Investors are conditioned to believe the Fed has got their back. But they might be wrong.

By Benjamin A. Smith, Lombardi Letter:

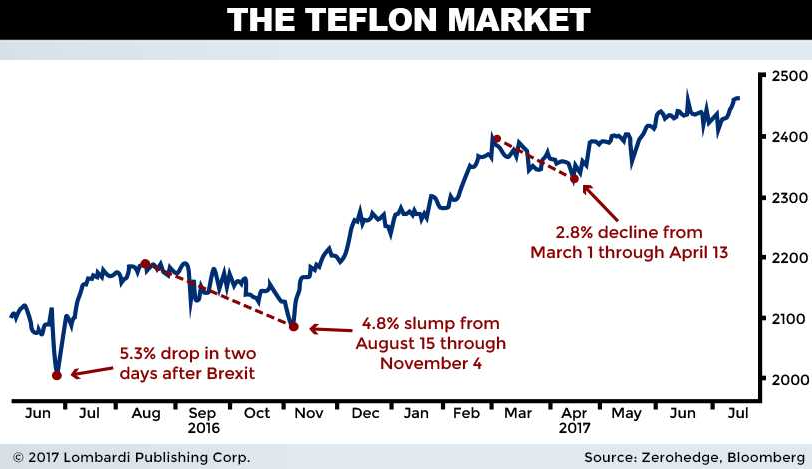

To say the stock market is on a roll is an understatement. The Big Three indexes (S&P 500, Dow Jones Industrial Average, NASDAQ) are making fresh highs, mostly because of valuation expansion. That is what investors are focused on. But what about the lack of market decline? The dynamics behind this fact could speak louder than any stock rally could.

The Wall Street Journal is reporting that major indexes haven’t gone a calendar year without a five-percent-or-more pullback in 20 years. The last time this happened was following the “Brexit” referendum, which eked out a 5.2% peak-to-trough loss. While not quite a “calendar” year, it was over a year ago that this happened. In fact, the 267-day streak with a five-percent decline is the longest going back to 1996.

Additionally, the S&P 500 has only experienced a 2.8% drawdown year-to-date. This, in contrast to a historical average of 14.4%. If it holds, it would be the second smallest drawdown in 60 years.

So what are investors to make of a market that won’t drop? From a surface perspective, the market appears incredibly strong and resilient. Although it’s tough to argue that fact, if we dig a little bit deeper, a different perspective emerges. It’s where excessive central bank liquidity (via asset purchases, swaps, interest rate policy etc.) exerts too much influence on the market. There’s a certain instability you can almost feel.

In essence, the market has become less about earnings growth and more about Central Bank liquidity. This is dangerous for two distinct reasons.

First, unless the Fed remains fiscally accommodative and active with asset purchases, the bubble will burst. In the meantime, the stock bubble keeps getting much larger and more expensive. The higher it goes, the more violent the unwind when the Fed removes the training wheels. Yes, eight-plus years into recovery, it still cannot let the economy fend for itself.

Second, there’s an assumption that the Fed actually knows what it’s doing. It’s assumed the Fed’s economic models are correct and that it’s in control. Both of these assumptions are dubious. The fact is, we’re in the midst of the greatest economic experiment ever devised. The Fed’s balance sheet has gone parabolic since the U.S. Housing crisis, which it’s attempting to unwind with unpredictable results. Interest rates were never this low for this long. The list goes on, but it’s important to understand that we’re actually living in extraordinary economic times. Things may seem “normal,” but if the Fed loses control or if a deep recession strikes, all heck can break loose.

What Does This Mean for the Stock Market?

The market melt-up on low volume should be a warning sign for investors. The lack of selling means that everyone is herded on the same side of the market, riding the tidal wave of Central Bank liquidity until it stops working. It’s reminiscent of the Tech Bubble, when everyone knew most internet stocks were bogus. But investors didn’t care, because they thought they could sell their positions before the market crashed.

The problem with that mentality is that after nine years of dip buying, the next dip could be the one that doesn’t come back. Investors are conditioned to believe the Fed has got their back. The belief is that if the market strays too far, the Fed will step in and stem the tide. But will it? That’s a very dangerous assumption being that it didn’t stop the 2001 and 2008 crashes from happening. The Fed is a critical player, but it’s not omnipotent.

