The governor of the People’s Bank of China chimes in.

All kinds of officials are fretting about the dangers of the housing bubble in China that has been fueled by easy credit that officials have made available last year to stop the implosion of the prior housing bubble.

City by city, they’re grappling with this problem, trying to put a lid on it. Caixin Online reports:

About 20 Chinese cities tightened home purchasing requirements in late September to cool an overheated market, with some prohibiting property developers from selling homes to residents who don’t have a local hukou, or residency registration, and to those who already own more than one home. Other cities have raised the minimum down payment required.

But easy credit still rules: Total new loans in August reached 948 billion yuan ($142 billion). Over 71% of this debt was taken out by households, mostly mortgages.

New mortgages skyrocketed from 2.2 trillion yuan in 2014, to 3 trillion in 2015, and already hit 3.6 trillion in 2016 through August, according to the Wall Street Journal. Medium and long-term household loans, mostly mortgages, are now up 27% from a year ago.

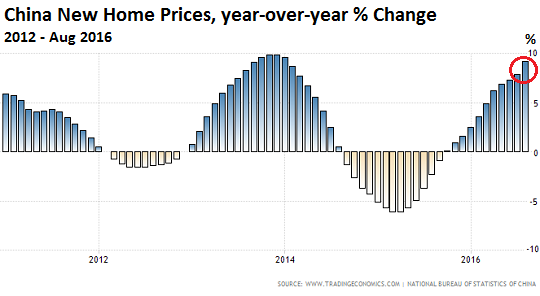

In response, the average new home price in 70 Chinese cities rose 9.2% in August year-over-year, according to the National Bureau of Statistics. In Beijing, the average price soared 23.5%, in Shanghai 31.2%! This chart by tradingeconomics.com shows the year-over-year percentage changes of the government induced boom-and-bust cycles:

Soaring leverage makes this housing bubble much more dangerous than the prior ones, not only to the banking system and financial stability but also to social stability. Folks there don’t like it when their life savings suddenly go down the floor drain, and they might react in ways that the government doesn’t appreciate.

The Wall Street Journal:

Such property imbalances have afflicted China before. Developers are still struggling to sell excess housing stock from the last boom in 2013, amid slowing economic growth and the state’s limited success in luring more farmers to cities. The large number of unsold homes dragged on the economy, leading Beijing last year to loosen home-purchase curbs and lending policies that contributed to the latest buying craze, economists say.

President Xi Jinping told senior policy makers at a recent meeting to “control asset bubbles” – and by far the biggest asset bubble is the property sector.

At China’s main housing regulatory agency, officials have met numerous times since July to discuss how to stabilize prices without triggering a sharp downturn, say people close to the agency.

But Beijing has announced no major policies.

That, however, may be about to change. The source of all this easy credit behind the big banks, the People’s Bank of China, is apparently getting very nervous.

PBOC governor Zhou Xiaochuan said in a speech at the IMF board meeting this weekend in Washington that the central bank would impose “certain controls over credit growth.”

This is central bank speak for what Caixin Online called “a squeeze on liquidity.” Since the credit growth is happening mostly with mortgages, he specifically targeted housing. He went on to elaborate:

“China will use various policy instruments to keep banking liquidity at an adequate level and allow credit and total social financing to grow at a steady and moderate pace.”

Caixin’s report – titled evocatively, “Central Bank Governor Hints at Credit Squeeze to Deflate Nation’s Property Bubbles”:

Zhou had warned earlier against the emergence of housing bubbles. Speaking at the G20 meeting of finance ministers and central bank governors in Washington on Thursday, Zhou said the government has already enacted policies to develop “a healthy property market.”

Zhou also proposed controlling credit growth to corporations by “lowering corporate leverage and dealing with piling debt through market-based approaches, such as debt restructuring, debt-to-equity swaps, securitization, and liquidation.” This came after the IMF warned that the country’s growing debt “posed risks to financial stability.”

Zhou remained officially sanguine about the state-owned megabanks. Though the ratio of nonperforming loans has risen, he said, the overall risks are “controllable” because banks have sufficient reserves to deal with them. Which is what all bank regulators always say publicly.

They fear the damage the ballooning property bubble will do when it deflates. But that ballooning property bubble has been the biggest growth engine in China’s economy, which has otherwise been dogged by a faltering manufacturing sector. Without that ballooning property sector, the Chinese economy would stall altogether. And if the property sector deflates rapidly, it would do a lot worse. Among other things, it would crush consumer spending – the other engine of economic growth. But by now, there appears to be no painless way out, and the PBOC might might have acknowledge that much.

