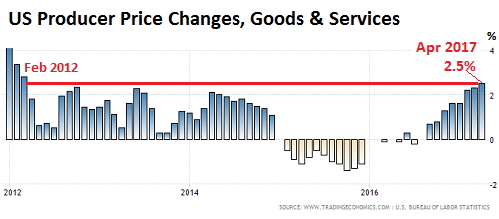

Inflation pressures further up the pipeline rise the most in 5 years.

The Producer Price Index, which measures inflation at the wholesale level for goods and services, and thus up the pipeline from the Consumer Price Index, jumped 2.5% in April from a year ago, the steepest increase since February 2012, blowing past consensus expectations of 2.2% (chart by Trading Economics):

On a monthly basis, seasonally adjusted, wholesale prices rose 0.5% from March. Nearly two-thirds of that increase was due to services, the biggest part of the US economy, where prices increased 0.4% from March. Among the standouts, services less trade, transportation, and warehousing, jumped 0.8% from March.

And it wasn’t “food and energy”: the PPI without food and energy (“core” PPI) jumped 0.7% from March, its 11th month in a row of increases. It’s up 2.1% year-over-year. Back in March, it was up only 1.7%. So picking up momentum.

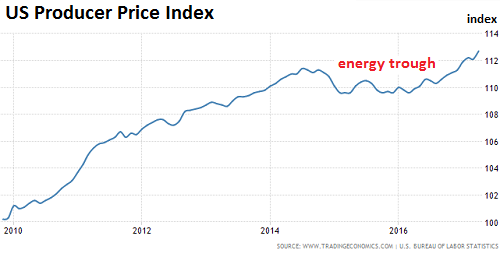

The Producer Price Index reached a new all-time high in April of 112.7 points. In the chart below by Trading Economics, note the big dip in late 2014 and through 2015, caused by the collapse in energy prices. While energy prices have increased since then, they remain much lower than they’d been through mid-2014, with crude oil still down 55%. But the rest of the wholesale price universe, particularly in services, has more than made up for it:

Wholesale price increases are price pressures that are building up in the pipeline and are filtering down into consumer prices with some delay. The Consumer Price Index is already up 2.4% from a year ago.

Today’s data adds to the basket of data points the Fed can use to justify its policies. It already brushed off the economic slowdown in the first quarter as “temporary.” Given how bad that slowdown was, it makes sense to expect the second quarter to look better in comparison – hence the sort of a rebound that would validate the “temporary” nature of Q1’s slowdown.

So more and more of the pieces are falling into place, outside of some “temporary” setbacks, for the Fed to pursue its path, not only to further raising its target rates but also to begin unraveling QE. And they’re stepping up to their pulpits and preaching it. We can ignore the few hawks on the FOMC. It’s the doves that matter when it comes to tightening. When the doves are squealing for tightening, it’s happening.

Just yesterday, Boston Fed Eric Rosengren exhorted his FOMC members to raise the federal funds target rate three more times this year, so to a range of 1.5% to 1.75%, and start unraveling QE by shedding some mortgage-backed securities and Treasuries. He wants to see “a gradual reduction in the balance sheet,” he said, to avoid an “over-hot economy.” All of this, “assuming the economy evolves like my forecast envisions.” Since last year, he has been worried about asset prices, and has specifically named the commercial real estate bubble and what it could do to “financial stability” with increasing intensity (here in March).

And today, it was New York Fed president William Dudley who observed that, based on the economy being “pretty close to full employment,” and inflation being “just a little bit below our target of 2% if you look at the underlying trend,” based on the Fed’s favorite core PCE inflation measure, “we are going to want to gradually remove monetary policy accommodation.” That includes not only raising rates, but also beginning to unravel QE “sometime later this year or next year.”

The Fed keeps its eyes riveted on the markets. It doesn’t want another “Taper Tantrum.” What it sees is that the stock market is ignoring it. Bonds with longer maturities are ignoring it. Junk bonds are ignoring it. Risks still don’t matter. The reach for yield continues. Asset prices are sky-high. In short, investors are ignoring the Fed – that’s what it sees, which is one more reason for the Fed to continue marching to its tune, though if markets get crashy, it could change its mind in a New-York-Fed minute.

