That trade was just waiting to unwind.

On Tuesday, the dollar fell 1.25% against the basket of currencies in the Dollar Index. The index is down 3% since its peak at the end of 2016. US companies that report in dollars but have sales and income outside the US in other currencies – which is much of the S&P 500 – love this. When they translate their foreign-currency revenues and earnings into weaker dollars, they get to show more dollars.

US consumers have benefited from the “strong dollar” because it kept a lid on price increases of imported goods and made overseas vacations more affordable.

But for companies, the “strong dollar” has been a common complaint during earnings calls since it started rising in mid-2014, when the end of QE Infinity approached. From April 2014 through its peak in late December 2016, the Dollar Index soared 32%. Global US companies have lamented this rise every step along the way.

So, by this logic, the dollar’s sharp drop on Tuesday should have caused stocks to surge. But they sagged.

In the media, the dollar’s tumble was presented as another Trump communication accomplishment. The dollar was “too strong,” he’d told the Wall Street Journal. “Our companies can’t compete with them now because our currency is too strong. And it’s killing us.”

There was even some head-scratching how Trump dared to say something like this, abolishing the official “strong dollar policy” of the past few decades, when in fact it had been abolished in all but name long ago, and for all to see. But there’s more to it.

The dollar has become a global magnet after the Fed started tightening – raising rates and even talking out loud about reversing QE and reducing the assets on its balance sheet – while other central banks are still buying assets and maintaining policy rates below zero.

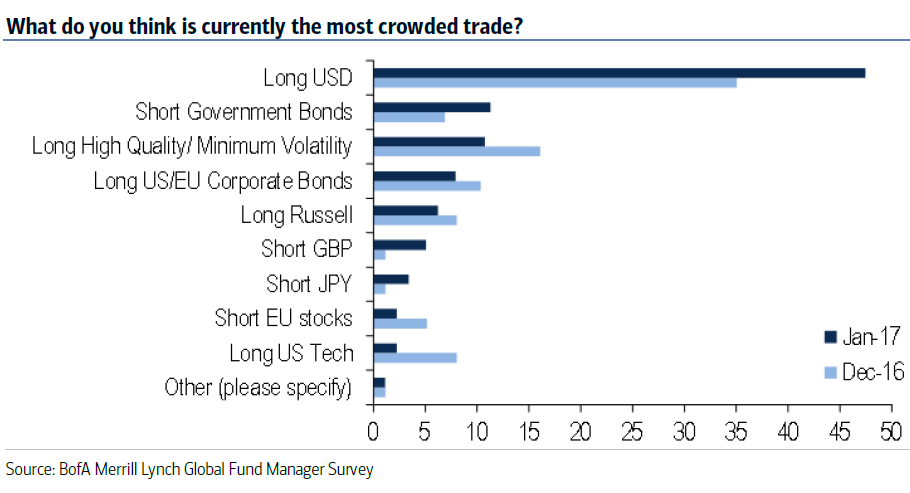

Everyone piled into the dollar, and it has become the “most crowded trade,” according to a survey of fund managers by Bank of America Merrill Lynch (more on that in a moment). And that “most crowded trade” was just waiting to unwind. In fact, it was already unwinding over the past two weeks. And now that that another spark has been delivered, it fell a bunch more:

So as folks scrambled to find the exit, the “most crowded trade” – long the USD – got a little less crowded.

Nearly half (47%) of the fund managers that participated in BofA Merrill Lynch’s survey for January called the dollar the most crowded trade, far ahead of the next trades in line. Here’s their chart, via Christine Hughes, Chief Investment Strategist at OtterWood Capital. Note how the perception of “crowded” jumped for the dollar since the prior survey in December:

The second most crowded trade, but lagging far behind: shorting government bonds. That trade too has gotten less crowded recently, as prices have risen and yields have fallen, putting a nerve-wracking squeeze on these short-sellers for the time being.

When a trade gets crowded, any little thing can serve as an impetus to get everyone to run for the exit at the same time, and it can cause a sudden unwind of that trade. But the trades of being long the dollar and short government bonds began unwinding over two weeks before Trump pulled his magic trick. Even if the dollar recovers, it might not surge much more, given how far it has already surged since 2014. People get edgy at these lofty levels and start unloading.

But US Treasury yields will likely resume rising. Yields had surged far too fast since the election and needed a big break. But that break might be about over.

