Five-year retail boom implodes.

Retail sales in Texas boomed for five years straight, from March 2010, their low point during the Great Recession. Sales tax collections jumped 46% from the first half of 2010 through the first half of 2015 – dizzying growth for a mature market! Given the size of the Texas economy, it helped prop up US retail sales. But by May 2015, 10 months into the oil bust, things began to sag.

Sales tax collections in September for sales that occurred in August dropped 3.5% year-over-year, according to the Texas Comptroller of Public Accounts. And in August, sales tax collections had dropped 3.0% from two years earlier. This was only the second time since the depth of the Financial Crisis that collections were lower than two years earlier, the first time having been in June!

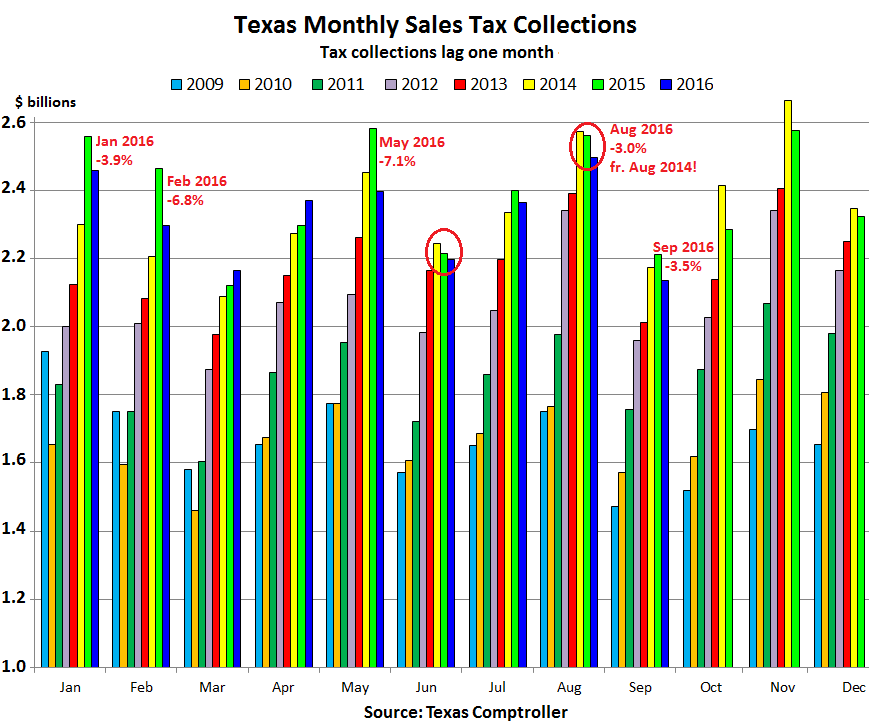

Year-to-date, sales tax collections fell 2.5% to $21.4 billion, and were practically flat with collections two years ago. On a per-capita basis, given the growth of the Texas population (up 8% since 2010), it looks even worse.

Sales tax collections aren’t an ideal gauge. Many food products are exempt. Taxes on motor vehicle sales and rentals are not included in this tally but are reported separately. The data is not seasonally adjusted, so it can only be compared to the same months in prior years. But it’s an unvarnished approximation of the movements of retail sales.

This chart by “David in Texas,” who also researched the sales tax collection data, shows how the boom since the Great Recession began to sag last year. I circled the two months when collections declined from two years ago. Note that sales tax collections lag sales by one month. So collections reported in September were for sales in August (click chart to enlarge):

But people in Dallas, Austin, and some other places are looking at this incredulously. The economy is hopping. So retail sales may not be all that strong either, but the exuberance for the booming housing market hasn’t cooled off. Home prices are still soaring. Job markets in those cities are still growing with only a few dark clouds in sight.

But then there’s the Houston metro, with a population of about 6.6 million, just slightly less huge than the Dallas metro. And there, the wheels are coming off the economy (below data via Houston.org, and the Bureau of Labor Statistics).

Construction sinks: In the Houston metro, total building contracts in August plunged 18% year-to-date compared to the same period last year, with nonresidential construction down 21% and residential construction down 16%.

