Why? Wall Street sells “more financial products and generates more profits when investors are bullish.”

“Covenant-lite” loans – risky instruments issued by junk-rated borrowers, with few protections for creditors – set an all-time record at the end of the second quarter.

They’re part of the risky universe of “leveraged loans,” and they’re secured by some collateral, but they don’t come with the protections and restrictive maintenance requirements in their covenants that traditional leveraged loans offer creditors.

Even leveraged loans with more restrictive covenants are so risky that banks just arrange them and then try to off-load them to institutional investors, such as pension funds or loan funds. Or they slice and dice them and package them into Collateralized Loan Obligations (CLOs) and sell them to institutional investors. Leveraged loans trade like securities. But the SEC, which regulates securities, considers them loans and doesn’t regulate them. No one regulates them.

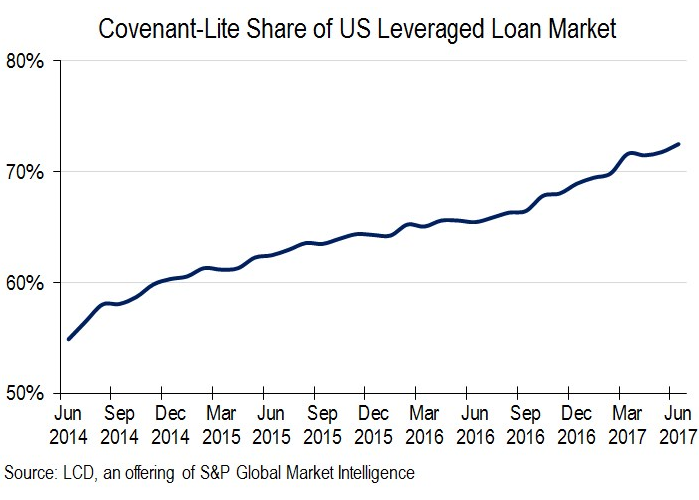

The amounts are not trivial. Total outstanding leveraged loans in the US reached nearly $1 trillion ($943 billion) at the end of the second quarter, according to S&P Capital IQ LCD. And covenant lite loans made up 72.5% of them, the highest proportion ever.

That’s up from 69% at the end of the fourth quarter. This chart shows the surge in the proportion of covenant-lite loans to total leveraged loans over the past three years, from about 55% at the end of Q2 in 2014 to 72.5% at the end of Q2 2017:

So what’s the big deal? When there is no default, there is no difference. And since there is apparently no longer any risk of default, it’s, well, no big deal. That’s what investors are thinking.

But when defaults do occur – as they have a nasty tendency to do – or before they even occur, investors have less recourse and fewer protections, and losses can be much higher.

The Fed and the OCC have been jawboning banks into backing off with leveraged loans for three years. Banks can get stuck with leveraged loans. They did during the Financial Crisis, which helped sink the banks. That’s when investors found out that leveraged loans are not exactly, as they say, as good as gold. But back then, the proportion of covenant lite loans was much smaller. So next time, the ride will be wilder.

Why do investors do this? They’re chasing yield, little else matters, and companies take advantage of that. LCD about the covenant lite loans:

For obvious reasons, they are more attractive to issuers, and have gained steady acceptance from loan arrangers [banks] and investors, particularly since 2012, when the US leveraged loan market found a higher gear after the financial crisis of 2007-08.

Then again, as naysayers are fond of pointing out, they’ve never comprised this much of the market before, so they will be under scrutiny once the current credit cycle turns.

This refusal to acknowledge the existence of risk has become a pandemic. This of course has been the explicit strategy of the Fed since the Financial Crisis – to push investors out ever farther toward the thin end of the risk branch, while getting paid less and less compensation for the risk of falling off.

Junk-bond guru Marty Fridson, chief investment officer at Lehmann Livian Fridson Advisors, is scratching his head about this in an analysis reported by Barron’s. He found that economists’ consensus sees a 15% probability of a recession, and he notes that economists have an optimistic bias and underestimate recession risks.

Recessions are important for the junk bond market. That’s when big losses occur as these over-leveraged companies get in trouble.

But the junk bond market, according to Fridson’s calculations, sees the odds of a recession as only 7% — barely above nothing. And so investors in these high-risk instruments are not being adequately compensated for the actual risks of a recession, he says.

