The Bank of Canada has been fretting about the ballooning debt of Canadian households. Last year, it repeatedly called it a risk to “financial stability,” perhaps in preparation for raising its benchmark interest rate. Then Canada’s economy tanked.

In July, when the freaked-out Bank of Canada cut its benchmark rate for the second time this year, it admitted that the rate cut comes at the price of “financial stability risks” which “remain elevated.” Governor Stephen Poloz added: “Of particular note are the vulnerabilities associated with household debt and rising housing prices.”

These rate cuts didn’t do much to support Canada’s resource economy that has been spiraling down in the wake of the commodities rout. But they made up for it by inflating the housing bubble even further.

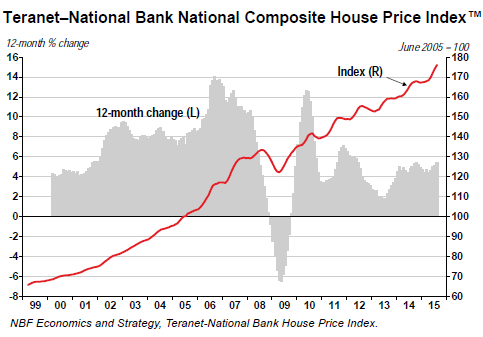

The Teranet–National Bank house price index, released September 14, hit new records every month this year. In August, it was up 5.4% year-over-year. Note how the index has soared since the peak of the prior housing bubble that ended with the Financial Crisis:

The index masks what Marc Pinsonneault, senior economist at NBF’s Economics and Strategy, calls the “dichotomy” of Canada’s housing market. In some cities, price increases are cooling, year over year: Victoria +3.2%, Edmonton +0.8%, Calgary +0.7%. In other cities, prices are actually falling year-over-year: Winnipeg -0.4%, Ottawa-Gatineau -0.4%, Montreal -0,5%, Quebec City -0.7%, and Halifax -1.4%.

But they’re sizzling in Vancouver +9.7%, Hamilton +8.8%, and Toronto +8.7%. And prices for non-condo homes in Vancouver and Toronto – the two cities account for 54.1% of the index – jumped over 10%!

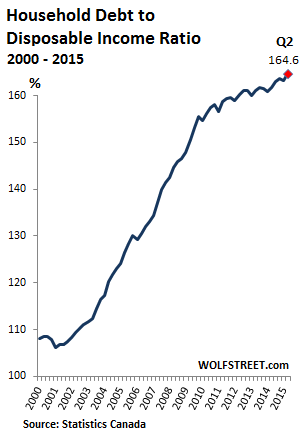

On cue, total consumer debt rose 4.9% year-over-year in July to C$1.86 trillion. A trend that has been picking up speed recently: on a monthly basis, consumer debt jumped in July at an annualized rate of 5.4%. Mortgage debt – over two-thirds of total consumer debt – soared at an annualized rate of 6.9%.

Yet disposable incomes only inched up 0.8% in the second quarter, Statistics Canada reported on September 11. So the household-debt-to-disposable-income ratio, a measure of household leverage, hit a record 164.6%, the largest jump in the ratio since 2011:

“Fortunately, there’s little need to fret about households’ ability to carry all that debt,” BMO Capital Markets senior economist Benjamin Reitzes wrote in a note. Interest rates are super-low, and thus the burden of carrying all this debt still manageable. But even he conceded that “further increases would start to ramp up our level of concern.”

The ratio is an average. There are many Canadian households with little or no debt. But then there are many other households whose incomes have not fared well, and who have piled on debt to buy a modest home in one of the most overpriced housing markets in the world.

And they’re not just borrowing to buy homes. In its consumer credit report for the second quarter, released September 15, Equifax Canada reported that auto-loan balances increased by 3.9% year-over-year. And installment-loan balances (credit cards, etc.) jumped 8.0%.

Consumers are beginning to stretch.