Housing hanging on by its nails: Home sales edged up 0.9% through August this year, and the median price is up 3.3% year-over-year, so seemingly still holding up despite the enormous headwinds. But active listings in August rose 16% year-over-year, and pressures are building.

Jobs in the goods-producing sector evaporate, government is hiring: Total nonfarm payroll employment for the Houston-Sugar Land-Baytown area edged up 0.4% in August year-over-year, to 3.12 million, but that’s still down 2.8% from the peak in April 2015. The Unemployment rate jumped to 5.8% in August from 4.9% a year earlier.

By contrast, in the Dallas-Fort Worth-Arlington area, employment rose 3.6% year-over-year to a new record of 3.574 million, with an unemployment rate of 4.1%.

Jobs in the service sector in Houston rose 1.7% year-over-year. But jobs in the goods producing sector (oil & gas, natural resources, construction, and manufacturing) plunged by 5.2%.

This helped push the unemployment rate for Texas overall to 4.7% in August, up from 4.4% a year earlier.

The hardest hit industries in Houston:

- Mining and Logging jobs, which are mostly oil & gas in Houston, fell 11.5% in August, year-over-year, to 87,500, down a stunning 21% from the peak of 110,800 in August 2014. Many of these jobs were highly paid engineering jobs.

- Manufacturing jobs, often making equipment for the oil and gas sector, dropped 12.4% from the peak in December 2014 to 230,000.

- Information Technology jobs, many of them also associated with the oil and gas sector, dropped 7.3% year-over year to 30,300, and are down 10% from their peak in December 2013.

- Professional and Business services jobs, including jobs related to oil & gas, fell 1.9% year-over-year to 465,000, and are down 2.1% from December 2014.

The biggest gainers (and the usual suspects):

- Government jobs rose 2% year-over-year to 368,300.

- Education and health services gained 4% to 385,100.

- Leisure and Hospitality jumped 7% to 327,600.

Foreign trade swoons. Exports measured in dollars plunged 21% in July year-over-year and 21.3% over the first seven months. Imports plunged 21% in July year-over-year and 30.3% over the first seven months.

The transportation sector wobbles lower:

- Port of Houston shipments in short tons fell 7.5% year-to-date through July.

- Air passengers at the Houston airport system in August are down 0.2% year-to-date, while landings and takeoffs are down 2.1%.

- Air freight is down 3.2% year-to-date.

And the beleaguered consumers are cutting back. Retail sales last year were down 10.3% from 2014. Here’s the big one this year, the largest category in retail sales: in August, new vehicle sales (in units) fell 7.2% year-over-year, having plunged 20% year-to-date, with new car sales down a spine-chilling 28.6% year-to-date, and even truck and SUV sales down 13.9%. It takes a lot of headwinds for a Texan to give up on buying a new truck.

But the weakness in Houston cannot alone explain the decline in sales tax collections across Texas that started in May 2015. There is more at play. Consumers are beginning to curtail their spending in other cities too – even if housing exuberance is still papering over their difficulties.

In the US, after six years of Fed and Wall Street hype, the real economy has some real problems. Read… The Great Debt Unwind: Business Bankruptcies Soar 38%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m a native Texan and I’ve seen a few Houston boom-bust cycles. Blind optimism that things will go on forever, no matter how many times it’s fallen apart before seems to be in their DNA. It’ll take a crap stabilize and in a few years start all over again.

Oilman’s Prayer: Lord, please give me one more boom. I promise not to mess it up.

The Texas economy is diverse and is still considered strong while attracting many new companies and residents. However, consumers are getting squeezed by soaring health insurance, healthcare, and higher education costs. Economists are seeing long-term trends of declining share of household spending on consumer categories like clothes and entertainment.

But supposedly http://www.bloomberg.com//news/articles/2016-10-07/consumer-borrowing-in-u-s-rises-by-most-in-nearly-a-year, with auto loans going up. Some other states must be making up what the Texans ain’t buying.

Yes, auto loan balances are up a lot, now amounting to over $1 trillion. But unit sales of new vehicles in the US were actually down in September and are up only 0.5% YTD.

What causes total auto loan balances to rise in this environment are higher prices (including used vehicles), longer loan terms, and higher loan-to-value ratios. And so we get this, despite stagnating sales:

Aren’t student loans just north of $1T as well? Interesting. Personal transportation and higher education are at roughly equivalent debt levels.

