PE firms win again. Stiffed creditors not amused in bankruptcy court.

Nearly every retail chain caught up in the brick & mortar meltdown is an LBO queen – acquired in a leveraged buyout by a private equity firm either during the LBO boom before the Financial Crisis or in the years of ultra-cheap money following it. During a leveraged buyout, the PE firm uses little of its own capital. Much of the money needed to buy the retailer comes from debt the retailer itself has to issue to fund the buyout, which leaves the retailer highly leveraged.

The PE firm then makes the retailer issue even more junk bonds or leveraged loans to fund a special dividend back to the PE firm. Come hell or high water, the PE firm has extracted its money.

Then the PE firm charges the retailer hefty management fees on an ongoing basis.

This form of asset stripping removes cash from the retailer and leaves it struggling under a load of debt. It works wonderfully until it doesn’t – until booming online sales started eating their lunch, sending these overleveraged retailers, one after the other, into bankruptcy court, where creditors learn what it means to end up holding the bag. But they’re not amused, as we now see. But first the numbers…

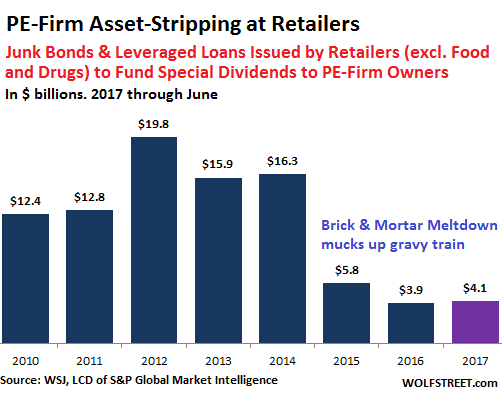

Since 2010, retail chains owned by PE firms have issued $91 billion in junk bonds and leveraged loans just to raise the money for the special dividends paid to their PE owners, according to data by LCD of S&P Global Market Intelligence, cited by the Wall Street Journal. This does not include debt piled on retailers during the LBO itself. And it does not include drug stores and food retailers – such as PE-firm-owned Safeway-Albertsons, caught up in the middle of the meltdown.

The chart shows how the asset stripping business boomed until 2015, when the brick-and-mortar meltdown set in (2017 issuance through June):

The PE firms get the cash. The retailer gets the debt. By the time the retailer goes bankrupt, the PE firms already got their money out. Creditors – usually institutional investors plowing in other people’s money – are left fighting over scraps…

Payless Inc., the shoe retailer with 22,000 employees and 4,000 stores in 30 countries, filed for Chapter 11 bankruptcy on April 4. In the filing, it said it plans to cut its debt in half, stiffing creditors for the rest. In 2012, Payless was acquired in a leveraged buyout by PE firms Golden Gate Capital and Blum Capital Partners. Less than five years from LBO to bankruptcy.

Over those five years, Payless piled on more than $700 million in new debt: This includes the debt resulting from the LBO, plus the debt to fund $350 million in special dividends to the PE firms. They also extracted management fees. In bankruptcy court, Payless revealed that in 2016, it had about $2.3 billion in revenues and $840 million in debt.

In addition, as it is shuttering hundreds of stores, its off-balance-sheet obligations – store leases – have come to the surface, and landlords are clamoring for their money. Vendors fear they’re getting shafted. And they all blame the special dividends and management fees extracted by the PE firms. The Journal:

Vendors and landlords alleged in court papers that the dividend payouts, along with other payments to the investors, left the retailer particularly vulnerable to collapse just as technology and shifting consumer behavior upended the retail industry.

“The depletion of their coffers put the company on a dangerous path that ultimately led to this instant bankruptcy filing,” a group of Payless’s unsecured creditors said in June court papers.

Lenders that are owed the majority of the debt will end up controlling the melted-down retailer. And they got a tiny consolation price for their screaming in bankruptcy court, according to The Journal:

Following heated exchanges in filings and in the courtroom, as well as private negotiations, the private-equity backers and lenders have agreed to give more than $20 million to the company, which will be used toward beefing up the creditors’ recoveries. Meanwhile, the creditors have agreed not to bring any legal claims against the backers following the bankruptcy filing.