So clearly, it’s not all careening downhill, at least not for everyone. “The new 1%” of the S&P 500 stocks gained $260 billion since March 1, while the 99% of the S&P 500 lost $260 billion. Read… “The Great Narrowing” of the S&P 500

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Never fear, Aunt Janet will find some reason to wait. It may not make sense to you or me, but then she doesn’t have to make sense to us.

Its a shame she (the fed is not elected by the people every 4 years ) that way she would keep her job based on the democratic majority 1 man 1 vote

Fact Check ; The US is not a one man one vote democracy nor have we ever been . Not even close . What we are is a representative Democratic Republic .. with over the last six years the emphasis being placed on the Republic … rather than the Democratic side of the coin .

FYI; The only truly democratic country … e.g. one man one vote.. is ….

Switzerland

Surprised ?

Yes!

The Fed is a criminal private banking cartel accountable only to its oligarch patrons and accessories.

Normally, I would say ‘Yes’, especially if Hillary or little Marco won. Since Trump won, I think the criminal enterprise of eventual negative rates is on hold and rates may rise due to FOMC decisions and balance sheet reductions. God, I hope. I hope he knows how to keep them gutless and obedient for a lot longer.

How’s the democratic stuff been working out for the last 30 years?

Just because you have a vote does not mean the country will go towards a better direction. Tons of third world countries are democratic too. And heck the US is heading towards third world country designation.

That would lead to financial collapse in short order, as the masses would do as they did in November, vote with their wallets.

What is good fro the wallets of the masses, short term (which is how the masses always vote(The inherent flaw in the current form of Democracy)) is not good for the Nation, long term.

Michael Belkin believes the fed will completely turn tail and run. But I hope they do raise rates as it will turn out to be very bullish for my mining stocks.

Money will become unaffordable. Too expensive.

US Federal tax receipts $2.14 trillion.

Current debt service @ 2.2% cost $432 billion.

This is at the current debt level.

When rates reach 6.2% the debt service balloons to $1.23 trillion.

At this point its game over, when your cost outstrips receipts.

To prevent this? The only remedy will be massive printing.

Inflation is a matter of price. Hyperinflation is purely a currency event.

This is a common misunderstanding. The treasury doesn’t get tax receipts and spend it on debt service. The federal government simply credits its cash account at the Federal Reserve for the monthly nut and debits various bank accounts of its creditors. When taxes come in, it debits its cash account and credits the accounts of tax payers.

The federal government’s account at the Fed always runs negative. And it is designed to do that. It’s basically a check kiting scheme with no penalties. Periodically, the Treasury will issue bonds to make up for the difference. The “debt” will go up, but it is never a problem to pay for it because the Treasury essentially has an infinite amount of money.

Taxes serve a different purpose: to absorb money out of the real economy to reduce the inflationary effects of government spending, and to give value to Federal Reserve Notes (you have to have them to pay your taxes, so you better give them some value).

This explanation is simplified, but the federal government cannot cause hyperinflation because it sterilizes all of its expenditures either through either taxation or through the issuance of bonds.

Banks are a whole different animal.

Kent,

thanks for your lucid explanation of Treasury/Fed accounts and purpose of taxation. Do you have some references for your explanation…it would be useful for many of us to understand this better. If the purpose of taxes is to pull excess money out of the economy to reduce/prevent inflation, that would appear to be a good argument for reducing taxes on the middle class and raising taxes on the upper class as the middle is not keeping up with inflation.

I don’t think I would find information to link to on this. I promise to look, but it isn’t something that fedgov wants for general distribution. If you spend time considering the implications, you’ll understand why. If you spend that time and don’t understand, back off from discussing these topics.

Who gets income from federal spending versus who pays the taxes is what politics is all about. Obviously the best situation is to receive income from the Feds but pay no taxes. Figuring out how to make that happen is well worth the effort.

But don’t think a very large group of very wealthy people haven’t understood this for decades. Competing at this point for the funds is ridiculously difficult. And the fact the average American will never understand how the system works makes change essentially impossible.

Wha…?

“to reduce the inflationary effects of government spending”???

“cannot cause hyperinflation”???

“Treasury has an infinite amount of money”.

