Atlanta Fed’s GDPNow kisses the Rosy Scenario goodbye.

After a crummy 4th quarter, everyone was looking for a turnaround. Annualized economic growth in Q4 of 1.4% was way below the “stall speed” of 2%, a growth rate below which the US economy has trouble staying airborne. After having wrongly hyped it for five years in a row, Wall Street economists aren’t even talking anymore about “escape velocity,” that elusive economic boom that would set in miraculously in the spring.

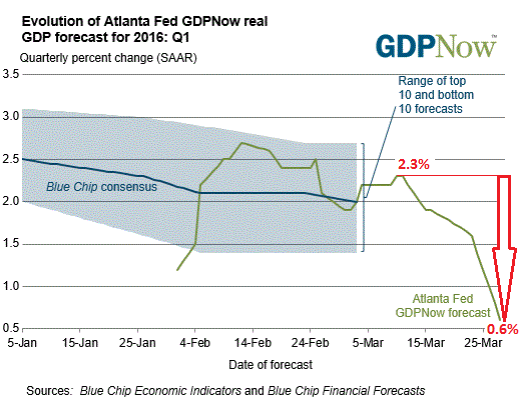

Nevertheless, forecasts for the first quarter by blue chip economists in early January ran between 2% and over 3%, with the “consensus at 2.5%. Even the Atlanta Fed’s GDPNow forecast — a strictly data-driven model of the first estimate of GDP, however off it might be — figured by mid-February that growth in Q1 would come in at above 2.5%.

But since then, more data on January and February has been reported. Mid-March, the GDPNow forecast started to deteriorate. By March 24, it had dropped to 1.4% GDP growth — once again below “stall speed.” And with today’s data on consumer spending and the contribution of exports to GDP, it plunged by more than half to 0.6%!

This plunge in the forecast from 2.3% to 0.6% in a little over two weeks — which I indicated on the chart below in red — can give someone the willies! It’s where GDP growth begins to flirt with a recession:

Culprit one was a shot of reality from the rest of the world: the advance report on US international trade in goods (excluding services) from the Census Bureau. The full trade data for February will be released next month. In February, the US trade deficit in goods rose 1.1% to a seasonally adjusted $62.9 billion, the fourth month in a row of increases.

“The forecast for the contribution of net exports to first-quarter real GDP growth declined from –0.26 percentage points to –0.52 percentage points,” the Atlanta Fed’s GDPNow comment explained.

Culprit two was the struggling American consumer. Consumer spending, at over two-thirds of the economy, is the biggie. It includes things like healthcare, which itself makes up nearly 20% of the economy. Turns out, consumers unexpectedly cut back on purchases of goods, and total personal outlays edged up a measly 0.1% in February from January, according to the Bureau of Economic Analysis. And January was revised down from a respectable 0.5% growth to a measly 0.1% growth.

Today’s report was a big disappointment for our blue chip economists. It induced the GDPNow model to slash its forecast for Q1 real consumer spending growth from 2.5% on March 24 to 1.8% now.

There was another wrinkle in today’s report on personal income and outlays: While government wages and salaries rose $3.5 billion, after rising $4.6 billion in January, private wages and salaries fell $12.9 billion in February, after rising $41.9 billion in January. In total, wages and salaries for the month fell by $9.4 billion. That’s not helpful for consumers.

GDPNow is essentially a computer model. The purpose isn’t to forecast actual GDP but the government’s “first estimate” of GDP. Forecasting GDP accurately would be a stroke of luck. But the model has the advantage that it isn’t a function of human interpretation of incoming data. It’s the model that decides, not economists paid by Wall Street to hype stocks and bonds or other financial instruments to unsuspecting bystanders while extracting fees coming and going.

GDPNow forecasts can be volatile early on in the period since they react to incoming data. But as it approaches the end of the quarter, it gets more accurate. For now, only January and February data are included, and it’s not looking exactly promising. March data would have to be miraculously strong to pull this one out — but miracles, we’ve learned, have become exceedingly rare in the US economy.

