The unintended consequences of NIRP.

After negative interest rates, called “punishment interest” in Germany, became established in Europe as the latest method of flogging savers until their mood improves, all kinds of absurdities have seen the light of the day. For example, bailed-out national governments can now fund their deficits at negative rates, extracting money from their bondholders, rather than paying them. Perhaps the coolest notion was that banks would be “paying your mortgage.”

That may have been an illusion – at least in Switzerland, where the Swiss National Bank slashed its benchmark rate on “sight deposits” to negative 0.75% on January 15, the day of the epic “Frankenschock.” That day, the SNB abandoned its cap on the franc, which within the blink of an eye, soared nearly 40% against the euro and the dollar, wiping out currency speculators in the process and shaking up global currency markets.

The negative benchmark rate had the effect that by now, 70% of franc-denominated corporate bonds trade with negative yields, according to Credit Suisse. And the theory was that mortgages would certainly head that way.

Initially, interest rates on 10-year fixed-rate mortgages plunged to about 1%, with some quoted below 1%, and folks were already speculating about 0% mortgages or negative-rate mortgages. But then something funny happened on the way to the bank: unintended consequences kicked in.

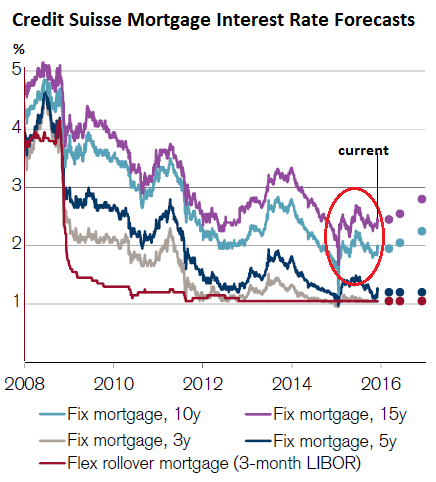

Swiss banks somehow decided, for whatever inexplicable reason, to make a living. That’s hard to do for banks when they lend out money in a negative interest-rate environment. So the biggest Swiss banks accomplished a unique feat: they’ve jacked up mortgage rates since then, with the 10-year fixed-rate now at about 2% and the 15-year fixed-rate at about 2.5%.

And they expect mortgage rates to rise further. Credit Suisse, in its latest report on mortgage rates, laments that the “Swiss economy continues to suffer from the strong Swiss franc” and that the economy in the third quarter “stagnated on a year-on-year basis.” So it expects that the SNB will “keep key interest rates at their current level.” And yet, it forecasts that over the “12-month horizon,” the 10-year fixed rate will rise to 2.3% (blue line) and the 15-year fixed rate to 2.8% (purple line):

This rise in mortgage rates “highlighted how unconventional monetary policies are producing perverse and unpredictable effects in European banking,” the Financial Times pointed out.

“We had some explaining to do why [mortgage] rates were not moving in parallel,” Paulo Brügger, treasurer at Raiffeisen bank, told the FT.

Switzerland is a country of savers. And their deposits are, according to the FT, “the most important source of funds for Swiss mortgages, a market dominated by UBS, Credit Suisse, ZKB, and Raiffeisen.” Turns out, negative deposit rates for retail bank customers would create all kinds of turmoil.

“If we introduced negative rates for client deposits, we could probably close the shop,” Brügger said. “It would create a huge noise with clients. They would never understand.”

The fear was that retail depositors and savers would yank out their money if they were charged for their deposits and stuff it into the freezer. So the banks decided to spare them the pain of confiscatory negative rates and instead make it up somewhere else.

And there was a another issue for banks, on the cost side of the equation. The FT:

At the same time, the costs of financing mortgages rose because of the effect negative interest rates had on capital markets. Banks had to pay a higher price to use market instruments to hedge the maturity mismatch between short-term retail deposits and long-term housing loans. As a result of increased hedging costs, mortgage rates rose.

“The market response to negative interest rates was highly logical because of the value of retail deposits,” UBS finance director Tom Naratil told the FT. “The bigger question for us was: would the other banks follow us or would they look to pick up market share?”

