“Let me assure you, if the revenue environment weakens or interest-rate structures don’t move up and the economy slows down, we’ll have to take out more costs,” Bank of America CEO Brian Moynihan said on Thursday at the Barclays Global Financial Services Conference. And that would mean more job cuts.

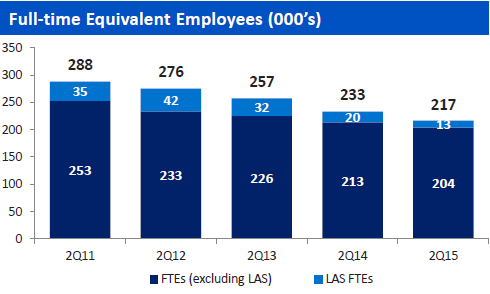

BofA is famous for whittling down its headcount in recent years. In Moynihan’s 25-slide presentation, there was this chart that shows just how skillfully he has trimmed down his workforce, chopping it by 25% overall since the second quarter of 2011:

So if, as he said, “interest-rate structures don’t move up,” there would be more of the same. These interest-rate structures are the result of the Fed’s zero-interest-rate policy. The purpose of this policy suddenly isn’t the wealth effect any longer – Bernanke’s stated purpose – but ironically, as Chair Yellen claimed today somewhat defensively, to “put people back to work.”

Not get them axed from banking jobs.

Banks try to make money in a myriad newfangled ways. But the classic way is on the spread between the interest they pay on deposits and the interest they charge on loans. A wide spread fattens their profits. But these spreads have become paper-thin.

Banks can get all the money they need from the Fed at near-zero cost. They don’t need depositors, and there is no competition for depositors. So, in one of the biggest scams in history, depositors get next to nothing from banks around the country. And the banks’ cost of money is near zero.

But there is desperate competition for making loans in an environment when bankers and their customers, especially big corporate customers, wade up to their nostrils in Fed-engineered liquidity. This mad frenzy pushes down lending rates (along with bond yields). And the banks’ spreads and profit margins have been squeezed.

The entire world has its eyes riveted on the Fed. There are days, like today, when nothing seems to matter other than what the Fed is going to do.

But the Fed once again couldn’t figure out what to do. It certainly didn’t want to ruffle the markets by doing anything in particular, such as raising rates from nearly nothing to almost nothing because it might somehow derail this economy of ours, or worse, that of the entire world.

So it did nothing. Now, no one can figure out under what conditions the emergency that led to this extreme monetary policy in 2008 might be deemed over, or whether it will be reclassified as a permanent condition, rather than an emergency, and remain in place until something Really Big breaks that will make the prior emergency seem banal.

Uncertainty – and frustrated bankers – is the result.

Instead of soaring, stocks languished. But the banking sector got hit hard. The KBW Bank Index dropped 3.0% from today’s high just before the announcement. Shares of Moynihan’s BofA dropped 3.9% from today’s high just before the announcement; Zions 4.2% from; Fifth Third Bancorp 3.8%; Citizens Financial 3.7%. Banks got crushed by the Fed’s inaction.

Now bankers are losing patience with the Fed. And they were firing back today while at the Barclays Conference.

US Bancorp CEO Richard Davis already lost patience; his bank would cut expenses – at a bank, that means jobs. Focusing on costs would allow him to “care less” about interest rates rise and whether they’d finally rise or not, he said according to the Wall Street Journal. And the shares of his bank dropped 2.4% following the Fed’s announcement.

“It would be a good thing to raise rates,” explained JP Morgan CEO James Dimon, as JPM dropped 3% from the hopeful moments just before the announcement. “It would be a good sign,” he said but didn’t expect his wishes to come true.

“I dream about it every night,” is what BB&T Corp. CEO Kelly King said about rate increases. His bank’s shares dropped 3.1% from the moments when hope still reigned.

A wider interest rate spread would come in handy because not all is well in banking land. Yesterday, Citigroup CFO John Gerspach, warned that trading revenue could fall 5% in the current quarter.

Moynihan’s slide deck shows that investment banking fees at BofA in Q2 2015 were lower than in both Q2 2014 and 2013. Sales and trading revenues were also lower in Q2 this year than in both prior years. Moynihan said that revenue from trading bonds, currencies, and commodities would be down this quarter as well.

Meanwhile, according to the presentation, BofA’s global average loan losses are rising. That’s not a good combination.

The financial sector plays an outsized role in the US economy, and if it sneezes, the Fed gets even colder feet. But the medication for banks – higher rates – may not be available, or not in sufficient measure, in this perverted economy that the Fed has so skillfully engineered over the past seven years.

