Hype works, until it doesn’t.

In theory, stock markets surge because earnings are rising or are expected to rise. But the astounding thing in this eight-year bull market is the combination of how far stocks have surged since 2011 and how lousy earnings have been – globally!

I’ve been pointing this out for US equities, but this is a global thing, with global implications, and of global magnitude, and on that level, it’s even grander and more astounding.

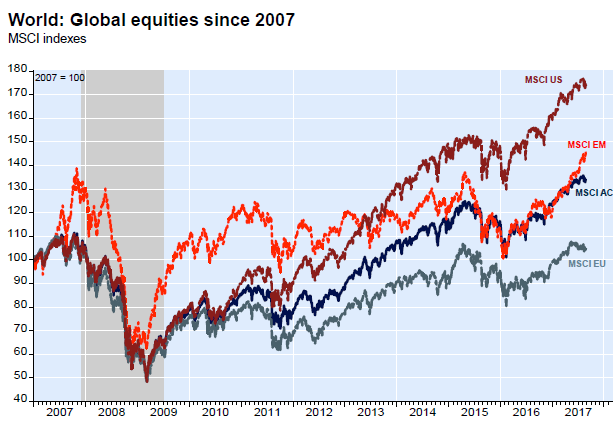

Global stocks, as measured by the MSCI AC, which tracks equity returns in 23 developed and 24 emerging markets, has soared over 11% year-to-date and is up 32% since pre-Financial-Crisis peak-year 2007. Some components within it:

- The MSCI US, reflecting US equities, is up 11.5% year-to-date and 75% since 2007.

- The MSCI EM for Emerging Markets surged 23% this year and is up 45% since 2007.

- Even the MSCI EU for European equities is above its level in 2007.

This chart by Economics and Strategy, National Bank of Canada, shows the increase of the MSCI indices for the US (brown line), Emerging Markets (red line), the World (blue line) and the EU (teal line at the bottom). The left scale is set at 2007 =100. So when the MSCI US is at 175 on the left scale, it has surged 75% from 2007:

So you’d think that these surging stock prices would be based on surging corporate earnings, that companies are raking in profits hand over fist, and that financial engineering, “adjustments,” and share buybacks are making these earnings looks even fatter and grander.

And you’d think the “estimated forward earnings” would be booming. There are what analysts and corporate PR departments put out to be their hope for future “adjusted earnings,” which are then massively slashed as earnings reporting dates move closer so that “adjusted earnings” have a chance of beating the lowered estimates. These “adjusted earnings” are earnings as reported under GAAP minus a ton of bad stuff “adjusted” out of them. They contrast with GAAP earnings.

The difference between earnings under GAAP and “adjusted earnings” can be significant. For example, these are among the biggest sinners in the S&P 500 for the second quarter (FactSet):

- GE’s “adjusted earnings” of $0.28 per share were 87% higher than GAAP earnings of $0.15 per share.

- Coca-Cola “adjusted earnings” of $0.59 a share were 84% higher than GAAP earnings of $0.32 per share

- DuPont’s “adjusted earnings” of $1.39 per share were 42% higher than GAAP earnings of $0.97 per share.

- Merck & Co. “adjusted earnings” of $1.01 per share were 42% higher than GAAP earnings of $0.71 per share.

- Pfizer “adjusted earnings” of $0.67 per share were 31% higher than GAAP earnings of $0.51 per share.

These forward earnings projections that are designed to inflate stock prices are the highest possible hope for “adjusted earnings.” But the ugly reality is that even these forward earnings estimates, however inflated they may be, went on a wild roller-coaster ride and, on a global basis, haven’t yet reached the peak they’d hit in mid-2008.

These are “forward earnings” expectations. They reflect hope not reality. These hopes didn’t begin to plunge until later in 2008, when the Financial Crisis was already in full swing.

This chart by Economics and Strategy, National Bank of Canada, shows that roller-coaster ride of global forward earnings per share, their peak in 2008, the plunge during the Crisis, the V-shaped recovery until 2011, and then the earnings doldrums. The last few years were rough for earnings (I added the red line):

So global forward earnings estimates by this measure today are finally back where they’d been in 2011 – six years of stagnation – but remain below the peak in 2008. If you ignore the plunges in between, forward earnings have now stagnated for nearly a decade.

