When will she buckle?

Shares of Deutsche Bank got bashed 7.6% today, to €10.49 in Frankfurt, down 67% from April 2015, to the lowest level since they started trading on the Xetra exchange in 1992. They traded below that level in the early 1980s, but decades of inflation have whittled down the purchasing power so much that comparisons are meaningless.

Deutsche Bank’s 5-year default probability spiked to the highest level this year.

Its balance sheet, bloated with opaque risks, equals 58% of Germany’s GDP. It lost €6.8 billion last year. To hang on another day and to prop up Tier 1 capital, it has raised $20 billion in capital, in 2010 and 2014, by selling shares and diluted existing shareholders, and by issuing contingent convertible bonds.

These infamous “CoCos” are designed to be “bailed in” before taxpayers get to foot the bill. Thus, they’re a measure of investor fears about getting bailed in.

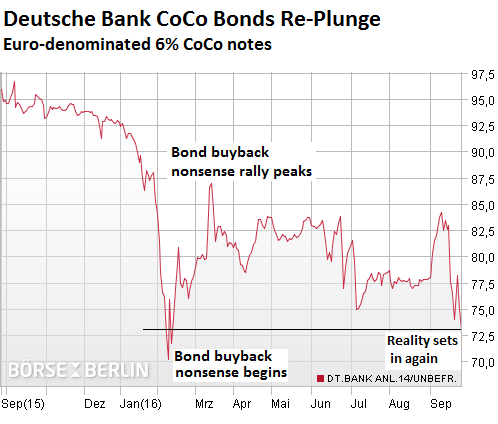

So when heck and high water came earlier this year, the bank responded by announcing on February 12 that it would buy back $5.4 billion of its own bonds! Everything soared! Even CoCos, though not included in the buyback, rose 24% over a few weeks. We have long ridiculed this manipulative move [here’s detailed explanation… Deutsche Bank’s CoCo Bonds Speak of Fear of the Worst].

Now shares hit new lows, and the miserable CoCos are getting clobbered, dropping 2.7% today to 73 cents on the euro, down 28% from April 2015 when they still traded at 102 cents on the euro. They’re now just a smidgen from also setting new lows.

The current rout – one in a long series – was triggered because Chancellor Angela Merkel, the ultimate political animal fretting about the general elections in the fall of 2017, let voters and taxpayers know what they wanted to hear. But investors were not amused.

On Friday, Focus Magazin reported that Merkel wouldn’t meddle in the legal disputes between Deutsche Bank and the US Department of Justice over the $14 billion fine related to the scandal surrounding residential mortgage-backed securities. This is what Merkel had “signaled” to CEO John Cryan in a “confidential meeting” this summer.

Citing “government circles,” Focus reported that CEO John Cryan had “suggested” in that conversation that diplomatic mediation by the German government would be helpful for Deutsche Bank. According to these sources, Merkel also “categorically” excluded the possibility of state aid in election year 2017.

Surely, the Chancellor did not ask for this “confidential meeting.” More likely, a desperate Cryon asked for it. But there’s no official statement about it. Instead, there’s a purposeful leak piped to voters by the ultimate politician trying to get re-elected. Another bailout of bank bondholders and stockholders just isn’t very popular at the moment.

Unlike prior crises at various banks – of which there have been many in Germany – the current crisis at Deutsche Bank is being silenced to death in Berlin.

The bank has settled a laundry list of allegations, including the Libor-rigging scandal, and is still mired down in a host of other investigations, including precious metal trading, currency manipulation, and money laundering for Russian tycoons. And no one knows what might ooze to the surface next.

Given the fines, potential fines, and whatever else might crop up next, and given the bank’s precarious and opaque balance sheet, markets consider it woefully undercapitalized, and they’re expecting something to happen.

Deutsche Bank accelerated its crisis management mode. Around noon in Europe, head of communications Jörg Eigendorf came out with a statement, carefully denying fragments of the reports, and thus, in the eyes of many, confirming them:

“At no point John Cryan has asked Chancellor Merkel to intervene in the RMBS issue with the US Department of Justice.”