But Wall Street engineering does perform miracles, even though investors in such miracles are now getting their hands burned off. Read… A Spinoff Goes to Heck, after Just 10 Months

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Banks in trouble??? My heart bleeds….

It should. Your wallet will be bleeding next and tens of thousands of bank employees will be losing their jobs.

You are completely wrong. When a bank like Chase tells me that I can no longer keep cash in my safety deposit box, it sends a clear signal they are too big NOT to fail.

And then Chase bank starts to limit overseas transactions that puts many small companies in a quandary because now they are made equivalent to drug dealer and launderers.

Also, if I thought it meant the loss of thousands of bank teller jobs, I would feel differently. But we all know they went the way of the elevator operator.

The rest are jobs that never should have been filled in the first place. Since all banks have an interest in the Federal Reserve, they HAVE ALL made their bed and now must lie in it.

Kinda funny how Wall Street thinks layoffs are good for a company, unless it’s bankers getting laid off.

Then it’s end of the world time.

Big Banks Cutting Tens Of Thousands Of Jobs; Huge Implications – By John Rubino

Money center banks — which over the past few decades have grown into the biggest financial entities the world has ever seen — appear to have hit a wall, and are now shedding tens of thousands of workers. Three recent examples:

Barclays plans to cut more than 30,000 jobs

Deutsche Bank to cut workforce by a quarter

UniCredit plans to cut around 10,000 jobs

http://dollarcollapse.com/banking/big-banks-cutting-tens-of-thousands-of-workers-huge-implications/

The Fed has chickened out. In Uk, base rate at 0.5% since March 2009 has fuelled a lending/borrowing boom in property investment and the thin margins have led to banks closing hundreds of branches regardless of the impact on local communities.

Time to see if they’ll follow up on their threats then. ;-)

In Europe Deutsche Bank and Unicredit recently announced layoffs that, combined, will lead to the loss of 33000 jobs. Lending margins are getting so thin, especially in the all-important real estate segment, banks are forced to do somersaults to turn a profit, including slashing their workforce and holding mountains of highly dubious derivatives.

Consumer credit, including auto loans, has so far managed to somewhat slow the bleeding but plainly put it’s not enough.

This is all due to a series of inderdependent factors of which banks are both culprits and victims… the true human tragedy.

Buy the banking Dip!! Ha ha.

I moved to Credit Union (community based, better insured) 35 years ago. People robbed banks and villified banksters during the Great Depression for a very good reason. Today, the same conditions apply. Investment Banks need to be charged under RICO. TBTF banks need to be broken up or nationalized. This should of happened in 2008. Meanwhile, folks can take their business to a credit union.

regards

I think Credit Unions are a great alternative. I couldn’t find one near me that also had safety deposit boxes so I opted for a small local bank.

What I would love to see are banking alternatives. One that I know will never see the light of day are “chip cards” that are able to store money. Limit them to a certain amount, say $100 or whatever.

And since banks aren’t interested in depositors, why not?

In my opinion, if the federal government had never set up any FDIC/FSLIC and just allowed the Free Market to take its course, there would be many alternatives to storing money right now.

You can buy a MC or Visa gift card/debit card in the supermarket and keep adding money to it. It isn’t free but it is a “non bank” alternative.

No FDIC insurance on accounts exists in credit unions at all and most have very limited operations that fall far short of full banking services provided by major banks.

Adam, you’re a fear-mongering bank troll! Or worse, a Fed troll? Everyone knows that the Federal Government insures participating credit unions just like it does banks, same amounts. Only the acronym of the insuring agency is different. Instead of the FDIC, it’s the National Credit Union Administration (NCUA). For the customers, it makes no difference what the agency is called.

I never understand this economics stuff. So banks are asking the Fed to raise the cost of raw materials for them because then “interest rates have gone up”, and they’ll make money. ?. So, what if ZIRP is real? What if the marginal return on invested money truly is zilch? If “the financial sector plays an outsized role in the US economy”, maybe this means that no enterprise anywhere is actually creating wealth. Maybe the whole economy is running transactions in a circle, hoping that someday The Market will run across some naif who has thrown some wealth into the pot. Not me, of course; some naif.

“Everybody wants to go to heaven, nobody wants to die”, as Ellen McElwain once sang.

There will come a time when no matter how low the Feds set its lending rate, the market will demand a higher interest rate in relation to US Treasuries.

