The current housing boom has Dallas solidly in its grip. As in many cities around the US, prices are soaring, buyers are going nuts, sellers run the show, realtors are laughing all the way to the bank, and the media are having a field day. Nationwide, the median price of existing homes, at $236,400, as the National Association of Realtors sees it, is now 2.7% higher than it was even in July 2006, the insane peak of the crazy housing bubble that blew up with such spectacular results.

Housing Bubble 2 has bloomed into full magnificence: In many cities, the median price today is far higher, not just a little higher, than it was during the prior housing bubble, and excitement is once again palpable. Buy now, or miss out forever! A buying panic has set in.

And so the July edition of D Magazine – “Making Dallas Even Better,” is its motto – had this enticing cover, sent to me by David in Texas, titled, “The Great Dallas Land Rush.” “Dallas Real Estate 2015: The Hottest Market Ever,” the subtitle says.

That’s true for many cities, including San Francisco. The “Boom Town,” as it’s now called, is where the housing market has gone completely out of whack, with a median condo price at $1.13 million and the median house price at $1.35 million. This entails some consequences.

The fact that Housing Bubble 2 is now even more magnificent than the prior housing bubble, even while real incomes have stagnated or declined for all but the top earners, is another sign that the Fed, in its infinite wisdom, has succeeded elegantly in pumping up nearly all asset prices to achieve its “wealth effect.” And it continues to do so, come heck or high water. It has in this ingenious manner “healed” the housing market.

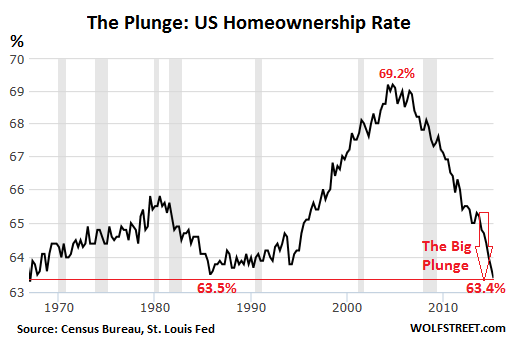

But despite the current “buying panic,” the soaring prices, and all the hoopla round them, there is a fly in the ointment: overall homeownership is plunging.

The homeownership rate dropped to 63.4% in the second quarter, not seasonally adjusted, according to a new report by the Census Bureau, down 1.3 percentage points from a year ago. The lowest since 1967!

The process has been accelerating, instead of slowing down. The 1.2 percentage point plunge in 2014 was the largest annual drop in the history of the data series going back to 1965. And this year is on track to match this record: the drop over the first two quarters so far amounts to 0.6 percentage points.

This accelerated drop in homeownership rates coincides with a sharp increase in home prices. Go figure.

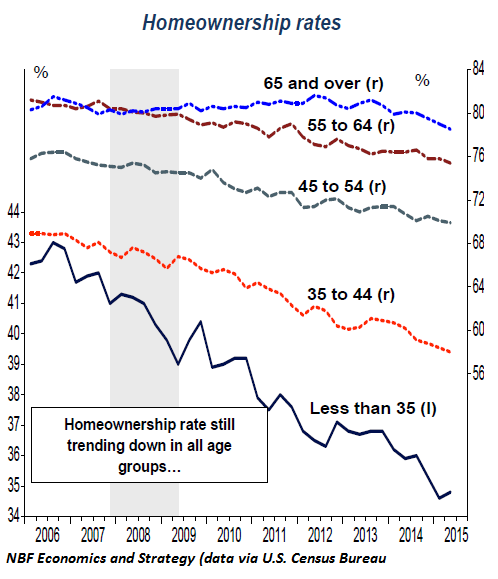

The plunge in homeownership rates has spread across all age groups, but to differing degrees. Younger households have been hit the hardest. In the age group under 35, the homeownership rate in Q2 saw a slight uptick to 34.8%, from the dismal record low of 34.6% in the prior quarter. Either a feeble ray of hope or just one of the brief upticks, as in the past, to be succeeded by more down ticks on the way to lower lows.

This chart by the Economics and Strategy folks at National Bank Financial shows the different rates of homeownership by age group. The 35-year and under group is where the first-time buyers are concentrated; and they’re being sidelined, whether they have no interest in buying, or simply don’t make enough money to buy (represented by the sharply descending solid black line, left scale). Note how the oldest age group (dotted blue line, right scale) has recently started to cave as well:

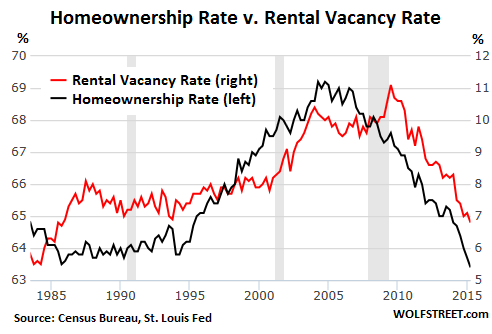

The bitter irony? In the same breath, the Census Bureau also reported that the rental vacancy rate dropped to 6.8%, from 7.5% a year ago, the lowest since 1985. America is turning into a country of renters.