Incidentally, if Trump continues to successfully talk down the dollar, it will relieve the Fed from having to worry about it. The “strong dollar” has been an issue with the Fed, and they’ve been keeping a nervous eye on it while tightening monetary policy. At some point, the Fed would try to push the dollar back down, either by jawboning it down, or by loosening monetary policy.

If Trump takes over the task of jawboning down the dollar, the Fed can raise rates further, and faster if it wishes, as some Fed governors have suggested. It can even allow some of the securities to roll off the balance sheet when they mature and thus shrink the balance sheet, as other Fed governors have suggested. And that would most likely cause long-term rates to rise, which would soothe the wounds of the beaten-up short-sellers of US Treasury bonds.

So what could a bond-selloff look like if it takes on momentum? Worse than the 1994 “Bond Massacre,” with “sustained double-digit losses on bonds, subpar growth in developed markets, and balance sheet risks for banking systems.” Read… How Bad Will the “Bond Massacre” Get?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I think you gave too much credibility to Trump as if he is the God of Finance. Most people only see straight line not like cycles. For instance, Plaza Accord was one of the events where other G-5 nations asking the U.S. to devaluate the dollar because it was too strong and it hurt they debt financing activity and subsequent followed by the Ruble debacle. Look at Kondratiff’s work. Seasons come and go.

The knowledge that currency rates reflect trade deficits and surpluses is mostly obsolete.

Jim Rickards

“US consumers have benefited from the “strong dollar” because it kept a lid on price increases of imported goods and made overseas vacations more affordable.”

Do these imported goods provide jobs and income which enable consumers?

no that’s the point. ordinary people gain as consumers but lose out as workers – if a country has a persistent trade deficit as a result of a strong currency it’s almost certainly a net negative

Ha, no!! But they’re cheaper than the same imported goods purchased with a watered-down dollar. A dollar move like this isn’t going to change where Walmart buys its clothes :-)

Whenever I read or listen to pieces that comment on the market being “short [the Dollar]” or that the [Dollar] [bullish] trade is crowded, I sort of cringe … makes it sound as there was this mysterious overhang of positions just waiting to flood and crush the market, or anybody that stands in its way.

Problem is that for every buyer or seller in a given market there has to be a counterparty with exactly the opposite view ?

If I’m selling because I take a negative view of the Dollar, surely the counterparty for that trade is taking the opposite view !! I’m bearish, they are bullish and it’s a zero sum change in market positioning. So, comments like the market being “short” or “long” I think are misleading.

Price changes result from momentary imbalances when buyers change their bids and/or sellers change their asking prices – . Yes, you can have increases in open interest, and you can call that an increasingly “crowded” trade, but the net of all these new positions is ZERO – there is no such thing as the market being net long or net short.

The only thing that gives any meaning to the expression a “market is short/long” is when INTENTIONS to buy or sell turn into bids/asks that actually hit the market – then the question becomes how sensitive these intentions are to new information.

How anybody can insinuate or assert to know the the sum of market intentions is beyond me. It’s hunches and guesses, dressed up as “analysis” and “forecasts”.

Oliver

You just fell off a logical cliff :-)

If the crowd of speculators and the hot money go from being bullish the dollar to being bearish the dollar it means that they try selling it. Since they’re all trying to sell it, no one is buying, so the price (in relationship to other currencies) drops until it drops far enough to where someone is willing to buy it. So the same NUMBER of dollars are just changing hands. But buying or selling pressure changes the PRICE of the dollar when it’s changing hands.

And PRICE (of dollars and bonds) is what this article is talking about, not the number of dollars and bonds out there.

good point , better than KAHN academy. How then and which data points determine what asset is a “crowded , long in the tooth ” trade. MAYbe the derivative market ? or is it subjective ? I thinking options would be a good indicator . thanks WR . the fog is clearing

BofA ML determined this by surveying fund managers. So 47% said that long the dollar as a trade, rather than neutral or short, is the most crowded (check out the chart … it’ll give you a feel for just how “crowded”). They’re specifically speculating in highly leverage bets that the dollar will rise against some other currency or currencies of their choice.

So, what, then is a crowded trade ? Or, when people proclaim that the “market is short this and long that”.

The way your piece reads seems to suggest a net positive number of Dollar long positions that have “built up” during the recent rallye, overhanging the market and threatening to bring down the price through the price-finding mechanism you describe … once they decide to bail.

But that cannot be since for each long there is a short taking the exact opposite view of the market, at a given price.