Then there’s Gymboree Corp. The operator of 1,281 children’s clothing stores and 11,000 employs filed for Chapter 11 bankruptcy on June 11, after defaulting on an interest payment. The leveraged buyout by Bain Capital in 2010 piled $1.8 billion in debt on the company. Bain also extracted management fees over the years.

The restructuring plan calls for stiffing creditors out of about $1 billion. And some of the creditors were having a cow. The Journal (emphasis added):

Earlier this month, Gymboree’s unsecured creditors, including vendors and landlords owed an estimated $220 million, said in court papers they have been investigating potential claims against Bain and other insiders. The creditors, which are slated to receive nothing, point to dividends and fees received by Bain and its affiliates.

And denim designer and retailer True Religion with 1,900 employees filed for Chapter 11 bankruptcy on July 5. PE firm TowerBrook Capital Partners had acquired the company for $835 million in 2013. The company is now saddled with $535 million in debt (it only had $370 million in revenue in 2016). Four years from LBO to bankruptcy.

In the “prepackaged” bankruptcy, TowerBrooks worked out a deal with senior lenders, including a debt-for-equity swap that will wipe out $350 million of its debt. These lenders will get 90% of the equity in the restructured company. But junior creditors are not amused. The Journal:

[A] junior debt lender, Ares Management LP, raised concerns about the proposed restructuring plan, which will leave the creditor with a slim recovery while private-equity backer TowerBrook Capital Partners LP is slated to receive the same or higher return as Ares. Typically in bankruptcy, lenders expect to be paid before equity owners.During the first-day hearing, an attorney for Ares said the firm didn’t support the plan and an investigation may be needed to better understand TowerBrook’s role.

A lot of times, these PE firms acquire part of the bonds before bankruptcy of their portfolio company for cents on the dollar. For example, Bain Capital bought significant amounts of Gymboree bonds. This gives PE firms more control during the bankruptcy proceedings, and they win again.

Why do institutional investors fund asset-stripping associated with LBOs and special dividends? Some of the answers are in Wall Street’s culture where fee extraction is everything, and one firm helps another. And too, they’re chasing yield in a world where central banks have repressed yield. Which turns out to be a costly chase.

Retail landlords are reading the memo, but it may be too late. Read… Will Plunging Store Rents Slow the Retail Doom-and-Gloom?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Gymboree’s unsecured creditors, including vendors and landlords owed an estimated $220 million, said in court papers they have been investigating potential claims against Bain and other insiders. The creditors, which are slated to receive nothing, point to dividends and fees received by Bain and its affiliates.”

Frankly, I find it hard to understand why a court would find it difficult to conclude that all of Bain’s asset striping here is a fraudulent conveyance that is recoverable by these victims. This is a blatant criminal scheme.

Seems to me there is a great amout of overt planning and collusion in many, if not all, of these “deals”.

They are ongoing criminal acts that should be prosecuted. Right down to the people that supplied the money to these crooks via loans, “invesments,” etc. ALL of those folks should be stripped of every dime that they injected AND every cent they recieved form these crooked schemes.

Then take everything eles they have or may ever have……….. Including their freedom……..

I HATE thieves – and thieves they are.

Me too Jim Just hate thieves and it seems I’m surrounded by them

I agree, it should be a crime, but it’s not…unfortunately the management knew what they were getting into, and probably took some of the action, leaving the employees and loyal customers in their wake…I would call this unethical and downright mean.

Wouldn’t argue the point of how it looks in the rear view mirror but you’d have a tough time arguing fraudulent conveyance as Bain could and would argue that their position in the equity had a lot of “checks and balances” along the way.

– Why did the leveraged loan / high yield / institutional market loan the business so much if it didn’t make sense?

– We had no incentive (wink wink) to asset strip the business. If it performed as planned, we’d make a boatload of money!

– We had a fiduciary duty to maximize our investors return.

etc…..

I work in this industry so I have seen these examples up close.

