Home prices are “weighing on affordability and constraining sales.”

Here’s another piece of an incomplete behind-the-scenes puzzle of the housing market that has surged to new record highs. Fannie Mae — one of the Government Sponsored Enterprises (GSE) that guarantee eligible mortgages and package them into mortgage-backed securities that are then sold to institutional investors — had some disconcerting words in today’s Mortgage Lender Sentiment Survey for Q2:

More mortgage lenders say they have eased credit standards recently and expect further easing in the coming months.

Why? Cooling demand for mortgages. Mortgage lenders in the survey include banks of all sizes, specialized non-bank mortgage lenders (they don’t take deposits), and credit unions.

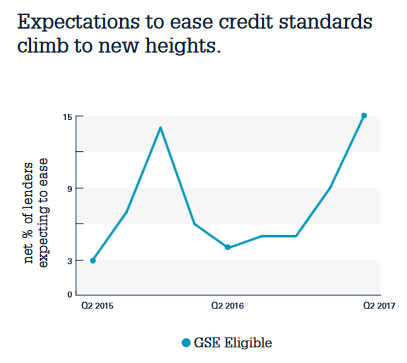

The net percentage of mortgage lenders that reported having eased credit standards over the past three months has been rising since Q4 2016. And the net percentage of lenders that expect to ease credit standards over the next three months for all three types of mortgages — GSE eligible, non-GSE eligible, and government loans such as FHA and VA insured mortgages – “reached or surpassed survey highs this quarter.”

The chart below shows the net percentage of mortgage lenders who expect to loosen credit standard of GSE-eligible mortgages – the “conforming” mortgages that adhere to GSE underwriting guidelines, including loan limits:

The driver behind the loosening of mortgage standards? Lenders want to write more mortgages. That’s their business. But the business hasn’t been going all that well recently, just when home prices across the country, and in particular in certain cities, have surpassed prior bubble highs, and prudence would now be more important than ever. So what drives them to lower their standards?

Cooling demand for mortgages.

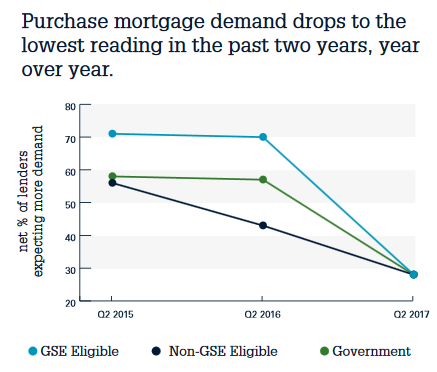

Lenders’ increasing concerns over “economic conditions” drove the easing of lending standards, as mortgage demand has taken a hit, and as the share of lenders who reported growth in purchase-mortgage demand “dropped to the lowest net reading in years.”

The report: “Across the three loan types, the share of lenders who reported growth in purchase mortgage demand dropped to the lowest net reading in years for a second-quarter period”:

Comments on why demand for mortgages was cooling differed by institution size:

- Larger Institutions: “Higher rates. Uncertain economic times” and “Competition.”

- Mid-sized Institutions: “Lack of inventory. We are an affiliated mortgage company and the lack of inventory in our markets effects our business directly.”

- Smaller Institutions: “Higher rates.” “Cost of housing.”

The report pointed out that this drop in demand for purchase mortgages confirms Fannie Mae’s report earlier in June that found that Americans were souring on the housing market, with the percentage of those thinking that now was a good time to buy a home dropping to a record low.

“Easing credit standards might also be due in part to increased pressure to compete for declining mortgage volume,” said Doug Duncan, senior VP and chief economist at Fannie Mae.

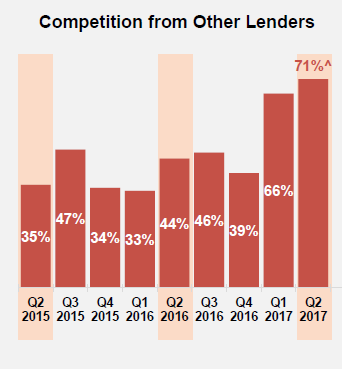

In face of declining demand, competition among mortgage lenders to write mortgages “heats up.” So they get more aggressive with their rates, which lowers their profit margins. And 71% of the lenders blame competition for their lower profit margin outlook, the highest percentage in the history of the survey and up from 44% a year ago:

Fannie Mae’s Duncan:

“Expectations to ease credit standards climbed to survey highpoints in the second quarter as more lenders reported slowing mortgage demand and increasing concerns about competition from other lenders.”

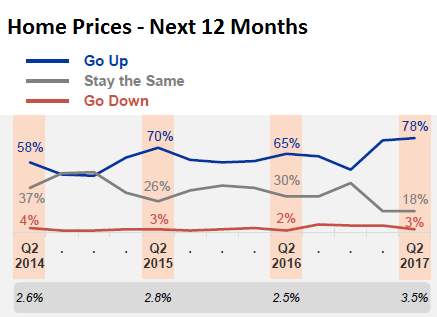

But the mortgage lenders remain an optimistic bunch in terms of home prices: 78% said that home prices over the next 12 months would rise, also a survey-high, with only 3% daring to think that home prices might go down over the next 12 months:

The report summarizes “Tight inventory has pushed up home prices, which is weighing on affordability and constraining sales.”

This survey is another piece of the puzzle of a housing market that has boomed in many cities beyond what is sustainable and affordable. Now the Fed has embarked on raising short-term yields and has brought them up one percentage point. Long-term yields continue to drop, and mortgage rates remain historically low. But the Fed is now also targeting long-term yields with its strategy of unwinding QE.

QE was designed, among other things, to bring down long-term yields and mortgage rates, and it did so successfully – hence the surge in home prices. Unwinding QE, including shedding the mortgage-backed securities now on the Fed’s balance sheet, will eventually have the opposite effect, just when home prices have surpassed the prior crazy bubble peak – in some cities by a big margin.

And that QE-Unwind may start in September. Read… Rising Wages Scare the Fed: “We Need to Get on with This”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

In socal where I live lack of inventory is creating bidding war.. i am.in San Diego

Most of the houses are sold for above asking price

Who knew there were so many rich people. As prices stand now there is no hope of me ever owning a home in socal ever again.

$600K gets you nothing great in a so so neighborhood…….that is so far beyond my reach as to be laughable. Based on 2015….a horrible year….I can afford a $230K house. Even based on 2014…..a much better year…..I can afford a $410K home

I’m screwed.

You need to have patience and save save save..

I

Socal has seen many boom and bust cycle and a busy may be on its way

Make sure you have cash and job to buy a house then

“I’m screwed.”

That’s because, like so many millons of other drones, you’ve allowed yourself to be persuaded that it’s all about money, when it’s really about quality of life. These are very different things.

A fine quality of life is quite unaffordable there unless you’re rich. So you need to relocate.

You Americans would be a lot happier if you weren’t such suckers.

Walter, that’s harsh. You know nothing about me but you sure seemed to have an opinion based on that post.

And i’m a drone?

WTF is wrong with people these days? Everyone is so weird. What’s with all the anger and belittlement?

Trust me, i’m no drone and my quality of life is just fine. I gave up the rat race decades ago when I woke up one day and thought “is this all there is”.

The reality is RE prices have divorced so far from reality as to be laughable and Jon is 100% correct, it’s going to crash again it’s not a matter of if…..still don’t know if i’d buy though. I hate yard work and the last house took all weekend just to mow and blow.

Gee Walter, what elite country do you live in where you can feel so superior? Canada? Saudi Arabia? Switzerland? You must believe that where ever you live is in a vacuum, and immune to dominos falling. Perhaps your MAP needs revision. You don’t have to insult the man and actually all Americans reading Mr. Wolf’s blog.

As for the young mans concern, as a former real estate broker and mortgage broker I can tell you that history is full of housing ups and downs that seem to go in a decade up and one down. Granted, this time the lenders have been given ‘get out of jail’ cards, especially with the Executive order that Obama made, deleting the ‘lender’ fraud clause from HUD docs (but who cares right), but none the less this will not go on.