Smart consumers are curtailing their discretionary purchases. I personally am bracing for the tsunami of tax and bond issues on the ballot here in California. While I typically vote no on the annual school and BART (Bay Area Rapid Transit) these things usually pass.

One wonders whether people are buying online from out-of-state vendors, and not reporting the purchases – thus dodging sales tax.

Amazon collects sales taxes on sales to Texas (as well as many other big states, including California). It lost that battle a few years ago, after Walmart went on an all-out war against Amazon’s sales tax dodging practices.

Yet the 5 largest companies by sales in the Consumer Discretionary Sector Index, which contribute the most to gains are:

1/ Amazon

2/ Home Depot

3/ Disney

4/ ComCast

5/ McDonalds

That gives some idea of what the consumer is spending that very thin slice, of wages that’s described as “discretionary” on.

Another little reported clue as to the health of the global economy came by way of the IMF on Friday. The IMF will eliminate interest rates for low-income countries until the end of 2018. Why?

Could it be that these “low-income countries” can’t even make the interest payments on their debt loads? Curious.

Alot of Amazon sales increases are due to e-tailers moving their business into the Amazon marketplace. Not all increases reflect increase in consumer spending but where they’re spending.

all i can say is that the metro-houston manufacturing base serving the hydrocarbon industry after the boom year of 2014 might just be off 40%-60%.

i see it in restaurants and in car dealer lots.

oddly, mall parking lots still appear to be full.

go figure…

Regarding those mall parking lots…

Recently a new mega-mall opened not far from where my grandmother lives. My brother works for one of the companies that built said mall so he had some very interesting numbers.

During the first four days the mall was visited by over 300,000 persons, perfectly in line with the owners’ estimate of 120,000 “families” meaning groups whose median size is 2.5.

However revenues for the mall during those four days were a seemingly massive €450,000 below projections. Why do I say “seemingly”?

All it took to blow those projections out of the water by almost half a million in just four days was for each “family” to spend €3.75 less than expected. A pittance until it’s multiplied by 120,000.

This explains very well why the present economy, which on paper is doing just fine, seems crummy when seen from the ground.

Mall parking lots are jammed full (we should have a picture competition about it now that we are heading toward Christmas) but money spent is declining, as discretionary income is eaten up by inflation (starting from rents and healthcare) and wage stagnation.

This decline is slow, almost imperceptible, but steady. In some countries it has been ongoing since the 90’s and was papered over only by extending leverage ratios to the Moon and courtesy of the deflationary wind blowing from Asia which moderated the oppressive inflationary heat generated by monetary and fiscal policies which made that leveraging possible.

anecdotal story. I went to Target in early September to buy a TV. A Samsung 40″ was on sale for $329 but they had sold out because, per the store employee, it was ‘back to school’ and lots of college kids needed a 40″ TV for their dorm rooms? Anyway went back last week and the TV was still on sale but not in stock either at Target or HH Gregg. This time it was blamed on the bankruptcy of Hanjin Shipping line. I guess there is a container ship somewhere in the Pacific loaded with Samsung TVs that can’t get to port so I will have to keep using my obsolete Sony CRT TV in the bedroom until Hanjin and Samsung work out their problems.

I worked in a large CT mall for 3 years. Foot traffic can be misleading.

Are the people carrying large bags and boxes, or are they empty-handed?

Did they spend over $1000 on clothes, or did they buy a card at Hallmark?

People go to the mall to get the kids out of the house or suck up the free A/C or a lot of reasons that don’t involve purchases.

Houston housing market leads the pack….down the slope. https://www.realestateconsulting.com/the-housing-cycle-market-by-market/

Thanks for the article. “Only Houston has entered the contraction phase”. But notes that other hot markets are flattening. I watch the walnut creek, CA market and houses are sitting on the market much longer now. How far away can the drop be? A year?

Watch the DOM (days on market) that is on an MLS printout. When that number rises, it’s the first sign of a slowing market. It changes before prices are reduced.

INCREDIBLE LINK! Thank you.

As a long-time landlord in Dallas this confirms my current strategy that now is the time to “take some chips off the table” and sell into the stupid money buying at the top of the cycle.