If you have a brand name firm that institutional investors are going to follow, you get away with A LOT.

Here is the trick to a large buyout ….

1. have a brand name for good sponsor coverage

2. bid high enough on a portfolio company that the board can’t say no without violating its “fiduciary” responsibility

3. lay the risk off to the “yield starved” institutional investors that are to lazy to question the underwrite (see point #1)

4. stomp the gas pedal to the floor – if it works, great! if not…..

5. keep track of where the “bodies are buried” i.e. where to buy the debt back on the cheap when the business hits the wall (ahem cough cough Apollo)

6. restructure as a distressed for control

7. rinse repeat

(abbreviated version)

and lose money now and then because you believe in your own cooking.

cheap money is the pepper that makes the pot hot.

It’s not difficult at all. Bain will know the law, which the court has no choice but to apply. If you were a public person you could face civil liability if you stated that officers of Bain were criminals.

Your target should be the law, not those taking advantage of it.

One area to focus on: severance pay for employees coming behind

secured creditors.

Sears Canada in bankruptcy just laid off over 2000 employees, with no severance plus an instant end to their pensions and benefits. Some had worked for Sears for thirty years.

Wolf Richter predicted the date of the filing almost to the day. It was just after the last day that the court’s ‘look back’ period for suspect conveyances would have found some. But the owner waited out the period so they weren’t fraudulent.

And even if he hadn’t it most likely would not have been much help to unsecured creditors.

There isn’t much point in trying to get other unsecured creditors (suppliers etc.) into the first line- up. Mortgages and first liens will always come ahead of them.

But getting severance, holiday pay and at least wages owed, higher on the ladder, might be politically possible. You would be making them, in effect, secured creditors, so a change in law is needed.

I’m with NY Geezer on this one, fraudulent conveyance.

There should be some burden on the defendents to show a reasonable business plan for how they were going to grow the business. The fees they took out should have a direct relationship with some brilliant new direction that the company hadn’t considered or taken previously. If there isn’t some massive initiative that got implemented, guilty.

As for the institutional investors, we have two issues:

1) The public must be made aware that not a one of these imbeciles can outperform the s&p 500. Unless a fund has shown it can do better, these pensions should be forced into Vanguard or Schwab S&P 500 funds. Hell, just make a state version. It’s simple, daily math. There should be a public option for retirement s&p index.

2) Corporations are public constructions, not private. They were originally created to protect financiers of major public works projects from being hurt personally if things go wrong. They weren’t intended to shield unethical trash from any and all liabilities.

There should be a law wherein any llc or corp that gets manipulated into hurting anyone’s retirements, all major equity holders are liable, economic entity separation or not. And the landlords get protected too.

But again, the key distinction to be made is whether the major equity holders really had a viable plan to grow the company or not. No one invests to lose money. If the pe’s can’t prove how they were going to make money with Gymboree in a new and reasonable way, guilty. Fraudulent conveyance.

And if found guilty, their own corporate protections should fall and their principals can never incorporate an entity again.

Bain gets a free ride because one of its principals ran for president. Remember Mitt Romney

Running for president is the ultimate BS crony criminal mulligan for anyone who has dark secrets in the closet.

Like Hillary

What do you expect? It’s after all called PRIVATE equity. PE is just short form for Pure Extraction.

Balzac: “Behind every great fortune, there’s a crime”. Muricans really have a hard time understanding that. Today PE, next one is Buffet.

Wasn’t that Voltaire?

Buffet is still a huge idol. There’s a long long way to go before the mainstream reaches realization.

It’s like the Lance Armstrong myth but thousands of times more potent. Many many years ago, before the scam was finally brought to light, a friend of mine who was an avid cyclist was dead convinced Lance was cheating all those years. Nobody believed him, including me. How could that be possible? Cheating for so many years, under the very nose of that huge global cycling machine, with all the testing, the federation, the sponsors, media, etc.?! Little did I know that the whole machine was in on it. That’s how it was possible. The popularity and profit for the sport were shooting to the stratosphere due to the Lance Armstrong phenomenon. Rising tide lifts all boats. Everyone in the circle turned a blind eye, if not actively participating in the scam.