Yes they do and when they add it to the current supply, they “inflate” the amount of that supply.

Everyday, common inflation is always a matter of price.

Hyperinflation is purely a currency event, brought about by government when they inflate the money supply beyond support. Remember, a bond is nothing but debt by another name.

The first rule of economics is;

All debt will be paid. Either with dollars worth pennies, or with pennies worth dollars. It will be paid.

Read some history covering the hyperinflation

event that occurred in Germany (1919-1923) and what caused it.

A few thoughts:

1. Think of it this way: the government spends a billion dollars. The economy now has a billion dollars more in the economy. Then the government taxes back $800 million. The economy now has $200 million more in the economy. Then the government issues a Treasury bond for $200 million. The economy is back to no change. This is the normal sterilization system. It works. But:

2. Suppose the Fed creates $1 billion in new currency and buys $1 billion of Mortgaged Backed Securities from some sleazy bank. In reality, the Fed moves the new money into the banks reserves held at the Fed, and the Fed moves the bonds onto its own balance sheet. Banks don’t lend reserves, but in a fractional reserve system, the banks can now lend more because they have higher reserves. This is inflationary in things banks like to lend on: assets.

3. The federal government doesn’t really have debt in the sense that a person does. If I have to pay debt, I have to forego some other purchase in order to make the payment. That’s why debt sucks. The federal government never has this problem, so they don’t care. That’s what VP Cheney was saying when he said “debt doesn’t matter”. We shouldn’t use the word “debt” for federal obligations. It’s misleading.

4. Weimar Germany was forced to pay war debt in a foreign currency: gold. The USA has to pay in its own currency. Using a foreign currency is truly debt in the personal sense. Using your own can’t be a problem as long as you’re forced to sterilize it. That is why Weimar or Zimbabwe aren’t relevant examples.

Kent. I’m sad to say that I do not find your explanation informative at all. Not even sure what you are trying to say when you say

“The treasury doesn’t get tax receipts and spend it on debt service. The federal government simply credits its cash account at the Federal Reserve for the monthly nut and debits various bank accounts of its creditors.”

Apart from using confusing colloquialisms such a “nut”, I’m not sure what the above paragraph is supposed to explain, nor whether it is even correct, whether in a colloquial or technical sense.

An easier explanation of what Kent is saying…. The USD isn’t backed by anything except more USD/Treasuries. So the Federal Government isn’t exchanging anything like Gold or Oil for USD, instead you get more USD/Treasuries and they can add those at anytime. So what if the US Government now owes 220 Trillion and interest is a trillion a year. Nothing prevents them from adding more numbers on their balance sheet.

If the dollar looses its world currency status, it will have to exchange something else like SDRs. At this point, collateral has to be exchanged to buy SDRs. Now interest rates COULD kill the US because it can print all it wants in the US, but not SDRs. Then again it will probably just try to bypass this mechanism and declare war on everyone else.

Justme,

I apologize for using accounting lingo and colloquialisms. The term “nut” means debt payments like a mortgage.

Let me say it differently. Suppose you are the treasury. You have two accounts with your bank: a standard checking account and a debt payment account (where your debts are recorded and payments are made).

1. You are required to pay people stuff. Buy guns, tanks, welfare payments etc… So you start writing checks. But you don’t have any money in your checking account.

2. Being the federal government, your checking account balance can go negative with no overdraft penalties. So your account goes negative very quickly.

3. And the economy has lots of new money in it that is inflationary.

4. Congress tells you to tax some people and things and put the money in your checking account. You begin doing so and your balance becomes less negative.

5. At the end of the quarter, you look at your still negative balance and you “borrow” the difference. Now your account is in balance, but you have an outstanding loan you have to pay back.

6. The new money originally put in the economy is sterilized. It has all been put back into your checking account, so there is no threat of inflation. But:

7. You now have to make principal and interest payments on the money you borrowed. Don’t you have to raise taxes to make that payment?

8. No, though you can if you want to. Prinicipal and interest are just another payment. And your checking account can go negative infinitely. So you will just write another check. If that increases taxes or future borrowing is purely up to you.

9. Japan has been doing this for a long time and there “debt” is way more than anyone else’s in the world. And it doesn’t hurt them a bit, because they use the same sterilization system as the US.

