD. OR they may want some Euros and the seller (loan shark”?) will only accept USD for the Euros. Or they are buying crude oil and the OPEC member selling it wants ONLY USD. OR they may want to mess with the heads of the feeble minded one in DC….

Or something else….?

I am sorry, but the captain of the Titanic probably also said: everything is fine. It is just a little hole, our ship is unsinkable, and we have so many compartments and life boats.

I think that we have been incredibly lucky: so lucky that I almost wonder if some agency or group is trying to preserve the U.S. dollar as a reserve currency status, by hook or by crook. However, I am not a believer in conspiracy theories.

It is just that the events that seek to keep helping the U.S. dollar stay alive as a world reserve currency are amazingly favorable. However, no one wins every bet. At some point, our dice will roll snake eyes.

If it ends the massive, current corruption, since 11% of Americans own 76% of our wealth, I have no problem with seeing those elite lose their shirts.

“so lucky that I almost wonder if some agency or group is trying to preserve the U.S. dollar as a reserve currency status, by hook or by crook. However, I am not a believer in conspiracy theories.”

Luck has nothing to do with it.

Show me a better, And tenable haven, outside CHF which is Expensive to hold and then convert to whatever you wish to use.

The Eur had potential however Fiscal union is taking to long and there are to many other cracks in Euro-land now to consider it for at least 15 years after “Fiscal union”

maybe the chinese want to lend their dollar pile to borrowers inside china, so those borrowers can’t send their dollars out of china.

and borrow dollars from outside to do it.

uh, a virtuous circle, very confucian.

I believe some European startups are issuing crypto denominated debt. Just not at retail level.

I wonder how many foreign banks the Fed will bail out when the whole over leveraged system comes crashing down? And for a country that doesn’t need dollars, China has sure burned through a lot of foreign reserves over the last few years.

Interesting article…Wolfstreet is picking up what ZH used to be…before they went down the click-bait rabbit hole.

Curious to hear your views on how the de-construction of the petrodollar will play out and any guesses on the timeline?

The core of the petrodollar was an agreement between Saudi Arabia and the US. We buy their oil, in turn they recycle those dollars by buying our Treasuries (and exports of all kinds). That deal is no longer needed. US net imports of oil have declined to where, given the overall size of the oil trade, they’re no longer the crux.

That global commodities are priced in the largest currency in the world (used by the largest importer) makes sense for many market participants on all sides. But commodities don’t have to be priced in dollars. They can be priced in anything the parties agree to. And this has been happening slowly, and should be happening. Why do China and Russia have to convert their trade into dollars? There’s no reason. They just have to work out the details. And they will.

That the dollar will lose some share as a trading currency is inevitable. The euro already has a big share as a trading currency (in some months equal to the dollar). Other currencies have smaller shares. Inevitably, the share of the RMB as a trading currency will grow. But I don’t think this poses a problem for the US, and I don’t think it will impact the dollar itself.

I thing china and the Ems are doing in this is soaking up or stealing some of the buyers of treasuries.

Intent/s.

1 Possibly to force up US govt interest rates as the demand wfor Genuine $ treasuries will be diminished by the amount of Asian ones.

This is a dangerous gamble for the Asian/EM issuers as they do not control $ direction and only china has enough Spending power to short term influence it without drastic action’s.

“Inevitably, the share of the RMB as a trading currency will grow. But I don’t think this poses a problem for the US, and I don’t think it will impact the dollar itself.”

CNY/RMB as a trading currency is definatly growing mainly due to chuinese forcefull coercion.

What is not growing is the % of CNY/RMB HELD LONG TERM in global reserves. It is still under 1%.

JUST like RBL. As a currency that you HOLD Both the RBL and CNY/RMB are non starters.

There is a huge difference between traded and held currencies, HUGE.

“That the dollar will lose some share as a trading currency is inevitable. ”

1) As a medium for trading, dead bugs and old tennis shoes would work if there were a market, especially if someone could come up with an angle to create synthetic old tennis shoe derivatives. Obviously, this won’t be soon, but the point is anyone will trade anything if a buck can be made and a greater fool can be found.

2) Re the dollar: Would you or anyone rather go long on a Euro or dollar … say for 5 years? Once Draghi goes off to his retirement, will his successor print into oblivion (answer = yes), otherwise the Eurozone fails once people realize printing money covers a large part of annual budgets. People already agree that low rates are a managed phenomena but choose to ignore the backstory, for now.