Save, save all you can, for there will be a day when these so called’ investors’ and bidding war asshats, won’t just run out of steam, but sell at any price. Remember, Mr. Wolf has pointed out the debt monster starring straight at us, the train wreck of commercial RE, retail destruction, stock market bubble, municipal and US debt, commodities tanking, and on and on. The world is in for some terrible, long term, hurt. Ask yourself if this sounds like a time to buy anything let alone a house with or without a mortgage. And, for God’s sake stay away from all condos.

“You Americans would be a lot happier if you weren’t such suckers.” A simple minded and inflammatory generalization.

Sorry Walter, simply not true,and really rather unfair.

People who want to build simple decent lives are being screwed by the real estate mega-bubble: they can’t even rent cheaply and save.

I hit the bottom in 2008-11 due to a total collapse in business, – just avoiding the streets – and believe me, it is all about the money.

We all live in highly advanced and very complex commercial societies. No one trades anything for ‘experiences’.

I like a walk in the woods in the Fall as much as any sane person, but it’s a hell of a lot better with a bulging wallet in my pocket, after that nasty experience.

Leave California and move to North Dakota!

Lot’s of cheap (and expensive too!) houses in Fargo, but RE taxes are high.

Going from California to North Dakota will broaden your horizons and make you enjoy the seasons. In particular the beautiful white winters (after the snirt season of course) with temps of -35.

Ice fishing in neighbouring Minnesota will get you going as well. Then once you get established just think how much more fun it will be to take a trip to Barbados or Hawaii in Winter!!

But please don’t even think about moving to Australia. The median price of a house in Sydney just hit A$1.005 million.

And for that matter don’t even think about taking out an interest only loan as the banks here are on a tear jacking up rates.

You’ll need at least 20% down for your Sydney hole in the wall and rates will be around 4.7% for variable rate mortgages.

How about Melbourne? You know,”the world’s most liveable city” ? We are growing faster than Sydney and will overtake them one of these years. Our median house price is about A$250,000 less than that place.

PS: Just out today from the 2016 census: Australia’s population grew by 8.8% in the past five years – now you know the reason for the increase in houses prices.

A Huuuuuuuuuge increase in demand.

Melbourne, yuck, a police state with horrific traffic only surpassed by its crappy weather.

The Poker and the food is good, but that’s it.

I live close to Melbourne, Florida! Nice downtown, booming job market, and $250,000 will buy you a nice new 3/2 on a 1/4 acre lot. Taxes are super low. The only downside is it’s 98 degrees on a typical summer day with 90% humidity. So stay indoors from May through October. Oh and Zika and West Nile are rampant in the mosquitos. And watch out for venemous snakes. They’re all over the place.

do not go to north dakota unless you are a polar bear.

Interesting –

I’m currently living in Van Nuys … Craig’s list place, no interest in throwing all my money to a landlord for an even crappier place to live.

My friends are in Orange County and San Diego so I drive to one and/or the other every weekend. Seem nice in comparison to here, although I’m only 38 so my friends live with their parents or rent overpriced apartments.

Just got to make the best of it. At least we can earn decent money here, as long as we can find a way to keep it from landlords.

People suggest all the time to move to cheaper locations, but they don’t realize it’s all about the jobs. You don’t move out f the blue and settle, you’ve got to go somewhere that has an employer willing to pay you.

Once you give up on having a place you can invite friends to and indefinitely push off raising a family, life becomes much easier and more affordable. Travel starts to look cheap as less than $2000 can get you anywhere in the world for 7-10 days, which is merely 2 months rent in a craigslist place. A crappy studio apartment would cost an extra $400/mo which would make it impossible to go anywhere.

Point is, don’t be discouraged- just change your goals to what makes sense. There’s a lot to see in this world, best not to waste your life struggling just to enrich our greedy landlords.

With a few exceptions, the job you have in Southern California exists in every other state. Healthcare, IT, FIRE, education, manufacturing, all of it takes place in other states. What you are ‘buying’ in California is the scenery and climate but the reality is 90% of the people in California don’t have a home with a view of anything other than the house or apartment next door and , unless you are homeless or your job requires it, you don’t spend much time outdoors.

If you can’t stand cold weather you can live in Florida. OK its hot and humid for 3 months but the other 9 months have better weather than California and, for the price of a California ‘crap shack’, you can buy a very nice house and have enough money leftover for a $200,000 boat to enjoy the water.

Interesting: run a rent vs buy calculator and it is likely you are better off renting in SoCal unless you want to head way inland. It doesn’t make sense to buy in this extreme seller’s market.

We talk periodically about leaving SoCal but probably won’t for a few years yet. It comes down to opportunity and resources – Cali has more of both than anywhere else I’ve been except maybe NY, and obviously the great climate helps. If CA state and local govt keep raising taxes and fees, we may hit our breaking point as business owners, but until then, as much as I complain, I honestly like the lifestyle here. I know I will leave one day, so I’m enjoying it for now!

I ran my own rent vs buy calculation in a Florida market. Just a simple cost per square foot versus rent per square foot for a similar house in the area. It was always cheaper to rent, at 73 cents to the dollar, than to buy. You also avoid the maintenance risks.

It isn’t rich people buying these houses. It’s soon-to-be bankrupt people who are taking on reckless and irresponsible debt levels to buy into a housing bubble at the peak. This will not end well for them, the banks, or taxpayers.

If you look at a nicer area the average household is bringing in $140k. Not uncommon to hit if you are dual income and one of you works at Qualcoom. This starts to put you in range of the average nice 3-4bed home which is around $750k.

That of course is slightly inland. Still a shit tone of money and out of reach of at least 75% of families in greater San Diego.

The real bummer is even 2 bedroom condos has been going nuts probably because people who should be buying bigger houses are forced to buy lower tier property.

A 2 bedroom that sold for $370k in 2013 is now selling for $500k plus an HOA.

I am highly reluctant to even grab a realtor and look at maybe only 1 in 20 places that pop up in our price range. And most of them wouldn’t be ideal 10 years from now.

I fear that buying a starter home now is a trap as its seems unusally likely home values will decline over the next decade as QE unwinds.

On a side note there may yet be a day where $410 can put you in a house in SD in an okay area. My stance is wait, hope and leave if prices keep going up for 10 years.

Yet it’s far more likely that the median in SD will resume falling to a level far lower than 2001 prices.

I was stuck in 3 lane traffic on 95 in a small town in Ma. recently, my car literally 100 feet away from what I’m guessing was a 1500sq/ft Cape Cod listed for sale. Quick search showed what was obviously a flip with an asking price of $750k. Seven hundred and fifty grand for a house whose living room windows have a great view of peoples car wheels. This is a big, expensive game of musical chairs which is not going to end well for some stupid people

750k is the sweet spot in san diego, if you have the means to buy above that, then you can get a great house.

My budget is 1 million in San Diego inland.. Not coastal

I can’t find any decent home to my liking for this much money

Id wait for few years

here we go again.

Incomes stay the same… assets go to the moon. What could possibly be wrong?

A lot of people fear missing out on the asset rise. Can you blame them?

It’s really going to take a market downturn and job losses to crater this thing. I think eventually, it’ll happen in tech as more high-end jobs to to India / Philippines / Romania from our globalist overlords. That’ll be the day of reckoning. I don’t think China’s going to actually stop its people from buying up our land. And the criminals from anywhere on planet Earth are also unlikely to stop unless the FBI gets even more serious.

And I still marvel at how well marketers (Google / Facebook) and distributors (Amazon) are faring against those who actually make shit. Something seems so wrong about it.

Wilbur Why doesn’t our govt stop China from buying up our land Oh right because they couldn’t care less about American homebuyers Right

We gave them the money and are just buying American “goods” with it. ;)

Did we expect them to not cash in their “claim checks” some time? It is payback for all the “free” stuff they shipped us in exchange for bits of paper years back.