Ultimately, the market sell-side is like a coiled spring. And the Fed is pulling the marionette strings in the background. People are allowing themselves to be puppeteered because it’s profitable to do so. But what the Fed giveth, the Fed can taketh away. Relying on a backstop to prevent a market crash is not an investment strategy.

This assumes it can even control the massive amounts of latent sell demand if the market really goes into reverse. Just think of all the record ETF inflows, investment fund money, and margin debt looking for a reason to sell after several years of riding the wave. When it happens, the bid could go dark. Prolonged high volatility and high volume days will tell us this is underway. By Benjamin A. Smith, Lombardi Letter

Investors who bought the hype are left holding the bag. Read… Another Former $2-Billion Startup Gets Rolled Up

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“The fact is, we’re in the midst of the greatest economic experiment ever devised.”

Even more significant, the entire planet is in the midst of the greatest economic experiment ever devised. Are there any central banks that aren’t doing what we’re doing?

If you keep in mind that the big banks in every country literally own the respective central banks, it is clear that if the ones in one country manage to pry funds virtually interest-free, as began with TARP and QE, the others almost must follow, because otherwise, what is to keep the big banks of Nation A from simply printing up money, virtually interest free, with which to scarf up the resources of nations B, C, and D? (now the basis for the much-derided gold standard becomes perfectly clear.) Anyone who regards this as “an experiment” is a masochist, IMHO.

As for the “Stunning Lack of Market Decline Highlights Surreal New Normal”, have a look at the graph of the Caracas stock exchange (IBVC) from Bloomberg:(https://www.bloomberg.com/quote/IBVC:IND). In nominal terms it has outperformed every other- it just goes up and up. And guess why.

I’m not sure your logic follows.

“what is to keep the big banks of Nation A from simply printing up money, virtually interest free, with which to scarf up the resources of nations B, C, and D?”

“Printing up money” would lead to inflation, devaluing the currency, and no net change in the ability to “scarf up the resources” of foreign nations.

“In nominal terms it has outperformed every other- it just goes up and up. And guess why.”

Hyperinflation… and according to you, Venezuela should be able to start purchasing the assets of other countries wholesale with all their new currency.

Where have you been? All this assets grab that’s been going on for years was made possible by easy money. Inflation and the effect of “devaluing of the currency” only affects those who haven’t received that easy money, which is basically all the ordinary people. In simple terms, if the Bank gives you a fresh-off-the-press $10 for a piece of your company that was worth $2 on the open market; and then you take that $10 to go buy yourself a burger (that $10 can no longer buy a burger+fries combo due to inflation), you would still have only paid $2 for that burger. On the other hand, the guy who didn’t benefit from the Bank’s generosity just saw the $10 in his pocket lose purchasing power.

Venezuela’s hyperinflation was not the direct result of them printing money.

” Are there any central banks that aren’t doing what we’re doing?”

No. It was a fad and now it’s a problem. People, being people, know exactly what the problem is. Those running the central banks are either stupid (some are) or are waiting out their terms. The plan is to leave the problem for the next person.

The ECB is a cynical money printer. The EU fails without it going full tilt until it can’t. China needs their central bank to hold the country together. Japan is just goofy … print forever then print some more. The Swiss depend on it to meet expenses. The Brits support a corrupt financial system, that is probably moving to Germany soon. The Fed supports the globalists but Trump makes them cringe because he threatens to force reality on them before FOMC members have a chance to retire and leave the problem to someone else.

Survival instincts are in control. Imagine yourself doing the job of a Central Banker. First you put your grand theories to work. When they fail you do what you boss tells you to do. Then, when you realize everything you did was not only wrong but harmful and needs to be backed out ASAP -or – you see that the new boss knows you’re full of sh*t – you leave it to the next shift to deal with while you look busy until your term expires. Or, like Kashkari, you’re still a true believer in the globalist way.

This encapsulates modern Central Bank management.

when us fed gets behind the growth & inflation eight-ball and is forced to act (instead of normalization with gradual & quarterly interest-rate rises)… WATCH OUT… PJS

” Just think of all the record ETF inflows, investment fund money, and margin debt ”

What a scary picture. Folks lining up to by ETF’s on margin!

Has the Federal Reserve Bank unloaded all (or any) of the “Toxic MBS” they gobbled up through the TALF windows?