No worries. Now the Swiss banks are in sync: ironic as it seems on first blush, mortgage rates will rise further, not despite, but because of the SNB’s negative-interest-rate policy.

This absurd NIRP environment has had another perverse effect: issuance of franc-denominated corporate bonds by non-Swiss companies has plunged 28% year-to-date from the same period last year, to CHF 18 billion, on track to be the weakest year in Dealogic’s data going back to 1995.

It seems investors just don’t like being charged for lending money to risky borrowers – with the only hope being that rates will drop even further, which, as mortgage rates are demonstrating, is not guaranteed. Faced with soft demand for these rip-off bonds, the players in this game are keeping issuance down to avoid pushing up yields.

As the Swiss mortgage debacle shows, markets can be recalcitrant and re-develop a will of their own when things get too absurd. And they can act counter to central planning. Ah, the unintended consequences of NIRP. Absurdities breed absurdities, and they’ll breed many more surprises.

NIRP is already in the toolbox of the Bank of Canada which has embarked on an all-out currency war. In another perverse side effect, there are clear winners: rich Chinese who buy homes in Canada. Read… Bank of Canada Crushes Loonie, Creates Mother of All Shorts

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Funny how this Poloz jerk fresh from the BIS school of, do we screw em and how is running contrary to Mr. Yellen’s rise of a measly quarter. Watching to see how the SNB screws the customers before diving in himself and calling this crap, tools!

Poloz is not an original thinker, second rate speech reader with out the prompters.

Again, a leopard cannot change his spots…

http://www.bankofcanada.ca/wp-content/uploads/2015/12/remarks-081215.pdf

Throw them all in jail where they belong.

The bank of Canada acknowledged that Canadians are piling on mortgage debt faster that their incomes. Statistics Canada reported Monday that household debt hit another record high in the third quarter, with debts reaching 163.7 per cent of incomes, up from 162.7 per cent in the previous quarter.There are roughly 720,000 Canadian households with debts equal to more than 3 1/2 times what they earn every year, the central bank said Tuesday in its semi-annual overview of the financial system.

The share of such indebted households with debts totaling more than 350 per cent of their annual income held has doubled to 8 per cent from 4 per cent since before the 2008-09 financial crisis.

And 40 per cent of all household debt in Canada is now in the hands of households with a debt ratio of more than 250 per cent, up from 28 per cent before 2008. Twenty-one per cent, or a total of $400-billion in debt, is held by Canadians with debt ratios of more than 350 per cent.

Some nice numbers for “responsible” Canadians. Dark clouds are here already and perfect storm is brewing.

American congress for the first time in history is debating on allowing sale of US oil outside of USA. This is going to lower price of oil even further down, due to surplus on market.

Just think for moment what is going to happen in Canada if oil stays this low (and more likely go lower to $20-25) in next couple of year.

re:

“American congress for the first time in history is debating on allowing sale of US oil outside of USA. This is going to lower price of oil even further down, due to surplus on market.”

How do you figure since the US produces around 45% of its needed and used petroleum energy? Plus, Canada remains the US largest supplier of petroleum and has been forever. If anything, it will raise domestic prices in the US higher.

The push to sell American energy is a push to keep America buying oil in the ME. If we stay tethered to Arabian oil, we must maintain a presence in the ME. The same interest who benefited from that policy in the past will benefit in the future, and it is not the American public.

Well said. The military industrial complex has so much more influence over policy than most anybody cares to acknowledge

We have had a problem with our Governors. Both Mark Carney and Stephen Poloz are overly talkative, overly reactive. The weekly fireside chat is unnerving.

But Carney was incredibly lucky. His tenure overlapped the oil/ commodity bull market. It died almost the day he left. The position could have been held by a blow-up doll, the Canadian economy would have been fine.

But even Carney was slapped down early on by his former boss, former Governor Dodge, who said that Carney was ‘dreaming in technicolor’ with his overly optimistic projections of growth.

For his part Carney, in his new job as Governor of the Bank of England ( his first real job) has been told by more than one columnist that the job

does not include a weekly column.

