Expect the unexpected.

By Larry Kummer, editor of the Fabius Maximus website:

Mainstream economists assure us that a recession remains unlikely in the foreseeable future. They have their reasons.

- They forecast steady slow growth. The Philly Fed’s Survey of Professional Forecasters sees 2.4 – 2.8% real GDP rising through 2018.

- Most indexes of leading indicators remain strong. The ECRI’s Weekly Leading Indicator hit bottom at 105.4 in March 2009; it’s remained above 130 since March 2013; it’s now 132. An exception is the OECD Composite Leading Indicator, which has been slowing since last Sept (“growth losing momentum”).

- Most of the standard warning metrics remain low. The recession probability indicator of Marcelle Chauvet and Jeremy Piper is at 0.3; it was 3.9 in November 2007 (the start of the great recession). The Econbrowser indicator of James Hamelton didn’t work in 2007 and has given odd readings since then.

These tools worked moderately well during the post-WWII era, when the Fed caused most recessions by raising rates to prevent inflation (they took “away the punch bowl just as the party gets going”). That era has ended. In this century unexpected economic shocks cause recessions, their severity depending on the size of the shock and the economy’s strength.

Bubbleville in Northern California

If it were a nation, California’s 2014 GDP would have been the 7th largest in the world (bigger than Russia or Brazil). It’s one-eighth of US GDP. A quarter of that comes from the San Francisco Bay Area, home to one of America’s most vibrant, cyclical, and cynical industries: manufacturing stock certificates (now mostly virtual) for sale to the gullible.

It’s a diversified industry — venture capital, social media, biotechnology, etc. — whose specialized requirements are uniquely met by America’s new city of dreams.

Consider Twitter’s Q2 results: $502 million revenue for a GAAP loss of $137 million (including $175 million of stock-based compensation). Revenue up 61% year-over-year; loss down 6% year-over-year. Party on while the music lasts! For details why it might not last long see The advertising glut dooms the social media industry.

For hard core speculation look at the biotech stocks. Don’t ask if there’s a biotech bubble. Ask why we have another bubble.

Venture capital is the engine of the bubble. VC returns during the past several decades have been mediocre at best. Even during the first tech bubble (1987 – 2000) they were roughly similar to those of public stocks. Bubbles eventually burst when investors demand profits – or radical corporate surgery on their properties. The pop will hit the Bay Area like an earthquake. But we’re better prepared for a quake, as I explain in Who will get hurt from the next stock market crash?

The resulting drag on the economy will add to the already severe downturn in the coal and oil-and-gas industries (~2% of GDP). The industries affected are geographically concentrated, but relatively small — and so are probably insufficient by themselves to start a recession (unlike the collapse in the broader tech and communications industries in 2000). The most serious and lasting damage to the nation might be the blow to our confidence from the third such crash in one generation.

Automobiles

Light vehicle sales have been one of the US economy’s largest engines of growth, now risen to 18 million/year from their trough of ten million during the recession. It has brought them to a level from which they’ve often fallen steeply during recessions.

Auto sales have reached impressive levels, but their foundation is less so. Prices have risen to the point of unaffordability without imprudent borrowing: average loan length is an incredible 65 months, with the average loan a nosebleed $27,000 (US median household income: $53,000). Of the trade-ins, 27% had negative equity, with an average deficit of $4,257. Subprime borrowers account for about 20% of auto loans made. This cycle will not end well [Auto loans: once a boon for America, now a bane].

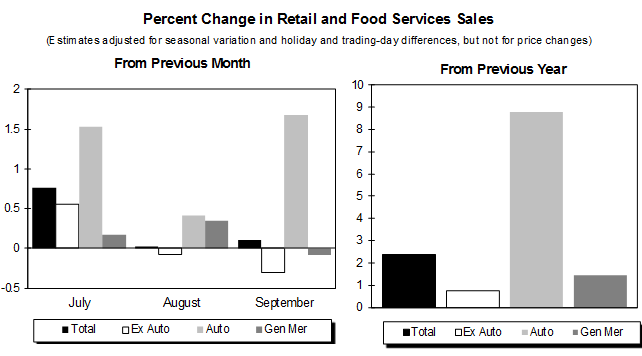

Even a small shock to the economy might have a large impact on the auto industry, which is about 2% of GDP (manufacturing and sales). Auto sales are the hot dot in retail sales. According to the Census Bureau, retail sales in September rose 2.5% year-over-year (not seasonally adjusted), but excluding autos and parts, they rose only 0.9%. And in August and September month-over-month (seasonally adjusted), retail sales ex-autos actually dropped:

A fall in auto sales, given the size of the industry, seems likely to magnify an economic shock, but unlikely to cause one by itself.