3) The dollar vs RMB: Possibly the RMB might gain in importance, after all the empty malls and empty cities are filled and bustling while the wealth management products stop appearing like they were designed by Bernie Madoff. See point 1.

I think I’d go long the Euro rather than the dollar only because the entire world seems to be turning its back on anything US these days and that comes from an American living that reality but hey who knows

Isn’t there a piece of the dollar trade having to do with a functioning legal system with the ability to enforce contracts. If you were say Brazil, would you rather write your contract under the US legal system or the Chinese or Russian legal systems and currency? Or the Saudi’s or ? Having an enforceable contract in a relatively stable currency may be the strongest argument for the dollar.

Yes, that’s what makes bonds with contracts written under US or UK law more attractive to foreign buyers than bonds written under, for example, Argentinian law. But that didn’t keep Argentina from defaulting on those bonds, as we have seen. There is some risk mitigation with foreign currency bonds (lower inflation, legal issues, etc.). But the credit risk can be very high – and it can happen suddenly.

“Yes, that’s what makes bonds with contracts written under US or UK law more attractive to foreign buyers than bonds written under,”

This is what makes me laugh with all the talk of all the banks leaving london and going to Euro land.

Those banks are in London as they issue bonds and like to, under “London Law”.

They may be forced to move some trading and clearing to Euro land they can not however move “London Law” to “Euroland” as it would become Bad Parisian Eurotrash law.

This is a free-for-all right now. Take out debt and spend like crazy. Then repudiate the debt down the road. We’re obviously at the point where debts will not be repaid.

The US Gov’t will be repudiating its $70T debt soon. Lots of articles lately about how pensions, social security, and medicare are ponzi’s.

Bobber,

Unfortunately, repudiation will result in massive upheaval and dislocation. The economic ticking watch only runs on perceived stability which implies a return for investors. I do believe there will be a huge corrrection and reset, mainly because this current valuation farce is built upon a foundation of greed and race for yield. But debt repudiation will result in a scad more Zimbabwes.

I just hope you are wrong because the result will be more misery than people remember or can imagine.

QUOTE: “But the Chinese Government doesn’t exactly need dollars. On October 9th, it reported that foreign exchange reserves – including $1.15 trillion in US Treasuries, according the US Treasury Department – rose to $3.11 trillion at the end of September, an 11-month high, as its crackdown on capital flight is bearing fruit (via Trading Economics):”

Okay, I have a question about this. These so-called “foreign exchange reserves” of China, they are not exactly the property of the Chinese government, are they? Are they not USD reserves of the Chinese banks, part of the capital of these banks?

If so, it is perfectly plausible that “China” (banks) can have large USD exchange reserves (or perhaps USD-denominated debt holdings), but that the Chinese government itself may have no surplus of USD, and indeed need to borrow USD for whatever purposes.

Same goes for any country that reports “foreign exchange reserves” — it is not necessearily (and most often not) the government that owns these reserves. Am I wrong?

In China doesn’t the government own everything? If YES, while the reserves are owed to the banks they are owned by the govt.

Someone from China or in expat would do us favor explaining property rights and different ownership classes…private/public/x/y/z in China. I don’t want to restrict to binary…

If the Chinese government really needed dollars, it has some options. For example, the PBOC could just print some yuan and buy dollars with it. If this is done on a large scale, it would put pressure on the value of the CNY v. the USD. So there are some limits. But $2 billion is nothing for an economy the size of China.

The Bank of Japan has done that to bring down the yen. It didn’t need the dollars, either. And the Swiss National Bank is still doing this, to enforce the cap on the CHF.

However, some countries worry about their currency losing value, such as Mexico. It cannot create pesos and buy dollars because it would crash the peso. It has been doing the opposite: selling its dollars for pesos to prop up the peso. The Mexican government also issues a lot of foreign currency debt (in dollars, euros, and yen) because it needs to borrow money at a lower cost. Borrowing in pesos is expensive. The 3-month yield on its peso debt is about 7% now, vs. 3-month US Treasury yield of 1.1%.