In this debt-fueled economy, the “hangover from years of lenient credit may become painful,” according to ratings agency Standard & Poor’s. Read… “Spike in Defaults”: Standard & Poor’s Gets Gloomy, Blames Fed

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

All this dropping number means is that soon bad news will be good again, at least if it gets the fed to ease some more.

Incidentally, I’m still waiting for one of the prez candidates to announce a fiscal stimulus program. It can’t only be monetary stimulus. And there are plenty of worthwhile projects that would quickly pay back more than they cost: infrastructure improvements comes to mind, but also increases spending on research or an effort to rework our intellectual property environment. Chinese espionage is very costly; paying a few billions to subsidize companies to beef up digital security would pay for itself almost immediately.

Spending money to fund Start ups / tech incubators would probably also pay for itself pretty quick.

Very droll.

Jonas

Why not just pile $100 in a heap and set them on fire?

Oh, wait, that’s what you’re proposing.

Never mind.

How about projects like Seattle’s Sound Transit spending 10.2 billion to extend it’s subway line 3.2 miles? Imagine all the pockets that could be lined and all the wheels that might be greased with more stuff like this.

At least we get something useful for our money. Sound Transit’s Light Rail opened a new extension of the system a couple of weeks back. It makes it a whole lot easier for thousands of people to get around without cars. We need a whole lot more of this sort of infrastructure. I’d sure as hell rather spend the money on this, than on F-35s, invasions of Iraq, bailouts for banksters, and the like.

It’s a near-certainty that CNBC shills will soon be calling on Ms. Yellen to rev up the printing presses…

The trouble is that money-printing only enriches those who are already rich…

And the few who are very rich can’t consume fast enough to make a difference…..

That’s how it’s been, what with QE and such. But it’s not up to the Fed to stimulate the economy. That’s government’s business. The Fed does what it’s told, including QE. It buys debt.

Honest statistics show that GDP growth has been negative since the present recession began in 2005.

http://www.shadowstats.com/alternate_data/gross-domestic-product-charts

Really, who you going to trust, ShadowStats or central banksters?

Walter i will definitely go with John Williams at Shadowstats every time

Meanwhile this little darling from the Blackstone cradle just stole $95M. I sure hope the SEC starts some serious clawbacks and jail time for these jerks.

http://www.zerohedge.com/news/2016-03-28/partner-blackstone-spun-private-equity-firm-arrested-charged-stealing-95-million

I guess I need to get a government job!

i’m generally concerned, but we are the best neighborhood in a bad town.

that makes me optimistic. i have to be.

“After a crummy 4th quarter, everyone was looking for a turn around.” Uh, no. Not everyone & not most of the people I come into contact with on a regular basis.

Beside all the financial shenanigans that most of us readers already know about, here’s a thought. There are many (mostly) part time workers where my wife is employed. Most of them don’t have health insurance & have a small enough income that they normally get a refund???? come tax time. This year, reality has kicked in & the uninsured aren’t getting any funds. Instead, they are getting fines. I’m thinking this has happened to millions of people so would this be a large enough cumulative sum to make a dent in the consumer spending ‘stats’? Would the realization amongst millions of people that they aren’t getting a ‘tax return’ cause them to be extra cautious regarding their spending habit adding more downward pressure on consumer spending? Will this put a dent in auto sales? Are there any verifiable annual tax refund data that could shed any light ? Maybe I’m way off base, anybody have any info?

Many of the guys my husband worked with in Florida went from spending about $300 a month for a family plan to $700 a month under Obamacare. The deductibles are now $5000, not a few hundred like before. They are spending all their disposable income on health insurance that is unusable. I don’t know anybody working a part time job that has any kind of health insurance, nada, nothing. A part time job barely pays for the gas. This is why no white working class guys will vote democrat in the coming election.