If any would have been concerned about the possibility of this happening they should have spoke up when we assumed the Chinese were just suckers taking easily printed paper”claim checks” for real physical goods.

Just wait until the $10 trillion cumulative balance of payments deficit starts to flow back to the states. America won’t be owned by Americans anymore. You haven’t seen a dent in real estate inflation yet if that happens.

Actually that is a good point. if china had not put capital controls on its currency’s outbound flows the rate of Chinese real estate ownership would be much higher. The Chinese don’t have to purchase treasury notes . We are feckless in negotiating fair

trade with china in the hopes they will intervene in

N. KOREA .

Frederick,

I don’t blame government for that. I blame our banking and oligarch overlords who have imposed the “Free Markets!” sickness on everything.

I see so many things now in terms of viruses. Take the ADS virus for example, It consumed the host until nothing was left but a shell, and death, and at the same time seeking a new host to start all over again.

When you start looking at companies, governments, greedy investors and so much more as viruses, you get the picture.

Tech in India is shrinking owing to automation. H-1B hires in the U.S. are down by 16% this year. Indian tech giants like Infosys are now hiring American citizens in its U.S. workforce.

https://www.washingtonpost.com/world/asia_pacific/the-high-tech-jobs-that-created-indias-gilded-generation-are-disappearing/2017/06/22/815f1d0e-5588-11e7-9e18-968f6ad1e1d3_story.html

New skills are called for in this scenario. in the Internet Of Things space, for instance.

Infosys is getting sued in Texas by a white guy claiming discrimination. I only saw the headline of the story because of paywall.

I find that almost all of the people i have met from India are highly analytical and deeply consumed by the importance of academic education, especially math and science. They are uniquely adapted to analytical pursuits, hence their disproportionate involvement in the tech and medical industry.

Interestingly, i do not see much representation from them here in the legal profession. Probably not enough math in that arena for them.

Preet Bharara :-)

Underwriting standards have been very tight since the the first few years after the global crash , but have been loosening up for the last few years. Inventory is still low and doesn’t seem to be growing….yet.

Yes Wilburt, incomes is actually down if you take into account inflation here in SoCal.

Similar things were said in the 80s about the Japanese and look at where we are.

Huge fan of your website Wolf, frequent it almost daily. But its interesting how you always seem to focus your oped with an almost always domestic focus.

Have you ever considered that our gov is sacrificing some domestic markets for international gain? After all, even Milton Friedman had to accept that foreign policy trumps domestic politics.

Amazon, eBay, and most dept stores selling cheap Asian goods to the detriment of small business have served a purpose too. Its two fold. It interrupted the spread and influence of unions in crucial markets avoiding the US from importing European Socialism, and bloated China with success pushing the Russian and European influence away. Feeding a credit frenzy that will now hurt them for at least one to two generations.

Like a snake that allows itself to be bitten before it strikes. Our gov might not be as corrupt or as short sighted as you may think. (or at least lets hope so)

Airbnb – masks underwater mortgages by blending the line between commercial/private real estate with out owning a single flat.

Uber – hiding unemployment in overpopulated urban areas without owning a single vehicle.

Are you sure its all just greed and chaos?

Wolf, can you explain the adoption of “the one child policy” by the communist Chinese? They sabotaged their own demographics.

1 Fed hike during 8 years Obama, already 3 hikes during Trump. Volker moment?

Lets hope the convictions remain. And thank you for keeping this website interesting Mr. Richter.

I could be completely wrong.

You are not wrong. The teachers unions love immigration because our young people can’t afford to marry and start families. The police gets to lock some of them up, the hospitals get to treat them, the real estate industry has to house them, etc……. Americans get poorer.

So we might have the crash by December or next year?

No crash. But the air might come out of it gradually.

So it will be painful and slow then.

Prior bubbles ended abruptly when people realized the party was ove. Why do you thinl that this time the landing will be so soft?

Hiho I disagree with Wolf again I think some black swan(think Lehmanesque) will swoop in and the whole Ponzi will implode in on itself in rather short order It’s just too out of whack and it’s been going on for far too long already

I’m not very confident in my theory… it’s just a theory. No one knows what’ll happen. But given all the liquidity out there, I think the process will be long and frustrating, rather than quick and dirty :-]

I’ve been talking about this in some articles and in the most recent X22 Report. There are a number of reasons, including the massive amount of global liquidity waiting to “buy the dip” and to “buy the crash.” They figure central banks will unleash more QE if prices crash past a certain point, and they want to front-run it. And each time, it stops the market from falling further. It also gives central banks a reason NOT to restart QE, and then the markets drift lower again….

That’s my theory…. Could be wrong…

Wolf, yet all this liquidity is the result of leveraged debts. We are starting to see the debts defaulting as in CRE and auto loans. Which may not be enough to kick the real decline into gear but between that and the FED’s actions, actual new debt creation has gone negative. This is a sign post.

It would seem logical that this is the end of this cycle. To stop the ensuing decline, all the FED can do at this point is to lower interest rates, which 1% isn’t much. And the other entity that could prolong it would be the federal government and they seem determined to crash the health care industry at all costs and increase the federal deficits with out putting any of that new debt into the hands of the working people… which is who ultimately pays for everything.

You have previously written about the apartment and condo glut that is coming to most cities. I have seen the cranes in quite a few US cities and concur that there are lots of projects coming to fruition.

So what all the massive liquidity did was to enable huge overcapacity in almost everything. To many vehicles, to many homes and condos, to much stuff.. Way beyond the economic need or ability to pay for it.. especially in these later stages when the developers paid to much for the properties.

The next phase may take longer to get going because there is still lots of liquidity or the appearance of liquidity out there.. But once it gets properly going, there will be a crash because there always is a crash when that proverbial wall is hit and faith is lost and no one will lend more money to fund a dying propositions such as an over valued condo complexes that no one can afford to rent or own.

It a herd mentality

Once people get a wind that these prices are not sustainable ..the music would stop…

Real estate is all about psyche…

Sorry if its not nested under your appropriate comment.

Would liquidity head to India instead and other cheaper Asian countries?

China’s workforce is getting expensive and the new single children grow up entitled. Money will funnel in cheaper alternatives. America is the safest place to park money, but its also at a premium now. I don’t disagree there’s plenty of liquidity out there but as Indian/US relationships attract, safety follows, so will investment that chases profits instead of just safety.

I don’t see a crash either, but i do see industries falling in certain regions of the US. Especially in coastal cities where the reasons for expensive real estate is being held up from tech jobs. If that slows, so will r/e prices. Facebook and Google have already opened offices in the recent years here in LA. Is it an expansion, or are they modestly escaping SF prices??? Will LA stay up but SF drop? What about SD? What about Miami? Latin america isn’t flocking as it used to, and i can give you plenty of examples of skyrises not starting produciton because they weren’t able to reach their pre-sale quota to make construction worth while.

Since the election, a majority of my coworkers are bringing lunch from home. When you see people making over $150k bringing food to save a buck, imagine the mentality they are in??

Would like to hear Wolf’s commentary on this ?

Here are two studies that show that the housing market is in an 18 year boom and bust cycle.

And some facts from the first link below…

“Perhaps the most stunning aspect of the real estate cycle is not its inevitability but rather its regularity. Economist Homer Hoyt, through a detailed study of the Chicago and broader US real estate markets, found that the real estate cycle has run its course according to a steady 18-year rhythm since 1800.

With just two exceptions (World War II and the mid-cycle peak created by the Federal Reserve’s doubling of interest rates in 1979), the cycle has maintained its remarkable regularity even in the decades after Hoyt’s observation.”

http://www.extension.harvard.edu/inside-extension/how-use-real-estate-trends-predict-next-housing-bubble

https://www.marketsandmoney.com.au/recession-2017-yes-no/2017/06/21/

Illinois is so close to the wall it may be the next much bigger Puerto Rico.

Latest hit: it will have to shut down the state lottery because it can’t come up with the prize money.