@Bandini,

The US dollar is backed by 2 things:

1. The wealth of the population of the nation. Meaning that you can exchange dollars for the property of the American people.

2. The conservatism of the American people to not allow long term debt monetization.

3. The willingness and capability of the federal government to use violence to impose its will on the population to collect taxes, and as you mention, the will to impose violence on the international community when it seeks to use something other than dollars for the exchange of certain valuable items.

Kent, I’m still not satisfied, and I doubt I will be. You say a lot of stuff, some of which is somewhat correct and a lot that is just not correct. What is correct I would just say as follows:

The USG has not for a long time, maybe ever, PAID DOWN any interest and principal. USG just rolls over the principal into new debt and adds some more debt to “cover” the interest.

See how easy that was? No contorted analogies, imaginary accounts, or anything like that. Just a clear and simple and CORRECT explanation.

Now, about the stuff about which you are severely incorrect. You claim that the government runs a negative account balance for each quarter, and then refills it from debt at the end of each quarter. I don’t think that is correct at all. The following shows the balance of the UST general account at the FRB. The data goes back to 1986 and the balance has never been negative.

https://fred.stlouisfed.org/series/WTREGEN

In other words, whatever defcit spending the USG engages in, it ALWAYS issues the debt BEFORE it spends the money.

I like keeping things simple and correct. I do not like contorted “explanations” that are either, well, contorted, or just plain wrong.

What happens when no one wants to buy US Government Bonds because the government spends way more than it can reasonably tax the citizens?

Then FRB buys the bonds instead, via the primary dealers. That’s called debt monetization.

If nobody wants to swap their currency for bonds, that implies that they’re happy using the currency that they have … spending, investing … That implies a healthy economy, and that’s a good thing.

Bonds versus taxation is a moral issue. If I tax someone I’m taking their money. If I issue bonds, I’m taking their money but giving them an interest bearing security in return.

The more you fund the government with treasury bonds, the more your freeing the population that has investable capital from having to pay taxes, while a greater relative burden falls on those with less capital.

Hence “tax cuts for the rich” really means the government still gets the same amount from them, it’s just that a greater portion is returned in the form of treasury bonds.

Jeebus Christ, Kent. Another whopper of a falsehood from you. You are claiming that taxing the rich is equivalent to NOT taxing the rich, because the USG will then borrow the untaxed money from the rich anyway.

But there is MASSIVE difference between the two cases. Is it not glaringly obvious that in the cases of taxation the public does not incur any debt, whereas in the case of borrowing we incur debt and it costs interest.

Kent: “because the Treasury essentially has an infinite amount of money.”

Given this, if the buys US T-bonds/prints $$s infinitely, what will happen to the value of the currency? Clearly it would decrease, and as you approach infinity it would approach zero. That is a hyperinflationary event like Weimar or Zimbabwe. Since the USD is a reserve currency the US has been conveniently able to avoid this result to date even with massively undisciplined debt spending. The national debt financing is a large component of the US Federal budget, and if interest rates rise in step with these inflation numbers, which is part of the definition of nominal i rates, US national debt financing will also rise consuming more precious budget room. This will encourage the Treasury/FED to print even more, as it represents a political crisis (this can be clearly seen in the current US political division), exacerbating the problem, and making the infinite supply of money you reference, go further and further down the bound to zero value.

Do you rrally think the FED has a handle on this?

I think we’re headed toward combinations of deflationary episodes (Great Depression, Great Recession), interspersed with inflationary events (that may be starting now).

Certainly one huge inflation has been the massive stock and real estate bubbles artificially inflated by easy FED money.

I don’t think the FED’s been through these waters before, and I think like the BOJ, there are no easy answers for them, no less because they are controlled by the large private banks, and not truly to do what’s good for the American people.

New higher oil prices will make sure that inflation will keep rising.

Until we will enter a recession.

At that point oil prices will not osc. like in 2008.

It will stay high, will not be affordable.

Michael And if that’s true we will be screwed as we haven’t taken the opportunity given to us by low oil prices over the last three years to establish a decent rail system in this country Unfortunately

How did you arrive at your prediction of higher oil prices that will stay high and not be affordable?