“If the Chinese government really needed dollars, it has some options. For example, the PBOC could just print some yuan and buy dollars with it. If this is done on a large scale, it would put pressure on the value of the CNY v. the USD.” Hasn’t that been what’s been happening for years, and isn’t that what’s happening now? Hasn’t the long term trend been the weakening of the yuan, with only temporary pauses as the Chinese government engages in various swaps and forwards in the background? Why have foreign reserves dropped by over a TRILLION in only a matter of years? Keep an eye on China’s interbank rates and “reported” treasury holdings. If China doesn’t need dollars, it’s doing a very good job of pretending it does.

That “11 month high” of $3 tn in reserves is actually close to a 6-year low. At their peak, in June 2014, they had almost $4 trillion.

From wikipedia:

Foreign-exchange reserves (also called forex reserves or FX reserves) is money or other assets held by a central bank or other monetary authority so that it can pay if need be its liabilities, such as the currency issued by the central bank, as well as the various bank reserves deposited with the central bank by the government and other financial institutions.[1]

Let’s be real, it is not feasible nor smart for the China government (Cgov) to confiscate outright the USD reserves of the China commercial banks (said reserves being on deposit at NY Fed, presumably). That would just cause a panic among bank depositors and unrest in China, and rightly so.

So instead Cgov is selling dollar denominated debt to its commercial banks, taking payment in USD reserves, and thereby removing USD reserves from the China banks. Which perhaps is the whole purpose of the operation.

Why would Cgov want to do this? I’m not sure. But perhaps this is just another part of the overall strategy of reducing/stopping the USD capital flight from China.

If we look at it from the side of the debt issuer, couldn’t be just a sign of severe despair to ask for money and promise that you will give usdollars back?

There is serious despair… among the savers who have been allowing zombie companies to stay afloat and many people to live well beyond their means since 2009.

The typical saver owns (or used to own) a highly varied mixture of assets which can vary between AAPL stocks and physical wands of Swiss francs/US dollars.

Traditionally one of the most prominent of these assets are securities, especially those of investment grade and with an above average inflation fixed yield. This asset class has been effectively wiped from the face of the world and this is something we are already paying dearly.

Desperate savers will hence look to junk bonds, such as those issued by shady African fishing companies, to cover the difference but most of these bonds have a big issue: they are issued in “emerging market” currencies. This means just converting the yield into the reserve currency of your choice is a hazard as these currencies are highly volatile and prone to bouts of mass inflation (defined as losing 9 to 49% of their value over a year).

There’s also the issue of benchmark rates: EM currencies tend to have relatively high benchmark rates meaning borrowing in those currencies is expensive relative to, say, US dollars or UK pounds.

Hence the issue of bonds denominated in reserve currencies. These have the double benefit of being far more palatable to savers in Europe and Japan driven to near-insanity and having far lower benchmark interest rates.

While junk bonds have their place in many (but not all) portfolios, using them to replace investment grade securities, such as my bank attempted doing, is effectively insanity.

Plainly put the risks savers run are completely out of proportions with the miserable yields they get.

I am not the only one thinking like this: recently the BNS bemoaned Swiss savers are sitting on “record amounts” of cash. I must confess I have never been so heavy into cash myself: there’s literally nothing to buy to replace investment grade bonds and I am not increasing my exposure to equities, let alone buying any of this high risk financial junk, at least not at these yields.

As usual not a word of gratitude for us savers who have been sacrificed on the altar of cheap car loans and 7.1% Tajikistan bonds.

Well said about safe investments.

About Tajikistan or Maldives. These loans will probably keep the crony governments going for another year, then default.

Looks like China’s Shanghai market wants to go down, but Chinese central planners won’t let it, at least not until after the CCP conference later this month. That chart looks like numerous central bank interventions. Must.project.stability.

http://www.marketwatch.com/investing/index/shcomp?countrycode=cn

Oh boy, I can already feel it……………

Another interest rate coming in December and the unwinding of QE is going to put a lot hurt on those people buying that crap.

A couple of more interest rate increases next year and then maybe Mr. Market will wake up to what is going on.

Denial in the FX market is rife and can be seen in the A$ which again is increasing in value even though iron ore is under US$60 a ton……………again.

It will be interesting to see if the Chinese start sending more money out of China as the Yuan falls in value.

Here in Oz, foreigners bought 25% or so the the new housing stock in NSW and 17% in Victoria last year. It seems the money flow and people never stops.