Even Chinese homebuyers know it’s a bubble, but that hasn’t stopped them yet. Read… Chinese Consider Home Prices “High and Hard to Accept,” but Buying Frenzy Surges

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Considering that housing is a huge investment vehicle for the Chinese population, it’s hard to believe they would threaten it.

Threatens to threaten it perhaps, same way USFED threatens to raise rates but secretly knows what the outcome will be?

Or perhaps they follow through on the threat, once insider friends and family are positioned to front-run the move.

Nice work if you can get it.

Yeah, another BS. Anyway, money in PRC seems unlimited. They just keep going from one bubble to another.

I think it’s about time for another big meteor to strike Terra ….!

….. THAT would pop more than a few ‘bubbles’ ….. ;'[

The context here is that the home buying public in China, the 20-54yr/old population grew by an average of 10.5 million persons a year from 1970 to 2014 (or +468 million).

2016 was the first year the 20-54yr/old Chinese population outright declined and is estimated from 2015–>2030 to decline by an average of 6.4 million every year (or -102 million…the estimates through 2050 are even worse but less reliable).

China has built a massive oversupply of credit fueled housing (and infrastructure, and factories, and and and) for a population that is never coming…in fact for a population that is in collapse from the bottom up This bubbles burst will likely take down the Chinese banking system and the Chinese government…and the last global engine of growth will go silent.

Everyone seems to think that the Chinese economy is built the same way as Western economies, but Michael Pettis from http://blog.mpettis.com/ has argued for a long time that it’s not so. Professor Pettis has argued that the Chinese economy will slow down to 3 to 4% long before anyone thought it’s possible, and he argues (quite convincingly) that there won’t be a banking crisis. The debt losses will still need to be allocated, but it won’t play out the way most people think it will.

But, the Chinese manufacturing sector built their multitude of factories predicated on +20% annual export growth. Flat or falling exports results in massive overcapacity and rampant deflation. US imports are flat or falling. European imports are flat or falling.

China’s most significant export is now the “bad” kind of deflation, the kind caused by massive overcapacity. What’s China’s solution to that problem? Keeping factories operating to mitigate unemployment increases deflation and adds to operating losses and ‘real’ NPLs. Shuttering factories increases unemployment and makes NPLs hard to ignore.

Mr. Pettit has stated that losses have to be allocated to either the government sector, corporate sector or to the public sector. So far it looks like the public sector is going to eat the losses. If so, there is not going to be any consumer economy developments to speak of because their wealth will be used to bail out the private and state owned sectors.

“So far it looks like the public sector is going to eat the losses. If so, there is not going to be any consumer economy developments to speak of because their wealth will be used to bail out the private and state owned sectors.”

in that case it is going to be much like the USSA and socialist Europe, isn’t it?

CHINA IS A GIANT DEFLATION MACHINE. PERIOD.

by the way, they’ve been known to be very creative with gambling schemes.

I don’t know if you are familiar with Paul Midler, an old China hand who has long lived and worked in the Celestial Kingdom and who wrote the excellent Poorly Made in China.

Midler is just one of the many who voiced doubts about how population statistics are kept in China. According to him the real population is most likely not only lower than the official figures, but also considerably older and more childless.

Apparently not only the damages of the One Child policies have been far more serious than usually considered but the Communist Party likes the idea of being able not merely to manipulate economic statistics but demographics as well.

By all account China already has a surplus of infrastructures that would last them at very least 10 years of real 7% yearly GDP growth even if they stopped building everything they are building right now.

Their strategic industrial overcapacity (cold rolled steel, glass panes, electrical wiring, solar panels etc) is truly the stuff of legend: it was built with double digit yearly economic growth in mind and to fuel exports that were supposed to increase between 10 and 20% per year from 2005 to 2030 at least.

And housing… just how many empty units are there in China? I understand the Chinese consider housing per se if not an investment at very least an insurance policy against inflation, but the only two reasons for owning a house in the end are either living in it or renting it out to get a steady yield.

One also needs to consider all those empty apartments that wealthy Chinese like to flip, just like those airports which have never seen an aircraft land after receiving CAAC certifications, are fast deteriorating.

If you’ve been to a Chinese hotel, even a high end one, you know what I am talking about and that’s the main reason Chinese owners leave their apartments devoid of the most basic finish. No point wasting time and money on something that’s merely meant as a speculative endeavor and in a few years will be sold to a developer to be razed so that a new unit can be built.

The cash reserve ratio for big Chinese banks is at 17% after being lowered 0.5% effective March 01, 2016. This is still one of the highest such ratios in the world.