How can this happen? Fridson in his report (emphasis added):

Considering, however, that many [forecasters] work for financial institutions that sell more financial products and generate more profits when investors are bullish, I think any bias is more likely to be on the optimistic side.

In any event, I would find the high-yield market more attractive if its implied recession probability were more pessimistic than the economists, rather than more optimistic. On balance, the analysis presented herein suggests that high-yield bonds are overpriced at present.

In other words, investors are delusional about the risks. And they’re delusional about it because Wall Street firms sell more financial products and generate “more profits when investors are bullish,” and in the end that’s what matters to Wall Street. And to heck with the retirement portfolios that are loaded with bond funds that will take the hit when the next recession hits.

An early red flag goes up for California. But the Bay Area is on the forefront. Read… These Job Trends in Silicon Valley, San Francisco Bay Area Will Hit Real Estate, the Economy, Municipal Budgets & Hype

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I keep getting offers to borrow up to $35K at ~30%. My credit is not great and they know that when they extend the offer. This should tell you everything you need to know.

30% APR makes up for a lot of sins (and commits some new ones).

You’re smart enough pass until your credit improves.

I’m having a hard time deciding whether the ‘ Institutional Investors ‘ making these ludicrous claims are ;

1) Deluded by ; a) An excess of unsubstantiated optimism …b) Their belief in technology and overly complex mostly irrelevant advanced mathematical formulas …c) A whole lotta Silicon Valley’s current substance of choice [ Dr Tim’s Kickapoo Joy Juice ] … or d) Some toxic concoction of a , b & c

or ;

2) They are the very epitome of propagandists attempting to quell the inevitable just long enough to get out with theirs

Hmmm … much as I’d like to believe its some variation / combination of number one .. methinks out of pure cynicism and blatant pessimism I’m gonna have to go with .. number two

Never rule out pompous stupidity when every other explanation fails.

Central bandits have made some dudes fabulously (real estate) wealthy, that does not mean they posses a brain.

MM .. blame the Congress and the Senate [ both sides of the aisle ] for the plethora of wretchedly excessive tax breaks , luridly liberal bankruptcy policies as well as a general lack of oversight benefiting the grifters /conmen otherwise known as Real Estate investors and developers

They don’t care it’s not their money. Most insurance and pension funds have to be invested, they don’t have a choice. The rating agencies are still rating crap at the highest ratings because otherwise they would be out of business. The borrowers having been through financial hell already, have lost their fear, and don’t care anymore. And the debt ceiling will go up because that is what it does.

All is not lost. FASB could always come up with a new way to deflect rising liabilities from unfunded pensions. When I studied accounting, if your actual liability was significantly greater than your estimated liability (uses imaginary numbers), you could defer the loss over a very long time. The problem vanishes if you get a little more creative.

This, of course, is only a last resort. Non-GAAP is coming to the rescue. Nobody cares about GAAP if you’re an investor in a public company any longer. Investors are cattle.

We are all closest to ourselves.

Even the smart Pension manager knows that if they don’t have any returns they are out of a job, so short term most important.

The upside if you are right and avoid HY and under perform for say two years? Probably sacked and even if you keep your job then whats the reward when the shit hits the fan and your loses are smaller than your competitors. When the disaster hits the pension that anyway are underfunded will have to come up with a new strategy and if your unlucky it doesn’t include you.

While I am sympathetic to pension managers, who apparently feel compelled to chase some returns no matter how risky, I must point out that they are fiduciaries for their pension funds. Pensions have been getting scalped too frequently: e.g., when the banksters sold them real estate mortgages they securitized, which were not supposed to fail, while the banksters bet that they would fail. See http://www.nytimes.com/2009/12/24/business/24trading.html?pagewanted=all. See also http://www.mcclatchydc.com/news/politics-government/article24561376.html

I fear that these pension managers, who control the enormous life savings of millions, are just trying to get some yield, get their salaries and bonuses and expect to be far away years later when their pensions implode. The laws should be made stricter so that both those that defraud pensions, and the knowingly-gullible pension managers, serve decades in prison for their culpable or at least, negligent conduct.