And for those that want a quick peek at the RE market in Melbourne, here is the latest headline about houses prices here:

“According to the Domain Group’s latest State of the Market report, released on Thursday, Melbourne’s median house price has risen to $880,902, a jump of more than $100,000 over the past year.” And

“House prices have now consecutively risen every quarter for five years, but the latest figures show growth is tapering off.”

I wish my house went up in value by A$100,000 last year – that would have been really, really nice. Better than working for a living.

That median figure is really skewed by the data from the ritzy, expensive areas near the CBD. The inner east, south, and suburban house price median is $A1.6, $A1.3, and A$1.5 million respectively.

Even the median house price in my area has soared as a result of a huge number of houses in the A$1 million plus price range that have sold recently

Next quarter when there are very few of those that come on the market, the stats will show that prices will have plunged………..

It will be interesting to see if the Chinese start sending more money out of China as the Yuan falls in value.

The wild gyrations in Bitcoin on various Chinese rumors and “crackdowns” looks like manipulation on a large scale by senior Chinese officials. It also looks like capital flight is accelerating.

Good post, thanks for the boots on the ground commentary.

Most people refuse to see the forest for the trees and thus rely solely on their implanted biases.

– And this is the reason why the USD rises in a crisis because when one is long USD denominated stocks, bonds, etc then one is automatically short the USD.

– 2008 provides a good example what happens when people start selling their stocks, bonds etc. Then they sell their bonds and “buy” USDs. Then demand for cash denominated in USD is (much) larger than demand for cash denominated in e.g. EUR, BRL, CAD, AUD. That’s why the USD rose sharply in the 2nd half of 2008 against a whole range of currencies (except the Yen).

– That’s why attempts by Trump and/or the FED to talk the USD lower will be futile.

– In that same 2nd half of 2008 we also saw the most toxic combination of 2 things happening: A shrinking US Trade Deficit/Current Account Deficit in combination with an (sharply) rising US federal budget deficit.

History is about to repeat?

Just like the Roman Empire didn’t fall in a day the De-dollarization is happening but is going slowly.

Maybe, but there’s no real long term alternative than the dollar. Everything else is hype, hope, and sales pitch to maintain trading markets. Given the endless need to print Euros and the endless need to manage Chinese society, a bongo buck makes as much sense as a substitute for a dollar as these two main stream alternatives.

Correct.

The USD is currency #7 of the historically dominant international currencies, since the advent of the ‘aureus’ of the Roman Empire.

The change from one global currency to another is a VERY slow process. Empirical records show one-to-two generations, sometimes longer.

During the switch, other currencies contribute as “fillers” in the change.

Those whom are prognosticating a “crash” of the USD have it wrong.

It will never “disappear”. Just suffer a slow international degradation, until it survives only as the currency of America within it’s borders.

Here I am, standing over here reading all the erudit comments, agog at the breadth and depth of the information flowing past – but totally confused! If I was the boss man at the PBOC I might just think that now might be a good time to grab off some cheap US$ in whatever form and use them to buy gold to stengthen my currency because the whole world financial mess is about to go south and guess what? Maybe I won’t have to pay the $ back!

Could it not be as simple as that?

The absolutely last thing China wants is a collapse of the US dollar. It would totally crush its economy and worse.

Important comment Wolf. A lot of people don’t realize that in a world of fairly free trade, there is no longer a need for empire. China doesn’t need to conquer Chile to get copper from Chile, it can just trade for it. Which means there is no real need for war anymore.

And global trade also make us all very interdependent. China is better off with a healthy growing USA and the USA is better off with a healthy growing China. It’s only zero sum if we choose it to be.

Smart world leaders understand this.

That’s a benefit of the Iran nuclear deal that I don’t see mentioned, anywhere (‘cheating’ notwithstanding): as Iran becomes more knitted into the world economy, it will have more incentive to ‘play nice.’ And, that’s the danger with North Korea not–for the most part–being part of the global community: nothing, really, to lose. Iran doesn’t want to buy billions of dollars worth of Boeing and Airbus aircraft to convert them to bombers.

That’s the thinking that led people to fall head-long into WWI.

“A lot of people don’t realize that in a world of fairly free trade, there is no longer a need for empire.”

Fairly free trade that benefits exploiter countries, that game the system at the expense of Western Unemployment .