And yet stocks have surged and surged and surged.

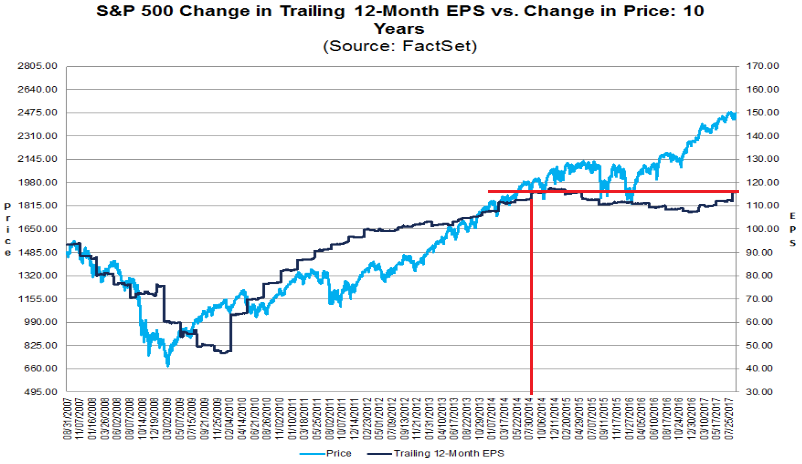

For stocks in the S&P 500, aggregate earnings per share (EPS) in Q2 on a trailing 12-months basis – adjusted earnings as reported, not as hoped – rose for the second quarter in a row are now where they’d been in… July 2014. Yet, over these three years of earnings stagnation, the S&P 500 index has soared 26%.

This chart shows those “adjusted” earnings per share for the S&P 500 companies (black line) and the S&P 500 index (blue line), via FactSet:

Since early September 2011, “adjusted earnings” per share for the S&P 500 have risen 21%, and the S&P 500 index has soared 113%. Nuts?

This relationship between stagnating earnings and soaring stock prices is not an indicator of a healthy market. It’s an indicator of dizzying “multiple expansion” when PE ratios blow through the roof, and when speculation knows no bounds. But PE ratios revert to the mean, and in the process overshoot to the downside, which forms the mean. This process of “multiple contraction” is carried out on stock prices.

Every time before this process begins, we hear that this time it’s different, that this time there are real reasons why high PE ratios will go ever higher, and why they won’t contract, and we hear that the paradigm has changed, and that the old measures no longer apply. That’s what we hear every time. And just when that chorus about the new paradigm gets sufficiently deafening, the process of multiple contraction takes off. This can be a slow and halting process whose beginning might not be remarkable, with many ups and downs that could drag out for many painful years.

This is how monetary policies have crushed the value of labor. Read… The US Cities with the Biggest Housing Bubbles

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Bubbles looking for pins. CAT bond market just found its pin

Pins and needles!

You can thank flat household incomes as compared to rising housing, education, healthcare and health insurance costs eating into disposable income. Not to mention the hidden food inflation that is there but no obvious because the CPI is rigged.

The Zimbabwe and Venezuela stock markets soared while the underlying economies were being destroyed and their currencies debased into worthlessness. Just saying’….

Their stock markets are denominated in their destroyed currencies. Once a currency hits hyperinflation, anything denominated in that currency is meaningless because you don’t know from one hour to the next just how much value that currency lost.

Aren’t all the global trading currencies being competitively debased against each other? If currency is the measuring stick we use to value companies and this measuring stick is slowly shrinking with all other sticks then of course companies will be valued ‘more’ on these shrunken measures of value.

While this may be true, the current debasements of the above referenced economies may not be comparable to what we are experiencing in the global economy today.

With most parts of the developed world accelerating debt ratios and printing at the same time, we must analyze this from a relative currency perspective.

Specifically, all developed world currencies can not crash at the same time. There should be relative weakness over long periods of time for the worst offending nations.

Other likely conclusions. This debasement will be felt in the financial comfort of the participants of these economies as their income and savings do not have the same purchasing power. ie currency debasement will be felt through the individuals in an economy ultimately.

This is playing out at the ballet box, as voters are rejecting the status quo. I suspect this will continue or accelerate to even more extremes politically until something dramatically up ends the current monetary regimes.