‘The state lotto requires a payment from the legislature each year. The current appropriation expires June 30, meaning no authority to pay prizes. In anticipation of a budget deadlock, the state already is planning to halt Powerball and Mega Millions sales.’

Since a lottery makes money a phone call to Goldy would permit the event to proceed, with 20% smaller prizes. But the 130 billion pension shortfall is not as easy to fix.

Some pubic figure, I can’t remember who, has warned the Fed against tightening too fast. His words almost exactly were: ‘We are only one major shock from a deflationary collapse’

People in Illinois are talking about some form of bankruptcy, although the official version is not legally possible. But if it can’t pay it can’t pay so some type of debt default is possible.

That might qualify as a ‘major shock’

Illinois has all the prospects of being the next boom. They have a crippled economy , RE, infrastructure, they have energy production where they consume 1/7 of what they produce and right demographics since their baby boomers have already flocked FL and excaped the -39 F. They have a Republican Governor but the legislature is a mess. Unions still strong.. and crime at all time highs..

but there are many states that are warmer, less liabilities form unions since they never got as big as Illinois at other highs, and have better tax regulations.. i dont see it happening there yet. unless its for political reasons to show how Republicans handle inner cities and help them out of depression…

Blog McMansion Hell being shut down by Zillow – this is a scoop guys’n’gals

https://www.reddit.com/r/LateStageCapitalism/comments/6jnq6n/mcmansion_hell_being_threatened_with_a_lawsuit_by/

Wolf, I know you have the skills to get this story out, this is the kind of thing I should be hearing about on the radio or reading in the newspaper. The ACLU should be on this and they’ll get on it once some NOISE is made about it. I know you stand a very good chance of starting that noise.

Thanks for bringing this up. Looks like a complex (and perhaps frivolous) issue of copyright…

From ars technica (which has a lot more muscle than I have):

https://arstechnica.com/tech-policy/2017/06/mcmansion-hell-used-zillow-photos-to-mock-bad-design-zillow-may-sue/

“McMansion Hell” used Zillow photos to mock bad design—Zillow may sue

“On Monday, Zillow threatened to sue Kate Wagner, [the blogger at “McMansion Hell”] saying that that she was violating its terms of use, copyright law, and possibly the Computer Fraud and Abuse Act because she took images from the company’s website without permission. However, on each of her posts, she acknowledged that the images came from Zillow and were posted under the fair use doctrine, as she was providing (often humorous) commentary on various architectural styles. Her website was featured on the design podcast 99% Invisible in October 2016.”

“Confusingly, Zillow does not even own the images in question. Instead, Zillow licenses them from the rights holders. As such, it remains unclear why the company would have standing to bring a lawsuit against Wagner.”

As bloggers, we constantly brush up against big companies. I’ve had my run-ins most recently with Amazon over my recent articles, with Hyundai that didn’t like my article in early June, Walmart, UBS, Lagunitas… I try to stay clear of copyright violations and things I cannot prove. So for most part, I haven’t had to back down. But it’s a fear we live with.

We bloggers are not protected media companies. We’re just sitting ducks. The threat of a lawsuit alone can shut us down, no matter how frivolous.

But ars technica picked up on it – and that’s good. It’s going to motivate Zillow to work something out.

Thanks for the insightful post Wolf. I just saw it on Reddit, tried the site and they’ve taken it down, saw that people on Reddit liked that site, and thought, well, here’s news.

Ars Technica is indeed some muscle that will make it a story if it is one.

Yeah, I can’t talk smack about Disney using Disney characters.

Addendum: They could talk smack about Zillow listings if they had their own people take photos of the exteriors of the same houses, or had readers send ’em in. But the photos Zillow uses are Zillow’s copyrighted photos.

Here is the Electronic Frontier Foundation, whose articles I cross-post from time to time, taking up her case:

https://www.eff.org/deeplinks/2017/06/mcmansion-hell-responds-zillows-unfounded-legal-claims

She is in good hands.

I was sued by a female couple from NYCity who were big shots at NBC for not bending over and kissing their You know what’s Luckily I had some of my own friends in high places so the case was dismissed It was pure BS all the way but it cost me in legal costs and stress on me and my family Bad bad people

Affordability is a powerful force. We need to see some changes in interest rates before anything will happen. Houses is only part of wider bigger asset bubble. The bond cycle is the scary one because will make those MBS government guarantees useless. They will try to inflate the debt with next QE (this time Fed will buy directly from treasury) and next the dollar system is gone.

Alesio Exactly true about the dollar and that’s why I’m buying real estate and gold bullion overseas My wife still believes in the USD so it’s been a chore getting her to agree to diversify out of ALL dollar denominated assets

My word of caution on betting against the dollar :

I bought an annual subscription in 2005 to an online financial newsletter written by a guy named Bill Fleckenstein.

He was negative on the dollar, adamant that an inflation tsunami was about to hit, negative on bonds and stocks and long on metals and miners. Anyways, i did not renew it the following year.

Fast froward 12 long years. The dollar is stronger, metals and miners have not done that well. No runaway inflation.

Now, i ‘m a patient enough guy. But 12 long years…, no thanks.

I think an official comment from the National Association of Rodents would be in order here ……

Like who will put the bell to the cat? Who stole my cheese? I stole your cheese! Stuff like that?

I don’t think you can deflate a bubble, it will still crash. The best you can do is reduce the effect the crash has in the economy, that’s it.

Raxadian If history is any indicator ” and it is” we will have a spectacular correction/ crash very soon or hyperinflation which is probably worse

The housing bubble will inflate until the proles can no longer afford the rent/mortgage payments. Then the property owners will borrow from the banks to cover their losses until they can’t service the loans. Then the banks will realize what’s happening and shut off all lending.

Then it will crash. But not before. People are still making their $2000/mo rent payments. There must still be some disposable income out there.

$2000/month? I pay $2800/month rent for a 1000 sq ft condo. It’s painful, but in my neck of the woods, a similar condo runs about $800k to buy, and $160,000 in cash as a down payment is way too much for a first time homebuyer. And the difference between a $500k condo and an $800k condo is dramatic – there’s an inflection point there where buying competition goes down and quality goes way up. That extra $300k buys much more than the first $500k.

What it comes down to for me is – do I blow all my cash on a down payment for a overpriced home, or do I keep my powder dry and ready to take advantage when the market corrects? Ride the market back up, then buy into the housing market when it troughs out 2-3 years after that.

A friend sells real estate here in the Sacramento valley. Even out here in the sticks, more than half her sales are cash. Cash sale means no mortgage. Some sales are Chinese or Indians, but most are Bay Area refugees or boomers downsizing.

My friends sells RE in the bay area. He says the cash buyer is a myth.

I’m sitting in one of the most expensive zips in SillyCon Valley…and yes, the discounts are starting to come in. And they’re double digit percentages.

Was NO myth in my case An English artist living in Manhattan paid all cash for my house in late 2014 I got out alittle early Sag Harbor NY

They may close the deal with pooled cash, but guess what they do next? Refinance through the bank and then payback all of their friends and families who loaned them the money in the first place. Then it’s you and me left holding the bag when this goes south.

I always thought it was a myth too, until we started seriously looking. I think some areas and price ranges are more cash heavy. We are cash buyers, and have looked both in greater LA and around the Bay Area. Both places, the realtors essentially said cash no contingencies is typical, and if our offer was cash WITH contingencies, it may not even be competitive. Which I took with a grain of salt, I don’t trust realtors at all. Still, cash offers are pretty common here.

Here in my little neighbourhood in Oz you can the see the cash offers quite easily.

The “For Sale” sign goes up and then either the “Under Contract” or a “Sold” sign goes up if the property is bought.

If the “Sold” sign goes up within a a couple of days or a week you can almost be certain it was a cash offer.

Those “Under Contract” ones usually stay up until finance comes though. You can also check on the various RE web sites as well. Then once finance comes though you see the sign changed to “Sold”.