The following is from RealClearMarkets today:

“After having crashed over a period of several years, hardly transitory, oil was supposed to make something of a straight line back toward, if not over, $100 as if the whole thing never happened. When it (WTI) reached $50 again relatively quickly by early June last year, it became common to hear that this level would be a floor for which further price increases would surely follow.

Instead, oil has stalled, trading mostly sideways ever since, with a downward rather than upward bias. It seems as if $50 has been something of a ceiling rather than a floor, with the risks “somehow” all remaining to the downside.”

ref: http://www.realclearmarkets.com/articles/2017/05/12/just_as_in_the_1930s_liquidity_preferences_still_rule_102683.html

“New higher oil prices will make sure that inflation will keep rising.”

Short of a major Middle Eastern conflict– as in, Iran vs. Saudi Arabia– this is a pipedream.

Its been reported that as much as 80% of NYSE trading volume is done by investors using algorithms to select stocks. If true, I wonder how much of that volume is transacted in the 5 one percenters?

‘Digital money’ has made all the talk about the M’s and debt levels irrelevant.

Traditional market place price discovery and asset pricing have no real foundations anymore.

The con games being played in the precious metal markets have resulted in gold and silver losing their traditional role. They don’t work anymore.

And as far as crude oil prices are concerned IMO the POO is going down, will stay down for a long time, and not go up until a huge number of projects are cancelled, demand outstrips supply by a large enough number to reduce the huge built up stockpiles in various countries and floating on ships around the world.

The current US stock of crude and products is the highest it has ever been and is over 2 billion barrels. In reality the small 5 million barrel draw this week is meaningless. Hype and nothing more. Oil is in huge oversupply.

If that has any impact on the price of gasoline who knows – it sure hasn’t here in Australia. You’d think by looking at prices and recent movements that the POO was near all time highs.

Of course all that would change if there were to be some type of black swan event such as a major Saudi oil facility being taken out……….

“‘Digital money’ has made all the talk about the M’s and debt levels irrelevant.”

Except for counterparty risk. Debt is not irrelevant. And we can’t easily accomplish debt jubilee. How will this look, some 4,000 years after Leviticus 25 was written?

Ignore the incessant jawboning of Yellen’s flying monkeys at the Fed who are trying to talk up the dollar and suppress the price of gold. Come the next Fed meeting, Yellen will once again resort to her played-out “Lucy and the Football” routine of more mumbled incoherent excuses why she can’t raise rates just yet despite the economy supposedly booming. Bilking savers out of interest income and forcing them to play in her Wall Street accomplices’ rigged casino is too lucrative a racket for these grifters to give it up voluntarily.

Remember, the Fed raised rates 3x at every other meeting (Dec, Feb, Apr). The May meeting was the off-meeting. The June meeting is on schedule to be the on-meeting. June will then be the fourth time in 8 meetings that the Fed raised rates. That’s the track they’re on for now.

The Fed could also use a “monetary shock” – such as a 50 basis points increase – to get people like you (and the whole market is full of them) to become believers. I’ve seen this before :-)

I’ll believe it when I see it. You seem to think the Fed will act like a responsible central bank. I think they’ll keep perpetuating their swindles against savers and the responsible until the bond vigilantes force Yellen’s hand.

Always remember that as insane as US Federal Reserve policies may look like, they are a bastion of common sense and integrity compared to those originating from the European Central Bank, Rijksbank, Banque Nationale Suisse, People’s Bank of China, Bank of Japan and many others.

Have you considered that the FAAGNS via cheap FED money have accumulated worth closing in on domination and control of the economy?

I think this more than anything else may be scaring them. That unexpected event that they have lost control of….the last thing the FED would stand for is loss of control.

A 50% increase in a few months of ‘worth’ is a loss of control.

Whats the maturity dates on the Non treasury section, of the FED balance sheet. (is that data available?)

A big lump, not rolled over, would justify a longer period of no rate rise, as it has the same effect in the system as a rate rise. And would throw the liquidity side of the market a curve ball.