Deliberate hollowing out of western economies and society’s to benefit a few oligarchs and their corrupt Mafia State allied governments.

Whilst keeping the lowest boat this free trade was supposed to raise first, firmly locked at the bottom.

Making the world for all but a few Worse off and much more dangerous.

Thats what your Fairly free trade globalization has achieved to date.

Either everybody starts playing by the same “strip mine the planet grossly abuse the poor” rules as china, or china and others start playing by the same rules as the west.

The Multiple systems played against each other, only benefiting china, can not continue.

Further it wont for much longer, with out massive long term negative consequences, for everybody.

A few comments on the China, NK, and Iran posts……….

Iran under its current leadership along with NK will never ‘play nice’.

Their philosophy and world outlook do not have ‘nice’ in them. If you ‘play nice’ with regimes such as those you are going to get your head handed to you.

China will game the system and adhere to it as long as it benefits from holding dollars and has access to the dollar markets in trade and finance.

(And by the way, the Iran deal is one of the worst deals that the USA has ever signed and the reasons for that assessment are based on my experience in the military.

Why in the world did we ever get involved with GW II……………….)

The reach for yield knows no borders. I’m not surprised to hear that China and emerging markets are issuing increased amounts of USD debt. I’m sure the rating agencies will bless it, like in other bubbles.

In this market, US banks, Ford, and GM could issue bonds securitized by future bailout monies. Why not build the bailout right into the plan.

Everyone knows this spineless government won’t let a hair fall off a dog in summer.

Ford didn’t get a bailout, Chrysler did (all got lines of credit from the government).

The reach for yield will eventually return nothing, as the highest yields are the most speculative investments.

So much capital will be destroyed by bad investments that it will make just sitting in cash look attractive.

The one point that everyone keeps missing is that the Fed is now actively running off the balance sheet, and shrinking the supply of money (albeit in a very gradual fashion), so dollar high power money is going to shrink over time.

Now, just think about a flight forward energy company like APA- $16 billion in equity value poised atop $6 billion in net balance sheet equity value. A minimal dividend, and uncertain energy pricing forcing operating losses?

$10 billion in valuation is simply a ?

Now, everything is leveraged up, and flying along with no real money in it. When the world is simply speculation, it pays to simply gamble. But what happens when the Martingale sings?

Delevering is a very bad meme for rentiers, and while they will clamor for continuing addition of high powered money, when the economic activity underlying the speculations does not yield a sufficient return, then return of capital once again becomes a problem.

In short, the world economy can keep churning along, and delevering will leave a lot of financial manipulation as dead as Sears.

The mirage of low interest rates should be concrete if higher rates mirror high risk- remember when high risk meant 15% annual interest rates?

The real problems start with the distortions of central bank fear of the rentiers. Let them eat cake- the people on the bottom will not take another round of austerity with banker’s being bailed out.

In short, the fear of de-dollarization is not a risk today, but for 30 years from now. Today, looking at commodities and the lack of wage growth, the biggest fear will be a long slow 15 year grind down of equities and bonds. Japan is our model circa 1990…..stagnation and the politics of contraction.

“With Yellen the Felon and her gang of counterfeiters and racketeers at the Fed intent on debasing the dollar into worthlessness”

You keep saying this; I don’t think you know what this means.

Oh we all know exactly what Gershon means

Will buy Maldives bond offering and won’t touch AAA mortgages on Fed Balance sheet even when Fed has sent 10 years of interest on trillion$ of “excess reserve” to its coop of banks and international friends expropriated from the money supply?

– In the posts above there has been talk about the socalled PetroDollar (PD). But a lot of people don’t understand the impact of that PD.

– The socalled PD (oil & commodities priced in USD) means that the US is FORCED to run Current Account Deficits (CAD)/Trade Deficits, that our US economy is subsidized by foreigners.

– US military spending outside the US (think: Capital Account) weakens the USD and that forces those same foreigners to subsidize those US wars outside the US even more.

– Are there no detrimental effects at all for the US (consumer) ? Yes, there are. A weakening USD means that US consumers pay higher prices for the same consumer goods than those foreigners.

– The weird thing is that the US consumer determines by how much foreigners are subsidizing that same US consumer. If e.g. the US consumer – for what ever reason – decides to spend less, and the CAD shrinks to zero then foreigners will stop subsidizing the US consumer.