As things stand, this Fed bankster-created, fantasy, bull market cannot continue forever. Even the bankster cartel, the “Federal” Reserve, is aware of this.

Prices are no longer supported by earnings or reasonably anticipated earnings, particularly since so many companies are keeping prices high by stock re-purchases that they finance by borrowing. Those loans will reduce future net earnings available for dividends or growth.

Even stock buybacks that are not financed by loans are still decreasing the future growth of companies, which investors apparently expect given the inflated PE rations. See http://www.marketwatch.com/story/apple-cisco-and-ibm-prove-that-stock-buybacks-are-a-sham-2016-01-29

Ultimately, pensions will suffer financial meltdowns: the net worth of their assets, reduced by their losses and the reduction on the value of assets that they purchased at inflated valuations, will not be enough to meet even a fraction of their commitments. Thus, while the pension managers and banksters that defraud pensions will have had a merry time with the money, the victims, the pensioners, will be left with tiny pensions.

Like in Russia, pensioners will have to eat out of the trash or find any kind of work, if they still can work.

https://www.bloomberg.com/graphics/2017-corporate-pensions/

The top 200 S&P 500 companies have pension shortfalls totaling $382 billion. GE spent more on share buybacks ($45b) than the size of their entire pension shortfall ($31b) which ranks as the largest in the S&P 500.

A while ago, my bank’s “financial advisor” called me and try to talk me into changing my investments to more aggressive, i.e. equity based. I objected: “But, but… a crash”.

He said, what do you worry about it? When it happens all will be gone,… puff.

Thank you “financial advisors”. If you were around when the universe was created, there wouldn’t be a universe at all.

Some of those ‘ Institutional Investors ‘ may have a computer program that they THINK can get them out before their ‘investments‘ break.

‘

Fat chance.

I guess Fannie Mae’s move to let students pay down their debt with a mortgage refinance could be termed a “leveraged loan”.

http://www.fanniemae.com/portal/media/financial-news/2017/student-loan-debt-6546.html

WOW! Thanks for that link Idaho. I am speechless.

And they make it sound as if they are doing these victims, I mean borrowers, a favor. The word shame doesn’t exist in the vocabulary of these people.

Wolf, you probably nailed it where the next shoe will drop. Some people might be scratching their head about it. If these loans won’t be the fuse, they will be the fire.

Wolf, did you surprise me. It seems to me that the one essential thing that needed to be done after the last financial fiasco is the establishment and enforcement of ratings standards for CLOs along with the other types of CDOs. Without standards for all types of CDOs there would appear to be a gaping hole in the risk management.

And I wonder why countries don’t issue “covenant-lite” loans? It seems countries like Argentina, Greece, Spain, etc. could then issue debt without having to worry about debtors trying to repossess the country when they default. In fact, depending on the exact “covenants”, companies that issue “covenant-lite” loans would appear to be behaving (legally and financially) just as independent countries do. The debtor has no more recourse than the company wants them to have.

It’s hard writing this while I’m doubled over laughing. A CDO is made up of the crap they couldn’t sell the in the first round of MBS or other collateral sales. If they put a realistic rating on it nobody could buy it, notice I said could not would, because they would buy it if the pension funds and insurance companies weren’t required to hold only highly rated securities.

As far as recovering assets on defaults, they know the loans are crap, but again, it’s not their money. If the borrowers had assets, they would not have put in the restrictions which free them from having to recover assets they already know the borrowers don’t have.

securitization is a “wonderful” way to remove loans from your balance sheet and place it on someone else’s balance sheet . A risk transfer system and a product of financial engineering . these cove-lite loans look like a Dodd-Frank workaround.

“As long as the music is playing, you’ve got to get up and dance”

Charles Prince Chief Executive of Citi Group

Problem is, this seems to become one of those dance marathons of the twenties.

And we all know how that ended.

I reviewed my copy of “The Big Short” over the weekend and watched an older documentary titled “The Last 72 Hours of Lehman”.

Now, today with this article its deja vu time!

No learning from past errors and transgressions, by the greed motivated Wall street criminals. Far from it. It seems their current method is, if it worked in the recent past lets do it again, only this time bigger!

The end result will be same – only this time much, much bigger.

I just watched “The Big Short” again on Netflix this weekend as well. Must be something in the air.