But no problem. Despite increased debt loads, the 90-day-plus delinquency rate is down 1.6% and bankruptcies are down 9.4%, Equifax reported, as they should be, given the increasingly easy and cheap credit sloshing through the land: borrowers aren’t going to fall behind if they keep getting new money. It’s when they can’t get anymore new money….

But suddenly there are problems: rising delinquencies in “some of the sub-segments” of the population, the report warned.

We’re starting to see the impact of low oil prices in the West as these prices are forcing a new reality on Alberta and Saskatchewan in particular. In these two provinces the debt levels are stable, but the delinquency rate has started to increase.

On a demographic basis, the 90+ day delinquency rate for Canadians aged 65+ rose for the first time since 2010. The rate increased by 2.4% this quarter versus a decrease of 5.1% in the previous quarter.

So the oil patch is experiencing rising delinquencies. And across Canada, for the first time since the Financial Crisis: seniors!

Equifax promised to “monitor this trend closely in the coming quarters.”

This ballooning household debt “puts Canadian consumers in a precarious situation,” Scott Hannah, CEO of the non-profit Credit Counselling Society, told the Toronto Star. “If they’re struggling to manage their increasing debt obligations now, a sudden change in external factors — like a rise in interest rates or the loss of a job — will leave many Canadians in greater financial difficulty.”

It’s for a reason that the Bank of Canada called this enormous amount of household debt a “financial stability risk.” The fact that delinquencies have started to rise in the first subsectors – despite historically low interest rates and super-easy money – is the audible ticking of a time bomb under one of the most overpriced housing markets in the world.

Spiking numbers of “half-empty” office buildings? “Canada is also in the midst of an ill-timed supply surge that caused vacancy rates to rise, warns a new report. It paints a picture of an epic office boom turned into an epic office glut. Read… What’s Coming Unglued Now in Canada?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The best argument for more debt is that one can carry infinite debt at zero percent. I wasn’t wise to this game to start with, so I missed out. I know, I am a dumb redneck. But, now, I realize I have missed a business opportunity! Now I am a smart redneck! I am going to open a bar called “Mercantilism” with a ZIRP bar tab policy. My sales are going have a figure 8 that looks like a figure 1 … Dy-No-Mite!

https://www.youtube.com/watch?v=v19PpD5uqL0

So, my customers can drink like mad, we put it on the tab, and because of ZIRP, they pay no interest, so they can drink all they want! Exports will sky rocket! My employees (and me) are going to be SO RICH!

I LOVE modern accounting where ASSETS matter and LIABILITIES don’t! Why didn’t Rome figure this out?!?!? Sometimes I wonder why they are so stupid.

Anyway, my brother in law (***hole) tells me folks will just drink, not pay their bills, and the worst of the worst will show up and crash my joint! So, I thought about that a bit and decided, maybe ZIRP wasn’t enough to drive my sales … I need NIRP! As long as no one uses cash, my patrons can take out 100 year bar tabs at negative, interest only payments, until the balloon is due.

Gravy! Prosperity is so easy, where is my Nobel Prize in Economics?

Regards,

Cooter

Cooter, I am submitting your name to the Nobel Prize Committee for Economics. Pack your bags my friend. You are going to Stockholm. After that, the Fed.

BTW, have you thought about securitizing this debt as a derivative vehicle? Because, since you will be in the area anyway, there is one town in Norway that I know will want to talk to you. Just tell them that Goldman-Sachs sent you. Trust me, they will love you.

NT

So you want to end up in the same hall of fame as P. Krugman? Why don’t you go for the Nobel Peace Prize? Then you’d really be in outstanding company.

CC up late, NT up early, the night shift stinks. When do I get buzzed?

Spencer, If you take a job in Cooter’s bar, maybe you can get buzzed on the job. Just a thought.

Regards

NT

Many first time home buyers should have a tougher time qualifying to buy homes in Canada, because Canadian student debt, although not at the level of US student loan debt, is still a present and future problem.