China can maintain their money market rates given the depth of reserves held and if need be, by further lowering of reserve requirements. China has a ton of room to drop rates. The other three big central banks not so much, as they are very near or below zero and are tightly restricted in any response to market shocks.

Also, the sheer size of China’s market provides great depth for bank maneuvering. Consider that there are 10 cities in the US with a population of 1 million or more. In China there are 160 such cities.

As the Chinese gained wealth, (particularly among the wealthy of the tier 1 & tier 2 cities) the wealthy, soon to be elderly didn’t trust banks or the stock market…instead they levered their savings primarily into real estate. The top quintile of Chinese earners purchased the bulk of the new, speculative inventory of high end housing…the typical buyer bought multiple apartments and condos. The vacancy rate among the housing segment in these cities is supposedly in excess of 20% (compared to a peak of 3% during the US subprime crisis). There are roughly 500 million households in China and best guestimates suggest that there are at least 50 million or so vacant housing units…or 10% of the national housing stock. And the collapsing population of 0-54yr/olds means there will literally be millions fewer potential tenants and buyers every year. The losses coming are staggering and likely 10x’s those seen in the US subprime crisis.

Given there is no fundamental support under the Chinese housing market (or CRE market for that matter) look for the PBOC to not only not attempt to pop the bubble but drop rates further and do the only thing it knows how…blow the bubble even bigger. Simply put, this is a national security level issue for China and no “free-market” price action will be allowed so long as they can avoid it.

Squatting China is my new website!

Just watch out for the police. In many places they don’t take kindly upon squatting.

Official statements always seem to confuse liquidity with solvency.

I see no way out for the Chinese economy. Tighten up lending and the Chinese government and banks can no longer create and circulate currency. Without easy money the requisite liquidity will dry up. Fail to tighten up lending and the whole thing blows up. Is there a middle road? Maybe, but that will take some remarkable monetary acrobatics.

The simple mistake being made by the Chinese Communist Party is that they don’t have a clear understanding of “money”,and, it is not only them that fail to have a clear grasp of this very simple topic.

Money, itself, must have value. A “storage” for wealth. IT must be something corrupt men (like us) can not counterfeit. Because of this, the only thing Physical on Planet Earth that can be used as “money”, true Money, is Gold, Cattle, or Women.

Cattle and Women take up too much space and have to be fed. GOLD doesn’t. It won’t rust, get old and lose all value, nor die.

Gold is Money. Money is Gold. Not perfect, but it is the best thing in our Physical World if we wish to go beyond bartering (which can not be corrupted) to an item used in exchange between what you have to barter and what the other person has to barter but neither of you want what the other has at that moment. Gold is the answer.

Today, with all the (controlled) Central Banks, we do not use money. We use credit. In paper form, they are called “notes”, as in Federal Reserve Notes which are used as the American currency. They are nothing more than printed paper which has NO value. This concept is so difficult for others to understand (not me) and for that reason, the (private) Central Banks get away with issuing of “credits” as “money”.

It is the most amazing scam in history and I wish I was in on it. But I am of the wrong religion. Very few people understand it.

China is a controlled economy. As in dictatorial control. Housing won’t go down because for prices to drop, owners have to sell.

Well guess what. Make a rule that if you want to sell, you have to at least get market prices (“our” market prices).

Problem solved.

I think all the banter about China imploding economically or socially is overdone. On the otherhand, their demand for goods and services outside of China has dropped signficantly and will likely stay so. And, demand for their cheap export crap has dropped as well, so they get to keep some of that stuff for themselves.

All told, a slow down for sure. Collapse? I doubt it.

Not really.

There is no reason the Bank of China can not buy each and every apartment, condo, or single family house placed on the market. There is absolutely NOTHING preventing them from doing so.

Back, a few hundred years ago, China would only accept only silver in exchange for goods. BUT, with modern, new-age, Western Eurocentric Ideas, the Marxist Government (An English man, imagine that) of China no longer has to accept silver. They no longer need silver. They can issue credits and there is really NO limit, since “credit to your account” is nothing more than a key-board entry. Wonderful.

So, to keep the Nominal Prices of the empty condos UP, they only need to issue notes/credits and purchase every single one that comes on the market.

This is what they will do. Sure, there may be “inflation”, but the public is too stupid to understand where the higher prices are coming from.

There is absolutely no reason for housing prices to fall in China. The prices can stay where they are, or go up, but the credits issued to purchase these empty condos will, of course, be worth-less, but the public is too stupid to know that.