Oliver

I explained above how BofAML determined what a crowded trade is – our comments must have crossed in the mail :-)

Price is determined by buying and selling pressure – how eager people or algos are to buy or sell – not by the number of dollars out there (that’s a separate issue).

So when everyone is trying to buy (bullish the dollar) the price goes up because potential sellers have to be induced to sell. The inducement is a higher price. Enough of this, and the trade gets “crowded.” Which means there aren’t enough eager buyers left who want to buy when someone is trying to sell. Now potential buyers have to be induced to step up to the plate. That inducement is a lower price.

During that process, the number of dollars out there doesn’t need to change (though it can change for many other reasons, having to do with banking, central banking, credit, etc.).

‘At a given price….’

That is your answer. A betting shop (or a stock market) will take a position opposite yours almost no matter what it is, as long as you accept their odds. There doesn’t have to be a long to match your short- the broker makes a market.

A trade being crowded is like a horse being a favorite. The wickets are literally crowded with folks who want to bet on him.

Therefore the trade is expensive- you may have to put up ten dollars to win one dollar.

The math of market dynamics also depends on the type of security. With currencies these are various.

In the futures market (and most derivatives) it is true that there is a buyer for every contract “sold”. But as others have alluded to above – there are rarely the same number of buyers and sellers at the current Price. Price moves to EXACTLY where the number of contracts buyers want to buy and sellers want to sell is equal at that moment in time. News and events change that equilibrium price constantly. Open Interest is watched by many – because if the number of open positions is expanding while price is moving, let’s say, Up, then it is interpreted that price is being “pushed” up by Buyers wanting more, more, more – as opposed to Sellers holding off for higher prices. If Open Interest is declining in an uptrend – it may be that Sellers just aren’t available at current prices.

But in the cash market it’s different. There are two “buyers” for every Short seller (not every Long seller). If Mr. A owns $100k of some security and I borrow it to short to Mrs. B – they both now “own” $100k each. It’s magic! So the Long trade can get “crowded” by adding more Shorts :)

And short squeezes can happen as price goes up not because there are more buyers than sellers, nor because short sellers get desperate. But simply because of the mechanics of borrowing. If the pool of securities available is pretty much already borrowed, a squeeze can develop because a whole bunch of Longs want to sell – yes, SELLING can cause short squeezes!

For Mr. A to sell the $100k security that I borrowed from him and sold Short to Mrs. B, he first needs to get that security back from me… to sell to another lucky buyer! And so I may have no choice but to go into the market to “buy in” / “cover” my Short, because I have to, not because I’m panicked. Even though, in theory there is one buyer and one seller – price dynamics come into play because I have little choice as to timing my buyback – the borrow contract states that Mr. A gets his security back on demand. Pros might get a day or two warning from their Prime Broker that this is likely to happen. John Q. Public gets an email that it was done for him already :(

Then, at even higher prices more Longs want to sell, and some demand their borrowed securities back, and price goes up more… Lather, Rinse, Repeat… I’m getting panicky just thinking about it.

You are talking FX and stock’s in the same post and conversation without differentiating.

This is confusing, some of what you are saying applied to FX appears inaccurate, but it is hard to be sure as you are mixing the two market’s.

And appear to be involving, Dollar future’s, Dollar future’s, are a dangerous thing with PE 45 about to take office, where the dollar can (and I believe will be deliberately, and repeatedly) be moved, by a 3 AM idiots tweet.

True – I was mixing the two – just trying to point out the mechanics of why a “buy for every sell” doesn’t determine the direction or momentum of price in futures, equities, or cash markets. But yes, it was a bit confusing – whaddya want – I tweeted it out at 4am :)

If your argument were extended to its logical conclusion, then markets could never move at all. After all, when there is /any/ transaction, for every buyer there is a seller (and vice versa)! This is toy academic analysis gone wild (but of course, is exactly the kind of thing that underlies the broken economic models prevailing today which are in large part responsible for mass economic and monetary mismanagement).

What is left out of your simplistic analysis is “market force”, i.e., bid and ask structure (as well as the psychology driving them). If bids are lowered and/or become fewer, then the same number of sales will tend to drive the price down; alternatively, if sales demand (all else equal) increases, it will tend to overwhelm the bid structure, “asks” will race to the bottom, and prices will fall. This can all happen in reverse as well.

So a “crowded trade” is one where there is a market “cliff” or “spike”, via the above dynamics, inherent in the set of past trades and the psychology behind them. The risk is highest when the most market participants are thinking alike and hence have positioned themselves similarly. It is a very real thing.