The Fed’s prime directive is to keep the banks, not the markets, safe, secure and a source of great wealth production. The Fed would readily sacrifice the real estate, health care and pension sectors for the survival of the banks. The bigger question is: which banks are included when it is once more time to bail them out? Last time Lehman Bros. CEO Stanley Fuld was shocked that his bank was excluded.

Lehman Bros. was not a bank. But then neither was Goldman Sachs or AIG. The member banks of the Fed are all commercial banks. GS made itself a bank in order to qualify for direct access to the fed window(fed money).

Investment svc companies are usually “investment banks”, regulated by the SEC, mostly. Commercial banks are regulated by the FDIC, Federal Reserve, etc. They are different types of banks.

During the financial crisis, no stand alone investment banks survived. Some restructured into bank holding companies.

In my opinion this whole episode totally negates any investment skill these people (bankers) are supposed to have. They fundamentally refused to manage their risk correctly, and were all bailed out. Note that guarantee by the taxpayers equals a bailout. The use of those funds and artificial control of interest rates costs other investors money- even if they say “we paid it all back”- they really did not.

For ml the very wealthy individuals who own a vast variety of assets I can’t imagine any fiscal crash is all that scary. Stressful perhaps if you think it puts your company at risk but very little chance of you going broke.

The sense in which they know the Fed has their back is that they will help them reinflate price after the crash.

But it seems like it is really hard to tell how much the fed is helping or hurting during a recession.

From my perspective all they have done is artificially inflate cali home prices back to bubble levels without real wage inflation but artifical interest rates. Which in my opinion is going to reck a generation of young people’s hopes that their first home could be an easy stepping stone into the trade up market.

Just had to comment on this one ;

You’d be surprised how many of those millionaire / billionaires are leveraged up to their eyeballs praying to what ever an excuse for a god they bow down before that nothing happens to upset their very vulnerable and overly exposed apple cart

In as far as todays moment of Wolf ….. a question ;

Is it really the delusional investors driving this insane verging on the ludicrous Potemkin Village market … or is it the Bots gone mad with everyone believing the virtual digital Ai’s must know something the human beings do not ?

The housing market in CA is totally disconnected from the stock market. If I remember correctly, after the dot com bust house prices in Silicon Valley went up. And I don’t remember employment dropping by large numbers even thought there were job losses.

Basically, the managerial class has been spared any downturn. I think unemployment among those with a Bachelor’s or higher degree never went above 3.4%.

The reason these clerks are being bankrolled is quite simple: without them, the supply chain collapses.

The point is that at this stage there is nothing BUT the managerial class. It’s suburbia, a big fat frog in the process of being boiled. It’s in the crosshairs–formerly a source of growth, now it simply a huge drain on money and resources. You can look at it two ways: you’re ruling from the suburbs, or you’re marooned in the suburbs (after all, the suburbs produce absolutely nothing). It’s the last store of huge wealth in the U.S. When it’s gone, you will know the banksters have simply abandoned the U.S., having squeezed it dry.

If I remember correctly, after the dot com bust house prices in Silicon Valley went up.

That’s because when the dot.com bubble burst, interest rates were lowered drastically. Same thing happened in Canada during the 2008-09 recession. Stocks crashed, unemployment rose, but… interest rates fell to nothing, and house prices – after a brief six month correction – took off again. They’ve never looked back.

There are some signs that the Canadian real estate bubble is finally exhausting itself, but I’ve mistakenly believed that before.

Many if not most corporations needed to stay very leveraged and not have liquidable (un leveraged assets) on their books because what has been increasingly happening for a few decade is there are hedge funds and private equity funds like the one Romney was involved with that would swoop in and grab the companies who’s stock price fell below the actual real value of its assets, take it over, leverage the assets and then either destroy the company, move it off shore or sell it or after dividing off the assets, sell the assets and dump the company… Just look at Sears Holding Company for an example…

So EVERY thing is leveraged… and leveraged as much as possible. That is why the increases in rents and lease fees was so harmful.. They could get cheaply made merchandise but they had to sell it for way more than was reasonable.. and thus many are closing down. Restaurants did the same business plan… borrow till it hurt and then any slight disruption or price increase (power, water, help, food, maintenance or fees would put them in a world of hurt. And under..