You all worry too much.

you make a good point. the fed did almost the same here. It always puzzled me why on earth should the government borrow from a private bank and pay interest to them where it can coin its own money. If we can print a dollar bond we can certainly print a dollar currency. Why should those private bankers have the enormous power to print and buy the whole earth without lifting a finger to create any wealth? And when they screw up, still the government has to bail them out, give them money so it can borrow from them and pay interest to them…crazy , isnt it?

“There is absolutely no reason for housing prices to fall in China. The prices can stay where they are, or go up, but the credits issued to purchase these empty condos will, of course, be worth-less, but the public is too stupid to know that.”

Exactly the same could be said for most of Europe and the US.

What the ECB is doing in Europe comes down to the same: printing money to keep home prices rising (or prevent them from further declines, in some areas like ClubMed) and causing inflation everywhere but of course not in the items that the government includes in its BS inflation statistics. Rents, healthcare, energy for the home, education, all kinds of taxes – it all keeps increasing, often at staggering rates, but the general public is saved by easy money and countless new subsidies (government gets money for less than free thanks to the ECB …) and mortgage rates that are close to zero so they still have some money to compensate for the unofficial inflation. Most of the public is totally oblivious to what is happening, their home valuations are rising again and that is all that counts! If you are renting you sure notice what is happening but renters don’t count (it’s surprising that they are still allowed to vote …).

After throwing everything and the kitchen sink at the epic Dutch housing bubble, my government has been negotiating for over a year now for the ECB to buy their huge mortgage debt bubble. The mortgage debt is bigger than GDP, much of it is under water by definition, yields that are close to zero and valuations are higher than anytime in the last 400 years – just the type of investment that the ECB wants … Still, the ECB hasn’t decided yet because they officially aren’t allowed to buy all those private properties and they have to find some backdoors in the regulations to make it possible.

From what I see, Chinese housing policy it far less idiotic than in my country and much of the West.

The Chinese bubble still looks mild in many ways compared to what has been going on in my country for many years. While high level officials in China worry openly (and have been doing that for some years) no politician or banker of any relevance in my country thinks we have a housing bubble or that Dutch home prices cannot continue growing into the stratosphere.

But let’s wait and see if the Chinese follow up their words with action: at IMF and BIS meetings there is always tough talk that is only for public consumption, as soon as the banksters are back home they continue blowing bubbles. At least in China there isn’t the Keynesian groupthink that dominates all Western economies; there are strong differences in opinion within China leadership and because of that, it wouldn’t surprise me if China is the first to really tackle the problem.

There are HUGE differences between the Chinese bubble and those in the West, e.g. that most of the real speculation (with high leverage, owning multiple properties etc.) there is confined to the upper classes, while in the West often the whole country is trying to get rich through housing. And unlike what goes on over here, people in China don’t buy homes with zero-down mortgages, almost-zero rates and full state guarantees against loss etc., especially not the lower classes.

As to ‘oversupply’, who knows … if Chinese people stop living with their parents until they marry (as is still quite common there) and prices come down I don’t think there is oversupply at all. There is probably oversupply (planning failure …) in some speculative areas but that’s something else.

http://www.bloomberg.com/news/articles/2016-10-10/one-u-s-recession-indicator-looks-less-scary-on-closer-inspection

wolf can you decipher this for me? is this an example of what you have been talking about?

im confused

Yes. I (along with many other people) have been worried about the inventory-to-sales ratio spiking like this since late 2014. It meant that eventually, businesses would cut orders to bring inventories in line with their lower sales. This is now happening.

Ironically, increasing inventories is additive to GDP (as a form of business investment). But when inventories fall, it’s a negative for GDP. This could happen slowly or suddenly. If it happens suddenly, it has a big impact on GDP and can trigger a recession.

But cleaning out those inventories has to happen eventually.

i get that. but the article makes it sound like its no big deal and its normal. cause in the first paragraph it says things are different this time. what i understand and know is the opposite. i work in the automotive industry, if cars are parked in the sales lot and not in a driveway, work will be slow at some point. it just caught me off guard for its positive nature.

If the inventory comes down slowly, over a longer period of time, as orders get curtailed just a tiny bit, it really doesn’t have a huge impact in one quarter. It will unwind the amount that the inventory increase had contributed to GDP in the first place, spread over a number of quarters. It will be a mild drag on GDP, but for a long time.

If it happens rapidly, it’s associated with large order cutbacks, layoffs, and the like around the entire country, and up the entire supply chains. And this can be brutal – as it was during the Financial Crisis.