This chart shows the dynamics between homeownership rates (black line, left scale) and rental vacancy rates (red line, right scale) over time: they essentially rise and dive together. It makes sense on an intuitive basis: as people abandon the idea of owning a home, they turn into renters, and the rental market tightens up, and vacancy rates decline.

This too has been by design, it seems. Since 2012, private equity firms bought several hundred thousand vacant single-family homes in key markets, drove up prices in the process, and started to rent them out. Thousands of smaller investors have jumped into the fray, buying homes, driving up prices, and trying to rent them out. This explains the record median home price across the country, and the totally crazy price increases in some key markets, even as regular Americans are trying to figure out how to pay for a basic roof over their heads.

This has worked out well. By every measure, rents have jumped. According to the Census Bureau’s report, the median asking rent in the US rose 6.2% from a year ago, and 17.6% since 2011. So inflation bites. But the Fed is still desperately looking for signs of inflation and simply cannot find any.

And how much have incomes risen over these years to allow renters to meet these rising rents? OK, that was a rhetorical question. We already know what has been happening to incomes.

That’s what it always boils down to in the Fed’s salvation of the economy: people who can’t afford to pay the rising rents with their stagnant or declining incomes should borrow the money to make up the difference and then spend even more on consumer goods. After us, the deluge.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

A housing boomin Dallas ? Even with oil prices coming down so sharply ?

Yeah. Dallas is a big city with relatively little exposure to oil. For an oil-bust led housing downturn, watch Houston. But so far, so good: a friend of mine just sold his house there after it had been on the market one day!

Smaller towns in TX, OK, and elsewhere that are oil-and-gas dependent are getting hit hard, though.

My folks sold an upscale condo in San Antonio one month ago the first day it was listed.

Yes, its true. The rich at least are buying houses at such a clip they can’t build them fast enough. These are the people that no matter what happens, they come out smelling like a rose and never miss a lick. Its great to be from old money or to be part of the in crowd. All you do is make the little guy pay for whatever you want. And they always do.

I see plenty of friends and colleagues mortgage themselves to the hilt in order to join the ranks of amateur landlords or proud owners of miniscule boxes. Since the credit is so cheap it seems like a no-brainer, regardless of the price. This time really is different. Sure, the mania is reaching fever pitch again, but the central banks really have figured it out this time. No more boom and bust, just an endless infinite boom.

Of course this obsession with property speculation is unhealthy – and irrational in the extreme – but absent an increase in the price of mortgage credit, it will continue in this vein for a long while yet.

I guess this is what happens when money dies.

I feel the same way. The boom will continue for a while. Until homes stop selling as if it’s a door buster Black Friday sale, prices will continue to go higher and so will rent. Even though people will have less and less money to spend, home prices will still go up anyway.

In 2008, we had a lot of home owners who really couldn’t afford those homes they bought but now, due to stricter lending rules, we have buyers who can actually afford those prices. As rents continue increasing, homeowners will continue to profit and won’t have much incentive to sell, keeping supply down, further increasing home prices along with rent prices.

The percentage paid toward rent of one’s income will keep increasing. We’ll see enough people spending over 60% of their income toward rent that will be considered normal. I see things flattening out, a new, higher cost of living norm, but not a crash. It won’t happen.

Those who are thinking of buying a home, BUY NOW. Those who already own a home and can rent out a room or two, do it and don’t be afraid to ask for a really high rent price, people need a roof over their head, it’s a necessity not a luxury so even if almost all of their income goes to rent, they’ll have no choice but to pay it.

The currently popular mainstream idea that we are “…entering a period of rising interest rates…” is dependent on the thinking that a) “the recovery” is going to “achieve lift-off” and, moreover b) that this is the upside out of a CYCLICAL downturn.

Perhaps there is only a statistical mirage and no real recovery at all.

Perhaps this is a SYSTEMIC downturn.

Though we the chastened cannot know the precise timing in a world of near-total manipulation, my bet is the “housing recovery” is dead in the water from here on.

If “interest rates”, mangled and rigged as are all prices, values, indices and statistics, DO rise it will be the governments’ and central bankers’ hands being forced by THE MARKET.