The houses around here seem to be about half cash and half finance. I posted before about a house that went up for sale on Thursday and the “Sold” sign went up on Monday. Yes, it was a cash sale to a Chinese couple at A$50,000 over the asking price.

Not much for sale in the neighbourhood area.

One went for “only” A$925,000 which was actually under the asking price range. Older house on a dead end street with a sloping yard. Nice big lot, but I guess it didn’t have the wow factor.

That multi-million dollar place around the corner from us on the main road with the big lot is still for sale.

Just up the road from that (About 1 mile further away) on a big acre lot is one just listed for A$1.6 million. Others that have come on the market range from A$775,000 to $A850,000 (2 houses) and two units ranging from $A570,000 to A$968,000. So there just isn’t much on the market.

Will have to catch up with the local RE agent who lives across the street from us for the latest news this weekend.

It will be interesting to see what happens after 1 July when the stamp duty for first home buyers changes. People have probably been holding back on buying as it will save them a bundle, but unfortunately the last time they changed the rules all it did was force prices higher.

Also I wonder what will happen to many of the retirement units for sale now that the reports on the company running them have come out. I feel sorry for those that have been taken advantage of and how it has affected their asset values. Many will now be unable to sell their properties……….

When I bought my home in Minneapolis twenty-two years ago, I was a cash buyer, but in reality, my father (with whom I was in an Ag business with) simply put money into a bank account for me to have a line of credit. After closing, we set up a mortgage with Hennepin county at 4% and all was legal to a tee. This let me buy a house and have the corresponding tax break. I am lucky and grateful to have had this opportunity.

MaxDakota:

My home went on market on a Monday. My realtor showed it to me Tuesday morning, and we put in a cash offer with no contingencies that day for just over asking price, and that got me the house. By Wednesday, there were five offers and one had a bit higher price than mine, but the seller had only one straight up offer, and he took it.

Good luck to you and yours in your quest to purchase an abode!

I sold last year in the Bay Area. There were a couple cash offers, but they were 10-15% lower than people that financed.

Well if it’s a myth then we were outbid on at least one house in San Francisco by a myth in 2015, then.

The word we got was that the owner would’ve rather sold to us since we’ve lived here for decades, but he couldn’t ignore the bit of extra money on the sale and the hassles and extra time for financing of a non-cash sale in our favor.

It turned out to be good it fell through since we got something that was never listed before selling, fits us better, needed less work and in a neighborhood we like better.

Housing markets have been invaded by investors. Thanks to inflated prices and flat wages since the 1970’s we have less buying power which turns us into renters or debt slaves. Other countries don’t allow foreigners to be property owners but America loves to capitalize on it.

That’s not totally true You can buy in Poland and Turkey just not certain large tracts of farmland or land near military installations

‘ There are a number of reasons, including the massive amount of global liquidity waiting to “buy the dip” and to “buy the crash.”’

What’s going to crash here? Real Estate or the stock market?

Is it possible to have a crash in one and not the other? Does the Fed view them the same way? Will it allow a stock market crash without a real estate crash? If real estate inventories are genuinely low, then that might keep prices high.

A “crash” in real estate takes years to play out anyway. The last one took about 4 years. And it’s very local, with each city following its own dynamics and timetable. Stocks can go down faster. So they may occur at the same time, but they don’t have to. Last time, one triggered the other. Every time is different.

This is what concerns me so much. I’ve been trying to stay informed through blogs like this over the last 7-8 years, so that we don’t make a huge housing mistake.

Now my business is finally to the point where we can afford to buy, but the market up here in Portland is at its all time worst, even compared to just 8 months ago. I naturally want to wait, but if this thing becomes a slow slog toward the bottom, where we don’t see a noticeable reduction in prices for years, I’m not sure it’s worth waiting and potentially bouncing around rentals for that much longer (especially considering my special needs son who’s going into kindergarten and thrives on stability/continuity.)

I’m one of the only people in my circle of friends /family who knows a little about things like foreign investment, QE, P/E ratios, etc., yet they’ve all bought in the last several years, despite my cautionary tales, and I’m worried I may be the one left holding the bag.

Probably you suffer from paralysis due to analysis…

No one knows how long the party would go on but for sure the music would stop at one point in time

It’s not really that. Like I said, after years of studying the market, we’re finally just now in the position to buy. The house we’re renting has gone up $200K (40%) in value in only 3 years, so it seems absolutely bonkers to buy right now, but a slow unwind may be too far off to wait.

The housing market will be climbing steadily for the next 7 years despite what everyone says about a bubble. And Trump will not be impeached, I believe he will win a second term to lead us into the next crash. Then a democrat president will lead us out of the crash. That’s how the system works it’s a pendulum that swings back and forth.

With that said, there is no point sitting on the sidelines waiting for 7/8 hrs for a crash. Do the math and decide what’s best.

No crash in single family real estate except for one scenario…..massive job loss.

Otherwise, the Fed can and will step in and buy mortgage paper for struggling loans. This is all implied and understood from the last crash.

Regarding the over supply of apartments, the Fed will step in and buy this paper from Fannie/Freddie/whomever when they start defaulting (and they will because they’ve overbuilt as long term demand will surely drop). These apartments are Obama’s gift to subsidized housing and many will be converted to such.

So it’s all good for now (with exception of massive job loss scenario). I’m being a bit sarcastic with that last line of course.

The prices would never crash.. this time is really different..my realtor told me so..

I think the housing crisis is limited to just a few crazy areas. Who should care if you can’t buy a house in San Francisco, or even California for that matter? You like warm sunny weather or ocean- go to South or Southeast. You like hiking and camping – go to Pacific Northwest. You like restaurants – go to Texas. You follow trends and like being seen by others – please stay in California.

We moved out of Southern California nearly two years ago to get out of it, but now prices in Portland have gone up 40% in that time. Argh.

There should be no involvement of government in housing insurance. Let the market take care of itself, and let the chips fall where they may.

Maximus Agree with that 100 percent

Unregulated markets are pretty much guaranteed to be rigged.

Predators like them, though.

interesting:

You did say you were screwed. In the effort to try to unscrew you I got under your skin.

Sometimes it helps, sometimes not: it depends on the subject. Specifically, it depends on how prepared you are to accept feeling like you’re screwed.

Sorry.

Running out of knife catchers was the beginning to reversion to the mean during the previous correction. This correction will go far far deeper.

Will Governor Scott of Florida vote for a new piece of legislature making it hard for Investors to borrow money from private lenders at high interest rates. Investors are not complaining about high interest rates because they understand that it is risky. Sometimes deals go south and one must live with that.

I heard a real estate agent complain last week that buyers have completely disappeared and those with deposits down are walking away. I’m in San Diego.

That’s not true..

Low inventory is not good for real estate agent as there won’t be large number of transactions and the prices would be pushed up because of low inventory… this would further push many people out of market beaus of low affordability…

There’s lots of house for sale here. Too many.

i suppose it all depends upon where you care to live. if you want to live in california, then you are going to be stymied unless you have the doremi.

if you think your $1,000,000 job in silicon valley will entitle you to a wonderful mansion, think again. all that wage will go for a poorly built bit of housing in a zero lot line community.

so, i think the time may have arrived for an exodus from california.

new mexico, texas, louisiana, georgia, alabama, mississippi.

some tell me that they stay in california for the culture. hah! i hazard a guess that metro houston offers more accessible, affordable culture than most citizens of LA or SFO frequent.

sure, some of these states aren’t paradise, but they are affordable. and i think that good jobs may be more available than in socal or norcal.

on the other hand, when quality of life issues are considered, these states may be more congenial than anyplace on the west coast.

oh, and another benefit. lower taxes. and a friendlier set of estate tax laws.

sometimes, i think citizens need to consider a menu of citizen-friendly issues. not just housing prices.

– I turn to Steve Keen’s formula: Income + change in debt = GDP. With “Mortgage demand cooling” it means that the “change in debt” is shrinking. Assuming that “income” remains flat it means that GDP here in the US is/could be already contracting (=recession).