The British are less into American-style PR than Canadians and do not like too much chat from their leaders.

Poloz needs to demonstrate a STEADY hand on the tiller, which is incompatible with announcing hypothetical jibes into hypothetical sea changes.

And please, it has been established that the low $C has done next to nothing for Ontario’s manufacturing. But every Canadian has to cough up $4.99 for broccoli (last week) and 4 bucks for a lettuce, etc. etc.

And Canadians of very modest means like to take the occasional trip to Arizona, Florida etc. during our winter. I’ve been told by more than cashier that it can’t be done with a 20% currency surcharge.

If the C$ drops below 70 cents US again, it is time to reconsider its utility as a store of value, which is one requirement of a serious currency.

PS: if the CBC’ s John Brown should be browsing this space, as we know he does. he may borrow the above without complaint or even a squeak from me.

Good points, Nick.

That is why we have one very large freezer full of home-grown vegetables, and one full freezer of salmon and chicken, caught and/or grown by us as well. Plus, canned supplies and full pantry. Oh yeah, we have a 10 year supply of wood in sheds for heat, full bank accounts and no debts with cash on hand. We bake our own bread and read at night or play music instead of clubbing and spending. Our big treat is a weekly lunch in town. My kids have also been brought up with this same mindset and are learning to be sceptical of all rosy promises made by Govt and corporate interests. It is also curious that many people in my rural valley share the same value system of being prepared as much as possible and being self-reliant with strong community relationships. Of course many of these folks have gone through previous tough times and have been screwed by Govt policies, (my east German refugee friend is a ready example).

Canadians need to remember where they came from and the struggles made by people in our past that created what we now take for granted. There is a big difference between adequate housing and universal medical coverage to the many superficial and debt-slave values of today. Will your world end if you don’t have a $600 dumb-phone and onerous cell plan? No. Do you need the million dollar fixer-upper? No. Do you really need a 35-45-or $80,000 Beemer to get to work and show off your success? Of course not.

The coming Canadian pain will be felt most by those who lost their way and believed in consumerism hype. Debt…have it now, all of it now, and pay later. Well, now is the time to pay the piper.

Who remembers the Canadian tradition of the ‘layaway plan’, you know, where the shop owner puts the product away for you on a back shelf and you pay for it a bit at a time until you own it and can take it home?

As an aside, I ran in to a young man who I knew years ago when he was a teenager. He wasn’t the sharpest knife in the drawer, but he was focused. He now drives a truck for a local lumber yard that I buy from. His wife works at a Home Depot, and is also quite lovely. They drive a beater truck and own their own home in a modest part of town. He does renos on the side for extra cash. They are 26 years old. Those are the new successful Canadians…the same as they have always been.

regards

The BNS (forgive me, but I’ve been accustomed at using its French title) has become more and more detached from reality in recent decades.

The Swiss economy, even more so than the German one, has long done very well with a strong currency: back in the 50’s and 60’s, when the franc was one of the strongest currencies around, Swiss companies made an authentic fortune selling industrial tooling and machinery to customers all over the world, with Japan and Italy being particularly enthusiastic buyers despite the unfavorable exchange rate.

Even when Japanese machinery started flooding the world, the Swiss barely lost any business: the secret was not a debased currency, but extremely high capex, which allowed them to remain highly competitive. The only two other European countries to understand capex and innovation trump a debased currency any day were Sweden and Germany.

But then Germany joined the currency wars, followed by Sweden, and the BNS felt obliged to reply by thrashing the franc. This proved exceedingly difficult: for us living in the eurozone, the franc has long been a reserve currency. Every franc the BNS printed, we gladly bought. In a way, Europe was to Switzerland what China was to the US: a sinkhole gobbling freshly issued currency.

The €/ChF peg was a desperation move the likes of which I’ve rarely seen before: the BNS bought euro-denominated assets like there was no tomorrow by using freshly issued francs.

The difference is the BNS is not the People’s Bank of China or the Bank of Japan: it cannot just park these assets in its accounts and leave them there. You see: the BNS is also the Confederation’s hedge fund: it needs to turn profits on its investments which are then distributed among the Cantons to balance budgets. The Cantons take these profits for granted, and plan accordingly.