And those companies with special deals or privileges who have monopolized a sector or people like Buffett who have special access to not only information but influence to change the rules… all do well.

But they are greedily taking more and more.. They buy into a company, get rid of the unions and cut the quality and raise the prices to us.. Make billions but they forget or don’t care or ? that the people and families they are taking from are the end users of their products…

Everything is getting stretched while the markets may reflect the reality of the current profits for the few, it no longer reflects the future..

Doubling the national debt has put us in a precarious position. If we raise interest rates then the U.S. government uses more of the budget to service debt. As they like to point out there isn’t much discretionary spending to cut so we then look to cut military spending or entitlement. Entitlements won’t be touched because those are the costs of voter loyalty. The market is riding high simply because no one makes money by putting it in the bank. Everyone is heavily invested in the market so when the selloff comes, there will be few buyers to a 10% correction is being optimistic. Maybe the Fed can buy it all after they dump their MBS portfolio.

My parents bought AMZN and could sell for a small profit. Should they get out now and hold cash.

AMZN is currently selling at about 195x its trailing 12 month earnings or about 609x its 5 year average earnings. The triumph of hope over experience.

What we have is “Nolmacy Bias” inside of the “Twilight Zone” of the “Outer Limits” “there is nothing wrong with your TV sets do not attempt to adjust the picture ” in the meantime while we’re in a trans the dam will break with the multiple asset bubbles…Newtons 1st and 3rd laws will be in effect.

Bubblelicious!

Everyone looks at the DOW or the S&P500 and forgets to look at –

The Russell 3000 Index. (RUA) Which covers about 98% of total stocks.

Last Wednesday July 19 2017, the RUA closed with a new record high of 1466.02 Today the RUA is currently trading at 1470.75 if it holds until close, it will be a new all-time high. Whopee! What could go wrong?

It is always been up, up, and away for almost a decade. It has been a lost decade for most while the protected bankers hoard the wealth for themselves. With minor glitch on the bots doing the high frequency trading, a nose dive will always be prevented due to circuit breakers are in placed. It is a difficult dilemma for bears to short especially one knows the fundamental does not go with the prevailing trends. I shorted and I lost my shirt (x times). You know as they say that trend is your friend. It does not matter what one thinks. The market will decide for you.

“It is always been up, up,”

Until it doesn’t!

The current bull market has now run for 104 months straight. There has been only one other time in the history of the markets, where it has run longer.

That was during the 90’s bull run of 117 months (almost 10 years) that culminated in the dot com bust of 2000 – 2001, which was mainly contained in the NASDAQ. This current bull run is getting fairly long in the tooth and the correction will affect ALL markets.

Seems FED taking QE to its limit to maximize postcrash. Using chaos implementing laws to centralize power making US a “democratic” dictatorship.

This is the final step. THE PRESIDENT.

These days we’re inundated with articles about the likely-hood of a crisis or crash brought on by CB intervention, but not a peep about the factual data out due to massive money printing in Venezuela and Argentina.

While I believe we’ll see some corrections and sell-offs, I don’t see how markets can crash anytime remotely soon because of the massive amount of currency pumped into the system and the undeniable fact that CB’s are set to overwhelm the system with more ‘market monetization’ at the slightest hint of selling.

So I ask anyone to explain exactly how asset prices fall substantially when the currency they’re valued against is being created at a record pace? Especially against an environment engineered by those same central banks to punish savers and steal purchasing power from anyone sitting in cash for long.

Venezuala Stock Market on 5/20/2017

http://ibb.co/kTXLek

Venezuala Stock Market on 7/21/2017 (2 months later)

http://ibb.co/gBMkC5

So based on the clear evidence out of Venezuela & Argentina, the correct trade looks like I should buy any big sell-offs in ‘necessity’ dividend paying pipeline, communications and utility stocks.

I believe writers are making a huge mistake in assuming the Fed and other CB’s will reverse course to prevent massive currency devaluation. While NONE of them want to see the currency devalue, ALL of them have made it abundantly clear that saving markets far outweighs inflation. They see a falling currency as ‘manageable’ via high taxes, confiscation and going cashless. What they won’t tolerate are crashing markets…cause that means the rich lose both wealth & power. And CB’s exist solely to create & preserve the wealth and power of the 1%.