Data on the maturities of the Fed’s balance sheet is out there, but I don’t have it at the tips of my fingers without some digging. With $3 trillion in securities on their balance sheet, there are large amounts maturing all the time. Currently the Fed buys bonds and MBS to replace the ones that mature. The purchase data is also available; it gives you an idea how much is currently rolling off and being replaced. Here are the last 25 transactions:

https://apps.newyorkfed.org/markets/autorates/tomo-results-display?SHOWMORE=TRUE&startDate=01/01/2000&enddate=01/01/2000

“Currently the Fed buys bonds and MBS to replace the ones that mature”

There was talk that the FED was only going to continue replacing Treasuries and not replace maturing MBS. And had on several occasion already done this in its balance sheet amendment program.

We haven’t as yet noticed any major change in sheet size or types of items on sheet. Like you say it’s 3 T anything under 100 B is a rounding error.

The FED remits its profits to the treasury.

If the FED ended up with a huge cash mountain, that it wanted to disperse, after selling all or most of its MBS, like a normal bank, this would also in the case of the FED go to Treasury not its Shareholders??

If the FED sells all those Qe MBS, eventually it may end up in such a situation.

Or would it simply sit on the cash, ready for next time it was need?

The way the Fed works is not like you and me. To buy bonds (during QE), it creates money by sending credits to is primary dealers’ accounts; in return, they send securities to the Fed for these amounts. When these bonds mature and are redeemed by the issuer, the process reverses; those credits come back to the Fed and just disappear. The Fed doesn’t sit around on them as cash. So the balance sheet will shrink on the asset side and the liability side by equal amounts of the redeemed bonds.

The Fed can always create more of these credits, so it doesn’t need to sit on cash.

Stupid me.

I forgot the issue of the Shareholder Banks and Bond Sellers accounts at the FED. Where the FED creates the money to buy the notes in the first place.

Just a general banks create money when making loans.

Must have been late in our night when I wrote that.

Thank’s for your tolerance.

The “markets” are calling BS on a rate hike in June. So am I.

The Fed, as the oligarchy’s chief instrument of plunder against the 99%, won’t raise rates unless/until their Goldman Sachs handlers go massively short, then order their albino hobbit at the Fed to jack up rates & implode the Wall Street-Federal Reserve pump & dump.

http://www.zerohedge.com/news/2017-05-11/betting-against-june-rate-hike-somethings-going

That’s EXACTLY what I’m saying. Re-read my above paragraph again. It says:

“The Fed could also use a “monetary shock” – such as a 50 basis points increase – to get people like you (and the whole market is full of them) to become believers. I’ve seen this before :-)”

“Remember, the Fed raised rates 3x at every other meeting (Dec, Feb, Apr). The May meeting was the off-meeting. The June meeting is on schedule to be the on-meeting. June will then be the fourth time in 8 meetings that the Fed raised rates. That’s the track they’re on for now.”

But do you really believe in the “track”? I mean, apart from the them remaining below “track” for the last 8 years, I don’t know why you all of a sudden would give their supposed pathway credibility.

“The Fed could also use a “monetary shock” – such as a 50 basis points increase – to get people like you (and the whole market is full of them) to become believers. I’ve seen this before :-)”

To believe what? That they’ll follow through on their threats to raise rates, or that the economy is legitimately strong enough to justify rate hikes? Because apart from Wall St sycophants who cheer every piece of mediocre economic data we’ve gotten over the last decade as if it represented something resembling strong growth, they’ve lost all credibility on the latter front.

They can raise rates all they want. It will simply hasten the next economic or market shock, whatever that may be– at which points rates will be coming back down again. What does it accomplish apart from establishing that A) they will, very rarely, keep their word and B) they are totally incompetent in managing interest rates relative to the strength, or more accurately, weakness of the underlying economy?

I would also point out that, while you are talking about PPI, Core CPI went down… lowest since 2015. So the Fed would have to cherry pick their inflation point to justify rate hikes– something I wouldn’t be surprised to see them do, but nonetheless the data is NOT all in their favor.

OK, four things:

1. CPI = 2.2% and core = 1.9% pushed down a smidgen by falling used car prices… which I’ve been talking about for months… for the Fed, that’s not an obstacle but part an oversupplied market. When you look at the monthly change, core CPI was actually UP sharply from March…. so going in the right direction, as far as the Fed is concerned.