While it is near impossible to determine the events as they play out, some conclusions can be drawn.

People’s standard of living will erode under this monetary regime.

Attempt to maintain wealth out of debased/ debasing currencies. This bodes well for commodities.

Blockchain looks most interesting. As it has the potential to end debasement within specific payment streems.

I have some good references for this topic for further reading.

Andy

Per my earlier post,

Found the “bible” of inflations.

Monetary Regimes and Inflation by Peter Bernholz

so what are you saying, we have hyperinflation without the hype? Bob Prechter says that hyperinflation comes after a deflationary crash, but the resulting hyperinflated currency never arrived, despite fed money printing, possible because of global coordination, since all currencies trade relative to one another, and the difficulty for Venezuela and Zimbabwe is no real connection to global trade. Venezuelas economy is entirely crude oil, and crude oil has crashed. if the global coordination were to end, and its hard to see how that could happen because any country which leaves the global trade pact is going to suffer the consequences.

Venezuela has hyperinflation, not the US.

This is true, but I would argue that the U.S. dollar also has been effectively, subtly “debased.” The QEs of the “Federal” reserve bankster cartel (called the “Fed”) mean that said entity holds ludicrous amounts of treasuries. See https://fred.stlouisfed.org/series/TREAST

I would contend that, despite obvious differences (e.g., U.S. treasuries have to be repaid at a certain time and have to pay interest dictated by demand at the time they are sold) U.S. treasuries are essentially U.S. money. Thus, when you put out vast amounts of treasures, plus vast amounts of other “digitally created” dollars, to save the banksters, you are debasing the U.S. currency.

Only the crises in other countries, e.g., Chinese commie crooks trying to take their ill gotten profits out of China that put them in a “safe” haven in the U.S., have prevented more loss in purchasing power for the U.S. dollar. Really, if I were working for the Fed, and had no ethics as I opine that they have none, apparently, I would seek to promote or create crises in other countries to keep the bubble in the value of the U.S. dollar inflated. “Wag the dog.”

The Fed has so many U.S. Treasuries that its decisions to sell can harm or destroy the U.S. Treasury market by fueling panics, and thereby hurt the U.S. stock market collaterally. (Of course, declines in the value of those treasuries also mean that the Fed will be bankrupt if interest rates rise a little.)

I submit that the stock market and the treasuries market in the U.S. are linked: investors have to either invest in stocks with ludicrously high PE ratios or in treasuries that may lose much of their value if the Fed starts selling masses of treasuries and the massively increased supply of treasuries (versus the limited supply of purchasers of Treasuries, particularly if there is a panic or loss of the reserve status of the U.S. dollar ) takes their price down. Treasuries also have a demand curve.

I think that may be the reason why even institutional investors, and other investors, are holding stocks. Institutional investors have to invest to chase yield as part of their fiduciary obligations; low yield is better than no yield.

A manager that invests in some high risk foreign country, which may pay a higher yield, is more likely to lose his job than one that sticks to “proven” markets, like the U.S. stock market. Asset managers will seek perceived safety.

Other investors, who manage investments for the wealthy, for example, may also invest in some stocks as the slightly less risky alternative than treasuries. Stock prices are inflated despite ludicrous PE ratios (which prices are supposed to be based on future, anticipated earnings not just current earnings versus prices), because investors figure that no QE unwinding is practical.

In other words, the U.S. government cannot pay its current debt obligations as it goes along if the rates that it has to pay on its regular refinances by sales of treasuries spike past a certain (very low) point. See https://www.usnews.com/news/articles/2012/11/19/how-the-nations-interest-spending-stacks-up

See also http://www.politifact.com/wisconsin/statements/2013/sep/15/chris-kapanga/interest-payments-us-debt-exceeds-us-tax-revenue-w/. I read quite a few articles about this critical point: the interest rate for U.S. treasuries at which the U.S. government will have to make enormous cuts on all spending just to avoid defaulting on its ongoing current debt obligations.

Investors may realize that the U.S. government is in too much of a tightrope act to allow interest rates on Treasuries (and thereby other interest rates) to rise much. Thus, an unwinding of the QE holdings is too risky to begin in any substantial way.