Concerning a bailout by the German government:

“This question is not on our agenda: Deutsche Bank is determined to meet the challenges on its own.”

So raising capital by diluting the beaten-up shareholders further and perhaps bailing in CoCo bondholders? Nope. No way. At least not “currently….” Emphasis added:

“The question for a capital increase is currently not on the agenda, we do comply with all regulatory requirements.”

Then Eigendorf reiterated on CNBC so that everyone gets it: “At no point of time, John Cryan has asked the Chancellor for support in the negotiations with the Department of Justice, and he doesn’t intend to do that. He is very strong on that position.”

The bank is “fundamentally strong,” he said. “Look at our credit story, evaluate risk very low, our credit portfolio very strong, our liquidity position very strong, very comfortable and the third quarter is almost over, and I can tell you today that we are fine and very comfortable here.”

But no one is buying that “comfortable” story.

The German government in turn stuck to its official silence this morning. Spokesman Steffen Seibert said blandly with reference to the leak reported by Focus: “There is no reason for such speculation, as they’re being depicted, and the German government is not participating in such speculation.”

Concerning the ongoing negotiations between the bank and the DOJ, he said the same thing the government has been saying all along, that the German government knows that the DOJ has reached agreements on fines with other banks in the past, and it assumes that in this situation too “a fair result will be achieved.”

And hedge funds are having a field day. By the end of last week, the largest short positions – not including the countless smaller ones – in Deutsche Bank shares had soared to €500 million, or about 3% of the float. Other estimates peg total short positions to be up to three times that, which would be close to 10% of the float!

Now folks are wondering how low shares can fall before the German government attempts to prop them up, at least with some official rhetoric. A big part of the German economy depends on Deutsche Bank remaining a well-greased money machine.

If shares drop below €9.10, the bank’s market capitalization will sink below the potential $14 billion hiccup with the DOJ. Is that the number everyone is waiting for before Merkel buckles and bails out stockholders and CoCo bondholders with a generous pile of taxpayer money? Or are its investors really on the hook without instant backing by taxpayers?

No one knows. But the odds are shifting. One thing will not happen – will not be allowed to happen, no matter what the EU rules on state aid may be: Senior bondholders and depositors will not be bailed in because the government knows that allowing a monster like Deutsche Bank to collapse into mayhem will make the Lehman moment look cute.

All this is happening even as central banks have the spigot wide open, and as the consequences of their monetary policies, including on banks, are raising fears in some unsuspecting quarters. Read… OECD Warns Fed, BOJ, ECB of Asset Bubbles, “Risks to Financial Stability,” Pinpoints US Stocks & Real Estate

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

These banks must be broke, given their leverage ratios?

“the bank responded by announcing on February 12 that it would buy back $5.4 billion of its own bonds! ”

Most likely there were some important accredited shareholders who wanted to bail last minute into strength.

I haven’t yet heard what Bove is saying about this or even if he’d tell the truth.

Deutsche Bank should be allowed to collapse, in my opinion. Let free market forces do what they do; if your business is insolvent, it goes under.

Depositors should be made whole, but tough shi# for stock holders and bond holders.

Another bank run by criminals and thieves. Let them die. Wall Street was allowed to live after 2008, and that has kept us at economic flat-line, increased wealth transfer to the uber-elite and allowed numerous felonies to be committed with no criminal charges (Wells Fargo & JPMorgan Chase to name a couple).