– The total amount of mortgage debt could still be growing but the “growth in debt” is shrinking. The pace at which the (mortgage) debt is growing is shrinking.

– Off topic: In a previous post Wolfstreet reported that A LOT OF US companies have issued socalled “Reversed Yankees”. US companies took out loans denominated in EUR. It was/is a bet on 2 things: 1) rates being lower in the Eurozone 2) the EUR/USD going lower.

– But now with the EUR/USD right now going higher those companies could have made the wrong bet. It remains to be seen whether or not the EUR/USD will keep rising but this “Reverse Yankee” could be turning out a time bomb under the companies that took out those loans.

– Becasue when those “Reversed Yankees” are paid back/sold it is a force pushing the EUR higher against the USD.

– I know a company that had A LOT OF income in USD but it took out loans in CHF because the rates were (much) low(er) when borrowing in CHF. But then the USD went down against the CHF significantly. And that meant the advantage of taking out a loan in a different currency turned into a “dis-advantage”.

– I also remembered that people in Poland & Hungary took out mortgages in CHF before 2008. But after 2008 the currencies of both countries started to go down against the CHF. It meant that thoses people saw the value of their mortgage debt and payments go up. Ouch & OMG.

See e.g.

http://www.zerohedge.com/article/swiss-franc-and-possibility-huge-mortgage-defaults-central-europe

Saving money at this point in time seems kind of dumb to me. Now saving in real money, i.e. gold or silver that makes sense. I think our next crisis will be an existential collapse of our currency to be replaced with a United States only currency to see massive devaluation v.s. the other world economies. Buy silver now while it is still ridiculously low and keep renting or whatever until the bottom falls out for real this time. Worst case is you will have real money that can be traded for whatever currency is the new world currency not the debased fiat that we are currently seeing. The amount of derivative exposure in the world, pension plans going bust etc should make everyone flee to real value which would be real estate that earns money, not your primary residence, gold, silver etc. There is a serious come to Jesus moment coming and when the smoke clears the only people who will be left standing will be those who have cold hard cash…cold silver or gold that is.

I guess I just don’t get what a collapse of our currency means to you. Our currency is a debt based currency.. I can see a collapse in debts owed.. In other words, defaulted upon causing a deflationary cycle. The currency wouldn’t go away, what currency that is left, those with actual incomes and savings would be able to purchase lots of stuff cheap because for a while, new debt creation would be severely reduced. This would make all assets cheaper, houses, vehicles, and gold and silver because there would be less available cash to purchase them with..

So in a debt collapse, how is gold or silver going to go up in value? You purchase gold at $1250/oz today and in a deflationary cycle it might only be able to be worth half that much?

Seems to me that the the advantage to PMs would be in an inflationary cycle where you purchase it today at $1250 and it becomes worth say twice that…. which only is good if the cost of food or housing doesn’t also double…

So…I like to look at history as an indicator of the future. The problem is we have never seen a global reserve currency collapse before. In other words, currencies collapse in a country which has the effects as seen in Mexico, Venezuela, Argentina and of course Weimar Germany.

The interconnected nature of transactions are pretty much worldwide especially when looking at the dollar.

To save on the long description we have been supported since Bretton-Woods, first in gold then in petro dollars and now in wars, theft of gold and narcotics dollar standards. This is enforced with the tip of the spear via our military and intelligence services so whenever someone dares to try and leave the dollar we invade them and steal their gold.

Fast forward to what it looks like here…I think it will be first an isolation of our country since the currency is sick. The main pain so to speak will show up in importation of goods, namely Chinese goods since our manufacturing is gutted. We don’t make anything here except service class but having that trade deficit with other nations will end up stripping us of assets. The Chinese have a vested interest in keeping us up for now since they are getting our businesses, land, precious metals etc. They don’t want to get stuck holding the bag with a bunch of treasury bills stacked in banks so they are trading it for real stuff all over the world. It is ultimately a confidence scheme built on the full faith and credit of the United States.

So when that confidence leaves we will see the inability to trade fake paper for real assets and that will be the bugger in my opinion. In the meantime there will be a race to the bottom as anything that is not nailed down is sold into the market for liquidity. I see this on Craigslist and Proxibid all the time. When you can buy assets for .10 cents on the dollar something is wrong. People have a short term vision since that is how you eat and pay your rent, cash for now is still king.

When the cash is devalued over and over again the real value of assets like gold and silver will become apparent. They are real money, fungible anywhere in the world at whatever exchange rate is the current one. For instance, going back to Venezuela, the Bolivar experienced massive arbitrage between what the Venezuelan government pegged the bolivar to the dollar at v.s. the real value. They said it was a 1 dollar to 6 bolivars but the black market disagreed and dollars were exchanged for hundreds and then thousands of bolivars. Anyone holding gold and silver in Venezuela could ignore the “value” and essentially trade it in Colombia or better yet the United States for whatever the spot value is here.

A decree by government cannot erase the intrinsic nature of specie payments. That is the reason central bankers hate gold and silver, they are outside of their system. The next crisis is not one that will be a situation that only affects the United States but anyone in the world holding dollars. Since nobody knows what it will look like AFTER that event you would not be able to safely hedge into a different fiat currency as all fiats are vulnerable to decree by their respective monetary authority.

The beauty of precious metals is that they cannot be created out of thin air with the wave of a wand and they are compact enough to carry v.s. say oil or some other commodity. These unique properties make it very suitable as a store of value and the reason why they are accepted everywhere since they are the only true forms of money. Real money withstands the test of time, is universally recognized etc. That is why it would buy you stuff in ancient Rome just like today whereas the dollar in ancient Rome would be laughed at.

Assets are neither created nor destroyed in a sense, they are only transferred so when all that stuff rushes to real value gold and silver will balance.

Roger,

As I understand the reserve currency status it is much more than just a petrodollar it is a legal contract of debt that can be enforced in the US and world courts. The only other currency which a contract could be written where there is an actual viable court system is Europe. But Europe has its problems and isn’t a great choice at this time. Also the Euro doesn’t have a big enough debt pool (float) to cover world trade. You can neither enforce nor guarantee a contract written under either Russian nor Chinese law because under their legal system, you really have no guarantees. And neither system is actually large enough to facilitate world trade. They can trade among themselves but not the world.

As for past history, the most recent demise of a world currency was the British Pound… There have been many.. You need both a very large float and a reasonable legal system in order for large trades in the world to occur. Either that or the ships have to carry large amounts of something that can be actually traded for something they can trade to someone else. Same reason that doesn’t work is the same reason the barter system doesn’t work. No, fiat currency is what facilitates world trade. You can not do it with PM’s unless they are backing some fiat currency. And that has issues to because of its limited expandability.

And that is why gold or diamonds or platinum nor any other commodity doesn’t work for world trade. It can back a currency but then the value of it in the trading partner’s currency will probably be different. All depends upon each country’s demand..

Buying assets cheap is what I call deflation. To many goods and to little available cash. (Different at the top of the pyramid where there is lots of liquidity. At the top where stocks and yachts are sold, there has been inflation. At the bottom, deflation). And IMO deflation is where we are heading when all this mal invested debt starts defaulting.

So in the bottom of this Super Cycle, I think we should see lots and lots of debt defaulted upon and lots and lots of re-purposing and re-valuing of assets. Lots and lots of debt will be written off. Most of the TBTF institutions we know will be changed significantly or gone.

As the dollar is a Federal Reserve Note, i.e. FED debt. The actual value of any cash that remains will actually purchase much more than it does today. The government guarantees on bank deposits will be demanded. In order for the government to actually create this money it will need the FED to massively increase its balance sheet. The FED may not want to do this as much of their existing balance sheet debt may have been wiped out. Leaving this private cartel with debts owed which they are unable or unwilling to pay. The government may then have to do away with the Federal Reserve System which will take time because it is a Constitutional Amendment…

And all this will happen rather quickly once the system breaks down. Selling anything to say something will be the trend. Lots of good deals near the bottom.. Then the bottom will be long and painful while institutions and confidence is rebuilt.