The inflated stock prices and incredibly high price earnings ratios may reflect the calculation that these stocks earnings (low as they are) may represent a better future return on investment. This means treasury interest rates are expected to remain low for many years.

Keep in mind that the Fed is in a dangerous position. If it sells too many U.S. treasuries, it will be effectively bankrupt if the value of those U.S. treasuries that it holds dips below a low threshold. The rise in interest rates if the Fed sells too many treasuries will also essentially “bankrupt” the U.S. government due to its debt service payments rising, so it will not be able to bail out the Fed, as before.

The Fed is holding on to the tail of a tiger, which will devour it if it lets go. It could not happen to nicer guys. Unfortunately, before we break out the popcorn to enjoy the scene, we must remember that the U.S. economy is on the back of that tiger, and we will be the next meal.

I think, as to foreign markets, that investors in stocks opine that those many governments also must keep supporting low interest rates and thereby manipulating their stock markets. Certainly, there could not be billionaires and trillionaires manipulating our U.S. and EU governments to protect their assets and profits, so these are just coincidences.

Thankfully, low rates and QE from the ECB and BOJ, reinvestment and low rates from the Fed, and Swiss bank stock buying are supporting the markets. Earnings, forward or otherwise, are window dressing. Investors are safe. The government is here.

Algos are the tool of the globalists, who depend on low rates, low wages, and flexible labor sources for their wealth. High markets send the message of prosperity. The low wages and low rates are good and necessary for some. Without them, the markets would not reflect prosperity. The message of prosperity from the markets pacifies the media and the government. Those who aren’t globalists who own equities feel wealthy. It’s a good life. (Earnings don’t figure into this feedback loop. Sorry.)

Higher rates for all who depend on interest income for personal income would toss a monkey wrench into the globalist plan. Earnings would start to matter again.

I wish I had a crystal ball.

you make an excellent point that explains why things may in fact be different this time – currency debasement.

The central banks have tipped there hand and the cards they are holding reveal they are willing to support asset prices even if it comes at the cost of destroying their currencies. They seem to be confident they can wipe out debts with inflation and start all over again with new fiat currencies. The only losers are savers and luckily there are not m many of those around.

Re savers: negative interest rates finish them off. Think of it as taxation to pay for socialized benefits and subsidize those who profit from being able to borrow at low and possibly negative rates. Best scam ever!

It used to bank robbers. Then came bank owners. Now it’s globalists who put their people in charge of central banks. (Hint: if you can control what they believe, you control them. See ‘Long Game’. See ‘Crisis as Opportunity’. Review bizarre theories that would have seemed comical a decade ago but are entrenched today.)

Almost everywhere you look there are government and CB policies that punish what used to be considered virtuous behavior (thrift, prudence – the ability to support oneself in adversity without outside help), and reward profligacy. There is no public shaming and shunning, and of course no jail time for those who cause widespread economic hardship.

I wonder if even another great depression would turn this social acceptance of bad behavior around.

Surging stock prices have more to do with a rigged bond market than with surging corporate earnings, which for the most part, do not exist. I used to be a regular buyer of muni bonds but haven’t bought any since Meridith Whitney’s bear market in California munis came to an end in 2011. Fortunately, when I was in the muni market, most of my purchases had good call protection and many were zero coupon/non callable. My longest bond comes due in about 11 years when I will be over 80, if I am still around then.

“Surging stock prices” correlate most directly with central banks mainlining $15 trillion in financial crack-cocaine “stimulus” (that they’ve acknowledged) so their bankster cohorts can engage in an orgy of speculative excess and asset-stripping of the distressed middle and working classes, with any and all losses transferred to the public ledgers or printed away by the central bankers.

For the past nine years the Fed and it’s fellow Keynesian fraudsters and “former” Goldman Sachs officials at the ECB, BoJ, BoE, BoC, etc. have used our Soviet-style CPI and BLS statistics to maintain the fiction that inflation is under 2% and the unemployment rate is ~4.5% (with 94.5 million euphemistically “out of the work force.”) Then they systematically bilk savers out of interest income through NIRP and ZIRP, forcing them to seek yield in the rigged Wall Street casino or equally manipulated and fraudulent “markets” overseas.