Of course free markets should be allowed to work. It aint happening though…

The trouble with economics in general is the notion of equilibrium. Long periods of stability lead to asset price bubbles and once they pop a period of instability. Equilibrium thinking is enmeshed in neoclassical economics as well as the Austrian school, which has been soundly ignored in Academia for failing to mathematically elucidate their theorems. Both schools fall into the notion of equilibrium – that sooner or later markets return to equilibrium. But we know from chaos theory that instability can lead to more instability, a self reinforcing loop, hence Government intervention at some level is critical to the system, the meta system has become far too complex to manage with diminishing returns along the whole spectrum. A govt with a high level of trust could probably pull of a bailout without much of a hiccup as the people can buy the story, a govt with a low level of trustworthiness won’t be able to pull it off due to the negative consequences involved. I suspect Germany will bail out DB but this will be at the expense of the Euro. They have a highly skilled labour force and lots of industry to survive a crisis of confidence in their paper money system.

Well stated VK. Most systems want/will return to equilibrium.

In the US, that will not happen with who are in positions of power. The current Attorney General of the USA is case in point for this ‘retain status quo’ by those in a position of power.

If Germany can’t deal with it- no one can.

Equilibrium is incompatible with a debt money system, the exponential debt growth forces boom/bust cycles, even without the central bank shaking the tree like they do.

The central banking is designed for this, it’s in the maths. The simple act of renting out a currency sets it all up, the formula is however so simple that most people overlook it.

Debt = Principal * (1.0%interest ^ years)

All the boom/bust/inflation/’growth’ and wealth transfer (it’s primary purpose) stems from that formula, just add interest and it’s a roller coaster wealth transfer.

“Of course free markets should be allowed to work.”

The free market wasn’t allowed to work in 2008, when a collapsing Deutsche Bank was bailed out by the U.S. Treasury and the Federal Reserve Bank:

“As one of the largest counterparties of failed insurer AIG, Deutsche Bank received $11.8 billion of the funds used to bail out AIG.

The Federal Reserve made emergency low-cost funds widely available to foreign as well as US member institutions through its discount window. Deutsche Bank was the second heaviest user of such funds, borrowing more than $2 billion.

The Federal Reserve also created a program known as the Term Asset-Backed Securities Lending Facility, which allowed banks to use their assets, including troubled or hard-to-value assets, as collateral for short term loans. Deutsche Bank was the largest user of the program, sending the Fed more than $290 billion worth of mortgage securities.”

“Deutsche Bank should be allowed to collapse”

Maybe. But putting it down like a rabid cur would probably result in rather a lot of avoidable collateral damage. A less destructive course might be to nationalize it, liquidate it over time, and recover some of the costs out of the ill-gotten wealth of the perpetrating executives.

Some consideration should be made for reducing the Financial Industrial Complex to the status of a well-regulated utility, given the reasonable rationales that global-scale piracy is counterproductive, that feeding the ravenous only makes them even more famished, and that letting them plunder the planet is risky to civilization.

Putting DB down like a rabid cur does have a certain appeal, though.

Remember what happened when Lehman was allowed to fail…..

Whether DB lives or dies is dependent on who they owe money to. If you have been paying attention, that is the standard. If those CoCo bonds are being used for collateral at other institutions, the depth and breath of those positions will determine the outcome. Come on guys, let’s not get sentimental and moralistic at this stage.

Two thoughts come to mind

I recall a trip wire in the stock price, around $10 or 10 euros, that would cause some action in the derivatives etc. Don’t recall exactly what

The DBank offer of a yield of 5% on larger deposits will come back to bite those foolish enough to think trying to grab 5 pfennigs in front of this out of control juggernaught was a good idea

The house of cards has got to collapse sooner or later and DB is TBTS (too big to save).

Germany will destroy itself trying to bail it out.

Time to sort it all out and start again, we are all getting tired of the slow motion train crash that has been going on since 2008.

I ‘m suspect a bail out of DB might cost Germany more than the entire integration of the old DDR.

“I ‘m suspect a bail out of DB might cost Germany more than the entire integration of the old DDR.”

And they wouldn’t be getting anything for their money except bigger and better future opportunities for economic collapse. Investing in East Germany at least generated some financial return.

TBTFs like being TBTF: they can hold the prosperity of entire populations hostage. Allowing the existence of TBTFs amounts to the legalisation of large-scale blackmail.