The currencies of both countries (Venezuela and Argentina) have totally collapsed due to years of rampant inflation. The stock markets in both countries are denominated in their collapsed currencies. The only thing your stock market charts show is just how much those currencies have collapsed. They don’t say anything about the stocks… you can’t measure anything correctly in a collapsing currency.

I hope you’re not taking your theme seriously. I hope it was just a joke that I didn’t get.

And the S&P is priced in Dollars, so how does it fall substantially in USD terms if the Fed is massively printing?

Priced in USD the IBVC is of course down somewhat but proves that their market preserved wealth far better than staying in cash (Bolivars). And in those types of nightmare scenarios, the only form of real income will be dividends, rental property, farming and jobs. Me personally, I’ll take dividends over renting to a broke populace, trying to protect my farm from a socialist gov, or finding & holding a job who’s wages don’t remotely keep up with inflation.

Gold & silver are fantastic for short to medium term crises but the problem is you’ll always eventually run out when the economic failure drags on for decades.

Unless the US decides to “helicopter drop” money into people’s hands (and it’s unclear to what extent they could even do that), we’re closer to a hyperdeflationary event than a hyperinflationary event.

Correct. That’s why I am 60% Treasuries, 20% stocks, 20% cash. I see deflation rather than inflation.

The best way to helicopter drop money into the hands of the masses is to revise the tax code. No tax on the first $20k, same or less taxes on the middle class/middle income people, and then ramp it up on the rich. No more Google and Apple etc paying NO taxes.

I think even assholes like Nixon were in favor of what was called a “negative income tax” where if you made under the poverty line, not only did you not pay taxes (and yes, even on $7k a year I’ve had to pay tax) the gov’t would GIVE you money. Get money into the hands of the proletariat and the whole economy benefits.

We have something like that in Oz, but only for people with children………it is called Family Tax Benefit.

No kids – no benefit.

The worst situation in Oz is to have one working person in a marriage on low income, one at retirement age, and no kids.

And if you have a little bit put away, they get you on that too.

You get the shaft every which way.

Don’t we have enough incentives not to wok already? The last thing we need is more welfare.

The refundable child tax credit is taken by many illegals. They file, claim a very small amount of income, and get a huge refund. In Florida, Xmas was at the beginning of the new year with a tax filing.

Recommended reading : Barton Biggs “Wealth War and Wisdom” published in 2008. He includes real investment returns for various countries from 1900-2000, 1900-49 and from 1940-49. Bonds usually underperformed stocks by wide margins in times of chaos.

I believe stock investors are thinking the following:

1) You need to be in assets when there is risk of inflation and maybe hyperinflation. The Fed will follow the path of least resistance, which leads to inflation. Who doubts the Fed will do all it can to prevent a stock market collapse, including more money printing?

2) If you borrow to invest, you are playing with other peoples’ money. It doesn’t necessarily have to be repaid in full. Plus, there’s safety in numbers. If you can’t repay your debt, neither can many others, and laws will change to accommodate your problems.

3) If the market collapses, it will prop back up within a few years (10 at most), just like EVERY time in the past. The long-term trend is undeniable.

4) If you don’t buy real estate now, you may be priced out of the market forever.

5) The trend is going up, so it’s time to be in the market. If it starts dropping, you can sell.

6) I know the market’s overpriced, but the market might 30% before it crashes, and it might only crash 10-20%.

The crash would come when everyone barring few would think it’s a new normal. Then, there would be a rush to exit accelerating the drop

So close we almost smell the deep state.

Stop digging.

The Federal Reserve since its clandestine 1913 inception has had one agenda: transferring the wealth and assets of the 99% to a rapacious oligarchy, with engineered boom-bust cycles being the most efficacious means of looting the proles. Now, as a corrupt and venal .1% in the financial sector amasses all wealth and power into its own hands, the pauperized proles are being locked out of the (illusory) “American dream.”

http://www.marketwatch.com/story/one-depressing-reason-millions-of-people-are-locked-out-of-the-american-dream-2017-07-25

There is still about, I would say, $50 trillion to loot before American homeowners (whose stored up wealth is what is being looted), have nothing–no home, no money, no job, no future, nothing. The only question is: how long will it take the banksters to loot it?

A lot of older Americans have no mortgage debt and pay off their credit card bills at the end of each month. They have very little to do with banksters. FYI, most bank employees don’t earn high salaries and the benefits are not as good as they used to be.