Both Oliver and his contrarians have a point.

Oliver: every trade has two parties, hence it is senseless to talk about “most participants” if by participant we imagine an abstract buyer or seller of a unit measure of the item traded. In terms of legal entities as participants it is of course very likely that at any one time there are a lot more in long position than in short or the other way around. That would just mean that those entities in minority position (opinion) have on average larger positions (greater conviction). But when weighted by volume, both sides are the same.

Contrarians: refusing to get that point, attempt to make another: that what is moving prices (undoubtably prices do move) are trends in the relative desirability of the opposing positions.

I find the contrarian arguments more problematic.. or rather imprecise and the quoted method of gauging the sentiment via surveying fund managers (47% of whom supposedly said something, compare 47% of my tosses were head) rather too practical and unprincipled.

Why are contrariens’ arguments problematic? To simplify them a bit: “everybody wants to buy, so prices go up”. Intuitive, appealing and truthful this inference may wish to be, it is missing substantive elements, precisely as Oliver (and nick kelly) point out. You can never have everybody wanting to buy pushing up prices because every push in price corresponds to a trade that had a selling side (who is thereafter equally unlikely to be wanting to buy for a while).

How to square this? Refine the claim somewhat to make it more precise what you mean: “[most] everybody wants to buy [at the current price] therefore the [next transaction] price will be higher [where there is a willing seller]”.

In short, nick kelly (above) put it right.

Inevitable follow-up meta-point:

Of course, once the inference is put in its correct form, gauging the sentiment becomes less relevant, since it (implicitly) refers to the price of the time of inquiry and may no longer be relevant after a change in price (all things still being equal after a minute, which they are not).

For the sentiment report to have any relevance, it would have to refer to sentiment wrt. a price range including the price at the time of reading the report (not to mention that all other factors would need to be equal at the time reported and the time the report was consumed).

The problems with this should be obvious. Since if the price now is 100 and it was knowable that everybody wants to buy while the price does not exceed 103 then before anyone got a chance to report that the price should have jumped to 103 or higher, making that information redundant.

Viz. the market reports on itself, sorry, you’re late.

Perhaps if it’s the weekend and people are willing to reveal to you what they will or would do if they could trade while not actually trading and you managed to collect and contain that information and all else remained equal then on Monday you could have an advantage in the first trade? Or would the first trade already be at 103 or higher? The latter, of course. Unless your report erred. So in order to gain a benefit from this invaluable report, you’d still need to find somebody to trade with otc over the weekend at or near Friday’s closing price of 100. But if your reporting is correct, there is no such party to trade with!

Ie. in a Goedelien twist, correctness of a market report should make it automatically useless. In other words, if you managed to make a buck, it was because you had wrong information! Take that.

So what is supposed to be the point of (reading) such reports? (Granted there may be numerous points of authoring them.)

Well, obviously to help you make a buck by giving you wrong information!

the desire to hold dollars has more to do with interest rates and hot money. if you perceive that interest rates will rise then foreign investment will be converted into dollar denominated bonds, then you want to own the dollar. for them its a hedge basically. so like WS says, Walmart wont change a thing, but they will probably be in the financial markets trying to hedge the extra costs in buying Chinese goods.

My personal definition of buying is promising more of the lower layers of Exter’s Pyramid to access the celestial promises of the upper layers (trust in the narrative, the promise of more immaterial interest).

http://www.mathsisfun.com/money/images/compound-graph-10.gif

So this must have been a buy. What exactly was bought eludes me at the moment. However when sell (trying to swap the spectral promises of the upper layers for something more down to earth and very scarce down the pyramid) occurs, now *that* will be a very crowded trade :)

https://silverbullionknowledgecenter.files.wordpress.com/2015/03/liquidity-pyramid-gold.png

Money is psychological trust in the narrative (getting more at a later time), and it was never different, since Mesopotamia, except in scale. Only the promises have value, and only for as long as the trust is there. If the promised stuff existed, it would be completely worthless.

Buy rumor, sell new’s, preinauguration, rumor time, is over.

Now we move to, what of his first 100 day threats, will he carry out, in his first 100 days, which will cause.???

I expect volatility, and inconsistency.

Also the tweet machine that, has been roiling stock’s, will now start to have similar effects on the $. IMHO

Wolf, love your work!