“Student debt grew 44.1 per cent from 1999 to 2012, or 24.4 per cent between 2005 and 2012.”

And will the Chinese Government’s crackdown on corruption put a damper on Vancouver’s insane real estate prices?

“In the last five years, the median selling price for residential properties in Vancouver has jumped 57 percent to $1.1 million (Canadian), according to data compiled by Reuters from the Real Estate Board of Greater Vancouver. The price of detached homes has soared 82 percent, to $2.1 million (Canadian). The median household income, meanwhile, has risen by an estimated 13 percent in the same period, according to Statistic Canada.

In interviews, five real estate agents who primarily sell homes on Vancouver’s exclusive west side estimated that between 50 percent and 80 percent of their clients have financial ties to mainland China.

A Reuters survey of 50 land titles for detached Vancouver Westside homes that sold for more than $2 million (Canadian) in the last year found that nearly half of the purchasers had surnames typical of mainland China, as distinct from those of earlier waves of immigrants from Taiwan and Hong Kong.”

If the sudden drop in Mainland Chinese buyers in Australia’s prime housing markets is anything to go by, either banks should start approving anybody with a pulse for mortgages worth millions of dollars, or troubles may be looming ahead.

Obviously blame is being shifted: first Australia’s war on cash, which hits Chinese buyers making payments through so called “grey channels”, then China herself, due to tighter capital controls… far from anybody blaming a bubble having finally run its course.

Household debt is booming in both countries, hinting at the fact Canadians and Australians are increasingly turning to borrowing to maintain standards of living they’ve been accustomed to during the commodity bubble or simply making ends meet. Somehow I doubt real price inflation is reflected by official CPI figures.

However deliquency rates stay low. Suspiciously low, I may add.

I have no idea of how the situation on the ground is in Australia and Canada, but one thing I can say is here in Europe not only interest rates are dropping again, but lending standards have been considerably loosened.

My main bank (one of Europe’s largest) has started offering loans to temporary workers with a two months contract. You read it right: to get any type of finacing all you have to do is show you’ll be working for two months from now, with no guarantee of being rehired or of finding another job.

And don’t think interest rates will kill you: we are talking under 9%, far less than what subprime lenders with less shaky credentials paid in 2007.

Honestly I’ve run out of words to describe this situation, after throwing a lot of expletives to my bank of course.

The non -Chinese buyers are buying to flip to Chinese buyers no doubt

Does anybody know if the Canadian debt, especially credit cards, was incurred in the US. As a Floridian, I am surprised by how long the Canadian sun birds stay and how well they live. Most own oceanfront condos, eat and drink out often, and stay 3 to six months. They are also fairly young looking, younger than retirement age in the US. This is something I could never have done even when I was doing very well.

Canadians were big buyers of US real estate in FL during the collapse. Does anybody know if they have cashed out yet? The should be strongly in the money if they haven’t.

Yes, go figure. As a Canadian living and working in the SF bay area, Canada or Ontario strikes me as so poor compared to where I am now. They are over taxed, even by CA standards, everything is so overpriced, cars, food, liqueur, even by Detroit Metro standards.

My guess, is the people that snap up land in FL are in the top 10%. They are the doctors, computer professions etc capable of afford it. But then again, every thing these days can be bought by going into debt, so you never know.

Petunia;

Ask them- many (most) will be government employees of some sort- teachers, admin, police, WCB(Osha) and so on…

Canada, like the U.S. has the super- wealthy, and they can live anywhere they like. But Canada has created a tier of well-to-do public employees, through government pensions, which private sector , non-public union employees work well into their retirement years to fund. While their public employee neighbours squeeze taxes out of them.

Everyone has these stories but I’ll write it, anyway.