HBO’s been re-airing ” The Big Short ” again lately …. so yes … there really must be something in the air . We watched it ( again ) .. along with a rather intensive documentary on the 1920’s leading up to the ‘ Great Depression ‘ that used multiple newsreels and radio broadcasts in order to add context to the documentary . I said this before but I’ll say it again … 99% of those 1920’s broadcasts were Deja Vu exemplified sounding like any one of them could be todays financial news

Institutional Investors are not stupid. The game in Murica is to quickly become TBTF and get bailed out every single time.

The sad part is how they can ruin the peoples lives and futures who had nothing whatsoever to do with all their bullshit. Then they just walk away to do it all over again.

Please give it a rest and leave the politics to the political sites . Especially overtly biased conspiracy theory based politics with no basis in reality

It’s easy go gamble when it’s not your own money placing the bets. Just look at the returns on investments that public pension funds gave to the hedge funds. Many didn’t beat the S&P. No one went to jail for bringing down Lehman Brothers. Jon Corzine didn’t pay a price for his role at MF Global. There’s ZERO correlation between real risk and what’s going on in the markets. The surge is because of ZIRP by the Fed which is about 8 years too long.

Jon Corzine was the Democratic Governor of New Jersey (my birth-state) from 2006 to 2010, and a Democratic United States Senator representing New Jersey in Congress from 2001 to 2006.

Evidently, it costs $5 Million to buy your way back to Wall Street if one is connected.

https://www.nytimes.com/2017/01/05/business/dealbook/mf-global-jon-corzine-penalty-settlement.html

Free Jon Corzine!

Oh, wait….

Corzine had a serious life threatening accident. He was telling a friend he was sure he had died at one point: “I was looking down on the world”

Friend replies: ‘Jon, if you had died you wouldn’t have been looking down’.

Is wall street going to pushed off a bridge. Not really.

Are Mr, Paul plus his good misbehaving Ti friends,

be punished and witness their best buddy being pushed off a bridge. Well, it’s only a bungee jump. Don’t worry, it’s for fun, a new type of game.

I just have to start making plans to hide, when this $H|T hits the proverbial fan, I don’t want to be near some of these people. Even if I told them whats coming and they should be selling, not buying.

The problem there is, I tried the survivalist/prepper rural area thing and …. there’s a reason I’m back in the city.

Fed says it will start to unwind its $4.5 trillion balance sheet “reasonably soon” or after Jesus returns, whichever comes second.

http://www.businessinsider.com/fed-statement-balance-sheet-interest-rates-july-meeting-2017-7

I’m an eternal optimist. I think they will sell some off.

Actually, given the corruption of the ECB, incompetence of the BOJ, and continuing needs of China to print for stability, eventually, the USA will look like a breath of fresh air and the place to put your money. This won’t happen for a few years and only if the globalists are kept in the corners and considered nothing but fringers.

The Fed allowing rates to rise while selling off the balance sheet will make the US shine in less than a decade. If only they are allowed/ forced to continue. Where to put your money.

Europe, by contrast, will look like a financial wasteland … Greece x 100 … by then. The choice – rates normalized in the Eurozone or the ECB coming up with new excuses to print even more and buy even more debt. Hell either way.

The problem for the ECB is they will run out of debt to buy. Even 60 billion a month is 720 billion per year and Germany, the biggest economy in the Eurozone doesn’t run big deficits. I’m sure the PIGS, if the ECB threw its capital key out the window ( like it does with its other rules) would issue all the debt Draghi would want but his term expires in Oct. 2019 and then… its Germany’s turn to head the ECB.

The ‘euro’ will be a busted flush at that point!

Investment advisors and financial consultants all get paid by getting you invested and keeping you invested. They are paid commissions on selling you financial products and are paid management fees for whatever it is they do after they sell you.

Their income drops if you cash out some or all of your funds. Thus, they have a plethora of reasons why you should never sell anything no matter what the market level is or your profits are.

In contrast, the Fed wants the wealth effect to make you feel richer and encourage you to spend from the wealth gifted to you by rising asset prices. Their entire QE and balance sheet expansion was based on the wealth effect expanding the economy.

Anyone see the problem here?