They reported yesterday that Trump sold his Park Avenue condo for 21M, asking price had been as high as 35M. I think this is a real sign of a falling market. I remember Trump pricing a Palm Beach house for 100M, a ridiculous price, and holding on to it until it sold. This time he caved on the price. I think the fat lady just sang.

I’ll let you chaps in the latest craze. Rent a tent in your back yard! And watch Blackrock and wall street securitize that!

Strange things afoot, the fed on one hand is driving housing prices higher via cheap credit used by investment firms or landlords to buy up single family housing while simultaneously the administration is pushing Affirmatively Furthering Fair Housing which by all logic would eventually force most housing prices down.

I guess the investors are figuring on some kind of back door bailouts, or maybe like in Seattle where they want to eliminate zoning for single family housing existing homes will increase in value since there will be no more new construction.

I think the lesson is, unless you’ve spent a lot of time looking at all these macro forces being engineered by the central planners you’re going to get your head lopped off.

The casino angle, all these people pulling the handle, waiting for the jackpot. A few will hit the jackpot, and they go on the seminar circuit and cable networks that you too can make scads of money with just a little “sweat equity” and OPM. The Siren call of the Greater Fool. But the casino is rigged and the House always wins, and the Dealer takes all pushes. No one seems to recall the last punishing crash. My advice would be the same to either a real gambler in Vegas or the gambler in Dallas real estate – cash in, and don’t put it back into the one armed bandit. But they will not listen, other than to call me a panic monger or a doomsayer. But I’m just the bell who calls others to meeting but itself hears not the sermon.

Yesterday my mother phoned me and told me to “pick up the local newspaper” because there was something I needed to see.

Sure enough there were eleven (!) pages of what in local legal language are called “Housing Executions”. This is somewhat similar to the US foreclosure: if someone gets too far behind his mortgage payments, his house gets repossessed and auctioned off to the highest bidder. These sales are controlled by lawyers with a mandate from the local courts.

To put the icing on the cake, my bank informed me they are opening a housing division. They have so many houses on their hands from foreclosures and as repossessed collaterals on loans they need to shift at least part of them quickly because they are quickly becoming a burden. Property taxes alone are seeing to that.

You’d expect in such an environment housing prices would, if not fall off a cliff, at very least decline a tiny bit. And you’d be awfully wrong.

Ever since 2010 prices have continued to soar in face of the most atrocious post-WWII slump in housing we ever experienced. After the fire sale in 2008-2009 sales have bogged down and refuse to budge. This is the true definition of inflation without compensation.

For all of those who think “central banks have this covered”, I’d like to add another couple snippets of housing madness.

Despite large unsold stocks, the race to build more housing units continues. I often joke we live in a Little China since our housing boom, very much like the Asian one, is not fueled by insatiable demand but by extreme values and cheap credit. Local councils, effectively insolvent if not downright bankrupt, fuel the race by providing building permits with complete abandon: if Chinese towns and cities stay afloat through land sales, local towns and villages stay afloat through fees and permits.

And then we get to mortgages and loans. Oh boy. Mortgages have never been so cheap: if you are not a complete deadbeat you can get a 30 year mortgage for under 4% these days. Our banking union recently lowered lending standards: even temporary workers with a three months contract can get approval now.

Yes, this will definitely end well, especially given not even this effectively free money is managing to prop up demand. First time buyers have literally disappeared. A toxic combination of very low wages for the under 35 and job insecurity (hence the need to be able to move quickly where work is to be found) pushed potential first time buyers into renting, if they are not staying home with their parents while looking for a better paid job.

I have no proof of this, but I strongly suspect this is all part of a grand scheme to replace our rapidly dwindling manufacturing base with an “eternal” housing bubble. All would be fine and dandy… if buyers existed. Not many billionaires are interested in buying a house in what is quickly turning into a Rust Belt with crumbling infrastructures and, for the first time in history, dealing with high unemployment.

Many people delude themselves into thinking the ECB or the government will somehow manage to turn things around. I get lectured at least once a week on how high housing prices, very much like price inflation, are “necessary to the economy”… often by people who then lament groceries are becoming more expensive by the week and whose sons and daughters are staying home because they cannot even afford rent on what their temporary jobs pay.

They are the true definition of what Lenin called “useful idiots”.

But the WSJ told me this isn’t a big deal because if you adjust for inflation, they’re still down 20%.

The inflation that the Fed and the BLS claim doesn’t exist?

We recently sold our house in a rather economically moribund counytyside area about an hour South of Richmond, VA.

It was on the market for six years and sold for about 70% of its appraised price when first listed.