Housing

Construction of housing provides one of the most powerful drivers of the US economy. Even now, as the Boomers begin their long downsizing — from home to retirement home to nursing home — their acceleration after the crash from 500,000 to 1.2 million units per year has provided much of the economy’s growth. Like auto sales, but much more so, it depends on the flow of credit.

Housing will crash before and during the next recession, as it almost always has — but with one-third or one-half of the impact on the economy as in past recessions, given the current low rate of activity (3.3% of GDP in 2014). That’s significant, but it seems unlikely to cause a recession by itself.

The Case-Shiller Indexes show that home prices have climbed back to the bubble levels of February 2005 (about 13% below their April 2006 peak). But asset price changes by themselves have little economic impact. The mass foreclosures of the great recession have left most surviving homeowners in good shape, with large-scale problems remaining in areas with local problems.

Inventories

Recessions are usually caused by a downturn of the major cyclical industries, often after a buildup of inventories. And inventories have built up since late last year, as aggressive ordering coincided with lackluster sales. So in August, wholesales declined again, wholesale inventories rose again, and the crucial inventory-to-sales ratio reached 1.31, a level it hit in October 2008, just after the Lehman moment.

A similar scenario is playing out with manufacturers’ and trade (retail) inventories. Their combined inventory-to-sales ratio in August reached 1.37, a level also associated with the economic fiasco following the Lehman moment.

Once businesses start trying to get their inventories under control, they will slash orders. These orders are sales to their suppliers. And so it cascades through the economy, which can trigger all kinds of unpleasantries, including a recession [Last Time that Ratio Soared like this, Stocks Crashed].

Exports

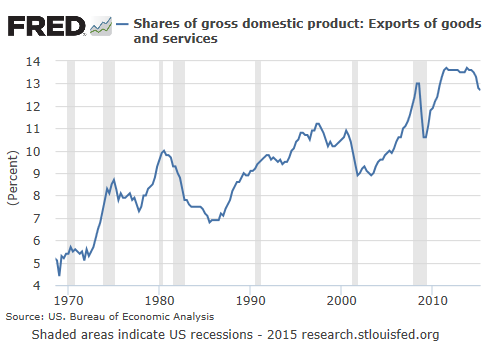

Despite claims that the US don’t make nothing, exports’ share of GDP has tripled — to over 13% of GDP. Exports are diversified both geographically and across industries. That means that their typical 10% drop during recessions can knock a point or so off nominal GDP. That would hurt, with nominal GDP running at 2.5 – 3.0% since Q2 2014.

Here we have another sufficiently large and volatile factor that might knock the US into a recession on its own. Such a drop might already have begun as our exports drop due to slowing growth in China, Brazil, and the world’s commodity exporters. And Citi’s economists worry this could cause a US recession in 2016.

It has been six years since the end of the previous recession, and there are obvious weaknesses in the US economy that combined in some form or one of them by itself – such as exports – could cause the next recession.

The bad news: the US economy has grown only slowly since the crash, making it vulnerable to a shock. The good news: this slow growth appears to have created few of the imbalances that create long deep downturns. But most of us thought this was true in 2007.

We are in a new age where many of the standard economic patterns and relationships of the post-WWII era no longer apply. Expect the unexpected. By Larry Kummer, editor of Fabius Maximus

The government has some strange and awesome powers to throw around when the next one hits. Read… And What’s Going to Happen at the Next Recession?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The article says inventories in the US are running so low that a drawdown in inventories wont cause recession. However, the inventory to sales ratio is huge and growing, running at 1.37x sales. The energy and mining and auto sector inventories are astronomical. uS auto inventories are currently far higher than theyve ever been over the past 30 years.

Yeah, I saw that too. Contradicts my own article on it. It might need a little edit.

Lamont,

August’s total inventory/sales ratio was 1.37. Compare that to 1.32 in late 2006, which had no ill effects. It is not “huge”.

Also, the level has been flat for the past 8 months. Not what we usually see before a recession.

The auto inventory/sales ratio is 2.08 vs. 2.07 a year ago. Obviously the auto manufacturers consider this the appropriate level.

Energy and mining are industries in a downturn. But they are very small industries.

Here, the whole is less than the sum of all the losses …

(urp!)

He should include military costs which are dead losses … and they aggregate, too.

He should include derivatives net exposure which could be multiples of real estate or energy losses. Watch the banks, they are teetering (particularly in China and eurozone).

Steve,

The post considers causes of a recession. These are changes in demand for goods and services. The “utility” of the demand makes no difference. Lipstick or guns, it is all just demand.

We’re just discussing economics.

Exactly, some goods and services are more productive than others.

I can kill someone with a $5 tire iron, I don’t need a $200 million dollar flying white elephant.

The white elephant is a dead loss that offers no return at all to the user, it represents funds that could be either spent on something offering a return (such as infrastructure improvement) or not spent at all (saved).