Buffet plays a similar role.

Wolf, as an avid consumer of financial media, I find your analyses head and shoulders above the rest when it comes to clarity, depth and nuance. Kudos.

Agree 100%. I don’t post much, but do read WS almost daily. It is one of the five sites I follow regularly.

Regards,

Cooter

Just a reminder, in the 80’s the LBO craze began when the parasites realized they could raid the well funded pension funds of major companies. They used the pension money of the target company as collateral to buy it and then paid off the employees with small cash payouts and annuity contracts. Labor has now been totally looted.

The practice of stealing worker’s labor and deliberately killing off businesses should be considered a crime against humanity.

“Lock Them Up.”

Once again, your insights are priceless.

I totally agree with Petunia, this should be illegal because it is a crime against humanity. Anyone who wants my vote or support needs to campaign against this kind of crime.

The jerk Mitt Romney comes to mind. And he thought he was going to be POTUS? LMFAO

Why is it that scum rises to the top and isn’t disposed of?

See the bond issuance, bank loans, fees, executive comp etc. that POTUS extracted from various casinos especially the Taj, that contributed to its debt and bankruptcies (plural)

POTUS has said he is an expert in bankruptcy law and here there is no reason to doubt his word.

BTW: Romney didn’t rise to the top.

I would say his lawyers are experts, POTUS has simply been surrounded by the right people to play the right game his entire life thanks to dear old dad.

At this point the general process he has to show up for is probably second nature to him while he can just let others handle the details.

If he was really an expert at anything beyond self publicity, he would have managed the same without getting blacklisted by so many lenders.

When even the Mob won’t lend to you and you have to go to the lenders of last resort, Russian oligarchs, you’re probably a sh!tbird.

Romney is right up there with the Clintoons in my book for the dirtbag of the year award no doubt

I blame the creditors that bought the debt without any safeguards in place. Nobody put a gun to their head.

PE firms are bloodsuckers with no loyalty to the business. Everybody knows that, so it’s pathetic to hear the creditors screaming like stuck pigs at this time.

Totally agree.

Why investors would do this can be baffling – until you look at the hype on Wall Street.

These people who work at institutional investors have a job to do. This job is to buy assets. And so they run with the herd because that’s safe. They buy what the hype organs say they should buy. If everyone goes over the cliff, and you’re one of them, it’s OK, because you’ve done your job, but the market turned on you. No one gets punished for getting caught in a market downturn.

These people just want to earn their bonus. Pretty soon, they’ll move to another company and don’t care anymore about their prior decisions.

You can’t work on Wall Street if you don’t buy the Wall Street hype. You’d have to work for a hedge fund that bets against the hype – and that’s normally a very painful experience – until suddenly, you’re right.

A little bit of LBO history:

When a young and ambitious Mitt Romney first went to Bill Bain with the idea of stripping companies and leaving the dry husks blowing in the wind, Bain reputedly said “brilliant idea—I’m in as long as you don’t fund it through our existing customer base.” After getting nowhere, Mitt came up with a plan to pitch the idea to a group of Salvadorian oligarchs who were the conduit for CIA money used to fund death squads in the Central American wars. They became the principal founding investors of Bain Capital, and the rest is history.

And who says Mitt didn’t have all the proper qualifications to become President?

Where did you read this stuff? I am interested to read more about how balls deep all our potential leaders are in this shit.

Many of the investors Romney worked with were living in Miami. Harry Strachan, a Bain Capital partner helped Romney make this connection in 1984. Among the investors: Miguel A. Duenas, the De Sola family, Ricardo Poma and former head of Monsanto Jack Hanley put in $1 million.

Hanley remarked to the LA Times, “It seemed like a hell of a smart thing for me to do to ride their coattails. I got rich.”

http://articles.latimes.com/2012/jul/19/nation/la-na-bain-creation-20120719

http://www.huffingtonpost.com/2012/08/08/mitt-romney-death-squads-bain_n_1710133.html

Speaking of Bain Capital, ZeroHedge just ran an article that claims Obama’s pick for the 2020 Democratic Presidential nominee should be Massachusetts Governor Deval Patrick, who currently works at Bain.

http://www.zerohedge.com/print/600902

What compensation were the executives of the looted companies getting on the way down?