I had two aunts who relocated from Toronto to Vancouver in 1969. They lived in an apartment their entire working lives. They were going to rent an apartment, again. They had some money saved and my Dad talked them into buying a house on west 4th!! no less, with a lovely view of the harbour, Lionsgate Bridge off to the extreme right, and the north shore mountains straight out their front room window. They were reluctant to take on a mortgage but my Dad co-signed for it. They paid $27,000 for a awesome little two bedroom bungalow, hardwood floors, leaded pane windows, but kitchen and bathroom updated. It even had a basement. I stayed there many times when I was a kid.

Fast forward 15 years and they sold it to some lawyer for $250,000 who promptly tore it down and built a modernized monstrosity that looked like several shoe boxes pile up on the lot…with windows. Fast forward again and it sold for 2 million, the house was again torn down and something else re-built in its place.

I guess the only thing left to do is buy two of the adjoining lots, tear them all down, and throw up multi-storied condos.

What I can’t understand is why why why anyone would move to Vancouver or Toronto unless they were already independently wealthy? It is impossible for a regular working person, (whether they are a professional, trades focused, or entry level worker), to ever get established in either Toronto or Vancouver and get ahead. I suppose the same is for SF, Seattle, and Portland. By the way, the Aunts relocated to Whiterock and lived happily ever after. My folks moved to Vancouver Island and then retired in Whiterock.

There is a time to move somewhere, and there is a time to leave. For those on the outside looking in it is quite apparent when that is. In fact, you don’t even need 20-20 hindsight to figure this out, (but it helps).

Don’t forget, debt that can be rolled-over is really an asset !

When will Canucks run out of money, or credit? They are well beyond the US Tipping point where our hottest real-estate markets melted, but like that energizer bunny, keep on buying! One would think they will hear the BOOM in Buffalo when Toronto finally wakes up. Nah, maybe not. Anyway, sure sucks to be a property buyer there right now, as Vancouver.

Maybe Cooter can place his new PUB there, he should do very well!!

Unfortunately, the average Canadian believes the meme that Canadian banks are solid, unlike in the US – because Canada has regulation. That’s what they are told by the MSM. The rest of the story is ZIRP, and global money laundering seeking for soft political environment.

Hello astute commenters

I am a 55 year old white male born and bred in Toronto.

The only thing that is actually happening here and in Vancouver is that the majority of expensive homes are all foreigners.

The world is becoming an extremely dangerous and unruly place and one of the best places to come to is Canada.

The house around the corner which is a cookie cutter gigantic house, 5 bedrooms, 5 baths sold for 1.4 million.

Its not even worth one million. The local bank, TD, is writing mortgages left and right.

You are becoming the minority, just like me.

The inequality grows everyday. These folks from overseas are simply buying there way in.

As for the Canucks in Florida, by and large they are part of the old school pension system where if you worked for GM or the govt, local or otherwise, you are just grooving on your monthly pension.

Ah for the good old days.

My buddy down the street picked up garbage for the City of Toronto, he’s 58, ready to retire and he will get $3300/month pension plus another $1500 to $2000 when he gets to be 65.

Go figure, I should have been the garbage man :)

There is a new paradigm in Canada that herds the financially distressed into Insolvency. Those rates have grown substantially. Some of your debt get forgiven, but you dont declare bankruptcy. THE CORPSE maintains the illusion of life with ZIRP like minimum payments. Once this process runs through the cycle, wages will be jacked up, “Jobs for debt slaves”, all others need not apply.

Our kids are in debt in magnitude I would have never imagined.

They don’t believe that real estate can drop in value, they don’t believe that interest rates can suddenly spike.

I lived through 20% mortgages in the 80’s, I can tell you that all of the above happens and WILL happen again.

Also correct about two classes of people in Canada…Public Service employees and the rest of us poor tax paying slobs.

What really irks me is the double dipping the government employees enjoy, collecting pensions from 2, even up to 3 different government departments.

Well…that party is going to end…and very soon I hope.

Maybe when the American real estate market takes it’s second leg down after the dead cat bounce (which is now over) Canadians will finally figure it out.