So now, after nine years of “emergency measures,” these Keynesian fraudsters and their grifter accomplices are running out of road to kick the can as the truly insane mountains of debt their ultra-loose monetary policies have created, the ailing REAL economy, and massive derivative overhangs are threatening their Ponzi markets and asset bubbles.

When will it end? I don’t know, but when the Fed and its coterie of fellow banksters can no longer play extend-and-pretend, the collapse of the their financial house of cards is going to be one for the books. And our captured media, politicians, and regulators will bleat that nobody could’ve seen it coming.

Gershon – You nailed it 100% A to Z. Seems like fiction to write but sad truth. This crisis will not land softly, especially when you have zero dry powder from a decade of exploiting “emergency measures”.

It’s not ‘Keynesianism’ – not even close. It’s just a fraudulent system by a bunch of ex-investment bank employees who are now entrenched in central banks globally and are making sure that their buddies still working in said investment banks (one in particular of course) have lots of cheap cash to speculate with, whilst they think up fancy names such as ‘quantative easing’ to justify transferring the risk of said speculation onto the state.

Politicians in those states are kept sweet by promises of great riches upon termination of their political careers, and populaces are kept mollified by the ever-rising price of their houses and lots and lots of lovely credit card cash to splurge.

Said financiers even have everybody believing that ‘debt is wealth’.

I guess you have to admire it in a grudging way. Everyone is living inside a cult of debt and – like all members of cults – they are quite happily sleepwalking, enjoying the fake ‘prosperity’, and don’t even realize it, whilst the financial speculators clear the pantry.

And the politcos are so brainwashed and dazzled by promises of future fast, easy riches, they even allowed the speculators to completely destroy the world’s economy – then go back to exactly what they were doing within the space of a few short years!

Remarkable.

The Federal Reserve cue card:

Step 1: Create fake money stealing value from everyone

Step 2: Loan the fake money to people with interest

Step 3: Take people’s stuff when they can’t repay the debt

Step 4: Get government to enforce our fraud

Step 5: Plunder humanity

YOU ARE ABSOLUTELY SPOT ON!!!

Amen

I too have not bought a muni bond since 2010. I always wonder who is buying muni bonds at these depressed rates. But they don’t seem to have a problem selling them.

Tax exempt. But after Puerto Rico, is that enough of a carrot?

Remember guys, no shorting. You’ll only be losing money for nothing.

Now, THAT’s one for the books!

Boy, if we just had “free markets”, all of this would get cleared up by our deity, Mr. Market and the Profit Motives. (Should be a band name. And on a tangent, I’ve always wondered how we ended up with ‘profit’ and ‘prophet’ as homonyms. Too good of a coincidence.)

You see, we need to help our crybaby in chief, Jamie Dimon. Just leave his business alone and they’ll be lending to small businesses and help grow the economy. Or not. And if he goes insolvent, come on, the whole workd would suffer. He needs a bailout for ‘us’, man.

We’re living in the ultimate Free Markets paradise. We have a weakened government, owned in full by the monopolies and oligarchs. Freedom to buy and control everything. Laws, crime and punishment? That’s for the little people. Honest taxation and everyone doing their part? Again, for the little people.

But we need less government and more free markets, bro! Profits don’t even matter. Our corporate overlords have complete freedom to rig any market they choose.

Wilbur, I used to think along the same lines as you, and still do for the most part. All except the ‘govt’ bit. You seem to think that it would help our cause if only it were bigger. I say that’s a pipe dream. See, it doesn’t matter one bit what size it is, its totally corrupted top to bottom. Nothing good or decent can, or will ever again, come of it. Democrats or republicans are two sides of the same coin. All vetted and funded by people unaccountable to any citizens. There’s never any real difference in policy no matter which ‘wins’. Only thing is that they always do the winning, while we, the ‘little’ people, do the losing. This last election cycle should have convinced everyone of the futility in voting.

It’s very difficult to find companies that have revenue AND earnings increases. Most of them have lower revenues and higher earnings per share – buybacks have something to do with this.

Ad then there are the talking heads on all the news channels talking of rainbows and unicorns.

How about a theory that stock prices follow the real inflation (invisible to central banks, of course) in property prices, and don’t give a hoot about earnings.