The sale was financed with a HUD-1 insured loan by a private investor.

Community banks are out of the home mortgage business in today’s conditions – another example of the government’s warping of the financing apparatus in this country.

The community banks are so heavily regulated that they can’t compete for mortgages, then their business is put out for grabs by government subsidized money sources.

Panic buying at the top of the market=you paid too much=tomorrow’s foreclosures=day after tomorrow’s foreclosure bargains.

PS If (when) these overpriced houses go into foreclosure, the borrower will owe the IRS taxes for imputed income based on the amount of the forgiven debt. 300k mortgage=taxes owed for 300k in income. Plus interest and penalties for every year that you can’t pay in full. Of course the real estate or bank people won’t tell you this.

35-44 demo here. We’re selling and going to renting after owning several homes for 18 years.

Two reasons: 1) Get (and then stay) out of debt as much as possible and 2) Get mobile. We’ve finally accepted we’re nomadic and higher quality of life is more important than owning a home. We’ll only be tied to our current location by my wife’s job and we’re trying to fix that ASAP. I could see purchasing some income producing property that we could live on, but that’s it.

So, I would say lack of income certainly plays a part in ownership going down, but some of us are just tired of this system and want to try something different. I think the model of go to college… get a career…have kids… buy a house… save for retirement… conform and submit is about to get turned on its ear. The takers are running out of middle class wealth to steal and they’ve f’d up all of the roads to get to the middle class.

The American Dream is turning into the American Nightmare for too many.

Well my little corner of the world – the western suburbs of Philadelphia( Collegeville are) my house, bought in December 2007, has lost substantially more than 150k in value and has not recovered. The seller had already come down very substantially by the time we saw the home and we offered 30k less than that and felt we were getting a good deal on a great house, well under other similar homes for sale in the area. ( this in certainly not our first home purchase – it’s our sixth!) A normal 3,100 sf two story colonial with a large well maintained pool and an acre of good land. And we have added hardwood floors and staircase throughout, a huge new laundry room full of high end cabinets, new stone fireplace in the family room and well as high end windows, a huge new deck and good landscaping. My neighbors have seen their values drop also and having similarly improved their homes. We and our neighbors and middle to upper class professionals. We are in a fine school district as well. We are not selling but had several realtors in to value the house, one of which we have dealt with for years and trust.

Also my kids are looking at not being able to buy their own homes any time soon nor even start a small family because wages are so far down and jobs are so scarce in their chosen fields in this area. One must stay here (due to a parent inlaw having long term illness and is widowed with just the one child – my wonderfuldaughter in law). . The other is looking nationwide while working seven days a week at three different part time jobs while battling a serious kidney problem …

We would like to downsize in two years but that is looking to be a seriously bad financial move so looks like we will stuck in a too large home and its corresponding upkeep costs unless the economy in PA improves substantially. Of course that, combined with helping our kids get started, means we are spending a LOT less as consumers ourselves. Which cannot be beneficial to the local economy either… Our neighbors , of various political leanings, are all doing the exactly same thing as they are in the same boat with their homes and kids.

. Local stores ( independent and large chain) are closing at an alarming rate hereabouts which to me means even more people are in the same boat as well. We all seem to have a very bad feeling about the future. We will likely be ok but what about our kids and grandkids? It’s not looking to be a pretty world in decades hence….

Wolf, I’m curious — Is the current housing bubble 2.0 confined mainly existing home sales, whereas the last bubble was in both existing home sales as well as a new home sales?

So maybe even though median prices (per house) are back to previous levels or higher, total dollar sales might yet still be smaller because this time around lacks the new home sales component?

Just wondering?

Ernest, new homes and existing homes are linked within each housing market. For example, in the LA area, a lot of Chinese buyers started switching to existing homes when new homes got too expensive recently. The opposite also happens, as during the bottom of the housing bust, when new homes dumped by desperate developers were cheaper in certain markets than existing homes. Buyers switch back and forth, depending on the circumstances.

So with some variation and perhaps a lag, if you have a price bubble in one, you’ll soon have it in the other as well.

BTW, we’re talking about asset price bubbles, so price per home, not volume bubbles. In terms of volume (number of units sold), housing sales are not anywhere near where they used to be.

Note that houses, stocks, bonds, etc are “generational” assets – the younger generation must buy in order for the older generation to monetize their assets. If the younger generation is broke on a net basis, debt can enable the buying for a bit but not forever. In order for retirement plans to function younger buyers must be continually drawn in who are willing and able to pay continually higher prices for stocks and bonds. Housing works similarly, when prices fall the market freezes up to some extent. If succeeding generations are poorer it all falls apart.