I predict that at some point, people will just cease to file their taxes, seeing as it is ONE BIG FRAUDULENT SCAM, with NO positive outcome!!

Just wondering what the status of the average American’s credit card debt is? You can’t buy crap you don’t need with money you don’t have when you have maxed out credit cards.

Another thought and let me reiterate, I am not an economist and my knowledge of accounting is limited. I have the grades from my time in C&BA to back up my statement. Taking a break from those courses with an earth science class found me a home in geology. Liked rocks better and had the extra benefit of walking around in flannel shirts and jeans with a cool rock hammer stuck in the belt.

My question regards the growing number of auto leases. Seems to me that leasing puts the consumer in the position of a never-ending car payment. I assume this boosts GDP for the auto sector, but possibly shorts other potential purchases of goods and services, especially with seemingly flat wage growth. So, is this a reasonable analysis, or am I off base?

night train No you are on track alright and in a saner world those people would be taking mass transit instead of owning(and i say owning lightly) a car that they can not possibly afford just wait till the price of oil stabilizes at a much higher level many of these people will be up the proverbial creek

To both Night Train and Frederick: Average credit card debt is $15k. Talk about credit slavery…

Regarding not owning a car: Here in Texas you could not survive without a car. In a few hipster areas you can walk to a coffee shop,bar and overpriced sandwich store but that is it. You still need to drive to your job or grocery store. With such a huge geographic sprawl, mass transit is not possible unless you want to travel 2+ hours by bus/train versus a 30 minute drive time. And that is only offered in very limited areas.

Regarding leasing: I too have noticed the increase in lease offerings and just don’t get it. Allowed miles are very limited and one is charged $.50 a mile for going over. Imagine how fast that would add up. For a company car sure…but a personal car?

I have a vendor from Austria who visits me in Texas once a year (among his other travels worldwide) and it is alway interesting to hear his view of current events, and the economy. We were talking about cars, spurred by his interest in how the VW scandal would impact US buyers (I said no one here cares) and then he brought up BMW.

BMW offers all of it’s employees a new car as part of their benefits package. They turn the car in each year for a new one and then that car is offered for sale at a steeply discounted price or put in a leasing pool. BMW even has a website to search for what you want. He said he always buys his car that way and milage is extremely low. The leasing options are so good that he said practically everyone drives a BMW….even college students. So BMW has it’s own built in economy of churning cars nationally. That works in Europe where they are not doing much driving. This business model will not work in the US because everything is so spread out and we don’t have the option of taking a train to a different city/country on weekends. Seeing all of these new leasing adds recently makes me wonder if the US is trying to copy this model to keep those new cars turning in the market place. It will not work here and will end badly for all.

Does anybody really take government statistics at face value? I’m by no means anything approaching a financial expert but more just an observer of the world around me. I can tell just by looking around that the whole show is collapsing. I just, depending on my mood, either laugh or or get pissed when I think about how much manipulation of the sheeple goes on through the government and the MSM.

Bill: I think many of us feel the disconnect between what we observe and what we are told by people and institutions who have serious conflicts of interest. We now know that the system we suspected of being gamed, is gamed. I enjoy Wolf’s site because he, those who contribute and many who comment here deep dive the data and question the assertions put out for public consumption. When I hear some of the BS the financial establishment spoon feeds the general public, I too go between laughing out loud and being mad enough to bite a ten-penny nail in two.

night-train: About the only solid data that I can look at with trust is that I’m way worse off than I was ten and twenty years ago. Now, granted, I’m in a particularly tough business due to the fact that the government is now controlled by ENGOs, at least in the area of fisheries. On a side note, regarding your comment about auto leasing, I read the other day, that Sub-Prime used car loans are defaulting at a higher rate than ever previously. To me, that shows that those in the lower end of the economic scale are really in trouble since their car is basically all that they can call their “own”, that is, besides the 64″ Plasma TV in their subsidized apartment…

Those TVs are paid for weekly on a lease to own scheme. So, no they do not own those either.