And yes, owning gold at that time will be good, IF you can find a buyer. You can’t buy food, pay a mortgage or insurance or the doctor with gold. You will have to sell it and again, once the break down has occurred, the gold you buy today may not be worth in dollars as much then. Any more than a diamond or anything for that matter as there will be few dollars in circulation. Lots of things, few dollars, means good deals for those with dollars.

Remember, most transactions today are via credit or digital. Most people do not pay anything in cash and do not have much actual cash or savings.

This is the other side of a credit bubble.

Fiat money is not going to go away unless we have a total collapse in civilization and then what will matter is location, food and survivability.

As I understand the reserve currency status it is much more than just a petrodollar it is a legal contract of debt that can be enforced in the US and world courts. The only other currency which a contract could be written where there is an actual viable court system is Europe. But Europe has its problems and isn’t a great choice at this time. Also the Euro doesn’t have a big enough debt pool (float) to cover world trade. You can neither enforce nor guarantee a contract written under either Russian nor Chinese law because under their legal system, you really have no guarantees. And neither system is actually large enough to facilitate world trade. They can trade among themselves but not the world.

Ok, so my response on this point is to look at the SDR (Special Drawing Rights) essentially this will probably become the new world currency/s. It is more of a basket of currencies with a variable float tied to and based on the amount of skin in the game for each country. That skin will likely be based on the gold holdings of each country who is included in it. Please note that China was recently allowed access to this SDR. I am not sure 100% how this will shake out but this will likely be the mechanism for international trade with the super currency status of these notes tied directly to gold. There is also going to be a measure of account where the countries will have to prove their gold holdings and the true amount that the Russians and Chinese will become known. They currently lie about how much gold they really have.

As for past history, the most recent demise of a world currency was the British Pound… There have been many.. You need both a very large float and a reasonable legal system in order for large trades in the world to occur. Either that or the ships have to carry large amounts of something that can be actually traded for something they can trade to someone else. Same reason that doesn’t work is the same reason the barter system doesn’t work. No, fiat currency is what facilitates world trade. You can not do it with PM’s unless they are backing some fiat currency. And that has issues to because of its limited expandability.

Regarding this point the British had a major issue with trade to China. China only accepted silver in trade for silk, spices etc. This was draining the silver reserves in the U.K. so they started sending opium to the Chinese via the Dutch East India Company. Things got a little out of hand (Opium Wars) and the rest of this is history.

And that is why gold or diamonds or platinum nor any other commodity doesn’t work for world trade. It can back a currency but then the value of it in the trading partner’s currency will probably be different. All depends upon each country’s demand..

If you have two buyers and one is paying $100.00 per oz of say silver and the other is paying $1,000.00 per oz the obvious would be selling to the person paying more and buying from the cheaper source. The difference is the arbitrage in the trade. This does not last since they will balance with each other up or down or someone will make a lot of money without any real work other than buying here and selling there.

Buying assets cheap is what I call deflation. To many goods and to little available cash. (Different at the top of the pyramid where there is lots of liquidity. At the top where stocks and yachts are sold, there has been inflation. At the bottom, deflation). And IMO deflation is where we are heading when all this mal invested debt starts defaulting.

To me there has already been a lot of deflation for the lower 90%. Business closures have caused a glut in the related materials and goods. This is evidenced by the various auction sites where you can literally buy stuff for pennies on the dollar. The majority of the QE has gone to the top of the pyramid so to speak so that is also where the inflation is currently showing up. A mere look at the stock market with the ridiculous P/E ratios shows that also with stock buybacks I think the company owners are and have insured their own bailout already at the expense of the companies that they run. The real inflation will happen when the lower 90% start getting that money in their pockets. Rather than stay out of the economy they are more likely to spend that money which will increase the prices of everything (housing is a good place where this shows up). It will also begin in wages as the value of currency decreases and people feel it more and more. Say in something like food it is inelastic but if you only have say $1,000.00 extra for food and stuff, an increase in inflation there is felt more than someone who has millions of dollars to spend. Percentage wise it affects the poor more causing more people to need assistance (we are there already with the 100 million+ Americans on some kind of assistance).

So in the bottom of this Super Cycle, I think we should see lots and lots of debt defaulted upon and lots and lots of re-purposing and re-valuing of assets. Lots and lots of debt will be written off. Most of the TBTF institutions we know will be changed significantly or gone.

This has been ongoing over the last few years. We have been in the pot slowly having the temperature increased but it is hidden. Someone I was watching used the cheeseburger index. I like to look at say Arby’s. Do you remember the 5 for $5.00 well now you might get one sandwich for $6.00. How many dollar menus are still around?

As the dollar is a Federal Reserve Note, i.e. FED debt. The actual value of any cash that remains will actually purchase much more than it does today. The government guarantees on bank deposits will be demanded. In order for the government to actually create this money it will need the FED to massively increase its balance sheet. The FED may not want to do this as much of their existing balance sheet debt may have been wiped out. Leaving this private cartel with debts owed which they are unable or unwilling to pay. The government may then have to do away with the Federal Reserve System which will take time because it is a Constitutional Amendment…

First, the FDIC system is nowhere near solvent to cover the potential losses. There is no chance in hell they will be able to cover all of the deposits currently there. Banking stress tests have proven this already where all of the banks tested failed. The most likely scenario here is the bail in where all deposits, 401K etc will be taken to monetize the banks. Laws are in place for this to happen where you the depositor is considered a shareholder in the bank and the “money” is not even considered to be yours. When brokerages hold funds in overnight accounts those too are considered to be a shareholder of the bank and truly would we expect government to not look at a huge pile of cash and not help themselves to it? Additionally having a current liability sheet of 4.5 Trillion seems like a lot to me already. This is what is set to be unwound in the next few years. The problem being is the assets themselves are toxic garbage that will need a serious write down if it is to be put into the market. Where are the buyers at for all the balance sheet items from the FED? I maintain they are lying about it and will likely continue to support the system. With the electronic algo trading it is very difficult to know how many actual people are in the markets v.s. how many computers chugging away.

And all this will happen rather quickly once the system breaks down. Selling anything to say something will be the trend. Lots of good deals near the bottom.. Then the bottom will be long and painful while institutions and confidence is rebuilt.

And yes, owning gold at that time will be good, IF you can find a buyer. You can’t buy food, pay a mortgage or insurance or the doctor with gold. You will have to sell it and again, once the break down has occurred, the gold you buy today may not be worth in dollars as much then. Any more than a diamond or anything for that matter as there will be few dollars in circulation. Lots of things, few dollars, means good deals for those with dollars.

See to me this is a major fallacy. Gold is money. We have been tricked into thinking it is a commodity. Already in Louisiana, Arizona, Utah etc we are seeing laws being passed recognizing this fact. Also, it is probably the most liquid form of money due to the intrinsic value it has. I have yet to see a pawn shop who does not offer to trade that gold you have for fiats…Certainly things like food, water, bullets and beans are not going anywhere but then again neither is gold and silver.

Remember, most transactions today are via credit or digital. Most people do not pay anything in cash and do not have much actual cash or savings.

This is the other side of a credit bubble.

Credit can be shut off at a moments notice. This is also why I think crypto currency will ultimately fail. A false flag EMP attack or even a real EMP attack would render credit and digital accounts to go adios. I am not sure if something like that is possible but I do know that anything can happen. Cash is one of those things that is dependent on where you live. In the south it seems like everything is in cash…not making this up. There are almost as many pawn shops as there are liquor stores and churches.

Fiat money is not going to go away unless we have a total collapse in civilization and then what will matter is location, food and survivability.

This is true but all things are relative. A crisis will not last forever and on the other end when a currency has been revalued the old dollars will be worthless. Gold or silver will be able to trade for whatever the new currency is. For an example look at what India recently did to their citizens by decree that their Rupee notes of certain denominations will no longer be valid. Anyone turning in more than a certain amount to exchange will be held to account. Indians hold a lot of gold and that makes it hard to keep them completely under the thumb of big brother.