Merkel isn’t playing ball because she’s still answerable to the voters, which explains why TBTFs are investing so heavily in replacing democracy with corporatism.

I don’t know if there is STILL a DDR- reunion cost deduction on every German pay check but there was not too long ago.

I doubt that anything could be that expensive, and it wasn’t that great an investment. Everything had to rebuilt- it had no competitive industry but worse you had a generation that didn’t easily fit into Deutschland Inc.

About ten years ago a German told me that it was still easy to spot Germans raised in the east.

At the time of unification I had a wealthy German real estate client- he almost had a coronary when he heard the DDR mark would be redeemed at par with the D-Mark

You could have picked that unconvertible toilet paper up for the price of good counterfeit a few months earlier.

BTW: a large part of the DRR’s ‘economy’ were extortionate fees charged by the DDR to supply West Berlin, or to permit it to supply itself, for everything from natural gas to water.

The “solidarity tax” or Solidaritätszuschlag, lovingly called “Soli,” is still in effect, though in 1991 when it was imposed, it was supposed to be just temporary. It now amounts to 5.5% of your income taxes.

In the UK income tax was a ‘temporary’ tax for a war, and the current VAT on heating was a ‘temporary’ tax to pay for the ERM disaster when we all enriched Soros via the ERM.

Really the only way (for the middle class) to avoid too much tax these days is to downsize and get paid less. You still have to pay VAT though, it’s effectively a tax on the poor, unlike income tax that has thresholds.

I’d be interested to hear what the chatter is in the trading rooms of the other banks that do business with DB. I

If that chatter is negative and the traders are staring to tighten up on trades with DB, as well as tighten up on overnight and short term loans, then- Look out!

The thing is that the stock price will go down incrementally at first, until the ‘Lehman Moment’ hits, then it will be dead within days. That’s how fast it happens, all the other banks etc. stop trading with them and it’s all over.

I hope depositors and folks that use them for wealth management are pulling accounts, like RIGHT NOW!

I know I would be. Once the stock waterfalls, it’s too late.

Donald? Hi, it’s Deutsche Bank. We’re calling our notes.

Just wondering – during the Great Depression, those peoples and nations of South America were actually better off without the “overseers” from Europe and the U.S. making policy for them that benefitted some of the people of the latter two entities.

Might it be possible that those of us who no longer live in the fore- and-afterthoughts of the power brokers of the “1%” and their politicians to live lives, more simply of course, without having to do whatever we do so as to enrich that bunch?

Just wondering…

Just waiting for Cramer to recommend a buy and then we know the game is over for Doosh Bank

https://www.youtube.com/watch?v=V9EbPxTm5_s

I half-expect him to pound his fist on the desk and yell at the ECB, “They know nothing, they know nothing, they know nothing….”

Haha Perfect comment Tom

The entire banking system’s business model is based on criminal activity of various kinds. In the United States the velocity of money has plunged to depression-type levels, in part due to the realization that banks are criminal enterprises.

There are approximately $1.3 TRILLION in cash and coinage in circulation with only half being within the borders of the United States of America. According to the UST OCC, in 2015 five banks (Citigroup, JP Morgan Chase, Goldman Sachs, Bank of America Merrill Lynch and Morgan Stanley) had derivatives exposures totaling $247 TRILLION*. Or, for those five banks less $.0025 cash available per dollar of derivatives liabilities.

The Public has lost confidence in the banks. They have also lost confidence in the US government. Anytime the US government investigates any bank it finds egregious criminality. Fines meant to restore confidence depletes bank capital, further sapping public and investor confidence.

The fact of the matter is that the banking business model is built entirely on criminality. It is an impossible task to remedy that fact. Confidence in banking continues to drop. The inability of the government to remedy that further saps confidence in government.

Everyone must understand that if you don’t have physical possession of your assets you have nothing. Either the government, the Con Street swindlers, the banking gangsters or the crony capitalist conporate criminals will steal it or vaporize it.

And…it’s gone. I’m sorry your accounts show balances of $0. Please leave the tellers line so that the next sucker, uh, customer may be served.