Whether rates go up, down, or stay the same, banks will continue to dump employees. Ultimately, online banking and ATMs will take the place of your local branch bank. Additionally, banks don’t want our money. One of my banks sent me a letter stating that it will start charging me, if I keep more than $5 million in my account. I have no idea why they sent me that letter, because there is a zero risk of ever seeing that kind of money in my bank account.

Still, compliance with Basil III and Dodd-Frank is expensive enough to gnaw away at banking’s retail profit machine. We’ve also seen that banks have been selling their mortgage servicing businesses to hedge funds and other servicing entities. So all these present and future layoffs will lower bank operating costs, decrease liabilities and increase profits

What the big banks should be looking for is a greater spread between the short term money they borrow and the longer term Treasuries they buy with that borrowed money. Therefore, it’s hard to see how a quarter point, short term interest rate hike will help them make more money in their Treasury Note carry trade, unless the longer term Treasuries show an even greater rate increase, giving the banks that greater spread. In that case, if the Fed lowers short term rates, shortly after hiking them, the big banks are left with bigger spreads, and who knows how highly those spreads are leveraged? That’s a scenario that could seriously enhance bank profits.

My take on banks is that, like other conglomerates, they aren’t happy with small, incremental profits or even regular profits. They are all chasing some huge gain. Why all the headlines about the Fed NOT knowing what to do? Of course they know…..as Jim Willie, the GoldenJackass, says they can’t raise rates and they know it. The system can’t afford any raise. It’s all theatre. We need to move onto another reality here and begin to re-invent our concepts of wealth.

LOL. Come on guys, look at a chart of the banking index from March 2009 until now. That is a huge gain, and ZIRP was in effect the entire time. If the Fed raised rates right now, the banks wouldn’t just be laying people off, they would be quickly going bankrupt. What the banks need, and will likely soon be getting, is more quantitative easing. Please don’t buy what these banksters are saying at these conferences. They say these things for public consumption to make it appear as if they aren’t just empty shells and zombie corporations. If raising rates was good for the banks, then the Fed would have done so.

I agree! They are not the VICTIM. They are the CULPRIT.

WE…. are the victims.

please, Brer Fox, please don’t throw me into the briar patch.

Over the last few decades the definition of banks has changed, and in my opinion, today’s banks should go back to the business model of the past.

For example, way back in the early ’60s, my folks took out a mortgage from Twin Cities Federal Savings and Loan to buy their first home. TCF required a down payment, good credit (you know, an actual job) and they wrote a loan with the house as collateral. TCF held the note in-house until my folks paid off the mortgage, and then transferred the deed of ownership to my parents.

There was no bundling of sub-prime toxic loans that got packaged and sold off like Wall Street did after the GLB Act was signed by Clinton. Banks’ balance sheets were actually legitimate as a mortgage was kept as an individual contract, and an accountant could asses the value of the home that was under a mortgage. Today’s TBTF banks are really Ponzi-schemes, and the banksters have honed their devious craft of manipulating ledgers to an art form.

Their is no way to turn back the clock to those simpler times … unfortunately.

In the early 90’s before Clinton, Wall St. was already buying mortgages to slice and dice. At that time, the firm I worked for was very careful to buy mortgages from only the best zip codes. They mastered the demographics of home ownership. Really good zip codes pay cash so supply is low and the mortgages that do exist are non conforming (over the limit). The really good zip codes for derivatives were working class neighborhoods where people had jobs and had been paying for a couple of years. Employment was the base that carried the economy. No jobs, no mortgages, no bonus for bankers.

The Fed is doing exactly what Japan did 25 years ago in 1990 and onward. The Japanese discovered what 0.25% BOJ lending could do, and they in 5 years held 9 positions of the Top 10 ‘banks by assets’ in the world ! , and subsequently started the global-wide Yen carry trade. The Fed wants to emulate and supplant the Yen in this regard, and initiate the global-wide Dollar Carry Trade as an emergency damage control initiative to the immanent demise and collapse of the global petro-dollar !!! And The Fed can only do this by maintaining a ZIRP for 20 years ! So all this ‘noise’ about ‘raising interest rates’ is total bullshit !!! IMHO The Fed won’t raise rates for 10 years !!! and you can quote me on that !!

As a side note, watch Max Keiser’s “Keiser Report” on RT, episode #811 part 2, for some good insight on how MainStreet thinks in regards to cash, gold, and Treasuries.

Nope. The Federal Reserve is far more constrained by law then the BOJ (Bank of Japan) and is not doing the same thing(s) at all as the BOJ has done. The BOJ has in fact MONETIZED Japanese government debt and has purchased large amounts of stock and the Federal Reserve is prohibited from purchasing even a single share of stock (equities) by the Federal Reserve Act.