The peg was abandoned because those euro-denominated assets threatened to drag down the whole hedge fund. In the aftermath of the peg’s demise it was discovered it had played havoc with the BNS’s balance sheet: in first six months of 2015 it had lost $20 billion on its dollar-denominated investments alone. By focusing too much on euro-denominated assets to enforce the peg, it lost the “long-dollar, short-euro” trade which has been turning fantastic profits this year (some ETF’s gained a massive 40%).

Needless to say, the Cantons aren’t too pleased, especially now that they have some grandiose engineering projects going on.

Those massively negative interest rates were put in place immediately after the peg crumbled: as all central banks, the BNS cannot be a gracious loser. They swore time and time again they’ll attempt reinstating the peg but so far this has proven nigh on impossible, given how much the euro is slipping and how alarmed the Cantons are about their budgets.

This was reflected by elections early this year which saw a very clear victory for monetary conservative, anti-EU parties. These have traditionally been very strong in the Waldstatten (Forest Cantons) like Uri, Schwyz, Unterwalden etc but they are making inroads in the urban Cantons (Zurich, Basel Stadt, Luzern etc) as well.

The balance of power is changing.

This is the best explanation of the Swiss devaluation/NIRP I have read so far.

I understand that watch sales are down due to the slowdown in the global economy, but how are the Swiss going to compete with smart watches, the new in thing. Any thoughts?

Forget smart watches: the problem right now are luxury watches.

You see: China has been a great customer for Rolex, Piaget, Breitling etc. Sales were booming both in Asia and in Swiss shops, especially in Zurich, Basel and Bern, where Chinese tourists flocked to buy those watches which can be found there even when they are sold out everywhere else. Mind we are talking watches costing ChF 2000 at the bare minimum, with 5000 being the mean value. These ain’t the cheap Casio’s I’ve always worn.

Last year I noticed what can only be called as a dramatic drop in the number of Chinese tourists in Zurich, the city I am most familiar with. And it came literally out of the blue.

This year those Chinese tourists have completely disappeared. Even in August I didn’t see a single one on the Bahnhoffstrasse. Watch shops have the full lineup available for sale, an extremely rare occurence since the various special and limited editions sell out in days.

But things in China are going even worse, if possible: exports to Hong Kong, the entry point for all Swiss watches into China, have gone down a staggering 39% since 2014.

Sure, the franc has gained against the dollar (and by reflex against the yuan) but this is hardly what one believing in that incredible 6.9% GDP growth would expect. In short the Chinese miracle has proven as long-lasting and performing as one of their chainsaws.

Now, regarding smart watches.

Tag-Heuer has already launched one (Android-based) this year. It costs about ChF2000.

To be honest I believe The Swatch Group (the largest watchmaker worldwide) is presently sitting on the fence: they want to see if these things sell because they are hot or just because they have an apple on it. ;-)

The smart watches are desired by the millennials, my son among them, which is why I posed the question. They don’t have to have an apple on them but price is still a big issue in that age group.

I wore a Tag watch for over a decade and I have reservations about their new smart watch because it is expensive and not a watch you can keep indefinitely. It is a watch that will require replacement frequently. Also the issue with replacing batteries on Tag watches is a major pain in the butt. You can only get the batteries replaced by authorized dealers, not a convenient feature.

I think that the Swiss watch makers will be losing a generation of buyers because of technology and income issues.

Very good insight. I read somewhere that the BNS had a hard time finding quality Euro investments even before the ECB started printing euros.

As other commenters noted, there is no similar pressure on the Canadian dollar which is heading in the opposite direction. Yet, the governor of the bank still manages to find similarities with NIRP countries.

Something to note is that Canada alone builds more houses than the whole of Europe:

http://www.tradingeconomics.com/country-list/housing-starts

If the Swiss banks lived solely on lending to homebuilders in Switzerland, they would be the size of small branch offices of the American banks.

True that those houses last for generations, whereas mine will be a teardown before I am gone.