In either case, it’s not good. And even if we get the long and slow version, Bloomberg is too sanguine about it.

there’s nothing that a little bit of more free money cannot solve in today’s economy…

Around 2012 – after a mild downturn in the housing market – my country had a housing stock for sale that would take at least 6 years to turn over, at the monthly sales rate of the time. New buyers could chose from an average of 40 new homes.

A few years later and the inventory is now equivalent to 6-12 months of monthly sales, and the average buyer can chose from about 10 homes (less in speculative hotspots). This turnaround didn’t happen due to discounts, no: it happened concurrently with the biggest price increases in 10-15 years. All thanks to the most lax conditions and the lowest rates ever for buying a home. Probably it helped that the government forced banks to be easy on people who were behind with the mortgage payments or severely under water, which probably removed some stock from the market. Plus strongly increasing rents which meant that if you sell, you simply have to buy another home or emigrate – there is no alternative.

See .. it’s really easy to get rid of overproduction, and jack up price and profit for the speculators along the way ;-(

China’s efforts to rein in their housing bubble should fun to watch. I’m unaware of any asset bubble that has ever leveled off into a plateau. As far as I know, asset bubbles are either inflating or deflating. There is no middle ground. Maybe the Chinese apparatchiks are magicians who can pull a real lion out of a hat. But, my money bets against them.

I am not certain how China can get out of this unscathed. It has a number of issues against it:

– Oversupply everywhere

– Excess credit from formal and underground sources

– Top heavy demographics with rapidly aging population

– Capital flight

I can only see the CCCP keeping its hands on reins of power by diverting the people’s attention elsewhere, and now unfortunately conflict is the only viable avenue.

I live in the most desirable neighborhood of Shanghai, but work in Pudong (the other side of the river) and am always itching to find a good apartment near my office there. So I have an up-close-and-personal view of the situation, in SH at least.

My apartment rent is 7,000RMB per month. The apartment above mine sold in December for 8,000,000RMB and is identical in every respect. So doing the math, my landlord’s yield is a risible 1.05%. In most of the city it is in the low-2’s.

A market cannot be so unmoored from fundamentals forever. Rents and mortgage payments are repaid with wage and salary income which is assuredly NOT rising at double-digit rates. And for those who believe in an omnipotent CB which can keep it going forever, I can point you to last year’s stock market debacle which saw the government powerless in the face of relentless selling.

I look for the impending collapse of the Tier-1 RE markets to be the biggest Black Swan that Western economies have ever seen. It will bankrupt the world.

Agree that this cannot continue, but your landlord didn’t pay 8M RMB for your apartment, he probably purchased for a way lower price so his yield is better. And the landlord upstairs (if he is going to rent out) will probably ask more than 7K per month, like most of the new owners – so rents will keep going up.

In my country the gross yield on rental properties is often 2-3% (that’s for the whole country, not just some big city hotspot). Deduct some upkeep, property taxes and vacancies and there is nothing left. But here too the numbers are based on current valuations. Much of the housing stock is from long ago, e.g. we have housing corporations who have massive amounts of homes that were build 60 years ago for 5000 guilders (official 2270 euros, but without inflation correction obviously and not including upkeep and some renovations since 1955). These 2.3K homes are now rented out for 1.1K per month in the free market (that’s yield of 570%, with ZIRP/NIRP everywhere) , although people on social security can rent them for 280 euros per month.

Same story for private landlords: if they buy now the only way to make money is to rent out the home per room to foreign workers, new migrants etc. which will probably cost a lot in the long run due to rapid degrading of the property. But many of them purchased years ago for way lower prices so they can still make money. The main problem here is that the average renter in my country pays nearly 50% of income for rent, there isn’t much room to increase that – so I guess that we are near the end of the cycle but who knows what other trick politicians will invent to kick the can down the road and let the elite pillage for a bit longer.

you wouldn’t suppose that some of that sales price found its way into…….the buyer’s pocket? the lender’s pocket?

you wouldn’t suppose?

would you?

would you like to see a chinese hud-1?

Thank god for a comment that doesn’t say all the govt has to do is print money.

For the first big disastrous attempt at this see the introduction of paper money in France in the mid- 18th Century.

Strangely enough it was a Scottish financier, gambler and jail breaker John Law, who finally found in the broke French monarch a receptive audience for his scheme to ‘turn paper into gold’

After a brief wild prosperity ( sound familiar) the system collapsed- Law barely managing to escape with his life, after having been for a time the head of state finance.

Much of the wealth of the middle and upper classes was wiped out- and not too long afterward came the French Revolution.

Maybe they’ll bring back tulips?