Not just the Investment advisors, brokerage firms and financial consultants cdr . Now the banks have taken it upon themselves to try and sell you a load of investment crap .. sometimes with ‘ guarantees ‘ that when the fine print is read guarantee nothing what so ever .

Once our bank started with that tactic we told them point blank either cease and desist or we’ll take our sizable accounts [ our liquid assets ] elsewhere . Amazing how effective such a threat can be in light of the amounts in question

I probably wan’t clear above.

THE REAL REASON QE AND THE WEALTH EFFECT DOES NOT WORK

On one hand, the Fed prints tons of money and lowers interest rates to create and maximize the wealth effect. Their thinking is that people will spend money if they feel wealthy. The wealth effect = Some of the money they printed that wound up in higher asset price valuations will be cashed out and spend, expanding the economy. Thus printed money expands the economy after passing through the stock market, according to Fed genius.

The reality – financial advisors detest people cashing out for any reason. Their income is based on commissions and asset management fees. They have a bazillion reasons why you should put money in and never take it out – even thinking of taking any $$ out of assets under management is harmful to your health.

Thus, the conundrum. This is why QE never works for Main Street but is worshiped by Wall Street. Cash checks into brokerage accounts and never checks out, except under great protest by the asset managers.

OR – to put it differently

For any Fed stimulus to work, it must bypass the middlemen.

Since a high percentage of brokerage accounts are managed by asset managers and since the entire financial media almost universally encourages you to let your profits ride and never sell in a crisis – churning is OK, though providing supervised by an expert who should be managing your money for you – buy and hold something – never cash out – is now and has always been and will always be the way of Wall Street.

To get cash to the masses, allow interest rates to rise so that savings accounts, CDs, and bonds generate an income people can live on. This will put actual cash in people’s pockets and it will be spent as it is earned.

Of course, Wall Street hates this advice for obvious reasons. Low rates create artificial value, which raises the value of assets under management, which increases their paychecks without having to do anything except convince account holders to never sell anything.

High rates require asset prices to rise for a good purpose, such as a good company doing well with good management and good ideas. Paper flipping for profit is far more difficult with higher rates than it is with lower rates.

High rates also make it easy for Joe and Jane MainStreet to put some savings in a CD and watch it grow measurably. No asset managers in the middle required. Just a little banking competition for deposits. Bonds and fixed income mutual funds are available for the more sophisticated MainStreeters.

This simple explanation, spread among these three replies – is the sum total reason why QE never works and will never work.

Normalized interest rates are the secret and key to a healthy economy.

“Risk has been Abolished, According to Institutional Investors ”

The subject classes are liable for all the debts of the master class, so of course, for the master class there is no risk.

I’d written my concerns on another of Wolf’s wonderful pieces about the leverage. Everything is leveraged. All big publicly traded businesses have to be or be in constant fear of being taken over and disassembled and sold off in pieces or the new controller leverages it to the hilt and takes the money and runs off.. often without paying a dime of taxes on the profits from destroying America one brick at a time.

We are run by a criminal enterprise and some people actually still think this is a democracy.

It is sure difficult trying to figure out how to stay out of their way and sights and survive what is coming.

Is a game of hot potato and everyone but the rich guys lose. Oh and the potato is a times bomb. I would say it will explode soon.

wall street BS and bank cartel sell bank products to itself. perfect scam. make the swap/cd/derv/equi/whatever – set the market – buy it – bid to infinity – bailout to infinity if it goes wrong – rich for ever without consequence. if you are the ordinary idiot on the street gets burned with inflationary bubble – well keep em happy with the melt up. it works – until – well it doesn’t any longer. then, well history repeats itself i suppose. seen this same garbage over the generations – how is it any different this time? it isn’t? just a matter of when things happen and what makes them unfold.

Any idea when all this collapse will start?

“..economists’ consensus sees a 15% probability of a recession, and he notes that economists have an optimistic bias and underestimate recession risks..”

Last week GoldMoney had a fabulous analysis of an IMF economist’s research that showed:

“..over three decades, of the 150 recessions recorded only two had been forecast, implying that since the turn of the century no recessions had been forecast at all. The failure rate has increased to 100%, not decreased, as might be expected from economic models that are updated in the light of experience.”

https://www.goldmoney.com/research/goldmoney-insights/why-economists-cannot-forecast-recessions