I am selling 6 of my “worst” properties and getting offers at 20-30% above what I think the real values are.

Note that these have all been fixed up FAR ABOVE AVERAGE, but I consider them my “worst” because they are non-standard properties that normally would have to sell at a discount (1 requires flood insurance, 1 is a half-duplex with trashy neighbors, 1 is in a small city that is actively forcing out landlords, 1 is a duplex converted into a 4-bedroom house with a very weird layout, 1 is a condo, etc.).

Here is a link to the half duplex due to close next week at $91,000 (the appraisal came in $10k under the buyer’s offered price). Zillow says this home is worth $81,674, but that is jump of $8,700 (12%) OVER THE PREVIOUS MONTH. The actual APPRAISED VALUE represents a jump of 32% IN 1 YEAR. To further illustrate the craziness, this half duplex had a market value of $48k just 2 years ago!

http://www.zillow.com/homedetails/10244-Hillhouse-Ln-Dallas-TX-75227/26908430_zpid/

Chris – what’s up with that 75% property tax increase???

Merlin, it is bad data at Zillow.

Tax RATES have been essentially flat in Dallas (about a 1% rise per year for the last 10+ years). Changes in tax AMOUNTS are primarily based upon changes in VALUE. Here are the EXACT values from the Dallas Central Appraisal District and a good example of how low the taxable values are in relation to actual market value:

YEAR VALUE INCREASE

———– ———- ————–

MARKET $91,000 75%

2016 $52,000 21%

2015 $42,930 16%

2014 $37,150 51%

2013 $24,600 0%

2012 $24,600 2%

2011 $24,150 -11%

2010 $27,100 -1%

2009 $27,430 -53%

2008 $57,880 106%

2007 $28,060 -58%

2006 $66,970 0%

2005 $66,970 0%

2004 $66,970 0%

2003 $66,970 0%

2002 $66,970 39%

2001 $48,210 0%

2000 $48,210 3%

1999 $46,660

That is amazing that you can get a decent little house in a big city with a booming economy for $91,000. I’m in California and you’d be lucky to get that for $910,000. So it sort of boggles the mind!

Are you sure you should be selling? I’d guess the rate of return is fairly decent.

Something that may impact the Texas economy from the election on out is a referendum on the Florida ballot, protecting the right of Floridians to install solar power on their homes. Solar power was constructively banned in the Sunshine State when I lived there. It was one of my pet peeves. If passed the amendment to the Florida Constitution will make it illegal to restricts its use.

There are a lot of people in Florida that will go solar regardless of the economics. It’s a green thing with them. Others may tire of the endless rate increases on power, which is very expensive in Florida. I’m saving money not living there.

Petunia, why will this impact the Texas economy?

Less demand for oil, gas, and related services. Plus from what I understand, Texas opposes alternative energy as a matter of policy, to protect their energy providers.

Nope.

Texas is HUGE into alternative energy, it is just that it is focused on Wind vs. Solar. If you combine both, we are about the same % of non-hydro renewable energy as California. Currently, Texas has 24% of the total U.S. wind power.

The problem is that the electric utility lobbyists (not petroleum) got rates passed so that they can discount the grid-tie power they buy from rooftop solar and yet sell nighttime power at full retail back to households. As soon as battery costs come down solar will EXPLODE in Texas.

By % the overwhelming majority of rooftop solar is in San Antonio, which has a separate utility that doesn’t have to follow the policies of the embedded and powerful state-wide utilities.

As far as hitting the economy, the worldwide surplus in oil and U.S. decline in fracking is having the majority of the effect.

Effing brilliant species we are. Meanwhile, the NGO crowd over at the COP thinks we are going to somehow rouse ourselves to make deep cuts to emissions in the 11th hour…

Dallas’ economy and housing demand are ON FIRE.

Unfortunately, there is a big lack of EXISTING affordable housing and virtually NONE of the NEW housing is affordable. To illustrate, just consider the HUGE variance between existing home values and the list prices of houses that are actually for sale:

PER ZILLOW >>> The median home value in Dallas is $150,400. Dallas home values have gone up 17.0% over the past year and Zillow predicts they will rise 7.6% within the next year. The median list price per square foot in Dallas is $188, which is higher than the Dallas-Fort Worth Metro average of $121. The median price of homes currently listed in Dallas is $369,850. The median rent price in Dallas is $1,450, which is lower than the Dallas-Fort Worth Metro median of $1,595.