Houston is already cracking. Dallas will follow-suit once the stock market corrects. This week we had another round of layoff announcements in the oil sector. Turns out company projections for a quick turnaround in the oil sector were premature. Who could have imagined?

Summer selling season has seen a brief respite from declining year-over-year comps (both sales volume and prices) here in West Houston. Houston in general has been faring a bit better than West Houston due to diversification from oil sector woes. That being said, the writing is on the wall. Either the Fed prints a few more trillion to prop up this re-inflated zombie Ponzi scheme, or it comes crashing down once again. Houston is already flirting with a recession. All it will take to put it there is a modest correction in the stock market and a vaporization of some of that phantom paper wealth.

http://aaronlayman.com/2015/07/u-s-rate-of-homeownership-falls-to-48-year-low-case-shiller-home-price-index-moderates/

Also living in the far north western exurbs of Philly, I have a 7 acre farmette for my horses, as do my neighbors in this small “farmette” community of 9 homes/barns. I bought right after the bubble burst in 2007 at what was then a great price, or so I thought. Saving grace – I paid cash, so I may lose when I eventually sell but I’ve saved a bundle on horse board fees, far more than I’ve paid in property taxes and upgrades. Priorities, you know. My neighbor behind me just sold his place to a young couple with young kids, after 9 months on the market and three price downgrades. The price the new neighbors paid ? The same the former neighbor paid almost 25 years ago when it was new, so no appreciation for him. The new neighbor commented to me yesterday that his first mortgage payment is now due, out of 360 – and he’s stretching to pay it. With young kids and a crappy economy, and property taxes ever rising ? Yeah, that place will be in foreclosure within two years is my prediction.

This surge in demand is not nation wide, I have owned an apartment complex in the Midwest for many years and we are currently experiencing the largest number of vacancies we have ever had. Many houses in my area are empty or under leased. In 2005 and 2006 prior to the housing collapse many people were looking at second homes, today they have shed the extra home and many have doubled up with family or friends.

I have been busy trying to make sense of the current economy, this is not an easy job. We are pushing on a string and calling it demand when someone who can barely pay the rent is encouraged by the government to buy a house they can neither afford or maintain. Currently we have a shortage of “qualified” buyers and renters.

For some time I have thought the primary reason that inflation has not raised its ugly head or become a major economic issue is because we are pouring such a large percentage of wealth into intangible products or goods. If faith drops in these intangible “promises” and money suddenly flows into tangible goods seeking a safe haven inflation will soar. The jump in housing in certain areas may be the first sign that this trend is underway. More on this subject in the article below.

http://brucewilds.blogspot.com/2014/04/inflation-seed-of-economic-chaos….

Wolf, do you think all these cash buyers from China plan to exit the California housing market when things turn south economically for the US? Or do you think these buyers may have long term intentions to stay and put their roots into such places as San Francisco or the Silicon Valley? Ultimately it is that question that makes me wonder if things are really different this time around.

My impression is that a lot of these buyers from China want an escape hatch. So that would be long term. The problem is that when local incomes can no longer afford local housing, the market will sooner or later get in trouble. Silicon Valley and SF are boom-and-bust places, with employment booming and plunging. Now is the boom. When the employment bust hits, that’s when housing will get hit.

And there’s a building boom going on right now, with about 60,000 units at various stages in the pipeline in SF alone. If these units come on the market during the employment bust, it will trigger the same thing that happened before: a housing bust.

I’ve been living in the Bay Area for 20 years now. Back when I moved here I felt home prices were way overvalued at $250k-$300k as the median home price, but have been blown away that they have quadrupled since then. Needless to say I know fundamentally this is way too fast for prices to appreciate, but have been proven again and again that this is the nature of the beast here and I best get use to it.

Do you feel that once the bond bubble bursts, home prices will finally come back down to Earth? Or being that global central banks are all in tune with each other, perhaps they can continue to re-inflate the most popular bubble asset around after a short term correction again? If you were to forecast and guess, what kind of correction do you think will see around here when things do fall back into balance? I would assume at lest a 30%, but realistically they should fall 40-50%. Perhaps over a decade? I keep wondering if this is the end of the “Golden Age of Technology” era in the Bay Area because it has become so expensive to do business here, much like how Hollywood is no longer the center of the entertainment industry anymore.

On the other side of the coin, I keep wondering if the housing price demand and rise is part of the exponential function in play with the human population story. Sorry for the long winded reply. Appreciate your insight.

The famous Dr. Housing Bubble discusses your area in his blog.

http://www.doctorhousingbubble.com/san-francisco-real-estate-median-home-price-new-record-sf-bay-area-housing-bubble/

Used my chart, too, without asking….