You wouldn’t know by looking at the US Treasury market, which remained relatively sanguine this week, with only a little panic buying on Tuesday. So 10-year Treasuries ended the week near where they’d started it. But at the other end of the spectrum, the riskiest portion of the junk bond market just blew up spectacularly.

There were a lot of culprits to catch the blame. At the top of the list was the devaluation of the Chinese yuan. It caught the corporate bond markets by surprise, though it shouldn’t have, injected all kinds of stress into them, and drove up bond spreads, with investors demanding a higher yields for riskier bonds. It hit the riskiest segment of the junk bond market with a sledge hammer.

Given the precarious state of the current credit bubble and the pandemic nervousness about it, bond investors were rattled by the moves of the People’s Bank of China. In prior crises, such as the 1997 Asian financial crisis and the 2008-2009 Global Financial Crisis, the PBOC had maintained a fixed exchange rate with the dollar. It didn’t devalue, as other countries were doing, to get out of the crisis. The yuan was seen as stabilizing the markets. Now the yuan is seen as destabilizing the markets.

It didn’t help that the Fed’s cacophony has been pointing at a September rate hike. It would be the first ever in the careers of millennials working on Wall Street. It would bring to an end the 30-year bull market in bonds. Even most middle-aged money managers have not yet experienced the alternative, other than a few short-lived dips and panics. On a visceral level, they simply can’t believe rates can ever rise over the long term. To them, rates can only go down.

And oil prices plunged to six-and-a-half year lows, taking out the low set earlier this year, instead of bouncing off it. West Texas Intermediate ended the week at $42.18 a barrel. But in Canada, the benchmark blend Western Canada Select hit a catastrophic C$29.79 a barrel.

WCS always trades at a discount to WTI. But as some refineries were shut down for scheduled maintenance, a BP refinery in Whiting, Indiana, that can process Canadian heavy crude, was also shut down for “unscheduled repair work.” Getting the refinery up and running at full capacity again could take several weeks. Meanwhile, the crude, with no other place to go, goes into storage.

This scenario was punctuated by a cascade of bankruptcies that eviscerated unsecured bond holders, and not all of them were energy-related. In Delaware alone, there were 20 Chapter 11 filings this week, including the prepacked bankruptcy of Hercules Offshore and a gaggle of related companies. Risk, which the Fed had so ingeniously removed from the equation, is suddenly rearing its ugly head again.

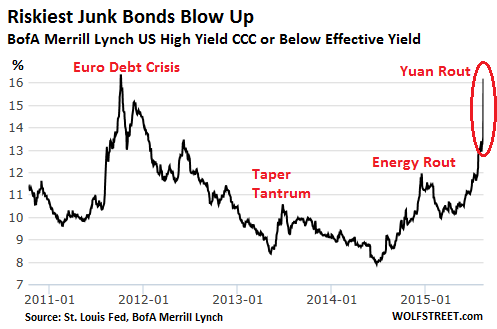

How suddenly? This chart of yields at the riskiest end of the junk bond market – bonds rated CCC and below – shows what happened. These bonds have been selling off over the past 12 months, with exception of the sucker rally earlier this year, and their yields more than doubled from less than 7.9% in June a year ago to 16.2% by Thursday evening. And Thursday was a massacre:

On Thursday, yields jumped 2.6 percentage points, from 13.58% to 16.18%, as these junk bonds plunged. Those kinds of single-day vertigo-inducing sell-offs are rare in normal times, and there haven’t been any since the Financial Crisis.

Junk-rated companies that confronted this spooked market during the week to issue new bonds “faced challenging conditions, as China’s yuan devaluation sent shockwaves across global markets and oil prices continued to fall,” S&P Capital IQ reported in its LCD High Yield Weekly. And the bane of all bond issuers: some of them had to offer “healthy concessions” to find buyers for their bonds.

Concessions! Investors are opening their eyes, and they’re demanding to be compensated at least a tiny bit for the enormous risks they’re taking at that spectrum of the market.

And in the secondary market, where junk bonds are traded, energy bonds got whacked again, in line with the ongoing oil price fiasco. “The damage was widespread, with some names trading 2-5 points lower,” LCD High Yield Weekly reported, and “the rough week in the commodities space weighed heavily on the broader market.”