My girlfriends ex husband is Russian. His family sold all of their belongings and were literally on their way to the airport to flee when the Rubble collapsed. They ended up losing everything except for the shirts on their backs because they had sold all of their commodities and only had the fiat currency. Kind of an interesting thing to ponder that when the Ruble took a tumble a few years ago, the Russians who knew what was going on immediately tried to buy anything that was not nailed down. Maybe they know something we don’t.

Hey Roger, good points..

SDR is not an insurable nor a legally binding currency as far as I know. At this point there is not a world government or a world military to enforce contracts written under the IMF’s SDRs. Would the US courts enforce a contract written under an IMF SDR? Doubt it but who knows. I personally hope there never is a world government. An SDR may be some form of interesting liquidity for CB or national governments but when you sell a container of Korean or Chinese made refrigerators to Canada, what enforceable currency do you write the sales contract in? Who will enforce that contract? And SDRs will be a form of debt. Who backs that debt without a world government? Why would the US borrow in SDRs when they can just create their own debt?

The FDIC is guaranteed by the US government.. So unless the government folds, the bank deposits will eventually be paid. The US situation is different. And unless some other insurable contract and currency with a large enough float miraculously appears, the US$ will remain the world’s reserve currency for the foreseeable future.

Russia was not the reserve currency of the world. The Russian government did not have a guarantee on deposits.

At the current time, gold is not money. In general, you can not pay a bill or buy anything with gold.. Not a vehicle, or fuel or real estate or food. Gold may someday be money but I doubt it. It can be converted (sold) to most local currencies but not easily. I always travel with a few ounces of gold as insurance but I have looked and in most countries, even this one, for places to convert, and they are not very accessible and in some areas of the world, not safe. Even when gold was used as currency, silver was more common and probably a better choice for local trade.

And yes credit can be shut off and I think at some point will be or severely curtailed. The pyramid Ponzi finance that is currently fueling corporate, businesses and consumers spending and world GDP growth will fail at some point. Debts that are not invested in anything that will repay that debt will eventually be defaulted upon. That is when cash in the local currency will be worth the most. When revenues can’t support the servicing of the debts, lots of sales will not occur (starting to happen). That is when the dollar will buy the most but then again under extreme fear of such a financial crisis will anyone spend their cash on anything other than necessities? This is the problem with a deflationary cycle which None of us has ever seen and yet is the other side of a debt binge.

I don’t think that our currency will be thrown out, or totally devalued and new currency issued because all the contracts are written in US$. This would amount to a total chaotic break down of our system. It would mean that our government totally collapsed and was rebuilt anew. A New World Order so to speak and if that came, I don’t think anything or anyone would be safe. You surely wouldn’t want anyone to know you had any gold or silver as either the new government or someone would just take it from you.. No government also means no law or law enforcement. I sure hope we never devolve to that level..

What you think might happen I believe is extremely unlikely. I think that the most likely scenario is that the value of gold and silver will fall along with all other assets when the debt binge finally collapses because in my mind, in the end we go back to basics which is supply and demand. When a finite supply meets a severely diminished demand, prices will collapse.

The only way that the government could prevent this would be not only to print (create) dollars and to actually get them into circulation. That would mean direct deposits or major tax reform for the working class… which pays most of its taxes in the form of SS taxes. For them to do more of what they have done in the past, create dollars has led us to this point of near failure. Any funds need to go directly to Main Street not Wall Street.

One workforce participation rate and the collapse of retail are showing how poorly this their plan isn’t working. Also the Velocity of Money charts at the FED show this..

They would have to get around the laws enabling the FED to just print money outside of creating debt. They can’t just create money out of thin air under the current laws. All they can do is just create more debts no one can service. And then what, sell it to themselves, like they are doing? Total insanity IMO. Not sustainable.

Interesting dilemma. Will we become an Argentina? As the worlds reserve currency? Will the entire world trade break down? There is no one able to step up as all countries have followed the US down this rabbit hole. What worries me that this could be a set up for a world war and a collapse of our way of life. At a minimum, things are changing fast and no one knows where all this will end up..

You’re betting that gold will be your survival mechanism. I have some and land and gardens and solar power and… Not what I was imagining for my golden years though.

Not sure if I can include links in here or not but this hopefully puts what the FDIC has v.s. what it is supposedly insuring into perspective. Warren Buffet called derivatives “Financial weapons of Mass Destruction” for a reason. I believe the current world wide derivatives exposure is somewhere between 1.5 and 2 quadrillion dollars so 1,500-2,000 Trillion. We had better start printing those Trillion dollar Zimbabwe bucks if we want to have any hope.

http://demonocracy.info/infographics/usa/fdic/fdic.html

It might be interesting for you to watch the series that Mike Maloney put out called the “Hidden Secrets of Money”. It is very well done and makes some of this stuff easier to understand.

In my opinion the information everywhere is obfuscated on purpose and by accident. In America we are not taught about money or monetary systems at all unless you learn about it yourself or go to a school to learn. Even then it is an unbelievably deep topic with conflicting opinions and ideas a lot of which have been postulated about but some have never been proven. Ron Paul for instance has been talking about this stuff since the 1970’s.

The thing that amazes me more than anything else is how long they are able to hold this stuff together and make it work. Pundits who study this for a living are routinely proven wrong when they try to apply the *when to the equation of what will happen. Like all fiat systems though, it will eventually collapse and I think people will be blindsided by it when it does.

In 2007-2008 I was working along and had no clue about any monetary policies, the FED or anything else. Then one day Bear Stearns and Lehman went tits up and they are talking about tanks in the streets if the TBTF banks were not “bailed out”. The next time around it will be a “bail in” not unlike Cypress and now two Italian banks in the last month or so.

Direct market intervention by printing prosperity never works, history proves that over and over again. First the coinage of the country suffers by debasement of the actual value of the coins. We saw this with dropping of silver from the coinage in the 1960’s and 1970’s and Nixon closing the gold window in 1973. Remember those silver and gold certificates anyone?

Gresham’s law

In economics, Gresham’s law is a monetary principle stating that “bad money drives out good”. For example, if there are two forms of commodity money in circulation, which are accepted by law as having similar face value, the more valuable commodity will disappear from circulation.

The penny had copper removed from it in 1982 and again Gresham’s law took hold. You can buy older coins and copper coins but the value is based on the intrinsic nature or “melt” value for the same.

Ultimately the system will work until other countries decide they no longer want monopoly money for real products. If it takes no effort or labor but the stroke of a keyboard key to “make money” how much value does that money really have? The only way to keep that type of system alive is to force those countries to sell you products and exchange them for your debased currency. That sounds an awful lot like slavery to me and it has worked as long as we can beat the country with our military.

The problem arises when you come up against a country you cannot beat like China, Russia and possibly Iran. Who knows maybe I am way off base on this but I find it interesting that all of the countries who try and bypass the dollar in trade (BRICS) end up becoming the enemy.

https://goldsilver.com/hidden-secrets/episode-1/

Part one only but you can watch the others at his website.

Roger, I don’t think it odd at all that our biggest real competitors for world domination are not our friends.. why would anyone think they would be our friends? The best they can be is the enemy of our enemies and thus an ally.

Again, in our system money is created thru creating debt. It is not printed as in Zimbabwe. It can still cause inflation but it is not the same as the inflation of Zimbabwe or Wiemar Germany. Under the FED inflation is in the rise of asset values. This can and does trickle down into the inflation that we all feel but when it gets to much, sales die and things start to unravel (as in what is currently happening). Why this distinction is so relevant is because when the debts collapse, as I think both of us believe they will, then the other side of the balance sheet also disappears.. as in that monetary value.. And cash will be rare.. Or cash that is outside the debt pyramid.

This country has not seen real deflation since the 1930’s. This pyramid of debt is much greater than then and I wonder how hard and how destabilizing the unraveling of this Ponzi finance will be. Once it starts, people will try and sell anything and everything in order to preserve something.