The Fed buys indirectly thru their most favored hedge fund.

I’ve been dealing with CIBC here for years with my store business and they are just full of BS. First off they nickel and dime you to death with fees. Fee for depositing cash, fee for depositing cheques, fee for depositing COINS?!!? Whaaaa.. ok then no more coins for you. They eliminate the small business wicket/teller.. whaaa?? why? Now I have to stand in line with the riff raff who think they are Donald Trump with a million things to do at the bank. Not to mention they are constantly moving the sh*t ( employees ) around from one bank to another bank. They have about 100 tellers and only 2 wickets open. It’s just a joke. They want to fire people.. go right ahead, no skin off of my balls.

Personally I’m thinking of changing to Alterna which used to be CS COOP here, much better service with less BS. But at the end of the day all banks are the same you just have to pick the one who fleeces you the least.

“But the classic way[banks make money] is on the spread between the interest they pay on deposits and the interest they charge on loans. A wide spread fattens their profits. But these spreads have become paper-thin.”

Baloney. They are geting away with usury pure and simple thanks to a toothless Congress and Judiciary. Paying $0.01% APR to savers (when they can’t get away with actually charging THEM interest in their savings (bail-ins), while charging cardholders 12-20+% APR (not counting myriad fees and juicy late charges) is the reality. And thre banks have been reporting near-record profits in case you had not noticed, all the while working as hard as they can to merge so as to be able to gouge customers with even more impunity.

Baloney indeed. Mine eyebrow doth raiseth at whoppers such as that one.

Did you check how little interest even junk-rated corporations are paying on bank loans? Every bank wants to lend them, and outside the energy sector, rates are ludicrously low.

Credit cards are a nice profit center for banks, but it’s TINY compared to corporate lending and mortgages. Even lowly auto loans (over $1 trillion) are bigger than credit card balances. And auto loans are as low as 2.5%.

A lot of banking profits came from other activities that are now declining, such as trading, as the article said. Hence the emphasis on making money the classic way on the spread.

So don’t confuse a tiny corner of consumer credit with overall banking.

Banks not making money in the USA?

Why don’t they set up an operation in Australia. They would love it here.

Variable mortgage rates near 5%, fees of 3% when you use your credit card overseas, charges for using a debit card to access your cash, cheque deposit fees, monthly accounts fees, etc.

The big four banks here have had near record profits year after year. Bank share prices have been at record levels over the recent past.

Oz the ‘lucky’ country – for some.

What makes you think they haven’t? Check who are the real owners of the 4 big “Ozzie” banks.

http://blog.creditcardcompare.com.au/big-four-ownership.php

Sorry, but you make the mistake of equating the shares held by ‘nominee’ holders as one that actually owns the shares: they don’t.

They are custodians of the shares with the real owners hidden. However, if one of those ‘hidden’ owners goes over 5% then they have to be identified.

As the report in your link stated stated it is unlikely that there are any substantial holders and none are shown or identified.

With huge companies like banks with large caps there is even less of a chance that one entity could ‘control’ or own one of these enterprises even by speading its money around. Why even bother: it would defeat the goal of control.

However, with smaller companies the nominee shareholding system is one way that share prices are controlled and manipulated and insider trading takes place.

it is a ‘dirty little secret’ that people don’t discuss ot talk about and one that never gets taken on by the regulators.

I guess it all depends on whose ox is getting gored. Personally I won’t get interested until I see bureaucrats getting pink slips in large numbers. I have cut back on using the bank as much as possible being on the road. I also have an account at a credit union, but they’re far worse than the bank at nickel and diming me.

Government employees have never felt the recession. They are overpaid and you get to work past 65 to pay their fancy pensions.

The cap rate is maxed out. Raising interest rates will cause valuations to be lowered. This has forced the Fed’s hand, it seems to me. They don’t want to be responsible for the crash. By waiting, the inevitable effects of having pushed easy credit as far as possible will be debt deflation and a crash. Since households were previously more or less all loaned up, the only real targets for large scale credit creation were corporate. (And the sub-prime auto market.) (Mortgage purchase apps have been stagnant & going nowhere fast for years.) (Capex has been nothing to write home about either, because with debt deflation, there will be no increase in final demand.) The largest junk bond bubble in history has been the result, and money wasted on stock buy backs. When it stops, then the crash. Who will the banks lend to in a deflationary environment? Defaults, bankruptcies and foreclosures on the way.

shut the government down and the BANKS….and especially …END THE FED….imho