It’s net, not gross that matters.

Why do we need a new recession? Why can’t we just keep using the same one we’ve had since 2008?

You can’t see a problem if your income depends on you not seeing the problem.

Quite a few people have made a lot of money in this “recession”. Not me though, too stupid to discount reality.

https://research.stlouisfed.org/fred2/graph/?graph_id=261712&category_id=

Get ready for a resumption of QEternity to bail the banks and to fund the increasing deficit to prevent nominal GDP from contracting.

And this time we will get to enjoy NIRP, bail-ins, and probably the Fed printing to buy bank, insurer, and builder stocks, equity index futures, subprime auto loans, energy debt, munis, junk bonds, equity ETFs, and probably Uncle Jed’s 1930s kitchen sink in the corner of the barn.

We’re all militarist-imperialist, rentier-socialist corporate-statists (well, 0.001-1% of us are) caught in a surreal end-game scenario for the fiat digital debt-money petrodollar reserve currency regime.

The Fedster and banksters’ credibility and legitimacy will be tried in the months and years ahead like never before, no doubt prompting them to resort to all manner of “extraordinary measures” and “whatever it takes” to defend their legitimacy, authority, status, and power at whatever costs to the rest of us.

And so it goes . . .

The next recession is here already. 70% of Americans are living from paycheck to paycheck, and no longer have enough credit to buy at Walmart. 1948 was the first year that workforce participation records were kept. Since that time, there has never been a smaller percentage of working age males in the workforce than there are today. Those working age males can’t afford to buy at Walmart. One out of four US children are on food stamps, and their parents do buy food at Walmart, but they aren’t buying all that much. When folks can’t afford to shop at Walmart, the country is in recession, regardless of where the government subsidized GDP number comes in.

Oct. 14, 2015 8:33 p.m. ET

“Wal-Mart Stores Inc. surprised investors Wednesday by predicting profits would drop as much as 12% next year”

True that the recovery from the last recession is milder than prior recoveries and therefore the fall will be less severe economically. Unfortunately, the stock and bond markets have exploded higher and are at such extreme valuations today that the next recession will cause chaos with savings and net worth for every American with a retirement or investment account. The Fed didn’t have a $4 trillion balance sheet and ZIRP the last recession either. The Fed is out of bullets and the markets are on their own for the next recession. Good luck with that!

I would frame that a bit differently. The economy has not really recovered from the last financial shock and is about to get hit with another one.

The popular analogy is that we’ve passed through the eye of the hurricane and we’re about get hit again by the back wall.

I would extend this analogy by adding that our economy is New Orleans.

You are correct Sir. We are “The Big Easy” in the analogy. And those levies look weak. Les se’ Bon Ton’ Roulet!!!

“The most serious and lasting damage to the nation might be the blow to our confidence from the third such crash in one generation.”

I would ask who it is that has confidence? If you are not a member in good standing of the monied investor class, you think the game is rigged. If you are an insider, you know it’s rigged.

The Romans had a saying: Gutta cavat lapidem, literally meaning a drop of water makes a hole in the stone. In a broader context it indicates that when small, seeming insignificant factors build up over a long time span, the consequences can be unimaginable and absolutely catastrophic.

I often hear people arguing over what will cause the next recession: some say a housing burst, others a stock market crash, others still the not-so-awesome-now situation in China. Some of them make very valid points, others less so.

But very few stop to connect all these dots together. Apart from stock markets (due to their psychological value, as they are always on front pages), none of these sectors alone has the potential to cause a full blown recession.

See the commodity massacre. One may say Brazil is getting slaughtered precisely because of it, but the reality is the commodity price slump and the storm clouds building over China are only part of the story. One may call them the straw which broke the camel’s back. Brazil was already set for a very hard landing in 2011-2012 if not earlier: high commodity prices and strong demand from China just delayed the inevitable.

I often try to connect at least the dots I am familiar with and the more complete the picture looks, the less I want to see of it. Taken overall we have a situation which to call “scary” is a mild, politically correct statement.

The picture increasingly looks like an elephant performing a precarious balancing act on top of a tall pyramid whose builders didn’t know how to make particularly good mortar. As long as that mortar holds and the elephant and its handler remain alert, all is more or less fine.

I really hope this is yet another case when luck lends a hand.

The “industry” most likely to usher in the next official recession is the financial industry, and not just the Bay area VC component. As the central banks of the world find it increasingly difficult to continually elevate stock and bond prices, banks and brokers will begin pairing back employment in an attempt to ride out the coming financial storm. Deutsche Bank, UBS, and Credit Suisse are battening down the hatches right now.

A QE of greed is gonna cause it. All the people I know want to have gains of 20%, recurrent and as quickly as possible.