Among the beaten down junk bonds were Chesapeake’s $1.1 billion of 5.75% notes due 2023. On July 21, last time I wrote about them, they’d just hit a new all-time low of 84.88 cents on the dollar. This week, they were reportedly pegged at 72 cents on the dollar. It seems, bond-fund managers are finally waking up from their Fed-induced torpor, and they’re suddenly seeing with horror what they’ve plowed their clients’ money into, and some of them are trying to get out while they still can.

China is also hitting global companies that generate a big part of their profits from their sales in the former growth miracle. Such as GM. But now elements are coagulating into a toxic mix. Read… China Mess, Yuan Devaluation Spread to the US

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

2008 was the big scare that ended without too much damage.

2015 people are now desensitized, complacent, especially after 6 years of QE.

Nobody will see this one coming.

75% have nothing to lose because they have nothing,

24% read and they are educated to preserve wealth,

1% are elite insiders and they will make money anyway.

Must be true of every financial crisis then, which means nobody loses any money when it collapses!?!

Regardless of what you might think there was never so much wealth created and rational people just get wealthier more and more by each passing day . Those who preach doom and gloom make money by preaching same story over and over again but still invest money and make money. So everybody wins, and I think by now you should get that.

There is only one way for market to go and it is UP, otherwise the hell will break out and I don’t think anybody wants that.

Next short term correction will burn only margin market players (as always) and the party will go on and on.

The 24% (sounds pretty generous!) may pull their money out of the risky bets in time, but they still get hurt every day by stagnant incomes and hidden inflation.

Pretty simplicist view of financial collapses, don’t you think? Especially considering all “paper” wealth including the US dollar could lose 30-50% of it’s value in short order. In that scenario, no one gets away unscathed.

Since 2008 the major economies have cranked up their debt quite considerably, there has been $12tn of QE and we have zero interest rates.

Things are going to be a lot worse than 2008.

Bonds lost about 35% in 1932; they are loans and when the economy dives, they should crash (for a while); but nothing is normal about Wall Street or WDC anymore but crime.

Wolf,

I often read your informative posts for a view of various aspects of our financial markets. Do you suggest that investors have all their assets in cash and be completely out of all long equity investment?

Wolf’s negative views are an important part of a comprehensive overall concept. Use it and use your own critical thinking skills to form your own opinions. I read his views regularly—with a grain of salt.

For a bit of perspective. As recently as the 1980s, talk to almost any smart wealthy folks and they would tell you to never invest money that you couldn’t afford to lose. Since that time, I have seen three major “corrections” with people invested heavily in markets with which they barely had rudimentary understanding. I have seen people carrying large credit card balances with interest rates of 12-18% socking all available, arguably borrowed, funds into the markets. And to bring in the suckers, even the nomenclature of money was sanitized to make owing more palatable. Being “leveraged” sounds much better than being in debt. There was also good debt and bad debt. Running up $60,000 for a degree in event planning was good debt.

But, now, it’s all different. Just jump on a bubble and ride it up and all you have to do is be sure to jump off before it pops. I am assured by all parties invested in the new economics, that it is all different this time. Yet again. I for one, am grateful for Wolf’s analyses. He isn’t afraid to call a frog ugly in a time where all frogs are princes. Please keep it coming.

Wolf, Night Train; people are acting like brainwashed suckers. What is not being digested is the American loss of middle income wages during this period of globalization and the misunderstanding of the difference between savings and the 401K. Compound interest on savings is so low it forces people to invest as a way to keep up with inflation. The rub is the bubble can wipe out ALL 401K savings. We are sheep being led to the slaughter and we know it’s risky but very few know how to get out and convert to cash. The tax implications are shocking to most 401K holders but this is the only option that guarantees you won’t get wiped out!

Karl: Well said and quite correct. It has worked out this way almost like it was someone’s plan.

Devil, no man can summon the future. The functions of commentators on the passing scene are invaluable because no one person can know everything there is to know about business or any other subject. I don’t find Wolf negative at all but a realist who looks on the passing scene skeptically when the need is there. Right now it’s a smorgasbord of desperate actions, both by central banksters and central governments. All we can do is observe the passing scene, gather as much information as possible then base our actions on our own judgement. You pays your money and takes your chances. Regards, JULIAN

So is the recommendation here be in all cash except to short the overpriced assets such as Amazon and the Homebuilders for example?