Get your assets into your grubby hands NOW or you WILL lose everything.

*Per the UST OCC 2015 report the total derivatives bubble is $553 TRILLION!!!!!

Let’s use our imaginations.

Imagine that in 2008-2009 TBTF banks had been allowed to instantly fail.

Right along with the big boys, a lot of average account holders (not investors in bank stocks) would have lost the “money” that was in their checking and savings accounts. Presumably those account holders would have a record of their accounts and it would have been bone simple for “the government” to determine if these records were accurate.

Now, instead of bailing out TBTF banks, imagine that the various central banks had literally printed cash notes to “bail out” — to reimburse — those average account holders. Yes, they printed the cash currency and snail-mailed it to those account holders.

Now, under that scenario, who would have lost their shirts? The “financial industry” — all of the investors in the banking system and the financial riggers and the currency manipulators, not the average people who had checking and bank accounts.

Average people would still have their cash to spend.

Some banks disappeared. Maybe the home-mortgages that those failed banks had on their books might also have disappeared and the homeowners may have actually become true home owners. What a terrible thought.

The blood-sucking-leech “banking industry” would no longer be controlling governments and the world and we would not be facing yet another “financial crisis” that will require an even more radical experiment in order to keep the TBTF banks alive. What a terrible thought.

Was what actually happened in 2008-2009 better than the imaginary one I described above? What does the future hold for what actually happened?

Just exactly WHO is it that benefited (and will benefit) from those TBTF bank bailouts?

Yes indeed!

Unfortunately Ben Bernanke studied the Great Depression and not the events leading up to 1929.

What did the bankers do before 1929?

They made bad loans and bundled them up into securities to sell them on.

As they could get these bad loans off their books, they could carry on making more and more loans.

Most of this lending was margin lending into the US stock market.

What did Glass-Steagall stop bankers doing?

Making bad loans and bundling them up into securities to sell them on.

When investment and retail banks are separate, the retail banks have to take responsibility for the loans they make as they stay on their books.

What happened when Glass-Steagall was removed?

The bankers made bad loans (e.g. NINJA mortages) and bundled them up into securities to sell them on.

As they could get these bad loans off their books, they could carry on making more and more loans.

Most of this lending was mortgage lending into the US housing market.

1929 and 2008 – debt inflated asset bubbles leading to “Minsky Moments”

it’s called a jubilee.

an interesting idea, liquidating deposits and closing the banks. you could front run it by cornering the mattress market.

This is an unfair situation, one in which DB got singled out not based on actual financial or ethical concerns which are even worse for other players, but because of antipathy towards Germany and its policies abroad. And once the market has found a scapegoat, the process often becomes self reinforcing.

But in the end this could lead to ruin for everyone (except those few well connected players which are leading this smear campaign). Just like the Lehman, Wachovia etc take down enriched a few banks and led to the misery of millions, so will this story go too unless it is stopped. Banking should not be a political arena. Tougher regulation and conservative management can really pay dividends over the long run; deregulation and financial wars not. I’m really worried by the rising international tension and the escalating tit for tat, of which this is a part.

If JPM and Goldman Sachs trading desks scream “This is a screaming buy at $5 a share’,

while doing the exact exact opposite trade, DBank is doomed and will STB. The muppets will be fleeced—again

DB didn’t get “singled out” by the DOJ about the RMBS scandal. US banks got hit first – and harder. Here is how they already settled that scandal:

– BofA for $16.7 billion (via its acquisition of Countrywide)

– JPMOrgan for $9 billion

– Citigroup for $7 billion

– Goldman for $5 billion

– etc. etc.

That’s just the RMBS stuff. They also paid many billions in settlements for other scandals. The amount which DB will eventually accept to settle for will likely put it in 2nd or 3rd place.

BTW, it’s the US entity of DB that is mired in this scandal.

“BTW, it’s the US entity of DB that is mired in this scandal.”

Has Yellen called yet?