I like the theory that says people buy stocks in an uptrend, and sell stocks in a downtrend. Look at the chart for the last 20 years. It shows big uptrends followed by big downtrends. Clearly, that’s the way fund managers think. They never question a trend because of valuation. Individual investors are the same way.

If you ask most people whether the next coin toss will show “heads” or “tails”, they’ll refer to the results of the past few tosses. Even some smart people think that way subconsciously.

Sounds about right.

What about FAANGs, adjusted va GAAP?

Under pressure, most of the FAANGs no longer offer “adjusted earnings,” but GAAP earnings. Netflix maybe the only exception.

Forget the USA and buy Japan – those stocks that aren’t subject to the BOJ through ETF purchases.

Lot’s of good companies in Japan with real earnings and cash on the books.

Good yields too.

Basically, we are living in the Soviet Union comrades; we just don’t know it. Communist China compromised a bit, and we compromised a bit, and we met in the middle.

The only difference is that this Soviet Union is painted so vividly and colorfully that most of the population can’t recognize it and we still believe we live in a capitalistic society.

Don’t forget da propaganda apparatus that would leave the Soviet politbiro green with envy.

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks…will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered…. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.” – Thomas Jefferson in the debate over the Re-charter of the Bank Bill (1809)

Try to spot the correlation: stock bubbles and central bank bond-buying.

http://www.zerohedge.com/sites/default/files/images/user3303/imageroot/2017/09/06/20170908_put.jpg

Gershon, that’s a very apt quote for our “interesting” times. The last time I read his words, I almost swore that Thomas Jefferson must have had a time machine with him when he imagined how “The issuing power should be taken from the banks and restored to the people”. During his time, there was no feasible mechanics how that could be achieved.

Central banks will inevitably have the currency issuing powers simply because modern societies require a hierarchy of financial powers to be consolidated and coordinated from the very top… Adam Smith’s invisible hand be damned.

More than 200 years later, we now may have the first inklings of the means to supersede this necessary evil of Central Banking. It is called distributed ledgers and blockchain technology.

Most big governments and big banks are hence, understandably wary, if not outright hostile, to this crypto-currency revolution. Of course, no one would expect them to not be kicking and screaming against losing their centralized financial power base over the commons.

Big government wants centralized control to tax the sheeple, while big banks wants centralized financial power to steal from the same sheeple. Both need to leech off the commons to feed their fat pockets.

The Big Gs and Big Bs will certainly attempt to consolidate control over this crypto-currencies via onerous regulation (under the guise of “protecting” the citizenry from various fraudulent ICOs… as if they really cared for the people in the first place. lol). If they win this new financial war, be prepared for even worse times ahead for the working poor, because digital cashless transactions under the watchful eye of an all-powerful Big G or Big B means your every penny WILL be taxed or stolen eventually.

Karl Marx is wrong on the revolution being between Capitalism and Socialism. Even in a Marxist economy, financial power still have to reside with the elites in some central bank, so the end result is still the same disenfranchisement for the common folks.

All forms of centralized control by the few over the many inevitably leads to abuse, just as absolute power corrupts absolutely.

Never would Marx have imagined that mathematics and technological advancements would offer an third alternative view for social organization. We are indeed living in “interesting” times.

Whether this will be a curse or a blessing depends on who is allowed to win this new financial revolution.

My hope, similar to Thomas Jefferson’s rumination, is for distributed ledgers to stay “distributed” so that no central authority is able to influence it. There are more than a few devious ways to silently subvert the distributed ledgers (e.g via 51% attack), so we should be watchful over the techie debates going on between the different implementations of these crypto-currencies. They are not just technicalities but their ongoing hard forks and developments may actually direct the path of future societies in ways that we might come to regret if we’re not careful now.

The Founding Fathers, as well as leading British and European statesmen, correctly realized that the greed and perfidy of the banksters posed an insidious threat to Republics and sovereign populations. They also were remarkable prescient in warning future generations what would happen to them if they failed to remain vigilant against the malevolent designs of financial and political elites who wanted a free hand for the unfettered pillaging of sovereign countries and peoples. Sadly, modern populations have been so dumbed-down and reduced to docility that everything our esteemed ancestors warned us about is coming to pass…yet still the sheeple slumber on.

http://www.themoneymasters.com/the-money-masters/famous-quotations-on-banking/