The major central banks have been *manipulating key markets since the end of 2009 *(in a major and significant way). This collusion was made easier with Obama as he gave them leeway and stayed out of their way.

Trump is just the opposite. He’s a bull in the china shop and will wreck the china but hopefully NOT THE SHOP; probably sooner than later. The CB players may just end up throwing up their hands and let the markets go where they might. Or they may try and stem the tide but it will be too strong.

Bottom line I’ve maintained all along, the CBs can control a lot and have been, but they can’t control a huge swell. They’ll let it play out and then try and repair afterwards (like 09).

I still like Trump in so much as he’s a refreshing anti-PC type of person. And frankely, some of the things he says have needed to be said for some time.

But any coherent policy???? I doubt it. Buckle up your seat belt. In fact, maybe you better put on a helmet as well.

Trump’s efforts to repatriate businesses to the US can only increase the value of the dollar. The more of these businesses commit to move here the more dollars it will take. The only counter to this is more printing. It seems simplistic but Trump is telling everybody what he is going to do, and showing us as well. Under those circumstances it would be foolish not to believe him.

Agree!

Our bet is on Trump: stocks “long” defense industry, heavy machinery for infrastructure building, etc.

“It seems simplistic but Trump is telling everybody what he is going to do, and showing us as well. Under those circumstances it would be foolish not to believe him.”

According to you, his actions will make the dollar stronger. But he JUST said he wants a weaker dollar. Can you explain to me your train of thought? What, exactly, am I supposed to believe given that he constantly contradicts himself?

Maybe Trump doesn’t understand that moving manufacturing back from overseas is going to require a wave of forex trading towards the dollar. He wouldn’t be the first one to misunderstand the forex markets.

Lets not forget margin debt.

Which is very high, at just short of record highs recently.

Most of those long/short positions have been purchased by utilizing margin debt to leverage up those positions.

Unwinding?

Time please! All margin accounts to be settled at end of business day.

Being caught on the wrong side can be a real b***h.

Look for fortunes being made and lost.

I’m selling some of my dollar hoard which I’ve been carrying at 2 percent per annum since late 2014 I’ve already diversified with physical gold and silver and some farmland with lemon and pomegranate trees I’m just debating whether to buy Turkish Lira and get the 11 percent interest rate or play it safe and buy more gold but I believe the dollar looks bubbly here

Where do you hide your gold? ;)

Foreign property is looking like a good investment…especially given depreciating foreign currencies (I got a 40% discount on my new home, paid in dollars). Good times to be flush with USD, that’s for sure – but with the incoming Orange menace, it surely won’t last much longer.

Yesterday morning the tangerine one exclaimed ” my dollars are too high”!

Who do you think said pronounced lament was directed toward? (Madam chairman?)

All roads Lead to a more compassionate dollar and another QE?

The fed will give you a 1% deal if you buy back 4.4 trillion and finance the transaction with a just in time QE (final?) Two more quarter points just hold together a little longer (two more meetings and than southwest air to Cancun)

Roll off the balance sheet and out the productive economy?

Reflation trade- convincing the money powers to float a loan to president trump that was offered to GWB during the housing meltdown(after he begged for money out of every space in the WH for a week)

trump having to beg congress for a bailout? TARP deux!

What does it really mean to “buy USD”? Seems to me that there are two major options.

Either you are buying USD futures contracts relative to some other currency, or you are buying US denominated debt (bonds).

All other forms of buying the USD eventually boils down to one of the above, perhaps indirectly via a bank that “converts” your foreign currency (or deposit) into a USD deposit (of some sort).

Hence, when people say that “buying the USD” is getting crowded, I think it really means that foreigners are buying US debt, private or public. Once “we” have sold them a lot of the US debt, it is time for FRB to increase interest rates again and crash the value of that debt for foreign holders relative to their native currencies. Profit!

This also rhymes with the observation that the 2nd most crowded trade is for US holder is to sell short US debt.

Man, I so wish wolfstreet posts had some level of editability, for typos and clarifications.

“There was even some head-scratching how Trump dared to say something like this, abolishing the official “strong dollar policy” of the past few decades, when in fact it had been abolished in all but name long ago, and for all to see.”

That in itself signals a risk factor of some significance, and there’s more where that came from. In aggregate they make for certain weirdnesses in the risk analyses. Nothing I can’t handle. A couple of options should cover it. Hi-de-ho!

https://newrepublic.com/article/139870/trumps-team-shaping-dangerously-incoherent