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks…will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered…. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.” – Thomas Jefferson in the debate over the Re-charter of the Bank Bill (1809)

Thank you Gershon. That is one quote that rings so true (and one I have posted here before-but without your timeline context, and the last sentence quoted).

Three years before the First Bank of the United States’ 20 year charter was granted by Congress in 1791, Jefferson stated, “Paper is poverty. It is only the ghost of money, and not money itself.”

The year before the Fed was approved by Congress and signed into being by President Wilson, J.P. Morgan testified before a hearing in Congress, “Gold is money. Everything else is credit.”

https://www.treasury.gov/about/history/Pages/1900-present.aspx

There’s no investments within a insolvent system. There’s only bets. How much of it is ‘managed money’? Looking for a return? Add CB qe to the mix and there’s your mad house. Assets my ass.

True. Its all gambling.

However we are in the calm before the storm. The relentless drive up will cause all remaining doubters to capitulate and buy in. That will be when the storm arrives.

Doom, gloom, the sky is falling down.

Look for stocks with a P/E of under 15, PEG under 1. Just bought Gilead recently and Seagate today. In every market there is a bargain. Buy dividend paying stocks for the long term. If the market goes up, good. If it goes down, buy some more and keep cashing those dividends. To heck with the Central Banks. They couldn’t stop market corrections in the past and they will not in the future.

If you’re as tired of all the conspiracy theories and teeth-gnashing as I am, here, have some kittens.

https://www.google.com/search?q=kittens&source=lnms&tbm=isch&sa=X&ved=0ahUKEwjU3JaXpqXVAhUX1GMKHWKrDRUQ_AUICigB&biw=1366&bih=572

The Seagate name is tarnished much the same way the Sony name was tarnished. The average person doesn’t know this but everyone in the computer field does. Good luck with that one you’ll need a miracle.

The times they are a changin…The FED has reinforcements…Otherwise lovingly known as the BOJ–PBOC–ECB–SNB–among others…

Yep. All these Keynesian fraudsters and “former” Goldman Sachs employees are acting in concert to enrich their oligarch patrons at the expense of everyone else.

This is Friedman Fraudsters. All of these banking and stock value ballooning is right from Milton Friedman and the Chicago School of economics.

Reality can’t be surreal, it’s the real thing. You don’t work for your savings anymore, you use the stock market.

Yellen will be with us a few more years and it’s clear that the FF rate will never exceed 2% (and that’s very very optimistic).

There is a nihilistic quality to much of the commentary I hear about the stock market these days. It’s based on backward thinking, reminiscing to a time in the 1950s when the markets were fair.

Well, those days are over and you’ll just have to be satisfied with making money day after day. Anyone under 35 understands how the US economy is a closed circle, with stock market gains feeding consumption. The US economy is very similar to China’s in that respect, with the FED and government spending keeping the economy growing.

We haven’t even reached to point where the common man starts jumping into the market!!

The BOJ now owns ~ %60 of all Japanese ETF’s.

The ECB has bought large amounts of European corporate bonds

The Norwegian sovereign fund is worth ~1 T and owns ~ %1.2 of world wide equities.

The Swiss national bank is rumored to own over 80 B in US stocks and ~20 B in European stocks.

Virtually all state and local pension funds have significant investments in equities and need high equity returns to meet their stated goals.

All of these entities and many others will suffer if the market even has a %5 correction.

So is it possible that there will never be a another significant correction?

re: So is it possible that there will never be a another significant correction?

Definitely possible. Getting a thousand heads in a row by flipping a coin one thousand times is also possible. In fact it is just as likely as any other head/tail combination.

If money is in fact the root of all evil, the FED is most certainly Satin.

At some point the greater fool phenomenon takes place, same as it ever was, and the last phase of the engineered wealth transfer cycle takes place. Watch as your 401k is being robbed

Rinse and repeat, thanks to Lord Satin.

Correction: The LOVE of money is the root of all evil, while the Fed is evil incarnate.

There, fixed it for you.

I remember the lineups to buy gold back in 1980 at deak perera. Today the lineups are at the food banks. In 37 years or less the middle class went from wealthy to completely broke. That of course is supposed to auger well for stocks as most companies are based on consumption from the middle class. The end result should be a stock market crash much worst than the 1929 crash.