I do not feel sorry for a single investor who was taken in by a PE scam. They should be intelligent and experienced enough to know that any PE deal today is crooked and to avoid them like the plague.

There is definitely a sucker born every minute. The question is how did so many of them wind up managing other people’s money?

I don’t care how much money investors lose. They are knowingly taking a risk. The problem is how the employees who were not knowingly taking risks are ripped off. When they steal the pension of a person who spent 20+ years working for that pension, that is a crime against the entire society.

Pension funds are very tempting.

A large pot of money just sitting

there waiting to be liberated. Of course

if you can substitute IOU’s that disappear

during BK, so much the better.

I am watching Academy Sports. A KKR roll up, high octane growth. And now lay off at Corp have begun…

Petunia,

I generally agree. However, when it comes to massive pension funds… I just don’t understand why they’re not simply put into s&p 500 funds and relatively safe bond funds.

How on earth is anyone’s retirement being put into corporate junk bonds? Wtf?

Wilbur they use obscure investment vehicles because they have to demonstrate their expertise. If they put the money into index funds the pension fund trustees might begin to question the fees the advisors and managers were receiving. Why pay for expertise that isn’t needed ? So, a lot of financial advisors could find themselves at the Unemployment Office. Simple really.

In biblical Sodom, there was only one crime that carried a death penalty. No one today knows exactly what it was. All we do know is that it was called “consulting”

It’s because of zero interest rates courtesy of the fed, and the pension funds having to state their investment goal at 7.5%. If they stated their investment goal at 2% which is more reasonable, the pensions would have to be funded something like 3x the level they are now.

Blame the fed, the root of all evil in our economy.

Wilbur,

Many public (and private) pension boards are stacked with people who have NO investment experience or expertise.

For example, the MBTA (Massachusetts’ public transportation authority) pension fund is in dire straits. Really badly underfunded, really terrible performance, really poor governance.

Many on the board– which manages over a billion dollars, mind you– were bus drivers, subway engineers, etc.

I’ve got nothing against bus drivers, but managing institutional assets should be left to professionals, with clear oversight and strong governance.

“I just don’t understand why they’re not simply put into s&p 500 funds and relatively safe bond funds”

When you’re of the size these guys are, it makes total sense to use active management, at least to some degree. What they shouldn’t be doing– and what many pension funds are– is investing in closet index funds and paying high fees for the privilege. Then they’re investing in hedge funds, and paying exorbitant fees for what has been very lackluster returns the past few years; again, at their size it makes sense to devote some level of assets to alternatives, but at their size it makes no sense to pay 2% management fees and a 20% cut of performance on top. They have the size to negotiate!

It’s not hard. It goes back to corporate governance. It is the single biggest issue with US pension funds, both public and private. The Fed boogeyman excuse doesn’t work either, since Canadian pension funds are much better off than US, and they’re dealing with the same markets, but are just oodles and noodles ahead of US pensions in terms of governance (not that they’re perfect, but much better).

With a lot of those guys you mentioned the union and board Memberships are subordinate to the MOB memberships.

Never forget that factor with anything in America that involves any form of union, even slightly.

Agreed. Lender beware. I wouldn’t lend my cousin $20 but he has run up 20k credit card debt and has a bad heart condition.

I don’t feel bad for the 0.1 percenters and public pension funds taken either.

One bubble exploded, what bubble is next?

That’s what we need, an app that lets you create your own bubble. :) And with all the suckers around it might actually work.

If the landlords are getting shafted they only have themselves to blame.

Why didn’t they evict companies bought in LBOs at the time (or asap)?

Because they were bound by the lease.

Our business schools have failed us since the late seventies…churning out little Gordon Gekkos at a furious pace.

