Financial Engineering bites back.

When IBM announced earnings last week, it talked about all the great things it was accomplishing to compensate for the fact that revenues had plunged 14% from a year ago to $19.28 billion, and that even “revenues from continuing operations,” after accounting for operations it had shed, dropped 1%. It was the 14th quarterly revenue decline in a row. Three-and-a-half years!

It’s not the only American tech company with declining revenues. There are a whole slew of them, mired in the great American revenue recession, including Microsoft, whose revenues plunged 12%. So they – big tech – are in this together.

But turns out, IBM’s revenues, as bad as they have been, might have been subject a little more financial engineering than normally allowed.

Today, IBM disclosed that the Securities and Exchange Commission is investigating how it has accounted for these lousy revenues. The one-sentence disclosure was tucked away in a footnote on page 45 of its SEC Form 10-Q, which it filed today:

In August 2015, IBM learned that the SEC is conducting an investigation relating to revenue recognition with respect to the accounting treatment of certain transactions in the U.S., U.K. and Ireland. The company is cooperating with the SEC in this matter.

“A company spokesperson wasn’t immediately available to elaborate on the probe,” according to the Wall Street Journal.

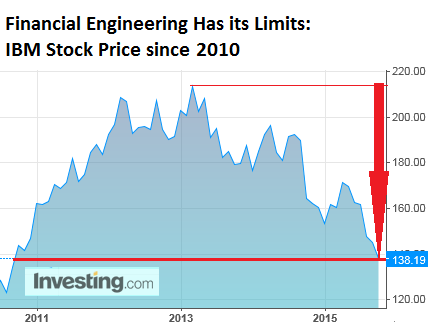

As I’m writing this, IBM is down 4% to $138, a new 52-week low:

Timing was impeccable: IBM had “learned” about this debacle in August. In order not to unduly disturb its already frazzled shareholders – August was a rough month for stocks – it mercifully kept quiet about it.

So today, mere hours before the disclosure, IBM announced a $4-billion stock buyback program, which brought the total current authorization to $6.4 billion, in order to put a floor under its shares in advance of the announcement.

Shareholders should be furious that IBM would blow another $4 billion on a scheme that over the past few years has done nothing but drive IBM deeper into the mire and enrich Wall Street entities that handle the process and extract their fees. Shares have now hit their worst level since late 2010 – despite the incessant share buybacks:

Instead of blowing tens of billions of dollars on stock buybacks to engineer its financial reports and pull, in cahoots with Wall Street analysts, a bag over investors’ heads with its per-share metrics, IBM should have invested those funds in actual engineering and in people, which might have helped it become great again. But this is unlikely to ever happen, given that Wall Street dominates the show.

“It’s been a rotten year for distressed and defaulted loan paper.” That’s how S&P Capital IQ LCD starts out its report on leveraged loans. “Rotten” may be a euphemism, as “fear has become a strong undercurrent.” Read… And Now Defaulted “Leveraged Loans” Go Kaboom

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

In a column a few years ago, Spengler at Asia Times calculated the ROI for tech companies outside the top 50 as -15%. Many tech companies are just money pits. Of course they make it up on volume…

And this is the entire problem with most of our economy:

“Instead of blowing tens of billions of dollars on stock buybacks to engineer its financial reports and pull, in cahoots with Wall Street analysts, a bag over investors’ heads with its per-share metrics, IBM should have invested those funds in actual engineering and in people, which might have helped it become great again. But this is unlikely to ever happen, given that Wall Street dominates the show.”

Technology, at least as far as IBM goes, is well into the commoditization phase and R&D can’t change that. Consider how much BNSF blows in R&D to make the company greater again. These days, IBM is different how?

They also probably have major problems compounding with foreign customers now that they are seen as being in bed with the NSA/etc. They screwed the pooch royally and won’t ever get those customer bases back. Maybe equity in their foreign competition might be an opportunity for the savvy investor.

What is happening is that the cash cow of recent decades (computing/info tech) is dead and something genuinely new has to come along and provide genuine economic gains, on a big scale and in terms of quality, efficiency, value, and so on. I thought nano-tech might revolutionize material science and shake up manufacturing, but now I am not so sure. BioTech is a big con for the most part, being as US insurance/health care is so screwed up, I don’t see how real ground up companies can compete on the basis of innovation in such a whore house.

So buckle up for hard times! That means get out of debt. Scale back regular expenses. Put some cash in a safe deposit box or under your mattress. Drive an old car. Keep a small tax footprint. Stay mobile!

Regards,

Cooter

Cooter’s got it right.

Here’s my status:

Out of stock market.

No debt.

Got 2 to 3 thousand cash around the house.

Driving a 5-year old Hyundai Elantra.

Combined 2016 (next year) income taxes (Fed and Cali) will be about $725.

Life is sweet.

IBM can’t innovate because it’s weighed down by its cash cows. As someone who works in technology, I am aware that IBM is putting its weight behind the hottest technology in software right now called Spark which came out of a UC Berkeley research. But so what really because IBM does not have its own cloud offering, so it has to constantly piggyback on other people’s work which then gets “lost” by marketing since the cash cow guys will eat up pretty much all the remaining budget.

The cloud is just a ham-fisted attempt to get customers to sign up for the service model (guaranteed revenue) rather than sell a product that might work for years and hinder future revenue.

One of my favorite examples is MS Word. The version I owned in 1998 works just as well (for what I do) as the version I use today which is 2013. So, why, in between, did I need to buy several new versions? Why can’t I just use the old one that I OWN?

Further, if one assumes malfeasance (who doesn’t these days) then the vendor of the cloud services is anonymously mining your data for their gain. Sure, it might be anonymous, but if you host most of the accounting services for small restaurants in the Seattle area, do you think you could find someone that might be interested in various profit margins, inventory ratios, and so on? You know, “anonymous” data because you don’t say who it is? What about those important contract documents with a potential major new client? Top secret, right?

The cloud is an insider traders wet dream. We actively refuse any cloud services at all at my employer (we all think the same thing).

Unless you are telling me what “spark” is, I am not impressed. I did a quick google and as best I can tell it is a webby, analytical software product that is clusterable. A MS SQL Server license for SQL 2014 which includes SAS Tabular retails for 10k or there about (at least for my company).

So, it is fine they are bringing on new products and all that, but this is hardly going to save their bacon.

IBM used to be the monopoly, just like AT&T, just like MS. But, funny how that doesn’t seem to go in a straight line.

Regards,

Cooter

Wolf, where can I find the write-up on ‘the great revenue recession’? It seems that this is hardly (or at least not necessarily) limited to the lumbering giants of the technology space. Funny, by the way, since I thought equities were generally considered to be ‘claims on future revenue streams.’ They also apparently work (for a while) as free money measurement and owner-initiated liquidation detection devices.

Here’s my series on the “revenue recession.” I first tagged articles that way on September 7. There might have been earlier articles on it, but they’re now harder to find. So make sure you look at the Sep 7 article first – it defines the issue:

https://wolfstreet.com/tag/revenue-recession/

IBM is still in business? I thought they died in the 90s. Maybe they’re just getting the Memo now?

Seriously… the ‘cloud’ is part of the race to the bottom in prices in the IT market, along with having your data held hostage and a total lack of privacy…with that said, nearly all the federal government agencies are moving to it. Lowest price, don’t you know?

Well Cooter I guess ‘planned obsolescence ‘ is alive and well. Can you imagine the frustration of future car aficionados trying to restore an old car and have to scrap the whole plan because the software that runs the “black box” can’t be purchased at any cost?