NAR blames ‘anomaly’ for plunging sales then destroys the theory

We’re always leery when something expected happens prematurely. We’ve seen home prices soar for years while real incomes for the lower 80% of households have declined. That math cannot work forever. We’ve seen sales hitting a wall here and there. And we expected that this would eventually percolate up in nationwide figures. But we didn’t expect this to happen so soon.

And in November it suddenly happened. We’re scratching our head. Could this already be the end of Housing Bubble 2?

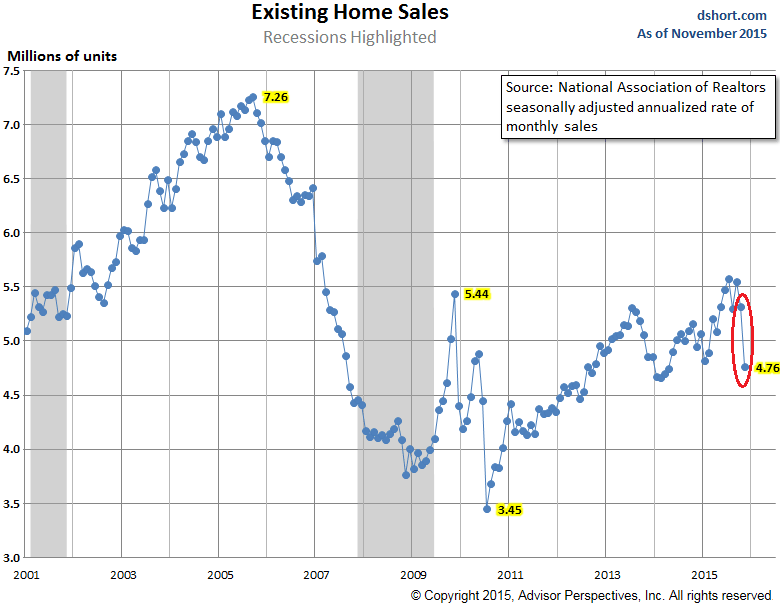

November existing home sales – completed transactions of single-family homes, townhomes, condominiums, and co-ops – plunged 10.5% from October to a seasonally adjusted annual rate of 4.76 million units, according to the National Association of Realtors, the lowest sales rate since April 2014, and the worst plunge since July 2010 (-22.5%). And sales were down 3.8% from November last year.

It shocked and appalled forecasters. The Investing.com consensus was 5.35 million units, just above the prior reading, as consensus forecasts usually are.

This chart by Advisor Perspectives shows the November plunge, circled in red:

So the search for a culprit is on. The obvious reason for slowing home sales – that prices have reached a level where more people cannot buy, given their stagnating incomes, and where others refuse to buy given the ludicrous prices – was dispensed with by mentioning “affordability” in passing.

Turns out, the report also showed that the median existing-home price in November jumped 6.3% from a year ago to $220,300, the “45th consecutive month of year-over-year gains.” Meanwhile, real incomes for the bottom 80% of households, the largest group of home buyers, have declined for years.

But it wasn’t the primary reason, according to the report. For once the NAR didn’t blame the weather, which had been too balmy. There were “multiple factors” that led this plunge, “but the primary reason could be an anomaly….”

Blaming an “anomaly” is always good.

The industry has the new “Know Before You Owe rule” to deal with, which brokers have long known about and have prepared for. Nevertheless, couched in words like “apparent,” “probably,” “may,” and “possible,” the report blamed “an apparent rise in closing timeframes that may have pushed some transactions into December.”

They supported this with survey results: “47% of respondents in November reported that they are experiencing a longer time to close compared to a year ago, up from 37% in October.”

Other data points were mixed. Signed contracts were “mostly steady in recent months.” Homes “typically” stayed on the market for 54 days in November, down from 65 days a year ago. Housing inventory fell 3.3% to 2.04 million units, which was 1.9% below November last year.

OK, but sales in November were 3.8% below last year. So that inventory-to-sales ratio has deteriorated year-over-year. And unsold inventory rose to a 5.1-month supply at the current sales pace, from 4.8 months in October.

Only 30% of the homes were sold to first-time buyers. “Continued absence from the market,” is what NAR called this phenomenon. First-time buyers were once upon a time considered the foundation of a sound housing market. At the time, they bought over 40% of existing homes. But forget that.

Instead, all-cash sales rose to 27%, up from 25% a year ago. Individual investors bought 16% of homes in November, up from 15% a year ago, with 64% of all investors paying cash.

So given this mixed data, the report found that “it’s highly possible the stark sales decline wasn’t because of sudden, withering demand.”

“Sudden withering demand” would be a national tragedy.

It’s possible the longer timeframes pushed a latter portion of would-be November transactions into December. As long as closing timeframes don’t rise even further, it’s likely more sales will register to this month’s total, and November’s large dip will be more of an outlier.

Let’s hope so. And we need to wait for the December report before we know if it was an “anomaly” or “sudden withering demand.” But um….

Here is why we have trouble believing the “anomaly” theory. The delay in closing sales – the “anomaly” – should affect all sales equally, including sales of single-family homes and condos, since the new rules apply to mortgages on all types of homes.

But here is what happened:

Single-family home sales plunged 12.1% for the month – worse than the overall 10.5% plunge – and 4.6% year-over-year. But condo and co-op sales rose 1.7% for the month, and they also rose 1.7% year-over-year.