Hey Wolf, you have it all wrong. It’s not that the economy is falling into a recession, that ‘Merkans are tapped out and drowning in debt, and that these companies were raped by pe. That’s simply ridiculous.

The real reason brick-and mortar retail is in trouble is because of AMAZON. That 3% market share they’ve grabbed from b&m has destroyed the whole market. /sarc

Do you truly believe online shopping isn’t more like 30 percent because I think it is Everyone I know uses online shopping a lot I’m in Warsaw Poland and the number of empty retail stores in the center is staggering Even the new H&M clothing store in a top location which opened three years ago is closed

We buy from Amazon, but it is a surprisingly small amount, maybe less than 5% of our total in the last 5 years. We really only buy hard to get items, everything else we buy local.

The reality is that between Amazon and Ebay where everything is available and out in the B&M world, you have to spend endless hours and most often can’t find what you want, I totally understand why B&M is having such a hard time.. There isn’t any real difference in cost for most items.

The difference is between the costs of shipping. Big Retail has bulk shippers and that costs a lot less than individual items personalized packaging and shipped. B&M also has the overhead of the real estate which I think is its worst problem.

It is to bad that the PE vampire squids are destroying the B&M along with the stupid management who for the most part doesn’t understand their customers or think they can take away their competitor’s customers by over building and then not being able to actually compete because the cost of overbuilding has squeezed their profit structures.

When I was growing up there were big stores with lots and lots of varied inventory. My local hardware stores were amazing. Lots of small US manufactures of all kinds of items. Now even the big stores have limited choices. Usually only one brand. And tools have just gotten to be throw aways. I still have tools that I had 40 years ago that work good and are repairable, if I can find the parts. Today’s plastic wonders are not repairable at all.. Just throw them in the land fills.. Such a waste of our non renewable resources.

So for a handyman like myself who wants to fix everything, I end up on line.. Most of the time I drive to my local stores and then go home and find what I need on line. Amazon has gotten better with diversity but Ebay is where the best deals and most variety is located. And with PayPal it is safe and convenient to purchase from some totally unknown vendor.

Yet the local stores are a part of the community of men and women and as we move further away from this community people become less and less friendly and even less logical. Losing our local retail is going to be more devastating to our civilization than just losing a few jobs.

Americans first did this to Europe and England post WW II where they perfected the methodology. Made a lot of money, and created much unemployment, that has never gone away.

They then had much American law rewritten to make these activities perfectly legal, in the land of legalized fraud, AKA America.

Now Americans are learning what it is like to have vampires come and rip the heart out of their, industrial and retail sector’s.

What goes around, deservedly come’s around.

One of the first big scams, the South Sea Bubble, was based in England and precedes the existence of the US economy.

US corporate law including bankruptcy law is largely English law.

In his book The Great Crash, John Galbraith wonders what set off the sudden loss in confidence and mentions the UK collapse of the Clarence Hatry empire, which involved ( as did the MUCH larger crash of Ivar Kreuger) counterfeit bonds serving as collateral.

There have been and are currently huge pension fund rips offs in the UK.

Can’t blame the US for everything, just a lot of things.

“Can’t blame the US for everything, just a lot of things.”

Reaching back to the South sea bubble is stretching the issue.

Reaching out of the 20th century or pre WW II in this modern asset stripping case is also really not relevant.

There will always be fraudsters, so some fund failures, as long as there are private fund’s. Most English fund failures end with prosecutions.

The south sea bubble cause changes in English law. As do most Major financial failures where a legal flaw can be shown.

Unlike the US where failures are used to model law to make more failures safer for the corporates that organise them.

What the Americans did in Europe post WW II when America boomed and they internationalized was. Organised cynical ASSET STRIPPING pure and simple.

Many of the familys damaged by that US asset stripping hav estill not recovered from it 2 generations later.

English Financial law is not always the best, but it is way better that what exist in the US, the land of legalized Corporate fraud. Where members of the house and congress, are immune from prosecution for insider trading. Which is. Self explanatory.