2. I’ve called the Fed “flip-flop Fed” throughout 2015 and most of 2016 – and for very good reasons, as we all recall. But in November, everything changed. Overnight, the Fed became a different creature. Now it’s on a mission. I’ve pointing this out, and so far, that has been correct.

3. No one knows for sure what the Fed will do a month from now. We’re all just guessing, based on how we read the evidence. I think it’s important for me to point out the change in the Fed’s demeanor, after having called it “flip-flop Fed” for about two years.

4. The Fed is now concerned about asset price inflation and the damage this can do to lenders (which it regulates) when prices go down sharply from very high levels. It doesn’t want to increase the risks associated with asset price inflation, and it doesn’t want more asset price inflation. It has been pretty clear about this. So a few squiggles in CPI or in GDP aren’t going to make a lot of difference for the Fed. Its eyes are elsewhere. It raised rates three times since December, even though GDP last year grew only 1.6%.

I wonder if they plan on driving up rates, then selling those steeply discounted low-rate (functionally non-callable) treasuries to a specific group of people?

Say, a group comprised almost entirely of themselves?

The only way it would funnier is if the Fed loaned the purchase money to the buyers of those discounted treasury bonds at zero (or even negative) interest.

>>The only way it would funnier is if the Fed loaned the purchase money to the buyers of those discounted treasury bonds at zero (or even negative) interest.

That worked once already in 2008-2013, with QE 1-2-3 providing payment at par (face value) for bad mortgage bonds (MBS) so that banks and hedge funds could turn around and buy the very same houses that were backing those MBS at steep discounts. It doesn’t get any better than that if you are a bank or large bondholder. Of course, everyone else, including taxpayers and depositors, lose.

One way to execute the scam this time around would be to let big stockholders sell their stock to the FRB at high values, (QE4) and then let them turn around and buy the cheap bonds. Then reduce the interest rate again, and PROFIT! on rising binds again. Yeah, baby!

Do you really believe a 25 or 50 basis raise will get anyone’s attention? They created the zombies.

Too much monetary “value” tied to assembled concrete, steel, and glass done ad nauseum. And into electronic numbers they call stocks. Do those things contribute anything real to advancing mankind? Virtually nil. But too bad that everyone from all over the wealth spectrum have no vision whatsoever other than acquire more paper currency other their peers.

Looking at that price index over the past 10 years one cant help but notice the masive theft that has been perpetrated on the savers with negative interest rates bu unleceted bureaucrats at the Fed. Shame.

Operating with very low interest rates distorts the entire economy. It was deemed a necessity to keep things from imploding after 2008. Whether it was a necessity or not is debatable.

That said, the Fed does want to normalize as much as possible. I think the days of 6% on the 10 year are long gone. But another 1 to 2 % from current may suffice.

Remember, lots of economic foundation players like insurance companies and others depending on safe yield have been getting killed with ZIRP. The Fed knows that and so they have to act.

What will be interesting to observe is the near total shutdown of the economy depending on cheap money. So they are painted in a corner and trying to step out but the paint may not be fully dry yet.

“Remember, lots of economic foundation players like insurance companies and others depending on safe yield have been getting killed with ZIRP. The Fed knows that and so they have to act.”

Many have adjusted their asset allocations to be more risk-seeking as well; if the Fed raises rates and the market tanks, what good does having 1 or 2% higher yields do? Like you said, they’ve painted themselves into a corner.

The US dollar is in demand not necessarily to buy US produced goods and services but to pay down debt dominated in US dollars and issued by non US entities. This results in a strong relative value of the dollar compared to other currencies. US producers of goods and services cannot compete with producers in other countries because of this. Trump believes or appears to believe that the problem is trade when the real problem is the US dollar and the multitudinous uses that generate demand for it globally. The possibility of coming trade wars won’t solve the problem because you can always devalue more, an option the US doesn’t have. The only lever available is maintaining very low interest rates in the US and relying on the cheap imports from other countries to keep inflation low. It also has the effect of keeping costs low in the US which is clearly an unhappy consequence which many Trump voters are aware off. The impact of much higher short term interest rates will not be benign for asset valuations, politicians faced with higher borrowing costs, the strength of the US dollar, or other countries that have borrowed heavily in US dollars. This is why I do not expect an aggressive attempt to raise US short term rates.