Suddenly the “anomaly” theory falls flat on its face. We don’t know why existing homes sales plunged in November. We’re still scratching our head. But blaming the rule changes, when only single-family home sales plunged and nothing else, makes zero sense. So we might try one of the other reasons and perhaps even dabble with that “sudden withering demand.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

…”makes zero sense”…

That’s him alright, NAR chief economist, Larry Yun.

“Rope a Dope.”

I still think it is all about income. Unemployment is reported to be down in Florida and it probably is, but the new jobs pay less, a lot less. These days it takes awhile to find a house to buy, and if your income falls while you are looking, you may have to walk away.

While foreigners are buying in Florida, the immigrants are buying back home in Cuba and Latin America. It’s not a big trend but I hear about it here and there.

Here is the trend Petunia.

http://www.zerohedge.com/news/2015-12-22/9-10-largest-us-occupations-pay-miserly-wages

Merry Christmas.

Come to Australia and win in the workers’ paradise……..

That is if you have the ‘right’ skills:

plumbers, electricians, bricklayers, and especially construction workers.

How about the king of labor trade: the Construction worker in Victoria?

They pull in an average of A$129,000 a year for UNSKILLED workers and around A$149,000 a year for SKILLED workers.

And as this is the holiday season the wage for work on Christmas and Boxing Day holidays for casual retail workers?

Only about A$75 an hour!!!

It’s about time for the real estate cycle to correct. Without relaxing mortgages or increasing incomes, it’s hard to imagine something that will boost the market at this point.

The point is the real estate sector was NOT ALLOWED to complete it’s cycle correction by the massive injection of freshly printed fiat, compliments of the Fed.

Without the Fed taking on all that toxic MBS from the banks and stuffing Freddie and Fannie to the rafters with it, the housing sector along with the banks would have failed along with the credit bubble. Instead they were “saved” and the liability shoved onto the backs of the taxpayer.

Not sure if it’s real or not, but a local friend told me that tax rules will be modified so that foreigners will pay the same amount of tax as local when purchasing a property. Currently foreigners pay a higher tax.

My friend’s suggesting that I buy a house to front trade future demand.

Globalization is a euphemism for an Elysium-like, global, neo-feudal rentier-socialism in which the top 0.001-1% are the feudal (dark) lords, the next 5-9% are their ministerial intellectuals, financier oligarchs, plantation managers, and skull-crushing, martial, police-state types, and the rest of us are neo-feudal peasants/serfs increasingly at risk of loss of income and purchasing power for subsistence.

Sell everything of liquidation value, pay off your debt, and be a happy car camper. You’ll be worth more than the bottom 89.999999999% of your peers, no doubt.

Better yet, if you have an elderly or Boomer parent, sell everything of liquidation value and move in with them and avoid having to shower at LA Fitness or 24-Hour Fitness, not that there’s anything wrong with that . . . :-D

Same as it ever was . . .

Power to us peasants!!!

and will this car have a refrigerator in the back, or will you just hunt and gather by the day?

perhaps a truck would be more suitable, with a gun rack.

So I see the Fed no longer prints “money”.

Why print money in a cash free economy!

Just edit that database…

Hmm…possible reasons (beyond the obvious one that people don’t have the income to support increased prices when interest rates aren’t falling anymore and all their living expenses are rising steadily…including healthcare…where many are finally seeing the bait-and-switch of Obamacare)”

1) How about Congress considering lowering the tax on real estate for foreigners (which was passed last week btw) causing delays in purchases by said foreigners….especially in the major metro areas which were driving the “national” averages higher.

2) How about the fact that the devaluation of foreign currencies against the dollar is seen to already be extreme enough over the past 3 months that foreigners see less reason to bid on “expensive” U.S. assets. (i.e. foreigners may expect the Dollar to pull back somewhat)

3) How about the fact that the meltdown in the U.S. oil patch (where they were paying extremely good wages (including overtime) as little as 9 months ago) has changed the buying confidence of individuals directly or tangentially related to those jobs (probably 200K direct full-time employees, another 200K direct part-time employees, and 8x this tangentially related).

4) How about investors in the junk bond market finally getting wise to the issue of “return OF capital” (repeat lesson from 2008!) as mortgage-related junk bond issuance has started backing up in to the financing pipeline at the investment banks…resulting in less enthusiasm by said investment banks to buying extremely low-quality loans. In this event, mortgage originators are faced with being forced to INCREASE quality of their loan….which INCREASES the cost of mortgages and can (dramatically) lowers the # of people who qualify. (The real estate profession would never reveal this (until the data is obvious) as it would cause POTENTIAL buyers to delay or abandon their search.)

Valuationguy

all good points. two main reasons:

1.tightish credit, high down payments, and idiots who don’t realize a 30 yr mortgage at 4% will be dirt cheap in 10 years. and yes, the gross numbers of well-employed stable buyers.

2. that idiotic TRID.

At least in America they still let out some negative numbers.

And the charts, disagree with the BS, they let out with those negative numbers.

Charts dont lie only, the interpreters, and the people faking the positive charts, do.

Copper, Lead, Tin, Aluminum, Zinc, Silver, suggest that the Story, that the price of silver is being held down, is that, and that the price of gold, the big diverger, is very very wrong.

The prices of silver and gold would be higher if investers thought they were worth more. Obviously that’s not the case so don’t be looking for conspiracies where there are none.

Nothing wrong with the price of Silver.

I said,

“The “Fairy story” that the price of silver is being held artificially low, is a “Fairy story””

It is put out by the same people, who have hyped they price of gold, to completely unrealistic, and untenable level’s, and wish to keep it there.

The “Divergence” between Gold and all the other metals mentioned, supports this.