Methinks the lenders maybe need to tighten up on their standards a little bit? Maybe buying bond issues from PE firms that turn around and funnel that money to shareholders rather than investing in productive assets within the company is not a good idea. Pretty much proves that the owners don’t consider the company to be a going concern, merely a dishrag from which to wring every last drop of water, so why should lenders base their decisions on different assumptions? Relying on bankruptcy proceedings to give them a fair shake seems like a really rotten strategy for bond buyers to pursue. I get that everyone is desperate for yield, but what good is that yield if you never get the principle back?

In short, there are two culprits here. Predatory PE firms who are sucking the lifeblood out of otherwise viable businesses, and lenders who are only too ready to aid and abet such lecherous activities. PE firms could never get away with loading debt onto their hapless victims if the lenders refused to play ball.

Very good point about the lenders.. So who are the lenders?

The lenders are the ones who buy the bonds used to finance these ridiculous wealth transfers. Institutional bond buyers of all sorts I assume – municipal pension plans, insurance companies, bond mutual funds, balanced mutual funds, etc.

They don’t entirely have a choice I guess. Insurance companies have to hold bonds by law. A bond or balanced mutual fund needs bonds in its portfolio, obviously. Pension funds need bonds for income stability, however paltry the returns. When central banks the world over have supressed yields to near zero, this is the result. Desperate yield seekers end up taking on way more risk than they ever intended.

Still, that doesn’t entirely excuse the bond buyers from doing their due diligence, and avoiding PE debt issues if the issuing firms are demonstrating obviously parasitic behaviour. If you asked me to buy bonds to finance your company because you were investing in productive assets and therefore could produce a given yield, I might consider it. If you ask me to buy bonds to finance your company and your company is nothing more than a flow-through entity that you use to funnel the borrowed funds to yourself and your buddies via “special dividends”, so that I, as a creditor, will have no claim on it when your company defaults, I would walk away. Yet these bloodsucking PE firms still find willing buyers for their debt. I don’t get it.

“A lot of the time, PE firms acquire the debt for cents on the dollar… more control during bankruptcy… they win again”

I must have missed where they won the first time… when they went bankrupt, or when they had to put more money into the deal? This is some real sloppy writing…

Q: who do they buy that debt from for cents on the dollar?

A: banks. Banks who have no obligation to sell their paper for those prices, but are perfectly willing to do so.

In everyday terms, this is like buying expired yogurt at a supermarket for 75% off. The supermarket (bank) is not in the business of selling expired yogurt, and you’re (pe firm) willing to risk eating old yogurt, knowing very well that you might get sick.

From the buyout firm’s perspective, its not easy throwing good money in (to buy loans) after bad money (the money that originally went into a company that’s almost bankrupt or in bankruptcy). And more often than not, they only do it because they want to salvage as much of their investors’ original investment as possible. The PE firm employees rarely make big bucks off these manoeuvres.

I feel like the author knows all of this, but still felt ok with writing some of this trash. Very unprofessional.

>>>”I must have missed where they won the first time… ”

You sure did. I mean, totally. Blew right over your head. The cash extraction – “asset stripping,” as the article called it, while they owned the place: the special dividend and fees. That’s what the article was all about. So read the article, and then apologize, no? :-)

I can’t offer any sympathy for these institutional investors that are left holding the bag in the debt of these businesses. They are good at seeing bad deals from a mile away, and jumping head-first into them. And until they get more assertive in their investment decisions, they’ll keep making the same mistakes.

Several suggestions I offer:

1. Insist that your investment is in the buy-out firms doing these deals, not the dregs of assets in the acquired firm;

2. If the above idea doesn’t work, insist on stronger debt covenants be written that restrict any special dividends be disallowed until the debt is reduced much further;

3. Write claw-back provisions into the debt covenants;

4. Don’t do stupid deals.

I offer these suggestions at no charge, because I know that these foolish lenders won’t listen to me. Instead, they’ll keep throwing away their money on bad deals.

“Don’t get taken every time,” is the best advice I can offer.

But they will.

– Don’t forget the shareholders who were bought out by the PE firms. They made a tonne of money as well. They were Lucky to be able to sell their shares/stakes in these companies.