Patience: days only have 24 hours.

Will the DOJ take co-co bonds or DB shares to pay the 14 billion?

One thing is for certain, DB will not be allowed to fail at the mercy of market forces.

The best case scenario for the masses is that Germany nationalizes the bank, sells of the healthy parts of the company to the highest bidder, lets the bad debt default, ensures that depositors are made whole, and the whole time reminds the markets that liquidity will be provided as needed and that the banking system will be stronger after the process is complete. This would accomplish many great things. One, other banks would see that they are not TBTF and they would conduct business accordingly. Two, the German government would be prove that they are serious when they say there will not be any bailouts. Three, bond risks will be re-priced as the markets decide who is most likely to pay back their debt obligations.

But that scenario is extremely unlikely. World markets would crater.

The most likely scenario is business as usual with the taxpayers paying for a bailout.

How is it realistic to even conceive Deutsche bank could be bailed in or out at this point? It’s insolvent! The theoretical exposure DB has to derivatives is in the untold of €trillions. It’s leveraged 40X and 58% of German GDP. There is no way it can be bailed out or in. Maybe the EU could declare a debt jubilee, but who is going to step up and take the hit? and what about the Italian banking system…? If the EU attempts to print its way out, it will crash the currency as there simply is not enough value in the system to handle it.

The passive way it’s being handled in the media reminds me of TEPCO and the fall-out (oops a pun) following the triple melt-down at the Fukushima plant. They really have no way to publicly address this and the truth is so heinous, they just sort of seem unwilling and helpless to point it out. The solution lies beyond the realm of knowledge anyone possesses to deal with this in any feasible way.

one thinks that the ec is adopting unorthodox policies, but they are not. they continually do the wrong thing. that is not the definition of unorthodox.

there i said it. i won’t say what i am thinking about the value of DB, but it is unduly affected by geopolitics.

As I understand Chaos Theory, getting in front of the rising chaos will end up like the student in China crushed by a tank. Until the chaos reaches near totality and order spontaneously arises from it, it will sweep away everything in its path. Not good, since the global banking structure is in the crosshairs. Eventually a new system will arise out of the ashes and say ‘never again’. Until next time.

“One of the greatest human misconceptions is that there is intelligent life on Earth.”

Rotflmao

How does a DB failure work for german companies with large loans outstanding frm DB?

Daimler-Benz for instance might be the larget borrower from DB. How would a DoucheBank failure impact Daimler? And other borrowers?

Current borrowers would be fine on current loans. But if they need new money, a jittery DB loan officer might not be willing to take risks and extend loans to weaker companies. Daimler will likely be OK. They can borrow anywhere, including from the ECB directly (via private placement). Shakier companies and smaller companies are going to have a huge problem getting a teetering DB to lend to them.

If DB collapses and doesn’t get bailed out, credit markets freeze up globally and no one can borrow for a while.

No bail in allowed. We just make sure that you will lose it through the market.

I’m seeing a lot of comments like ‘Let the banks fail but bail out the depositors’. As conveniently just as that sounds, it’s not remotely a realistic scenario. Printing to bailout private clients of a bank, at the expense of devaluing a currency for everyone, is not only socialism in it’s most extreme form but would guarantee hyperinflation. I know that’s a term thrown around a lot, but making every depositor ‘whole’ in scenario where a country’s largest banks have failed is simply not possible w/o out devastating a currency.

So (as unpopular as it still is), what they did in 2008 was the only realistic option, along with QE1. But the no-way-out scenario we have today was that QE, ZIRP & easing never stopped. Instead it spread like a virus throughout central banks and became defacto policy. So the bailouts will start again but this time there will be an unending line of banks, pensions, insurers & corporations all waving a white flag for rescue. The EU & ECB know that once it starts, it won’t end…and they won’t say no until the currencies have become devalued to the point that confidence is lost. Then it’ll be the SDR everyone looks to as the savior to bailout the CBs. They’ll print into the 100’s of trillions and confidence there too will be lost. Only after adding gold (at a seriously revalued price) as the 6th ‘currency’ of the SDR will confidence begin to return. And only then IF the gold ratio to all 5 other currencies is ‘fixed’ so that no one can print w/o adding their gold to the kitty.