Furthermore, I believe that NEW REGULATIONS and DESTRUCTION OF CHEAP HOUSING will cause demand/rents to rise even more than Zillow predicts.

The Dallas City Council just approved a VAST REWRITE of housing regulations for the first time in 20 years. Ostensibly, this is being done for the very laudable goal of forcing slumlords to improve their properties. Many other local cities are doing the same.

However, the vast majority of rental houses are owned by middle-class people with just 1 or 2 rental houses. The new regulations will likely raise their costs and thus rents by 10-20%. In the City of Dallas alone (which represents about 1/8th of the area population) there are over 50,000 rental HOUSES.

In the case of the most affordable houses, complying with the new regulations will require $10k-$20k per property. Most middle-class owners do not have that kind of extra cash and thus their properties will sit vacant until they get foreclosed upon.

And unfortunately, catastrophic negative consequences are already starting. Just this week we learned that 305 month-to-month tenants were given eviction notices to move by the end of October BY A SINGLE SLUMLORD. Rather than spend the $6-12 MILLION required to bring these decrepit houses up to the new high standards, the landlord is either just shuttering them or bulldozing them and selling the lots.

These 305 families are essentially 3 WEEKS AWAY FROM HOMELESSNESS as market rents are 2-3 TIMES over the rents they are paying for their current substandard housing ($800-$1200/month vs. $400/month).

Plus, they are competing with thousands of better-qualified tenants for JUST 249 houses, mobile homes, condos and townhomes available IN THE ENTIRE COUNTY that rent for less than $1200/month.

And you can forget about any housing help from the city.

The Dallas Housing Authority (DHA) Section 8 Housing Choice Voucher waiting list is currently closed. It was last open for two days in July 2016, and prior to that for four days in July 2015. There is no notice of when this waiting list will reopen.

http://affordablehousingonline.com/housing-authority/Texas/Dallas-Housing-Authority/TX009/

The last time the waiting list was open there were over 10,000 people applying online and in-person! I have heard that there are currently over 2,000 families waiting on the Section 8 waiting list.

But the bureaucrats screwed this up as well. Like ALL of the landlords that I know WE NO LONGER RENT TO SECTION 8 TENANTS for five reasons:

1) burdensome regulations,

2) a 3 week loss of rent due to the initial inspection and approval process vs no lost rent for regular tenants,

3) much shorter length of tenancy of Section 8 tenants due to the programs actively trying to cull their tenant base to stay within ever-decreasing budgets (yes, decreasing even under Obama),

4) which make it uneconomical to put up with the significantly higher maintenance costs for these levels of tenants,

…and most importantly…

5) a change from above-market rents that made all the above BS somewhat worth it, to BELOW-MARKET-RENTS.

Lastly, conversations with public officials in charge of the new rental regulations reveal that they are a cynical effort to push poor people OUT of Dallas (reducing their public services cost), replace them and their rental housing with Millennials and Empty Nesters owning homes (increasing property tax and sales tax revenue), using the new regulations and a costly Rental Registration program to fund more code enforcement (to further raise property values/taxes), and at the same time PANDERING for votes from the very people they are screwing.

You definitely know your market.

Are the Chinese buying in Dallas yet?

It seems they are buying in everywhere.

Chris from Dallas……how will the rental market be impacted by HUD’s newest program to increase the amounts(in some cases, doubled) allowed for Section 8 vouchers. Julian Castro is implementing the Small Area Fair Market Rents(SAFMR) this month. An article in New York Post, dated 5/08/2016, is quite interesting, and gives an overview of the plans, one of which is to force suburban landlords into accepting Section 8 tenants…..even with criminal records, or Castro will charge them with discrimination. This appears to be another layer added to the insane “Affirmatively Furthering Fair Housing” which went into affect last year. Neither of these required congressional oversight or approval.

Big oil companies are no longer trying to replace all their production through conventional exploration, the energy consulting company said in a report published Tuesday.

More http://www.bloomberg.com/news/articles/2016-09-20/oil-majors-must-count-on-m-a-to-replenish-reserves-woodmac-says