/ Did you know that in 1920’s Weimar Germany, patrons would pay for their meal beforehand because the cost would have risen significantly by the time they’d finished?

In theory, since 1 January 2011, there is a 100,000 EUR deposit insurance for German banks. The Bundesverband deutscher Banken as they call it. “The protection ceiling for each creditor is 30% of the liable capital of the Bank …”

I wonder how many Euros are on deposit at DB that would have to be insured if the bank collapses.

The powers that be do seem to be aligning for a global SDR fiat currency. The almighty petro-dollar still rules today, but China and Russia are trading together in non-dollar transactions. China is issuing SDR bonds.

2017 will be a year of upheaval and mayhem.

I would suggest the geo-eco-political collapse will occur in about a year from now – September-October-November 2017, just after all the key elections in Europe (Netherlands, France, Italy (likely), Germany, Spain (likely) are out of the way) and just in time to sink the world into a great economic uncertainty heading into 2018 – and the Russian Presidential Elections!

Target No. 1 – V. Putin.

Good timing isn’t it? It’s just a matter of whether they can hold out for another 12 months of can kicking.

Given the expertise we’ve seen in can-kicking I can’t see why another 12 months can’t be managed.

Anybody thought, if Germany lest DB go under, the Italians and the rest of club med, are not going to have any choice in the matter of their dinosaurs with massive NPL portfolios.

Germany has paid a little, to force others to pay a lot, on several occasions, in these ECB, EU financial games.

I have written this before, when discussing DB, early in the Piece of its issues..

DB wicked web

http://wallstreetonparade.com/2016/09/the-new-banking-crisis-in-two-frightening-graphs/

Honest question: When I look up Germany’s GDP for 2015, I find about 3.4 trillion dollars. When I look up DB’s 2015 revenue, I find about 47 billion dollars. When I look up DB’s EBITDA I get about 4 billion dollars. When I look up DB’s market cap, I get about 16 billion dollars.

None of these are small numbers, and I’ve been following this keenly… but I don’t see how DB’s balance sheet could equal “58% of Germany’s GDP.” Could somebody spell it out for me?

“Balance sheet” means assets, liabilities, and capital. Revenues and earnings are part of the “income statement.”

DB has €1.8 trillion ($2 trillion) in assets. That’s where the 58% comes from.

Here is the latest earnings release. For the assets on the consolidated balance sheet go to p. 14

https://www.db.com/ir/en/download/FDS_2Q2016.pdf

Wow. Thank you.

174,940,000,000 Eur, Other assets.????????????

428,411,000,000 Eur Net loans.??????????

9,907,000,000 Eur Goodwill. ??????????

Three line items that are not well documented, and will under pressure realize 20% of their book value???

Then there is the 615,426,000,000 Eur Positive market values??????? from those thing that attack the Hysterical ones in volume(so Shush, about those).

which makes over 50% of their assets recoverable, at less than 20% of book value.

Another way to deal with DB could be to put it under state supervision, in bankruptcy protection. Which means nobody but depositors (who get everything, get paid anything for a very long time.

Yes. It looks terrible. And no one outside the bank – and maybe even no one inside the bank – knows exactly what’s behind these numbers.

Goodwill is an expense that has been parked on the balance sheet to be written off later.

Could Merkel let DB fail to blow up the current financial system on purpose?

The motive would be to get rid of US occupation in general and to stop the flooding with so-called refugees that are immigrating into the welfare system.

Moreover, the German industry exports a lot to Russia and imports oil and gas from russia. US imposed sanctions hurt the industry.

A new financial system would be based on gold and silver; few years ago German mainstream tv published a poll that private Germans hold some 8000 tons of gold and 28000 tons of silver. If true that should do as foundation for new money.